June 2014 TransAlta Investor Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

June 2014

TransAlta

Investor Presentation

2

Forward Looking Statements

This presentation may contain forward looking statements, including statements regarding the business and anticipated financial performance of

TransAlta Corporation in 2014, 2015 and subsequent years. All forward looking statements are based on our beliefs and assumptions based on

information available at the time the assumptions were made and on management’s experience and perception of historical trends, current conditions

and expected future developments, and other factors deemed appropriate in the circumstances. These statements are not guarantees of our future

performance and are subject to a number of risks and uncertainties that may cause actual results to differ materially from those contemplated by the

forward looking statements. In particular, this presentation contains forward looking statements pertaining to, among other things: expectations

relating to the timing of the completion and commissioning of projects under development and their attendant costs; our estimated spend on growth

and sustaining capital and productivity projects; expectations in terms of the cost of operations, capital spend and maintenance; expectations in

respect of future electricity prices and the impact of natural gas prices on electricity prices; the impact of certain hedges on future reported earnings

and cash flows; expectations related to future earnings, cash flow and funds from operations; expectations for demand for electricity in both the short-

term and the long-term and the resulting impact on electricity prices; expected impacts of load growth on electricity supply and the development of

additional generation; expectations in respect of generation availability, capacity and production; expected financing of our capital expenditures;

expected governmental regulatory regimes and legislation and their anticipated impact on us; our trading strategy and the expected results from our

trading activities; and expectations in respect to the global economic environment. Factors that may adversely impact our forward looking statements

include risks relating to, among other things: fluctuations in market prices and availability of fuel supplies required to generate electricity and in the

price of electricity; the regulatory and political environments in the jurisdictions in which we operate; environmental requirements and changes in, or

liabilities under, these requirements; changes in general economic conditions including interest rates; operational risks involving our facilities,

including unplanned outages at such facilities; disruptions in the transmission and distribution of electricity; effects of weather; disruptions in the

source of fuels, water, or wind required to operate our facilities; natural disasters; the threat of domestic terrorism and cyber-attacks; equipment

failure; energy trading risks; industry risk and competition; fluctuations in the value of foreign currencies and foreign political risks; the need for

additional financing counterparty credit risk; insurance coverage; reliance on key personnel; labour relations matters; and risks associated with

development projects and acquisitions. The foregoing risk factors, among others, are described in further detail in the Risk Management section of

our 2013 annual MD&A and under the heading “Risk Factors” in our 2014 Annual Information Form.

Except to the extent required by law, we assume no obligation to publicly update or revise any forward looking statements, whether as a result of new

information, future events or otherwise. All forward looking statements in this presentation are expressly qualified in their entirety by these cautionary

statements. For information on our risks please refer to our 2014 Annual Information Form which has been filed on SEDAR and can be accessed at

www.sedar.com.

Unless otherwise specified, all dollar amounts are expressed in Canadian dollars.

This presentation may contain references to comparable earnings comparable earnings per share, comparable EBITDA, funds from operations, and

funds from operations per share which are not defined under IFRS. Refer to the Non-IFRS financial measures section of TransAlta’s 2013 annual

MD&A for an explanation and, where applicable, reconciliations to net earnings attributable to common shareholders and cash flow from operating

activities. The presentation may also contain references to gross margin and operating income, which are Additional IFRS measures. Please refer to

the Additional IFRS measures section of the MD&A.

3

Strategic & Financial Objectives

4

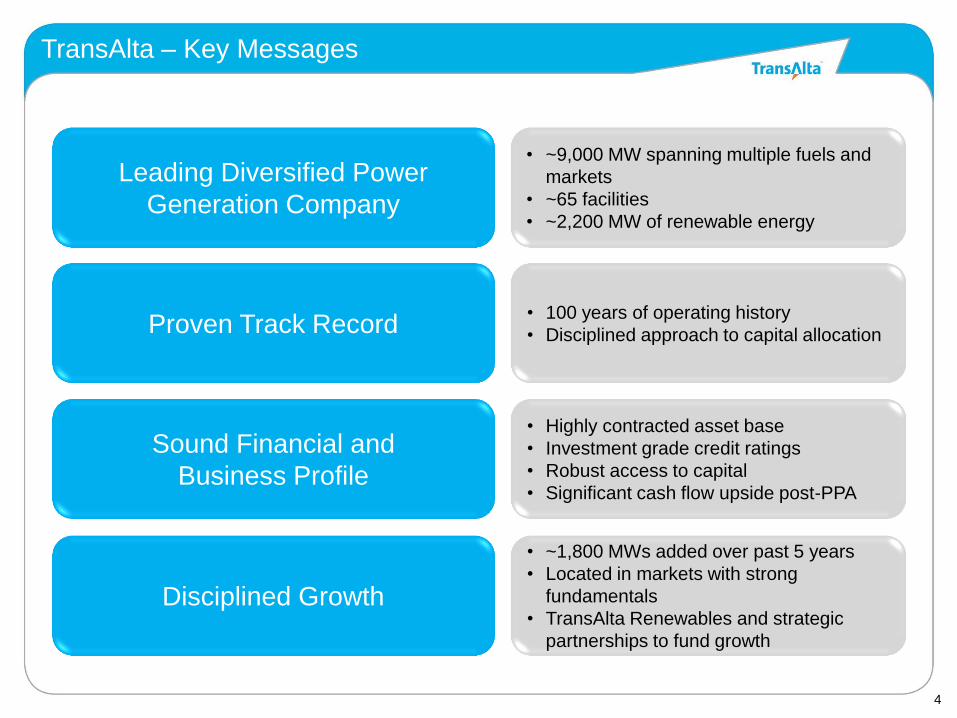

Leading Diversified Power

Generation Company

Proven Track Record

Sound Financial and

Business Profile

Disciplined Growth

• ~9,000 MW spanning multiple fuels and

markets

• ~65 facilities

• ~2,200 MW of renewable energy

• 100 years of operating history

• Disciplined approach to capital allocation

• Highly contracted asset base

• Investment grade credit ratings

• Robust access to capital

• Significant cash flow upside post-PPA

• ~1,800 MWs added over past 5 years

• Located in markets with strong

fundamentals

• TransAlta Renewables and strategic

partnerships to fund growth

TransAlta – Key Messages

5

Our Business

Canada’s largest publicly traded wholesale power

generator & marketer with over 100 years of operating

experience

Diversified asset base with ~65 facilities strategically

positioned in Canada, Western U.S. and Western

Australia

Total fleet capacity of ~9,000 MWs

Our business lines:

• Coal

• Gas

• Renewable energy (Hydro and Wind)

• Energy trading, which optimizes our other

business lines

Sponsor and majority owner of TransAlta Renewables

Listed on Toronto and New York stock exchanges

Coal:

4,930 MW

Gas:

1,695 MW

Hydro:

914 MW1

Wind:

1,271MW1

1Includes 100% of TransAlta Renewables’ assets.

6

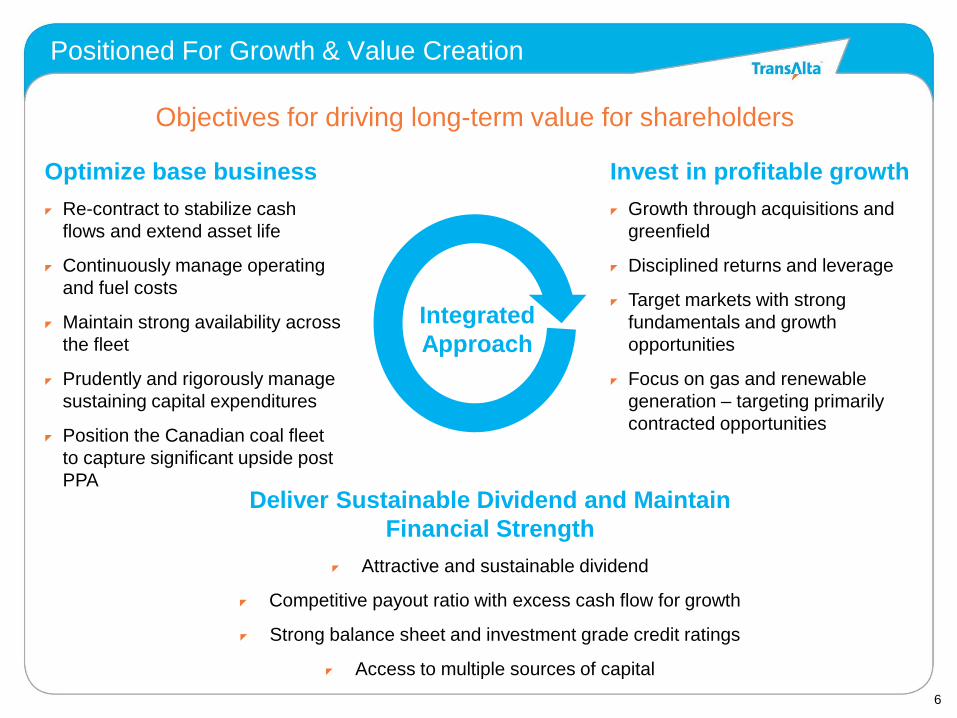

Objectives for driving long-term value for shareholders

Deliver Sustainable Dividend and Maintain

Financial Strength

Attractive and sustainable dividend

Competitive payout ratio with excess cash flow for growth

Strong balance sheet and investment grade credit ratings

Access to multiple sources of capital

Optimize base business

Re-contract to stabilize cash

flows and extend asset life

Continuously manage operating

and fuel costs

Maintain strong availability across

the fleet

Prudently and rigorously manage

sustaining capital expenditures

Position the Canadian coal fleet

to capture significant upside post

PPA

Invest in profitable growth

Growth through acquisitions and

greenfield

Disciplined returns and leverage

Target markets with strong

fundamentals and growth

opportunities

Focus on gas and renewable

generation – targeting primarily

contracted opportunities

Positioned For Growth & Value Creation

Integrated

Approach

7

20001

20141

Strategic Evolution of TransAlta

1Net Capacity Ownership Interest. Includes 100% of TransAlta Renewables’ assets.

Actively shifting our business

mix by growing renewables

8

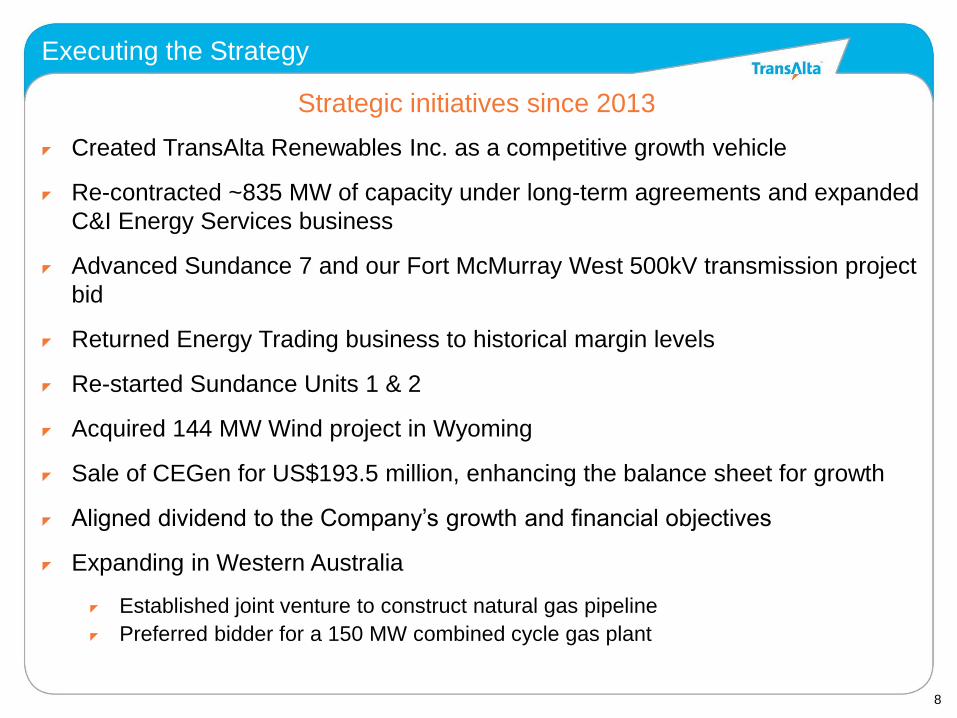

Executing the Strategy

Created TransAlta Renewables Inc. as a competitive growth vehicle

Re-contracted ~835 MW of capacity under long-term agreements and expanded

C&I Energy Services business

Advanced Sundance 7 and our Fort McMurray West 500kV transmission project

bid

Returned Energy Trading business to historical margin levels

Re-started Sundance Units 1 & 2

Acquired 144 MW Wind project in Wyoming

Sale of CEGen for US$193.5 million, enhancing the balance sheet for growth

Aligned dividend to the Company’s growth and financial objectives

Expanding in Western Australia

Established joint venture to construct natural gas pipeline

Preferred bidder for a 150 MW combined cycle gas plant

Strategic initiatives since 2013

9

2008 2009 2010

2011 2013 2012 2013

694 MW

Canadian Hydro

80 MW

Kent Hills 123 MW

Ardenville / Kent Hills 2 19 MW

Bone Creek

225 MW

Keephills 3

125 MW

Solomon

68 MW

New Richmond

2011

132 MW

Summerview 2 / Blue Trail

2010

144 MW

Wyoming Wind

Disciplined growth with a focus on contracted assets

TransAlta’s 5-Year Growth Track Record

~ 1,800 MW added in our core markets over 5 years1

150 MW

Western Australia Gas

Plant and Pipeline

¹Indicative illustration based on annualized EBITDA contributions. 2013 includes recent acquisition of 144 MW Wyoming Wind assuming full year pro-forma. Does not include natural gas

pipeline in Western Australia which will contribute EBITDA beginning in 2015. EBITDA does not include Port Hedland which will commission in early 2017.

2014

10

Creation of TransAlta Renewables

29 megawatts installed

generating capacity

1,255 billion total

market capitalization

$ 1.3 billion assets

$2.0 renewable power

generation facilities

One of the Largest Publicly-Traded Renewable Companies in Canada

British Columbia 4 hydro

77 MW

Alberta 4 hydro

21 MW

10 wind

417 MW

Ontario 4 hydro

7 MW

3 wind

398 MW

Quebec 1 wind

68 MW

New Brunswick 2 wind

125 MW

Bone Creek 19MW

Upper Mamquam 25MW

Pingston 23MW

Akolkolex 10MW

Summerview One 70MW

Sinnott 7MW

Castle River 44MW

Belly River 3MW

Waterton 3MW

Cowley North 20MW

Summerview Two 66MW

Macleod Flats 3MW Blue Trail 66MW

Soderglen 35MW Taylor Hydro 13MW

McBride Lake 38MW

Ardenville 69MW

St. Mary 2MW Misema 3MW

Moose Rapids 1MW

Appleton 1MW

Galetta 2MW

Wolfe Island 198MW

Melancthon One 68MW

Melancthon Two 132MW

New Richmond 68MW

Kent Hills One 80MW

Kent Hills Two 45MW

High Quality Diversified Portfolio 5 Operating Regions

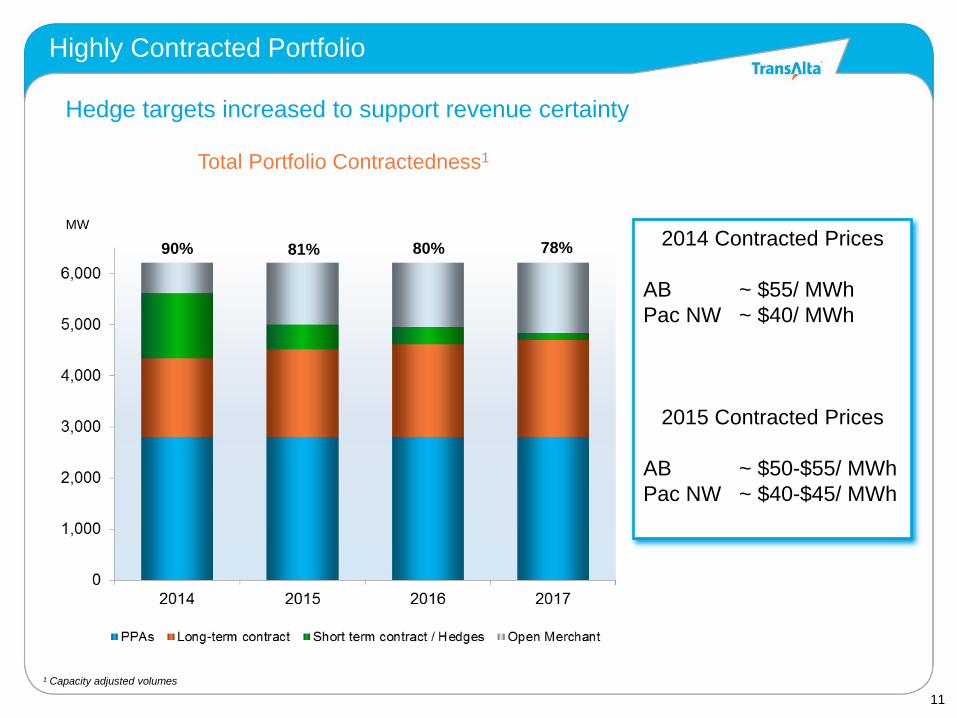

11

Total Portfolio Contractedness1

Hedge targets increased to support revenue certainty

2014 Contracted Prices

AB ~ $55/ MWh

Pac NW ~ $40/ MWh

2015 Contracted Prices

AB ~ $50-$55/ MWh

Pac NW ~ $40-$45/ MWh

Highly Contracted Portfolio

¹ Capacity adjusted volumes

MW

90% 81% 80% 78%

12

Financial Review & Outlook

13

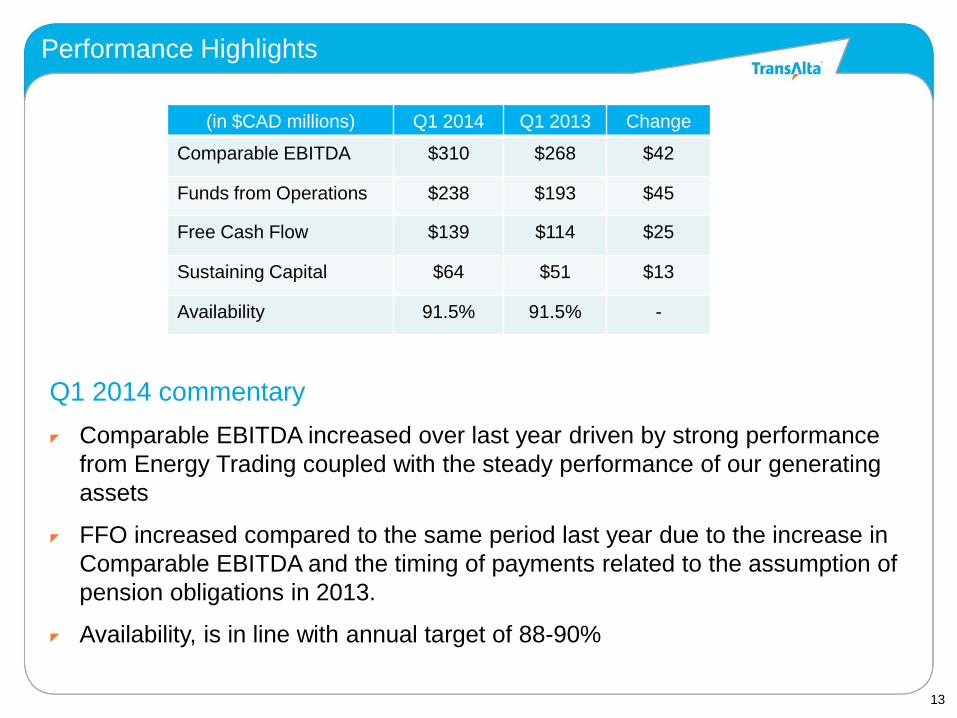

Performance Highlights

Q1 2014 commentary

Comparable EBITDA increased over last year driven by strong performance

from Energy Trading coupled with the steady performance of our generating

assets

FFO increased compared to the same period last year due to the increase in

Comparable EBITDA and the timing of payments related to the assumption of

pension obligations in 2013.

Availability, is in line with annual target of 88-90%

(in $CAD millions) Q1 2014 Q1 2013 Change

Comparable EBITDA $310 $268 $42

Funds from Operations $238 $193 $45

Free Cash Flow $139 $114 $25

Sustaining Capital $64 $51 $13

Availability 91.5% 91.5% -

14

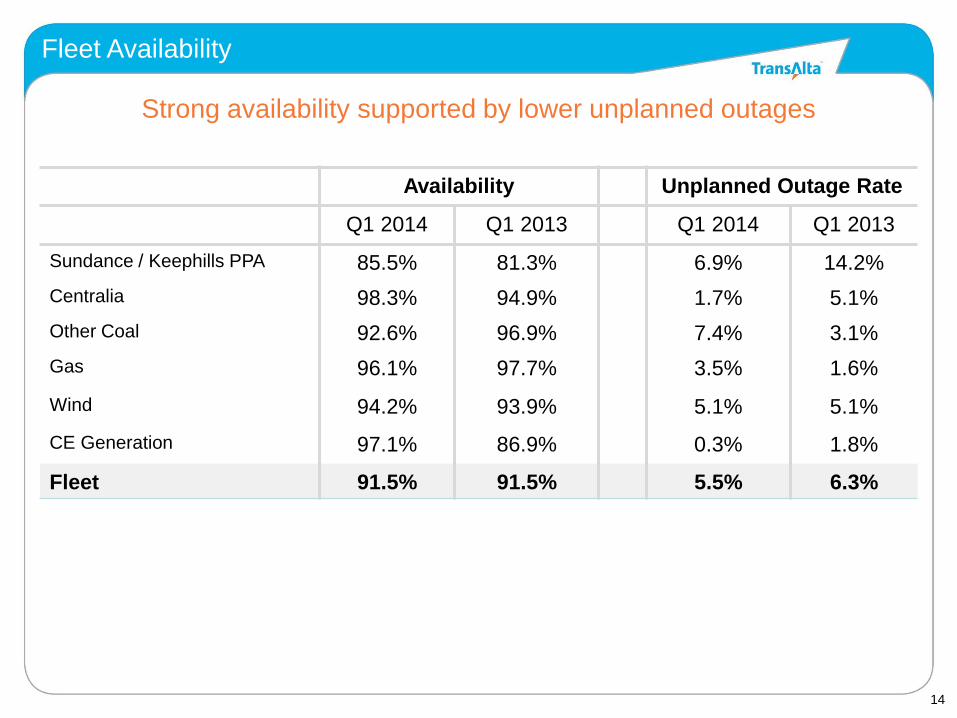

Fleet Availability

Availability Unplanned Outage Rate

Q1 2014 Q1 2013 Q1 2014 Q1 2013

Sundance / Keephills PPA 85.5% 81.3% 6.9% 14.2%

Centralia 98.3% 94.9% 1.7% 5.1%

Other Coal 92.6% 96.9% 7.4% 3.1%

Gas 96.1% 97.7% 3.5% 1.6%

Wind 94.2% 93.9% 5.1% 5.1%

CE Generation 97.1% 86.9% 0.3% 1.8%

Fleet 91.5% 91.5% 5.5% 6.3%

Strong availability supported by lower unplanned outages

15

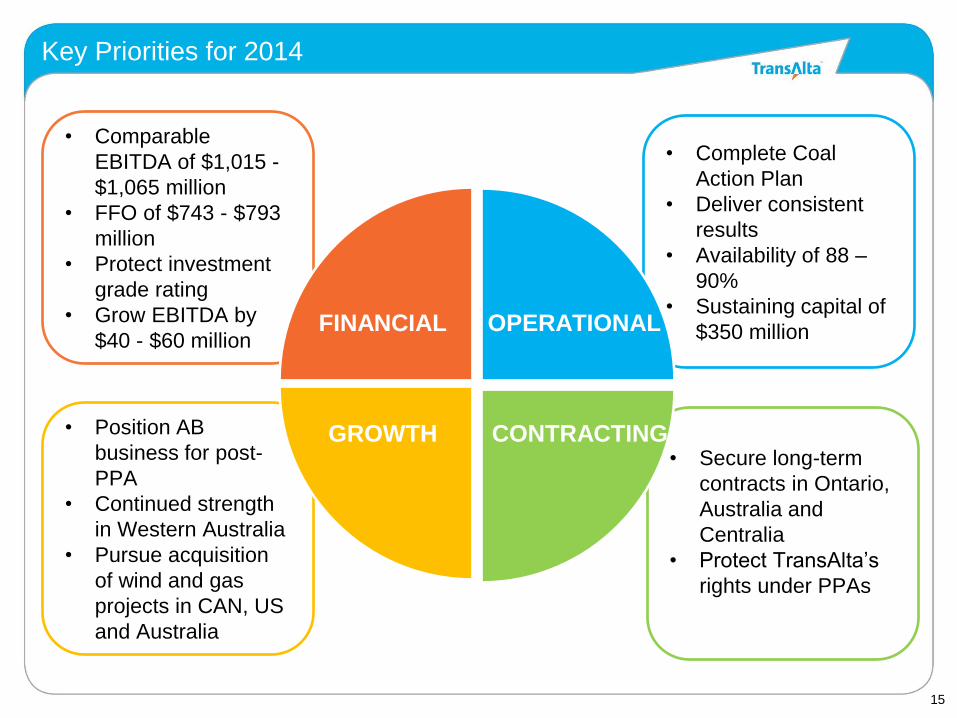

Key Priorities for 2014

• Secure long-term

contracts in Ontario,

Australia and

Centralia

• Protect TransAlta’s

rights under PPAs

• Complete Coal

Action Plan

• Deliver consistent

results

• Availability of 88 –

90%

• Sustaining capital of

$350 million

• Comparable

EBITDA of $1,015 -

$1,065 million

• FFO of $743 - $793

million

• Protect investment

grade rating

• Grow EBITDA by

$40 - $60 million

• Position AB

business for post-

PPA

• Continued strength

in Western Australia

• Pursue acquisition

of wind and gas

projects in CAN, US

and Australia

OPERATIONAL

CONTRACTING

FINANCIAL

GROWTH

16

Canadian Coal Improvements

New leadership with proven experience in similar vintage and type of assets:

Substantial cost reductions

Management of structural change across entire portfolios in response to

very challenging power market conditions

Implementation of Coal Action Plan focused on:

Organizational effectiveness

Reliability engineering

Major maintenance execution efficiencies

Operational Discipline

Focus on competitive operating model

Maintain daily focus on the competitiveness of the mining operation

Raising the bar at CDN Coal

17

Markets and Growth

18 ¹Per AESO

Markets where TransAlta is Positioned for Growth

Western U.S. Alberta

Ontario / B.C. Western Australia

GDP growth of 2 – 3% per year

6,000 MW of new generation by 20221

Cogen and combined cycle

Strong load growth

Coal generation retirement

~1.4% annual load growth over next ten years

California: 15,000 MW by 2020

WECC: 25,000-30,000 MW by 2020

Opportunity for gas-fired generation

GDP growth of 3 – 4% per year

Mining industry is largest driver of new opportunities

Ontario:

Near term conservation measures

Medium-term opportunity due to nuclear retirements/ refurbishments

B.C.:

~3% load growth to 2020

LNG development

19

Sundance 7

Continued development of Sundance 7 with the filing of

AUC permits and completing a Request for Interest from

engineering companies for the construction contract

TAMA Transmission

Successfully qualified to compete in the next phase of the

Fort McMurray West 500 KV Transmission Project

Western Australia Pipeline

Constructing a natural gas pipeline with joint venture

partner in Western Australia to serve customers in the

region to be operational in early 2015

Port Hedland

Named the successful bidder to build, own and operate a

150 MW combined cycle gas power station in South

Hedland, Western Australia. Full commissioning in 2017.

Recent Growth Progress

20

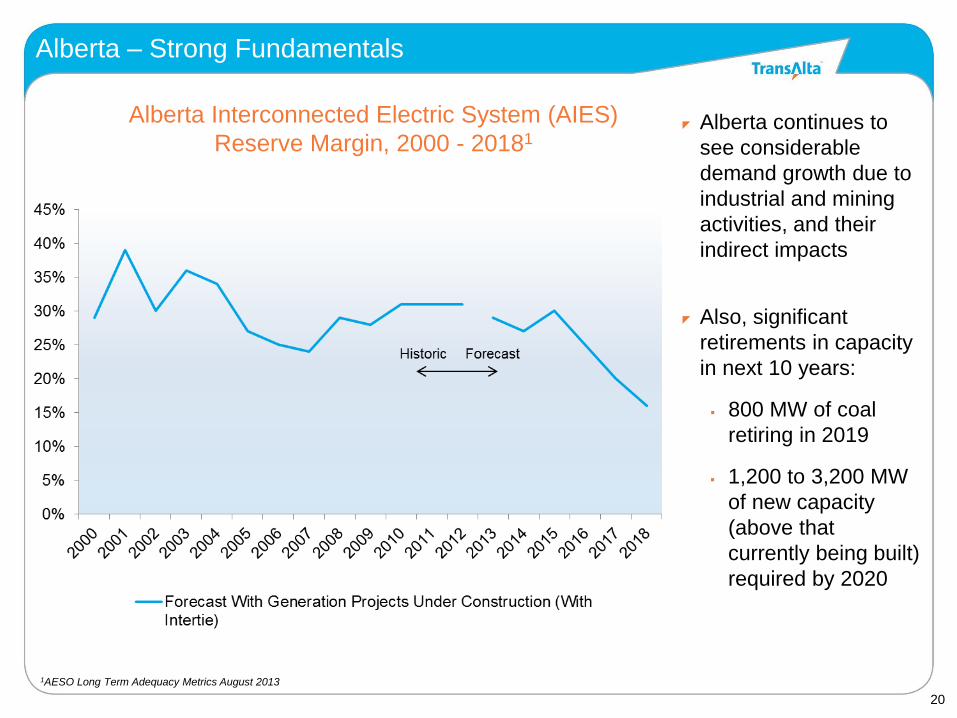

Alberta Interconnected Electric System (AIES)

Reserve Margin, 2000 - 20181

1AESO Long Term Adequacy Metrics August 2013

Alberta continues to

see considerable

demand growth due to

industrial and mining

activities, and their

indirect impacts

Also, significant

retirements in capacity

in next 10 years:

800 MW of coal

retiring in 2019

1,200 to 3,200 MW

of new capacity

(above that

currently being built)

required by 2020

Alberta – Strong Fundamentals

21

Since deregulation, AB Pool prices have averaged $65 / MWh

Source: AESO

Historical Power Prices in Alberta

22

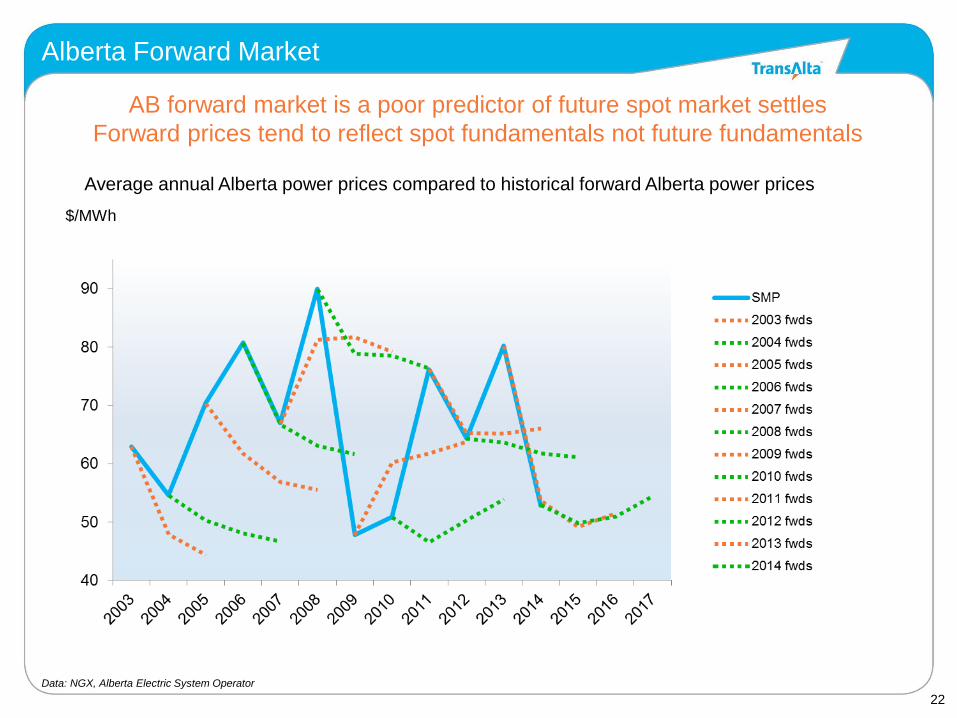

Data: NGX, Alberta Electric System Operator

AB forward market is a poor predictor of future spot market settles

Forward prices tend to reflect spot fundamentals not future fundamentals

$/MWh

Average annual Alberta power prices compared to historical forward Alberta power prices

Alberta Forward Market

23

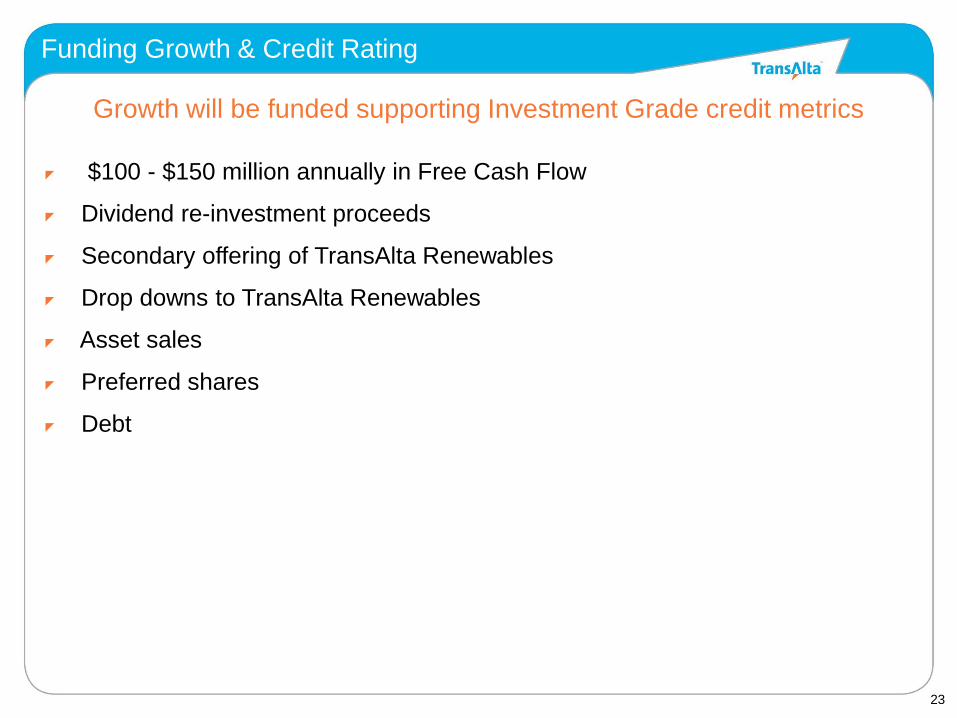

Funding Growth & Credit Rating

$100 - $150 million annually in Free Cash Flow

Dividend re-investment proceeds

Secondary offering of TransAlta Renewables

Drop downs to TransAlta Renewables

Asset sales

Preferred shares

Debt

Growth will be funded supporting Investment Grade credit metrics

24

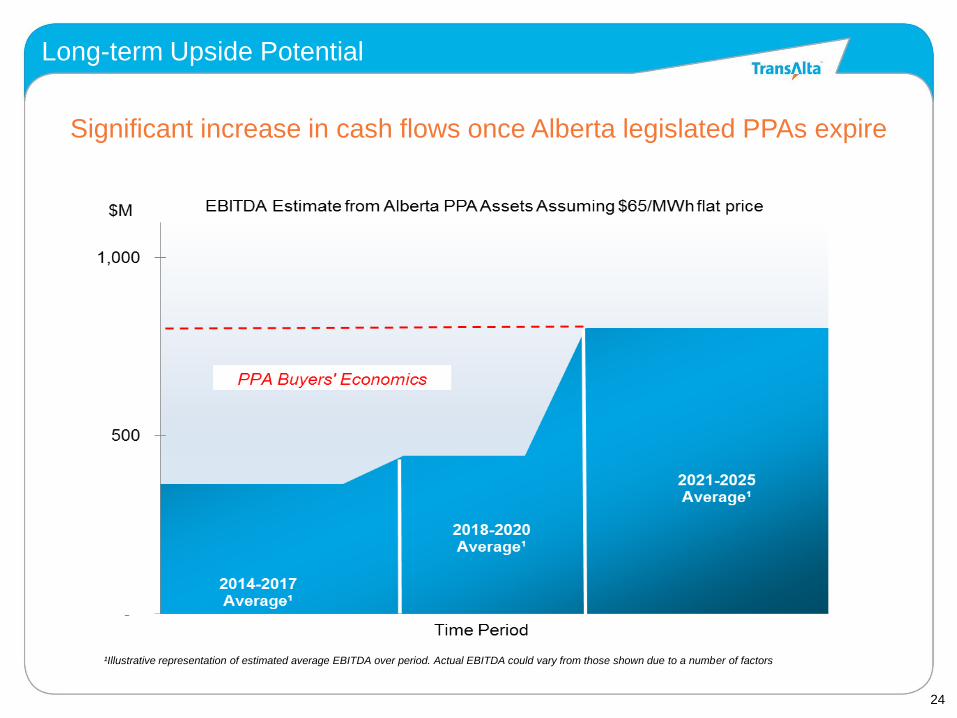

Long-term Upside Potential

Significant increase in cash flows once Alberta legislated PPAs expire

¹Illustrative representation of estimated average EBITDA over period. Actual EBITDA could vary from those shown due to a number of factors

25

Focused on Creating Value

Integrated approach to driving long-term shareholder value

Diversified and highly contracted portfolio

Attractive and sustainable dividend

Strong balance sheet and free cash flow

Well positioned for growth in markets with strong fundamentals

Significant upside post-PPA

Related Documents