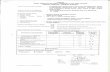

LEMBAR HASIL PENILAIAN SEJAWAT SEBIDANG ATAU PEER REVIEW KARYA ILMIAH : JURNAL ILMIAH Judul karya ilmiah (artikel) : The Determinants of Taxpayer Compliance with Tax Awareness as a Mediation and Education for Moderation Jumlah Penulis : 4 Orang Status Pengusul : Penulis ke 2 Nama Penulis : Dr. Indira Januarti, SE, M.Si, Akt Identitas Jurnal Ilmiah : a. Nama Jurnal : Jurnal Ilmiah Akuntansi dan Bisnis : b. Nomor ISSN : p-ISSN 2302-514X e-ISSN 2302-1018 : c. Volume, nomor, bulan, tahun : Vol 15, issue 1, 2020, Januari pp. 1 s/d 12 : d. Penerbit : Universitas Udayana : e. DOI artikel (jika ada) : : f. Alamat web jurnal : https://ojs.unud.ac.id/index.php/jiab/article/view/515 62 : g. Terindeks di scimagojr / Thomson Reufer ISI knowledge atau di nasional / terindeks di DOAJ, CABi, Copernicus : ARJUNA Sinta 2, Garuda, Crosssref, DOAJ, Google http://sinta.ristekbrin.go.id/journals/detail?id=319 Kategori Publikasi Jurnal Ilmiah : Jurnal Ilmiah Internasional /Internasional bereputasi (beri pada kategori yang tepat) Jurnal Ilmiah Nasional Terakreditasi Jurnal Ilmiah Nasional/ Nasional terindeks di DOAJ, CABI, Copernicus Hasil Penilaian Peer Review : Komponen Yang Dinilai Nilai Maksimal Jurnal Ilmiah Nilai Akhir Yang Diperoleh Internasional bereputasi (Maks 40) Internasional Nasional Terakreditasi (Maks 25) Nasional Tidak Terakreditasi (Maks 10) Nasional Terindeks DOAJ dll. (Maks 20) a. Kelengkapan unsur isi artikel (10%) 4 2 2,5 1 2 2,1 b. Ruang lingkup dan kedalaman pembahasan (30%) 12 6 7,5 3 6 7 c. Kecukupan dan kemutahiran data/informasi dan metodologi (30%) 12 6 7,5 3 6 7 d. Kelengkapan unsur dan kualitas penerbit (30%) 12 6 7,5 3 6 7 Total = (100%) 40 20 25 10 20 22,5 Nilai pengusul = = (40% X 22,5)/3=3 KOMENTAR / ULASAN PEER REVIEW Kelengkapan dan kesesuaian unsur Penulisan sudah cukup sesuai dan lengkap, mencakup; judul, pendahuluan,, sampai dengan kesimpulan dan daftar pustaka. Subtansi artikel cukup relevan dengan bidang ilmu pengusul. Ruang lingkup dan kedalaman pembahasan Substansi artikel cukup sesuai dengan ruang lingkup jurnal (Jurnal Ilmiah Akuntansi dan Bisnis). Kedalaman pembahasan cukup baik didukung dengan sumber rferensi yang memadai. Kecukupan dan Kemutakhiran Data & Metodologi Data dan metodologi merupakan metode yang cukup baru dengan hasil penelitian menunjukkan cukup adanya kebaruan informasi tentang Taxpayer Compliance, Tax Awareness as, and Education. Kelengkapan unsur dan kualitas penerbit Jurnal ini termasuk sebagai nasional terakreditasi ARJUNA Sinta 2, Garuda, Crosssref, DOAJ, Google http://sinta.ristekbrin.go.id/journals/detail?id=319. Indikasi plagiasi Hasil uji ternutin menunjukkan similarity index = 9% Kesesuaian bidang ilmu Jurnal cukup selaras dengan bidang ilmu pengusul, yaitu Akuntansi . Jurnal cukup selaras dengan bidang ilmu pengusul, yaitu Akuntansi . Semarang, 2020 Reviewer 1 Prof. Dr. Abdul Rohman, M.Si, Akt NIP. 196601081992021001 Departemen Akuntansi FEB Undip Jabatan Fungsional : Guru Besar

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LEMBAR

HASIL PENILAIAN SEJAWAT SEBIDANG ATAU PEER REVIEW

KARYA ILMIAH : JURNAL ILMIAH

Judul karya ilmiah (artikel) : The Determinants of Taxpayer Compliance with Tax Awareness as a

Mediation and Education for Moderation

Jumlah Penulis : 4 Orang

Status Pengusul : Penulis ke 2 Nama Penulis : Dr. Indira Januarti, SE, M.Si, Akt

Identitas

Jurnal Ilmiah

: a. Nama Jurnal : Jurnal Ilmiah Akuntansi dan Bisnis

: b. Nomor ISSN : p-ISSN 2302-514X e-ISSN 2302-1018

: c. Volume, nomor, bulan,

tahun

: Vol 15, issue 1, 2020, Januari pp. 1 s/d 12

: d. Penerbit : Universitas Udayana

: e. DOI artikel (jika ada) :

: f. Alamat web jurnal : https://ojs.unud.ac.id/index.php/jiab/article/view/515

62

: g. Terindeks di scimagojr /

Thomson Reufer ISI

knowledge atau di

nasional / terindeks di

DOAJ, CABi, Copernicus

: ARJUNA Sinta 2, Garuda, Crosssref, DOAJ, Google

http://sinta.ristekbrin.go.id/journals/detail?id=319

Kategori Publikasi Jurnal Ilmiah : : Jurnal Ilmiah Internasional /Internasional bereputasi

(beri pada kategori yang tepat) Jurnal Ilmiah Nasional Terakreditasi Jurnal Ilmiah Nasional/ Nasional terindeks di DOAJ, CABI, Copernicus

Hasil Penilaian Peer Review :

Komponen

Yang Dinilai

Nilai Maksimal Jurnal Ilmiah Nilai Akhir

Yang

Diperoleh

Internasional

bereputasi

(Maks 40)

Internasional Nasional

Terakreditasi

(Maks 25)

Nasional

Tidak

Terakreditasi

(Maks 10)

Nasional

Terindeks

DOAJ dll.

(Maks 20)

a. Kelengkapan unsur isi artikel (10%) 4 2 2,5 1 2 2,1 b. Ruang lingkup dan kedalaman pembahasan

(30%) 12 6 7,5

3 6

7 c. Kecukupan dan kemutahiran data/informasi

dan metodologi (30%) 12 6 7,5

3 6

7 d. Kelengkapan unsur dan kualitas penerbit

(30%) 12 6 7,5

3 6

7 Total = (100%) 40 20 25 10 20 22,5

Nilai pengusul = = (40% X 22,5)/3=3

KOMENTAR / ULASAN PEER REVIEW

Kelengkapan dan kesesuaian unsur Penulisan sudah cukup sesuai dan lengkap, mencakup; judul, pendahuluan,, sampai dengan kesimpulan dan daftar pustaka. Subtansi artikel cukup relevan dengan bidang ilmu pengusul.

Ruang lingkup dan kedalaman pembahasan Substansi artikel cukup sesuai dengan ruang lingkup jurnal (Jurnal Ilmiah Akuntansi dan Bisnis). Kedalaman pembahasan cukup baik didukung dengan sumber rferensi yang memadai.

Kecukupan dan Kemutakhiran Data &

Metodologi

Data dan metodologi merupakan metode yang cukup baru dengan hasil penelitian menunjukkan cukup adanya kebaruan informasi tentang Taxpayer Compliance, Tax Awareness as, and Education.

Kelengkapan unsur dan kualitas penerbit Jurnal ini termasuk sebagai nasional terakreditasi ARJUNA Sinta 2, Garuda, Crosssref, DOAJ,

Google http://sinta.ristekbrin.go.id/journals/detail?id=319.

Indikasi plagiasi Hasil uji ternutin menunjukkan similarity index = 9%

Kesesuaian bidang ilmu Jurnal cukup selaras dengan bidang ilmu pengusul, yaitu Akuntansi . Jurnal cukup selaras dengan bidang ilmu pengusul, yaitu Akuntansi .

Semarang, 2020

Reviewer 1

Prof. Dr. Abdul Rohman, M.Si, Akt

NIP. 196601081992021001

Departemen Akuntansi FEB Undip

Jabatan Fungsional : Guru Besar

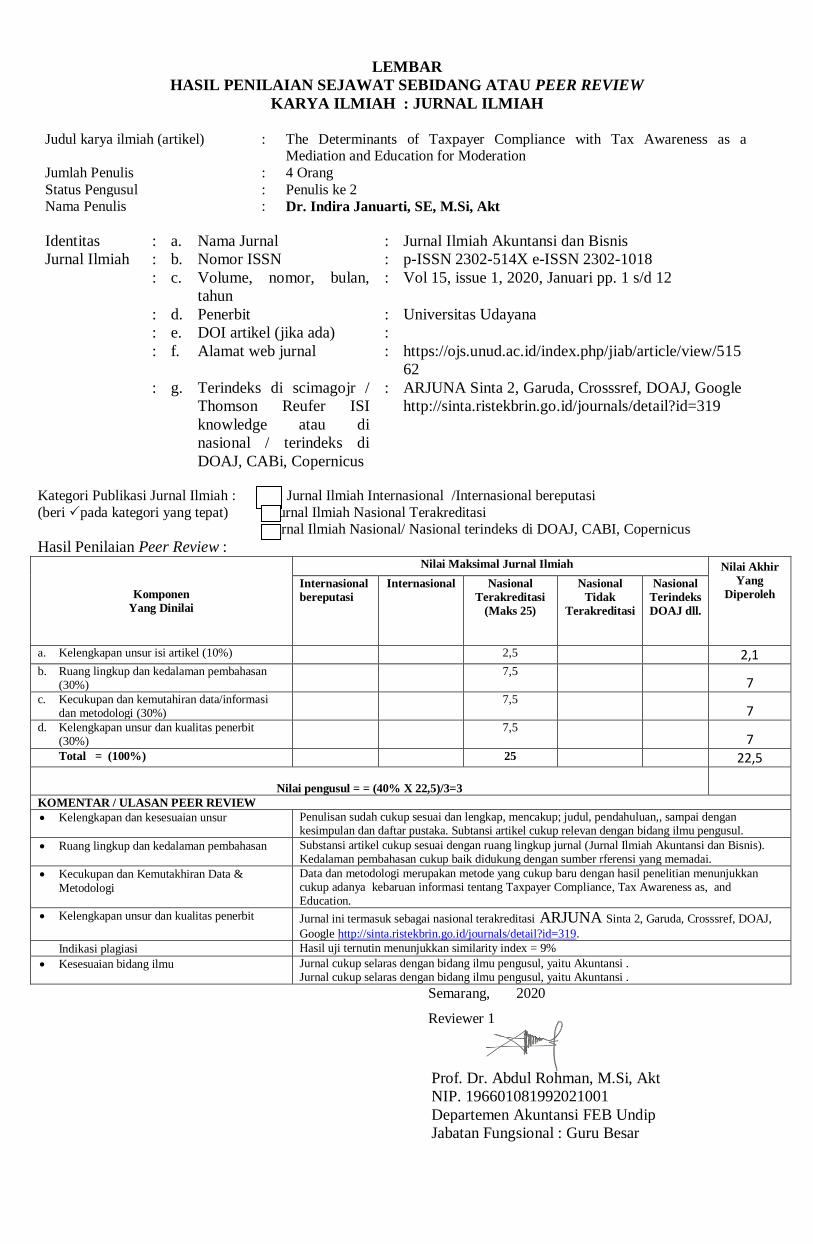

LEMBAR

HASIL PENILAIAN SEJAWAT SEBIDANG ATAU PEER REVIEW

KARYA ILMIAH : JURNAL ILMIAH

Judul karya ilmiah (artikel) : The Determinants of Taxpayer Compliance with Tax Awareness as a

Mediation and Education for Moderation

Jumlah Penulis : 4 Orang

Status Pengusul : Penulis ke 2 Nama Penulis : Dr. Indira Januarti, SE, M.Si, Akt

Identitas

Jurnal Ilmiah

: a. Nama Jurnal : Jurnal Ilmiah Akuntansi dan Bisnis

: b. Nomor ISSN : p-ISSN 2302-514X e-ISSN 2302-1018

: c. Volume, nomor, bulan,

tahun

: Vol 15, issue 1, 2020, Januari pp. 1 s/d 12

: d. Penerbit : Universitas Udayana

: e. DOI artikel (jika ada) :

: f. Alamat web jurnal : https://ojs.unud.ac.id/index.php/jiab/article/view/515

62

: g. Terindeks di scimagojr /

Thomson Reufer ISI

knowledge atau di

nasional / terindeks di

DOAJ, CABi, Copernicus

: ARJUNA Sinta 2, Garuda, Crosssref, DOAJ, Google

http://sinta.ristekbrin.go.id/journals/detail?id=319

Kategori Publikasi Jurnal Ilmiah : : Jurnal Ilmiah Internasional /Internasional bereputasi

(beri pada kategori yang tepat) Jurnal Ilmiah Nasional Terakreditasi Jurnal Ilmiah Nasional/ Nasional terindeks di DOAJ, CABI, Copernicus

Hasil Penilaian Peer Review :

Komponen

Yang Dinilai

Nilai Maksimal Jurnal Ilmiah Nilai Akhir

Yang

Diperoleh

Internasional

bereputasi

(Maks 40)

Internasional Nasional

Terakreditasi

(Maks 25)

Nasional

Tidak

Terakreditasi

(Maks 10)

Nasional

Terindeks

DOAJ dll.

(Maks 20)

a. Kelengkapan unsur isi artikel (10%) 4 2 2,5 1 2 2,5

b. Ruang lingkup dan kedalaman pembahasan

(30%)

12 6 7,5

3 6 7

c. Kecukupan dan kemutahiran data/informasi dan metodologi (30%)

12 6 7,5

3 6 6,9

d. Kelengkapan unsur dan kualitas penerbit (30%)

12 6 7,5

3 6 7

Total = (100%) 40 20 25 10 20 23,4

Nilai pengusul = 0.,4/3

3,12

KOMENTAR / ULASAN PEER REVIEW

Kelengkapan dan kesesuaian unsur Unsur yang dinilai telah ditulis dengan lengkap dan baik.

Ruang lingkup dan kedalaman pembahasan Peraturan perpajakan yang baru dan fokus negara terhadap pajak, maka sangat relevan penelitian ini dilakukan. Dengan menggunakan teori atribusi yang memberikan penjelasan bahwa ketaatan seseorang untuk memauthi peratauran dipengaruhi oleh faktor internal dan eksternal telah dijelaskan dengan baik.

Pembahasan hipotesis didukung dengan argumn yang baik dan beradsarkan hasil pengolahan data yang ada.

Kecukupan dan Kemutakhiran Data &

Metodologi

Penelitian menggunakan data promer. Penjelasan terkait dengan metode penelitian telah dilakukan dengan baik. Artikel pendukung banyak yang terbarukan 5 tahun dari sekarang.

Kelengkapan unsur dan kualitas penerbit Jurnal terakreditasi dengan No. 21 / E / KPT/ 2018, Masuk kategori Sinta 2” dari Vol. 11 No.1 Tahun 2016 sampai Vol. 15 No. 2 Tahun 2020.

Indikasi plagiasi 9%

Kesesuaian bidang ilmu Bidang kajian akuntansi keperilakukan di perpajakan untuk mengetahui faktor yang mempengaruhi ketaatan terhadap pembayaran pajak

Semarang, April 2020

Reviewer 2

Prof. Faisal, SE, M.Si, Ph.D

NIP. 197109042001121001

Departemen Akuntansi FEB Undip

Jabatan Fungsional : Guru Besar

v

VOLUME 15 ISSUE 1 JANUARY 2020 p-ISSN 2302-514X, e- ISSN 2303-1018

Do Individual Risk Attitudes, Experience, and Organizational Culture

Influence the Conservatism of Indonesian Auditors? Agus Fredy Maradona

Disclosure of Risk Factors on Prospectus and Initial Public Offerings (IPO)

Performance: Evidence from Indonesia Randy Kuswanto

Role of Hedging Mechanism in Maintaining Volatility Cash Flow and Growth

Opportunity and Their Impact on Investor Reaction Hartono, Oktavianus Pasoloran, Fransiskus Eduardus Daromes

Analyzing and Formulating a Statutory General Anti-Avoidance Rule (GAAR) in Indonesia Suparna Wijaya, Dewi Sekarsari Kusumaningtyas

The Determinants of Taxpayer Compliance with Tax Awareness as a

Mediation and Education for Moderation Pancawati Hardiningsih, Indira Januarti, Rachmawati Meita Oktaviani, Ceacilia Srimindarti

Tax Authority Versus Peer Communication: The Influence of Trust,

Service Climate, and Voluntary Cooperation Elisa Tjondro, Lajuntri Patuli, Richard Andrianto, Delitha Julitha

Corporate Governance, Market Share, and Intellectual Capital Disclosure:

Evidence from the Indonesian Agriculture and Mining Sectors Saarce Elsye Hatane, Elenne Stefanie Kuanda, Elizabeth Cornelius, Josua Tarigan

Influence of Intellectual/Emotional/Spiritual Intelligence, Independence, and Tri Hita

Karana on Auditor Performance I Gusti Ayu Made Asri Dwija Putri, Ni Gusti Putu Wirawati

Effect of Governance on the Efficiency of the Indonesian Banking Industry Fransiska Novina Hayu Indrianti, Sutrisno T., Erwin Saraswati

Tax Sanctions from the Authority Perspective Cindy Fitria Sumuan, Fidiana

The Impact of Internal Control and Individual Morals on Fraud: An Experimental Study Efrizon, Rahmat Febrianto, Rayna Kartika

Development of Management Control System Research: Study on Behavioral Research

in Accounting Journal (2006–2018) SeTin SeTin, Yvonne Agustine

Volume 15

Issue 1

Page 1-140

Denpasar January 2020

p-ISSN 2302-514X

e-ISSN 2303-1018

JURNAL ILMIAH

AKUNTANSI DAN BISNIS

JURNAL ILMIAH

AKUNTANSI DAN BISNIS

JIAB JURNAL ILMIAH AKUNTANSI DAN BISNIS

p-ISSN 2302-514X, e-ISSN 2303-1018

VOLUME 15 ISSUE 1, JANUARY 2020, Page 1-140

Jurnal Ilmiah Akuntansi dan Bisnis (JIAB) aims as a media of information and exchange of

scientific articles between teaching staff, alumni, students, practitioners and observers of science

in accounting and business. JIAB editors received scientific articles from empirical research and

theoretical studies related to accounting and business, which of course have never been

published elsewhere. Jurnal Ilmiah Akuntansi dan Bisnis (JIAB) is published twice a year in

January and July by the Accounting Department of Udayana University collaborated with the

Ikatan Sarjana Ekonomi Indonesia (ISEI). Editor In Chief

Dodik Ariyanto, Faculty of Economics and Business, Udayana University

(Scopus ID: 57211398891)

Managing Editor

I Gusti Ayu Eka Damayanthi, Faculty of Economics and Business, Udayana University

(Scopus ID: 57200207404)

Ayu Aryista Dewi, Faculty of Economics and Business, Udayana University

(Scopus ID: 57213172617)

Associate Editor

Yuni Yuningsih, Curtin University

(Scopus ID: 36620017700)

Editorial Board

Agoes Ganesha Rahyuda, Ikatan Sarjana Ekonomi Indonesia (ISEI)

(Scopus ID: 57195473487)

Noor Adwa Sulaiman, University of Malaya

(Scopus ID: 55968241600)

Phong Thanh Nguyen, Ho Chi Minh City Open University

(Scopus ID: 57211379007)

Shankar Kathiresan, Alagappa University

(Scopus ID: 56884031900)

Adji Achmad Rinaldo Fernandes, Faculty of Math and Science, Brawijaya University

(Scopus ID: 56374014200)

I G. A. M. Asri Dwija Putri, Faculty of Economics and Business, Udayana University

Ni Putu Sri Harta Mimba, Faculty of Economics and Business, Udayana University

(Scopus ID: 36442521600)

Ardi Gunardi, Faculty of Economics and Business, Pasundan University

(Scopus ID: 57191667735)

Dewa Gede Wirama, Faculty of Economics and Business, Udayana University

Administration

I Ketut Suadnyana, Faculty of Economics and Business, Udayana University

I Made Gilang Jhuniantara, Faculty of Economics and Business, Udayana University

Ni Putu Cempaka Widyawati, Faculty of Economics and Business, Udayana University

Editor’s Address

Journal Room, BJ Building Lt. 3, Faculty of Economics and Business,

Udayana University

Managed by Accounting Department and in collaboration with

Association of Indonesian Bachelor of Economics Denpasar Branch

P. B. Sudirman Street Denpasar-Bali, Indonesia

E-mail : [email protected]

Telp. 0361-255511 / Fax. 0361-223344

https://ojs.unud.ac.id/index.php/jiab/index

JIAB JURNAL ILMIAH AKUNTANSI DAN BISNIS

p-ISSN 2302 - 514X, e-ISSN 2303-1018

VOLUME 15 ISSUE 1, JANUARY 2020

i

TABLE OF CONTENTS

Editor’s Introduction .......................................................................................................................... ii

Do Individual Risk Attitudes, Experience, and Organizational Culture Influence the

Conservatism of Indonesian Auditors?

Agus Fredy Maradona .......................................................................................................................... 1-14

Disclosure of Risk Factors on Prospectus and Initial Public Offerings (IPO)

Performance: Evidence from Indonesia

Randy Kuswanto ................................................................................................................................... 15-22

Role of Hedging Mechanism in Maintaining Volatility Cash Flow and Growth

Opportunity and Their Impact on Investor Reaction

Hartono Hartono, Oktavianus Pasoloran, Fransiskus Eduardus Daromes ............................................ 23-34

Analyzing and Formulating a Statutory General Anti-Avoidance Rule (GAAR) in

Indonesia

Suparna Wijaya, Dewi Sekarsari Kusumaningtyas .............................................................................. 35-48

The Determinants of Taxpayer Compliance with Tax Awareness as a Mediation and

Education for Moderation

Pancawati Hardiningsih, Indira Januarti, Rachmawati Meita Oktaviani, Ceacilia Srimindarti ............ 49-60

Tax Authority Versus Peer Communication: The Influence of Trust, Service Climate,

and Voluntary Cooperation

Elisa Tjondro, Lijuntri Patuli, Richard Andrianto, Delitha Julitha ....................................................... 61-74

Corporate Governance, Market Share, and Intellectual Capital Disclosure: Evidence

from the Indonesian Agriculture and Mining Sectors

Saarce Elsye Hatane, Elenne Stefanie Kuanda, Elizabeth Cornelius, Josua Tarigan ........................... 75-84

Influence of Intellectual/Emotional/Spiritual Intelligence, Independence, and Tri Hita

Karana on Auditor Performance

I Gusti Ayu Made Asri Dwija Putri, Ni Gusti Putu Wirawati .............................................................. 85-92

Effect of Governance on the Efficiency of the Indonesian Banking Industry

Fransiska Novina Hayu Indrianti, Sutrisno T., Erwin Saraswati .......................................................... 93-106

Tax Sanctions from the Authority Perspective

Cindy Fitria Sumuan, Fidiana Fidiana .................................................................................................. 107-118

The Impact of Internal Control and Individual Morals on Fraud: An Experimental Study

Efrizon Efrizon, Rahmat Febrianto, Rayna Kartika .............................................................................. 119-126

Development of Management Control System Research: Study on Behavioral Research

in Accounting Journal (2006–2018)

SeTin SeTin, Yvonne Augustine .......................................................................................................... 127-140

Subject Index ....................................................................................................................................... 141-142

Author Index ....................................................................................................................................... 143

Reviewer .............................................................................................................................................. 144

Guidelines for Writing ........................................................................................................................ 145-147

List of Previous Articles

JIAB JURNAL ILMIAH AKUNTANSI DAN BISNIS

p-ISSN 2302 - 514X, e-ISSN 2303-1018

VOLUME 15 ISSUE 1, JANUARY 2020

ii

EDITOR’S INTRODUCTION

Dear reader,

Jurnal Ilmiah Akuntansi dan Bisnis (JIAB) is published twice a year, in January and July. JIAB

is published with reference to the Periodical Accreditation Guidelines (Number 49 / Dikti / Kep / 2011)

as well as the JIAB Article Writing Guidelines included at the end of this journal. JIAB aims as a media

of information and exchange of scientific articles between teaching staff, alumni, students, practitioners

and observers of science in the fields of accounting and business. The JIAB editorial staff received

various scientific articles as a result of empirical research and theoretical studies related to accounting

and business, which of course have never been published in other media. For the first time in Volume 15

Issue 1 January 2020, JIAB published an article which was entirely in English.

JIAB Volume 15 Issue 1 January 2020 published twelve scientific articles on various interesting

topics with quantitative and qualitative analysis. Journal topics published in this number consist of Do

Individual Risk Attitudes, Experience, and Organizational Culture Influence the Conservatism of

Indonesian Auditors?, Disclosure of Risk Factors on Prospectus and Initial Public Offerings (IPO)

Performance: Evidence from Indonesia, Role of Hedging Mechanism in Maintaining Volatility Cash

Flow and Growth Opportunity and Their Impact on Investor Reaction, Analyzing and Formulating a

Statutory General Anti-Avoidance Rule (GAAR) in Indonesia, The Determinants of Taxpayer

Compliance with Tax Awareness as a Mediation and Education for Moderation, Tax Authority Versus

Peer Communication: The Influence of Trust, Service Climate, and Voluntary Cooperation, Corporate

Governance, Market Share, and Intellectual Capital Disclosure: Evidence from the Indonesian

Agriculture and Mining Sectors, Influence of Intellectual/Emotional/Spiritual Intelligence,

Independence, and Tri Hita Karana on Auditor Performance, Effect of Governance on the Efficiency of

the Indonesian Banking Industry, Tax Sanctions from the Authority Perspective, The Impact of Internal

Control and Individual Morals on Fraud: An Experimental Study and Development of Management

Control System Research: Study on Behavioral Research in Accounting Journal (2006–2018).

Jurnal Ilmiah Akuntansi dan Bisnis (JIAB) indexed by crossref, SINTA 2 Riset Dikti, IPI,

Google Scholar, Directory Of Open Access Journals (DOAJ). We are waiting for the participation of

readers to submit the best articles for us to publish in subsequent editions.

Happy reading,

Editorial Team

Do Individual Risk Attitudes, Experience, and Organizational Culture Influence

The Conservatism of Indonesian Auditors?

Agus Fredy Maradona

Faculty of Economics and Business, Universitas Pendidikan Nasional, Indonesia

email: [email protected]

1Maradona, Do Individual Risk ...

DOI: https://doi.org/10.24843/JIAB.2020.v15.i01.p01

INTRODUCTION

This study examines the factors that influence

the judgement and decision of auditors when

performing an audit of financial statements in

Indonesia. Specifically, this study investigates the

effect of individual risk attitude, experience, and

organisational culture on the conservatism of auditors

when performing audit procedures on items of

financial statements of their clients. As the Indonesian

financial accounting standards are moving closer to

full adoption of the International Financial Reporting

Standards (IFRS), these Indonesian standards have

become more principles-based, and less rules-based,

in comparison to the previous versions of the

standards (Maradona & Chand, 2018).

Principles-based accounting standards demand

extensive use of professional judgements and require

company managers to make a significant number of

accounting estimates in their financial statements

(Nobes, 2005; Bennett, Bradbury, & Prangnell, 2006;

Carmona & Trombetta, 2008; Bradbury & Schröder,

2012; Wehrfritz & Haller, 2014). As managers can

exercise their judgments and discretions when

determining accounting estimates, and as there have

been cases where auditors have been held

responsible for failure to properly evaluate such

estimates, there has been a growing concern by

authorities over the conservatism of auditors when

evaluating these judgements and estimates (see Firth,

Mo, & Wong, 2014). This issue, in turn, has also

attracted growing attention in the auditing literature

(Lu & Sapra, 2009; Feldmann & Read, 2010; Firth,

Mo, & Wong, 2014; Lennox & Kausar, 2017).

Conservatism is one of the oldest principles in

accounting and auditing (Watts, 2003; Lu & Sapra,

2009). The Financial Accounting Standards Board

(FASB) (1980) defines accounting conservatism as

“a prudent reaction to uncertainty to try to ensure

that uncertainties and risks inherent in business

situations are adequately considered” (par. 95). In a

more elaborate manner, Gray (1988) defines

conservatism in the context of financial reporting as

ABSTRACT

This study examines the effects of individual risk attitudes, professional

experience, and organizational culture on auditor conservatism in

Indonesia. On the basis of a factorial survey involving 153 auditors in

three major cities in Indonesia (Jakarta, Surabaya, and Denpasar),

this study finds strong evidence that, compared with others, auditors

with a lower tendency to take risks and those who have less

professional experience tend to be more conservative when

performing audit tasks. Nonetheless, this study does not find evidence

of the influence of organizational culture on auditor conservatism.

Overall, the findings of this study could be of interest to professional

associations, regulatory bodies, and other policymakers in Indonesia

and other countries as they attempt to constrain aggressive reporting

through high-quality independent audits by public accountants in their

jurisdictions.

Keywords: Auditor conservatism, risk attitudes, experience,

organisational culture, auditing standards.

Received:

01 November 2019

Revised:

29 November 2019

Accepted:

08 January 2020

ARTICLE INFORMATION:

Volume 15

Issue 1

January 2020

Page 1 - 14

p-ISSN 2302-514X

e-ISSN 2303-1018

Jurnal Ilmiah Akuntansidan Bisnis(JIAB)

Analyzing and Formulating a Statutory General Anti-Avoidance Rule (GAAR)

in Indonesia

Suparna Wijaya1

Dewi Sekarsari Kusumaningtyas2

1,2Department of Tax, Polytechnic of State Finance STAN, Indonesiaemail: [email protected]

DOI: https://doi.org/10.24843/JIAB.2020.v15.i01.p04

INTRODUCTION

The International Monetary Fund (IMF) Country

Report for Indonesia in 2017 (2018, 11) states that

Indonesia’s tax-to-GDP ratio has continued to decline

in recent years. Based on data from the World Bank,

Indonesia’s tax ratio continued to decline from 2012

to 2016, which were 11.38 percent, 11.29 percent ,

10.84 percent , 10.75 percent , and 10.33 percent,

respectively. The Indonesian tax ratio in 2016 even

ranks lowest among developing countries in Asia

(IMF, 2018).

According to Besley & Persson (2014, 109),

one of the main factors in low tax revenue in

developing countries is the practice of high tax

avoidance. Tax is a compelling contribution to the

state. In the theory of risk aversion, Allingham and

Sanmo believe that no individual is willing to pay taxes

voluntarily (Sarjunajuntak & Mukhlis, 2012).

Individuals will always oppose paying taxes. In other

words, taxpayers will make various efforts to reduce

the tax burden so that the net income obtained

becomes greater. Efforts to reduce the tax burden

are often carried out through aggressive tax planning

ABSTRACT

Dealing with the practice of tax avoidance in general, many countries have

compiled and implemented their own general anti-avoidance rules (GAAR).

This research aims to explore the potential of statutory GAAR in handling

tax avoidance practices in Indonesia and SAAR formulas that are suitable

for the Indonesian context. This qualitative research employed a case study

approach. Results show that the application of SAAR and the principle of

substance over form in Indonesia cannot yet be applied properly; thus

GAAR is needed. It is expected that the implementation of statutory GAAR

can accommodate the limitations of regulators in light of unknown and

future tax avoidance schemes.

Keywords: Tax-avoidance, tax planning, specific anti avoidance rule (SAAR),

international tax.

practices or tax avoidance practices. According to

the Australian Tax Office (2004, 11), aggressive tax

planning is the point where tax planning goes beyond

the policy intent of the law. Meanwhile, tax avoidance

is a manipulation of one ‘s affairs within the law in

order to reduce the tax dues (James et al., 1978).

According to Deny (2016) Bambang Brodjonegoro,

as Minister of Finance at that time, once stated that

since the past ten years, 2,000 foreign investment

companies (PMA) have not paid taxes. As a result,

in this period the country suffered losses of up to

Rp. 500 trillion. This condition shows the high

practice of tax-avoidance in Indonesia.The General

Director of Taxes at the time, Ken Dwijugiasteadi,

revealed that those who intended not to pay taxes

were those companies not paying Corporate Income

Tax (PPh) Article 25 and Article 29 for reasons of

continuous loss, even though in fact they still managed

to exist from year to year. Ken also stated that Article

25 and Article 29 PPh is the type of tax that is most

difficult to withdraw because it is attached to the

Agency itself (Ariyanti, 2016).

Received:

28 June 2019

Revised:

18 September 2019

Accepted:

28 November 2019

ARTICLE INFORMATION:

Volume 15

Issue 1

January 2020

Page 35 - 48

p-ISSN 2302-514X

e-ISSN 2303-1018

Jurnal Ilmiah Akuntansidan Bisnis(JIAB)

Wijaya and Kusumaningtyas, Analyzing and Formulating... 35

The Determinants of TaxpayerCompliance with Tax Awarenessas a Mediation and Education for

Moderationby Indira Januarti

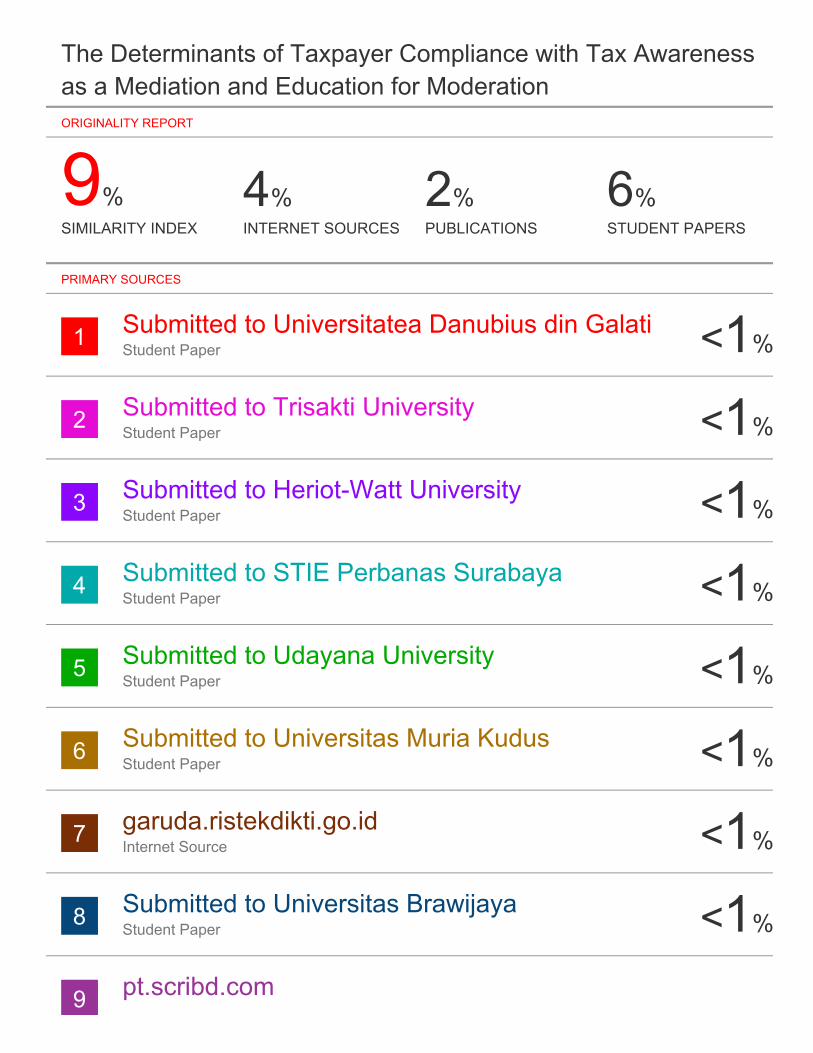

Submission date: 04-Jul-2020 10:39AM (UTC+0700)Submission ID: 1353261598File name: Jurnal_Unud_2020.pdf (429.42K)Word count: 6966Character count: 39426

9%SIMILARITY INDEX

4%INTERNET SOURCES

2%PUBLICATIONS

6%STUDENT PAPERS

1 <1%

2 <1%

3 <1%

4 <1%

5 <1%

6 <1%

7 <1%

8 <1%

9

The Determinants of Taxpayer Compliance with Tax Awarenessas a Mediation and Education for ModerationORIGINALITY REPORT

PRIMARY SOURCES

Submitted to Universitatea Danubius din GalatiStudent Paper

Submitted to Trisakti UniversityStudent Paper

Submitted to Heriot-Watt UniversityStudent Paper

Submitted to STIE Perbanas SurabayaStudent Paper

Submitted to Udayana UniversityStudent Paper

Submitted to Universitas Muria KudusStudent Paper

garuda.ristekdikti.go.idInternet Source

Submitted to Universitas BrawijayaStudent Paper

pt.scribd.com

<1%

10 <1%

11 <1%

12 <1%

13 <1%

14 <1%

15 <1%

16 <1%

17 <1%

Internet Source

pdfs.semanticscholar.orgInternet Source

giapjournals.comInternet Source

media.neliti.comInternet Source

ejournal.upbatam.ac.idInternet Source

Submitted to Asia Pacific University College ofTechnology and Innovation (UCTI)Student Paper

Suyanto Suyanto, Endah Trisnawati. "THEINFLUENCE OF TAX AWARENESS TOWARDTAX COMPLIANCE OF ENTREPRENEURIALTAXPAYERS AND CELENGAN PADJEGPROGRAM AS A MODERATING VARIABLE: ACase Study At The Pratama Tax Office OfWonosari Town", INFERENSI, 2016Publication

Submitted to iGroupStudent Paper

Submitted to Universitas Jenderal SoedirmanStudent Paper

18 <1%

19 <1%

20 <1%

21 <1%

22 <1%

23 <1%

24 <1%

25 <1%

26 <1%

Jorge Luis García-Alcaraz, Diana Jazmín Prieto-Luevano, Aidé Aracely Maldonado-Macías, JulioBlanco-Fernández et al. "Structural equationmodeling to identify the human resource value inthe JIT implementation: case maquiladorasector", The International Journal of AdvancedManufacturing Technology, 2014Publication

Submitted to Universitas Mercu BuanaStudent Paper

Submitted to Coventry UniversityStudent Paper

journal.umy.ac.idInternet Source

www.mdpi.comInternet Source

ojs.unpkediri.ac.idInternet Source

open.library.ubc.caInternet Source

jurnalmahasiswa.unesa.ac.idInternet Source

Submitted to Politeknik Negeri SriwijayaStudent Paper

Spohrer, Kai. "Findings", Progress in IS, 2016.

27 <1%

28 <1%

29 <1%

30 <1%

31 <1%

32 <1%

33 <1%

34 <1%

35 <1%

36 <1%

37 <1%

Publication

Submitted to University of HullStudent Paper

Submitted to Universiti Teknologi MalaysiaStudent Paper

text-id.123dok.comInternet Source

pasca.unhas.ac.idInternet Source

eprints.undip.ac.idInternet Source

Submitted to Bournemouth UniversityStudent Paper

Submitted to Fakultas Ekonomi UniversitasIndonesiaStudent Paper

karyailmiah.unisba.ac.idInternet Source

journal.unismuh.ac.idInternet Source

www.arabianjbmr.comInternet Source

Submitted to University of Pretoria

38 <1%

39 <1%

40 <1%

Exclude quotes On

Exclude bibliography On

Exclude matches Off

Student Paper

Submitted to Ghana Technology UniversityCollegeStudent Paper

Submitted to Universiti Putra MalaysiaStudent Paper

Related Documents