Journal of Applied Economics Volume XIII, Number 1, May 2010 XIII Edited by the Universidad del CEMA Print ISSN 1514-0326 Online ISSN 1667-6726 Hakan Berument Afsin Sahin Seasonality in inflation volatility: Evidence from Turkey

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Journal ofAppliedEconomics

Volume XIII, Number 1, May 2010XIII

Edited by the Universidad del CEMA Print ISSN 1514-0326Online ISSN 1667-6726

Hakan BerumentAfsin Sahin

Seasonality in inflation volatility: Evidence from Turkey

Journal of Applied Economics. Vol XIII, No. 1 (May 2010), 39-65

SEASONALITY IN INFLATION VOLATILITY: EVIDENCE FROM TURKEY

M. Hakan Berument*Bilkent University

Afsin SahinGazi University

Submitted May 2008; accepted July 2009

This paper assesses the presence of seasonal volatility in price indexes where a similar typeof pattern has been reported in asset prices in financial markets. The empirical evidence fromTurkey for the monthly period from 1987:01 to 2007:05 suggests the presence of seasonalityin the conditional variance of inflation. Thus, inferences for the models that do not accountfor the seasonality in the conditional variance will be misleading.

JEL classification codes: E31; E37, E30.Key words: inflation volatility, seasonality, EGARCH.

I. Introduction

Economists are interested not only in the level of inflation but in its volatility

because the latter also adversely affects economic performance.1 The purpose of

* M. Hakan Berument (corresponding author): Department of Economics, Bilkent University, 06800Ankara, Turkey; phone: +90 312 2902342, fax: +90 312 2665140, e-mail: [email protected],URL: http://www.bilkent.edu.tr/~berument. Afsin Sahin: School of Banking and Insurance, GaziUniversity, 06500 Ankara, Turkey; phone: +90 312 582 1100; fax +90 312 221 3202; email:[email protected]. URL: http://afsinsahin.googlepages.com. We would like to thank two anonymousreferees and Rana Nelson for their helpful comments.

1 Hafer (1986) and Holland (1986) report the negative effects of inflation volatility on employment.Friedman (1977), Froyen and Waud (1987) and Holland (1988) argue that there is a negative relationshipbetween output and inflation volatility. Wilson (2006) suggests that increased inflation volatility isassociated with higher average inflation and lower average growth. Berument and Guner (1997), Berument(1999) and Berument and Malatyali (2001) find a positive relationship between inflation volatility andinterest rates.

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 39

this paper is to assess whether there is any regularity in inflation volatility. To be

specific, we will assess whether there is any seasonal pattern in the conditional

inflation variability series by considering seasonally unadjusted as well as seasonally

adjusted monthly data.2 Understanding any seasonal pattern in inflation volatility

is important. First, more efficient estimates of inflation forecasts will be gathered

by better modeling conditional inflation variances. Second, if seasonal patterns

exist using seasonally adjusted data, one may need to develop a new set of

algorithms that addresses the seasonality in volatility. Third, since inflation

volatility explains the behaviors of other macroeconomic variables, addressing

the seasonality of inflation volatility may help to better capture the effects of

inflation volatility on those variables.

There are a limited number of studies that analyze the determinants of inflation

volatility. Bowdler and Malik (2005) provide evidence that openness reduces

inflation volatility. Smith (1999) and Engel and Rogers (2001) argue that exchange

rate volatility explains part of price volatility, and Ghosh et al. (1996) claim that

pegged exchange rates are associated with significantly lower variability. Similarly,

Bleaney and Fielding (2002) find that countries that peg exchange rates have

lower inflation volatilities than floating-rate countries. According to Rother (2004),

activist fiscal policies may have an important impact on inflation volatility, and

volatility in discretionary fiscal policies increases inflation volatility. Aisen and

Veiga (2008) argue that higher degrees of political instability, ideological polarization

and political fragmentation are associated with higher inflation volatility. Dittmar

et al. (1999), Gavin (2003) and Berument and Yuksel (2007) discuss the effect of

inflation targeting regimes; Grier and Perry (1998), Kontonikas (2004), and

Berument and Dincer (2005) point out the effect of inflation on inflation volatility.

All these studies analyze the effect of economic and political variables on inflation

volatility. The aim of this paper is to model inflation volatility by considering

seasonal patterns of the general Consumer Price Index (CPI) inflation and its sub-

components.

This paper provides evidence regarding the seasonal pattern of Turkish inflation

volatilities for the period from January 1987 to May 2007. Although most prices

are set monthly in Turkey, price changes make their biggest adjustment once a year

–at the beginning of the year or when a new set of products enters the market. For

some products, prices are generally set to include the expected inflation for the year,

Journal of Applied Economics40

2 Similar analyses have been performed on stock market volatilities since the mid-1980s. See, forexample, French and Roll (1986), and Savva, Osborn and Gill (2006).

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 40

according to the government’s prediction, such as refrigerators, health services.3

The credibility of the government’s policies is assessed with the announced targets

when the budget details are released at the beginning of the fiscal year. Thus, one

may expect that volatility reaches its peak at the beginning of the fiscal year –

January. Thus, it is expected that for most products and for the general CPI, January

has the highest volatility. For some other products, prices are quite seasonal, such

as those for food, or prices are set mostly by the rest of the world, such as those for

automobiles.4 However, for agriculture, new seasonal products enter the market

around April and May, and for automobiles, around July and August. Thus, one

may expect that food and transportation volatilities peak around April-May and

July-August, respectively. In regulated sectors such as health and housing, volatility

is at its minimum just after a month after the price increases made because most

adjustments for the year are made in the previous month or towards the end of the

fiscal year when firms are close to finalizing their balance sheets.

The paper is organized as follows: Section II introduces and elaborates on the

data. Section III introduces the model employed in the paper. Section IV reports

the empirical evidence, while Section V provides a set of extensions of our models

as robustness tests. The last section concludes the paper.

II. Data Characteristics

We gathered data from the Turkish Statistical Institute (TurkStat) covering monthly

periods from January 1987 to May 2007. We examine the Consumer Price Index

and its seven components to determine if there is any seasonality in the conditional

variances for these series. The indexes that we consider are: Consumer Price Index

(CPI), Group Index of Clothing (Clothing), Group Index of Culture, Training and

Entertainment (Culture), Group Index of Food-Stuffs (Food), Group Index of Home

Appliances and Furniture (Furniture), Group Index of Medical Health and Personal

Care (Health), Group Index of Housing (Housing) and Group Index of Transportation

and Communication (Transportation). Figure 1 reports the graphs of the variables.

Seasonality in Inflation Volatility: Evidence from Turkey 41

3 Government plays a big role in Turkey both in its share in the economy and its regulatory power. Forexample, Nevzat Saygilioglu (a former acting Treasury under-minister) argued that the share of thegovernment sector to total income reached was around 70% at a particular point in the sample we consider(see Aydogdu and Yonezer 2007, pp. 387-397).

4 The Turkish domestic automobile industry is integrated with the rest of the world. Moreover, a sizeableportion of automobile sales are of imports; the share of imports to consumption is 66% for 2007 (seeAutomobile Manufacturers Associations 2008).

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 41

Table 1 reports various diagnostic tests. Panels A, B and C report the unit root

tests of the price indexes that we consider in their logarithmic form, with a constant

(Panel A), with a constant and time trend (Panel B) and a constant in logarithmic

first differences (Panel C). Each panel reports unit root tests for seasonally unadjusted

Journal of Applied Economics42

Figure 1. Graphs of observed data series (logarithmic, monthly change, seasonally unadjusted)

CPI Clothing

Culture Food

Furniture Health

Housing Transportation

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 42

Seasonality in Inflation Volatility: Evidence from Turkey 43Ta

ble

1. P

relim

inar

y di

agno

stic

test

s

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

Pane

l A. U

nit r

oot w

ith lo

g le

vels

and

con

stan

t

A1. S

easo

nally

una

djus

ted

DF-0

.796

0-0

.788

8-0

.913

3-0

.204

30.

7974

-0.4

415

-1.4

335

0.48

81

ADF

-1.9

599

-1.7

796

-2.0

432

-2.2

506

-2.4

737

-1.6

244

-1.9

028

-2.4

117

PP-1

.827

3-1

.753

2-1

.757

4-2

.502

2-1

.424

9-1

.950

5-1

.482

5-1

.491

3

KPSS

2.01

6***

2.00

4***

2.01

1***

2.01

3***

2.00

9***

2.01

2***

2.02

2***

2.01

6***

A2. S

easo

nally

adj

uste

d

DF-0

.699

20.

3205

0.81

37-0

.121

60.

8022

0.25

45-0

.563

80.

152

ADF

-2.2

34-1

.805

5-2

.075

8-2

.423

1-2

.466

7-2

.478

2-2

.353

8-2

.547

7

PP-2

.037

5-2

.279

8-1

.599

3-1

.621

-1.5

772

-1.6

14-1

.780

8-1

.531

8

KPSS

2.01

6***

2.00

4***

2.01

1***

2.01

3***

2.00

9***

2.01

2***

2.02

2***

2.01

6***

Pane

l B. U

nit r

oot t

ests

with

log

leve

ls, c

onst

ant a

nd tr

end

B1. S

easo

nally

una

djus

ted

DF-1

.448

8-1

.923

3-1

.223

3-0

.841

5-0

.123

3-1

.075

3-2

.347

70.

8917

ADF

3.05

11-0

.852

90.

3526

2.12

472.

8131

3.64

35-0

.922

31.

7452

PP2.

7186

1.27

492.

536

2.06

952.

4438

2.95

632.

8143

2.58

41

KPSS

0.44

3***

0.44

2***

0.44

7***

0.45

5***

0.43

4***

0.44

0***

0.41

91**

*0.

4367

***

B2. S

easo

nally

adj

uste

d

DF-0

.203

8-0

.913

50.

5845

0.13

08-0

.189

6-0

.125

7-0

.931

30.

9809

ADF

3.13

450.

4079

2.51

932.

3901

2.48

841.

8037

0.53

121.

8603

PP2.

9457

3.01

073.

3137

3.27

912.

3762

2.33

52.

6934

2.55

23

KPSS

0.44

33**

*0.

4418

***

0.44

73**

*0.

4558

***

0.43

50**

*0.

4406

***

0.41

91**

*0.

4368

***

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 43

Journal of Applied Economics44Ta

ble

1 (c

ontin

ued)

. Pre

limin

ary

diag

nost

ic te

sts

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

Pane

l C. U

nit r

oot t

ests

with

log

diffe

renc

es a

nd c

onst

ant

C1. S

easo

nally

una

djus

ted

DF-3

.142

2***

-2.7

039**

*-4

.563

8***

-3.7

773**

*-2

.851

9***

-2.7

378**

*-1

.876

9*-4

.181

6***

ADF

-3.1

331**

-4.1

11**

*-5

.503

2***

-4.8

523**

*-5

.652

1***

-3.8

260**

*-2

.795

4*-5

.452

9***

PP-8

.381

***

-8.7

01**

*-1

1.65

2***

-9.4

93**

*-9

.476

***

-11.

973**

*-8

.526

***

-11.

100**

*

KPSS

1.36

95**

*1.

1209

***

1.50

75**

*1.

7136

***

1.27

41**

*1.

6158

***

1.07

27**

*1.

6618

***

C2. S

easo

nally

adj

uste

d

DF-2

.420

6**-3

.126

0***

-3.5

682**

*-2

.454

6**-2

.075

5**-2

.073

9**-1

.917

9*-1

0.75

47**

*

ADF

-3.3

251**

-2.8

687*

-4.6

410**

*-3

.493

1***

-3.1

997**

-3.5

581**

*-2

.757

0*-1

0.79

00**

*

PP-6

.169

1***

-5.4

852**

*-1

2.89

8***

-8.7

284**

*-7

.208

8***

-11.

504**

*-5

.637

9***

-10.

790**

*

KPSS

1.36

95**

*1.

2637

***

1.33

81**

*1.

4085

***

1.27

98**

*1.

4221

***

1.08

55**

*1.

6737

***

Pane

l D. L

jung

-Box

Q te

st s

tatis

tics

D1. S

easo

nally

una

djus

ted

6[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

12[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

24[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

36[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

D2. S

easo

nally

adj

uste

d

6[0

.187

1][0

.000

8][0

.727

2][0

.646

9][0

.005

4][0

.148

6][0

.019

9][0

.936

4]

12[0

.409

9][0

.005

4][0

.381

0][0

.611

2][0

.064

4][0

.184

0][0

.148

6][0

.989

8]

24[0

.156

4][0

.171

5][0

.588

8][0

.428

6][0

.557

0][0

.281

8][0

.719

4][0

.883

4]

36[0

.594

1][0

.109

8][0

.037

4][0

.323

3][0

.690

0][0

.073

4][0

.661

1][0

.259

6]

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 44

Seasonality in Inflation Volatility: Evidence from Turkey 45Ta

ble

1 (c

ontin

ued)

. Pre

limin

ary

diag

nost

ic te

sts

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

Pane

l E. A

RCH-

LM te

st s

tatis

tics

E1. S

easo

nally

una

djus

ted

6[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

12[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

24[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

36[0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0][0

.000

0]

E2. S

easo

nally

adj

uste

d

6[0

.013

1][0

.025

9][0

.352

9][0

.129

4][0

.013

5][0

.403

6][0

.044

2][0

.825

1]

12[0

.022

2][0

.125

2][0

.000

2][0

.012

3][0

.038

1][0

.215

4][0

.089

3][0

.986

9]

24[0

.206

6][0

.382

2][0

.001

2][0

.036

9][0

.448

9][0

.112

3][0

.555

6][0

.841

3]

36[0

.195

8][0

.766

8][0

.001

8][0

.192

4][0

.666

2][0

.036

5][0

.976

7][0

.282

6]

Note

: p-v

alue

s ar

e re

porte

d in

bra

cket

s. **

* , **an

d *

indi

cate

reje

ctio

n of

the

null

at th

e 0.

01%

, 0.0

5% a

nd 0

.10%

leve

ls, r

espe

ctive

ly.

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 45

and adjusted series.5 We consider four unit root tests: Dickey-Fuller (DF), Augmented

Dickey-Fuller (ADF), Phillips-Perron (PP) and Kwiatkowski, Phillips, Schmidt and

Shin (KPSS). For DF, ADF and PP, the null hypothesis is unit root (rejecting the

null suggests stationarity) and for KPSS, the null is stationarity (rejecting the null

suggest non-stationarity). Panels A, B and C overall suggest that the series that we

consider have a unit root in log levels, but the differenced series do not have a unit

root. Thus, we carried our analyses for the indexes in their logarithmic first differences.

Panel D of Table 1 reports the p-values of Ljung-Box Q test statistics for 6, 12,

24 and 36 lags of the series in their logarithmic first differences. Panel E of Table

1 reports the ARCH-LM tests of the same series for 6, 12, 24 and 36 lags. We reject

the null of no autocorrelation for the non-seasonally adjusted data, but no general

pattern appears for the presence of autocorrelation for the seasonally adjusted data.

However, the strong contrast between Panels D1 (for the seasonally unadjusted

series) and D2 (for the seasonally adjusted series) suggests a strong presence of

seasonality in the mean equation of the seasonally unadjusted series.

Panel E of Table 1 reports the ARCH-LM test statistics.6 The null hypothesis

that there is no ARCH effect up to order q in the residuals fails to be rejected when

we employ seasonally unadjusted data for all the lag orders that we consider. When

we employ seasonally adjusted data, the null is rejected at the 5% for at least one

lag order that we consider but Transportation; for Transportation we cannot reject

the null for any of the lag orders that we consider. Thus, inflation volatility needs

to be modeled somehow.

Table 2 reports the descriptive statistics for the general CPI and its seven

components. Panel A reports the statistics when we used the original (seasonally

unadjusted) inflation data; Panel B uses the seasonally adjusted data. The means

of Housing, Health, Transportation and Food are higher than the CPI for both the

seasonally unadjusted and adjusted data and the means of Culture, Clothing and

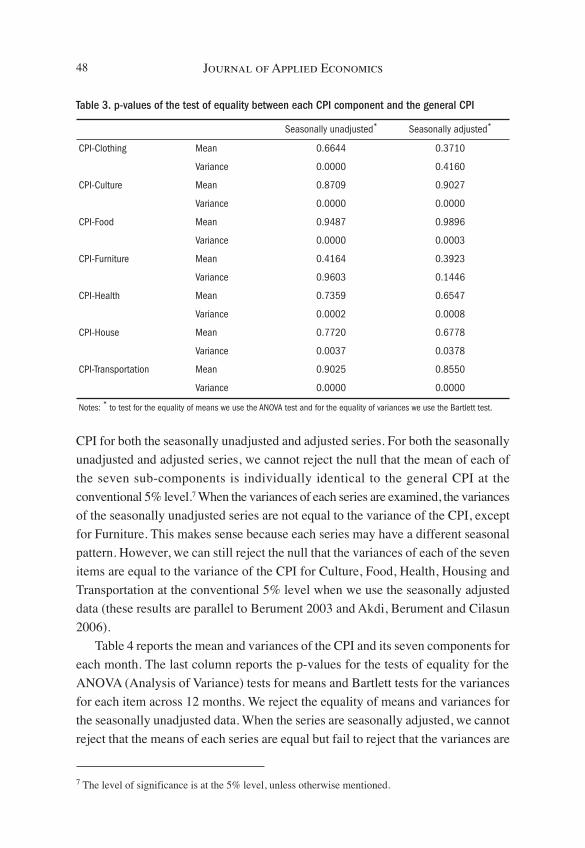

Furniture are less than the CPI. Table 3 reports the p-values for the test statistics:

the mean and variance of each item are equal to the mean and variance of the general

Journal of Applied Economics46

5 Although the price series that we consider have a high degree of seasonality, there is no officialseasonally adjusted data for Turkey. However, the Central Bank of the Republic of Turkey uses theCensus X11 (historical, additive) procedure to seasonally adjust series in its annual reports. Thus, weused the same procedure to seasonally adjust our series.

6 We specify the autoregressive equation with its q-lags (where q-lags are determined by the finalprediction error (FPE) criteria, whose properties we discuss later in the text) and a constant term. Whenwe used seasonally unadjusted data, 11 seasonal dummies are also included.

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 46

Seasonality in Inflation Volatility: Evidence from Turkey 47Ta

ble

2. D

escr

iptiv

e st

atis

tics

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

Pane

l A.

Seas

onal

ly u

nadj

uste

d un

ivaria

te d

ata

stat

istic

s

Mea

n3.

5597

3.38

863.

5057

3.57

883.

3641

3.65

33.

6237

3.59

81

Med

ian

3.28

242.

5739

2.30

533.

4895

3.16

992.

6023

3.48

972.

8982

Max

imum

22.0

7818

.107

23.5

9626

.53

18.1

0819

.038

13.2

2139

.027

Min

imum

-0.9

286

-8.8

068

-1.8

828

-5.0

766

-2.2

154

-0.9

337

0.20

74-1

.776

4

Varia

nce

6.72

7329

.309

18.8

1613

.625

6.68

3811

.004

4.58

3916

.087

Coef

f. of

var

.0.

7286

1.59

771.

2373

1.03

140.

7685

0.90

810.

5908

1.11

47

Skew

ness

1.76

070.

3869

2.22

941.

0114

1.56

071.

5261

0.83

673.

9839

Kurto

sis

12.7

642.

8059

8.43

498.

1013

9.86

425.

8259

4.24

2930

.093

Jarq

ue-B

era

1041

.56.

1515

477.

7229

1.12

549.

6516

7.25

42.0

0277

09.5

Sum

sq.

dev

.15

54.1

6770

.443

46.5

3147

1543

.925

41.8

1058

.937

15.9

Obse

rvat

ions

232

232

232

232

232

232

232

232

Pane

l B. S

easo

nally

adj

uste

d un

ivaria

te d

ata

stat

istic

s

Mea

n3.

5586

3.37

23.

529

3.56

163.

3761

3.66

123.

6376

3.61

13

Med

ian

3.83

153.

719

3.40

933.

4119

3.58

293.

3845

3.74

672.

9871

Max

imum

20.6

4612

.235

16.1

0124

.955

17.3

1917

.733

14.2

9337

.787

Min

imum

0.09

89-4

.038

2-5

.296

4-2

.063

-1.8

975

-1.5

033

0.02

31-1

.908

8

Varia

nce

4.76

465.

3033

8.77

527.

6706

5.77

487.

4327

3.62

2514

.512

Coef

f. of

var

.0.

6134

0.68

30.

8394

0.77

760.

7118

0.74

470.

5232

1.05

49

Skew

ness

2.05

67-0

.020

60.

9378

2.16

551.

4753

1.27

290.

7218

4.07

75

Kurto

sis

17.8

784.

4885

6.40

1317

.065

10.5

676.

4475

5.84

231

.876

Jarq

ue-B

era

2303

.221

.435

145.

8420

93.5

637.

7217

7.54

98.2

2187

03.4

Sum

sq.

dev

.11

00.6

1225

.120

27.1

1771

.913

34.1

1717

.183

6.8

3352

.4

Obse

rvat

ions

232

232

232

232

232

232

232

232

Note

: Coe

ffici

ent o

f var

iatio

n is

def

ined

as

(std

. dev

/mea

n).

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 47

CPI for both the seasonally unadjusted and adjusted series. For both the seasonally

unadjusted and adjusted series, we cannot reject the null that the mean of each of

the seven sub-components is individually identical to the general CPI at the

conventional 5% level.7 When the variances of each series are examined, the variances

of the seasonally unadjusted series are not equal to the variance of the CPI, except

for Furniture. This makes sense because each series may have a different seasonal

pattern. However, we can still reject the null that the variances of each of the seven

items are equal to the variance of the CPI for Culture, Food, Health, Housing and

Transportation at the conventional 5% level when we use the seasonally adjusted

data (these results are parallel to Berument 2003 and Akdi, Berument and Cilasun

2006).

Table 4 reports the mean and variances of the CPI and its seven components for

each month. The last column reports the p-values for the tests of equality for the

ANOVA (Analysis of Variance) tests for means and Bartlett tests for the variances

for each item across 12 months. We reject the equality of means and variances for

the seasonally unadjusted data. When the series are seasonally adjusted, we cannot

reject that the means of each series are equal but fail to reject that the variances are

Journal of Applied Economics48

7 The level of significance is at the 5% level, unless otherwise mentioned.

Table 3. p-values of the test of equality between each CPI component and the general CPI

Seasonally unadjusted* Seasonally adjusted*

CPI-Clothing Mean 0.6644 0.3710

Variance 0.0000 0.4160

CPI-Culture Mean 0.8709 0.9027

Variance 0.0000 0.0000

CPI-Food Mean 0.9487 0.9896

Variance 0.0000 0.0003

CPI-Furniture Mean 0.4164 0.3923

Variance 0.9603 0.1446

CPI-Health Mean 0.7359 0.6547

Variance 0.0002 0.0008

CPI-House Mean 0.7720 0.6778

Variance 0.0037 0.0378

CPI-Transportation Mean 0.9025 0.8550

Variance 0.0000 0.0000

Notes: * to test for the equality of means we use the ANOVA test and for the equality of variances we use the Bartlett test.

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 48

Seasonality in Inflation Volatility: Evidence from Turkey 49Ta

ble

4. Te

st o

f equ

ality

acr

oss

each

mon

th o

f the

yea

r for

diff

eren

t pric

e in

dexe

s

Jan.

Feb.

Mar

.Ap

r.M

ayJu

n.Ju

l.Au

g.Se

p.Oc

t.No

v.De

c.Te

st o

f equ

ality

*

CPI

Mea

n (N

SA)

4.20

003.

2718

3.44

115.

3458

2.99

961.

3776

1.80

272.

6384

5.11

825.

4975

4.24

902.

7234

0.00

Varia

nce

(NSA

)6.

0187

3.75

863.

3244

21.7

590

4.29

061.

0333

2.64

962.

5773

5.54

516.

0239

3.31

902.

8045

0.00

Mea

n(SA

)3.

6360

3.41

723.

3360

4.27

523.

4695

3.37

413.

5295

3.46

613.

6351

3.47

093.

4843

3.59

490.

99

Varia

nce

(SA)

4.35

823.

0260

2.93

4019

.545

05.

1658

2.34

143.

9187

2.98

423.

9786

3.70

293.

0673

3.68

830.

00

Clot

hing

Mea

n (N

SA)

-2.1

504

-2.5

737

1.28

4810

.369

07.

1558

2.68

38-1

.370

1-1

.225

46.

1456

11.8

430

6.60

611.

7536

0.00

Varia

nce

(NSA

)7.

4792

5.98

686.

1892

9.05

875.

7122

0.95

807.

5411

5.01

367.

4604

14.6

030

10.5

580

3.25

860.

00

Mea

n(SA

)2.

9827

3.36

913.

4002

3.53

563.

7706

3.13

653.

4578

2.91

263.

7007

3.62

643.

4353

3.10

570.

99

Varia

nce

(SA)

5.42

003.

9198

4.38

5811

.604

05.

2767

2.82

064.

8468

5.17

896.

0144

6.12

086.

3948

3.76

290.

29

Cultu

re

Mea

n (N

SA)

4.56

132.

3393

2.19

082.

7409

2.24

661.

3944

2.32

817.

1181

10.9

540

3.05

651.

4674

1.90

920.

00

Varia

nce

(NSA

)12

.195

05.

0940

4.31

3713

.273

06.

1425

0.96

574.

6484

37.7

840

51.1

020

6.36

352.

5135

2.66

320.

00

Mea

n(SA

)3.

5384

3.35

713.

3191

3.98

743.

2921

3.49

573.

4912

5.12

082.

2407

3.75

353.

3234

3.43

730.

52

Varia

nce

(SA)

6.06

223.

8257

3.80

1613

.204

08.

1052

1.86

044.

7580

27.7

340

20.9

830

7.67

214.

5979

3.49

190.

00

Food

Mea

n (N

SA)

4.90

325.

3741

4.94

165.

6553

1.70

61-1

.148

90.

3015

1.97

734.

7980

5.99

435.

2477

3.01

780.

00

Varia

nce

(NSA

)6.

7521

8.38

816.

9163

35.9

600

7.97

842.

2885

6.08

146.

0152

6.08

669.

3748

4.84

316.

0608

0.00

Mea

n(SA

)3.

6379

3.31

473.

1368

4.42

363.

3536

3.46

923.

8705

3.39

023.

4984

3.57

153.

4422

3.63

170.

99

Varia

nce

(SA)

6.22

884.

2521

5.70

3730

.648

08.

6871

3.44

177.

8488

6.56

614.

2922

5.86

424.

4939

6.36

560.

00

jaeXIII_1:jaeXIII_1 5/11/10 9:20 PM Página 49

Journal of Applied Economics50Ta

ble

4 (c

ontin

ued)

. Tes

t of e

qual

ity a

cros

s ea

ch m

onth

of t

he y

ear f

or d

iffer

ent p

rice

inde

xes

Jan.

Feb.

Mar

.Ap

r.M

ayJu

n.Ju

l.Au

g.Se

p.Oc

t.No

v.De

c.Te

st o

f equ

ality

*

Furn

iture

Mea

n (N

SA)

5.20

162.

7502

2.93

103.

9806

3.74

182.

8023

3.31

562.

8943

4.10

503.

1210

2.91

472.

6140

0.07

Varia

nce

(NSA

)10

.516

04.

7781

4.58

8418

.637

013

.224

02.

5668

2.98

862.

9183

5.64

274.

2244

2.91

483.

6943

0.00

Mea

n(SA

)3.

4213

3.53

133.

1039

3.78

143.

6760

3.37

062.

9696

3.24

543.

4004

3.44

083.

3293

3.21

190.

99

Varia

nce

(SA)

5.81

176.

3183

2.99

8017

.206

012

.199

03.

8097

2.89

543.

7209

4.95

613.

7567

3.99

593.

6693

0.00

Heal

th

Mea

n (N

SA)

7.78

234.

6732

3.79

733.

8286

2.71

893.

1433

4.74

303.

3855

2.58

152.

1725

2.88

372.

1045

0.00

Varia

nce

(NSA

)22

.700

010

.275

07.

2182

18.3

360

8.17

517.

5612

13.1

840

4.29

174.

0879

2.91

916.

4727

5.07

950.

00

Mea

n(SA

)4.

0809

3.82

783.

3843

3.78

613.

8349

3.52

753.

6853

3.43

343.

5116

3.42

093.

6571

3.77

440.

99

Varia

nce

(SA)

12.5

750

8.44

757.

8395

15.6

000

8.81

015.

3113

8.20

973.

6593

4.52

763.

0364

7.15

967.

4277

0.03

Hous

ing

Mea

n (N

SA)

5.47

253.

2884

2.60

283.

2967

2.78

733.

1579

3.89

804.

1606

4.88

743.

9334

3.26

402.

8685

0.00

Varia

nce

(NSA

)9.

6567

3.30

452.

5935

8.84

632.

6843

2.07

123.

0808

3.79

964.

9050

3.36

992.

3308

2.28

940.

00

Mea

n(SA

)3.

4637

3.42

743.

5104

4.09

023.

5033

3.62

793.

6470

3.70

273.

8684

3.53

923.

6428

3.62

940.

99

Varia

nce

(SA)

4.02

552.

7438

3.24

619.

4232

2.87

532.

6115

2.74

833.

3001

5.06

963.

0984

2.77

283.

1404

0.11

Trans

porta

tion

Mea

n (N

SA)

5.52

932.

7648

2.85

255.

5041

3.03

413.

3619

4.59

023.

3837

4.15

042.

4856

2.06

663.

4665

0.11

Varia

nce

(NSA

)24

.649

05.

0216

4.00

8573

.968

04.

5966

8.32

4216

.643

07.

9424

24.3

000

4.74

642.

3389

10.0

520

0.00

Mea

n(SA

)4.

6285

3.12

753.

3552

5.20

073.

2463

3.22

713.

3225

3.21

384.

1544

3.31

003.

1728

3.35

090.

82

Varia

nce

(SA)

23.3

320

4.05

164.

6444

69.6

870

4.65

947.

8631

15.9

170

6.76

0722

.879

05.

2835

3.48

357.

5971

0.00

Note

s: *

test

of e

qual

ity re

ports

the

p-va

lues

of A

NOVA

and

Bar

tlett

test

s fo

r the

mea

n an

d va

rianc

es o

f ser

ies,

resp

ectiv

ely.

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 50

the same for all but Clothing and Housing. Therefore, these three tables suggest

that even if we account for seasonality, the volatility of each series from the general

CPI and the volatility of each series from each other are different. When we consider

the seasonally unadjusted and seasonally adjusted series, Table 4 also suggests that

the lowest variances are observed in June for the general CPI, Culture, Food and

Housing; in October for Health; in November for Transportation; in June and

December for Clothing. On the other hand, the highest variances are observed in

April for the general CPI; October, November and April for Clothing; August and

September for Culture; April for Food; April and May for Furniture; January and

April for Health; January, April and September for Housing; January and April for

Transportation. These highest and lowest volatilities do not take into account the

dynamics of the economy and assume that positive and negative inflation shocks

affect volatility in the same way. In the next section, we will employ Nelson’s (1991)

Exponential Generalized ARCH model to assess any regularity in the conditional

variances of inflation series.

III. Method

The economic literature suggests various methods for measuring inflation volatility,

either through direct measures of volatility, by using survey data, or through indirect

measures of volatility, usually by using sophisticated econometric techniques.

Bomberger (1996) argues that using dispersion of the survey data measures

disagreement rather than inflation volatility. Moreover, he argues that some forecasters

may not want to deviate from other forecasters’ estimates, so the value of expected

inflation may be biased.

The Kalman filtering and ARCH types of conditional variance modeling are the

two most common sophisticated econometric techniques researchers employ to

measure inflation volatility indirectly. The Kalman filter is a discrete, recursive

linear filter that measures instability of the structural variability of the parameters

of an equation. ARCH-type models assume that the parameters of the model are

stable but estimate the variance of the residual term for the inflation specification.

Evans (1991) and Berument et al. (2005) argue that the ARCH class of models is

a better way of measuring risk/uncertainty, whereas the Kalman filter is better for

capturing model (or parameter) instability. Therefore, we model volatility employing

ARCH/GARCH models.

The conventional ARCH models are not capable of capturing the asymmetric

effects of negative or positive inflation surprises on the volatility specification

Seasonality in Inflation Volatility: Evidence from Turkey 51

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 51

(Black 1976, Engle and Ng 1993). In order to account for this, we use the EGARCH

specification. The contribution of this paper is to assess whether there is any regularity

in the volatility of price indexes that is beyond the dynamics of the volatility captured

by the lagged conditional variance and the innovation of inflation.

Following Berument (1999 and 2003), we model inflation using lagged inflation

and monthly seasonal dummies to account for seasonality. Whether seasonality is

significantly related to volatility can be tested by examining the statistical significance

of the estimates of each month’s coefficients. The model allows for both autoregressive

and moving average components in the heteroskedastic variance.

Equations (1) and (2) give the mean and variance specifications, respectively.

The mean equation is specified as:

(1)

where πt is the inflation rate. Mit is for the monthly dummies accounting for monthly

seasonality, wherein i = 1, 2, 3, 4, 5, 7, 8, 9, 10, 11, 12. D94t is the dummy variable

that takes the value of 1 for the fourth month of 1994 to account for the 1994 financial

crisis, and takes the value of zero otherwise. εt is the error term at time t. To avoid

the dummy variable trap, M6t (which represents the dummy variable for June) is

not included in the specification of the conditional mean inflation. Following Hansen

and Juselius (1995), we also include 13 lag values of inflation and later in the study

we also consider alternative lag structures. Following Nelson (1991), we also assume

that εt has General Error Distribution with mean zero and variance (ht2). Lastly,

following Bollerslev and Woolridge (1992), we use the Quasi-Maximum Likelihood

method to estimate the parameters.

The EGARCH representation of the conditional variance of inflation at time t

is given by equation (2) as:8

(2)

Here, |εt-1/ht-1| represents the absolute value of the lagged residual over the

conditional standard deviation at time t – 1, (εt-1/ht-1) represents the lagged residual

over the conditional standard deviation and log(h2t-1) represents the logarithm of the

conditional variance at time t – 1.

log ht i iti

i iti

tM M20

1

5

7

12

1 1( ) = + ∑ + +∑= =

−β ψ ψ β ε / hh ht t t th− − − −+ +( ) ( )1 2 1 1 3 12β ε β/ .log

π π θ θ λ αt i iti

i iti

t ii

M M D= + ∑ + ∑ + + ∑= = =

01

5

7

12

1

13

94 ππ εt i t− + ,

Journal of Applied Economics52

8 See Berument et al. (2002) for the advantages of the EGARCH presentation of the conditional varianceover other types of ARCH specifications for Turkey.

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 52

In Equation (2), several meaningful restrictions can be tested. |β3| < 1 implies

that inflation volatility is not explosive. If β2 > 0, then a positive shock to inflation

increases volatility more than a negative shock. If β2 < 0, a positive shock generates

less volatility than a negative shock.

IV. Empirical Evidence

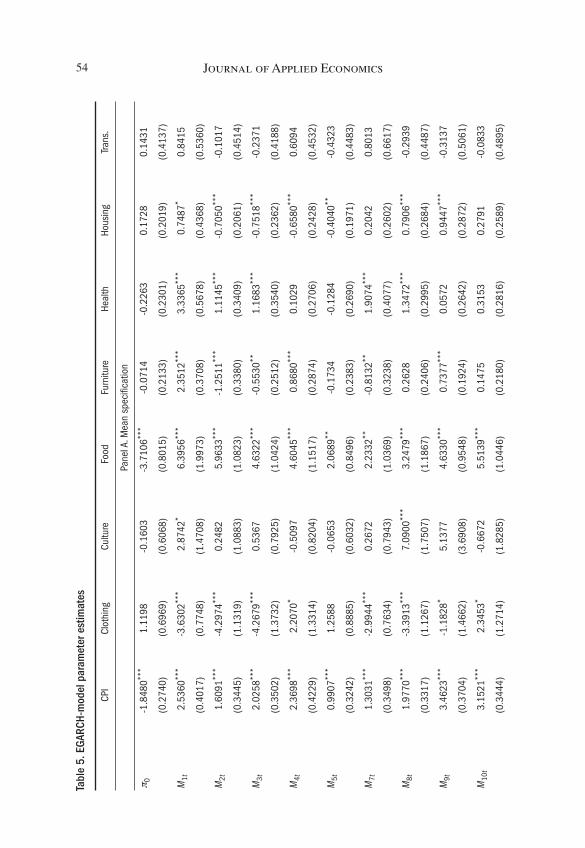

Table 5 reports the estimates of Equations (1) and (2) for the general CPI and its

seven sub-components by using seasonally unadjusted data. Panel A reports the

estimates of the inflation equation (Equation 1) and Panel B reports the estimates

of the conditional variance equation (Equation 2). Panel C reports two diagnostic

test (Ljung-Box-Q and ARCH-LM) statistics for the standardized residuals by using

various lag orders and Panel D is for summary statistics. Variables M1t to M12t are

estimated coefficients for the monthly dummies.

Panel A of Table 5 suggests that the lowest monthly effects in the mean equation

are observed in June for the general CPI; in February for Clothing; in November

for Culture; in June for Food; in February for Furniture; in May for Health; in March

for Housing; and in November for Transportation. The highest monthly effects in

the mean equation are observed in October for the general CPI; in October for

Clothing; in August for Culture; in January for Food, Furniture and Health; in

September for Housing; in January for Transportation. These findings are parallel

with the results listed in Table 4. Here, we do not interpret the estimated coefficients

for the lag values of inflation but the characteristic roots of the polynomials are all

inside the unit circle; thus the series are considered as stationary.

Panel B of Table 5 suggests that for the general CPI the highest volatility is in

January; in September for Clothing; in August for Culture; in April for Food; in

January for Furniture, Health and Housing; in July for Transportation. The lowest

volatilities are observed in November for the general CPI; in June for Clothing; in

December for Culture; in November for Food and Furniture; in February for Health

and Housing; in November for Transportation. These findings are parallel to the

expectations stated in the introduction. For the general CPI and most other items

January is the month that conditional inflation variance is highest except for food

(April) and Transportation (July). The lowest volatilities are observed towards the

end of year except for Health (February) and Housing (February).

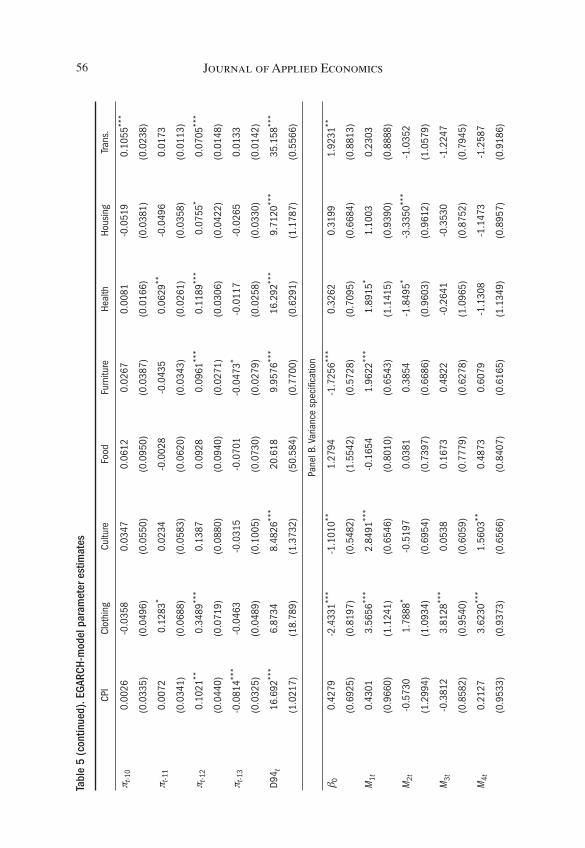

Next, we test whether the conditional variance is the same across each month.

In particular, we test the null hypothesis that the estimated coefficients for the eleven

monthly dummy coefficients are jointly zero for the conditional variance specification

Seasonality in Inflation Volatility: Evidence from Turkey 53

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 53

Journal of Applied Economics54Ta

ble

5. E

GARC

H-m

odel

par

amet

er e

stim

ates

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

Pane

l A. M

ean

spec

ifica

tion

π 0-1

.848

0***

1.11

98-0

.160

3-3

.710

6***

-0.0

714

-0.2

263

0.17

280.

1431

(0.2

740)

(0.6

969)

(0.6

068)

(0.8

015)

(0.2

133)

(0.2

301)

(0.2

019)

(0.4

137)

M1t

2.53

60**

*-3

.630

2***

2.87

42*

6.39

56**

*2.

3512

***

3.33

65**

*0.

7487

*0.

8415

(0.4

017)

(0.7

748)

(1.4

708)

(1.9

973)

(0.3

708)

(0.5

678)

(0.4

368)

(0.5

360)

M2t

1.60

91**

*-4

.297

4***

0.24

825.

9633

***

-1.2

511**

*1.

1145

***

-0.7

050**

*-0

.101

7

(0.3

445)

(1.1

319)

(1.0

883)

(1.0

823)

(0.3

380)

(0.3

409)

(0.2

061)

(0.4

514)

M3t

2.02

58**

*-4

.267

9***

0.53

674.

6322

***

-0.5

530**

1.16

83**

*-0

.751

8***

-0.2

371

(0.3

502)

(1.3

732)

(0.7

925)

(1.0

424)

(0.2

512)

(0.3

540)

(0.2

362)

(0.4

188)

M4t

2.36

98**

*2.

2070

*-0

.509

74.

6045

***

0.86

80**

*0.

1029

-0.6

580**

*0.

6094

(0.4

229)

(1.3

314)

(0.8

204)

(1.1

517)

(0.2

874)

(0.2

706)

(0.2

428)

(0.4

532)

M5t

0.99

07**

*1.

2588

-0.0

653

2.06

89**

-0.1

734

-0.1

284

-0.4

040**

-0.4

323

(0.3

242)

(0.8

885)

(0.6

032)

(0.8

496)

(0.2

383)

(0.2

690)

(0.1

971)

(0.4

483)

M7t

1.30

31**

*-2

.994

4***

0.26

722.

2332

**-0

.813

2**1.

9074

***

0.20

420.

8013

(0.3

498)

(0.7

634)

(0.7

943)

(1.0

369)

(0.3

238)

(0.4

077)

(0.2

602)

(0.6

617)

M8t

1.97

70**

*-3

.391

3***

7.09

00**

*3.

2479

***

0.26

281.

3472

***

0.79

06**

*-0

.293

9

(0.3

317)

(1.1

267)

(1.7

507)

(1.1

867)

(0.2

406)

(0.2

995)

(0.2

684)

(0.4

487)

M9t

3.46

23**

*-1

.182

8*5.

1377

4.63

30**

*0.

7377

***

0.05

720.

9447

***

-0.3

137

(0.3

704)

(1.4

662)

(3.6

908)

(0.9

548)

(0.1

924)

(0.2

642)

(0.2

872)

(0.5

061)

M10

t3.

1521

***

2.34

53*

-0.6

672

5.51

39**

*0.

1475

0.31

530.

2791

-0.0

833

(0.3

444)

(1.2

714)

(1.8

285)

(1.0

446)

(0.2

180)

(0.2

816)

(0.2

589)

(0.4

895)

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 54

Seasonality in Inflation Volatility: Evidence from Turkey 55Ta

ble

5 (c

ontin

ued)

. EGA

RCH-

mod

el p

aram

eter

est

imat

es

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

M11

t2.

0317

***

0.33

35-0

.904

65.

2943

***

-0.4

453*

0.27

62-0

.205

2-0

.752

6*

(0.2

993)

(0.9

054)

(0.9

818)

(0.9

921)

(0.2

455)

(0.2

736)

(0.2

392)

(0.4

316)

M12

t1.

5123

***

-0.0

571

0.43

643.

9950

***

-0.8

099**

*0.

0355

-0.5

819**

-0.0

724

(0.2

957)

(0.3

796)

(0.8

110)

(1.1

566)

(0.2

499)

(0.2

405)

(0.2

436)

(0.4

393)

π t-1

0.44

13**

*0.

2735

***

0.27

00**

0.37

34**

*0.

3073

***

0.16

12**

*0.

2897

***

0.23

77**

*

(0.0

334)

(0.0

525)

(0.1

116)

(0.0

767)

(0.0

509)

(0.0

310)

(0.0

290)

(0.0

334)

π t-2

0.06

74-0

.095

2*0.

1120

0.08

480.

3287

***

0.10

37**

*0.

0597

-0.0

028

(0.0

460)

(0.0

539)

(0.0

727)

(0.0

771)

(0.0

411)

(0.0

281)

(0.0

375)

(0.0

244)

π t-3

-0.0

694

0.04

110.

0652

-0.1

133

-0.0

208

0.06

67**

*0.

1260

***

-0.0

496**

(0.0

486)

(0.0

477)

(0.0

445)

(0.0

862)

(0.0

389)

(0.0

240)

(0.0

378)

(0.0

214)

π t-4

-0.0

039

0.05

15-0

.043

7-0

.033

50.

1484

***

0.10

87**

*0.

1042

***

0.06

99**

*

(0.0

337)

(0.0

566)

(0.0

500)

(0.0

719)

(0.0

339)

(0.0

197)

(0.0

347)

(0.0

196)

π t-5

0.13

40**

*0.

1083

*0.

0574

0.19

78**

0.02

330.

0044

0.10

25**

0.08

00**

*

(0.0

356)

(0.0

609)

(0.0

674)

(0.0

834)

(0.0

310)

(0.0

259)

(0.0

418)

(0.0

238)

π t-6

0.09

66**

*0.

1363

**0.

0484

0.11

030.

1476

***

-0.0

043

0.17

64**

*0.

0468

**

(0.0

326)

(0.0

641)

(0.0

552)

(0.0

713)

(0.0

361)

(0.0

276)

(0.0

435)

(0.0

235)

π t-7

0.05

01**

-0.0

565

-0.0

318

0.02

200.

0205

0.01

50-0

.066

10.

0257

**

(0.0

232)

(0.0

512)

(0.0

537)

(0.0

760)

(0.0

285)

(0.0

261)

(0.0

434)

(0.0

120)

π t-8

0.03

11-0

.029

20.

0682

0.09

81-0

.034

60.

0220

0.03

800.

1549

***

(0.0

266)

(0.0

472)

(0.0

496)

(0.0

696)

(0.0

327)

(0.0

173)

(0.0

371)

(0.0

175)

π t-9

0.13

20**

*0.

1126

***

0.01

820.

0462

0.01

64-0

.027

10.

1092

***

-0.0

415*

(0.0

373)

(0.0

417)

(0.0

493)

(0.0

829)

(0.0

343)

(0.0

199)

(0.0

399)

(0.0

233)

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 55

Journal of Applied Economics56Ta

ble

5 (c

ontin

ued)

. EGA

RCH-

mod

el p

aram

eter

est

imat

es

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

π t-1

00.

0026

-0.0

358

0.03

470.

0612

0.02

670.

0081

-0.0

519

0.10

55**

*

(0.0

335)

(0.0

496)

(0.0

550)

(0.0

950)

(0.0

387)

(0.0

166)

(0.0

381)

(0.0

238)

π t-1

10.

0072

0.12

83*

0.02

34-0

.002

8-0

.043

50.

0629

**-0

.049

60.

0173

(0.0

341)

(0.0

688)

(0.0

583)

(0.0

620)

(0.0

343)

(0.0

261)

(0.0

358)

(0.0

113)

π t-1

20.

1021

**0.

3489

***

0.13

870.

0928

0.09

61**

*0.

1189

***

0.07

55*

0.07

05**

*

(0.0

440)

(0.0

719)

(0.0

880)

(0.0

940)

(0.0

271)

(0.0

306)

(0.0

422)

(0.0

148)

π t-1

3-0

.081

4***

-0.0

463

-0.0

315

-0.0

701

-0.0

473*

-0.0

117

-0.0

265

0.01

33

(0.0

325)

(0.0

489)

(0.1

005)

(0.0

730)

(0.0

279)

(0.0

258)

(0.0

330)

(0.0

142)

D94 t

16.6

92**

*6.

8734

8.48

26**

*20

.618

9.95

76**

*16

.292

***

9.71

20**

*35

.158

***

(1.0

217)

(18.

789)

(1.3

732)

(50.

584)

(0.7

700)

(0.6

291)

(1.1

787)

(0.5

566)

Pane

l B. V

aria

nce

spec

ifica

tion

β 00.

4279

-2.4

331**

*-1

.101

0**1.

2794

-1.7

256**

*0.

3262

0.31

991.

9231

**

(0.6

925)

(0.8

197)

(0.5

482)

(1.5

542)

(0.5

728)

(0.7

095)

(0.6

684)

(0.8

813)

M1t

0.43

013.

5656

***

2.84

91**

*-0

.165

41.

9622

***

1.89

15*

1.10

030.

2303

(0.9

660)

(1.1

241)

(0.6

546)

(0.8

010)

(0.6

543)

(1.1

415)

(0.9

390)

(0.8

888)

M2t

-0.5

730

1.78

88*

-0.5

197

0.03

810.

3854

-1.8

495*

-3.3

350**

*-1

.035

2

(1.2

994)

(1.0

934)

(0.6

954)

(0.7

397)

(0.6

686)

(0.9

603)

(0.9

612)

(1.0

579)

M3t

-0.3

812

3.81

28**

*0.

0538

0.16

730.

4822

-0.2

641

-0.3

530

-1.2

247

(0.8

582)

(0.9

540)

(0.6

059)

(0.7

779)

(0.6

278)

(1.0

965)

(0.8

752)

(0.7

945)

M4t

0.21

273.

6230

***

1.56

03**

0.48

730.

6079

-1.1

308

-1.1

473

-1.2

587

(0.9

533)

(0.9

373)

(0.6

566)

(0.8

407)

(0.6

165)

(1.1

349)

(0.8

957)

(0.9

186)

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 56

Seasonality in Inflation Volatility: Evidence from Turkey 57Ta

ble

5 (c

ontin

ued)

. EGA

RCH-

mod

el p

aram

eter

est

imat

es

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

M5t

-0.8

588

2.65

95**

-0.0

771

-0.1

253

0.23

72-0

.251

4-1

.994

5*-0

.572

1

(1.3

133)

(1.1

228)

(0.6

764)

(1.0

791)

(0.4

481)

(1.1

984)

(1.0

973)

(0.8

935)

M7t

-0.3

288

4.19

94**

*0.

4563

0.35

751.

1272

**0.

0631

-1.0

397

0.38

55

(1.1

599)

(1.4

894)

(0.6

929)

(0.6

991)

(0.4

987)

(1.2

908)

(1.0

103)

(0.8

255)

M8t

-1.1

582

2.29

73**

3.49

71**

*0.

1250

-0.4

209

-1.6

579

-0.3

781

-1.3

342

(1.0

313)

(1.0

749)

(0.6

479)

(0.9

247)

(0.6

630)

(1.1

652)

(0.8

936)

(0.8

581)

M9t

-0.1

208

4.25

67**

*1.

8683

**-0

.932

4-0

.366

20.

0265

-0.9

316

0.01

75

(0.8

194)

(0.9

932)

(0.7

978)

(0.8

975)

(0.5

963)

(1.1

833)

(0.9

217)

(0.9

281)

M10

t-1

.003

73.

1697

***

-0.1

863

-0.6

303

0.33

32-1

.221

9-1

.257

7-0

.725

6

(0.9

592)

(1.0

205)

(0.8

592)

(1.1

469)

(0.7

253)

(0.9

643)

(0.8

963)

(1.0

031)

M11

t-2

.054

1**2.

2834

**-0

.307

2-1

.212

9-0

.606

80.

1051

-1.6

397*

-1.5

972*

(0.8

228)

(0.9

871)

(0.7

383)

(0.8

890)

(0.6

805)

(1.0

061)

(0.8

417)

(0.9

440)

M12

t-0

.663

31.

2874

-0.9

635

-0.2

644

0.28

87-0

.564

9-0

.675

3-1

.350

7

(1.5

817)

(1.0

012)

(0.6

999)

(1.3

330)

(0.7

435)

(1.0

607)

(0.9

318)

(0.9

300)

|εt-1

/ht-1

|0.

2642

-0.2

930**

0.95

40**

*0.

2468

2.01

58**

*0.

1779

0.82

79**

*0.

2683

(0.2

456)

(0.1

363)

(0.2

671)

(0.2

497)

(0.2

200)

(0.1

720)

(0.2

415)

(0.3

623)

ε t-1

/ht-1

-0.1

068

0.15

310.

2258

-0.0

264

-0.0

152

0.15

86-0

.034

50.

5855

**

(0.1

801)

(0.0

983)

(0.1

723)

(0.1

386)

(0.1

526)

(0.1

453)

(0.1

575)

(0.2

297)

Logh

2 t-20.

3295

0.83

01**

*0.

7038

***

-0.0

406

0.19

090.

9505

***

0.82

30**

*0.

0335

(0.8

832)

(0.0

841)

(0.1

675)

(1.1

004)

(0.1

207)

(0.0

397)

(0.0

952)

(0.2

511)

LRT

2.51

3253

.134

***

105.

44**

*13

.295

022

.805

**35

.113

***

28.7

90**

*6.

1122

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 57

Journal of Applied Economics58Ta

ble

5 (c

ontin

ued)

. EGA

RCH-

mod

el p

aram

eter

est

imat

es

CPI

Clot

hing

Cultu

reFo

odFu

rnitu

reHe

alth

Hous

ing

Trans

.

Pane

l C. D

iagn

ostic

test

s

Lags

Ljun

g-Bo

x Q

stat

istic

s

12[0

.445

0][0

.631

0][0

.601

0][0

.398

0][0

.238

0][0

.225

0][0

.520

0][0

.117

0]

24[0

.550

0][0

.700

0][0

.700

0][0

.538

0][0

.405

0][0

.275

0][0

.377

0][0

.248

0]

36[0

.507

0][0

.844

0][0

.734

0][0

.478

0][0

.644

0][0

.603

0][0

.371

0][0

.244

0]

ARCH

-LM

test

s

12[0

.585

3][0

.957

2][0

.743

8][0

.070

6][0

.413

3][0

.582

7][0

.254

6][0

.573

1]

24[0

.333

4][0

.978

1][0

.516

2][0

.481

3][0

.061

2][0

.960

1][0

.403

9][0

.999

5]

36[0

.744

2][0

.772

5][0

.185

2][0

.659

9][0

.319

9][0

.901

4][0

.494

1][0

.758

9]

Pane

l D. S

umm

ary

stat

istic

s

GED

para

met

er0.

9731

1.98

2119

2.68

002.

1339

6.60

780.

7850

1.09

060.

8500

(0.1

528)

(0.4

410)

(119

6.90

00)

(0.5

047)

(2.7

116)

(0.1

104)

(0.1

819)

(0.1

049)

R-sq

uare

d0.

8072

0.90

750.

4943

0.71

000.

5634

0.43

700.

7267

0.49

06

Adj.

R-sq

.0.

7625

0.88

610.

3771

0.64

290.

4623

0.30

660.

6634

0.37

26

S.E.

of

regr

essi

on1.

2826

1.85

253.

4276

2.20

851.

9036

2.75

871.

2557

3.21

28

Sum

sq.

resi

d29

1.32

607.

4720

88.1

086

3.35

641.

4513

48.1

027

8.95

1827

.40

DW s

tat

1.71

161.

6929

2.38

141.

9268

1.97

582.

0451

1.87

491.

6224

Log

likel

ihoo

d-3

04.3

6-3

67.2

9-4

18.6

3-4

47.6

7-3

46.1

2-4

35.9

1-2

69.5

3-4

51.6

9

Note

s: S

tand

ard

erro

rs a

re re

porte

d in

par

enth

eses

and

p-v

alue

s ar

e re

porte

d in

bra

cket

s. **

*in

dica

tes

sign

ifica

nce

at th

e 1%

leve

l z =

2.5

8. **

indi

cate

s si

gnifi

canc

e at

the

5% le

vel z

= 1

.96.

*in

dica

tes

sign

ifica

nce

at th

e 10

% le

vel z

= 1

.64.

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 58

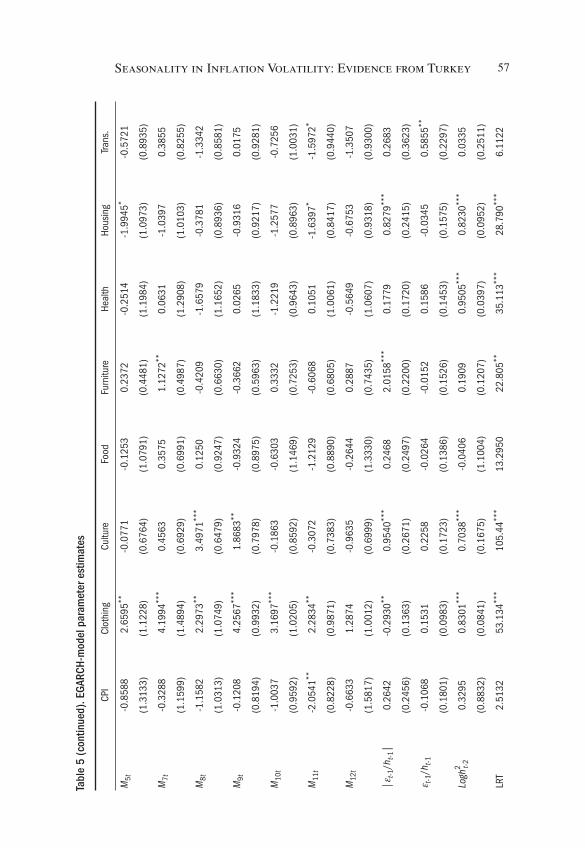

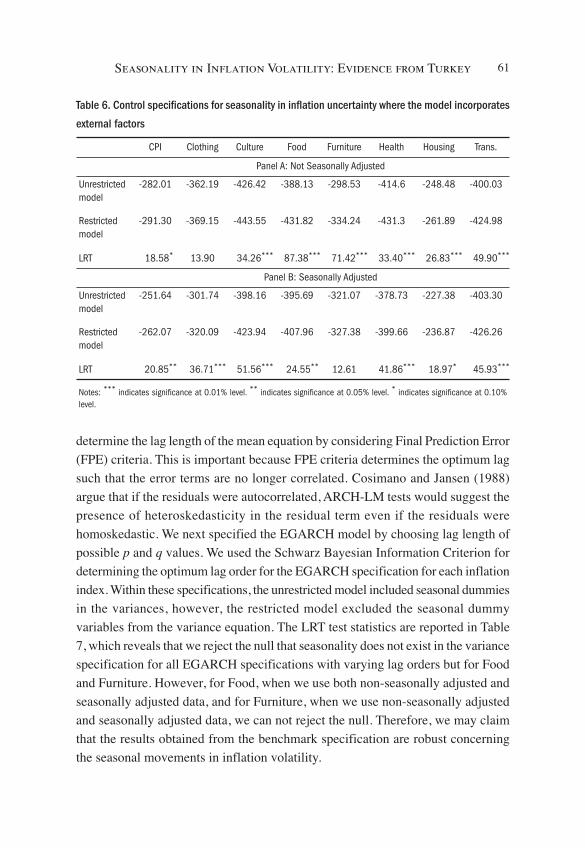

(this does not rule out that each individual coefficient is not zero). Log Likelihood

Ratio (LRT) statistics report the corresponding value. We can reject the null for

Clothing, Culture, Furniture, Health and Housing. In order to see whether the month

the conditional variance is maximum (or minimum) and statistically significant for

the other indexes (general CPI, Food and Transportation) as reported in Table 5,

we include just one dummy variable for the month corresponding to the conditional

variance specification. These coefficients are statistically significant individually

(not reported to save space.) Thus, we can claim that the conditional variance is not

the same across each month.

In volatility specifications, our estimates of the lagged value of the conditional

variances are less than one for each item; this implies that inflation volatility is not

explosive (Panel B). However, there is higher persistence in the volatilities for

Clothing, Culture, Health and Housing than for the others. Moreover, for Clothing,

Culture, Health and Transportation a positive shock to inflation increases volatility

more than a negative shock – the leverage effect. For the rest of the series, in the

general CPI, Food, Furniture and Housing, negative residuals tend to produce higher

variances. Panel C reports the Ljung-Box Q statistics and ARCH-LM tests for the

12, 24 and 36 lags. None of the test statistics is significant at the 5% level.

It is plausible that the results we gathered might be a type of seasonal accounting

and that the estimates could be sensitive to deseasonalization. Thus, we repeat the

exercise with the seasonally adjusted data (these estimates are available from the

authors upon request). The lowest volatilities are in November for the general CPI

and in February for Housing. Moreover, the highest volatilities in January for the

general CPI, in August for Culture and in January for Furniture and Health are

robust. This finding is the same for the estimates from Table 5. Furthermore, even

if the volatilities in June for Clothing, in December for Culture and in November

for Furniture are not the lowest, as reported in Table 5, they are the second-lowest

volatilities. This exercise reveals that November for Transportation is the third

lowest and the same month for Food is the fourth lowest. January is the second

highest for Transportation. Last, September for Clothing and January for Housing

are fourth highest. Thus, one may claim that the results from Table 5 are mostly

robust.9

Seasonality in Inflation Volatility: Evidence from Turkey 59

9 We also tried different deseasonalization methods; although the specific month for the maximums andminimums changes, the results are mostly robust.

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 59

V. Extensions

In this section of the paper, we will consider a set of specifications to assess the

robustness of our estimates. First, it is plausible that the seasonality in volatility

may exist due to other determinants of inflation (or its volatility). In order to account

for this we set up two models, both of which include a set of additional variables

with a lag to both mean and variance equations. The first (unrestricted) model

includes monthly dummies in the variance specification and the second (restricted)

model does not include monthly dummies in the variance specification. The additional

variables included in these two sets of specifications are the: squared industrial

production deviation (calculated by the square of deviations from the trend obtained

by Hodrick’s and Prescott’s 1997 methodology), logarithmic first difference of the

exchange rate basket (basket is the Turkish lira value of the US dollar + the Euro),

logarithmic first difference of oil prices (Dubai spot), logarithmic first difference

of the real exchange rate; interbank rate, and an election dummy (general and local).10

As in the paper, for the seasonally unadjusted series our unrestricted model includes

seasonal dummies in the variance and mean equation and our restricted model

excludes seasonal dummies from the variance specification, but keeps seasonal

dummies in the mean equation only. For the seasonally adjusted series, we also

exclude seasonal dummies from the mean equation for both specifications. Panel

A of Table 6 reports the likelihood values of the estimates that use seasonally

unadjusted data and Panel B reports the same value for the seasonally adjusted data.

Likelihood Ratio Test (LRT) statistics clearly reject the null that the estimated

coefficients for the seasonal dummies are jointly zero in the variance specification

when the other explanatory variables are included.11

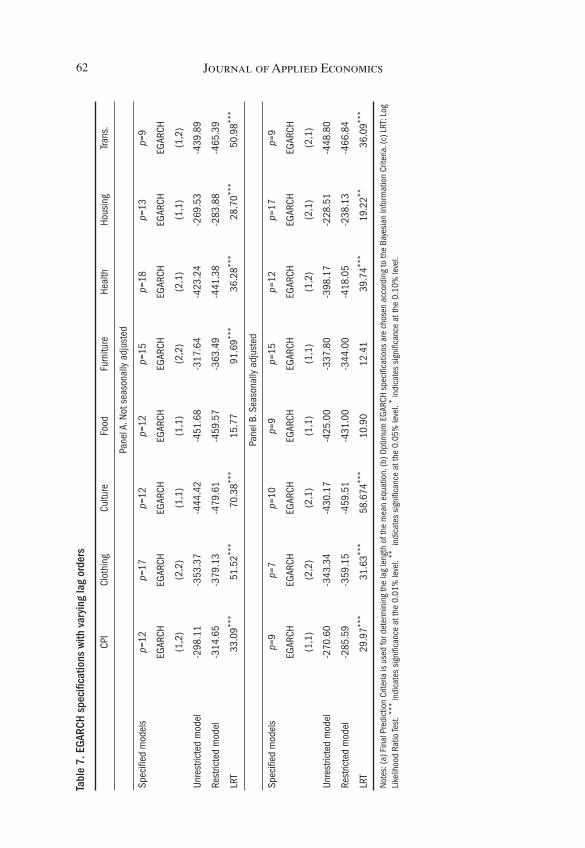

Second, it is plausible that the final models are mis-specified because the same

lag structure for each of the mean and variance equations for different price indexes

are used. Thus, we estimate a set of models such that lag selection is determined

by a set of statistical criteria for the seasonally unadjusted and adjusted data. We

Journal of Applied Economics60

10 We gathered the industrial production, exchange rate basket and interbank rate data from the CentralBank of the Republic of Turkey’s electronic data delivery system. The data for oil prices is gatheredfrom the International Monetary Fund’s International Financial Statistics Database. We constructedelection dummy data from the Office of the Prime Minister, the Director General of Press and Informationand the Grand National Assembly of Turkey.

11 Both the exchange rate depreciation and the real exchange rate depreciation variables are statisticallysignificant in both the mean and variance specifications.

jaeXIII_1:jaeXIII_1 5/11/10 9:21 PM Página 60

determine the lag length of the mean equation by considering Final Prediction Error

(FPE) criteria. This is important because FPE criteria determines the optimum lag

such that the error terms are no longer correlated. Cosimano and Jansen (1988)

argue that if the residuals were autocorrelated, ARCH-LM tests would suggest the

presence of heteroskedasticity in the residual term even if the residuals were

homoskedastic. We next specified the EGARCH model by choosing lag length of

possible p and q values. We used the Schwarz Bayesian Information Criterion for

determining the optimum lag order for the EGARCH specification for each inflation

index. Within these specifications, the unrestricted model included seasonal dummies

in the variances, however, the restricted model excluded the seasonal dummy

variables from the variance equation. The LRT test statistics are reported in Table

7, which reveals that we reject the null that seasonality does not exist in the variance

specification for all EGARCH specifications with varying lag orders but for Food

and Furniture. However, for Food, when we use both non-seasonally adjusted and

seasonally adjusted data, and for Furniture, when we use non-seasonally adjusted

and seasonally adjusted data, we can not reject the null. Therefore, we may claim

that the results obtained from the benchmark specification are robust concerning

the seasonal movements in inflation volatility.

Seasonality in Inflation Volatility: Evidence from Turkey 61

Table 6. Control specifications for seasonality in inflation uncertainty where the model incorporates

external factors

CPI Clothing Culture Food Furniture Health Housing Trans.

Panel A: Not Seasonally Adjusted

Unrestrictedmodel

-282.01 -362.19 -426.42 -388.13 -298.53 -414.6 -248.48 -400.03

Restrictedmodel

-291.30 -369.15 -443.55 -431.82 -334.24 -431.3 -261.89 -424.98