International Accounting and Financial Reporting Winter 2009 William F. O’Brien, MBA, CPA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Accounting and Financial Reporting

Winter 2009

William F. O’Brien, MBA, CPA

Session III

From My Way to Our Way

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

3

Session III Objectives

Hofstede and Gray assessment How did we get to where we are Arguments for harmonization, convergence

and adoption Arguments against harmonization,

convergence and adoption Influence of culture

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

4

Hofstede’s Cultural Dimensions

Individualism versus collectivism Power distance (hierarchical order) Uncertainty avoidance Masculine versus feminine characteristics Long-term orientation

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

5

Gray’s Accounting Values

Professionalism versus statutory control Uniformity versus flexibility Conservatism versus optimism Secrecy versus transparency

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

6

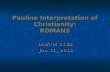

Hofstede-Gray MatrixProf. St.

Cont.Unif. Flex. Cons. Opt. Secr. Trans.

Indiv. + - - + - + - +Collect. - + + - + - + -Large PD. - + + - n/a n/a + -Small PD. + - - + n/a n/a - +Uncert. Avoid.

- + + - + - + -

No Unc. Avoid.

+ - - + - + - +

Masc. + n/a n/a n/a - + - +Fem. - n/a n/a n/a + - + -Short. + - n/a n/a - + - +Long - + n/a n/a + - + -

GH

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

7

Cultural Dimensions

Gray’s Cultural Influences

External Influences

Ecological Influences

Institutional Consequences

Actg. SystemsActg. Values

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

8

Authority and Enforcement

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

9

Accounting Values and Societal Values

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

10

Why a Single Set of Standards

A level playing field Common rules for a global economy Consistent high quality standards

Efficiency and effectiveness Improved understanding Cost effective approach

10

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

11

History of Prior Attempts The problem: A worldwide Tower of

Accounting Babel The solution?:

The U.S. way or the highway Harmonization Convergence Adoption of IFRS

11

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

12

U.S. GAAP—the Only Way

Before Enron and WorldCom: U.S. GAAP is the highest quality financial reporting in the world

After Enron and WorldCom: Let’s talk

12

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

13

Harmonization

A perceived win-win Countries keep their own standards Differences are minimized

Close doesn’t count Inconsistencies remained Comparability problems continued

13

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

14

Convergence The best of the best

Define “best” Local standards remain

Pronouncements are jointly produced but separately issued

Minor differences continue Define “minor” difference

However, a necessary precursor to full adoption

14

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

15

Current Convergence Projects

The Norwalk Agreement – 2002 FASB – IASB commitment to mutual

development of standards On-going recommitments to conclusion

2006 and 2008 Conceptual Framework Project

The foundation of financial accounting theory and financial statement format

15

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

16

Status of 11 Convergence Projects

• 4 complete: Bus. combinations Consolidations Derecognition Fair value

• Intangibles deleted• Financial instruments “in

process”

16

• 5 Planned for 2011: F/S presentation Leases Liabilities and equity Revenue recognition Post employment

benefits

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

17

Rationale For and Against a Single

Standard Rationale for

Efficient flow of capital Comparability of information Reduction in administrative cost

Rationale against Neither practical nor necessary One size does not fit all

May be costly for developing regions Does not address local business practices

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

18

Pressures1 for a Single Standard

Investors Reliability of cross-border investments

Multinationals Availability of foreign capital Reduced cost of financial statement preparation

Regulators Reduced cost of regulation. (High cost might impair cross-border flow of

capital) Securities exchanges

Growth of stock exchange volume Emerging economies

Urgency for accounting standard development Avoidance of costly reconciliations

1Indifferent with respect to rationale

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

19

Obstacles1 against a Single Standard

Corporate/country self interest Nationalism Absence of a strong accounting profession “Big GAAP” versus “Little GAAP” Emotionalism Debate over rules-based versus principles-

based standards

1Indifferent with respect to rationale

INTERNATIONAL ACCOUNTING & FINANCIAL REPORTING-2010

20

Key Points-Session III Hofstede-Gray dynamic There is a real difference between “my way”

and “our way” There are persuasive arguments for and

against a single standard system

Related Documents