3rd Quarter 2010 Results November 12 th , 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

3rd Quarter 2010 ResultsNovember 12th, 2010

2

Disclaimer

The forward-looking statements presented herein are subject to risks and uncertainties. These

statements are based on the beliefs and assumptions of our management, and on information

currently available to us.

Forward-looking statements are not guarantees of performance. They involve risks,

uncertainties and assumptions because they relate to future events and therefore depend on

circumstances that may or may not occur. Our future operating results, financial condition,

strategies, market share and values may differ materially from those expressed in or suggested

by these forward-looking statements. Many of the factors that will determine these results and

values are beyond our ability to control or predict.

Forward-looking statements also include information concerning our possible or assumed future

operating results, as well as statements preceded by, followed by, or including the words

''believes,'' ''may,'' ''will,'' ''continues,'' ''expects,'‘ ''anticipates,'' ''intends,'' ''plans,'' ''estimates'' or

similar expressions.

3

Wesley Mendonça Batista

CEO of JBS USA

Joesley Mendonça Batista

CEO of JBS S.A.

Guilherme Arruda

Investors Relations

Presenters

Jeremiah O’Callaghan

Investors Relations Officer

Agenda

4

Market Overview

JBSS3

Analysis and

Measures

Company Overview

3Q10 Highlights

5

Our MissionTo be the best at what we set out to do, totally focused on our business, ensuring the best

products and services for our customers, solidity for our suppliers, satisfactory profitability for

our shareholders and the certainty of a better future for all our employees.

Our ValuesExcellence

Planning

Determination

Discipline

Availability

Openness

Simplicity

Who We Are

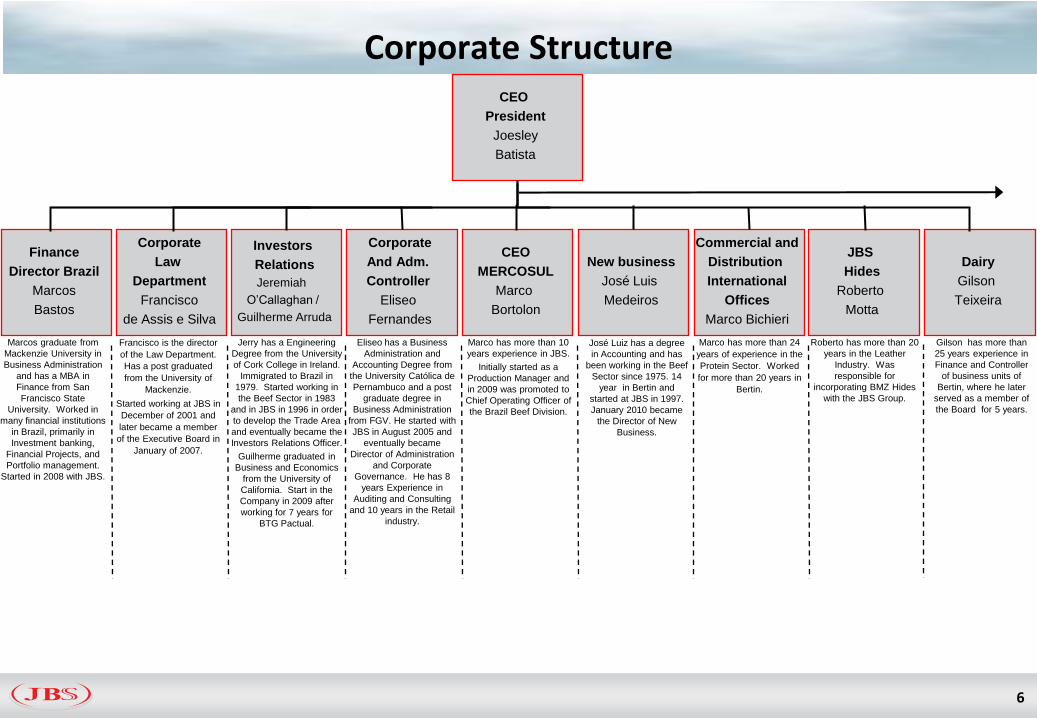

Corporate Structure

Investors

Relations

Jeremiah

O’Callaghan /

Guilherme Arruda

Finance

Director Brazil

Marcos

Bastos

Corporate

Law

Department

Francisco

de Assis e Silva

Marcos graduate from

Mackenzie University in

Business Administration

and has a MBA in

Finance from San

Francisco State

University. Worked in

many financial institutions

in Brazil, primarily in

Investment banking,

Financial Projects, and

Portfolio management.

Started in 2008 with JBS.

Francisco is the director

of the Law Department.

Has a post graduated

from the University of

Mackenzie.

Started working at JBS in

December of 2001 and

later became a member

of the Executive Board in

January of 2007.

Jerry has a Engineering

Degree from the University

of Cork College in Ireland.

Immigrated to Brazil in

1979. Started working in

the Beef Sector in 1983

and in JBS in 1996 in order

to develop the Trade Area

and eventually became the

Investors Relations Officer.

Guilherme graduated in

Business and Economics

from the University of

California. Start in the

Company in 2009 after

working for 7 years for

BTG Pactual.

Corporate

And Adm.

Controller

Eliseo

Fernandes

Eliseo has a Business

Administration and

Accounting Degree from

the University Católica de

Pernambuco and a post

graduate degree in

Business Administration

from FGV. He started with

JBS in August 2005 and

eventually became

Director of Administration

and Corporate

Governance. He has 8

years Experience in

Auditing and Consulting

and 10 years in the Retail

industry.

Dairy

Gilson

Teixeira

CEO

MERCOSUL

Marco

Bortolon

JBS

Hides

Roberto

Motta

New business

José Luis

Medeiros

Commercial and

Distribution

International

Offices

Marco Bichieri

CEO

President

Joesley

Batista

Marco has more than 10

years experience in JBS.

Initially started as a

Production Manager and

in 2009 was promoted to

Chief Operating Officer of

the Brazil Beef Division.

Marco has more than 24

years of experience in the

Protein Sector. Worked

for more than 20 years in

Bertin.

Roberto has more than 20

years in the Leather

Industry. Was

responsible for

incorporating BMZ Hides

with the JBS Group.

Gilson has more than

25 years experience in

Finance and Controller

of business units of

Bertin, where he later

served as a member of

the Board for 5 years.

José Luiz has a degree

in Accounting and has

been working in the Beef

Sector since 1975. 14

year in Bertin and

started at JBS in 1997.

January 2010 became

the Director of New

Business.

6

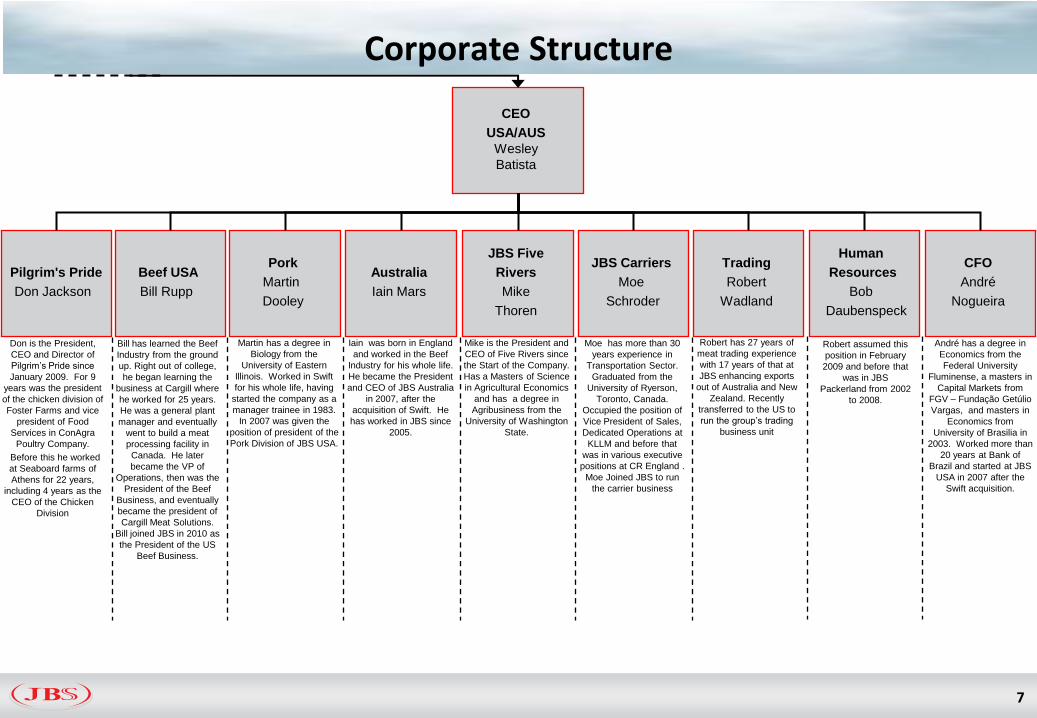

Corporate Structure

Australia

Iain Mars

Pilgrim's Pride

Don Jackson

Beef USA

Bill Rupp

JBS Five

Rivers

Mike

Thoren

JBS Carriers

Moe

Schroder

CEO

USA/AUS

Wesley

Batista

Pork

Martin

Dooley

Iain was born in England

and worked in the Beef

Industry for his whole life.

He became the President

and CEO of JBS Australia

in 2007, after the

acquisition of Swift. He

has worked in JBS since

2005.

Martin has a degree in

Biology from the

University of Eastern

Illinois. Worked in Swift

for his whole life, having

started the company as a

manager trainee in 1983.

In 2007 was given the

position of president of the

Pork Division of JBS USA.

Moe has more than 30

years experience in

Transportation Sector.

Graduated from the

University of Ryerson,

Toronto, Canada.

Occupied the position of

Vice President of Sales,

Dedicated Operations at

KLLM and before that

was in various executive

positions at CR England .

Moe Joined JBS to run

the carrier business

Mike is the President and

CEO of Five Rivers since

the Start of the Company.

Has a Masters of Science

in Agricultural Economics

and has a degree in

Agribusiness from the

University of Washington

State.

Bill has learned the Beef

Industry from the ground

up. Right out of college,

he began learning the

business at Cargill where

he worked for 25 years.

He was a general plant

manager and eventually

went to build a meat

processing facility in

Canada. He later

became the VP of

Operations, then was the

President of the Beef

Business, and eventually

became the president of

Cargill Meat Solutions.

Bill joined JBS in 2010 as

the President of the US

Beef Business.

Don is the President,

CEO and Director of

Pilgrim’s Pride since

January 2009. For 9

years was the president

of the chicken division of

Foster Farms and vice

president of Food

Services in ConAgra

Poultry Company.

Before this he worked

at Seaboard farms of

Athens for 22 years,

including 4 years as the

CEO of the Chicken

Division

Trading

Robert

Wadland

Robert has 27 years of

meat trading experience

with 17 years of that at

JBS enhancing exports

out of Australia and New

Zealand. Recently

transferred to the US to

run the group’s trading

business unit

CFO

André

Nogueira

Human

Resources

Bob

Daubenspeck

André has a degree in

Economics from the

Federal University

Fluminense, a masters in

Capital Markets from

FGV – Fundação Getúlio

Vargas, and masters in

Economics from

University of Brasilia in

2003. Worked more than

20 years at Bank of

Brazil and started at JBS

USA in 2007 after the

Swift acquisition.

Robert assumed this

position in February

2009 and before that

was in JBS

Packerland from 2002

to 2008.

7

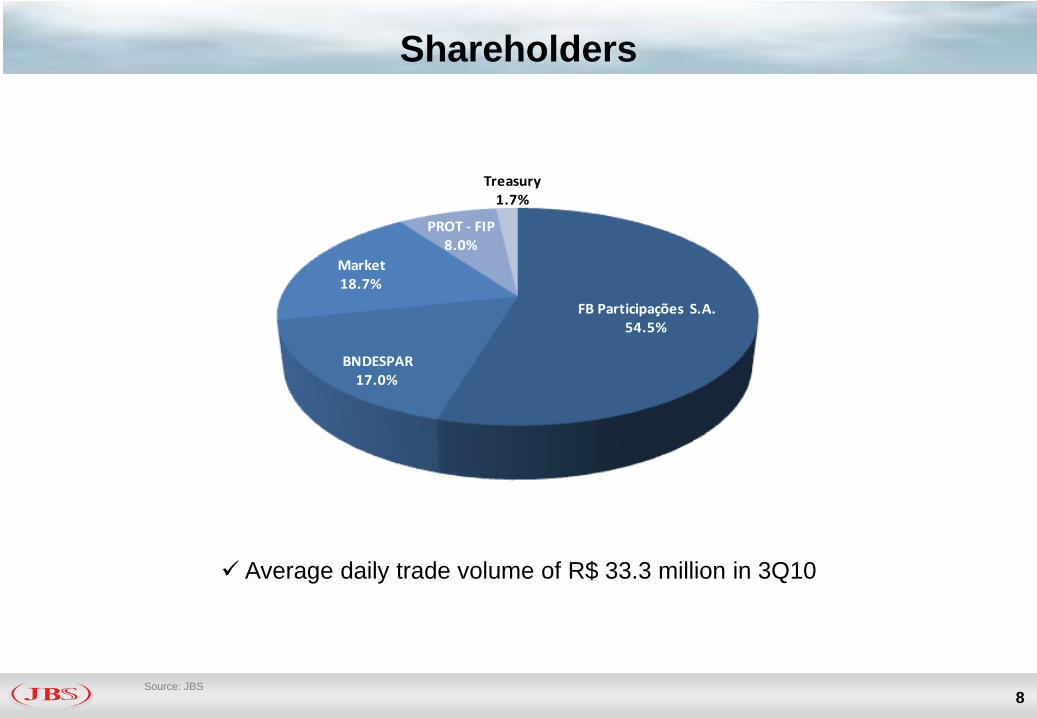

Shareholders

8Source: JBS

FB Participações S.A.54.5%

BNDESPAR17.0%

Market18.7%

PROT - FIP8.0%

Treasury1.7%

Average daily trade volume of R$ 33.3 million in 3Q10

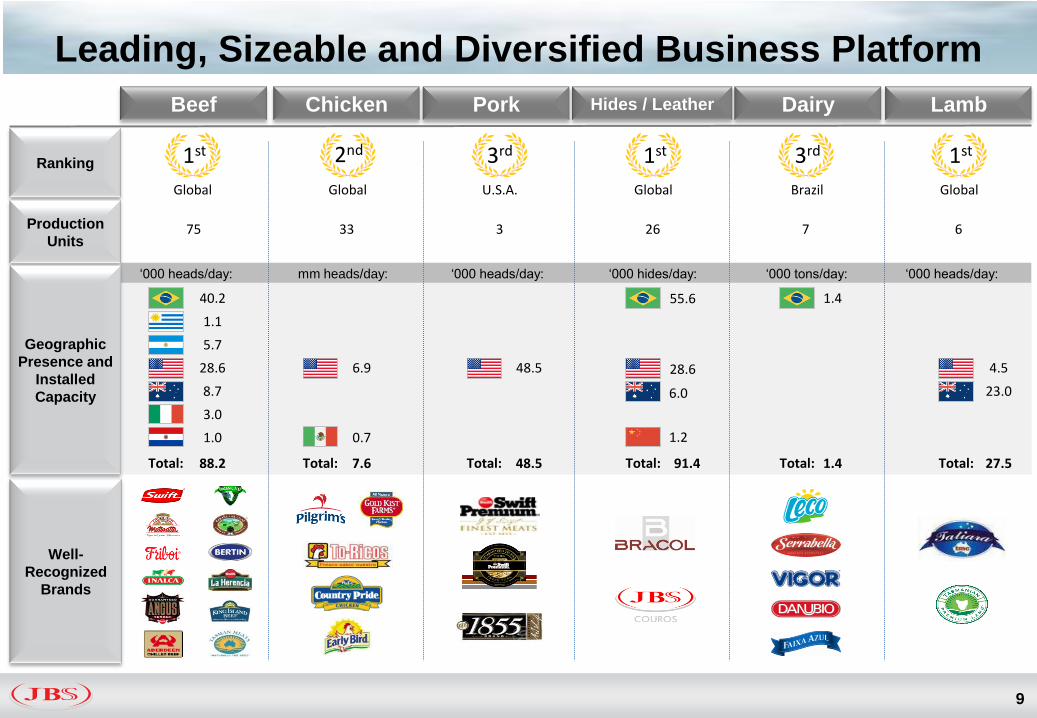

Leading, Sizeable and Diversified Business Platform

9

1stRanking

Well-

Recognized

Brands

Production

Units

Geographic

Presence and

Installed

Capacity

2nd 3rd 1st 3rd 1st

Global Global U.S.A. Global Brazil Global

Beef

40.2

1.1

5.7

28.6

8.7

3.0

1.0

‘000 heads/day:

6.9

0.7

mm heads/day:

48.5

‘000 heads/day: ‘000 hides/day:

1.4

‘000 tons/day:

4.5

23.0

‘000 heads/day:

Total: 88.2 Total: 7.6 Total: 48.5 Total: 91.4 Total: 1.4 Total: 27.5

Chicken Pork Hides / Leather Dairy Lamb

75 33 3 26 7 6

55.6

28.6

6.0

1.2

Our Strategy

10

Production platform

Sales and distribution platform

Value added products

Branding

JBS’ Value & Strategy

EBITDA Margin

Financial structure

Experienced management

Cost reduction, process

optimization

Risk management

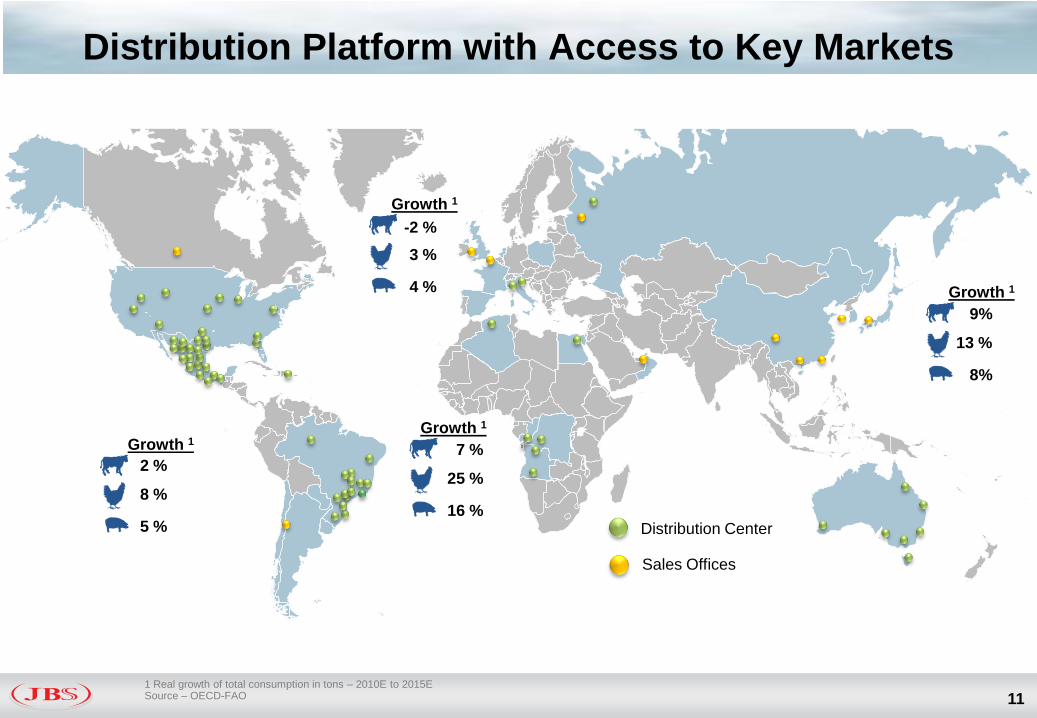

• Developed an efficient and diversified global production platform

• Expanding a global distribution platform to reach end clients

• Customized and further processed products for the end users

• Associating quality and branding to increase client loyalty

Rationale

Distribution Platform with Access to Key Markets

111 Real growth of total consumption in tons – 2010E to 2015ESource – OECD-FAO

Distribution Center

Growth 1

2 %

5 %

8 %

Growth 1

7 %

16 %

25 %

Growth 1

9%

8%

13 %

Growth 1

4 %

3 %

-2 %

Sales Offices

Agenda

12

Market Overview

JBSS3

Analysis and

Measures

Company Overview

3Q10 Highlights

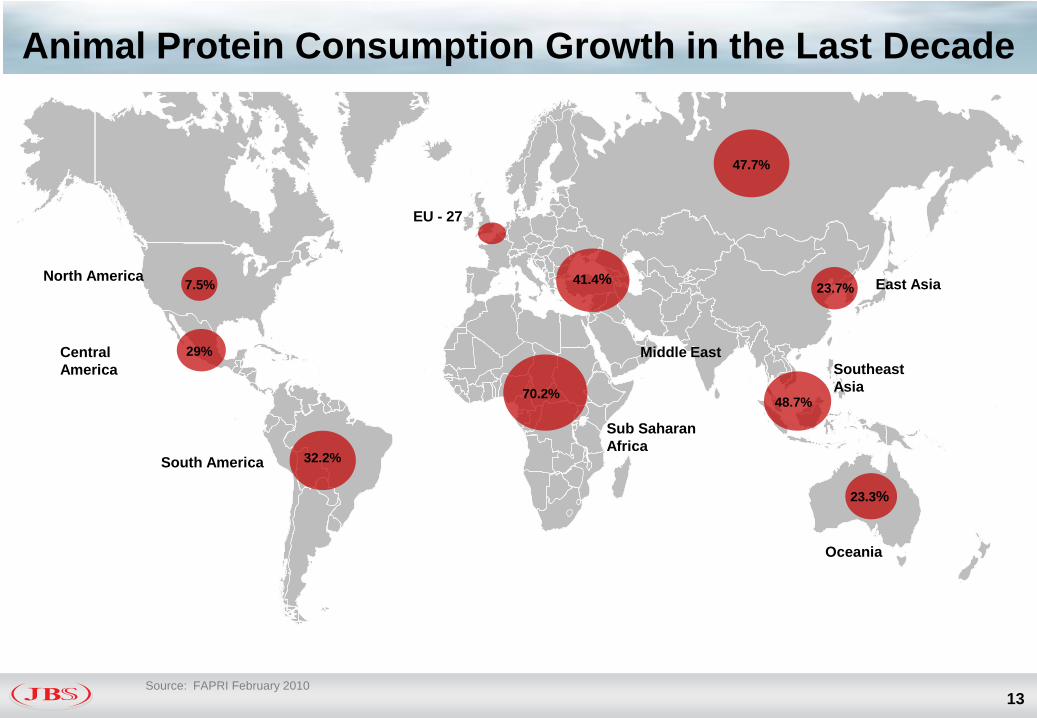

Animal Protein Consumption Growth in the Last Decade

13

3

Source: FAPRI February 2010

7.5%

29%

32.2%

70.2%

41.4%

47.7%

23.7%

23.3%

48.7%

North America

Central

America

South America

Sub Saharan

Africa

Middle EastSoutheast

Asia

East Asia

Oceania

EU - 27

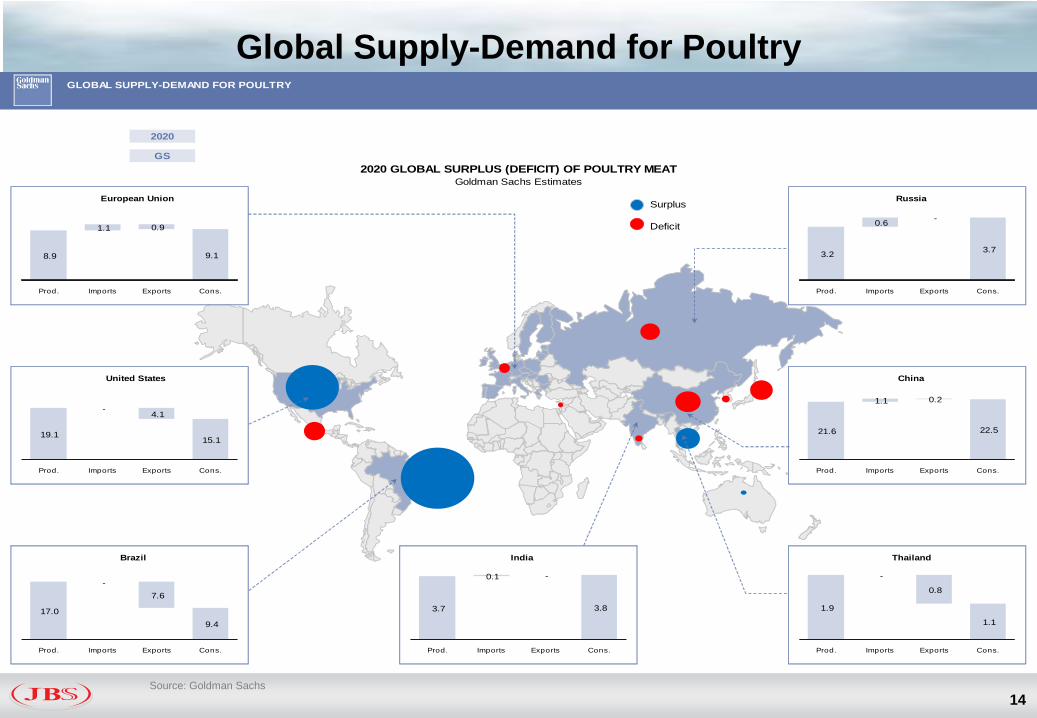

Global Supply-Demand for Poultry

14Source: Goldman Sachs

GLOBAL SUPPLY-DEMAND FOR POULTRY

Choose Year for Chart: 2020

Estimates for Chart GS

Goldman Sachs Estimates 2020 GLOBAL SURPLUS (DEFICIT) OF POULTRY MEAT

Goldman Sachs Estimates

Surplus

Deficit

8.9

1.1 0.9

9.1

Prod. Imports Exports Cons.

European Union

3.2

0.6 -

3.7

Prod. Imports Exports Cons.

Russia

19.1

-4.1

15.1

Prod. Imports Exports Cons.

United States

21.6

1.1 0.2

22.5

Prod. Imports Exports Cons.

China

17.0

-

7.6

9.4

Prod. Imports Exports Cons.

Brazil

1.9

-

0.8

1.1

Prod. Imports Exports Cons.

Thailand

3.7

0.1 -

3.8

Prod. Imports Exports Cons.

India

Global Supply-Demand for Pork

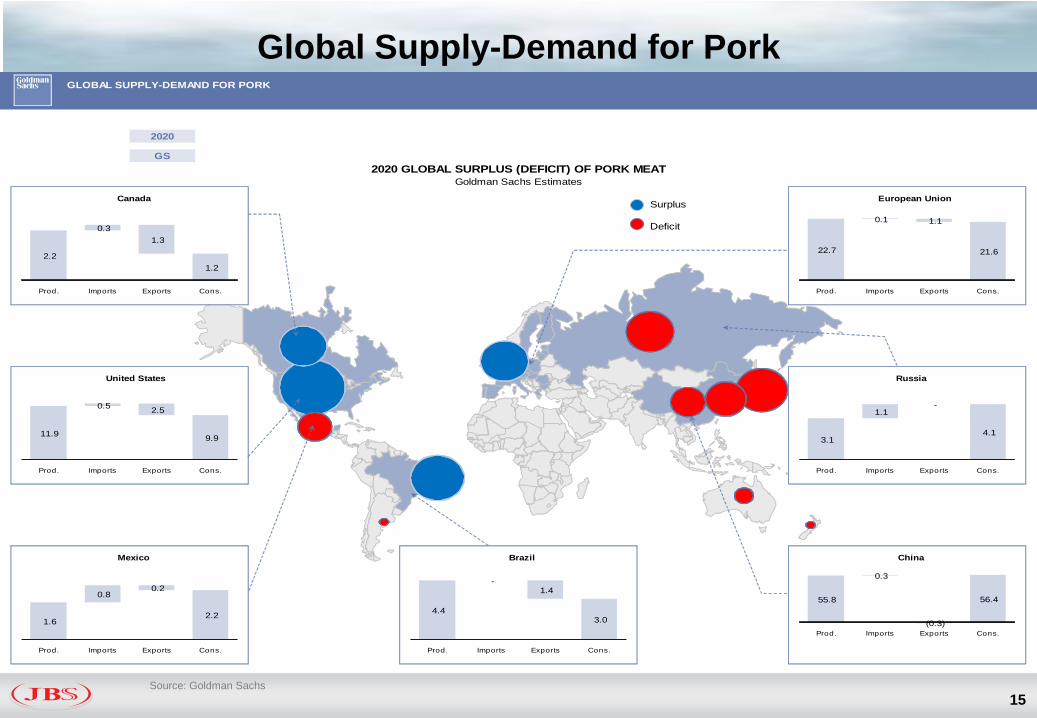

15Source: Goldman Sachs

GLOBAL SUPPLY-DEMAND FOR PORK

Choose Year for Chart: 2020

Estimates for Chart GS

Goldman Sachs Estimates 2020 GLOBAL SURPLUS (DEFICIT) OF PORK MEAT

Goldman Sachs Estimates

Surplus

Deficit

2.2

0.3

1.3

1.2

Prod. Imports Exports Cons.

Canada

22.7

0.1 1.1

21.6

Prod. Imports Exports Cons.

European Union

11.9

0.5 2.5

9.9

Prod. Imports Exports Cons.

United States

3.1

1.1 -

4.1

Prod. Imports Exports Cons.

Russia

1.6

0.8 0.2

2.2

Prod. Imports Exports Cons.

Mexico

55.8

0.3

(0.3)

56.4

Prod. Imports Exports Cons.

China

4.4

-1.4

3.0

Prod. Imports Exports Cons.

Brazil

Global Supply-Demand for Beef

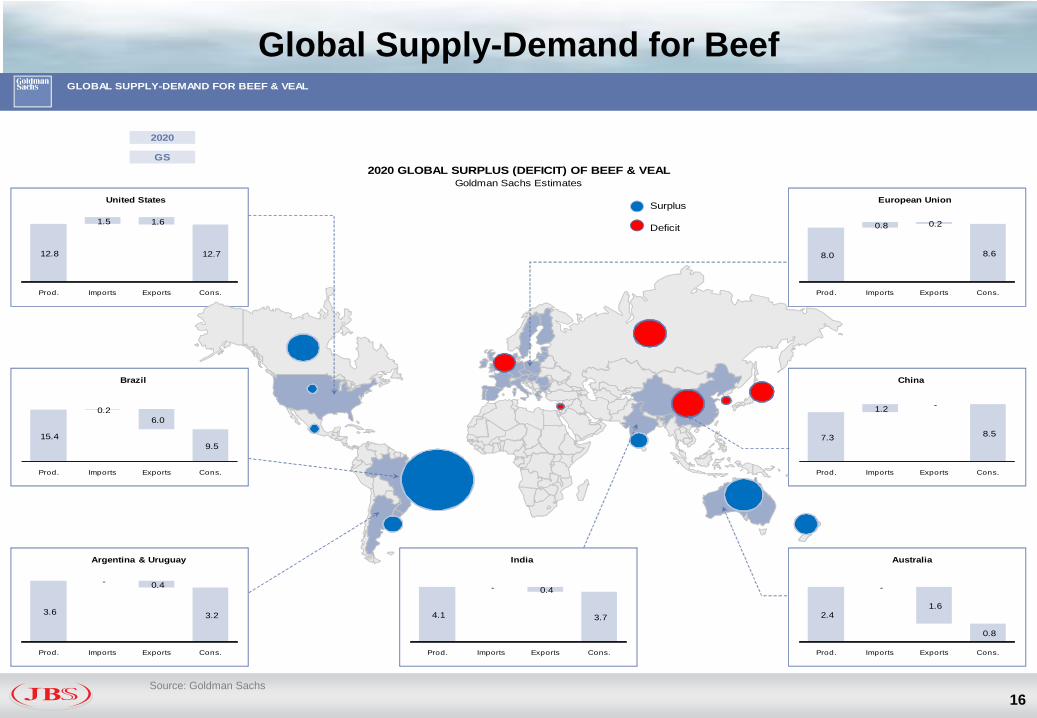

16Source: Goldman Sachs

GLOBAL SUPPLY-DEMAND FOR BEEF & VEAL

Choose Year for Chart: 2020

Estimates for Chart GS

Goldman Sachs Estimates 2020 GLOBAL SURPLUS (DEFICIT) OF BEEF & VEAL

Goldman Sachs Estimates

Surplus

Deficit

12.8

1.5 1.6

12.7

Prod. Imports Exports Cons.

United States

8.0

0.8 0.2

8.6

Prod. Imports Exports Cons.

European Union

15.4

0.2

6.0

9.5

Prod. Imports Exports Cons.

Brazil

7.3

1.2 -

8.5

Prod. Imports Exports Cons.

China

3.6

- 0.4

3.2

Prod. Imports Exports Cons.

Argentina & Uruguay

2.4

-

1.6

0.8

Prod. Imports Exports Cons.

Australia

4.1

- 0.4

3.7

Prod. Imports Exports Cons.

India

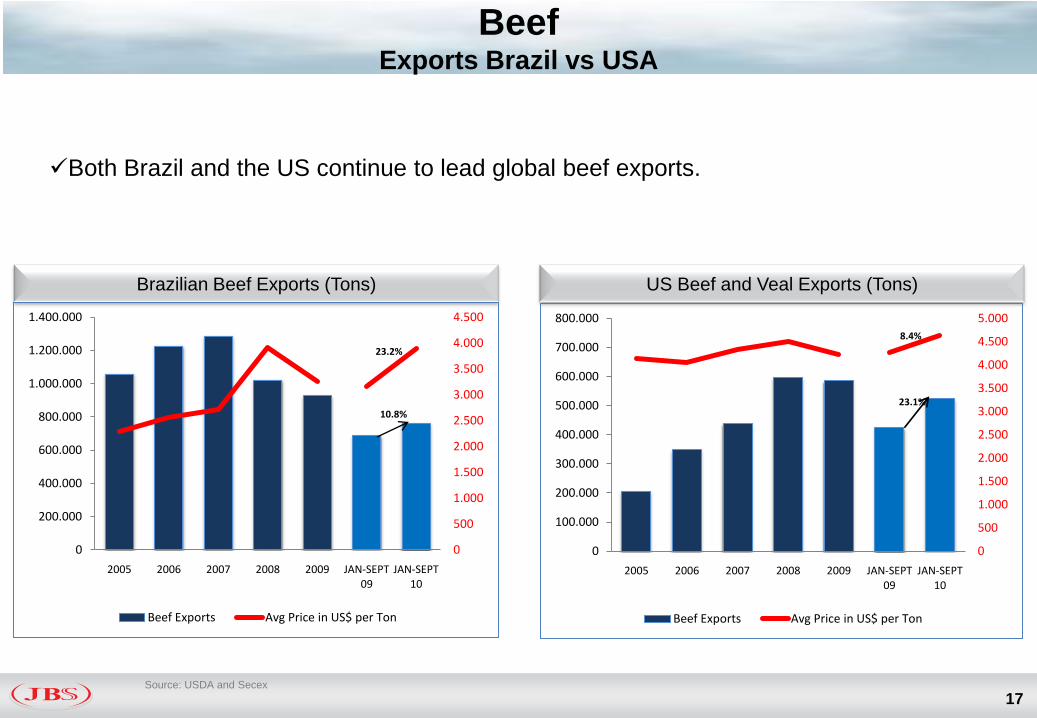

BeefExports Brazil vs USA

17Source: USDA and Secex

US Beef and Veal Exports (Tons)Brazilian Beef Exports (Tons)

Both Brazil and the US continue to lead global beef exports.

0

200.000

400.000

600.000

800.000

1.000.000

1.200.000

1.400.000

2005 2006 2007 2008 2009 JAN-SEPT 09

JAN-SEPT 10

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

Beef Exports Avg Price in US$ per Ton

10.8%

23.2%

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

2005 2006 2007 2008 2009 JAN-SEPT 09

JAN-SEPT 10

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

Beef Exports Avg Price in US$ per Ton

23.1%

8.4%

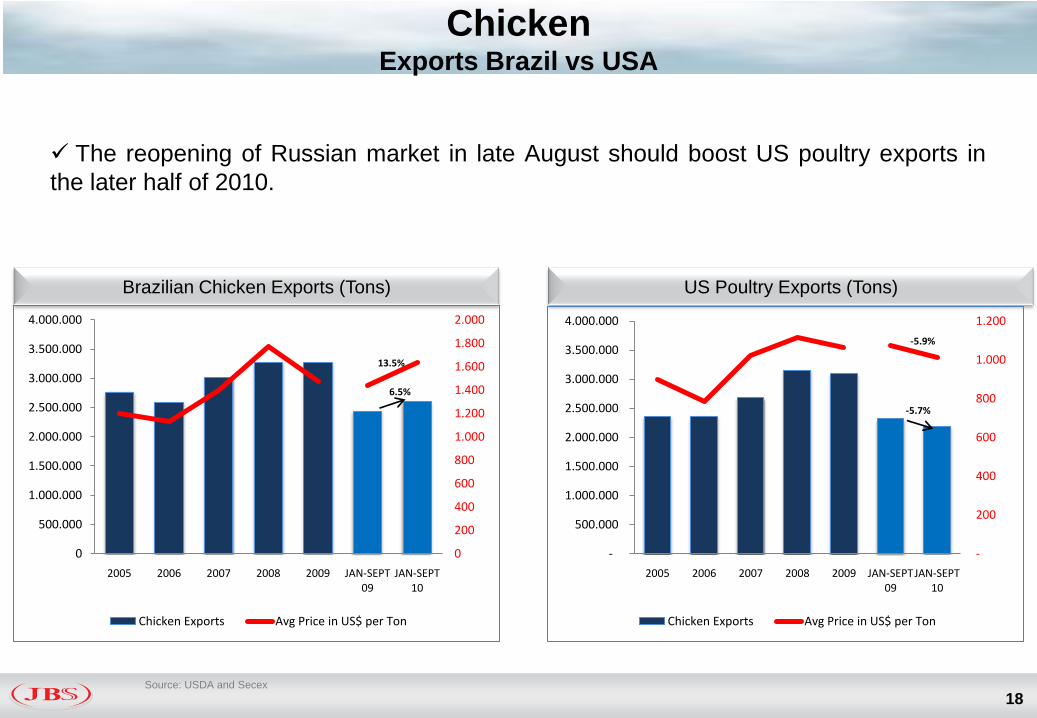

ChickenExports Brazil vs USA

18Source: USDA and Secex

Brazilian Chicken Exports (Tons) US Poultry Exports (Tons)

The reopening of Russian market in late August should boost US poultry exports in

the later half of 2010.

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

4.000.000

2005 2006 2007 2008 2009 JAN-SEPT 09

JAN-SEPT 10

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2.000

Chicken Exports Avg Price in US$ per Ton

6.5%

13.5%

-

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

4.000.000

2005 2006 2007 2008 2009 JAN-SEPT 09

JAN-SEPT 10

-

200

400

600

800

1.000

1.200

Chicken Exports Avg Price in US$ per Ton

-5.7%

-5.9%

Agenda

19

Market Overview

JBSS3

Analysis and

Measures

Company Overview

3Q10 Highlights

Highlights - 3Q10

20

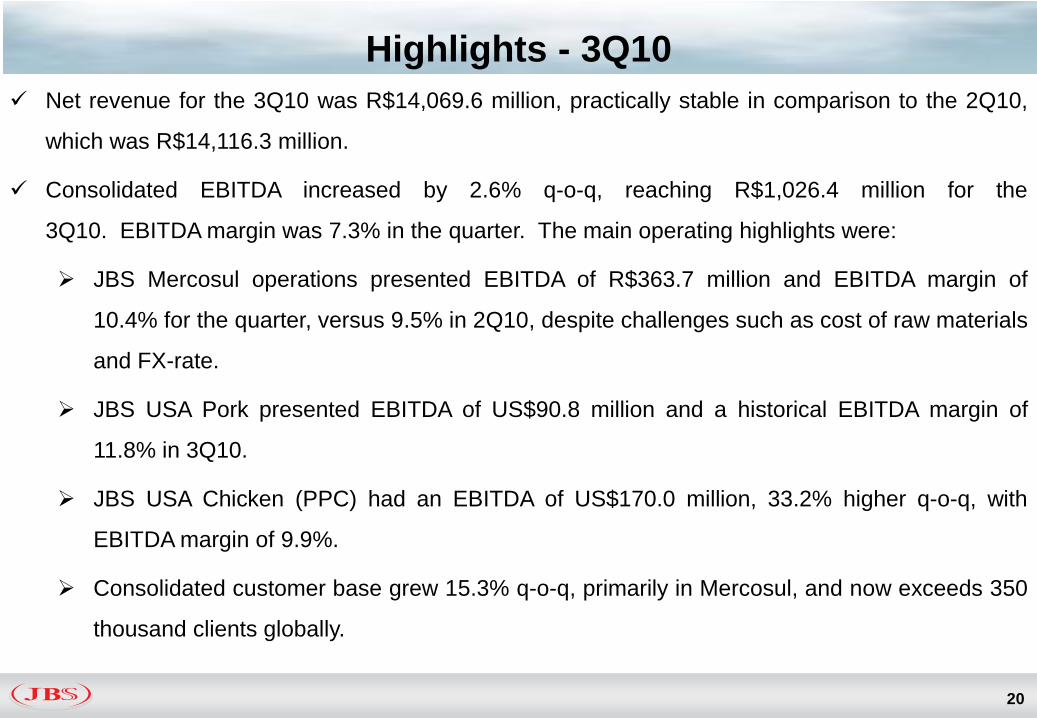

Net revenue for the 3Q10 was R$14,069.6 million, practically stable in comparison to the 2Q10,

which was R$14,116.3 million.

Consolidated EBITDA increased by 2.6% q-o-q, reaching R$1,026.4 million for the

3Q10. EBITDA margin was 7.3% in the quarter. The main operating highlights were:

JBS Mercosul operations presented EBITDA of R$363.7 million and EBITDA margin of

10.4% for the quarter, versus 9.5% in 2Q10, despite challenges such as cost of raw materials

and FX-rate.

JBS USA Pork presented EBITDA of US$90.8 million and a historical EBITDA margin of

11.8% in 3Q10.

JBS USA Chicken (PPC) had an EBITDA of US$170.0 million, 33.2% higher q-o-q, with

EBITDA margin of 9.9%.

Consolidated customer base grew 15.3% q-o-q, primarily in Mercosul, and now exceeds 350

thousand clients globally.

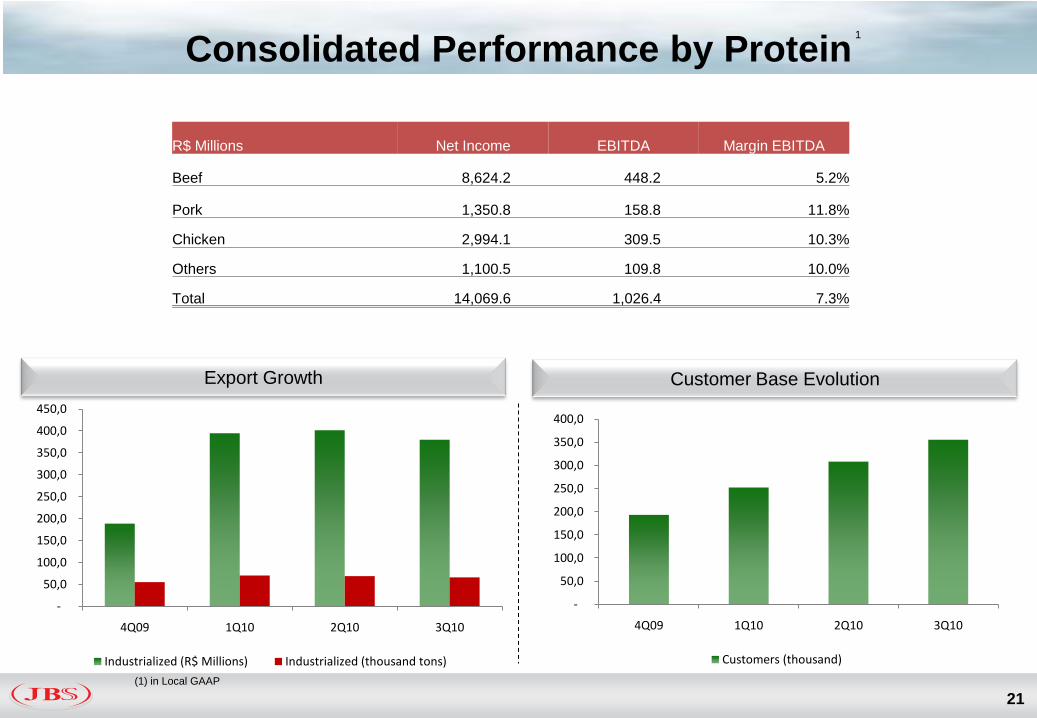

Consolidated Performance by Protein

21

Export Growth Customer Base Evolution

(1) in Local GAAP

R$ Millions Net Income EBITDA Margin EBITDA

Beef 8,624.2 448.2 5.2%

Pork 1,350.8 158.8 11.8%

Chicken 2,994.1 309.5 10.3%

Others 1,100.5 109.8 10.0%

Total 14,069.6 1,026.4 7.3%

1

-

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

4Q09 1Q10 2Q10 3Q10

Customers (thousand)

1

-

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

450,0

4Q09 1Q10 2Q10 3Q10

Industrialized (R$ Millions) Industrialized (thousand tons)

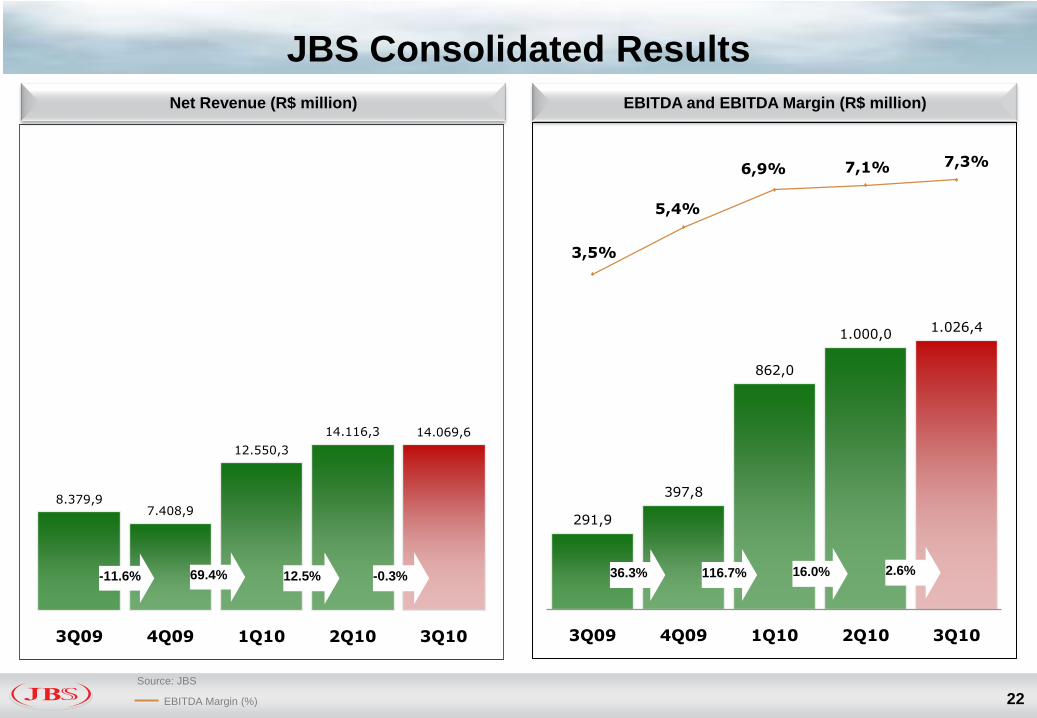

JBS Consolidated Results

22

Source: JBS

EBITDA Margin (%)

Net Revenue (R$ million) EBITDA and EBITDA Margin (R$ million)

8.379,97.408,9

12.550,3

14.116,3 14.069,6

3Q09 4Q09 1Q10 2Q10 3Q10

12.5%69.4% -0.3%-11.6%

291,9

397,8

862,0

1.000,01.026,4

3,5%

5,4%

6,9% 7,1% 7,3%

3Q09 4Q09 1Q10 2Q10 3Q10

36.3% 116.7% 16.0% 2.6%

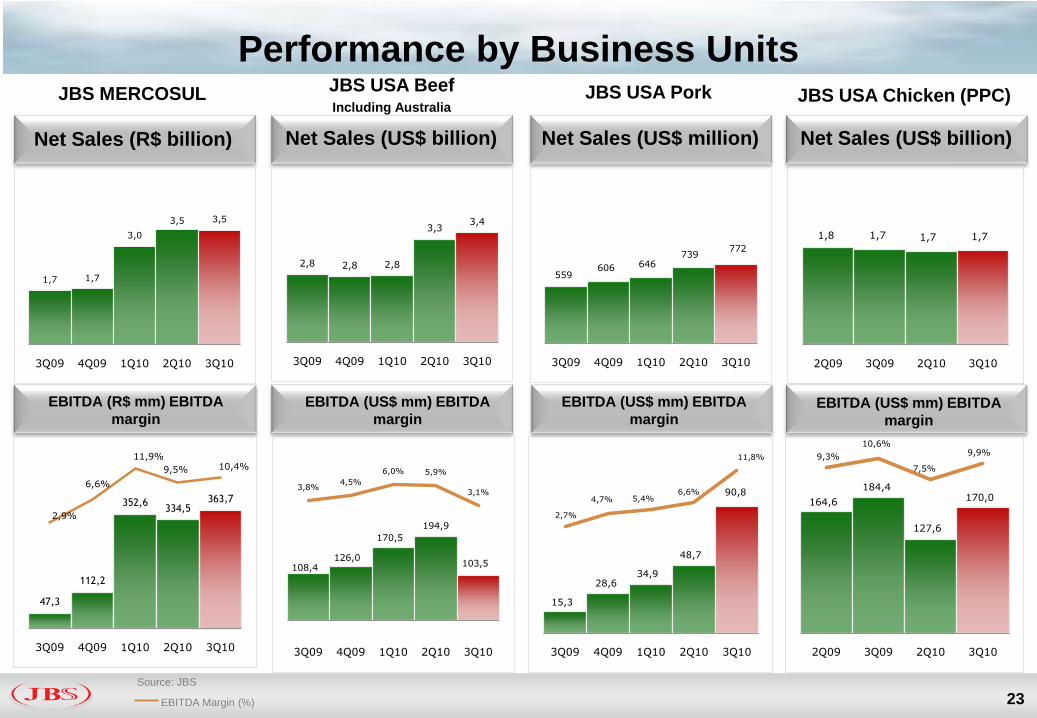

Performance by Business Units

23

Net Sales (US$ billion) Net Sales (US$ million) Net Sales (US$ billion)

EBITDA (US$ mm) EBITDA

margin

EBITDA (US$ mm) EBITDA

marginEBITDA (US$ mm) EBITDA

margin

JBS USA BeefIncluding Australia

JBS USA Pork JBS USA Chicken (PPC)

Source: JBS

EBITDA Margin (%)

Net Sales (R$ billion)

EBITDA (R$ mm) EBITDA

margin

JBS MERCOSUL

1,7 1,7

3,0

3,5 3,5

3Q09 4Q09 1Q10 2Q10 3Q10

2,8 2,8 2,8

3,33,4

3Q09 4Q09 1Q10 2Q10 3Q10

108,4126,0

170,5

194,9

103,5

3,8%4,5%

6,0% 5,9%

3,1%

3Q09 4Q09 1Q10 2Q10 3Q10

559606 646

739772

3Q09 4Q09 1Q10 2Q10 3Q10

15,3

28,634,9

48,7

90,8

2,7%

4,7% 5,4%6,6%

11,8%

3Q09 4Q09 1Q10 2Q10 3Q10

1,8 1,7 1,7 1,7

2Q09 3Q09 2Q10 3Q10

164,6

184,4

127,6

170,0

9,3%

10,6%

7,5%

9,9%

2Q09 3Q09 2Q10 3Q10

47,3

112,2

352,6334,5

363,7

2,9%

6,6%

11,9%

9,5% 10,4%

3Q09 4Q09 1Q10 2Q10 3Q10

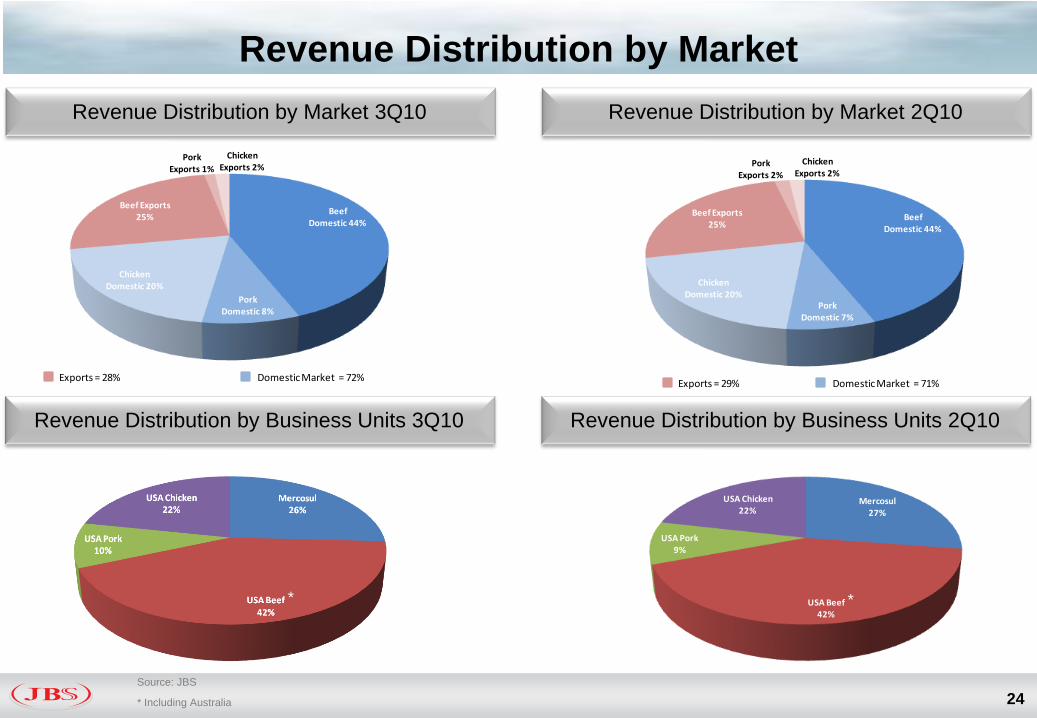

Revenue Distribution by Market

24

Revenue Distribution by Market 3Q10 Revenue Distribution by Market 2Q10

Revenue Distribution by Business Units 3Q10 Revenue Distribution by Business Units 2Q10

Beef Domestic 44%

Pork Domestic 7%

Chicken Domestic 20%

Beef Exports 25%

Pork Exports 2%

Chicken Exports 2%

Exports = 29% Domestic Market = 71%

Source: JBS

* Including Australia

Mercosul27%

USA Beef42%

USA Pork9%

USA Chicken22%

* *

Beef Domestic 44%

Pork Domestic 8%

Chicken Domestic 20%

Beef Exports 25%

Pork Exports 1%

Chicken Exports 2%

Exports = 28% Domestic Market = 72%

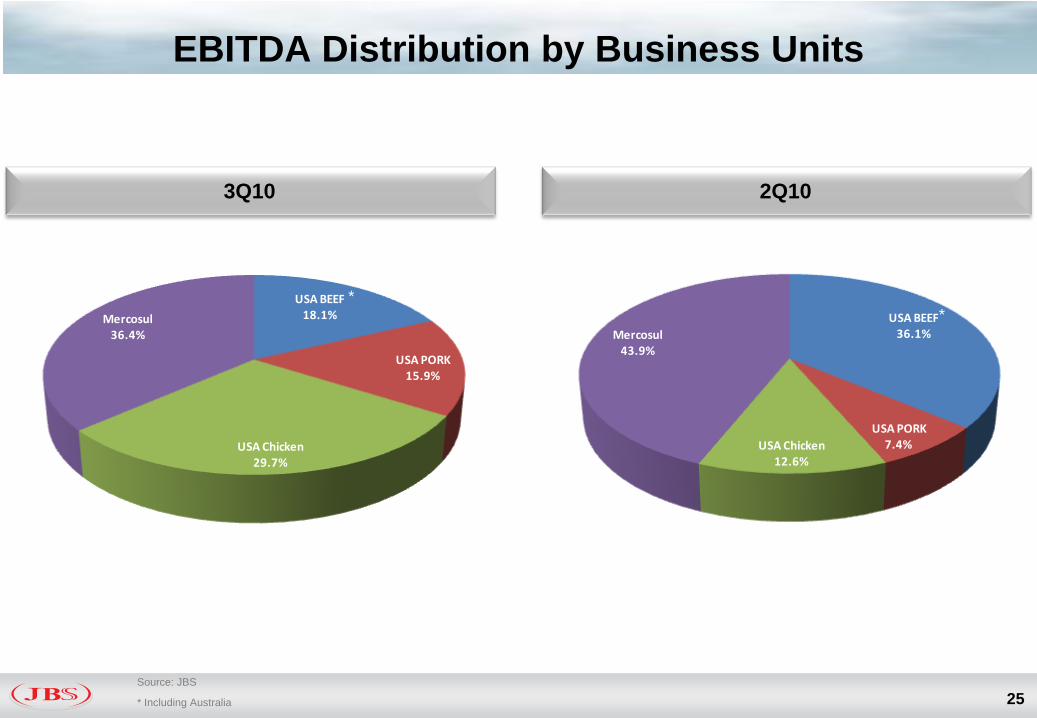

EBITDA Distribution by Business Units

25

3Q10 2Q10

USA BEEF18.1%

USA PORK15.9%

USA Chicken29.7%

Mercosul36.4%

USA BEEF36.1%

USA PORK7.4%USA Chicken

12.6%

Mercosul43.9%

Source: JBS

* Including Australia

**

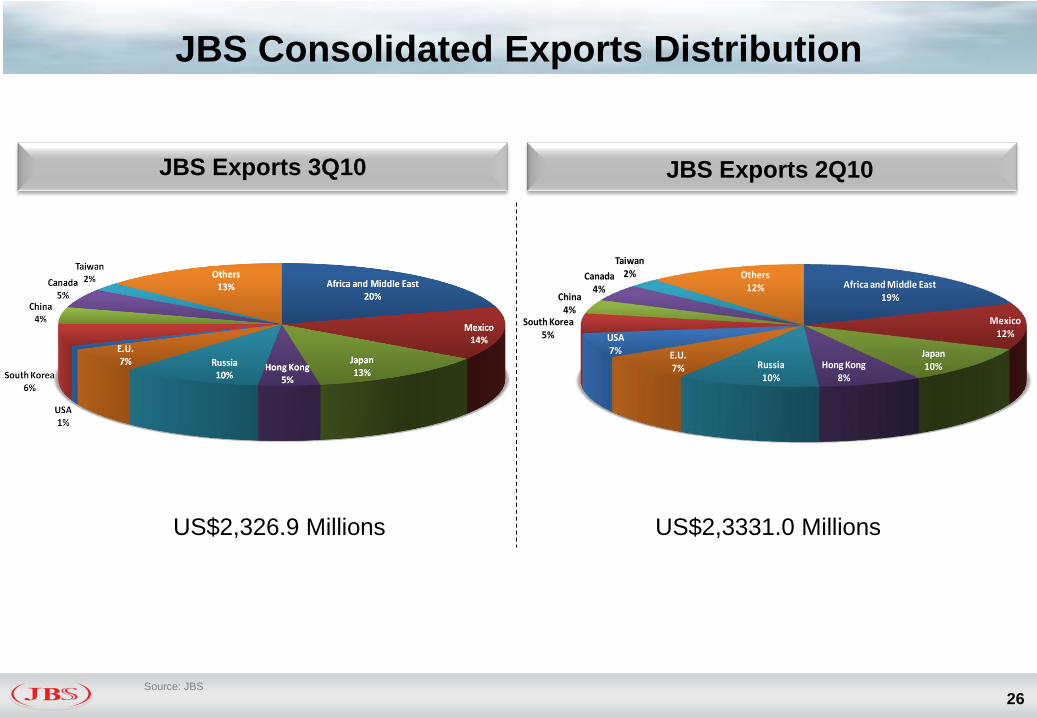

JBS Consolidated Exports Distribution

26

JBS Exports 3Q10 JBS Exports 2Q10

US$2,3331.0 MillionsUS$2,326.9 Millions

Source: JBS

Africa and Middle East19%

Mexico12%

Japan10%Hong Kong

8%Russia

10%

E.U.7%

USA7%

South Korea5%

China4%

Canada4%

Taiwan2% Others

12%

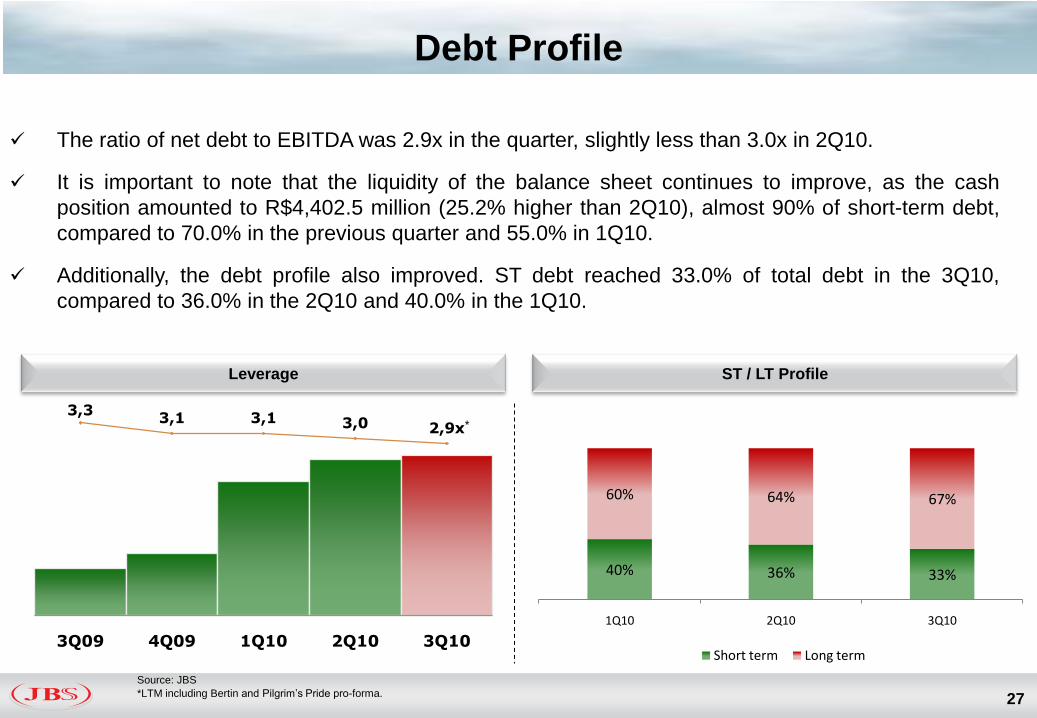

Debt Profile

27

The ratio of net debt to EBITDA was 2.9x in the quarter, slightly less than 3.0x in 2Q10.

It is important to note that the liquidity of the balance sheet continues to improve, as the cash

position amounted to R$4,402.5 million (25.2% higher than 2Q10), almost 90% of short-term debt,

compared to 70.0% in the previous quarter and 55.0% in 1Q10.

Additionally, the debt profile also improved. ST debt reached 33.0% of total debt in the 3Q10,

compared to 36.0% in the 2Q10 and 40.0% in the 1Q10.

*3,3

3,1 3,1 3,0 2,9x

3Q09 4Q09 1Q10 2Q10 3Q10

Leverage ST / LT Profile

40% 36% 33%

60% 64% 67%

1Q10 2Q10 3Q10

Short term Long term

Source: JBS

*LTM including Bertin and Pilgrim’s Pride pro-forma.

Agenda

28

Market Overview

JBSS3

Analysis and

Measures

Company Overview

3Q10 Highlights

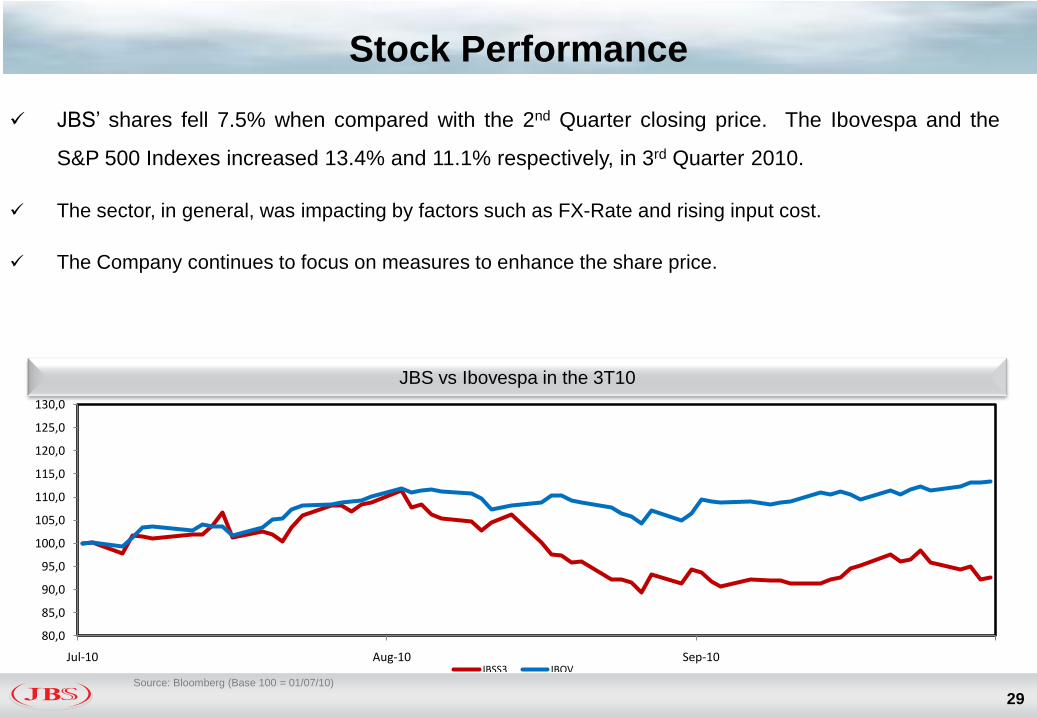

Stock Performance

29Source: Bloomberg (Base 100 = 01/07/10)

JBS’ shares fell 7.5% when compared with the 2nd Quarter closing price. The Ibovespa and the

S&P 500 Indexes increased 13.4% and 11.1% respectively, in 3rd Quarter 2010.

The sector, in general, was impacting by factors such as FX-Rate and rising input cost.

The Company continues to focus on measures to enhance the share price.

JBS vs Ibovespa in the 3T10

80,0

85,0

90,0

95,0

100,0

105,0

110,0

115,0

120,0

125,0

130,0

Jul-10 Aug-10 Sep-10JBSS3 IBOV

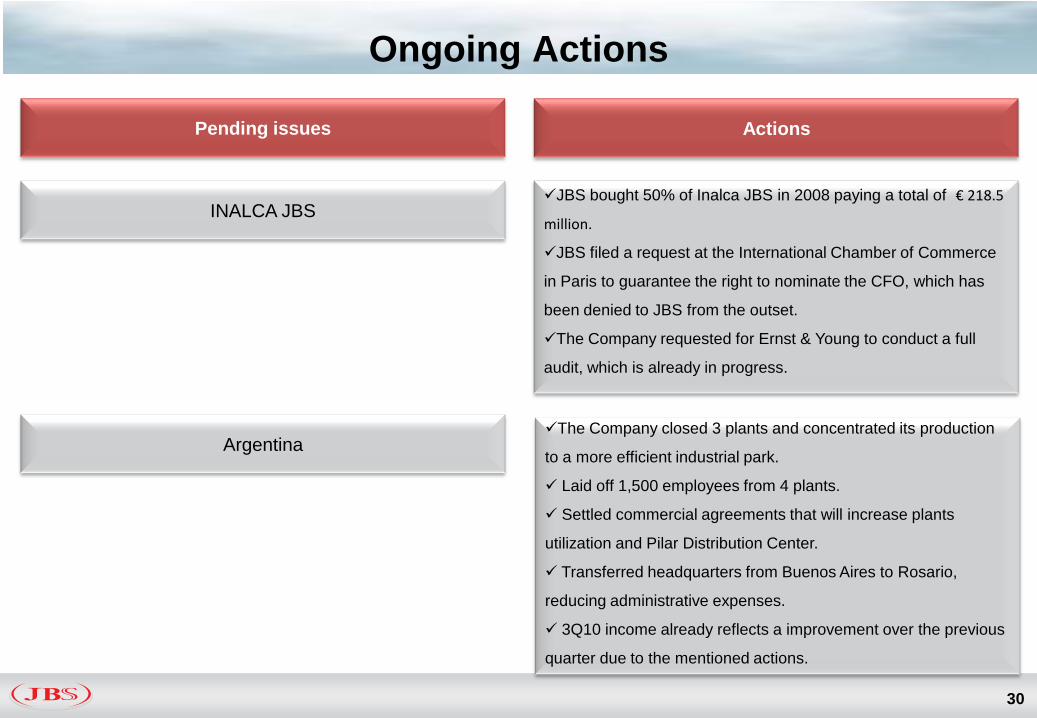

Ongoing Actions

30

INALCA JBSJBS bought 50% of Inalca JBS in 2008 paying a total of € 218.5

million.

JBS filed a request at the International Chamber of Commerce

in Paris to guarantee the right to nominate the CFO, which has

been denied to JBS from the outset.

The Company requested for Ernst & Young to conduct a full

audit, which is already in progress.

Argentina

Pending issues Actions

The Company closed 3 plants and concentrated its production

to a more efficient industrial park.

Laid off 1,500 employees from 4 plants.

Settled commercial agreements that will increase plants

utilization and Pilar Distribution Center.

Transferred headquarters from Buenos Aires to Rosario,

reducing administrative expenses.

3Q10 income already reflects a improvement over the previous

quarter due to the mentioned actions.

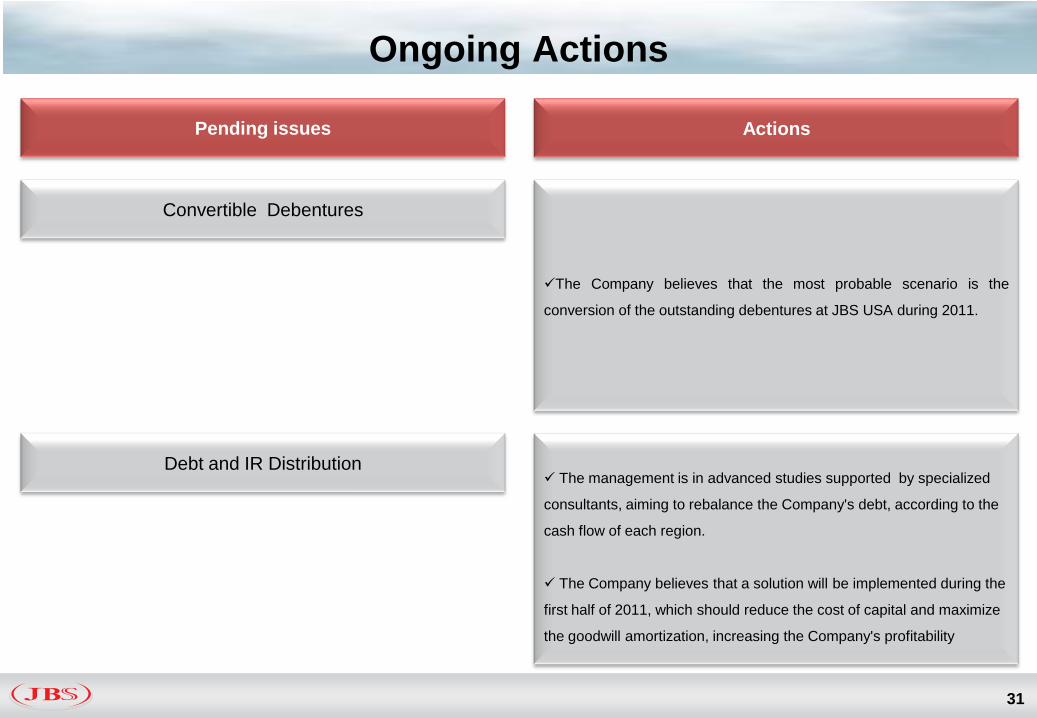

Ongoing Actions

31

Convertible Debentures

The Company believes that the most probable scenario is the

conversion of the outstanding debentures at JBS USA during 2011.

Debt and IR Distribution

Pending issues Actions

The management is in advanced studies supported by specialized

consultants, aiming to rebalance the Company's debt, according to the

cash flow of each region.

The Company believes that a solution will be implemented during the

first half of 2011, which should reduce the cost of capital and maximize

the goodwill amortization, increasing the Company's profitability

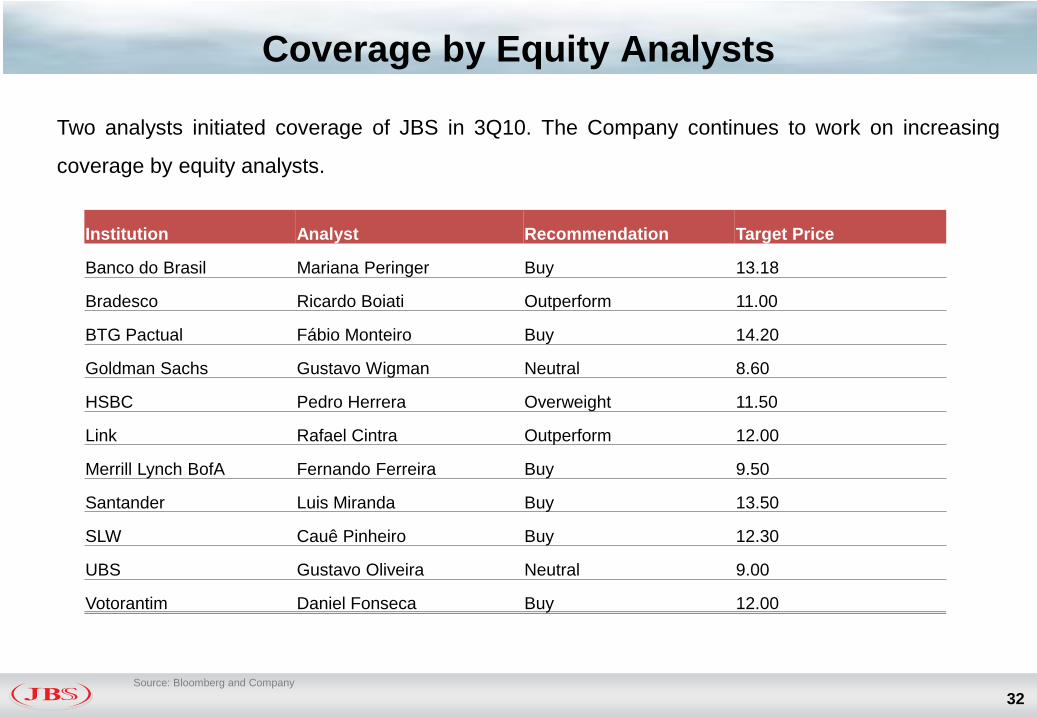

Coverage by Equity Analysts

32

Two analysts initiated coverage of JBS in 3Q10. The Company continues to work on increasing

coverage by equity analysts.

Source: Bloomberg and Company

Institution Analyst Recommendation Target Price

Banco do Brasil Mariana Peringer Buy 13.18

Bradesco Ricardo Boiati Outperform 11.00

BTG Pactual Fábio Monteiro Buy 14.20

Goldman Sachs Gustavo Wigman Neutral 8.60

HSBC Pedro Herrera Overweight 11.50

Link Rafael Cintra Outperform 12.00

Merrill Lynch BofA Fernando Ferreira Buy 9.50

Santander Luis Miranda Buy 13.50

SLW Cauê Pinheiro Buy 12.30

UBS Gustavo Oliveira Neutral 9.00

Votorantim Daniel Fonseca Buy 12.00

Final Remarks

33

The efficiency gains, business diversification of the Company and expansion of the direct distribution

have been more than offset the increase in some input costs.

Global demand for protein continues solid and the Company believes that it can benefit from this

scenario through its market penetration around the world.

The Company remains committed to reducing its financial leverage.

The Company's management is taking the measures to address outstanding issues in order to

enhance share value.

JBS’ customer base continues to grow organically, particularly in Mercosul, and the Company remains

committed to expanding the global direct distribution

34“In God We Trust, Nature We Respect”

IR Contacts:

+55 11 3144 4447

www.jbs.com.br/ir

Thank You!

Related Documents