Volume 9, Number 5, May 2013 (Serial Number 96) Journal of Modern Accounting and Auditing David Publishing Company www.davidpublishing.com Publishing David

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Volume 9, Number 5, May 2013 (Serial Number 96)

Journal ofModern Accounting and Auditing

David Publishing Company

www.davidpublishing.com

PublishingDavid

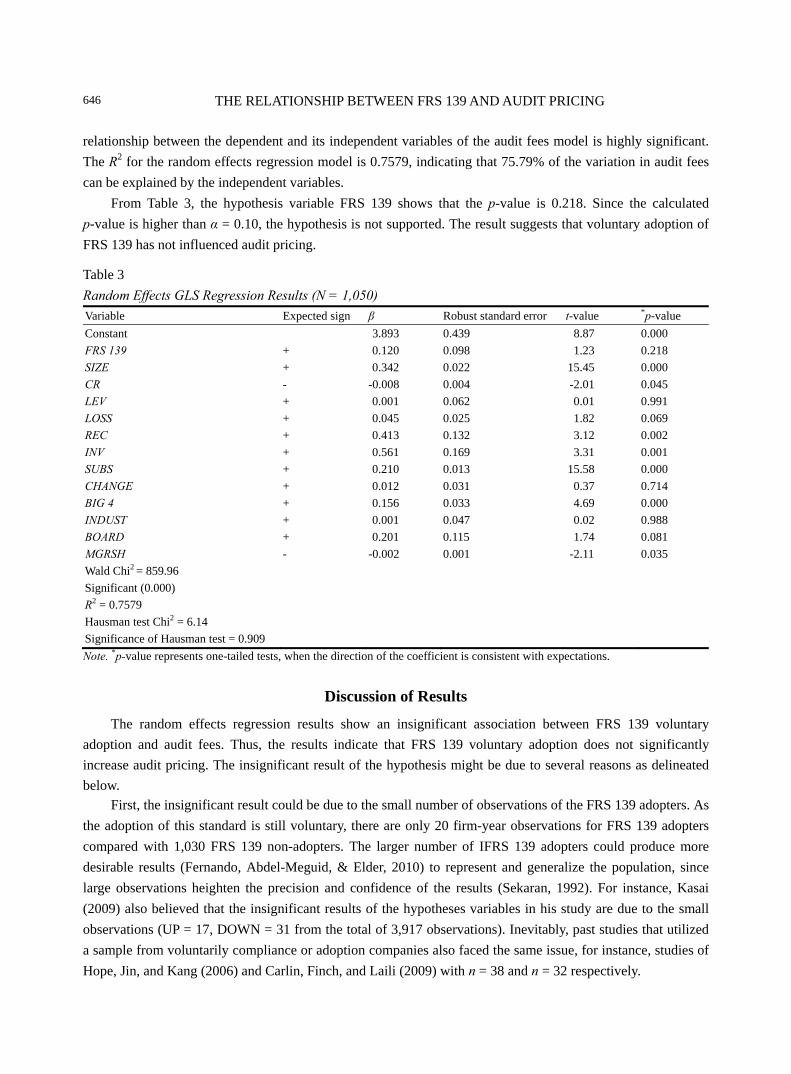

Publication Information: Journal of Modern Accounting and Auditing is published monthly in hard copy (ISSN1548-6583) and online (ISSN1935-9683) by David Publishing Company located at 9460 Telstar Ave Suite 5, EL Monte, CA 91731, USA. Aims and Scope: Journal of Modern Accounting and Auditing, a monthly professional academic journal, covers all sorts of researches on accounting research, financial theory, capital market, audit theory and practice from experts and scholars all over the world. Editorial Board Members: Benedetta Siboni, Italy. Brad S. Trinkle, USA. Daniela Cretu, Romania. Elisabete Fátima Simões Vieira, Portugal. Haihong He, USA. Joanna Błach, Poland. João Paulo Torre Vieito, Portugal. Liang Song, USA. Lindita Rova, Albania. Mohammed Al-Omiri, Saudi Arabia. Mohamed Rochdi Keffala, Tunisia. Mohammad Talha, Saudi Arabia. Monika Wieczorek-Kosmala, Poland. Narumon Saardchom, Thailand.

Peter Harris, USA. Philip Yim Kwong Cheng, Australia. Rosa Lombardi, Italy. Sheikh Abdur Rahim, Bangladesh. Thomas Gstraunthaler, South Africa. Tita Djuitaningsih, SE, M.Si., Ak., Indonesia. Tiziana Di Cimbrini, Italy. Tumellano Sebehela, United Kingdom. Valdir de Jesus Lameira, Brazil. Valerio Pesic, Italy. Vintilescu Belciug Adrian, Romanian. Wan Mansor W. Mahmood, Malaysia. Zeynep Özsoy, Turkey.

Manuscripts and correspondence are invited for publication. You can submit your papers via Web Submission, or E-mail to [email protected]. Submission guidelines and Web Submission system are available at http://www.davidpublishing.com. Editorial Office: 9460 Telstar Ave Suite 5, EL Monte, CA 91731 E-mail: [email protected], [email protected] Copyright©2013 by David Publishing Company and individual contributors. All rights reserved. David Publishing Company holds the exclusive copyright of all the contents of this journal. In accordance with the international convention, no part of this journal may be reproduced or transmitted by any media or publishing organs (including various websites) without the written permission of the copyright holder. Otherwise, any conduct would be considered as the violation of the copyright. The contents of this journal are available for any citation, however, all the citations should be clearly indicated with the title of this journal, serial number, and the name of the author. Abstracted/Indexed in: Database of EBSCO, Massachusetts, USA ProQuest Cambridge Scientific Abstracts (CSA)-Natural Sciences Australian ERA Universe Digital Library Sdn Bhd (UDLSB), Malaysia Chinese Database of CEPS, Airiti Inc. & OCLC Chinese Scientific Journals Database, VIP Corporation, Chongqing, P.R.China Ulrich’s Periodicals Directory Database of Summon Serials Solutions, USA Subscription Information: Price (per year): Print $640; Online $480; Print and Online $800 David Publishing Company 9460 Telstar Ave Suite 5, EL Monte, CA 91731, USA Tel: 1-323-984-7526, 323-410-1082; Fax: 1-323-984-7374, 323-908-0457; E-mail: [email protected]

David Publishing Company

www.davidpublishing.com

DAVID PUBLISHING

D

Journal of Modern Accounting and Auditing

Volume 9, Number 5, May 2013 (Serial Number 96)

Contents Accounting, Auditing & Financial Management

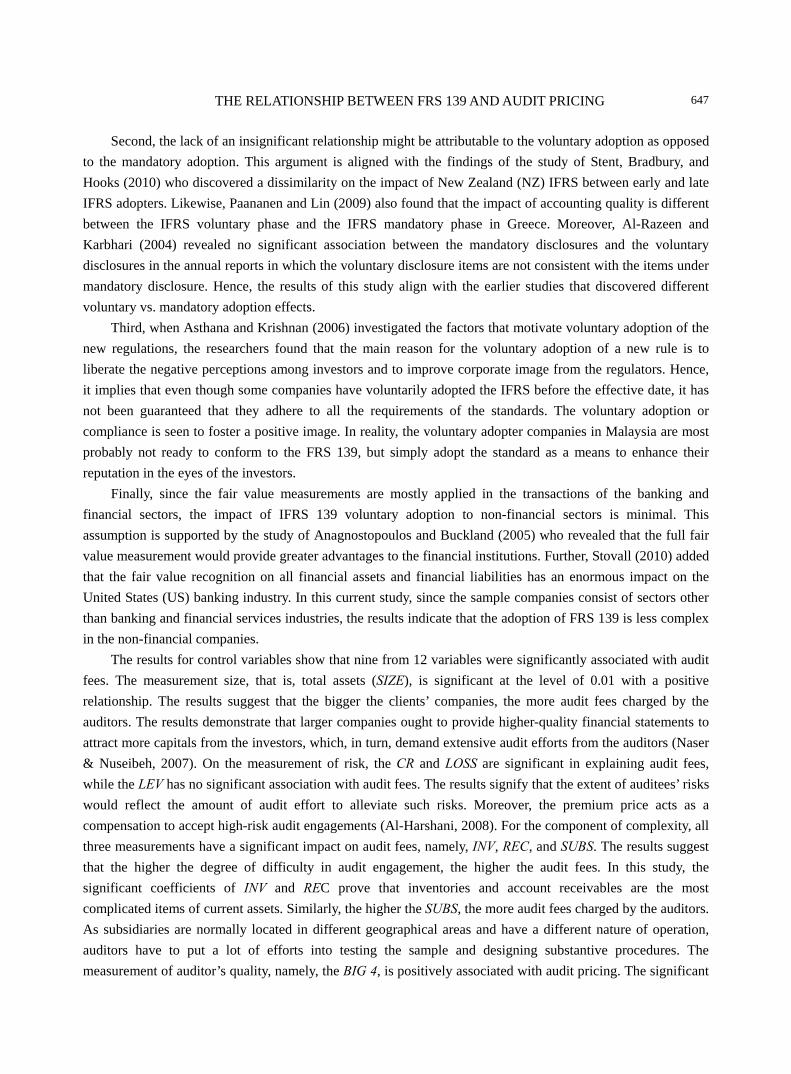

Financial Statement Comparability: Empirical Evidence From Brazil 587

Sirlei Lemes, Luciana de Almeida Araújo Santos, Núbia Aparecida Rodrigues

Can the Dominant Trait Indicator Predict Success in a Financial Accounting Principles

Course? A Preliminary Look 602

John Garlick, Susan Shurden, Mike Shurden

Accounting of Foreign Currencies: Difference in Exchange Transactions and Relation With

Taxation of Indonesia (Case Study in Fishery Company) 609

Ilham Hidayah Napitupulu, Abdul Rahman Dalimunthe

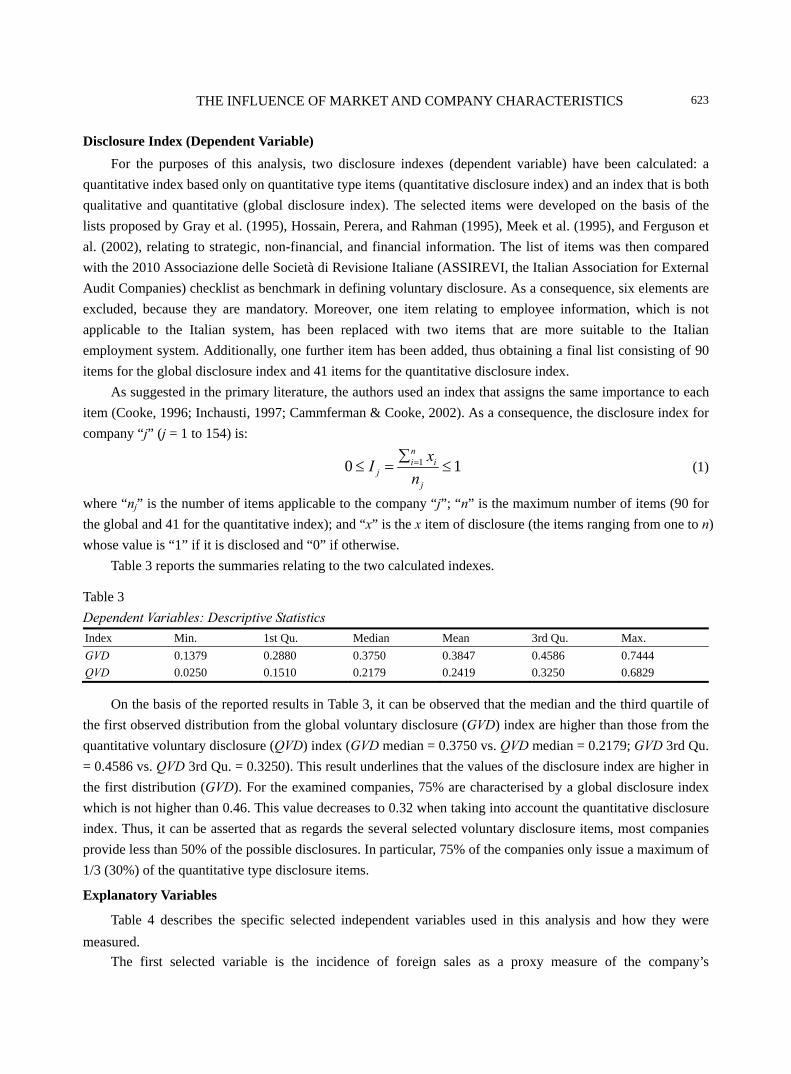

The Influence of Market and Company Characteristics on Voluntary Disclosure 616

Eugenio D’Amico, Anna Maria Biscotti

Audit Reports of Financially Distressed Companies: Emphasis of Matter (EOM) Versus

Disclaimers 634

Hashanah Ismail, Mazlina Mustapha

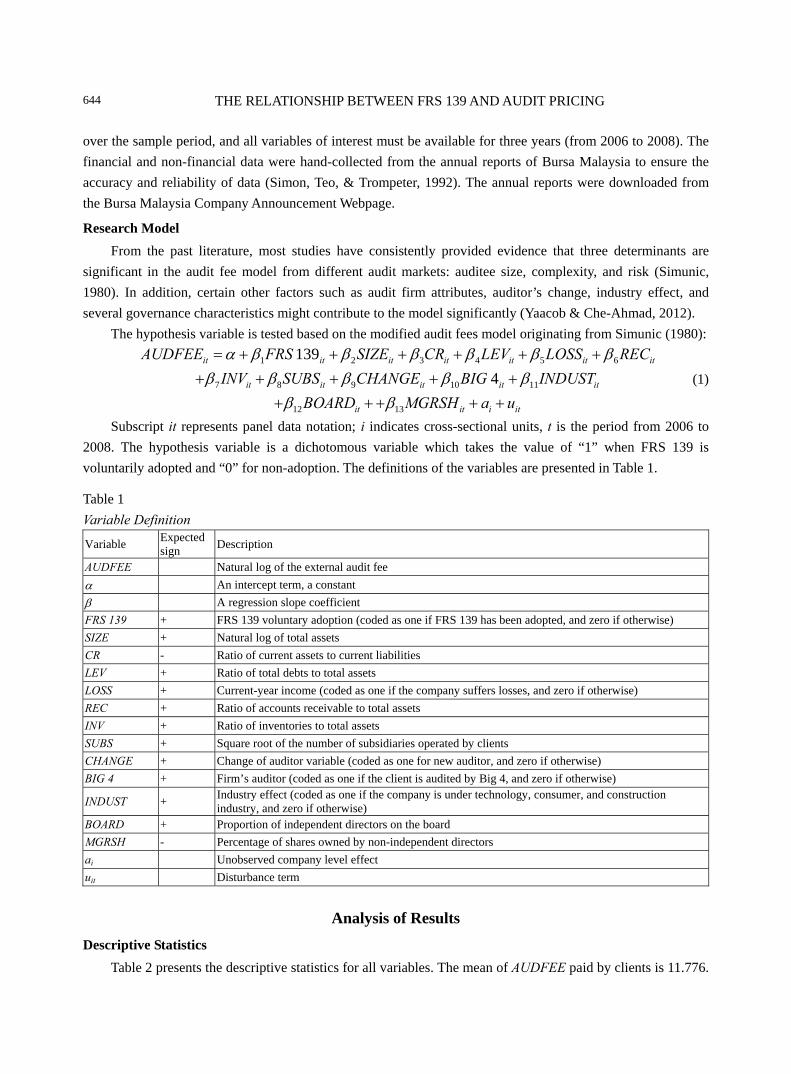

The Relationship Between Financial Reporting Standards (FRS) 139 and Audit Pricing:

The Case of Malaysia 641

Najihah Marha Yaacob

Executive Compensation and Corporate Financial Performance: Empirical Evidences on

Brazilian Industrial Companies 650

Elizabeth Krauter, Almir Ferreira de Sousa

Capital Market & Economy

The Recent US Financial Crisis: Its Impact on Dividend Payout Strategy and a Test of

the Silver-Lining Hypothesis 662

Chuo-Hsuan Lee, Edward J. Lusk, Michael Halperin

The Adoption and Maintenance of Executive Stock Option Plan (ESOP): Company

Characteristics Evaluation in Indonesia 678

Nur Fadjrih Asyik

Pyramid Schemes and Multilevel Marketing (MLM): Two Sides of the Same Coin 690

Olubusola H. Akinladejo, Marjorie Clarke, Felix O. Akinladejo

The Income Security System in Japanese Traditional Performing Arts: A Strategy for

Utilizing the Nation’s Traditional Arts Resources 697

Tadashi Yagi, Chisako Takashima, Yoshinori Usui

Analysis of Salaries and Some Non-traditional Measures of Location 711

Milan Terek, Nguyen Dinh He

A New Latent Class Stochastic Frontier Model for the Best Practices of USA’s Corporate

Governance 719

Wided Khiari, Yosra Mellouli

Journal of Modern Accounting and Auditing, ISSN 1548-6583 May 2013, Vol. 9, No. 5, 587-601

Financial Statement Comparability:

Empirical Evidence From Brazil

Sirlei Lemes, Luciana de Almeida Araújo Santos, Núbia Aparecida Rodrigues

Federal University of Uberlandia, Uberlandia, Brazil

The convergence of accounting standards started in the 1970s, with international norms issued by the International

Accounting Standards Board (IASB) and with the efforts of various countries to adopt the International Financial

Reporting Standards (IFRS), already mandatory in Brazil since 2010. Thus, comparable accounting information is

clearly important, and this study plans to confirm the level of comparability of net income and equity of companies

in the financial sector (in Brazil, “Finance and Others”), listed in the stock exchange, futures, and commodities

(BM&F Bovespa1), issued according to Brazilian Generally Accepted Accounting Principles (BR GAAP) and the

IFRS. This study is descriptive, using a quantitative approach. Data were collected from secondary sources, more

specifically, from the explanatory notes in the financial statements of the companies listed in the financial sector of

the BM&F Bovespa in the fiscal year of 2010. The results showed a reasonable level of comparability, with 68% of

the companies presenting materially comparable information for net income and 72% of them for equity. However,

decisions made based on data issued following the two different standards may have suffered the influence of

asymmetric information; in other words, the comparability of information did not seem to satisfy those companies

during the studied period of time. The main limitations of this study were data collection and selection for the

development of the research because of: (1) inconsistence in net income and equity reconciliation criteria in the

companies investigated; and (2) lack of uniformity in designating the adjustments that affect net income and equity

in the conversion of the BR GAAP standard into the IFRS.

Keywords: comparability, International Financial Reporting Standards (IFRS), Brazilian Generally Accepted

Accounting Principles (BR GAAP)

Introduction

The reflex of global economy on accounting can be seen in the need to harmonize accounting language,

once the information needs to be understood by users worldwide, so as to subsidize them in the

decision-making process. Such a convergence can be seen as an improvement in global accounting

communication, because it allows for faster capital market transactions and possibly reduces the cost of

information.

Attempts to converge accounting standards can be identified since the 1970s, with the creation of the

International Accounting Standards Committee (IASC), being that in the 2000s, the process is strengthened by

Sirlei Lemes, Faculty of Accounting, Federal University of Uberlandia. Email: [email protected]. Luciana de Almeida Araújo Santos, graduate student, master in Management, Federal University of Uberlandia. Núbia Aparecida Rodrigues, Faculty of Accounting, Federal University of Uberlandia.

1 Bolsa de Valores, Mercadorias, & Futuros de São Paulo, a stock exchange located at Sao Paulo, Brazil.

DAVID PUBLISHING

D

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

588

the transformation of the IASC into the International Accounting Standards Board (IASB) in 2001. The latter

then becomes the body responsible for the release of the International Financial Reporting Standards (IFRS).

This process is further reinforced by the decision of the European Union to fully adopt the IFRS beginning in

2005.

Thenceforth, a growing demand of unified accounting standards can be clearly seen, so that organizations

can operate in global markets. In that sense, Brazilian accounting has been going through the process of

implementation of the international standards since 2010 when the IFRS was made compulsory. This evolution,

however, brings about quite a few challenges regarding the change of accounting with a strong normative and

fiscal character into a more subjective and interpretative one.

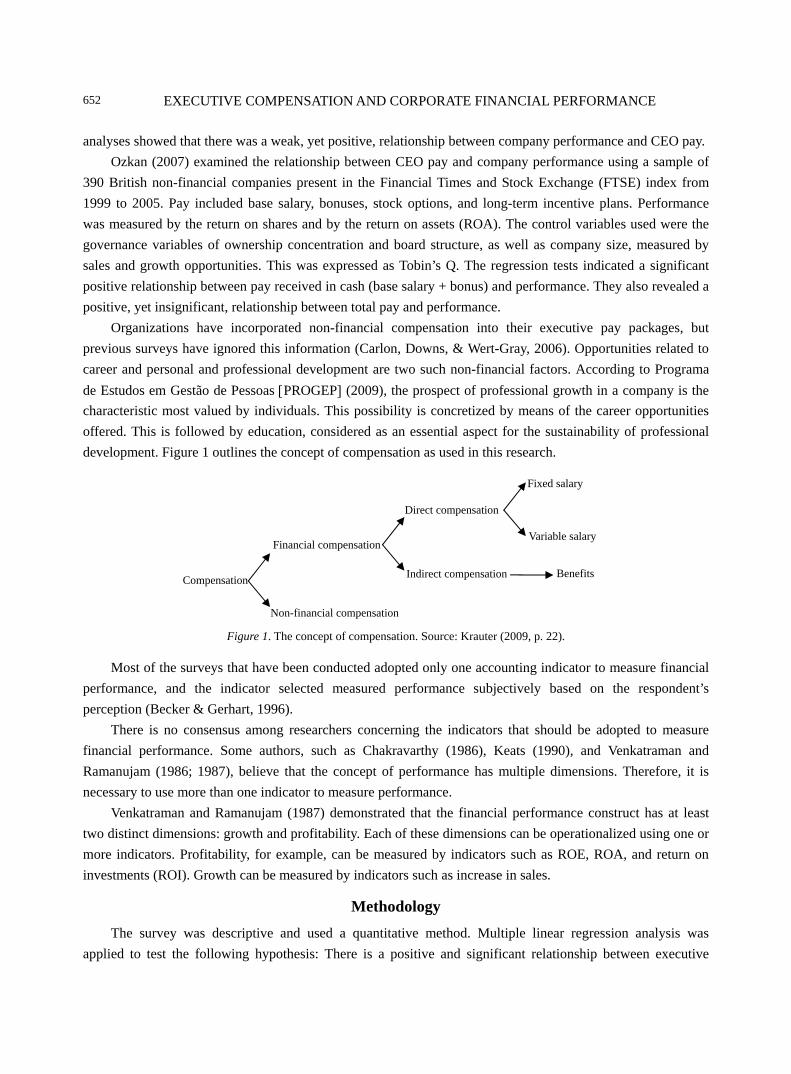

The basic conceptual statement issued by the CPC2 in 2008 regards comparability as one of the main

qualitative traits in accounting information. This declaration defines comparability as the ability to allow the

user to compare accounting demonstrations of one or various business entities, over time, in order to identify

patrimonial and financial tendencies, performance, and financial position mutations.

The disclosure of accounting demonstrations following the IFRS became mandatory in Brazil starting in

2010. Because of that and of the importance given to accounting information comparability within the

convergence process, the aim of this study is to answer the question what the level of comparability of the net

income and equity of the companies is within the financial sector listed in the BM&F Bovespa following

Brazilian Generally Accepted Accounting Principles (BR GAAP), if compared with the IFRS.

Therefore, this article proposes to verify the level of comparability between the net income and equity,

within BR GAAP standards and according to the IFRS of companies in the financial sector listed on the stock

exchange, futures, and commodities (BM&F Bovespa, 2011). In order to accomplish such a proposal, the

comparability index was used, and the adjustments which caused a divergence between the information

generated by the two standards were identified. The data used for the study were taken from the net income and

the equity of the companies in 2009, disclosed in the 2010 financial statements and their respective

reconciliation frameworks, when disclosed.

Several studies about the subject do not include the financial sector in their sampling because of its

peculiarities and, often, because of its more complex regulations. Therefore, the aim of this work is to

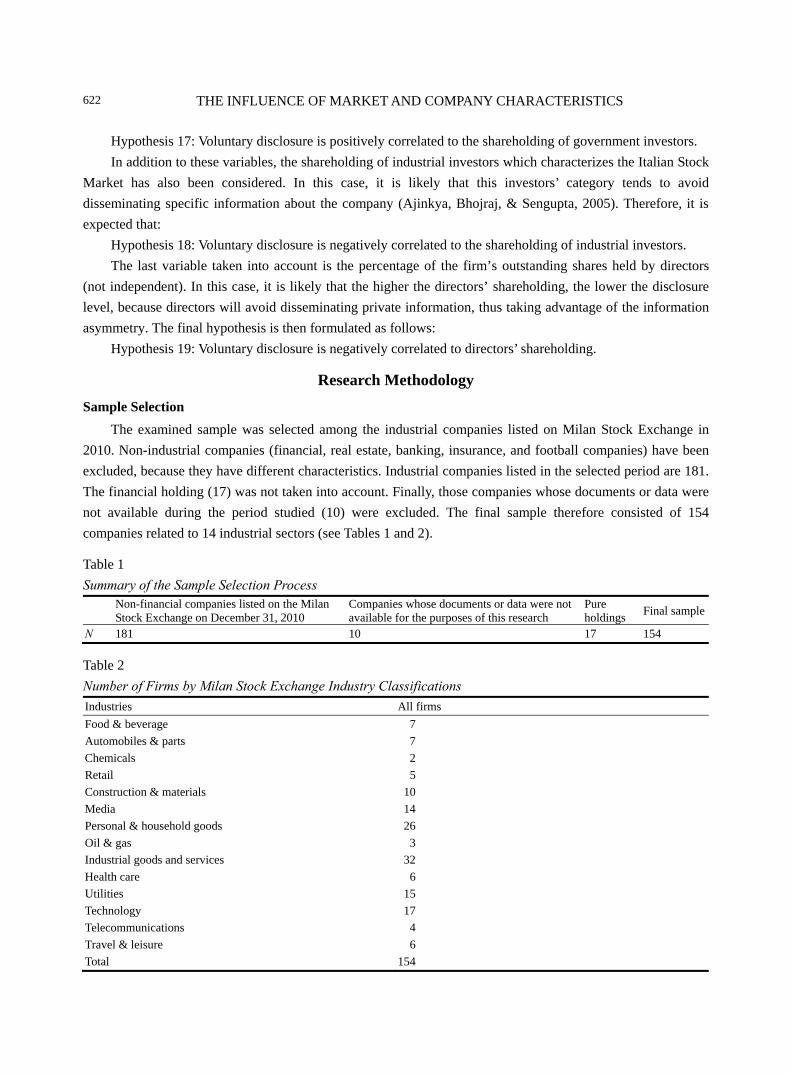

specifically study this very sector, denominated “Financial and Others” in the BM&F Bovespa classification.

Structurally, this article is presented in four sections besides this one. Section 2 deals with the evolution of

international accounting and its development in Brazil, and, furthermore, the issue of accounting information

comparability. Section 3 handles the methodological aspects and describes the samples used. Thereafter, an

analysis of the results is presented, and finally, in Section 5, the closing remarks are presented.

Theoretical Foundation

The beginning of the convergence process of accounting language was already identified in 1973, with the

launching of the IASC, with headquarters in London, through a deal among accounting entities in Australia,

Canada, France, Germany, Japan, Mexico, the Netherlands, the United Kingdom, Ireland, and the USA. The

idea to create such a committee came about in 1972, during the 10th World Congress of Accountants in

Sidney. 2 Comite dos Pronunciamentos Contábeis, Accounting Pronouncement Agency, a Brazilian organization created to centralize the issuing of norms converging with the international accounting standards.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

589

The goal of the IASC was to formulate and publish, in a totally independent way, international accounting

norms suitable to be accepted by the whole world (Filho, Lopes, & Pederneiras, 2009), trying to “simplify the

capital flow between all countries, easing the comparison of accounting statements” (Lemes & Carvalho, 2009,

p. 31).

The structure of the IASC was changed in 2001, originating the IASB, committee responsible for issuing

the IFRS, which, since then, has been trying to obtain approval of various countries to the convergence process

to improve the utility of accounting information internationally.

The approval of Ruling 1606/2002 by the European Union may be seen as an incentive for the

convergence to international norms in other countries. Such a ruling predicted the obligatoriness of the full

adoption of the IFRS by all companies listed in the European stock market, beginning in January 2005 (Callao,

Jarne, & Lainez, 2007). According to Farah, Martins, Romani, and Lisboa (2010, p. 21), “The adoption of the

IFRS by European countries was very fast. Actually, around 7,000 companies listed in the European Stock

Market have already adopted the IFRS⎯275 of these did so before 2005”.

The adoption of the IFRS as an accounting standard is spreading all over the world. According to Farah et

al. (2010), it has been adopted by more than 100 countries, including Brazil.

Brazilian accounting, historically, shows strong normative characteristics and is highly influenced by

fiscal legislation. Law 6404/763 (Corporations Law) regulates the activities of corporations. The remaining

types of society are regulated by Book II (from Article 966 to Article 1195) of Law 10.406/02 (The New

Brazilian Civil Code). Norms for specific sectors are also issued by entities entitled with such powers: Central

Bank of Brazil (BACEN, Banco Central do Brazil), Real Estate Values Committee (CVM, Comissão De

Valores Mobiliários), Private Security Superintendence (SUSEP, Superitendência de Seguros Privados), and

National Electric Power Agency (ANEEL, Agência Nacional de Energia Elétrica).

The conceptual aspects of accounting science were handled by Independent Brazilian Auditors Institute

(IBRACON, Instituto dos Auditores Independentes do Brasil) until the creation of the Federal Accounting

Committee (CPC). IBRACON approved the basic conceptual accounting structure elaborated by Accounting,

Actuary, and Financial Research Institute (FIPECAFI, Fundação Instituto de Pesquisas Contábeis, Atuariais e

Financeiras) which dealt with theoretical accounting framework and also with the GAAP. The CPC issued the

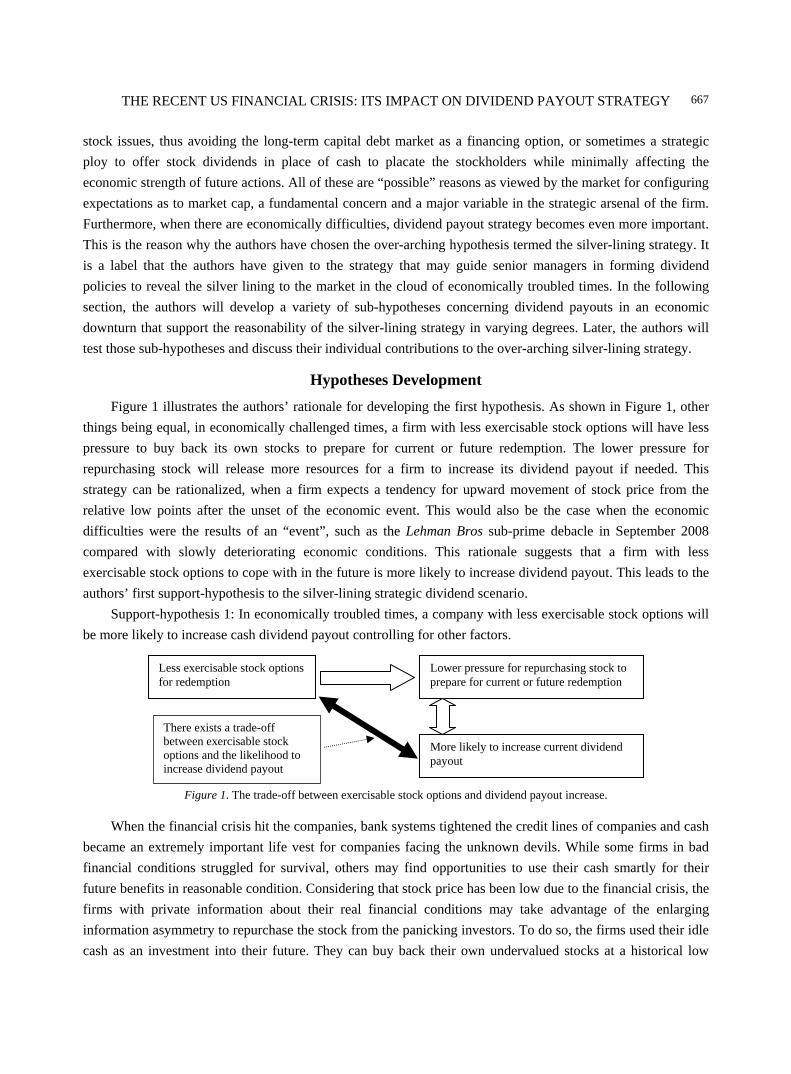

fundamental accounting principles (PFC, princípios fundamentais de contabilidade), through resolution

750/1993 of the Federal Accounting Council (Conselho Federal de Contabilidade, CFC). It was common for

both agencies to handle the same matters in distinct ways.

Thus, within the setting of international convergence of accounting norms and facing the diversity of

current standards and regulatory inspection bodies operating in the country, an internal restructure became

paramount in order to facilitate adaptation to the International Accounting Standards (IAS).

This process began in Brazil in 2000, when Bill 3.741 was submitted to the Chamber of Deputies,

proposing the modernization of Law 6404/76, through an update in its Chapter 15, aiming the elimination of

regulatory barriers and the alignment of Brazilian norms and accounting practices to their international ones

(Farah et al., 2010).

Afterwards, in 2005, the CPC was created through CFC Resolution 1055/05, with its aim defined as:

3 Brazil Law No. 6404 of December 15, 1976 (and amendments). Provides for the corporations. Official Gazette, Brasília, DF, December 17, 1976. Retrieved from http://www.planalto.gov.br/ccivil03/Leis/L6404consol.htm.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

590

The study, preparation and issuance of technical pronouncements for accounting procedures, and disclosure of information, to allow the issuance of norms by the Brazilian regulatory body, aiming the centralization and standardization of its production process, always considering the convergence of Brazilian accounting with international standards. (Federal Accounting Council, 2005)4

Bill 3.741 was approved in December 2007, originating Law 11.638/07 which determined that all

applicable norms to Brazilian public companies should be formulated in line with the international standards

used in the main securities markets. It also allowed its application to large companies. Even before Bill 3.741

was transformed into law, the CVM had already ruled, through Normative Instruction 457/07, that public

companies would have to submit their financial statements in accordance with IASB regulations by the end of

2010. This Instruction also ruled that international norms should be applied to the statements of the previous

year, so as to allow a comparison. Later, in November 2010, the CPC issued Statement 37, approved by the

CVM (Deliberation 647/10), reinforcing in its Item 34 the mandatory use of the IFRS in accounting statements

as of fiscal year of 2010.

The convergence to international standards imposes, however, a few challenges for Brazilian accounting,

as highlighted by Farah et al. (2010):

We can immediately see a fundamental conceptual barrier to the understanding, acceptance, and practical application of the IFRS in Brazil: the Brazilian accounting system, which has always suffered great influence from the fiscal environment, is strongly based on definite rules, whereas the IFRS have been traditionally based on much less detailed principles, with great emphasis on the economic substance of the operations, and on the use of judgment. (p. 22)

As for fiscal interference in the generation of accounting information, the changes to Law 6.404/76

progress to minimize the problem, for Item 2 of Article 177 determines that the company’s bookkeeping shall

not be modified by the provisions of tax law which must be registered in ledgers.

According to Iudicibus (2000, p. 28), “The main aim of accounting (and the reports emanating from it) is

to provide relevant economic information so that each user can make their own decisions, and safely carry out

their judgments”. Thus, the role of accounting is to provide information to various users, both inside and

outside the company.

According to Niyama and Silva (2009):

The presence of the user in the accounting process makes it necessary that the information evidenced is comparable. The user needs to analyze the performance of the company, and such analysis is made through comparison with what has taken place in the company at other times, or with what happened to other companies. That is only possible when accounting proceedings are coherent amongst all companies. (pp. 1-2)

The need for a convergent accounting language emerges in a global stage where financial statement cost

and processing time reduction can represent competitive advantages to companies. According to Niyama

(2006, p. 39), “Another advantage for companies, especially for those in emerging countries in search of

resources from foreign investors, is the possibility to disclose their financial statements in understandable

language”.

Comparability of accounting information among countries is also another benefit of the convergence

process, and the basic conceptual declaration says (Accounting Pronouncement Committee [Comitê de

Pronunciamentos Contábeis—CPC], 2011):

4 Retrieved from http://www.cfc.org.br/sisweb/sre/detalhes_sre.aspx?Codigo=2005/001055.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

591

Users must be able to compare the financial statements of a company over time, so as to identify possible tendencies in its patrimonial and financial position, as well as in its performance. Users also must be able to compare financial statements of different companies in order to relatively evaluate their patrimonial and financial position, their performance, and mutations in their financial situation. Consequently, the measuring and disclosure of the financial effects of similar transactions and other eventualities must be performed consistently by the company, over time, and also by different companies. (p. 8)

This statement considers qualitative characteristics to be the attributes that make financial statements

useful for the users, such as comprehensibility, relevance, reliability, comparability, materiality, adequate

representation, primacy of substance over form, neutrality, prudence, and integrity. The first four of these

characteristics are the main ones, according to the pronouncement.

According to Choi, Frost, and Meek (1999; as cited in Lemes & Carvalho, 2009, p. 28), “Information is

comparable if it is similar enough to allow users to compare it without having to be intimately familiar with

more than one accounting system”.

Haverty (2006) has researched comparability and convergence of two sets of accounting norms (US

GAAP and IFRS) between 1996 and 2002. For that, he used a sample of 11 companies of the Republic of

China listed on the New York Stock Exchange (NYSE). During his research, the author used the Gray Index (or

comparability) to verify the comparability between the net profit (Lucro Líquido, LL) and the equity

(Patrimônio Líquido, PL) in the two groups of norms. As a result, he could verify that notwithstanding the

progress towards harmonization, no real convergence took place, and the main reason for the lack of

comparability was the revaluation of fixed assets. While the IFRS allows revaluation, the US GAAP only

allows the evaluation of fixed assets through their historical costs.

Nogueira and Lemes (2008) have carried out a research about the level of comparability of the adjustments

to the LL and PL of 28 Brazilian companies that issued American Depositary Receipts (ADRs) in 2006. The

comparison was made between BR GAAP and US GAAP from 2000 to 2006, and the adjustments concerning

business combination, intangibles, goodwill, fixed assets, pension funds, monetary correction, and deferred

taxes were the main reasons of the conflicts. In this study, the use of a variable of the Gray Index allowed them

to identify the incomparability of the partial adjustments issued by the companies, and it was proved that there

was no comparability improvement during the time of the analysis.

Liu (2011) also used the Gray Index to identify the causes of comparability differences between 15

Chinese companies that used the IFRS and performed information reconciliation in US GAAP from 2002 to

2006. The study pointed out the following as main differences: deferred taxes, exchange adjustments, goodwill,

asset revaluation, minority interest, and business combinations and acquisitions.

Aiming to evaluate the differences between the net income in BR GAAP and US GAAP, Lemes and

Carvalho (2009) have applied the same index in 30 companies between 2000 and 2005. They concluded that an

expressive number of companies showed materially incomparable results, identifying the adjustments resulting

from goodwill and business combination as the most frequent in the companies in the sample.

Another similar study has been carried out by Klann and Beuren (2010), in which 33 enterprises listed on

the London Stock Exchange (LSE) that negotiate ADR on the NYSE, using their financial statements for 2004

and 2005 as reference, disclosed to the LSE and the NYSE. Their work analyzed the reflexes of the differences

between the norms of the IFRS and US GAAP, in accounting disclosure, through the identification of the main

adjustments to the accounts of the balance sheet, operational profit, and the net income of the yearly income

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

592

statement. No comparability index was used for this study. Instead, they opted to identify the relative variations

between one standard and the other. The goodwill and the benefit plan for employees were identified as the

main causes of the accounting information asymmetry.

Previous reports highlight adjustments to goodwill as one of the main reasons for the incomparability of

information collected in different standards, as identified in all studies quoted, followed by those related to

business combinations which appear in three of the studies and the deferred taxes mentioned in two of them.

Methodological Aspects

This research was descriptive. One of its goals is the description of the characteristics of a given

population or phenomenon, using the technique of data collection (Gil, 2006; Beuren, 2006). According to

methodological procedures, this study is a documentary research. As for the approach to the problem, this is a

quantitative article, because, according to Martins and Theóphilo (2007, p. 103), quantitative evaluation is “to

organize, summarize, characterize, and interpret collected numeric data”.

Data were collected through secondary sources, more specifically, from the explanatory notes in the

financial statements of the companies listed in the financial sector of the BM&F Bovespa issued in the fiscal

year of 2010.

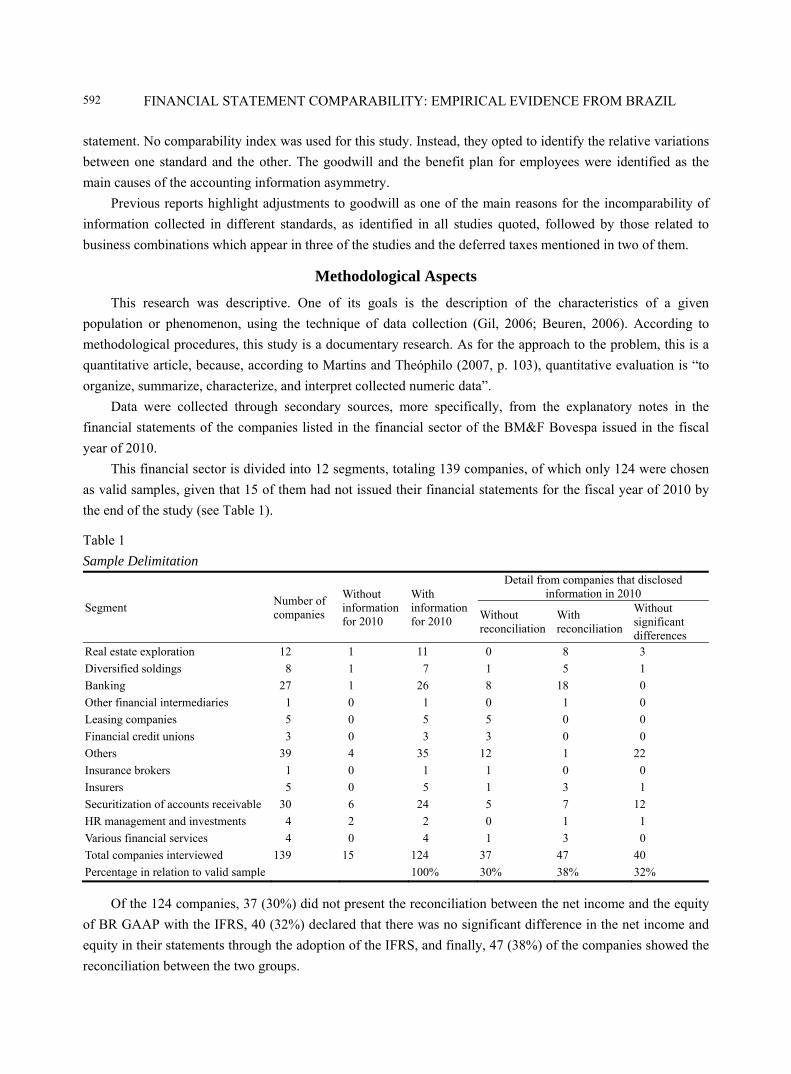

This financial sector is divided into 12 segments, totaling 139 companies, of which only 124 were chosen

as valid samples, given that 15 of them had not issued their financial statements for the fiscal year of 2010 by

the end of the study (see Table 1).

Table 1

Sample Delimitation

Segment Number of companies

Without information for 2010

With information for 2010

Detail from companies that disclosed information in 2010

Without reconciliation

With reconciliation

Without significant differences

Real estate exploration 12 1 11 0 8 3

Diversified soldings 8 1 7 1 5 1

Banking 27 1 26 8 18 0

Other financial intermediaries 1 0 1 0 1 0

Leasing companies 5 0 5 5 0 0

Financial credit unions 3 0 3 3 0 0

Others 39 4 35 12 1 22

Insurance brokers 1 0 1 1 0 0

Insurers 5 0 5 1 3 1

Securitization of accounts receivable 30 6 24 5 7 12

HR management and investments 4 2 2 0 1 1

Various financial services 4 0 4 1 3 0

Total companies interviewed 139 15 124 37 47 40

Percentage in relation to valid sample 100% 30% 38% 32%

Of the 124 companies, 37 (30%) did not present the reconciliation between the net income and the equity

of BR GAAP with the IFRS, 40 (32%) declared that there was no significant difference in the net income and

equity in their statements through the adoption of the IFRS, and finally, 47 (38%) of the companies showed the

reconciliation between the two groups.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

593

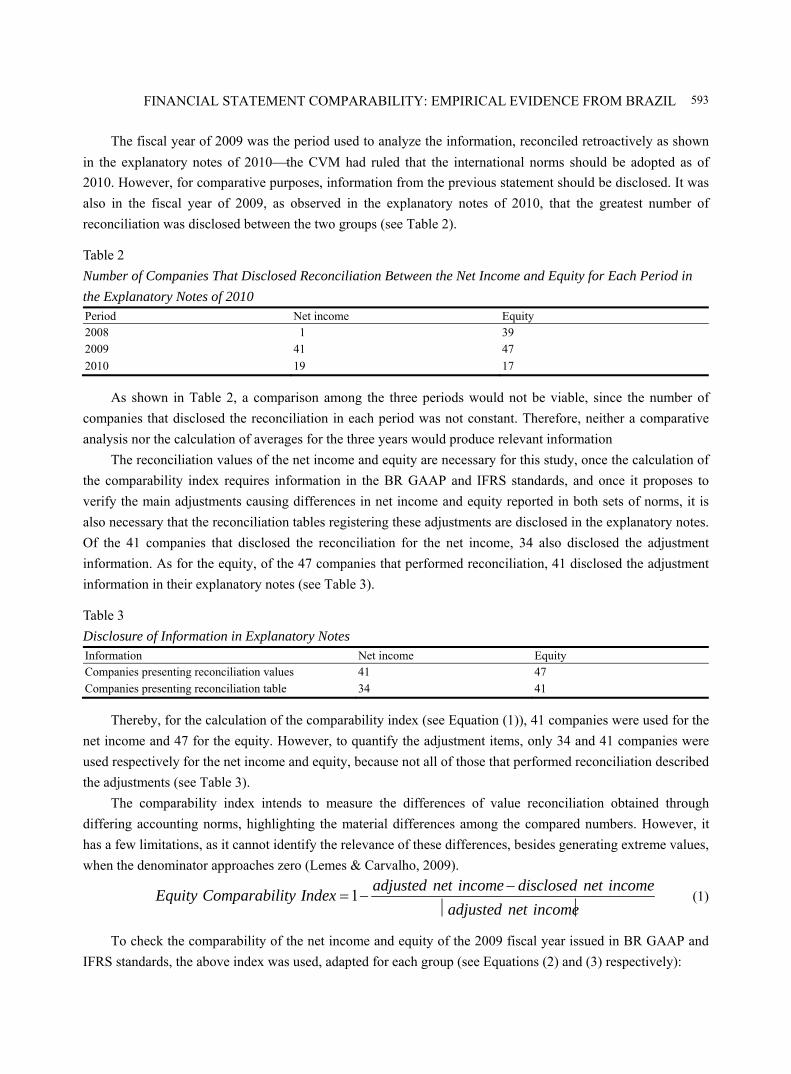

The fiscal year of 2009 was the period used to analyze the information, reconciled retroactively as shown

in the explanatory notes of 2010⎯the CVM had ruled that the international norms should be adopted as of

2010. However, for comparative purposes, information from the previous statement should be disclosed. It was

also in the fiscal year of 2009, as observed in the explanatory notes of 2010, that the greatest number of

reconciliation was disclosed between the two groups (see Table 2).

Table 2

Number of Companies That Disclosed Reconciliation Between the Net Income and Equity for Each Period in

the Explanatory Notes of 2010 Period Net income Equity 2008 1 39

2009 41 47

2010 19 17

As shown in Table 2, a comparison among the three periods would not be viable, since the number of

companies that disclosed the reconciliation in each period was not constant. Therefore, neither a comparative

analysis nor the calculation of averages for the three years would produce relevant information

The reconciliation values of the net income and equity are necessary for this study, once the calculation of

the comparability index requires information in the BR GAAP and IFRS standards, and once it proposes to

verify the main adjustments causing differences in net income and equity reported in both sets of norms, it is

also necessary that the reconciliation tables registering these adjustments are disclosed in the explanatory notes.

Of the 41 companies that disclosed the reconciliation for the net income, 34 also disclosed the adjustment

information. As for the equity, of the 47 companies that performed reconciliation, 41 disclosed the adjustment

information in their explanatory notes (see Table 3).

Table 3

Disclosure of Information in Explanatory Notes Information Net income Equity Companies presenting reconciliation values 41 47

Companies presenting reconciliation table 34 41

Thereby, for the calculation of the comparability index (see Equation (1)), 41 companies were used for the

net income and 47 for the equity. However, to quantify the adjustment items, only 34 and 41 companies were

used respectively for the net income and equity, because not all of those that performed reconciliation described

the adjustments (see Table 3).

The comparability index intends to measure the differences of value reconciliation obtained through

differing accounting norms, highlighting the material differences among the compared numbers. However, it

has a few limitations, as it cannot identify the relevance of these differences, besides generating extreme values,

when the denominator approaches zero (Lemes & Carvalho, 2009).

1

adjusted net income disclosed net incomeEquity Comparability Index

adjusted net income

−= −

⏐ ⏐ (1)

To check the comparability of the net income and equity of the 2009 fiscal year issued in BR GAAP and

IFRS standards, the above index was used, adapted for each group (see Equations (2) and (3) respectively):

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

594

1

IFRS BRGAAP

IFRS

net income net incomeNet Income Comparability Index

net income

−= −

⏐ ⏐ (2)

1 IFRS BRGAAP

IFRS

equity equityEquity Comparability Index

equity

−= −

⏐ ⏐ (3)

Much like the studies of Nogueira and Lemes (2008) and Lemes and Carvalho (2009) who compared

information in BR GAAP and US GAAP, an index result greater than one means that the net income (or equity)

determined according to Brazilian norms is greater than the one shown in IFRS or, similarly, the net income (or

equity) less than one in BR GAAP is less than the one found in IFRS, whereas an index equaling to one

indicates neutrality, in effect, that the compared numbers are identical, which, in a temporal analysis, allows

identification of their approximation, and therefore, the verification of their possible convergence.

“This indicator allows identification of the normalization process of the gaps between the two values”

(Lemes & Carvalho, 2009, p. 38) and, in relation to the greater or lesser proximity to neutrality, in some studies,

the adoption of materiality tracks which are intervals in which the indicator is classified, in order to establish

the relevance of comparability. Although there is no consensus as far as the acceptable limits, the percentages

of 5% and 10% are mostly used in studies, meaning that, when the comparability index is located away from

neutrality in 5% (from 0.95 to 1.05) or 10% (from 0.90 to 1.10), the analyzed values are considered comparable

to 5% or 10% materiality respectively (Haverty, 2006).

Thus, after the comparability indices were calculated for the net income (see Equation (3)) and the equity

(see Equation (4)), they were classified into the materiality tracks, using the intervals from 0.95 to 1.05 (5%

materiality) and from 0.90 to 1.10 (10% materiality). Then, the adjustments that contributed to the main

resulting differences were identified, according to the two norms.

Result Analysis

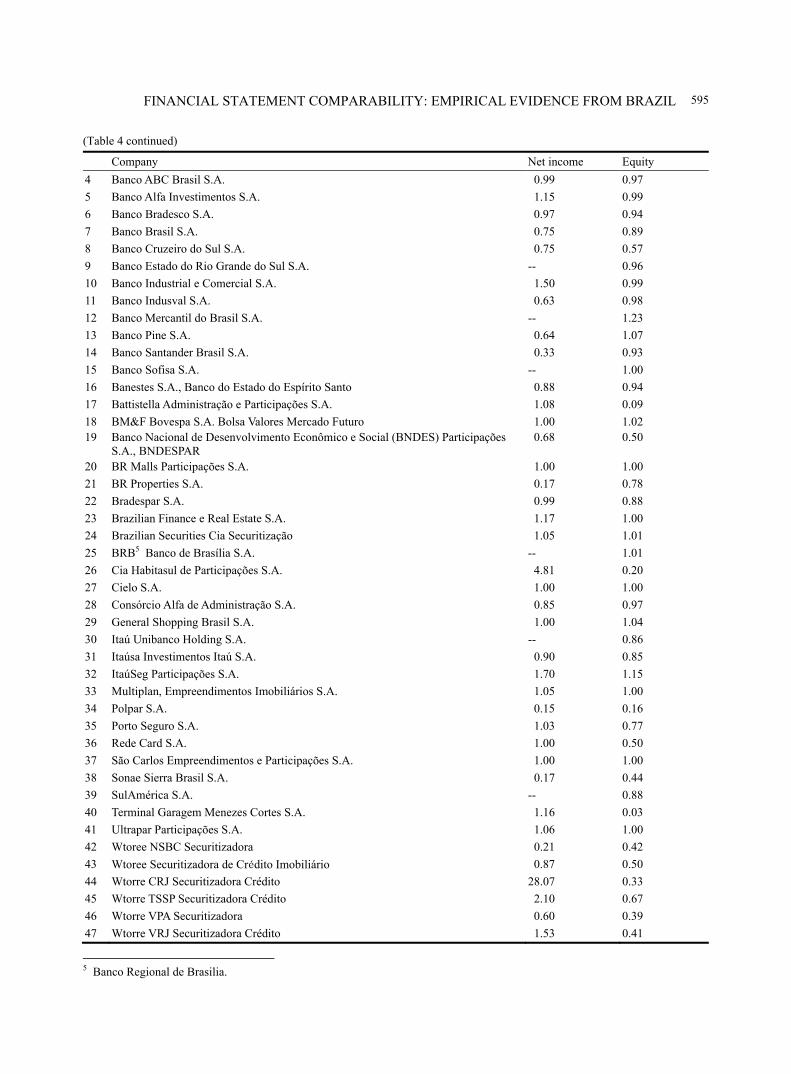

Table 4 shows that, of the 47 studied companies, three (BR Malls Participações S.A., São Carlos

Empreendimentos e Participações S.A., and Cielo S.A.) presented a result for the Gray Index equaling to one,

not only for the net income but also for the equity, which corresponds to 6% of the total. BM&F Bovespa,

General Shopping Brazil S.A., and Rede Card S.A. (7%) obtained the same index only for the net income, and

finally, the resulting index for Multiplan, Empreendimentos Imobiliários S.A., Ultrapar Participações S.A.,

Banco Sofina S.A., and Brazilian Finance e Real Estate S.A. (9%) was also equal to one, but only for the

equity.

Of the three companies with identical results for the net income, according to the two norms, only Rede

Card registered a greater distance from neutrality for the equity (0.50), while the results for the equity indices to

BM&F Bovespa and General Shopping Brazil S.A. were closer to neutrality (1.02 and 1.04 respectively, see

Table 4).

Table 4

Net Income and Equity Comparability Indices

Company Net income Equity

1 Alfa Holdings S.A. 0.86 0.98

2 Alliance Shopping Centers S.A. 0.88 0.92

3 Andrade Gutierrez Participações S.A. 0.13 0.81

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

595

(Table 4 continued)

Company Net income Equity

4 Banco ABC Brasil S.A. 0.99 0.97

5 Banco Alfa Investimentos S.A. 1.15 0.99

6 Banco Bradesco S.A. 0.97 0.94

7 Banco Brasil S.A. 0.75 0.89

8 Banco Cruzeiro do Sul S.A. 0.75 0.57

9 Banco Estado do Rio Grande do Sul S.A. -- 0.96

10 Banco Industrial e Comercial S.A. 1.50 0.99

11 Banco Indusval S.A. 0.63 0.98

12 Banco Mercantil do Brasil S.A. -- 1.23

13 Banco Pine S.A. 0.64 1.07

14 Banco Santander Brasil S.A. 0.33 0.93

15 Banco Sofisa S.A. -- 1.00

16 Banestes S.A., Banco do Estado do Espírito Santo 0.88 0.94

17 Battistella Administração e Participações S.A. 1.08 0.09

18 BM&F Bovespa S.A. Bolsa Valores Mercado Futuro 1.00 1.02 19

Banco Nacional de Desenvolvimento Econômico e Social (BNDES) Participações S.A., BNDESPAR

0.68

0.50

20 BR Malls Participações S.A. 1.00 1.00

21 BR Properties S.A. 0.17 0.78

22 Bradespar S.A. 0.99 0.88

23 Brazilian Finance e Real Estate S.A. 1.17 1.00

24 Brazilian Securities Cia Securitização 1.05 1.01

25 BRB5 Banco de Brasília S.A. -- 1.01

26 Cia Habitasul de Participações S.A. 4.81 0.20

27 Cielo S.A. 1.00 1.00

28 Consórcio Alfa de Administração S.A. 0.85 0.97

29 General Shopping Brasil S.A. 1.00 1.04

30 Itaú Unibanco Holding S.A. -- 0.86

31 Itaúsa Investimentos Itaú S.A. 0.90 0.85

32 ItaúSeg Participações S.A. 1.70 1.15

33 Multiplan, Empreendimentos Imobiliários S.A. 1.05 1.00

34 Polpar S.A. 0.15 0.16

35 Porto Seguro S.A. 1.03 0.77

36 Rede Card S.A. 1.00 0.50

37 São Carlos Empreendimentos e Participações S.A. 1.00 1.00

38 Sonae Sierra Brasil S.A. 0.17 0.44

39 SulAmérica S.A. -- 0.88

40 Terminal Garagem Menezes Cortes S.A. 1.16 0.03

41 Ultrapar Participações S.A. 1.06 1.00

42 Wtoree NSBC Securitizadora 0.21 0.42

43 Wtoree Securitizadora de Crédito Imobiliário 0.87 0.50

44 Wtorre CRJ Securitizadora Crédito 28.07 0.33

45 Wtorre TSSP Securitizadora Crédito 2.10 0.67

46 Wtorre VPA Securitizadora 0.60 0.39

47 Wtorre VRJ Securitizadora Crédito 1.53 0.41

5 Banco Regional de Brasilia.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

596

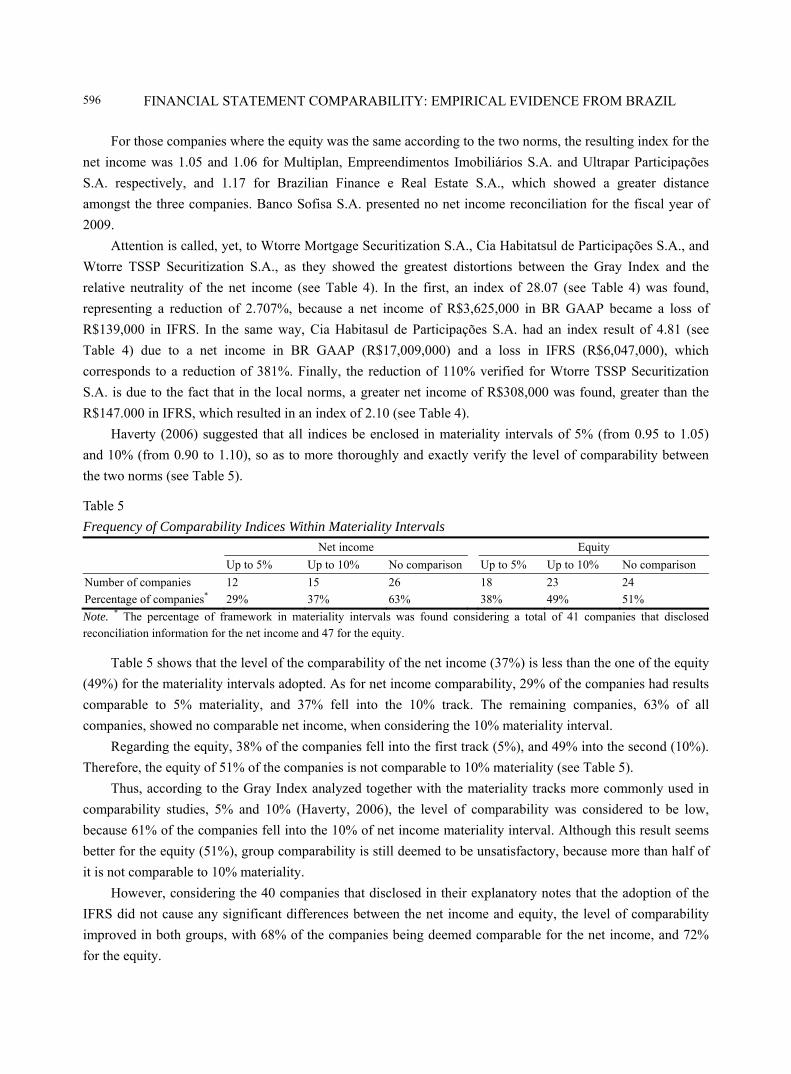

For those companies where the equity was the same according to the two norms, the resulting index for the

net income was 1.05 and 1.06 for Multiplan, Empreendimentos Imobiliários S.A. and Ultrapar Participações

S.A. respectively, and 1.17 for Brazilian Finance e Real Estate S.A., which showed a greater distance

amongst the three companies. Banco Sofisa S.A. presented no net income reconciliation for the fiscal year of

2009.

Attention is called, yet, to Wtorre Mortgage Securitization S.A., Cia Habitatsul de Participações S.A., and

Wtorre TSSP Securitization S.A., as they showed the greatest distortions between the Gray Index and the

relative neutrality of the net income (see Table 4). In the first, an index of 28.07 (see Table 4) was found,

representing a reduction of 2.707%, because a net income of R$3,625,000 in BR GAAP became a loss of

R$139,000 in IFRS. In the same way, Cia Habitasul de Participações S.A. had an index result of 4.81 (see

Table 4) due to a net income in BR GAAP (R$17,009,000) and a loss in IFRS (R$6,047,000), which

corresponds to a reduction of 381%. Finally, the reduction of 110% verified for Wtorre TSSP Securitization

S.A. is due to the fact that in the local norms, a greater net income of R$308,000 was found, greater than the

R$147.000 in IFRS, which resulted in an index of 2.10 (see Table 4).

Haverty (2006) suggested that all indices be enclosed in materiality intervals of 5% (from 0.95 to 1.05)

and 10% (from 0.90 to 1.10), so as to more thoroughly and exactly verify the level of comparability between

the two norms (see Table 5).

Table 5

Frequency of Comparability Indices Within Materiality Intervals

Net income Equity

Up to 5% Up to 10% No comparison Up to 5% Up to 10% No comparison

Number of companies 12 15 26 18 23 24

Percentage of companies* 29% 37% 63% 38% 49% 51%

Note. * The percentage of framework in materiality intervals was found considering a total of 41 companies that disclosed reconciliation information for the net income and 47 for the equity.

Table 5 shows that the level of the comparability of the net income (37%) is less than the one of the equity

(49%) for the materiality intervals adopted. As for net income comparability, 29% of the companies had results

comparable to 5% materiality, and 37% fell into the 10% track. The remaining companies, 63% of all

companies, showed no comparable net income, when considering the 10% materiality interval.

Regarding the equity, 38% of the companies fell into the first track (5%), and 49% into the second (10%).

Therefore, the equity of 51% of the companies is not comparable to 10% materiality (see Table 5).

Thus, according to the Gray Index analyzed together with the materiality tracks more commonly used in

comparability studies, 5% and 10% (Haverty, 2006), the level of comparability was considered to be low,

because 61% of the companies fell into the 10% of net income materiality interval. Although this result seems

better for the equity (51%), group comparability is still deemed to be unsatisfactory, because more than half of

it is not comparable to 10% materiality.

However, considering the 40 companies that disclosed in their explanatory notes that the adoption of the

IFRS did not cause any significant differences between the net income and equity, the level of comparability

improved in both groups, with 68% of the companies being deemed comparable for the net income, and 72%

for the equity.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

597

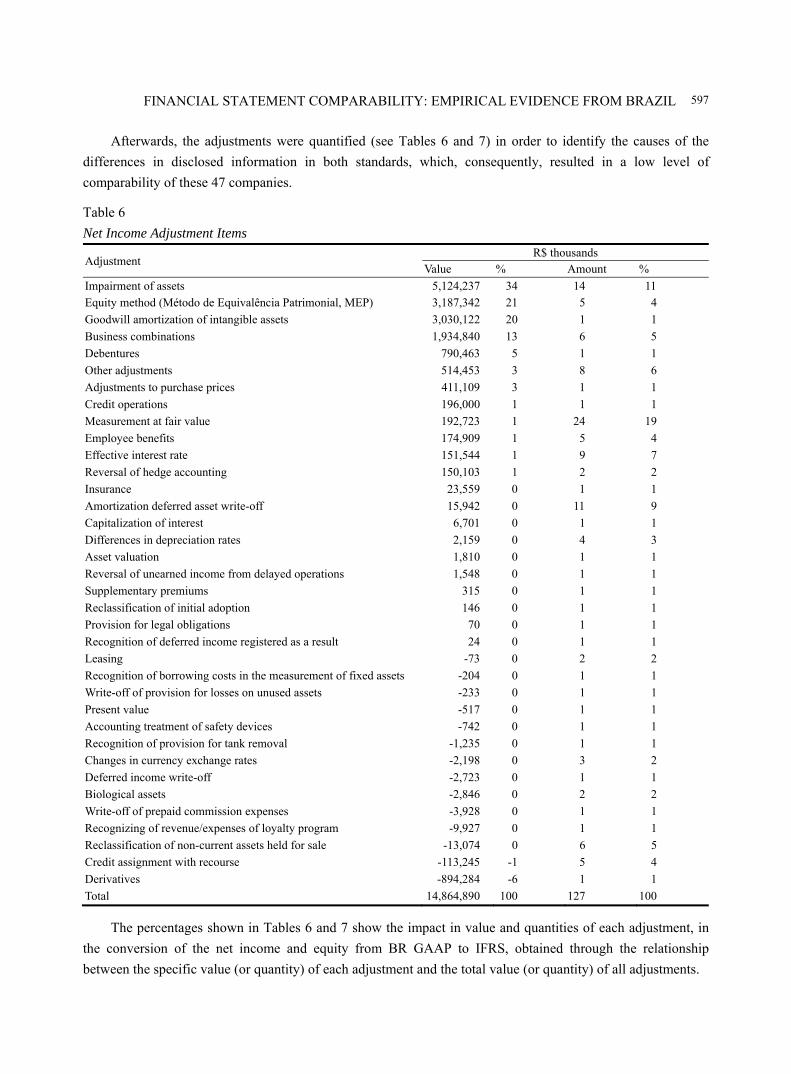

Afterwards, the adjustments were quantified (see Tables 6 and 7) in order to identify the causes of the

differences in disclosed information in both standards, which, consequently, resulted in a low level of

comparability of these 47 companies.

Table 6

Net Income Adjustment Items

Adjustment R$ thousands

Value % Amount %

Impairment of assets 5,124,237 34 14 11

Equity method (Método de Equivalência Patrimonial, MEP) 3,187,342 21 5 4

Goodwill amortization of intangible assets 3,030,122 20 1 1

Business combinations 1,934,840 13 6 5

Debentures 790,463 5 1 1

Other adjustments 514,453 3 8 6

Adjustments to purchase prices 411,109 3 1 1

Credit operations 196,000 1 1 1

Measurement at fair value 192,723 1 24 19

Employee benefits 174,909 1 5 4

Effective interest rate 151,544 1 9 7

Reversal of hedge accounting 150,103 1 2 2

Insurance 23,559 0 1 1

Amortization deferred asset write-off 15,942 0 11 9

Capitalization of interest 6,701 0 1 1

Differences in depreciation rates 2,159 0 4 3

Asset valuation 1,810 0 1 1

Reversal of unearned income from delayed operations 1,548 0 1 1

Supplementary premiums 315 0 1 1

Reclassification of initial adoption 146 0 1 1

Provision for legal obligations 70 0 1 1

Recognition of deferred income registered as a result 24 0 1 1

Leasing -73 0 2 2

Recognition of borrowing costs in the measurement of fixed assets -204 0 1 1

Write-off of provision for losses on unused assets -233 0 1 1

Present value -517 0 1 1

Accounting treatment of safety devices -742 0 1 1

Recognition of provision for tank removal -1,235 0 1 1

Changes in currency exchange rates -2,198 0 3 2

Deferred income write-off -2,723 0 1 1

Biological assets -2,846 0 2 2

Write-off of prepaid commission expenses -3,928 0 1 1

Recognizing of revenue/expenses of loyalty program -9,927 0 1 1

Reclassification of non-current assets held for sale -13,074 0 6 5

Credit assignment with recourse -113,245 -1 5 4

Derivatives -894,284 -6 1 1

Total 14,864,890 100 127 100

The percentages shown in Tables 6 and 7 show the impact in value and quantities of each adjustment, in

the conversion of the net income and equity from BR GAAP to IFRS, obtained through the relationship

between the specific value (or quantity) of each adjustment and the total value (or quantity) of all adjustments.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

598

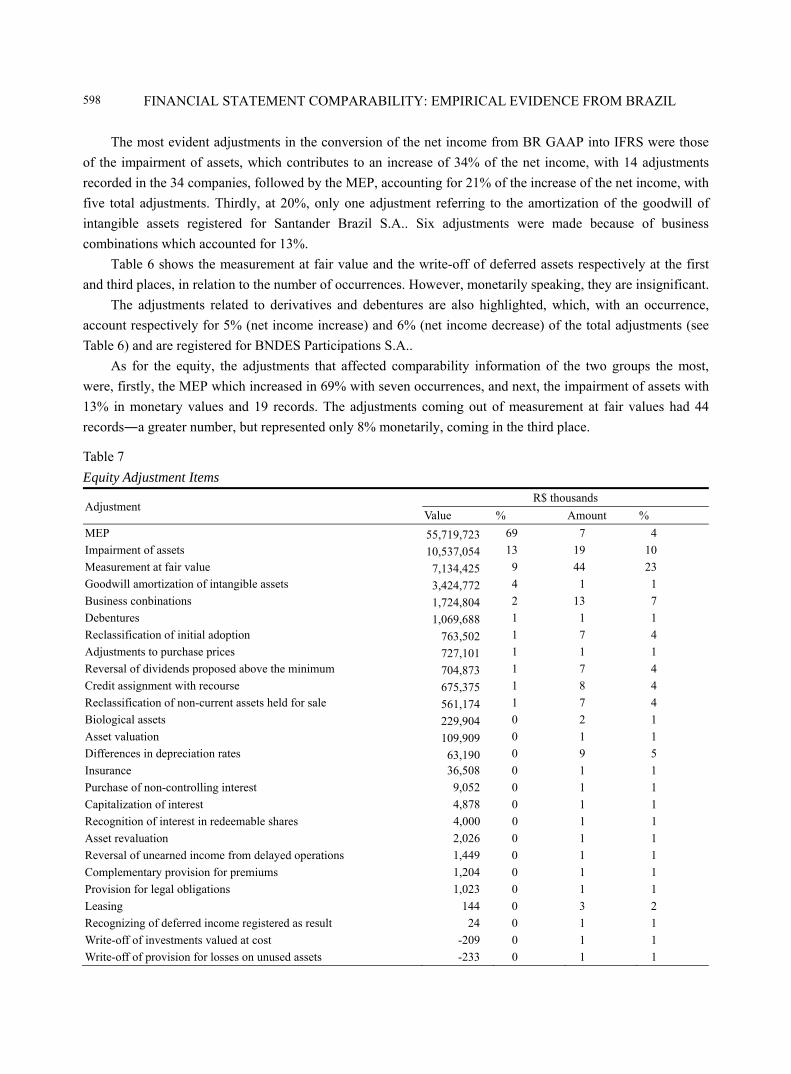

The most evident adjustments in the conversion of the net income from BR GAAP into IFRS were those

of the impairment of assets, which contributes to an increase of 34% of the net income, with 14 adjustments

recorded in the 34 companies, followed by the MEP, accounting for 21% of the increase of the net income, with

five total adjustments. Thirdly, at 20%, only one adjustment referring to the amortization of the goodwill of

intangible assets registered for Santander Brazil S.A.. Six adjustments were made because of business

combinations which accounted for 13%.

Table 6 shows the measurement at fair value and the write-off of deferred assets respectively at the first

and third places, in relation to the number of occurrences. However, monetarily speaking, they are insignificant.

The adjustments related to derivatives and debentures are also highlighted, which, with an occurrence,

account respectively for 5% (net income increase) and 6% (net income decrease) of the total adjustments (see

Table 6) and are registered for BNDES Participations S.A..

As for the equity, the adjustments that affected comparability information of the two groups the most,

were, firstly, the MEP which increased in 69% with seven occurrences, and next, the impairment of assets with

13% in monetary values and 19 records. The adjustments coming out of measurement at fair values had 44

records―a greater number, but represented only 8% monetarily, coming in the third place.

Table 7

Equity Adjustment Items

Adjustment R$ thousands

Value % Amount %

MEP 55,719,723 69 7 4

Impairment of assets 10,537,054 13 19 10

Measurement at fair value 7,134,425 9 44 23

Goodwill amortization of intangible assets 3,424,772 4 1 1

Business conbinations 1,724,804 2 13 7

Debentures 1,069,688 1 1 1

Reclassification of initial adoption 763,502 1 7 4

Adjustments to purchase prices 727,101 1 1 1

Reversal of dividends proposed above the minimum 704,873 1 7 4

Credit assignment with recourse 675,375 1 8 4

Reclassification of non-current assets held for sale 561,174 1 7 4

Biological assets 229,904 0 2 1

Asset valuation 109,909 0 1 1

Differences in depreciation rates 63,190 0 9 5

Insurance 36,508 0 1 1

Purchase of non-controlling interest 9,052 0 1 1

Capitalization of interest 4,878 0 1 1

Recognition of interest in redeemable shares 4,000 0 1 1

Asset revaluation 2,026 0 1 1

Reversal of unearned income from delayed operations 1,449 0 1 1

Complementary provision for premiums 1,204 0 1 1

Provision for legal obligations 1,023 0 1 1

Leasing 144 0 3 2

Recognizing of deferred income registered as result 24 0 1 1

Write-off of investments valued at cost -209 0 1 1

Write-off of provision for losses on unused assets -233 0 1 1

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

599

(Table 7 continued)

Adjustment R$ thousands

Value % Amount %

Present value -452 0 1 1

Provision for asset retirement -2,000 0 1 1

Changes in currency exchange rates -2,775 0 2 1

Write-off of prepaid commission expenses -4,303 0 1 1

Deferred income write-off -8,427 0 1 1

Recognizing of revenue/expenses of loyalty program -9,927 0 1 1

Recognition of borrowing costs in the measurement of fixed assets -12,802 0 1 1 Contribution to business service management (BSM) establishment, treated as investment

-20,000 0

1

1

Recognition of provision for tank removal -38,008 0 1 1

Write-off of deferred assets -78,092 0 11 6

Financial assets available for sale -179,000 0 1 1

Effective interest rates -230,228 0 10 5

Other adjustments -261,707 0 8 4

Employee benefits -836,667 -1 9 5

Derivatives -894,284 -1 1 1

Total 80,926,688 100 191 100

Business combinations were registered 13 times in the equity adjustments, but with a rather insignificant

value (see Table 7), different from the impact it had on the net income, with lower registered occurrences, but

with more relevant values (see Table 6).

Deferred asset write-off and effective interest rate appear 11 and 10 times respectively, but with a less

representative impact on the equity, in monetary terms (see Table 7).

The item, business combinations, which was pointed out by Nogueira and Lemes (2008), Lemes and

Carvalho (2009), and Liu (2011) as one of the causes for incomparability, was also verified in the adjustments

of both the net income and the equity of the 47 companies on the financial sector.

Goodwill, highlighted as one of the main causes of different information found in the various sets of

norms (Nogueira & Lemes, 2008; Liu, 2011; Lemes & Carvalho, 2009; Klann & Beuren, 2010), was not clearly

identified in the adjustments of the companies that presented explanatory notes with reconciliation information

for the net income and equity. Goodwill amortization of intangible assets recorded by Santander Brazil S.A.

may include adjustments for both goodwill and business combinations, but they do not present the two items

separately.

Adjustments for asset revaluation (Haverty, 2006; Liu, 2011), intangibles (Nogueira & Lemes, 2008), and

employee benefits (Nogueira & Lemes, 2008; Klan & Beuren, 2010), identified as relevant in this study,

occurred unobtrusively in the companies studied.

The adjustments resulting from MEP, one of the most significant in the conversion of the net income and

equity, and the reversal of dividends proposed above the minimum (with seven occurrences, totaling 1% of the

total value of adjustments in the equity), correspond to differences that continue to be identified in next periods,

according to the two sets of standards, because there is no convergence in treating these items.

Finally, deferred tax adjustments amounted 29 and contributed to the reduction of the net income

from BR GAAP to IFRS by R$4,303,124. As for the equity, 33 adjustments took place, and the adoption of the

IFRS reduced this group by R$22,673,421. However, deferred taxes were excluded from the adjustment items,

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

600

so that the real magnitude of the impact of the other adjustments on the net income and the equity could be

verified, given that a few companies disclosed the net tax adjustments. Additionally, the item is often treated as

an adjustment, but practically, it only refers to the recalculation of taxes on the differences identified.

Closing Remarks

In the Brazilian scenario of convergence to IAS, the purpose of this study is to assess the level of

comparability of the net income and equity in companies listed in the financial sector of BM&F Bovespa,

commonly excluded from other studies because of its peculiarities.

The level of comparability was considered reasonable, because, analyzing the 40 companies that reported

not having found significant differences with the adoption of the IFRS, plus the 47 that presented reconciliation,

(41 of them for the net income), 68% of them had their information materially comparable to the net income

and 72% to the equity.

Although the percentage of companies that present comparable net income and equity is around 70%, it is

possible that decisions made based on the information disclosed by the two sets of norms are influenced by

information asymmetry. In effect, net income and equity comparability were not satisfactory for the companies

within the period studied.

The adjustments that most stood out in monetary terms were both for the net income and the equity,

monetarily speaking, the impairment of assets (34% for the net income and 13% for the equity), the MEP (21%

for the net income and 69% for the equity), business combinations followed with 13% for the net income, along

with measurement at fair value, with 9% for the equity. The measuring at fair value (24 records) appears in

greater numbers in the reconciliation of the net income, and the deferred income write-off (11 records) takes the

third place; however, both are irrelevant in terms of monetary value. In the case of the equity, business

combinations (13 records), write-off of deferred assets (11 records), and effective interest rates (10 records) are

significantly recorded, but are negligible in value.

Adjustments for the MEP and reversal of dividends proposed above the minimum are worth noting and

will continue to be identified in next periods, because both sets of norms are not convergent for the two items.

The main challenges in the course of this study were data collection and selection for developing the

research because of: (1) inconsistence in net income and equity reconciliation criteria in the companies

investigated; and (2) lack of uniformity in the designation of the adjustments that affect the net income and

equity in the conversion of the BR GAAP standard into the IFRS.

Regarding the lack of criteria consistency, there is the fact that some companies reported only the numbers

of the net income and equity according to the two standards, without detailing, in the explanatory notes or

reconciliation tables, the adjustments that caused the differences, as from the 47 companies that reconciled net

income and equity values, 34 presented adjustments for the net income and 41 for the equity.

Concerning the designation of the adjustments in the reconciliation disclosed in the explanatory notes, it

can be seen that various names were used for one single type of transaction, which damaged the uniformity of

information.

Because these research results are only applicable to the companies in the sector studied, it is suggested

that further work be carried out to study other sectors, aiming to analyze the comparability behaviors among

different sectors and that other aspects of the qualitative characteristics of the information be evaluated, because,

although this work proposes to study comparability, it detects deficiencies in other qualitative characteristics of

accounting information, such as in comprehensibility, adequate representation, and integrity.

FINANCIAL STATEMENT COMPARABILITY: EMPIRICAL EVIDENCE FROM BRAZIL

601

References

Accounting Pronouncement Committee [Comitê de Pronunciamentos Contábeis—CPC]. (2011). Basic conceptual pronouncement

(R1): Preparation and disclosure of accounting and financial reporting in correlation to international accounting standards—The conceptual framework for financial reporting. IASB-BV 2011 Blue Book, Brasília, Brazil, December 2, 2011. Retrieved from http://www.cpc.org.br/pdf/CPC00_R1.pdf

Beuren, I. M. (2006). Designing jobs in accounting monographics (3rd ed.). Sao Paulo: Atlas. BM&F Bovespa. (2011). A nova bolsa. Retrieved from http://www.bmfbovespa.com.br Callao, S., Jarne, J. I., & Lainez, J. A. (2007). Adoption of IFRS in Spain: Effect on the comparability. Journal of International

Accounting, Auditing, and Taxation, 16(2), 148-178.

Farah, P. L. S., Martins, E., Romani, S. R., & Lisboa, L. P. (2010). The international financial reporting standards⎯IFRS and key

similarities and differences in relation to Brazilian accounting standards and practices: introduction. In Ernest & Young and FIPECAFI, Handbook of international accounting standards: IFRS versus Brazilian standards (2nd ed.). Sao Paulo: Atlas.

Filho, J. F. R., Lopes, J., & Pederneiras, M. (2009). Studying theory of accounting. Sao Paulo: Atlas. Gil, A. C. (2206). Designing research projects (4th ed.). Sao Paulo: Atlas. Haverty, J. L. (2006). Are IFRS and US GAAP converging? Some evidence from People’s Republic of China companies listed on

the New York Stock Exchange. Journal of International Accounting, Auditing, and Taxation, 15(1), 48-71. Iudicibus, S. (2000). Accounting theory (6th ed.). Sao Paulo: Atlas. Klann, R. C., & Beuren, I. M. (2010). Reflections of differences between IFRS and US GAAP in accounting disclosure. Advances

in Scientific and Applied Accounting, 3(1), 2-240. Retrieved from http://www.asaaccount.org/ Lemes, S., & Carvalho, L. N. G. (2009). Comparability between the results in BR GAAP and US GAAP: Evidence from Brazilian

companies listed on US stock exchanges. Journal of Accounting and Finance, 20(5), 25-45. Liu, C. (2011). IFRS and US-GAAP comparability before release N. 33.8879: Some evidence from US-listed Chinese companies.

International Journal of Accounting and Information Management, 24(1), 24-33. Martins, G. A., & Theóphilo, C. R. (2007). Methodology of scientific research for applied social sciences. Sao Paulo: Atlas. Niyama, J. K. (2006). International accounting. Sao Paulo: Atlas. Niyama, J. K., & Silva, C. A. T. (2009). Theory of accounting. Sao Paulo: Atlas. Nogueira, L. M. M, & Lemes, S. (2008). Study level comparability of partial adjustments to US GAAP and GAAP. Journal of

Accounting and Organizations, 11, 19-36.

Journal of Modern Accounting and Auditing, ISSN 1548-6583 May 2013, Vol. 9, No. 5, 602-608

Can the Dominant Trait Indicator Predict Success in a Financial

Accounting Principles Course? A Preliminary Look

John Garlick South Carolina State University, South Carolina, USA

Susan Shurden Newberry College, South Carolina, USA

Mike Shurden Lander University, South Carolina, USA

The Myers Briggs Type Indicator (MBTI) test has been widely used in schools and career placement organizations

to counsel individuals into compatible career choices. The test has also been utilized in academia to enhance

instructor’s knowledge of the different learning styles and thus allows them to develop strategies to increase

students’ learning. The test is a forced-choice self-reporting exam comprised of 126 questions. Based on Jung’s

theory of personality type, the test seeks to categorize personality types into 16 discrete groups based on the four

preference poles (Myers, 1962). The poles are based on the preference for: (1) introversion (I) or extroversion (E);

(2) sensing (S) or intuition (N); (3) thinking (T) or feeling (F); and (4) judging (J) or perception (P). Laribee (1994)

studied American accounting students and found that certain personality traits were over represented in upper-level

accounting courses, while Macdaid, McCaulley, and Kainz (1986) found that the same personality trait groups

were over-represented in the profession. Oswick and Barber (1998), however, found no significant relationship

between the grade earned in an introductory accounting course and the personality traits as identified by the MBTI

with 344 UK-based accounting students. This study investigates the relationship between a student’s academic

success in a financial accounting principles course and the MBTI personality type indicators. The type distribution

of 59 historically black colleges and universities’ (HBCU) business administration majors was analyzed and

separated into two groups. The groups were then tested to determine if there was a significant difference in the

mean grade of the groups in accounting principles.

Keywords: accounting, personality, grades, introvert, extrovert

Introduction

For over 50 years, the Myers Briggs Type Indicator (MBTI) has been the most used method of measuring personality type. It is generally administered to about three million people a year. The four dimensions that are measured are:

John Garlick, Ph.D., adjunct, Department of Accounting, South Carolina State University. Susan Shurden, ABD, Department of Business, Behavioral and Social Science, Newberry College. Mike Shurden, DBA, School of Management, Lander University. Correspondence concerning this article should be addressed to Mike Shurden, DBA, School of Management, Lander University,

320 Stanley Avenue, Greenwood, SC 29649, USA. Email: [email protected].

DAVID PUBLISHING

D

SUCCESS IN A FINANCIAL ACCOUNTING PRINCIPLES COURSE

603

(1) Extroversion (E) vs. introversion (I): Indicates social relationships and whether the individual has more of an outward vs. inward orientation;

(2) Sensing (S) vs. intuition (N): Indicates whether an individual relies more on their senses or perceptions; (3) Thinking (T) vs. feeling (F): Indicates whether an individual relies more on impersonal characteristics

of cause and effect or values and beliefs to draw conclusions; (4) Judging (J) vs. perception (P): Indicates whether an individual is decisive with an inclination toward

organization or is more flexible and tolerant. After individuals take the 126-question test, they are rated as either one or the other in the above

dimensions. Their scores are then combined to categorize them as one of the 16 possible personality type combinations. For example, an individual would be of introversion, sensing, thinking, and judging (ISTJ) type, if he/she is “serious, quiet, and prefer to earn success through concentration and thoroughness” (Parkinson & Taggar, 2007, p. 55).

According to Parkman and Taggar (2007), approximately 20 studies have been published of accountants, and the revelation is that most accountants are either ISTJ or ESTJ. They went on to state that:

When faced with a decision, we (accountants) tend to be decisive and seek closure. In general, we have an aptitude for planning and organizing. When making decisions, we use the principles of cause and effect, and we tend to be impersonal. And, when we believe something, it is based on information received by our senses. The only surprise finding is that about half of us are introverts and about half are extroverts. (p. 55)

One study of Laribee (1994) gave useful knowledge about the psychological makeup of US accounting students. In his study, he indicated that in the lower-level accounting courses, students with a preference for E, N, F, and P personality types are predominant. However, in the upper-level accounting courses, students with these personality types become less numerous with S, T, and J type personalities being predominant in final-year accounting courses (Laribee, 1994). The conclusion that Oswick and Barber originally reached based on Laribee’s research was that the increase in the number of STJs to higher-level accounting courses could be attributed to more motivation and a higher ability than the NFPs. A note by this author is the fact that being extroverted or introverted in the higher-level classes is not noted. This could be explained by the finding of Parkinson and Taggar (2007) shown above which states that about half of accountants are introverts and half are extroverts.

Oswick and Barber (1998) conducted a study in which the MBTI was used to try to determine if psychology type is related to success and grade performance in introductory accounting courses. Their working hypothesis was that “The average performance of STJs on an introductory-level accounting course will be higher than the average performance for NFPs taking the same course”. The conclusion reached was that personality type had no relevance on success or grade performance in lower-level accounting courses. Additionally, the original hypothesis made by them that STJs were superior in performance was not even credible. There have been numerous studies which indicated that STJ was the most prevalent type among accountants (Shackleton, 1980; Jacoby, 1981; Otte, 1983; Kreiser, Mckeon, & Post, 1990; Scarborough, 1993). However, the overall conclusion is that it is an incorrect assumption that the STJs have outstanding ability in accounting, just because they tend to be attracted to that field (Oswick & Barber, 1998).

This study also seeks to determine if a student’s academic success in a financial accounting principles course is related to personality type as measured by the MBTI. According to Wheeler (2001), there are mixed

SUCCESS IN A FINANCIAL ACCOUNTING PRINCIPLES COURSE

604

reviews of the correlation between academic performance in accounting classes and the relationship to MBTI personality types. Another study of Nourayi and Cherry (1993) indicated a strong correlation between personality types in the SN scale and academic performance. This study differs from previous work in that the subjects are all students at a small historically black institution in the Southeastern United States.

Methodology

The MBTI exam was administered to 131 historically black colleges and universities’ (HBCU) students during a professional development class. The sample size was reduced to 52 usable student tests for this study. Excluded from this study were those students for whom complete data regarding the grade earned in financial accounting principles were not available, resulting in a total sample of 52 students. Also excluded in the study were those students who might have transferred in credits for the course from another institution, might currently be enrolled in the course, or might not have taken the course at the time the MBTI was administered. The sample was then divided into two groups, the first being those students whose MBTI tests indicated a preference for accounting (19 participants) and those whose type indicators exhibited a preference for other career paths (33 participants).

Table 1 Sample Characteristics

Description Gender (%) Major (%) Male 58 Female 42 Management 40 Marketing 34 Agribusiness 6 Accounting 12 Economics 4 Other 4

The demographics of the course are reflected in Table 1. Fifty-eight percent of the students surveyed were male, and 42% of the students were female. Marketing and management accounted for 74% of the students surveyed. Accounting majors accounted for 12% of the students.

Table 2 MBTI Results

Personality classification Percent of students (%) ISTJ 21 ENTJ 15 ESTJ 12 ISFJ 8 INFP 8 ESFJ 8 ISTP 6 ENTP 6 INTP 4 ESTP 4

SUCCESS IN A FINANCIAL ACCOUNTING PRINCIPLES COURSE

605

(Table 2 continued)

Personality classification Percent of students (%) ESFP 4 ISFP 2 ENFJ 2 INFJ 0 INTJ 0 ENFP 0

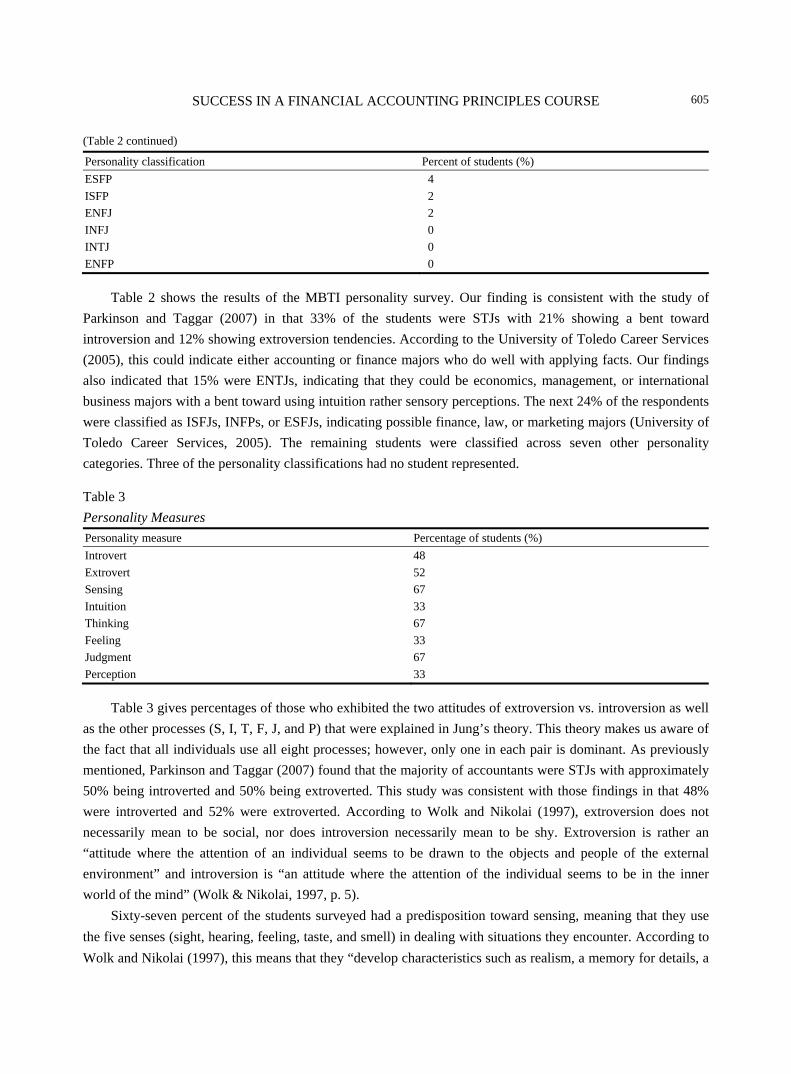

Table 2 shows the results of the MBTI personality survey. Our finding is consistent with the study of Parkinson and Taggar (2007) in that 33% of the students were STJs with 21% showing a bent toward introversion and 12% showing extroversion tendencies. According to the University of Toledo Career Services (2005), this could indicate either accounting or finance majors who do well with applying facts. Our findings also indicated that 15% were ENTJs, indicating that they could be economics, management, or international business majors with a bent toward using intuition rather sensory perceptions. The next 24% of the respondents were classified as ISFJs, INFPs, or ESFJs, indicating possible finance, law, or marketing majors (University of Toledo Career Services, 2005). The remaining students were classified across seven other personality categories. Three of the personality classifications had no student represented.

Table 3 Personality Measures

Personality measure Percentage of students (%) Introvert 48 Extrovert 52 Sensing 67 Intuition 33 Thinking 67 Feeling 33 Judgment 67 Perception 33

Table 3 gives percentages of those who exhibited the two attitudes of extroversion vs. introversion as well as the other processes (S, I, T, F, J, and P) that were explained in Jung’s theory. This theory makes us aware of the fact that all individuals use all eight processes; however, only one in each pair is dominant. As previously mentioned, Parkinson and Taggar (2007) found that the majority of accountants were STJs with approximately 50% being introverted and 50% being extroverted. This study was consistent with those findings in that 48% were introverted and 52% were extroverted. According to Wolk and Nikolai (1997), extroversion does not necessarily mean to be social, nor does introversion necessarily mean to be shy. Extroversion is rather an “attitude where the attention of an individual seems to be drawn to the objects and people of the external environment” and introversion is “an attitude where the attention of the individual seems to be in the inner world of the mind” (Wolk & Nikolai, 1997, p. 5).

Sixty-seven percent of the students surveyed had a predisposition toward sensing, meaning that they use the five senses (sight, hearing, feeling, taste, and smell) in dealing with situations they encounter. According to Wolk and Nikolai (1997), this means that they “develop characteristics such as realism, a memory for details, a

SUCCESS IN A FINANCIAL ACCOUNTING PRINCIPLES COURSE

606

keen sense of observation, and practicality” (p. 4). While 33% of the students were intuitive, meaning that they go beyond the five senses when making observations. They “often see the ‘big picture’ and develop imaginative, theoretical, abstract, and creative characteristics” (Wolk & Nikolai, 1997, p. 4).

Additionally, 67% of the students surveyed were predisposed to the process of thinking, and 33% were predisposed to feeling. Thinkers are more logical and “develop characteristics such as analytical ability objectivity, and a concern with principles of justice and fairness” (Wolk & Nikolai, 1997, p. 4). Likewise, feelers “are more likely to have an understanding of people, a concern for the human aspect of issues a capacity for compassion, and a desire for harmony” (Wolk & Nikolai, 1997, p. 4).

Finally, 67% of the students in this study dominate in the judgment process, while 33% dominate in perception. Judgment personality types are “concerned with planning operations, organizing activities, making decisions, and getting closure” (Wolk & Nikolai, 1997, p. 5). Perception personality types “prefer to see all sides of an issue and to stay open to new information and last minute options” (Wolk & Nikolai, 1997, p. 5).

Since previous studies (Shackleton, 1980; Jacoby, 1981; Otte, 1983; Kreiser et al., 1990; Scarborough, 1993) have indicated accountants to be STJs with a close to 50/50 split between extroversion and introversion tendencies, this study tends to conclude that this is indeed the case with STJs dominating with 67% in each category of sensing, thinking, and judging.

Further analysis using a chi-square test of independence was conducted to determine if there was a significant difference between ISTJ/ESTJs and the other personality classifications with regard to the grade made in a financial accounting class. One would expect that there would be a significant difference regarding grades in favor of those whose personality indicates a preference toward an accounting major. However, the authors did not find any significant difference between the grade made and the personality types. This finding is consistent with the study done by Oswick and Barber (1998) who also found no significant difference between personality type and grade performance in introductory accounting courses. Further studies need to be conducted with larger sample sizes to further investigate this hypothesis.

Conclusions

How do these conclusions impact the future of the accounting profession? Research has indicated that there has been a consistent number of STJ personality types entering and remaining in the accounting profession despite 20 years of constant changes within the profession itself. However, among different specialties and at differing levels within the firm, there are found to be more differences in personality types (Wheeler, 2001). Likewise, while Parkinson and Taggar (2007) indicated that there are a relatively equal number of extroverts to introverts, Wheeler (2001) indicated that the number of extroverts has increased. National firms would also have more extroverts than introverts.

Wolk and Nikolai (1997) suggested in their study that using the MBTI to determine personality characteristics in students might be helpful in guiding more students who have desirable personality traits to the profession. They likewise conducted a study of accounting faculty and determined that 56% are sensing and 87% are thinking, while 75% are judging. This analysis of accounting faculty likewise supports the conclusion reached by the authors of this study that accountants are dominant in the STJ processes. Therefore, a conclusion reached by the current authors would be that students with the desirable STJ traits could go on to become accounting faculty.

SUCCESS IN A FINANCIAL ACCOUNTING PRINCIPLES COURSE

607

Recommendations for Future Research

As with the recommendation by Wolk and Nikolai (1997) that accounting faculty personality should be measured with the teaching method used, this analysis would be helpful in determining if the teaching method used is effective in teaching the students. Additionally, this analysis would tie into a recommendation that students be measured on learning styles and see if one is more “suited” to certain “accounting” personality types than others. Likewise, the question arises as to whether the faculty teaching expressed a significant learning style. As Wolk and Nikolai (1997) suggested, the dynamics of classroom instruction can be measured. They went on to indicate that faculty with a predisposition toward intuition, feeling, and perceiving traits are more willing to accept innovation and changes in their teaching methods; whereas sensing, thinking, and judging traits prefer structures, rules, and situations that are not ambiguous. These accounting faculties would tend to resist changes, especially changes that lean toward solving problems from a creative stance. Likewise, this study shows that 60% of the accounting faculties are introverts and are consequently more private, tending to prefer communication that is written as opposed to having more oral communication (Wolk & Nikolai, 1997). This aspect of the nature of accounting faculty is compared with the impact that STJ accounting students have on academia. Booth and Winzar (1993, p. 114) indicated that accounting students “prefer structured learning experiences which present rules and concepts”. They additionally prefer repetition and step-by-step arguments, as well as being given appropriate feedback which includes an explanation for errors.

In summary, this paper examined the likelihood that students at a historical black college (HBC) taking a financial accounting principles course with a predisposition toward an accounting personality type based on the MBTI might have a higher grade than those who had other personality types. No significant difference was found in this case. Likewise, a conclusion was reached that the STJ personality type had a bent toward being an accounting major. Likewise, literature was examined in other cases where students and faculty had the STJ personality type, and a conclusion was reached that faculty tended to prefer the lecture method of teaching with written assignments rather than oral with little tendency toward a desire to change to more innovative teaching methods. These findings of accounting faculty create a challenge for the trend of more innovative teaching methods which have been advocated by the Accounting Education Change Commission (AECC) that in 1990 encouraged “changes in the basic accounting curriculum and explanation of teaching modalities to encourage students to ‘learn how to learn’ and to develop their critical thinking skills”. The present authors suggest further analysis as to the implementation of changes and the effect on the teaching of accounting courses and the learning of accounting students.

References Booth, P., & Winzar, H. (1993). Personality biases of accounting students: Some implications for learning style preferences.

Accounting and Finance, 33(2), 109-120. Jacoby, P. F. (1981). Psychological types and career success in the accounting profession. Research in Psychological Type, 4,

24-37. Kreiser, L., McKeon, J. M., & Post, A. (1990). A personality profile of CPAs in public practice. Ohio CPA Journal, 49(4), 29-34. Laribee, S. F. (1994). The psychological types of college accounting students. Journal of Psychological Type, 28, 37-42. Macdaid, G. P., McCaulley, M. H., & Kainz, R. (1986). Myers-Briggs type indicator: Atlas of type tables. Gainsville, FL: APT

Publications. Myers, I. B. (1962). Manual: The Myers-Briggs type indicator. Princeton, NJ: Educational Testing Service. Nourayi, M. M., & Cherry, A. C. (1993). Accounting students: Performance and personality types. Journal of Education for

Business, 69(2), 111-115.

SUCCESS IN A FINANCIAL ACCOUNTING PRINCIPLES COURSE

608

Oswick, C., & Barber, P. (1998). Personality type and performance in an introductory level accounting course: A research note. Accounting Education, 3(7), 249-254.

Otte, P. (1983). Do CPAs have a unique personality: Are certain personality types found more frequently in our profession? The Michigan CPA, 42(1), 29-36.

Parkinson, J., & Taggar, S. (2007). Earning and outgoing. Financial Management, pp. 55-56. Scarborough, D. P. (1993). Psychological types and job satisfaction of accountants. Journal of Psychological Type, 25, 3-10. Shackleton, V. (1980). The accountant stereotype: Myth or reality? Accountancy, 113(11), 122-123. University of Toledo Career Services. (2005). MBTI and major choice. Wheeler, P. (2001). The Myers-Briggs type indicator and applications to accounting education and research. Accounting

Education, 16(1), 125-150. Wolk, C., & Nikolai, L. (1997). Personality types of accounting students and faculty: Comparisons and implications. Journal of

Accounting Education, 1(15), 1-17.

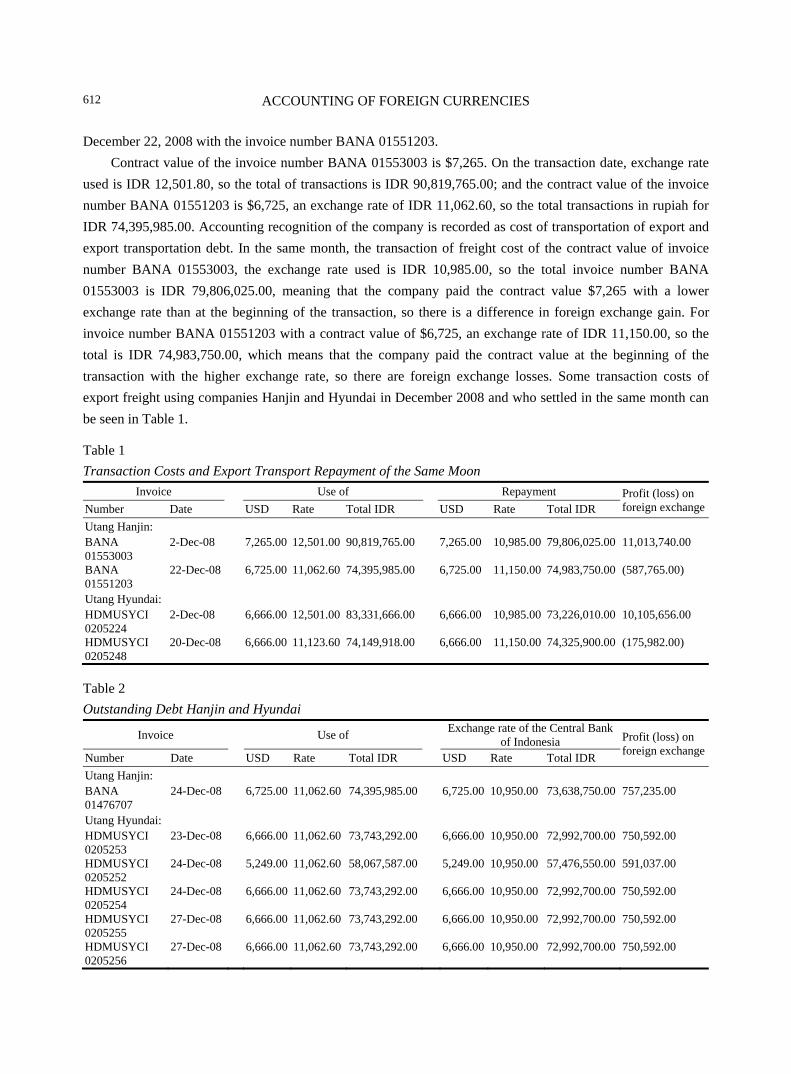

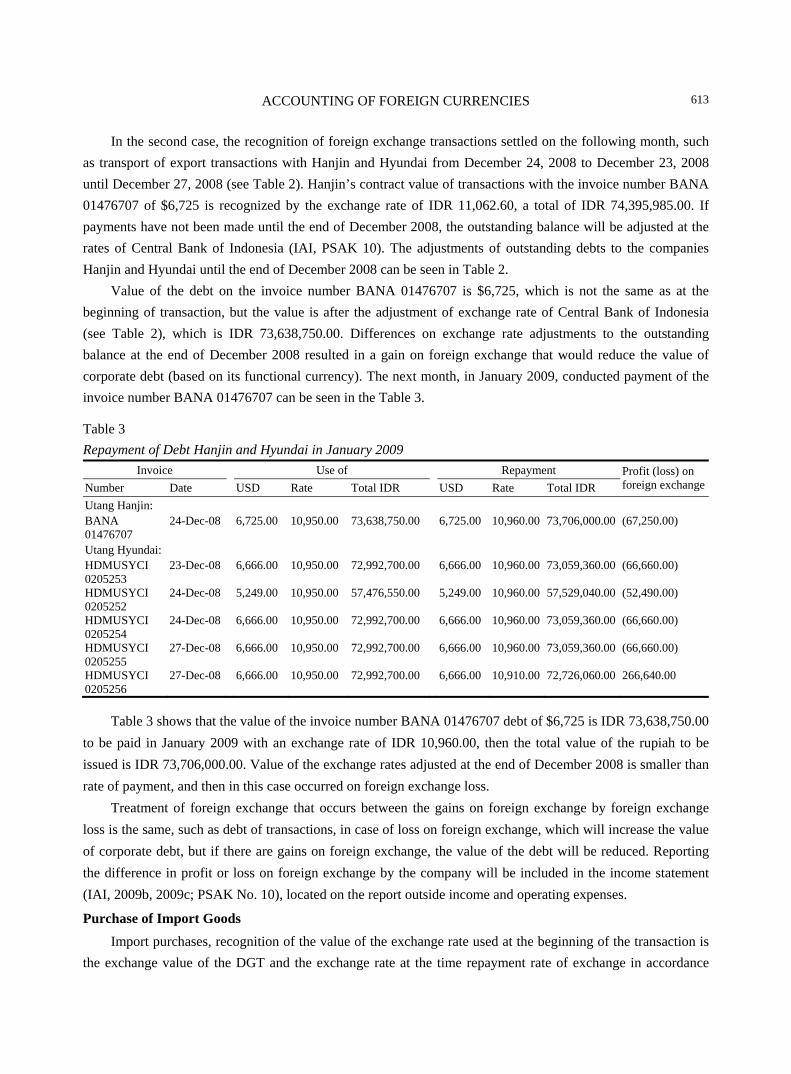

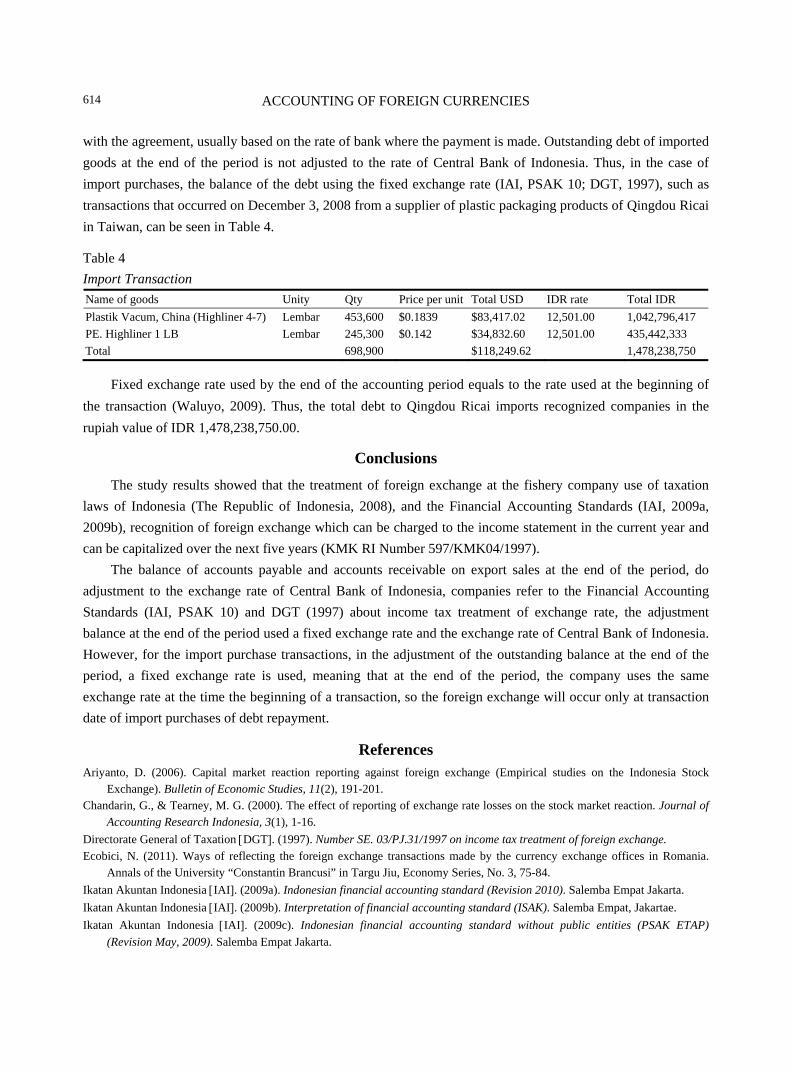

Journal of Modern Accounting and Auditing, ISSN 1548-6583 May 2013, Vol. 9, No. 5, 609-615

Accounting of Foreign Currencies: Difference in Exchange

Transactions and Relation With Taxation of Indonesia (Case

Study in Fishery Company)

Ilham Hidayah Napitupulu Padjadjaran University, Bandung, Indonesia; Politeknik Negeri Medan, Medan, Indonesia

Abdul Rahman Dalimunthe Politeknik Negeri Medan, Medan, Indonesia

Future need of globalization in business is no longer focused on the local transaction; instead, it has involved many

countries so as to affect the exchange rate of rupiah against foreign currencies. As a result, differences in the

exchange rate will lead to foreign exchange, be it a foreign exchange gain or foreign exchange losses. Exchange

rate used at the beginning of the transaction is the exchange rate on the transaction, but in Indonesian currency