Joseph V. Rizzi June 15, 2011 Setting Risk Appetite in the New Regulatory Environment Linking Strategy, Risk and Capital Structure © The views expressed are the author’s, and do not reflect those of CapGen Financial RISK MINDS USA

Joseph V. Rizzi June 15, 2011 Setting Risk Appetite in the New Regulatory Environment Linking Strategy, Risk and Capital Structure © The views expressed.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Joseph V. RizziJune 15, 2011

Setting Risk Appetite in the New Regulatory Environment Linking

Strategy, Risk and Capital Structure ©

The views expressed are the author’s, and do not reflect those of CapGen Financial

RISK MINDS USA

2

Risk Appetite2

Introduction1

Capital Structure3

Conclusions4

1. INTRODUCTION

3

Introduction

4

Need to incorporate capital structure and risk considerations as an input versus consequence of strategyCapital as cost of riskReturn as cost of capitalRisk as cost of return

Risk appetite links strategy, risk and capital –represents total risk exposure an organization is willing (and capable?) to accept and retain in pursuit of its strategy

(Risk Appetite as a Process…

… Not a Number)

Introduction (cont) (Once set…

5

Return Opportuni

ties

Governance

Volatility LiquidityStrategic CapitalBudgeting (CEO)

Correlations

Risk Management

(CRO)Risk Appetite

Capabilities

External Stakeholders

ShareholdersRisk/Return Regulators

Performance

Capital StructureCFO

Rating Agencies

…Risk appetite is continuously monitored and revised)

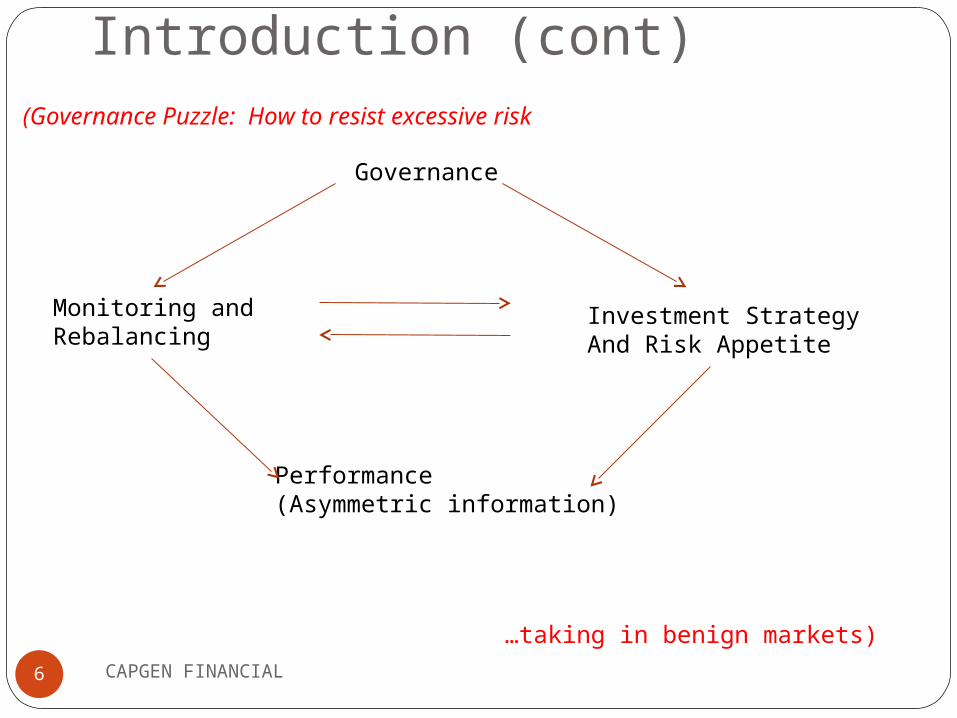

Introduction (cont)

CAPGEN FINANCIAL6

Governance

Monitoring andRebalancing

Investment StrategyAnd Risk Appetite

Performance(Asymmetric information)

(Governance Puzzle: How to resist excessive risk

…taking in benign markets)

2. RISK APPETITE

7

8

(Return on equity value illusion…

…Confusing key performance Indicators with value drivers)

Implications of Risk Appetite Charges

9

(Not all Risk is the Same…

Return

E F Risk

Capital Requirement

Efficient Frontier (Beta)

CA

B

…Cost of Risk is Capital)

A – CurrentB – TargetD – C = Capital Need to Support TargetEF = Increased Risk Appetite

D

Rf

10

(High Returns Evidence of Skill……

… Or Extreme Risk Taking?)

Problem – Procyclical Risk Appetite

11

Low High

Bull

Bear

Strong

Capital

Weak

Market State

Risk

2003/06 2007

2009 2008

Reinforcement•Budgets and Bonuses - KillerBs hard to recognize risk if you are paid not to do so•Preoccupation with Growth – Barclays?•Herding

… and vary over time depending on wealth)

Risk Appetite

(Risk Appetite Changes are Prone to Behavior Bias and Drift…

3. CAPITAL STRUCTURE

12

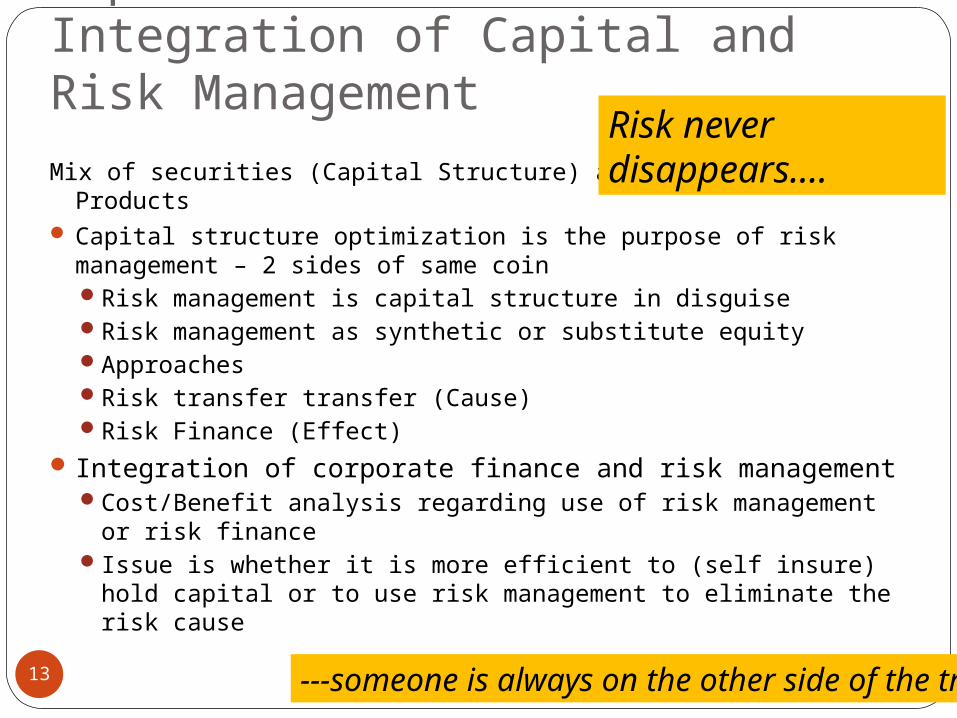

Capital Structure – Integration of Capital and Risk Management

13

Mix of securities (Capital Structure) and Risk Management Products

Capital structure optimization is the purpose of risk management – 2 sides of same coinRisk management is capital structure in disguiseRisk management as synthetic or substitute equityApproachesRisk transfer transfer (Cause)Risk Finance (Effect)

Integration of corporate finance and risk management Cost/Benefit analysis regarding use of risk management or

risk financeIssue is whether it is more efficient to (self insure) hold

capital or to use risk management to eliminate the risk cause

Risk never disappears….

---someone is always on the other side of the trade

Stakeholder Views of Capital Differ

14

Capital focus is primarily on tangible equity capital and capital replenishment capabilities.

Concern on through the cycle capital and buffers

Are focused on capital discipline and allocation

Capital Returns and bonuses

Rating Agencies

Regulators

Shareholders

Is the glass half full or half empty

… it depends on whether you are pouring or drinking

Management

Capital Guidelines

S&P: RAC

Very strong >15%

Strong 15/≤ X <10%

Adequate 10 ≤ X < 7%

Moderate 7% ≤ X < 5%

Weak 5% ≤ X < 3%

Very Weak >3%

CAMELS – “C” and “A”:Classified Assets/T1 + ALL

1 - O ≤ X ≤ 25%

2 – 26%< X ≤ 40%

3 - 41% < X ≤ 80%

4 - 81% ≤ X ≤ 100%

5 - > 100

CAPGEN FINANCIAL15

(How much is enough?…

…it depends

Scenarios: To Assess Possible Strategies Against Capital Structure Robustness

16

Financial policy implications:

The upside (U) and base (B) cases generate excess capital which points toward shareholder distributions

The downturn (D) scenario suggests possible changes in risk appetite and the development of appropriate contingency plans to maintain ratios, sell assets and raise capital.

Forward looking Core Tier 1 development under alternative scenarios

U- - - - - - - - - - - - - - - - - - - - - - - - -

B- - - - - - - - - - - - - - - - - - - - - - - - -

D

T

ReturnCapital

Raise/release Capital

Probably

May be

Unlikely

Unlikely

May be

Probably

(Can I survive and tolerate…..

…the worst plausible outcome?)

(Stress testing)

17

Decisions at Risk (DAR) Control Framework

(Who decides…

…And how do they decide?)

Elements of Strategy Based Capital Structure Management

Choice of Markets with Attractive economics inwhich the organization enjoys a competitive advantage

Risk the organization is willing and able to accept in

pursuit of its strategy

Risks underwritten and retained

Capital relative to Ratings Agencies, Regulators and peersActual Capital

Return capital to shareholders when actual capital exceedsneed, or raise capital when exceeds actual capital

Allocation to business units based on an economiccapital determination

18

(Risk and capital as inputs into strategic planning….)

(…and not just consequences)

Strategy

Risk Appetite

Risk Assessment

Capital Need and

Capital Assessment

Capital Plan

Capital Allocation

4. CONCLUSION

19

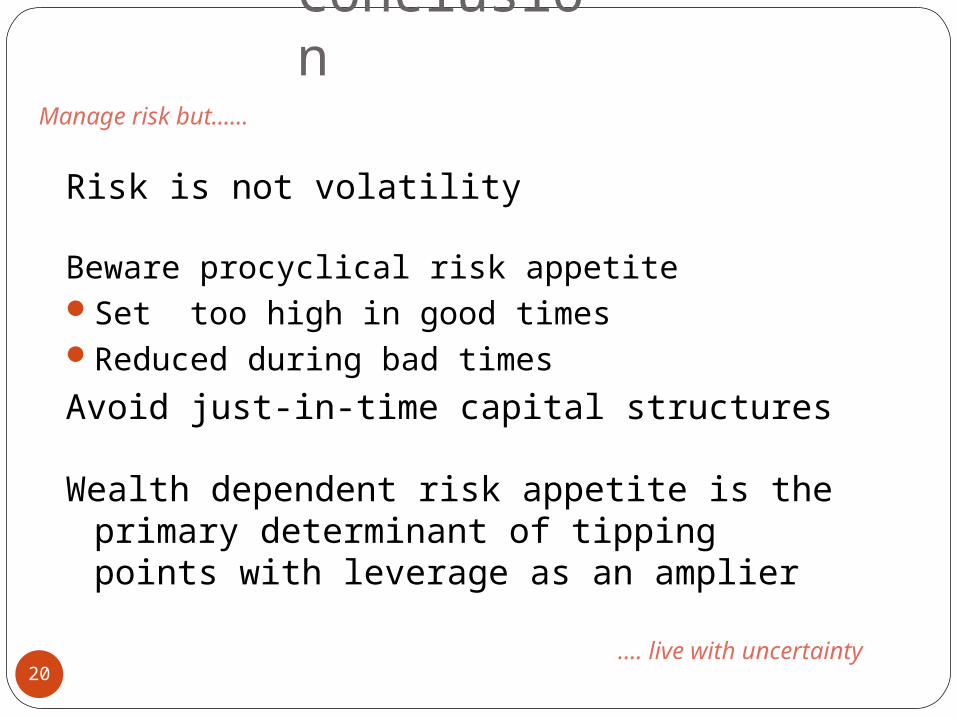

Conclusion

Risk is not volatility

Beware procyclical risk appetiteSet too high in good timesReduced during bad times

Avoid just-in-time capital structures

Wealth dependent risk appetite is the primary determinant of tipping points with leverage as an amplier

20

Manage risk but……

…. live with uncertainty

Related Documents