1 JFE Group Growth Strategy November 30, 2010 Hajime Bada, President and CEO JFE Holdings, Inc. Securities code: 5411

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

JFE Group Growth Strategy

November 30, 2010

Hajime Bada, President and CEO

JFE Holdings, Inc.

Securities code: 5411

2

Table of Contents

1. JFE Key Facts page 3

2. JFE Steel’s Overall Strengths page 7

3. JFE Steel’s Technological Strengths page 11

4. JFE Steel’s Growth Strategies page 19

5. Results Forecast for FY 2010 page 34

This presentation material is not a disclosure document based on the Financial Instruments and Exchange Act, and neither its accuracy nor integrity are ensured. Forecasts made in this material are based on information available at the time of this investor meeting and may include uncertainties. Please refrain from making any investment decision based solely on this material. The company does not assume any responsibility for any loss resulting from the use of this material.

3

1. JFE Key Facts

JFE Key Facts

1. JFE Key Facts

4

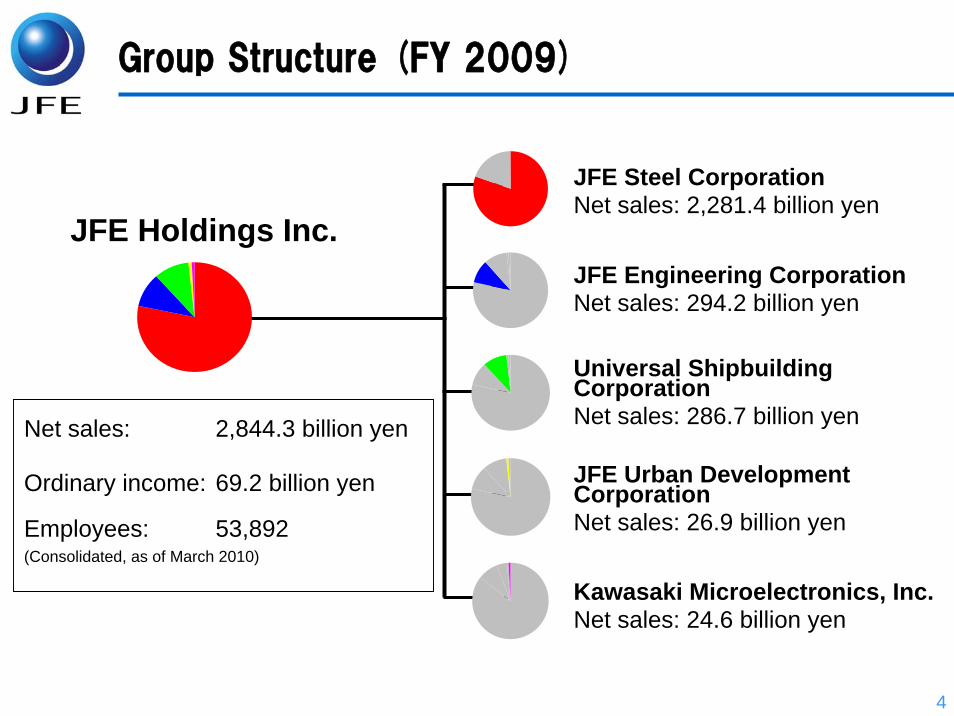

JFE Holdings Inc.

Net sales: 2,844.3 billion yen

Ordinary income: 69.2 billion yen

Employees: 53,892 (Consolidated, as of March 2010)

JFE Steel CorporationNet sales: 2,281.4 billion yen

JFE Engineering CorporationNet sales: 294.2 billion yen

JFE Urban Development CorporationNet sales: 26.9 billion yen

Kawasaki Microelectronics, Inc.Net sales: 24.6 billion yen

Universal Shipbuilding CorporationNet sales: 286.7 billion yen

Group Structure (FY 2009)

5

Upward-trending Output and Results

26.48 27.01 27.65 26.72 29.04

30.52

26.55 25.83 29.00

33.00

20.00

25.00

30.00

35.00

FY 02 FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11

104.7 218.4

460.6 517.3 513.5 502.9 400.5

69.2 220

0100200300400500600

FY 02 FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10

Production: Crude Steel Production

Profit: Ordinary Income(Target)

(million tons)

(billion yen)

6

Four Key Challenges

Technological evolution looking to 2020Development of business in AsiaDevelopment of environmental and energy businessBalancing financial base versus long-term investment

The JFE Group is addressing four key challenges in response to major developments following the global economic crisis, particularly downturns in developed economies including Japan and the robust recovery of emerging economies centered on Asia.

7

2. JFE Steel’s Overall Strengths2. JFE Steel’s Overall Strengths

8

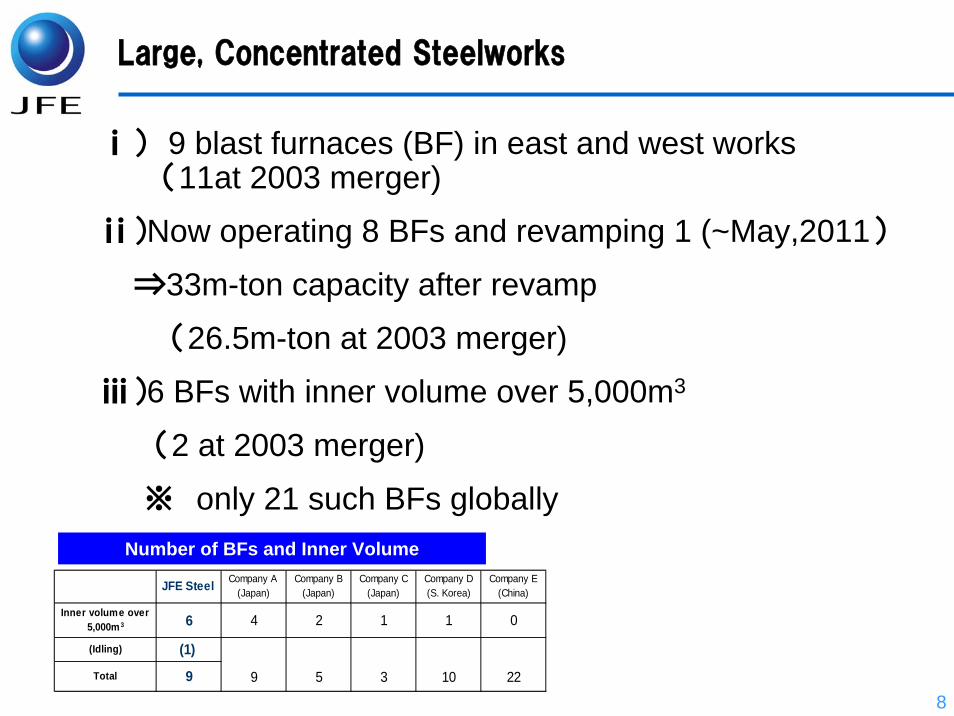

Large, Concentrated Steelworks

Number of BFs and Inner Volume

JFE Steel Company A(Japan)

Company B(Japan)

Company C(Japan)

Company D(S. Korea)

Company E(China)

Inner volume over5,000m3 6 4 2 1 1 0

(Idling) (1)

Total 9 9 5 3 10 22

ⅰ) 9 blast furnaces (BF) in east and west works (11at 2003 merger)

ⅱ)Now operating 8 BFs and revamping 1 (~May,2011)

⇒33m-ton capacity after revamp

(26.5m-ton at 2003 merger)

ⅲ)6 BFs with inner volume over 5,000m3

(2 at 2003 merger)

※ only 21 such BFs globally

9

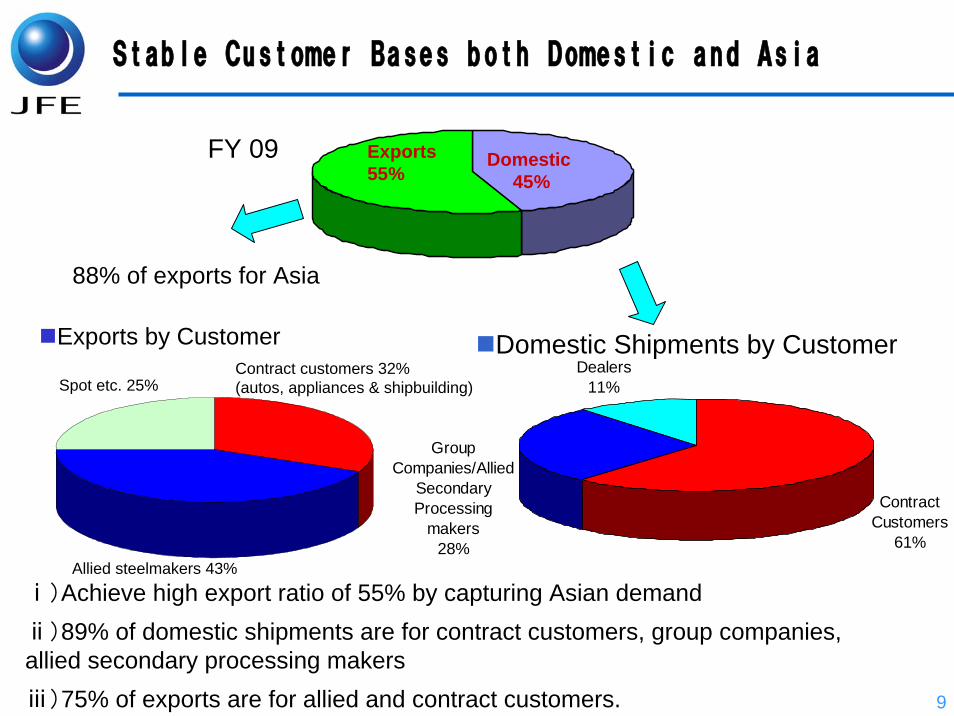

ContractCustomers

61%

Dealers11%

GroupCompanies/Allied

SecondaryProcessing

makers28%

FY 09

Domestic Shipments by Customer

Stable Customer Bases both Domestic and Asia

Exports by Customer

Allied steelmakers 43%

Contract customers 32%(autos, appliances & shipbuilding)Spot etc. 25%

Domestic45%

Exports 55%

88% of exports for Asia

ⅰ)Achieve high export ratio of 55% by capturing Asian demand ⅱ)89% of domestic shipments are for contract customers, group companies, allied secondary processing makers ⅲ)75% of exports are for allied and contract customers.

10

Expansion of shipments to Allied Steelmakers

Shipments to Allied Steelmakers (in thousand ton)

Shipments to allied steelmakers, following a temporary decrease due to the global economic crisis triggered by the collapse of Lehman in FY2008, continue to increase as the company captured growing demand for high-end steel in Asian markets.

3000

3500

4000

4500

5000

5500

FY20

03

FY20

04

FY20

05

FY20

06

FY20

07

FY20

08

FY20

09

FY20

10(e

)

11

3. JFE Steel’s Technological Strengths

12

Increasing Needs for High-end Steel

The demand for quality will continue to rise:

• More safety• More comfort• More cost reduction• More energy efficiency• More advanced (frontier) energy

Customers will increasingly demand high-end steel for sophisticated quality needs, sometimes even seemingly contradictory needs (ex., high strength and high formability) .

13

0

20

40

60

80

100

120

2010 11 12 13 14 15 16 17 18 19 20

Automobiles

Packages

ElectricalappliancesShipbuilding

Petroleum gas

Asia’s High-end Steel Market GrowthAdditional demand 33 million tons by 2020

Additional demand by 2020: 33 million tons Shares: Automobiles 13 million tons, petroleum gas 10 m/t, electrical appliances 7 m/t, and shipbuilding 3 m/t

(million tons)

14

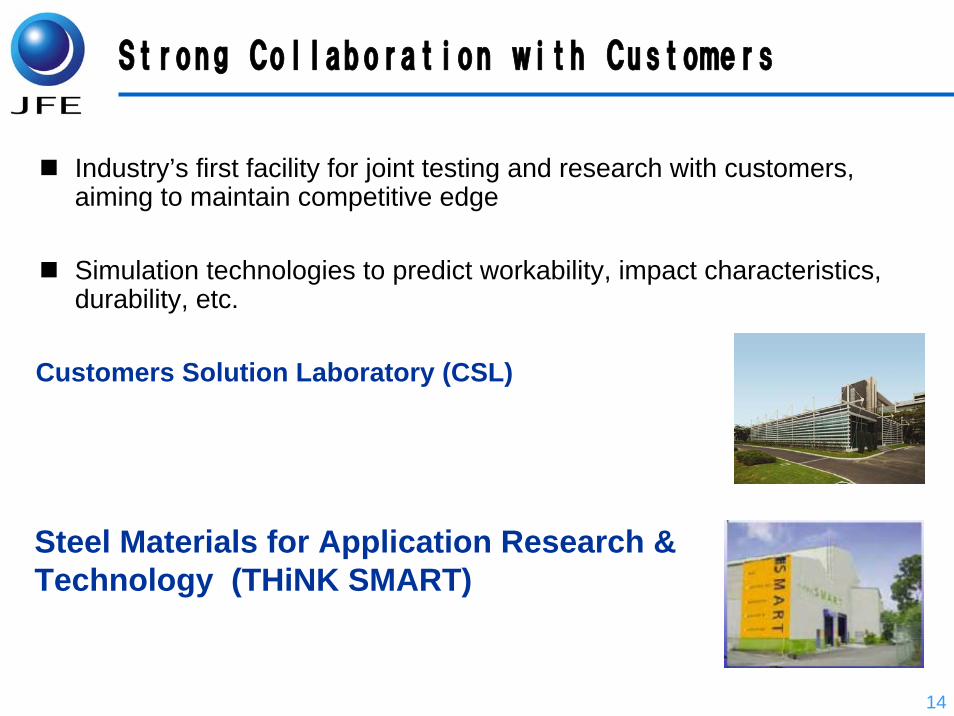

Strong Collaboration with Customers

Customers Solution Laboratory (CSL)

Steel Materials for Application Research & Technology (THiNK SMART)

Industry’s first facility for joint testing and research with customers, aiming to maintain competitive edge

Simulation technologies to predict workability, impact characteristics, durability, etc.

15

Our studies show that JFE product’s high formability is superior to Competitors’ products at all strength levels.

Elon

gati

on:

EL(%

)

Tensile strength: TS (MPa)

Strength

Form

abilit

y

Quality of products depends on balance between the strength and formability(elongation)

JFE products

CompanyX products(JFE estimate)

Superior Materials: High-tensile Steel (Automotive Steel Sheet)

16

JFE Automotive Steel Sheet is Used Worldwide

■JFE Steel’s steel sheet technology is used in 12% of all automobiles produced worldwide.

- Among Japanese autos, more than 25% worldwideand 35% in Asia-Oceania region.

※JFE Steel’s steel sheet consists of that shipped from JFE and JFE-licensed alliance partners overseas.

■Automakers rate JFE Steel highly for - Advanced technologies

- Sophisticated business capabilities ・ Early vendor involvement ・ Dependable deliveries

・ Skilled sales force■Our advantages will increase with the rise of new demand for

hybrid automobiles and electric-motor automobiles whichneed high-end electrical steel sheets for their motors.

※

17

World’s first completely continuous high-end plate production process

Plate Manufacturing Line

Rolling Quenching Tempering

Cooling bedSuper-OLAC

Hot levelerFinishing train

HOPRougher

Furnace for slab

Super-OLAC

○High speed cooling technology

⇒Achieve the same level of cooling

speed as that of sheet

○Homogeneous cooling technology

⇒Halve the dispersion (60 to 27Mpa)

HOP

○Induction heating system

⇒Enhance efficiency on tempering

Heating speed :70× faster (0.15 to 10℃/s )

○Uniform temperature control

⇒Increase temperature accuracy to ±10℃

Achieving large scale cut in production term (1/20th)

Saves energy and reduces inventories

18

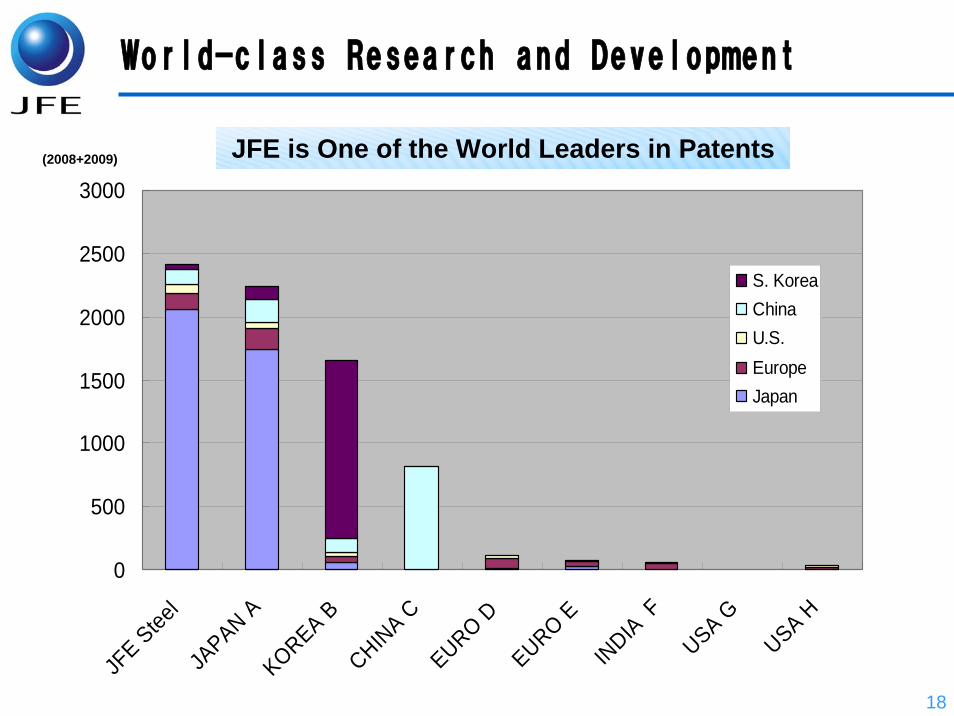

World-class Research and Development

JFE is One of the World Leaders in Patents

0

500

1000

1500

2000

2500

3000

JFE Stee

lJA

PAN AKOREA B

CHINA C

EURO DEURO EIN

DIA F

USA G

USA H

S. KoreaChinaU.S.EuropeJapan

(2008+2009)

19

4. JFE Steel’s Growth Strategies

20

Emerging Countries’ Growing Use of Steel

Apparent Crude Steel Consumption per Person

1964Tokyo

Olympics

1970OsakaExpo

Japan 447

1988Seoul

Olympics

S. Korea

974.1

China

2010Shanghai

Expo

2008Beijing

Olympics 422.1

India49.80

200

400

600

800

1000

1200

1400

50 55 60 65 70 75 80 85 90 95 2000 05

Cru

de S

teel

Con

sum

ptio

n (k

g/ p

er p

erso

n)

JapanS. KoreaChinaIndia

Lehmancrash

• Chinese and Japanese consumption are equal• Potential increase in India

21

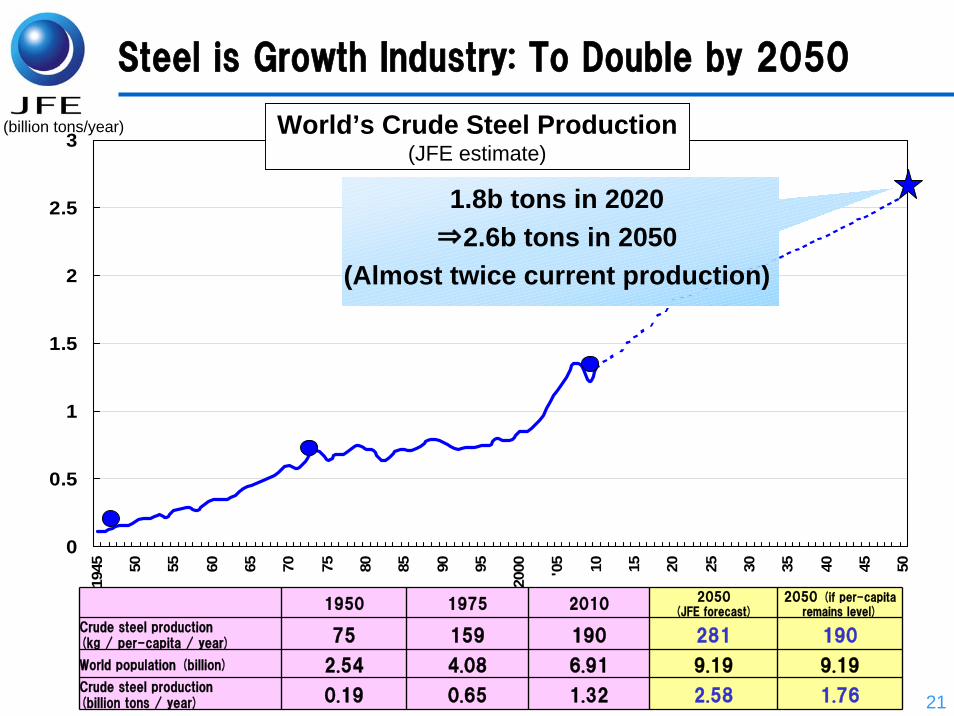

Steel is Growth Industry: To Double by 2050

0

0.5

1

1.5

2

2.5

3

1945 50 55 60 65 70 75 80 85 90 95

2000 '05 10 15 20 25 30 35 40 45 50

(billion tons/year) World’s Crude Steel Production (JFE estimate)

1950 1975 20102050

(JFE forecast)2050 (if per-capita

remains level)

Crude steel production(kg / per-capita / year) 75 159 190 281 190

World population (billion) 2.54 4.08 6.91 9.19 9.19Crude steel production(billion tons / year) 0.19 0.65 1.32 2.58 1.76

1.8b tons in 2020⇒2.6b tons in 2050

(Almost twice current production)

22

2001 20090

100(%)

60

40

80

Middle Class Drives High-end Steel Demand

20

Poor

Middle

The Indian middle class is driving high-end steel demand through its growing consumption of the 3Cs (cars, [air]coolers and color TVs), the same phenomenon seen in Japan’s “economic miracle” era in the 1960s.

Example: Growing ratio of India’s middle-class populationWealthy

23

China(10.25 mil tons)

South Western Asia(5.40 mil tons)

Middle and Near East(6.63 mil tons)

Hot-rolledsheet

Cold-rolledsheet

Plate

Regional Import Volumes in 2009(see legend)

2.56

1.23

2.84

0.58

1.393.42

Export Expansion Focusing on Asia

3.51

3.71

5.56

East Asia(12.78 mil tons)

10.25

3.13

12.78

4.25

5.4

6.63

0

5

10

15

20

25

30

35

Total imports Exports fromJapan

35.06 mil tons 8.32 mil tons

China

Middle and Near East

South Western Asia

East Asia

Legend

3.96

0.94

5.35

Total imports are smaller than the exports from Japan.

24

Develop Business Models that Respond to Each Market

Localization

Distance from Japan

S. Korea China ThailandEast

AsiaIndia

Middle East

North America

South America

Europe

Exports

Vertical Alliances

(Export semi-

finished goods)

Dongkuk

HyundaiHysco

Tongbu

GJSS

Tin Plate Mill

TCR

TCS

JSG

Tin Plate Mill CSI

Tin Plate Mill

Localization

Study feasibility of integrated steel work projects

AK Steel

Study feasibility of slab projects

Technological

Alliances

Dongkuk

HyundaiHysco

AK Steel

(USS)

TKS

GMH

(JSW)

Expand Sales

25

For 33 million tons capacity (9 BFs)

Production IncreaseRaise production from 29 million tons in 2010 (8 blast furnaces) to about 33 million tons (9 blast furnaces) from 2011⇒+3.5 million tons increase in exports

Export IncreaseHigh-end products for autos, ships, electrical appliances, etc.:increase of 33 million tons over 10 yearsCustomized commodity-grade steel

StrategiesLeverage strengths of partner trading companies in specific countriesStrengthen established relationships and develop new alliancesStrengthen relationships with core rerollers

26

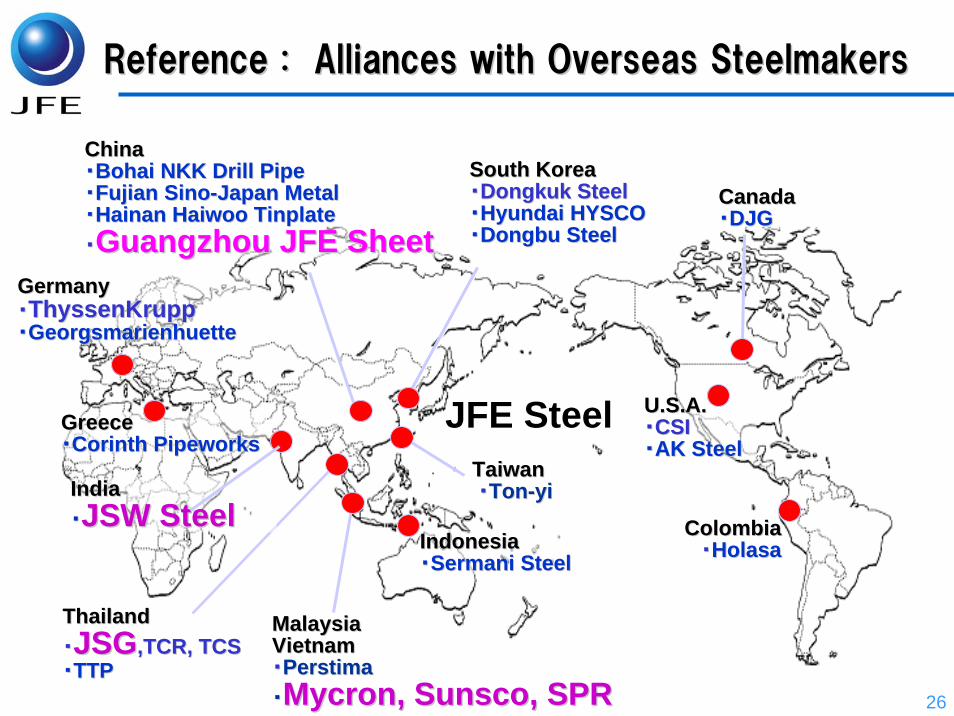

Reference : Alliances with Overseas SteelmakersReference : Alliances with Overseas SteelmakersReference : Alliances with Overseas Steelmakers

GreeceGreece・・Corinth Corinth PipeworksPipeworks

CanadaCanada・・DJGDJG

U.S.A.U.S.A.・・CSICSI・・AK SteelAK Steel

South Korea・Dongkuk Steel・Hyundai HYSCO・Dongbu Steel

South KoreaSouth Korea・・DongkukDongkuk SteelSteel・・Hyundai HYSCOHyundai HYSCO・・DongbuDongbu SteelSteel

JFE SteelJFE Steel

ThailandThailand・・JSGJSG,,TCR, TCSTCR, TCS・・TTPTTP

ColombiaColombia・・HolasaHolasaIndonesiaIndonesia

・・SermaniSermani SteelSteel

MalaysiaMalaysia Vietnam Vietnam ・・PerstimaPerstima・・MycronMycron, , SunscoSunsco, SPR, SPR

GermanyGermany・・ThyssenKruppThyssenKrupp・・GeorgsmarienhuetteGeorgsmarienhuette

ChinaChina・・BohaiBohai NKK Drill PipeNKK Drill Pipe・・Fujian SinoFujian Sino--Japan MetalJapan Metal・・Hainan Hainan HaiwooHaiwoo TinplateTinplate・・Guangzhou JFE SheetGuangzhou JFE Sheet

Taiwan Taiwan ・・TonTon--yiyiIndiaIndia

・・JSW SteelJSW Steel

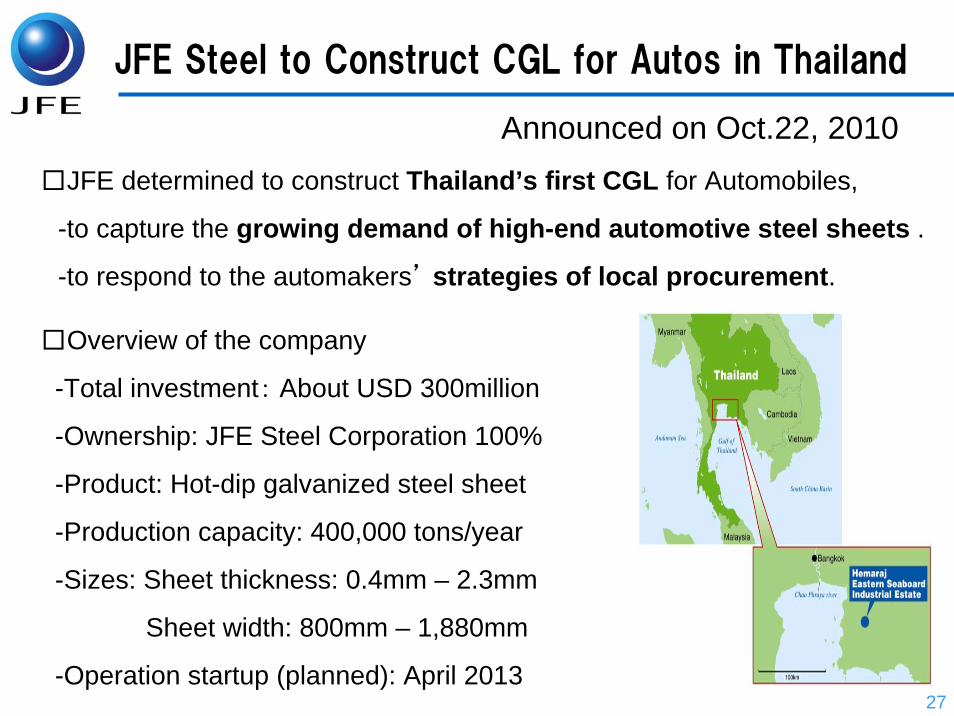

27

□JFE determined to construct Thailand’s first CGL for Automobiles,

-to capture the growing demand of high-end automotive steel sheets .

-to respond to the automakers’ strategies of local procurement.

□Overview of the company

-Total investment: About USD 300million

-Ownership: JFE Steel Corporation 100%

-Product: Hot-dip galvanized steel sheet

-Production capacity: 400,000 tons/year

-Sizes: Sheet thickness: 0.4mm – 2.3mm

Sheet width: 800mm – 1,880mm

-Operation startup (planned): April 2013

Hemaraj Eastern Seaboard Industrial

Announced on Oct.22, 2010

JFE Steel to Construct CGL for Autos in Thailand

28

Equipment Shipments(operating) (1,000t/p.a.)

High-end SteelAuto (GA) 600

400Under Construction Electric (GI) 200

Auto (CRC) 500

1,800 400 Electric (CRC) 200

CRC 200

900

CAL

PL-TCM No.2 CGL

No.1 CGL

Expansion of Capacity in Guangzhou, China

Guangzhou JFE Steel Sheet (JFE ownership: 50%)Phase 2: Construction start from Oct.,2007. Operation start in FY2011

Providing HRC

JFE Steel

29

JFE STEEL & JSW STEEL COME TOGETHER IN A STRATEGIC COLLABORATION

Announced on Jul. 27th ,2010

(A) Collaboration for Automotive Steel Production:・ Supply of substrate materials for hot rolled, cold rolled and galvanized products.・Joint service activities including application engineering and product

development for automotive customers.

(B) Further Collaboration in the near future: ・Production of steel products other than automotive steel. ・Saving energy ・Quality and yield improvement programs

・Performance audit of JSW facilities・Benchmarking of techno-economic parameters between the parties・JFE’s shareholding of JSW

30

JFE has determined to acquire Jeong An Vina Co to capture the strong demand for construction steel pipe especially in Vietnam where many projects for ports, railways and other major infrastructures are being launched.

Company OverviewShare: JFE Steel 35%, Maruichi Steel Tube 35%, Toyota Tsusho 30%

Total investment:18 billion Korean won (about 1.3billion Yen)

Production capacity: 50,000 tons/year

Facilities: Spiral steel pipe production

Coating

Products: Steel pipe pile

Steel pipe sheet pile

JFE Steel Acquires Spiral Steel Pipe Maker in Vietnam

Announced on Nov.15th,2010

31

15%

18%

30%30%

0%

10%

20%

30%

40%

Current FY2011

Ore

Coal

Ex. Ore:Acquired a 6.5% interest in NAMISA in Brazil (‘08)

Ex. Coal: Acquired a 20% interest in new Byerwen Coal in Australia(‘09)

Ex. Ore:Acquired a 6.5% interest in NAMISA in Brazil (‘08)

Ex. Coal: Acquired a 20% interest in new Byerwen Coal in Australia(‘09)

Increasing Self-Sufficiency RatioIncreased from 15% to 18% by acquisition of Australian Coal Mine interests (JFE Shoji Trade announced on Oct. 20, 2010)

32

700 Billion yen is scheduled to spend by FY2011.

・100 Bn for JSW (Completed)・400 Bn for Capex ・200 Bn for prospective investments

-mainly for the mining interests acquisition -remainder for expansion of alliance network

Plan for the Investment and Capex

33

(Appendix)JFE-Group expansion to China

Auto

Tinplate

SMLS pipe

Drum

Resources

Coil center

Bohai NKK Drill Pipe

Pancheng Yihong Pipe

Guangzhou JFE Steel Sheet

Fujian Sino-Japan Metal

Fujian Ton Yi

Hainan Haiwoo Tinplate

Jiangsu Ton Yi

Wuhan Excellent Steel Center

Inner Mongolia ERDOSEJM Manganese Alloy

Named companies: JFE steel equity holding

Non-named companies:JFE Group companies equity holding

34

5. Results Forecast for FY 2010

35

Results Forecast for FY 2010

Improving to three times of FY2009

(billion yen)

FY2009(A) 1H Total

Net Sales 2,844 1,572 3,360

Operating income 89 115 230

Ordinary Income 69 105 220

Net Income 46 46 110

FY2010(e)

36

Financial Forecast for FY10

Sales/Recurring Profit by Business Segment

1H 2H Total 1H 2H(e) Total

Steel Net Sales 1,062 1,219 2,281 1,370 1,531 2,900Ordinary Income ▲ 72 105 32 88 112 200

Engineering Net Sales 117 177 294 105 165 270Ordinary Income 3 11 13 3 5 8

Shipbuilding Net Sales 139 148 287 107 103 210Ordinary Income 10 11 22 13 1 13

Others Net Sales 23 29 52 21 17 38Ordinary Income ▲ 2 ▲ 1 ▲ 3 0 ▲ 1 ▲ 1

Adjustments Net Sales ▲ 34 ▲ 36 ▲ 70 ▲ 30 ▲ 29 ▲ 58Ordinary Income 4 1 5 1 ▲ 1 ▲ 1

Total Net Sales 1,307 1,537 2,844 1,572 1,788 3,360Ordinary Income ▲ 58 127 69 105 115 220

FY2009 FY2010(e)

37

10.5

17.5 26.3

58.570.5

68.8

49.0

0

10

20

30

40

50

60

70

80

FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09

(billion yen)

Proactive Return to Shareholders

Yield(%) 2.0% 1.6% 3.3% 2.5% 1.7% 2.0% 0.5%

Basic Policy for pay-out ratio is around 25%.

15

45

100

120 120

90

2030

69.7

16.1 16.4 18

23.426.6 25.3

23.2

0

50

100

150

200

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09

0

20

40

60

80

Yen/Share

Payout Ratio

Midterm dividend in 2010 :20 yen/share

38

Thank you very much for your kind attention

Related Documents