Short Presentation Ventura Securities Ltd. by On Jagran Prakashan

Jagran Prakashan coverage by Ventura Securities

Jul 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Short Presentation

Ventura Securities Ltd.

by

On

Jagran Prakashan

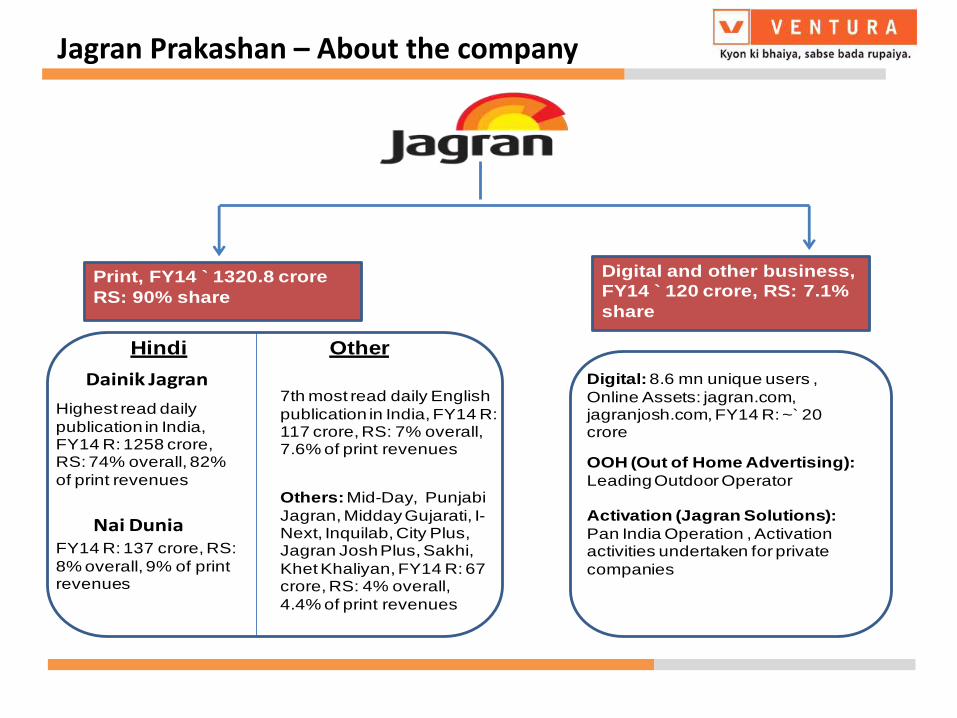

Jagran Prakashan – About the company

Nai Dunia

Print, FY14 ` 1320.8 crore

RS: 90% share

Hindi Other

Highest read daily

publication in India, FY14 R: 1258 crore, RS: 74% overall, 82%

of print revenues

Dainik Jagran

FY14 R: 137 crore, RS:

8% overall, 9% of print revenues

7th most read daily English

publication in India, FY14 R: 117 crore, RS: 7% overall, 7.6% of print revenues

Others: Mid-Day, Punjabi

Jagran, Midday Gujarati, I-Next, Inquilab, City Plus, Jagran Josh Plus, Sakhi,

Khet Khaliyan, FY14 R: 67 crore, RS: 4% overall,

4.4% of print revenues

Digital and other business,

FY14 ` 120 crore, RS: 7.1%

share

Digital: 8.6 mn unique users ,

Online Assets: jagran.com, jagranjosh.com, FY14 R: ~` 20 crore

OOH (Out of Home Advertising):

Leading Outdoor Operator

Activation (Jagran Solutions):

Pan India Operation , Activation activities undertaken for private

companies

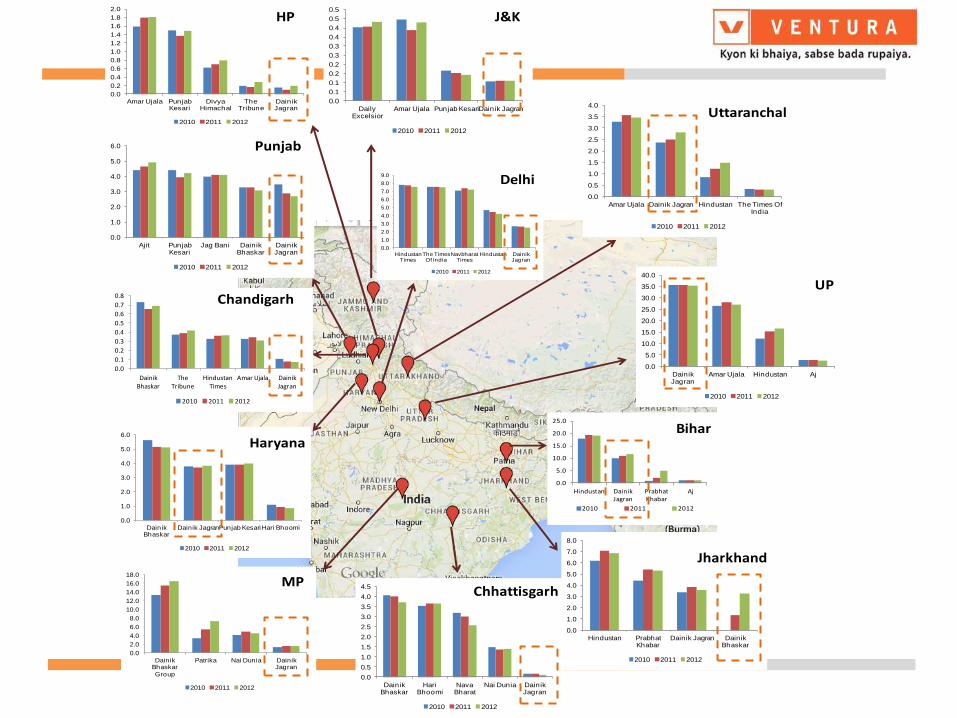

Enjoys leadership position in the large, high growth markets

•JPL derives ~75% of revenues through Dainik Jagran, of which advertising revenues accounted for 76%

of revenues in FY14, with circulation revenues accounting for the rest.

•According to the Indian Readership Survey, 2013 (IRS), Dainik Jagran is the highest read publication in

India with a weekly readership of 15.5 mn followed by Hindustan having a weekly readership of 14.2 mn.

Publication Language Readership ( in mn)

Dainik Jagran Hindi 15.5

Hindustan Hindi 14.2

Dainik Bhaskar Hindi 12.9

Malayala Manorama Malayalam 8.6

Daily Thanthi Tamil 8.2

Rajasthan Patrika Hindi 7.7

The Times Of India English 7.3

Amar Ujala Hindi 7.1

Mathrubhumi Malayalam 6.1

Lokmat Marathi 5.6

Source: IRS 2013

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Dainik Bhaskar

The Tribune

Hindustan Times

Amar Ujala Dainik Jagran

2010 2011 2012

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Dainik Bhaskar

Hari Bhoomi

Nava Bharat

Nai Dunia Dainik Jagran

2010 2011 2012

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Hindustan Times

The Times Of India

Navbharat Times

Hindustan Dainik Jagran

2010 2011 2012

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Dainik Bhaskar

Dainik JagranPunjab KesariHari Bhoomi

2010 2011 2012

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Amar Ujala Punjab Kesari

Divya Himachal

The Tribune

Dainik Jagran

2010 2011 2012

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

0.4

0.5

0.5

Daily Excelsior

Amar Ujala Punjab KesariDainik Jagran

2010 2011 2012

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Hindustan Prabhat Khabar

Dainik Jagran Dainik Bhaskar

2010 2011 20120.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Dainik Bhaskar

Group

Patrika Nai Dunia Dainik Jagran

2010 2011 2012

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ajit Punjab Kesari

Jag Bani Dainik Bhaskar

Dainik Jagran

2010 2011 2012

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Dainik Jagran

Amar Ujala Hindustan Aj

2010 2011 2012

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Amar Ujala Dainik Jagran Hindustan The Times Of India

2010 2011 2012

0.0

5.0

10.0

15.0

20.0

25.0

Hindustan Dainik Jagran

Prabhat Khabar

Aj

2010 2011 2012

HP J&K

Uttaranchal

Bihar

Jharkhand

ChhattisgarhMP

Haryana

ChandigarhUP

Delhi

Punjab

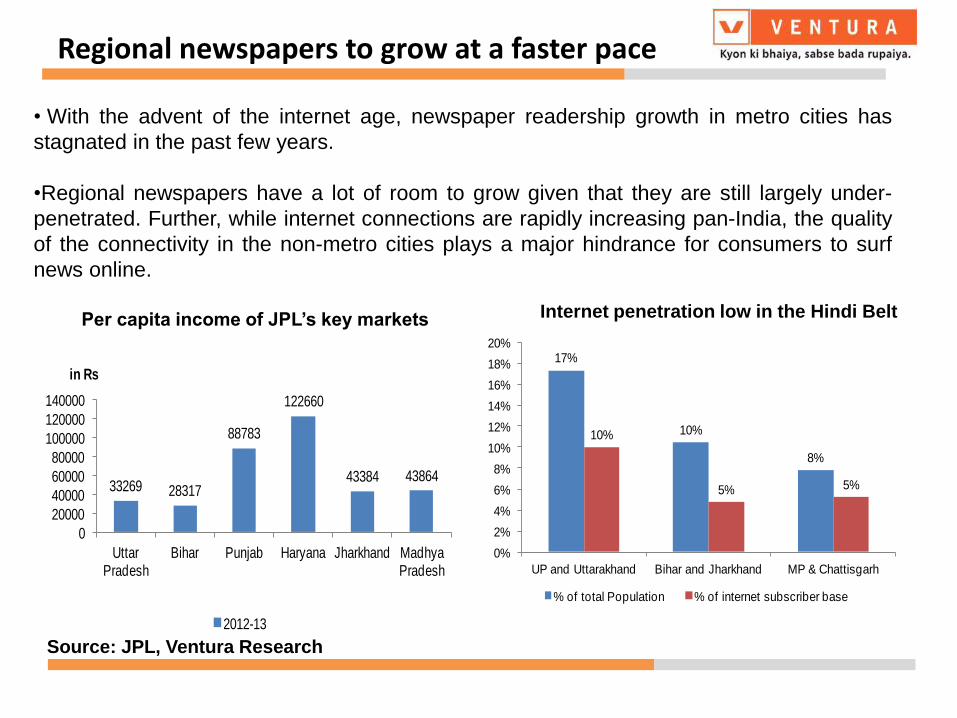

Regional newspapers to grow at a faster pace

• With the advent of the internet age, newspaper readership growth in metro cities has

stagnated in the past few years.

•Regional newspapers have a lot of room to grow given that they are still largely under-

penetrated. Further, while internet connections are rapidly increasing pan-India, the quality

of the connectivity in the non-metro cities plays a major hindrance for consumers to surf

news online.

33269 28317

88783

122660

43384 43864

0

20000

40000

60000

80000

100000

120000

140000

Uttar Pradesh

Bihar Punjab Haryana Jharkhand Madhya Pradesh

in Rs

2012-13

Per capita income of JPL’s key markets

17%

10%

8%

10%

5% 5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

UP and Uttarakhand Bihar and Jharkhand MP & Chattisgarh

% of total Population % of internet subscriber base

Internet penetration low in the Hindi Belt

Source: JPL, Ventura Research

JPL’s print revenues to grow at a steady rate

• JPL’s print media division has consistently grown with expansion in new markets, launch of

new editions and acquisition of publications viz. Mid-Day in 2010 and Nai Duniya in 2012.

•Its print media revenues have grown at a 3 year CAGR of 12.2% as compared to the industry

average of 8% (Source: FICCI, KPMG 2014 Report).

• We expect print media revenues to grow at a steady 3 year CAGR of 10% to Rs 2049 crore

by FY17. The growth drivers will be yield and volume improvement led by pick-up in economy

and consequently higher corporate spending on advertisements.

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

500

1,000

1,500

2,000

2,500

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Revenues ( in Rs crs) Revenue growth (RHS)

in Rs crs

Expected 3

year CAGR

FY17E

Revenues

%

contribution

Dainik Jagran 9.6% 1656 81%

Mid-Day 4.4% 133 6%

Nai Dunia 10.2% 183 9%

Others 4.3% 76 4%

Total 12.2% 2049

Outdoor and Activation business: Shift in Strategy

• Outdoor and Activation business includes JPL’s digital, OOH and Activation segments.

•JPL’s main digital assets: jagran.com and jagranjosh.com clock 168 mn page views per

month. At Rs 17-18 crs of revenue, the company currently earns revenues Rs 21 per user,

expect 30-40% CAGR in this segment

• JPL is focusing on more private sector contracts in its outdoor and activation segments

instead of public/government contracts that it undertook in the past. Stuck receivables an

issue in public contracts. Winding down government contracts will result in revenue loss in the

next two years.

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

FY13 FY14 FY15E FY16E FY17E

Revenues ( in Rs crs)

We expect this segment

to clock revenues of Rs

94 crore in FY17

0%

2%

4%

6%

8%

10%

12%

14%

0

500

1000

1500

2000

2500

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Revenues ( in Rs crs) Revenue growth (RHS)

Jagran Prakashan – Financial Performance

Revenues to grow at 3 yr CAGR of 8% to Rs

2142 crores by FY17

480

500

520

540

560

580

600

620

640

Jan

-10

Ap

r-10

Jul-

10

Oct-

10

Jan

-11

Ap

r-11

Jul-

11

Oct-

11

Jan

-12

Ap

r-12

Jul-

12

Oct-

12

Jan

-13

Ap

r-13

Jul-

13

Oct-

13

Jan

-14

Ap

r-14

Jul-

14

Oct-

14

Jan

-15

USD per tonne

Newsprint prices on a declining trend…

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

FY11 FY12 FY13 FY14 FY15EFY16EFY17E

Overall Dainik Jagran Mid-Day

Nai Dunia Others

…hence overall EBITDA margin to expand

to 25.7% in FY17

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0%

5%

10%

15%

20%

25%

30%

35%

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

PAT margin RoE D/E (RHS)

PAT margin, ROE to improve; D/E on a decline

Radio City Acquisition by Jagran Prakashan

• Jagran Prakashan, in 2014, acquired 100% stake in Music Broadcasters Pvt. Ltd, which runs

the Radio City FM station for an enterprise value of ~Rs 410 crores (excluding Rs 200 crores

of Migration fee expected for renewal of Phase II licenses)

• Radio City has 20 stations, with 7 in the top metro cities wherein it enjoys a high listenership.

Mumbai Share % T.S.L Tarp%

Radio City 19.0 5.52 1.4

Big FM 17.5 6.03 1.3

Radio Mirchi 13.8 4.22 1.0

Fever FM 12.5 6.14 0.9

Red FM 12.1 4.11 0.9

Oye 3.2 3.12 0.2

Radio One 3.1 2.26 0.2

Delhi Share % T.S.L Tarp%

Fever FM 19.5 5.15 1.4

Radio City 13.0 3.54 1

Big FM 12.7 3.41 0.9

Radio Mirchi 12.6 3.27 0.9

Red FM 9.7 2.55 0.7

Oye 5.3 2.55 0.4

Radio One 2.6 1.34 0.2

Kolkatta Share % T.S.L Tarp%

Radio Mirchi 20.9 4.3 1.7

Big FM 17.2 5.2 1.4

Oye 10.2 3.4 0.8

Radio One 10.1 3.38 0.8

Red FM 8.4 2.56 0.7

Fever FM 7.2 3.05 0.6

Bengaluru Share % T.S.L Tarp%

Radio City 24.2 9.48 2.7

Big FM 21.0 8.09 2.4

Radio Mirchi 17.9 7.27 2

Fever FM 10.6 6.51 1.2

Red FM 6.6 4.2 0.8

Radio One 3.4 3.01 0.4

RAM ratings for Week 47 (All 25 years +, 16Nov to 22Nov, Mon-Sun 12AM-12AM)T.S.L = Time Spent Listening, Tarp%= Target Audience Rating Points are also known as ratings and are an estimate of the size of a specific

viewing audience to a channel, programme or timezone. 1 TARP is the equivalent of reaching 1% of the target audience.

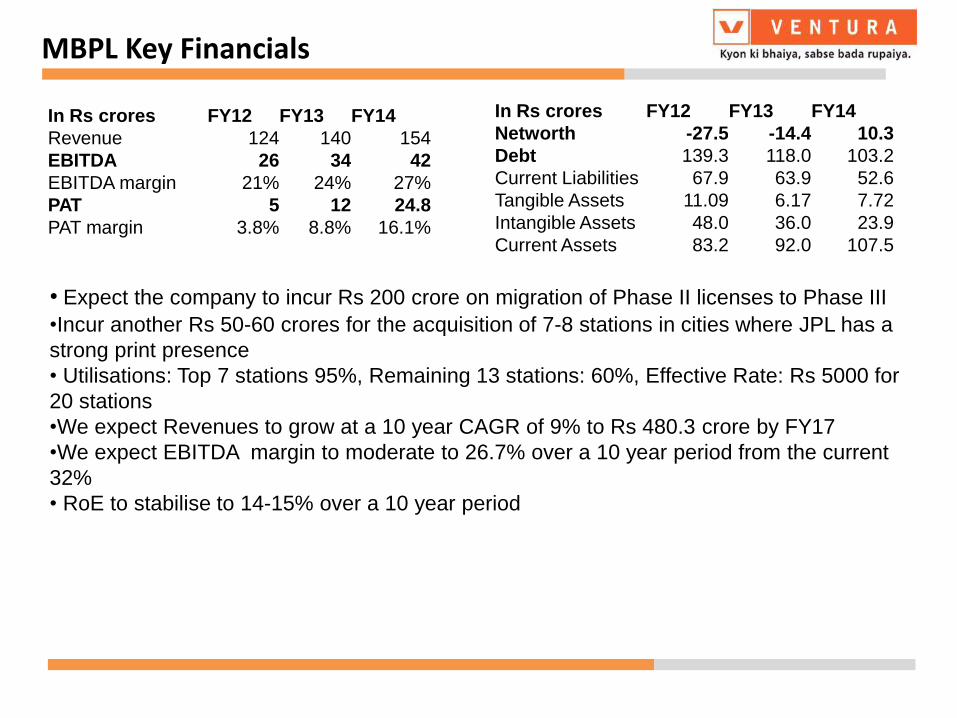

MBPL Key Financials

In Rs crores FY12 FY13 FY14

Revenue 124 140 154

EBITDA 26 34 42

EBITDA margin 21% 24% 27%

PAT 5 12 24.8

PAT margin 3.8% 8.8% 16.1%

• Expect the company to incur Rs 200 crore on migration of Phase II licenses to Phase III

•Incur another Rs 50-60 crores for the acquisition of 7-8 stations in cities where JPL has a

strong print presence

• Utilisations: Top 7 stations 95%, Remaining 13 stations: 60%, Effective Rate: Rs 5000 for

20 stations

•We expect Revenues to grow at a 10 year CAGR of 9% to Rs 480.3 crore by FY17

•We expect EBITDA margin to moderate to 26.7% over a 10 year period from the current

32%

• RoE to stabilise to 14-15% over a 10 year period

In Rs crores FY12 FY13 FY14

Networth -27.5 -14.4 10.3

Debt 139.3 118.0 103.2

Current Liabilities 67.9 63.9 52.6

Tangible Assets 11.09 6.17 7.72

Intangible Assets 48.0 36.0 23.9

Current Assets 83.2 92.0 107.5

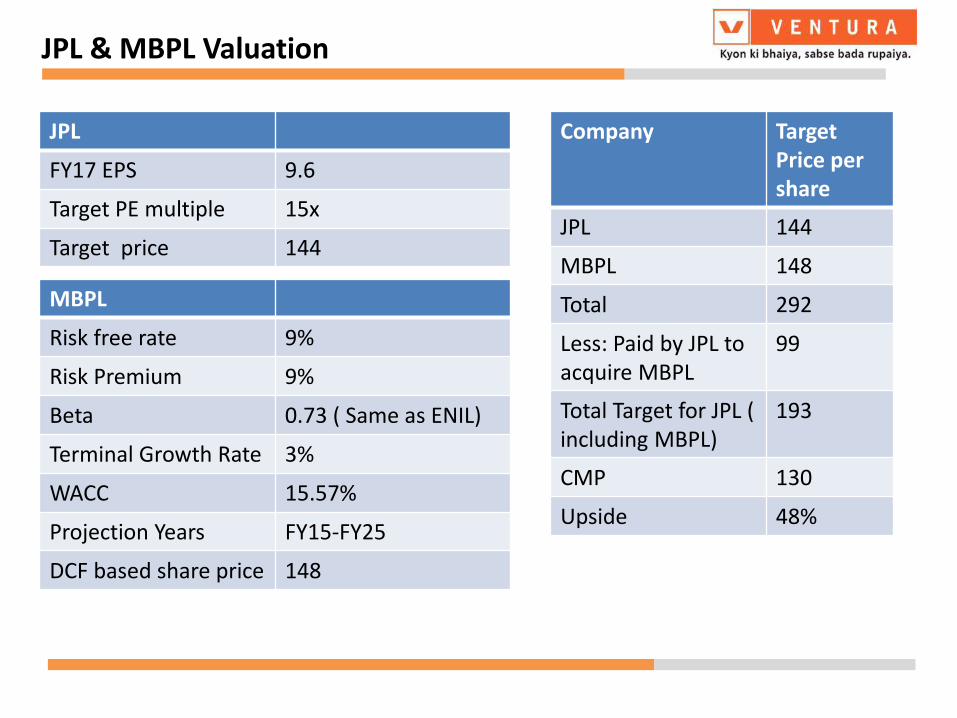

JPL & MBPL Valuation

JPL

FY17 EPS 9.6

Target PE multiple 15x

Target price 144

MBPL

Risk free rate 9%

Risk Premium 9%

Beta 0.73 ( Same as ENIL)

Terminal Growth Rate 3%

WACC 15.57%

Projection Years FY15-FY25

DCF based share price 148

Company Target Price per share

JPL 144

MBPL 148

Total 292

Less: Paid by JPL to acquire MBPL

99

Total Target for JPL ( including MBPL)

193

CMP 130

Upside 48%

Ventura Securities Limited

Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079

This report is neither an offer nor a solicitation to purchase or sell securities. The information and views expressed herein are believed to be

reliable, but no responsibility (or liability) is accepted for errors of fact or opinion. Writers and contributors may be trading in or have positions in

the securities mentioned in their articles. Neither Ventura Securities Limited nor any of the contributors accepts any liability arising out of the

above information/articles. Reproduction in whole or in part without written permission is prohibited. This report is for private circulation.

Related Documents