Worldtrade Management Services It is what it is. Or is it? The art of customs classification Trade Intelligence Asia Pacific June / July 2017 www.pwccustoms.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Worldtrade Management Services

It is what it is. Or is it?The art of customs classification

Trade Intelligence Asia PacificJune / July 2017

www.pwccustoms.com

2 PwC

Key intelligence

Implementation of nationwide customs clearance integration in China Page 19

Impact of India’s new GST regime on customs Page 22

A wider net to recover duties in Australia

Page 16

Philippines modifies its tariffsPage 32

New task force in Indonesia to focus on high-risk importersPage 25

Details on Thailand’s Customs Alliance programme

Page 40

3Trade Intelligence Asia Pacific June / July 2017

Trade Intelligence Asia Pacific seeks to capture the essence of selected issues that are of particular interest to clients of PwC. Our regional network of customs and international trade consultants routinely gather, analyse and disseminate information and knowledge to our clients. Based on studies as well as meetings and discussions that take place across the region with various trade and customs officials, we consolidate our findings into Trade Intelligence Asia Pacific.

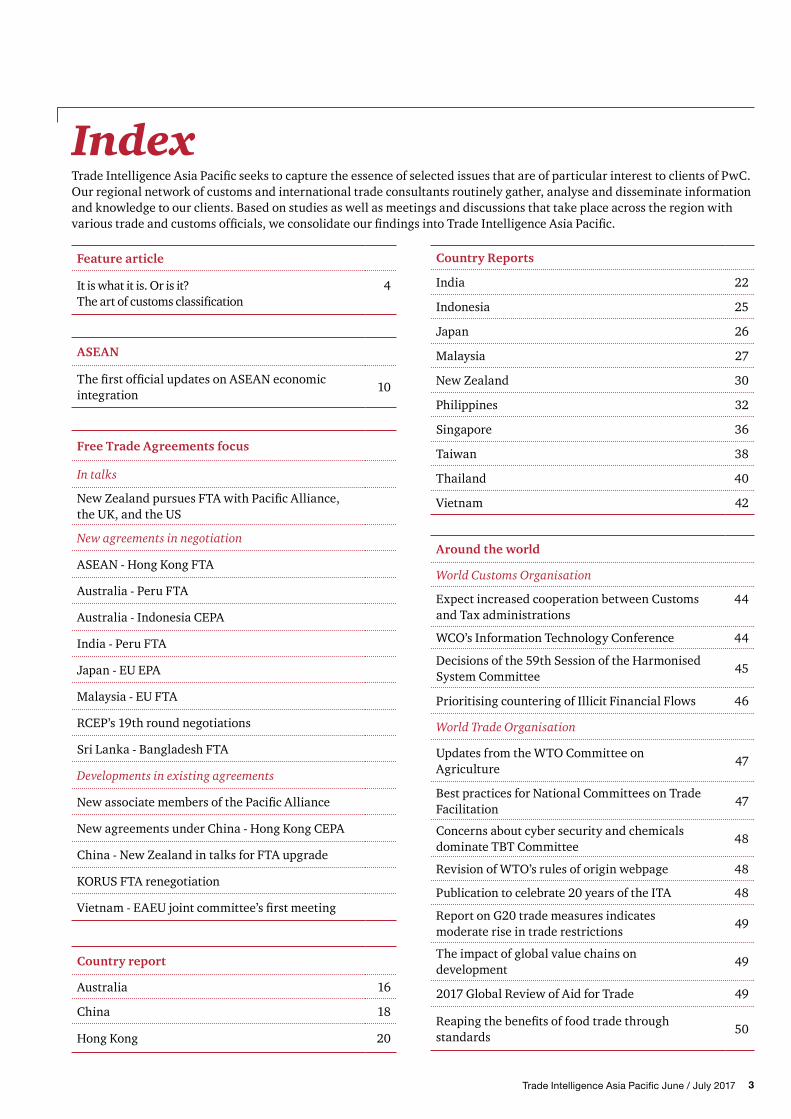

Index

Feature article

It is what it is. Or is it?The art of customs classification

4

ASEAN

The first official updates on ASEAN economic integration

10

Free Trade Agreements focus

In talks

New Zealand pursues FTA with Pacific Alliance, the UK, and the US

New agreements in negotiation

ASEAN - Hong Kong FTA

Australia - Peru FTA

Australia - Indonesia CEPA

India - Peru FTA

Japan - EU EPA

Malaysia - EU FTA

RCEP’s 19th round negotiations

Sri Lanka - Bangladesh FTA

Developments in existing agreements

New associate members of the Pacific Alliance

New agreements under China - Hong Kong CEPA

China - New Zealand in talks for FTA upgrade

KORUS FTA renegotiation

Vietnam - EAEU joint committee’s first meeting

Country report

Australia 16

China 18

Hong Kong 20

Country Reports

India 22

Indonesia 25

Japan 26

Malaysia 27

New Zealand 30

Philippines 32

Singapore 36

Taiwan 38

Thailand 40

Vietnam 42

Around the world

World Customs Organisation

Expect increased cooperation between Customs and Tax administrations

44

WCO’s Information Technology Conference 44

Decisions of the 59th Session of the Harmonised System Committee

45

Prioritising countering of Illicit Financial Flows 46

World Trade Organisation

Updates from the WTO Committee on Agriculture

47

Best practices for National Committees on Trade Facilitation

47

Concerns about cyber security and chemicals dominate TBT Committee

48

Revision of WTO’s rules of origin webpage 48

Publication to celebrate 20 years of the ITA 48

Report on G20 trade measures indicates moderate rise in trade restrictions

49

The impact of global value chains on development

49

2017 Global Review of Aid for Trade 49

Reaping the benefits of food trade through standards

50

4 PwC

It is what it is. Or is it?The art of customs classification

Accurate tariff classification is a fundamental obligation of importer compliance. Not only is it a process that dictates duty rates and eligibility for customs and trade programs - it is a cornerstone of a company’s risk profile.

It is therefore somewhat surprising that so many companies, small and large, do not have, or bother to find, the technical resources or leadership support for funding for an effective tariff classification compliance program. Good tariff classification essentially requires good data and a robust and intelligent process. Although in the Information Age, more and more data is available, one of the biggest issues importers face is getting and managing what they need. Complete data is paramount to classification but blind spots are common, because of a lack of understanding, inadequate processes, inappropriate resources, changing business characteristics, or simply a lack of care.

A successful classification program is one that is comprehensive, robust and prepared for change at multiple levels. Internally, most companies seek cost reduction opportunities but few are fortunate enough to catch potential errors before unfavorable consequences occur. Externally, decisions made by a national customs regime, and even at the World Customs Organization (WCO) level, introduce a challenges over time. The best classification solutions are those designed for a particular business model and agile enough to withstand regular shifts in ground.

In this article we look at some typical challenges that companies run into when classifying products for customs purposes, and what are some of the possible mitigations to consider to reduce risks and exposures.

5Trade Intelligence Asia Pacific June / July 2017

Global challenges

The WCO’s maintenance of the Harmonized System (HS) is a delicate balance of reducing classification uncertainty and staying relevant with modern technology. In recent history, the WCO’s five-year review cycle has occurred four times since the HS was implemented in 1998. While the HS Committee meets twice per year to review questions and disputes, it is difficult to ascertain whether these efforts create meaningful improvements across the board or if they are just enough to keep the massive obligation of global trade compliance at bay.

Recently, in its 59th session, the HS Committee published 30 amendments to the Explanatory Notes, 28 rulings, and 27 opinions covering a range of merchandise in various HS sections. This amount of decision-making seems fairly productive, considering the HS Committee is composed of representatives of the Convention’s 156 contracting parties. Given the speed of information today, one might wonder whether certain products and industries benefit more than others in terms of reducing classification uncertainty.

For example, the latest HS reform introduced a new HS heading 9620, titled “Monopods, bipods, tripods and similar articles”. The new heading noticeably omits a “parts of” provision, and while the WCO’s Explanatory Note (EN) to heading 9620 provides scope on the expression “similar articles” it does not explain how “parts” of these products should be classified. This leaves the door open for misclassification by importers and customs authorities alike.

While companies are not entitled to request amendments to the HS nomenclature, some countries have mechanisms in place that enable the trade community to help shape their national Harmonized Tariff Schedules. It may take years for a recommended EN change to reach the WCO level, but more participation at the national level is certain to have a trickle-up effect that will continue to decrease classification uncertainty over time.

National challenges

For companies that actively import into numerous countries, such as Multinational Corporations (MNCs), the most common difficulties with classification arise when specific terms or provisions of a national tariff schedule are undefined. Details surrounding the envisioned intent of scope for a particular tariff provision are frequently unavailable. In practice, it is often the customs authorities who get to define the provisions as they see fit.

6 PwC

Complicating matters further is the fact that formal guidance from customs authorities, if it does exist, may not be updated regularly and thus may not reflect the policy of the current customs administration. These issues coupled with the massive list of public customs classification rulings (in the US, the EU and assorted other jurisdictions), which many companies refer to despite known inconsistencies, become the fertile soil from which many classification questions grow.

Smaller companies often face classification challenges when entering new markets. When looking at a tariff schedule, most classification teams want to know just how detailed are the data requirements and whether their existing classification support is sufficient. Less experienced teams or individuals may be unaware that each WCO member country has the right to incorporate national-level Section and Chapter notes, and even national additions to the General Rules of Interpretation, which should be considered instruments and not obstacles to making a classification decision.

While the structure of the HS is designed to create a level playing field, the reality is that companies should expect some fragmentation in the specific types of data required around the world. Crafting a “defensible” classification position is wise, even if the ambiguity is only statistical in nature.

Classification mapping services are available to assist in navigating the differences of national tariff provision language, but most companies find that the classification process cannot be automated entirely because the required data elements for their products are not readily available. The most common approach for many MNCs is to settle on a product’s global classification number (i.e., a six-digit level HS code), and then identify what the additional data requirements are and how to satisfy them on a country-by-country basis. From there, other complicating factors, such as a national tariff schedule that changes unpredictably throughout the year, tend to make the classification process appear unstable at times.

An exception to the rule from one country skews statistics and compliance from a broader perspective. This is especially true for companies that import a wide range of products – it becomes a struggle to maintain classification consistency at the commodity level when a customs authority establishes a precedent or decision that is disharmonized globally.

Occasionally, Customs may even be forced to adjust its original classification decision so that it aligns with a decision from a national court case or other government agency directive. Keeping up with the myriad of decision-makers globally is no easy task, but the most prepared companies are those equipped to handle unexpected circumstances from any direction.

Our Managing Partner has two young daughters. Like many kids, they like toys and they like chocolate. One of the products they like is Kinder Joy – an egg-shaped product that contains a type of chocolate confectionary in one half, and a toy in the other. Fortunately, one of them likes the chocolate best, and the other one the toy, which is great for both budget purposes and peace in the house. But for customs classification purposes, it is a nightmare. Which of the two is it – a chocolate or a toy? Irrespective of duty rates, the conclusion will determine labelling requirements, applicability of health and safety regulations, food regulations etc. And all those can vary significantly by country.

Basically, it is a composite product that cannot be classified using GRI1. But to apply GRI3(b), a decision needs to be made as to its essential character. Asking our Partner’s two daughters will not help – they will have a very different opinion. Asking a broker, or an artificially intelligent robot, or even Customs, may not help much either. A company website description is also not very helpful in this respect: “Kinder Joy is the only product that combines the tastiness of a milky cream and a cocoa cream, with two crispy wafer-balls and many new & surprising toys.” Of course if neither the chocolate nor the toy part is more essential than the other, GRI3(c) will offer some respite. Otherwise, it may well be that an argument as to where in a shop the product can be found (in the confectionary section or with other toys) can be persuasive in arriving at a supportable classification conclusion.

7Trade Intelligence Asia Pacific June / July 2017

Furthermore, it is not uncommon for a company of any size to be challenged by Customs on a classification issue at some point. Based on our recent survey on managing customs and international trade across the Asia Pacific region, the largest (59%) proportion of company respondents indicated that classification was commonly challenged by customs authorities, higher than valuation (57%), origin (21%), and non-tariff measures (14%). In many cases, the practical question is a matter of whether a product should be classified in a code that has a higher rate of duty. Most customs regimes allow the importer only a short amount of time to respond to an inquiry relating to any material or functionality concerns, which for the unprepared often becomes a scramble to substantiate claims. If an importer relies on external resources (brokers, logistics service providers, etc.), they may find that the existing classification documentation is limited, or based on erroneous assumptions. If there is a lack of precedent in the matter, the tendency is to explain why the existing classification is correct, whereas best practice would be to also explain why the recommended new classification is wrong, should the circumstances permit.

Organizational challenges

While MNCs generally have more experience than companies just entering the global arena, the difficulties of maintaining a robust classification program are ultimately similar, regardless of company size. For manufacturers, one of the major challenges is getting access to technical information that is otherwise controlled and not publicly available. For resellers,

the difficulty often lies in the availability and accuracy of information obtained from other sources.

From either viewpoint, organizations that operate globally must ensure that translations, and even vernacular, do not lead to misunderstandings of product descriptions, capabilities, or uses. Most manufacturers utilize multiple levels of product descriptions (from broader group descriptions to item specific), which may be somewhat helpful to the classification process, but is just as likely to cause confusion for trading partners that lack visibility to the complete picture, and thus lead to inaccurate or unsupportable classifications.

More mature compliance programs are increasingly using in-house or packaged software solutions which integrate the management of product data with classification analysis documentation. While some of these solutions are better than others, those that retain the formatting from source documentation are typically a step ahead of the curve. Whereas the structure of the HS is set in a logical fashion, errors are less likely to occur when the classification team does not lose sight of the indentation levels of more complex national tariff schedules. Less experienced companies are likely to find that changes in staffing or service providers over time may lead to inconsistent classification determinations when viewed through a historical lens. The best practice to resolve internal classification differences is to consider the facts available at the time before deciding what course of action is necessary. Changes in the classification of merchandise can and do occur for

8 PwC

reasons stemming not only from changes in institutional or national policy, but also from technological advances that have the ability to disrupt industries altogether.

The success of a customs compliance program is directly related to the strength of its classification team. Whether led by an expert, or a master knowledge tool, the future of tariff classification will require continued learning.

Process challenges

Obviously, not all importers are the same. Different business models place different burdens on the classification process. Beyond mere data gathering issues, the greater challenge for many companies is the actual process of classification itself.

A common stumbling block for companies new to international trade, and even many experienced one, is the proper use of the tariff schedule. The General Rules of Interpretation should be quick and easy to understand, but instead read as legalese. Section and chapter notes are critical but depending on the product may require classification experts, engineers or chemists to explain in layman’s terms. The actual punctuation (e.g. commas, semi-colons) of a tariff heading is considered critical to the understanding and determination of correct classification, such that at least one customs regime has provided guidance to this effect.

With regard to the classification of complex products, or kits containing various goods, a deeper understanding of the concepts of classification is indispensable. A determination as to the “essential character” or “principal function” (see box) of a product may be necessary and a brief explanation should be documented as a best practice. Resources such as the WCO’s Explanatory Notes are supportive when considering advanced classification scenarios, but as reference materials that are not legally binding, such analyses benefit most from critical thinking and firm documentation.

Whether using best-in-class software solution or a limited master spreadsheet, periodic database reviews should be mandatory for high volume importers. By reviewing products in groups, an auditor may expect that the classification analysis is consistent throughout and that any outliers are adequately supported to explain the legitimacy of any exceptions. Similarly, the citation of any customs rulings or other guidance should be reviewed periodically to verify that the logic supporting the determination is still valid. Proactively seeking errors in a classification database will limit a company’s risk exposure and hopefully reduce the likelihood of a successful challenge by Customs.

Regardless of size, all companies should have a written classification procedure established as part of their compliance programs. The strongest procedures are those having contingency plans that enable a company to handle unexpected situations, such as when a change in classification is required. For example, should a new ruling be published by a customs authority that revokes a previous ruling, then the procedure should state what immediate corrective actions, if any, should be taken in the company’s classification database or active imports universe.

Common problems

Compliance programs that frequently experience setbacks are usually those that do not have the proper controls in place. In terms of classification, errors and inconsistencies can be attributed to lack of oversight or understanding of the core concepts. Whereas the process of classification can be time consuming for the inexperienced, companies that allow their brokers or other service providers to oversimplify that process may suffer otherwise avoidable consequences.

A company’s risk profile is further amplified when classification is needed for large volumes of products with quick deadlines. Classifying solely by product description is a common disadvantage, since a description alone generally lacks

9Trade Intelligence Asia Pacific June / July 2017

the depth of information needed to classify. Additionally, classification decisions made without fully documenting the relevant legal support are baseless on their own. In US speak, they do not show “reasonable care”.

Moreover, classification services that allow indiscriminately high error tolerance rates may create additional problems down the road. In jurisdictions where penalties are most severe, customs authorities may find that a disorganized classification process is responsible for creating noncompliance in others areas. We worked with an importer in China who was downgraded 4 notches on its old importer ranking scale because of the flippant approach the company had taken to classification, even though upon close analysis it turned out to have overpaid duties in the process for years. The result was extensive clearance inspections, more frequent audits, slower time-to-marker, and a painful five year period of gradually moving back up the ranking scales.

Best-in-class solutions

Preparation is the key for a company to maximize its compliance goals. Creating tools such as commodity criteria templates, decision trees, product checklists and review worksheets are supportive from process and organizational perspectives, but for some companies this may not be enough.

A robust classification process is one that incorporates multiple levels of internal review for accuracy, consistency, and continued assurance. Periodic database review is a necessary step to mitigating risk, but the process does not end there. The manner in which a company reacts to a need for change in a product’s classification is indicative of the success of the compliance program as a whole.A dedicated classification team should have experience in reviewing technical data in various industries. The process of assembling a sizable team with the appropriate knowledge and building experience takes time. Whereas a classification “expert” will inevitably

make a mistake at some point, the real value of retaining such a trusted classifier lies in his or her ability to think ahead.Achieving optimal classification compliance at the lowest cost ultimately comes down to the most agile and adaptable processes. Best-in-class will be different for different organizations. Best-in-class should essentially be fit-for-purpose. Whether that requires a large in-house dedicated team, a clever IT based solution, or an outsourced process, is a decision each company needs to make for itself. Applying a fair dose of ROI analysis (see our October/November 2016 issue of Trade Intelligence) will be instrumental in making the right choice.

For more information on PwC’s customs classification outsourcing service, please check our website http://www.pwccustoms.com/en/services/ensure-comp/outsourced-global-customs-classification-services.html or contact Paul Sumner ([email protected]) or Jonathan Wiens ([email protected])

10 PwC

ASEANThe first official updates on ASEAN economic integration

To celebrate its 50th anniversary and the second year of the ASEAN Economic Community (AEC), the ASEAN Secretariat published its inaugural issue of the ASEAN Economic Integration Brief (AEIB) aimed at providing updates to the public on ASEAN economic integration and on global developments in relation to ASEAN.

In its first issue, the publication provides an overview of the region’s economic outlook and provides an update on the key initiatives and developments in relation to the AEC. It also includes a special feature article written by Mr Pascal Lamy, former Director General of the World Trade Organisation (WTO).

A copy of the full Brief can be obtained from the following link: http://asean.org/storage/2017/06/AEIB_No.01-June-2017_rev.pdf

The key developments surrounding the ASEAN Economic Community since its formal establishment on 31 December 2015 and what else can be expected in the near future in terms of cross-border trade are as follows.

Key initiatives and developments of the ASEAN Economic Community

AEC Blueprint 2025 • Developed to guide the strategic direction of ASEANs regional economic integration for the next 10 years

• It will be supported by AEC 2025 Monitoring and Evaluation (M&E) Framework. This replaces the AEC 2015 Scorecard. This framework will be supported by the ASEAN Community Statistical System (ACSS) to monitor areas beyond compliance to evaluate potential impact.

AEC 2025 Consolidated Strategic Action Plan (CSAP) on 6 February 2017

• Serves as an operational framework for the Blueprint elaborating strategic measures as operationalised by strategic action plans that will be pursued by relevant ASEAN sectoral bodies in order to achieve the five characteristics of the AEC 2025. It is aimed at information outreach and will be updated periodically.

ASEAN Trade Facilitation Framework

• Adopted in 2016, at the ASEAN Economic Ministers’ (AEM) 23rd Retreat in March 2017, a target to reduce 10% of trade transaction costs by 2020 was set. As part of the framework. The ASEAN Trade Facilitation Joint Consultative Committee (ATF-JCC) was set up with both public and private sector representatives in addition to other sectoral bodies.

• The entry into force of the World Trade Organization Agreement on Trade Facilitation in February 2017 is also expected to spur further trade facilitation initiatives

ASEAN Trade Repository (ATR)

• A one stop online database on ASEAN trade and customs related information. It is also expected to provide public access to the National Trade Repositories (NTRs).

11Trade Intelligence Asia Pacific June / July 2017

Key initiatives and developments of the ASEAN Economic Community

ASEAN Tariff Finder • A cost free search engine for tariff and tariff related information for all ASEAN free trade agreements.

ASEAN Solutions for Investments, Services and Trade (ASSIST)

• A non-binding and consultative mechanism for the expedited and effective solution of operational problems encountered by ASEAN-based businesses on cross border issues related to the ASEAN agreements.

ASEAN Intellectual Property (IP) Portal

• This portal is expected to provide a consolidated platform to access IP information including databases on trademarks, geographical indications, and case laws.

ASEAN Coordinating Committee on Electronic Commerce (ACCEC)

• This committee was set up in acknowledgement of growing e-commerce in the region. The committee is charge of the ASEAN Work Programme on e-commerce.

ASEAN Roll-on Roll-off (RORO) and ASEAN Customs Transit System (ACTS)

• The ASEAN RORO sea linkage route between Davao (Philippines) and Bitung (Indonesia) is expected to enhance connectivity in the region.

• Similarly the ACTS (currently piloted in Malaysia, Singapore and Thailand), a computerised customs transit management system is another tool that is expected to enhance connectivity in the region.

Initiative for ASEAN Integration (IAI) Work Plan III in 2016

• Adopted in September 2016, this initiative provides special assistance to Cambodia, Lao PDR, Myanmar and Vietnam to advance regional integration in order to narrow the development gap within ASEAN.

12 PwC

Free Trade Agreements focus

on 5 July 2017. Topics discussed include tariffs, rules of origin, sanitary measures, services, movement of people, e-commerce, and investment. Both sides have stated an interest in increasing agricultural exports, boosting the trade of professional and mining-related services, and promoting bilateral trade and investment.

Free trade talks between India and Peru are also scheduled to begin in August 2017. Prior to negotiations, both countries have set up joint study groups and conducted feasibility studies which have been completed in October 2016. If successful, the FTA will likely result in reduced tariffs on both sides. India has strong industrial and IT sectors and high technological capabilities while Peru is rich in natural resources, providing possibilities for mutually beneficial partnerships between various sectors.

ASEAN – Hong Kong FTA on track for finalisation by November 2017

After three years of negotiations, FTA talks have now reached the final stages and Hong Kong is working intensively with ASEAN partners to finalise and sign the AHKFTA on the side lines of the 31st ASEAN Summit in November 2017. The FTA is expected to strengthen economic ties between ASEAN members and Hong Kong by facilitating trade in goods, services and investments. Key elements covered by the FTA includes the reduction and elimination of tariffs, liberalization of trade and services and intellectual property cooperation.

Australia and India to begin FTA negotiations with Peru

Australia and Peru have commenced with the first round of FTA negotiations

13Trade Intelligence Asia Pacific June / July 2017

Australia, Canada, New Zealand and Singapore admitted as associate members of the Pacific Alliance

The Pacific Alliance, which includes Chile, Colombia, Mexico and Peru, has admitted Australia, Canada, New Zealand, and Singapore as associate members. This is a step towards broadening the reach of its trade flows and investments into the Asia – Pacific region amidst protectionist measures by the US. Associate members are admitted to the Pacific Alliance for establishment of stronger relations with member countries.

The concept of an associate member is a new addition to the Pacific Alliance structure. The creation of ‘associate members’ was initiated at the Pacific Alliance Leaders Summit on 29-30 June 2017 in Santiago de Cali, Colombia and became one of the key points of the Cali Declaration. This development has marked a milestone of a more externally oriented strategic platform of the Pacific Alliance. Even though the Cali Declaration has not specifically elaborated on what it means to be an associate member, being an associate member is believed to open up the possibility of negotiating trade deals as well as deeper integration of services, resources, investments, and movement of people with the member countries – the strategic objectives of the Pacific Alliance.

There are currently 52 countries participating as Pacific Alliance observers, including - among others - China, India, Indonesia, Japan, Korea, and Thailand.

Negotiations for the Indonesia – Australia Comprehensive Economic Partnership (IACEPA) to be completed this year

Australia and Indonesia have reaffirmed commitment to complete the IA – CEPA by end 2017. Currently, both countries have held seven rounds

of negotiations on the IA – CEPA, which is based on the ASEAN – New Zealand FTA (AANZFTA) and will eliminate tariffs on 10,012 types of goods. In particular, Indonesia has agreed to lower tariffs on Australian sugar to 5% and to increase the maximum weight for imported Australian feeder cattle. Indonesia is also negotiating with Australia for the removal of tariffs on palm oil and paper products exported to Australia.

The IA – CEPA is expected to boost bilateral trade and investment cooperation between both countries. In 2015, bilateral trade recorded USD 11.2 billion. There have also been bilateral investments and cooperation between both nations in the agriculture, construction, infrastructure, finance, healthcare, food and transportation sectors. Third and fourth agreement under the China – Hong Kong CEPA signed

China and Hong Kong have signed two new agreements under the existing CEPA on 28 June 2017, namely the Investment Agreement and the Economic and Technical Cooperation (Ecotech) Agreement.

Under the Investment Agreement, businesses will be able to enjoy preferential investment access to both service and non-service sectors including assets investment, mining and manufacturing. Current provisions only extend this benefit to service sectors. This will, however, exclude 26 specific sectors including petroleum and natural gas. Measures for better investment protection, such as uniform procedures for approvable of investment applications and dispute settlement mechanisms, will also be established and implemented. The Ecotech Cooperation Agreement aims to create a closer economic and trade relations between Hong Kong and China in alignment with China’s belt and road initiative.

The Ecotech Agreement took immediate effect on 28 June 2017, while the

Investment Agreement will be officially implemented from 1 January 2018. With the signing of the two new agreements, both countries have signed, in total, ten supplementary agreements, six appendices and four agreements under the CEPA since it entered into force in 2003. The other two agreements are Agreement on Trade in Services (signed on 27 November 2015) and Agreement between the Mainland and Hong Kong on Achieving Basic Liberalisation of Trade in Services in Guangdong (signed on 18 December 2014). China and New Zealand resume talks for FTA upgrade

China and New Zealand have commenced FTA talks on 4 July 2017 for an upgrade of the existing agreement. The focus will be on reducing barriers to trade and to address any issues that have surfaced thus far. Both parties have stated that efforts will be made towards improving existing processes, such as to streamline processes and reduce red tape in China, and to modernize the FTA to reflect developments in regulations and trade policies since its entry into force in 2008. China has also agreed to facilitate investments and access to the China market, including to its service industries.

Both countries have spent two years exploring and agreeing on the scope of negotiations for upgrade of the FTA. Topics to be discussed include areas such as technical barriers to trade, digital trade and agricultural cooperation among others.

Japan and the EU on course to sign FTA after breakthrough in negotiations

After four years of negotiations, Japan and the EU have managed to resolve differences and reach a broad political agreement regarding the Japan – EU Economic Partnership Agreement (JEEPA). In particular, Japan has agreed to liberalize its highly protected

14 PwC

dairy sector, and reduce tariffs on sensitive European imports including chocolate, pasta, wine and cheese. Tariffs on wine will be scrapped immediately while duties on chocolates, pasta will be scraped within 10 years. Duties on cheese will be eliminated over 15 years. Europe has in turn agreed to lower tariffs on Japanese electronics, imported cars and products such as Japanese sake and green tea. Tariffs on electronics will be scrapped immediately while duties on cars will be phased out after 7 years.

Despite this, the signing and subsequent entry into force of the trade pact could require a much longer period of time as both countries seek to agree on a system to settle trade disputes, and obtain agreement from all EU member states. Both nations are aiming to reach a final agreement and enter the trade pact into force by early 2019.

Apart from eliminating 99 percent of tariffs between Japan and the EU, the finalized JEEPA will also expand the market for services and government procurement, and enhance regulatory cooperation.

US requests to renegotiate the US – Korea Free Trade Agreement (KORUS FTA)

The US has initiated a special joint committee meeting and is seeking to renegotiate the KORUS FTA with South Korea. US’ trade deficit with Korea has doubled from USD 13.2 billion to USD 27.6 billion, and exports have declined by 3% since the FTA took effect in 2012. The US administration has expressed concern over this widening trade imbalance and is looking to hold talks to review the KORUS and agree on more balanced terms and reduce barriers to trade. Re-negotiation of the FTA would also provide an opportunity to review implementation progress and resolve problems relating to market access in Korea for US exports.

As proposed during the Korea – US Summit in June, both countries have agreed to jointly investigate, analyse and evaluate the effects of the FTA and ascertain whether the trade deficit was caused solely by the FTA or other fundamental economic issues. The joint committee meeting will be held in August, where representatives from both sides will meet to discuss mutual interests and concerns. The US has

stated that Korea remains one of its key trading partners and the re-negotiation would help to strengthen ties and achieve more fair and balanced trade.

European Union (EU) resumes FTA talks with Malaysia

EU and Malaysia have committed to resume FTA negotiations within the year. Talks have commenced since 2010 but negotiations have been put on hold due to the exhaustion of negotiating options. Following internal assessments and consultations with various stakeholders on both ends, the EU has submitted a proposal at Brussels in July to re-launch formal negotiations and finalize the trade pact. Discussions are expected around reducing tariff and technical trade barriers relating to palm oil and palm product exports from Malaysia.

The EU is Malaysia’s third largest trading partner and bilateral trade is expected to increase further following the FTA. In 2017, trade with the EU recorded a trade surplus of MYR 10.6 billion, an increase of MYR 1.3 billion from the previous year.

15Trade Intelligence Asia Pacific June / July 2017

dairy farming, jewellery, energy, shipping, tourism, and health management sectors. Both governments are also working on reducing tariff and non-tariff barriers, preventing double taxation, and initiating dialogues to share experiences on issues such as disaster management and agricultural production.

However, before an FTA is signed, issues surrounding rules of origins, tariff and non-tariff barriers as well as labour laws will have to be ironed out. In particular, Bangladesh is to facilitate movement of people and seeking for reciprocal facilities for its citizens to work in Sri Lanka. Both countries have agreed to solve these issues in a mutually beneficial manner and aims to sign the bilateral FTA by end 2017.

The first meeting of the Eurasian Economic Union (EAEU) and Vietnam FTA joint committee

On 29 June 2017, seven months after the FTA entered into effect, the EAEU – Vietnam FTA joint committee held its first meeting in Moscow to review implementation of the trade pact, and its impact on bilateral trade. Since the inception of the FTA, trade volume between Vietnam and the Eurasian Customs Union has increased approximately 30%, with improved performance in the commodities sector and other sectors not targeted by the pact.

Both nations are also in discussions on how measures can be harmonized among member countries in areas such as animal – plant quarantine and certification of goods of origin in order for smooth coordination and implementation of the FTA. Assessment units will also be set up to advice the joint committee on issues with differing opinions, including safety standards for plants and animals, and health impacts of construction materials.

New Zealand pursues FTA with the Pacific Alliance, the US, and the UK

New Zealand has launched FTA talks with the pacific alliance countries, Chile, Colombia, Mexico and Peru. The FTA is expected to result in lower tariffs and improved market access for New Zealand’s beef and sheep produce, dairy, and service export sectors. The FTA will also help to diversify export options, encourage investment and goods and services trade, and encourage integration in other areas such as financial markets and free movement of people.

New Zealand has also expressed an intention for 90% of its exports to be covered by FTAs by 2030. As such, it has actively pursued trade talks with the United States (the US) and the United Kingdom (the UK). The UK has expressed commitment towards negotiating trade agreements with New Zealand and formal negotiations will be launched once Britain leaves the EU. The US has also indicated that it is open to FTAs and there are no major road blocks to a trade deal with New Zealand.

The 19th round of Regional Comprehensive Economic Partnership (RCEP) negotiations

In the 19th round of negotiations on 24 July 2017, representatives were aiming to reach a consensus and move towards finalization of the list of goods on which duties will be eliminated. Several member countries have requested India to eliminate duties on 90% of traded goods as part of the RCEP. India has also raised concerns over its widening trade deficit with China, and dumping of goods from China. Negotiations on trade in services have also been proceeding slowly, with many RCEP members hesitant towards liberalizing their service sector for India service exporters.

The five-day negotiations in Hyderabad also involved discussions between India and ASEAN relating to health, transport and communications in order to harness the potential within these sectors. India put forth proposals for establishing infrastructure such as high capacity fibre optic networks to enhance digital connectivity and build connectivity linkages both within India and with ASEAN member states. Both sides are also looking to cooperate in areas such as education, tourism, power, and urban infrastructure.

Several RCEP members, including China and Singapore, have expressed their intention to facilitate and expedite trade negotiations for finalization of the trade pact. The negotiators are reportedly aiming to conclude their negotiations either late in 2017 or within the first half of 2018. Prior experience of trade negotiations suggest that this timetable may very well slip.

Sri Lanka and Bangladesh enhanced economic cooperation

Sri Lanka and Bangladesh have signed 13 Memorandum of Understandings to enhance economic cooperation and investment promotion. Plans have been made towards setting up joint ventures between the private and public sectors, such as the apparel, pharmaceutical,

16 PwC

Country reports

Gary Dutton

+61 (7) 3257 8783 [email protected]

Australia Clarification on definition of “owner” for revenue recovery purposes The Department of Immigration and Border Protection (DIBP) has released a notice to provide general advice to industry and importers on the definition of “Owner” contained in the Customs Act 1901 (the Act). The notice addresses that in a contract of sale, the use of Incoterms® will usually set out the responsibilities of each party to the commercial transaction and usually identifies the person with the responsibility for paying the relevant duties, taxes and border charges. However, under the Act, the responsibility to comply in relation to the making of an import declaration and payment of duty, rests with the “Owner” as defined in section 4 of the Act. The section 4 definition includes most parties participating in an import or export supply chain.

In addition, the notice outlines the broad compliance approach for the purposes of duty demands and revenue recovery under section 165 of the Act. The broad definition of “Owner” allows DIBP to consider issuing a demand for unpaid duty on parties other than the importer nominated on the import declaration. These parties may differ depending on the nature and circumstances of how the goods were imported and the status of the goods.

Businesses should take note that this recent notice represents a change in practice by DIBP and demonstrates a clear intention to pursue outstanding or underpaid duties from multiple parties in a supply chain.

New benefits for Australian Trusted Traders (ATT)

The DIBP recently announced a significant new labour mobility benefit for accredited Trusted Traders. From 1 July 2017, the DIBP changed how businesses become an ‘Accredited Sponsor’ for 457 visas and the assessment criteria of new sponsorship applications. These changes are designed to ensure that a larger number of lower risk sponsors have access to accreditation. Under the changes, accredited ATTs have priority allocation and streamlined processing arrangements under one of the new distinct accreditation characteristic categories. This will enhance the ability of ATT-participating businesses to bring skilled labour and experienced personnel into Australia. In addition, the Minister for the DIBP recently announced that Australia has entered into several new Mutual Recognition Arrangements (MRAs), specifically with the Canadian Border Services Agency, the Customs and Excise Department of Hong Kong, and Korean Customs Service. These developments will assist Australian exporters participating in the ATT by providing recognition of their “trusted” status in Canada, Hong Kong, and Korea.

17Trade Intelligence Asia Pacific June / July 2017

Export reporting obligations

The DIBP recently released a notice to improve awareness with regards to export reporting obligations. It is the responsibility of exporters and their agents to understand their obligations and to ensure that exported goods are reported correctly. The DIBP has noted that offences related to export reporting may undermine its ability to perform its designated role in preventing the exportation of illicit goods and the application of government policy. The notice sets out information related to the following issues:• Reporting Exports;• Accurate Export Data;• Australian Harmonized Export Commodity Classification;• Export Permits;• Prescribed Warehouse Goods;• Permission to Move, Alter or Interfere with Export Goods; and• Confirming Exporters.More information can be found at the following link: http://www.border.gov.au/Customsnotices/Documents/dibp-notice-2017-17.pdf

Guidance on refund provisions under Australia’s FTAs The DIBP released Notice No. 2017/13 outlining considerations relating to the assessment of refund applications under Australia’s various Free Trade Agreements (FTAs). The notice provides guidance on the refund circumstances for Australia’s FTAs with Chile, China, Japan, Korea, Malaysia, Singapore, Thailand and the US.

Specific circumstances of refund and the period of refund application can be accessed here: https://www.border.gov.au/Customsnotices/Documents/dibp-notice-2017-13.pdf

Commonwealth penalty unit value increases from A$180 to A$210

On 1 July 2017, the value of a Commonwealth penalty unit increased from A$180 to A$210. Consequently, the maximum financial penalties for committing various Commonwealth offences also rose from this date. The new penalty unit value will only apply to offences that are committed on or after 1 July 2017. This increase in the value of the penalty unit ensures that financial penalties remain an effective punishment and deterrent. To ensure the real value of the penalty unit is maintained, the penalty unit will then be automatically increased according to inflation every three years, beginning from 1 July 2020.

The increase in penalties rates raise the base penalty for non-compliance to A$9,450 per instance of non-compliance.

18 PwC

Implementation of nationwide customs clearance integration

Effective from 1 July 2017, China Customs implemented its Risk Management Centre and Duty Collection and Supervision Centre nationwide. The intention is to centralize and unify important customs services, such as risk prevention and control, and duty collection. This replaces the former regional document verification centres and departments. Self-declarations, tax payments, self-disclosure, and centralized duty collections are all part of this effort.

Susan Ju

+86 (10) 6533 3319 [email protected]

China

Derek Lee

+86 (21) 2323 7733 [email protected]

Frank Wu

+86 (21) 2323 3864 [email protected]

Introduction of China-New Zealand MRA

Effective from 1 July 2017, the “Mutual Recognition Arrangement (MRA) of PRC Customs Enterprises Credit Management and Secure Exports Scheme between General Administration Customs of PRC and New Zealand Customs” has been implemented. Under this MRA, China and New Zealand Customs would provide the following customs clearance facilitation to Authorized Economic Operator (AEO) enterprises, i.e. Advanced Certified Enterprises of China Customs and members of the “Secure Exports Scheme” of New Zealand Customs.

• Reduction in document verification rates;• Priority on customs inspection;• Appointed customs officer to facilitate customs clearance; and• Fast clearance when trade suspension is recovered.

China Customs is looking to actively facilitate the AEO mutual reorganization cooperation with important trade partners, countries under FTA, and “one belt, one road’ countries.

19Trade Intelligence Asia Pacific June / July 2017

After self-declaration, the Risk Management Centre will conduct a risk assessment of entry. The Duty Collection and Supervision Centre will be responsible for tax-related risk verification. This includes verifying and processing tax related declaration elements such as classification, valuation and country of origin as follows:

Duty Collection and Supervision Centre

Commodities Chapters in Tariff Book

Shanghai Mechanical and electronic category

84-87, 89-92

Guangzhou Chemical category 25-29, 31-40, 68-83

Beijing/Tianjin Agriculture and forestry, textile industry, food, drugs, light industry, aircraft industry and others

1-24, 30, 41-67, 88, 93-97

With this, businesses can choose to declare their imports to any customs office nationwide. It helps to ensure the consistency of implementation of regulations. Meanwhile, the emphasis on “release first, duty collection afterwards” is expected to reduce clearance formalities and improve customs clearance efficiency. From a business point of view, this helps decrease the cost of clearance.

Businesses should actively adapt to the new regime, learn the customs regulations related to the two new centres and build appropriate working relationships with Customs.

A simple overview of the customs clearance regime is as illustrated as follows:

20 PwC

Hong Kong

Import and Export (Strategic Commodities) Regulations (Amendment of Schedule 1) Order 2017 takes effect

Further to our last Trade Intelligence Asia Pacific issue regarding the announcement of Import and Export (Strategic Commodities) Regulations (Amendment of Schedule 1) Order 2017 (“the Order”), the TID recently issued Strategic Trade Control Circular No. 9/2017 to inform the public that the Order came into operation on 3 July 2017.

For further details of the Order, please refer to our last update or visit the link below for the legal texts of the Order: http://www.gld.gov.hk/egazette/pdf/20172112/es22017211242.pdf

Making requests for developing CEPA Rules of Origin

As of today, there are 1,891 Mainland 2017 Tariff Codes covered under CEPA for claiming preferential treatment. For goods that have no CEPA Rules of Origin (ROOs), Hong Kong manufacturers may request for developing CEPA ROOs for such goods at the Trade and Industry Department of Hong Kong (TID).

The TID will conduct CEPA ROO consultations with the Mainland twice a year in respect of such goods. Applications received from Hong Kong manufacturers on or before 31 July 2017 will be included in the second round of consultations in 2017; whereas applications received after 31 July 2017 will be included in the next phase of consultations in 2018.

Derek Lee

+86 (21) 2323 7733 [email protected]

21Trade Intelligence Asia Pacific June / July 2017

Report on anticipated activities involving Scheduled Chemicals

Strategic Trade Controls Circular No.10/2017 was issued on 3 July 2017. It invites operators that expect to be engaged in specified activities involving Scheduled Chemicals controlled by the Chemical Weapons (Convention) Ordinance (“the Ordinance”) in 2018, to report details of their anticipated activities to the TID.

The purpose of the Ordinance is to enable the Chemical Weapons Convention (“the Convention”), an international treaty that aims to prohibit the development, production, acquisition, stockpiling, retention, transfer and use of chemical weapons, to be fully implemented in Hong Kong.In accordance with the Ordinance, the following permit and reporting requirements should be met:

• Operators are required to obtain permits from the TID if they are engaged in specified activities involving Scheduled Chemicals in quantities over the respective thresholds.

• Permit holders are also required under the Ordinance to lodge annual reports with the TID on their anticipated activities involving Scheduled Chemicals for the coming calendar year before the end of the current year, and their past activities during the previous year at the beginning of the current year.

The TID will send the circular to individual operators who may, according to their knowledge, be engaged in specified activities involving Schedules Chemicals.

Operators who receive the circular from TID must complete and return the reply slip latest by 17 July 2017 to indicate whether or not their facilities would be engaged in any specified activities involving Scheduled Chemicals in 2018.

If so, they must complete the designated report forms on anticipated activities and return them to the TID by 24 July 2017.

Operators who do not receive the circular by mail from TID but believe that their facilities may be engaged in specified activities involving Scheduled Chemicals in 2018 are also encouraged to provide details of the activities by completing and returning the reply slip to TID.

For full details of the circular, refer to the following link:http://www.stc.tid.gov.hk/english/circular_pub/2017_stc10.html

22 PwC

Implementation of GST regime from 1 July 2017

With effect from 1 July 2017, India has moved from a myriad of domestic taxes to a single Goods and Services Tax (GST) regime. Various amendments have also been made to the customs law to align with the new regime.

The key changes pertaining to import, export and foreign trade policy are summarized below:

Customs – Import

• Under the GST Regime, basic Customs Duty (BCD) and other customs duties such as Anti-dumping duty (ADD) and Safeguard duty (SD) will continue to be levied on import of goods.

• Countervailing Duty (CVD) and Special Additional duty (SAD) applicable under the earlier regime are replaced with Integrated Goods and Service Tax (IGST) and GST Compensation Cess, with a few exceptions. Examples of such exceptions include specified petroleum products or alcohol for human consumption etc., where CVD and SAD will continue to apply.

• GST compensation cess is applicable only to specific products such as aerated waters, tobacco products, cars etc. These rates are mostly ad valorem. However some goods may also be subject to specific rates or mixed rates (e.g. ad valorem rates + specific rates).

• While BCD, ADD and SD continue to be a cost on import, IGST will be available as input tax credit to the importer subject to certain conditions.

• An illustrative list of taxes applicable on import and method of computation of such taxes is summarized in the below table:

Current regime New GST regime

Purchase price Purchase price

BCD (Purchase price*%) BCD (Purchase price*%)

CVD [(Purchase price+BCD)*%] Customs Cess (BCD)*%

Customs Cess [(BCD+CVD)*%] IGST [(Purchase price +BCD)*%]

SAD [(Purchase price +BCD+CVD+Cess)*%]

• Various exemptions and procedures under the customs law have been updated to align with GST rates with effect from 1 July 2017. Aligned procedures include amendments to the format of bill of entry, which requires mandatory inclusion of the GSTIN (GST registration number).

• There is no change in the operations of the Special Valuation Branch (which is applicable for valuation in case of import of goods from related parties) on introduction of GST.

• Previously, service tax was leviable on import of services in India. Under the new GST regime, import of services is liable for IGST, which will be available as input tax credit subject to certain conditions.

India

Nitin Vijaivergia

+91 (0) 982 023 [email protected]

23Trade Intelligence Asia Pacific June / July 2017

Customs - Export

• Export of goods and services will be treated as zero-rated supplies (i.e. no GST on output). Although GST is still liable on import, input tax credit is refundable on account of exports under the following options:

- Supply without payment of GST and refund of unutilized input tax credit; - Supply with payment of GST and refund of GST so paid.

• Although exports are zero-rated under GST, GST would have to be discharged along with interest if:

- Goods are not exported within 3 months of date of export invoice; - Foreign remittance is not received within 1 year of date of service invoice.

• Key changes in the export procedures under GST law: - Requirement of bond/letter of undertaking is extended to service exporters; - All exports of goods can be done under self-sealing procedures (without supervision by tax authorities as per the old regime). This is subject to an initial one-time verification of premises by authorities; - Intimation is required to be filed with customs authorities at the time of each export consignment; - No requirement of furnishing bond and bank guarantee for exports if specified criteria are met with respect to foreign currency realization during the previous year.

• No amendments have been made to the drawback provisions under the Customs law in the GST regime. Hence, the drawback scheme will still provide an option of claiming drawback under either an All Industry Rate or Brand Rate.

Foreign Trade Policy (FTP)

• Under the earlier regime, benefits under FTP were available for nearly all import taxes including CVD, SAD etc. However, under the new GST regime, FTP benefits are proposed to be restricted to BCD and other customs duties only. A detailed notification in this regard is expected soon. There are no benefits on GST paid on imports, including the exemptions applicable under Advance Authorisation scheme and Export Promotion of Capital Goods Scheme.

• The scrips under export incentive schemes can be utilised only for payment of customs duties such as BCD at the time of import. They cannot be utilized for payment of IGST or for payment of GST on domestic procurements.

• The Import Export Code (IEC) will be replaced with a PAN number (issued under income tax) to keep the identity of an entity uniform across the ministries/ departments. However, application for IEC will continue.

Export Oriented Units (EOU)

• Under the pre-GST regime, all taxes (BCD, CVD and SAD) were exempt for procurements by EOUs. This exemption is now available only with respect to BCD and not IGST. The input tax credit of IGST paid on imports can be utilized for payment of GST on the goods cleared from the EOU. Refund of unutilized credit can also be claimed when exports are made from such EOU. In case of clearances of goods from EOU to domestic units within India, benefit of BCD taken earlier will be required to be reversed.

Special Economic Zone (SEZ)

• Under the pre-GST regime, procurements by SEZ units were exempt from customs and indirect taxes subject to certain procedures and conditions. This will continue to be applied under the new regime and all supplies to SEZ units will be considered as zero-rated (i.e. at par with exports).

24 PwC

Project Imports

• Under the GST regime, classification for the purpose of IGST levy is simplified. All imports under the Project Imports scheme will be classified under heading 9801 and duty will be levied @ 18%. There is no requirement for classification of individual goods, unlike under the pre-GST regime.

PwC Comments

With such a monumental change in the indirect tax regime, it is important for businesses to undertake an analysis to ensure compliance. Businesses may consider undertaking the following measures to align with the new GST regime:

• Conduct a review of existing cross border transactions and examine the impact of the change in tax structure in relation to specific transactions such as high seas sales, inbound and outbound transactions with Free Trade Warehousing Zone/ Special Economic Zone and Bonded warehouse, or imports under various FTP schemes;

• Amend existing standard operating procedures to align with regulatory amendments; • Conduct training and awareness programs for logistics and customs teams; • Re-evaluate benefits under FTP and explore changes in existing business model;• Adapt to changes in import and export documentation, and other new requirements

under the Customs and GST laws.

25Trade Intelligence Asia Pacific June / July 2017

Improvements to Intellectual Property Rights protection

On 2 June 2017, the Indonesian government enacted Regulation No. 20 of 2017 on Control of Import and Export of Goods Constituting or Deriving from Intellectual Property Rights (IPR) Infringement. This can be seen as a step forward as it is the first regulation to govern a Customs IPR border protection system, both on export and import. The types of IPR covered under this regulation are, but not limited to: trademark, copyright, patents, industrial design, integrated circuits design, plant variety, and geographical indications.

Indonesian legal entities who own or hold a trademark or copyright may (it is not mandatory) file a written application to Customs along with proof of trademark or copyright ownership, information on authenticity, data on characteristics or specification, and a statement from the owner of the trademark or copyright, to have their IPR protected goods recorded with Customs.

Any imported or exported goods that are allegedly derived from trademark or copyright infringement can be restrained by Customs provided that the trademark or copyright of the restrained goods has been recorded at Customs. Customs restraint is the administrative action of postponing the clearance and loading or unloading of the imported or exported goods until all customs requirements and formalities are fulfilled.

Customs is also authorised to suspend the clearance of IPR infringing goods from a customs area. However, the provision does not apply to personal effects of passengers, carrier crew, or border crossers, or postal items and consignments which are carried for personal – not commercial – purposes. Further regulations are expected with respect to these matters.

The suspension provision is also not applicable to transhipment. In this instance, Customs will send a notification to the customs authority in the next destination country to advise them that certain goods allegedly constitute or derive from IPR infringement.

The regulation took effect from 2 August 2017.

Indonesia

Enna Budiman

+62 (21) 5289 0734 [email protected]

New task force to focus on high-risk importers

On 12 July 2017, the MOF together with the Indonesian National Police (POLRI), the Corruption Eradication Commission (KPK), the Attorney General of Indonesia, the Indonesian National Air Force (TNI), and the Indonesian Financial Transaction Reports and Analysis Center (PPATK) set up a task force to crack down on illegal imports and clean up business practices.

The Ministry of Finance has indicated that around 1,500 importers are currently classified as high-risk importers, and among those, 679 did not have a Taxpayer Identification Number (NPWP). These high-risk importers are also reported to engage in corruption and bribery practices. Products affected are predominantly textiles, electronics, and alcoholic beverages.

The task force will focus on import activities at the major ports of Belawan, Tanjung Priok, Tanjung Emas, Tanjung Perak, and Cikarang, as well as ports in the east coast of Sumatra. For now, the Directorate General of Customs and Excise (“DGCE”) will conduct operational tactical activities through internal performance monitoring, and cooperate with law enforcement officers and ministries/agencies. In the future, the DGCE is looking to build a customer service compliance system. Together, it is hoped that the efforts will successfully tackle illegal and unfair trading, and also protect state and taxation revenues.

26 PwC

Countries graduating from the Generalized System of Preferences

Japan Customs has announced that Antigua and Barbuda, and the Republic of Seychelles are expected to graduate from the Generalized System of Preferences (GSP) from April 1, 2018.

The GSP is a system designed to promote economic growth in developing nations, and provides preferential duty-free treatment on certain products to designated beneficiary countries and territories, including the Least-Developed Beneficiary Developing Countries (LDBDCs). To ensure the GSP benefits only LDBDCs, Japan has implemented a system where certain countries that have achieved economic development equivalent to that of a developed country will be considered to have “graduated”. These countries will no longer be eligible for preferential duty-free treatment under the GSP and will instead be subject to the Most-Favoured Nation (MFN) duty rate.

Under current criteria, a country/territory will be excluded from the list of beneficiaries of Japan’s GSP scheme if it has been classified as a “high income country” for three consecutive years according to the income classification in the “World Bank Statistics”. Least developed countries (LDCs) are not subject to the system of “graduation”. Should the country or territory subsequently not qualify as a “high income country” for three consecutive years, a request can be filed to be designated as a beneficiary again under the GSP Scheme.

With effect from 1 April 2019, the government will also implement new criteria for the “entire graduation” of countries from the GSP. Compared to current practice, where countries have to be classified as a “high income country”, a country/territory is now expected to “graduate” if it has, for three consecutive years, been:

• Classified as an “upper-middle income economy” in the “World Bank Statistics”; and

• Has an annual export value of more than 1% of the global annual export value.

Countries that have satisfied the above two conditions for one year will be deemed to have “partially graduated”. The new criteria on partial graduation will be implemented a year earlier, with effect from 1 April 2018.

Refer to the following link for more details on the review of the system of ‘graduation” under the GSP Scheme: http://www.customs.go.jp/english/gsp/index.htm

Japan

Howard Osawa

+81 (0) 3 5251 [email protected]

27Trade Intelligence Asia Pacific June / July 2017

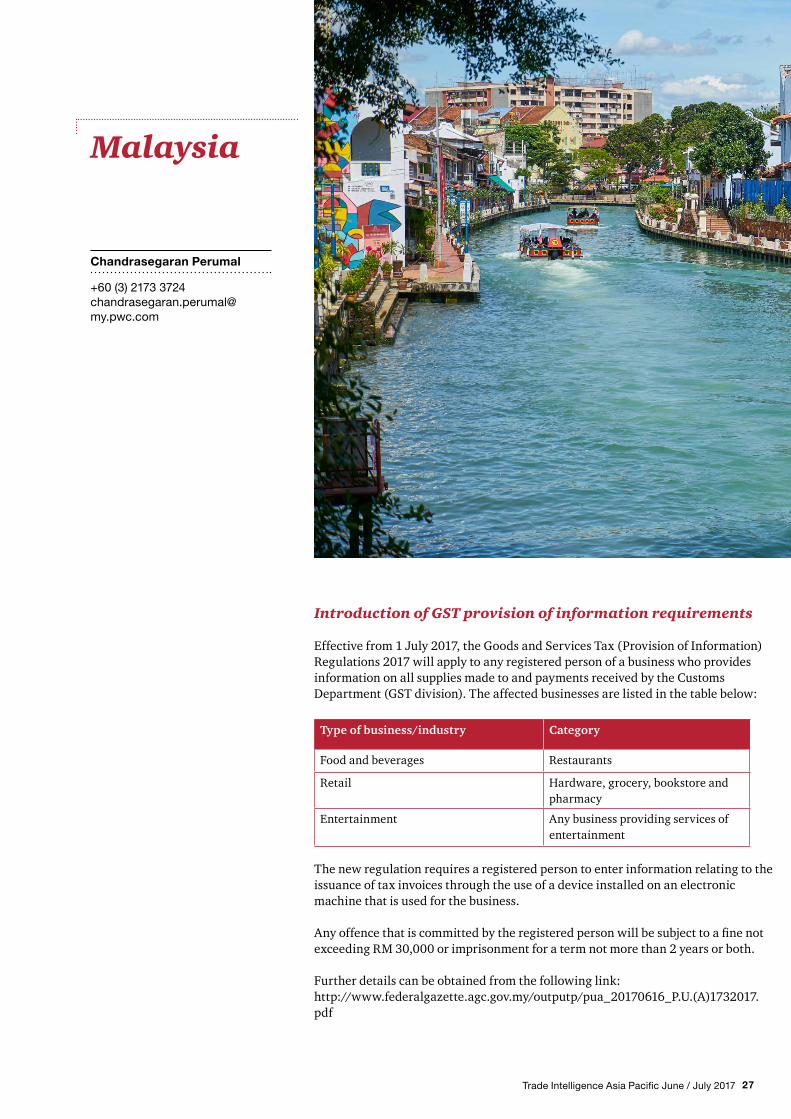

Introduction of GST provision of information requirements

Effective from 1 July 2017, the Goods and Services Tax (Provision of Information) Regulations 2017 will apply to any registered person of a business who provides information on all supplies made to and payments received by the Customs Department (GST division). The affected businesses are listed in the table below:

Type of business/industry Category

Food and beverages Restaurants

Retail Hardware, grocery, bookstore and pharmacy

Entertainment Any business providing services of entertainment

The new regulation requires a registered person to enter information relating to the issuance of tax invoices through the use of a device installed on an electronic machine that is used for the business.

Any offence that is committed by the registered person will be subject to a fine not exceeding RM 30,000 or imprisonment for a term not more than 2 years or both.

Further details can be obtained from the following link:http://www.federalgazette.agc.gov.my/outputp/pua_20170616_P.U.(A)1732017.pdf

Malaysia

Chandrasegaran Perumal

+60 (3) 2173 [email protected]

28 PwC

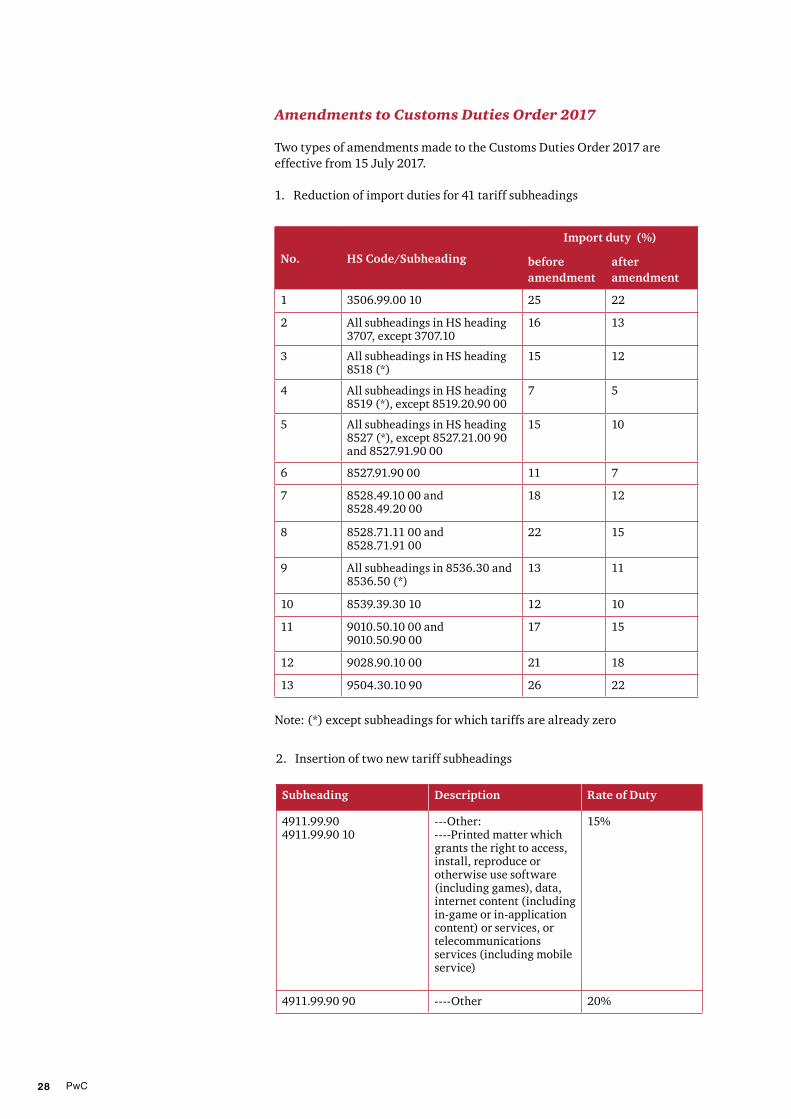

No. HS Code/Subheading

Import duty (%)

before amendment

after amendment

1 3506.99.00 10 25 22

2 All subheadings in HS heading 3707, except 3707.10

16 13

3 All subheadings in HS heading 8518 (*)

15 12

4 All subheadings in HS heading 8519 (*), except 8519.20.90 00

7 5

5 All subheadings in HS heading 8527 (*), except 8527.21.00 90 and 8527.91.90 00

15 10

6 8527.91.90 00 11 7

7 8528.49.10 00 and8528.49.20 00

18 12

8 8528.71.11 00 and 8528.71.91 00

22 15

9 All subheadings in 8536.30 and 8536.50 (*)

13 11

10 8539.39.30 10 12 10

11 9010.50.10 00 and 9010.50.90 00

17 15

12 9028.90.10 00 21 18

13 9504.30.10 90 26 22

Note: (*) except subheadings for which tariffs are already zero

2. Insertion of two new tariff subheadings

Subheading Description Rate of Duty

4911.99.90 4911.99.90 10

---Other:----Printed matter which grants the right to access, install, reproduce or otherwise use software (including games), data, internet content (including in-game or in-application content) or services, or telecommunications services (including mobile service)

15%

4911.99.90 90 ----Other 20%

Amendments to Customs Duties Order 2017

Two types of amendments made to the Customs Duties Order 2017 are effective from 15 July 2017.

1. Reduction of import duties for 41 tariff subheadings

29Trade Intelligence Asia Pacific June / July 2017

Customs urged to tighten its internal SOP on export control

On 3 July 2017, The Ministry of International Trade and Industry (“MITI”)’s Deputy Minister urged Customs to tighten its standard operating procedures (SOP). This is following investigations into the controversy involving the shipment of high-tech radar equipment via Port of Tanjung Pelepas (PTP) in Gelang Patah, Johor.

MITI stressed the importance of Customs ensuring that all cargo shipped by a company is in compliance with export control procedures. According to the Strategic Trade Act 2010, the import and export of military and sensitive equipment requires approval from MITI.

Ban on export of rubberwood

Effective 1 July 2017, the export of local rubberwood has been banned to address the shortage of the native raw material faced by the local furniture industry. The decision to ban the export of rubberwood was made after considering complaints made by the industry and exporters.

According to the government, rubberwood is the main raw material used in furniture making. By implementing a ban on the export of rubberwood, the government hopes to help the country retain the raw material, produce more furniture and create more business opportunities. It is hoped that the ban will boost Malaysia’s furniture export business in the next few years, with the target being RM12 billion by 2020. Last year, the figure was at RM9.53 billion.

30 PwC

New ZealandUpdate on new Customs and Excise Bill

The new Customs and Excise Bill is currently awaiting its Second Reading in Parliament. The Bill is expected to be passed with receipt of Royal Assent by end 2017. Most key provisions under the new bill will enter into effect on 1 April 2018, or six months after the date of royal assent.

New Zealand – China Mutual Recognition Agreement

The Mutual Recognition Agreement (MRA) between New Zealand Customs Service (NZCS) and the General Administration of China Customs (GACC) has officially entered into effect on 1 July 2017.

Under the MRA, NZCS and the GACC will mutually recognise each country’s equivalent of the Authorised Economic Operator (AEO) exporter program, also known as the Secure Exports Scheme in New Zealand, which will allow accredited exporters to receive special treatment at both borders.

Accredited exporters can expect:

• Expedited clearance with reduced frequency of inspections and document checks.

• Shipment inspection prioritisation, where shipments requiring inspection will be prioritised

• A designated contact at each of the Customs agencies.

• Expedited recoveries –AEO exporters will receive prioritised clearance should a trade disruption occur.

Eugen Trombitas

+64 (9) 355 8686 [email protected]

31Trade Intelligence Asia Pacific June / July 2017

New duty rates and levies on alcohol and fuel products

As of 1 July 2017, new excise duty rates and levy rates have entered into effect. These levies specifically include the following:

1) Health Promotion Agency (HPA) levy rates for alcohol

The reduced HPA rates below are applied to alcoholic beverages removed from a licensed manufacturing area or imported after midnight on 30 June 2017.

Class Current HPA rates to 30 June 2017

New HPA rates from 1 July 2017

(A) 1.15–2.5 % alcohol 0.5707 cents per litre 0.5409 cents per litre

(B) 2.5–6 % alcohol 1.6945 cents per litre 1.6152 cents per litre

(C) 6–9% alcohol 3.0435 cents per litre 2.8847 cents per litre

(D) 9–14% alcohol 3.8043 cents per litre 3.6059 cents per litre

(E) 13-23% alcohol 6.8014 cents per litre 6.4281 cents per litre

(F) more than 23% alcohol 14.5799 cents per litre 12.4064 cents per litre

2) Excise duty rates for alcohol

Excise duty rates for alcohol are adjusted annually based on movements in the consumer price index. The new increased rates will be applied to alcohol products removed from a licensed manufacturing area or imported after midnight on 30 June 2017.

Specific duty rates are detailed in the Excise and Excise equivalent Duties Table Amendment Order: http://www.customs.govt.nz/news/resources/legal/Documents/Excise-and-Excise-equivalent-Duties-Table-Alcoholic-Beverages-Indexation-Amendment-Order-2017.pdf

3) ACC motor spirits levy

The ACC motor spirits levy was decreased from 6.9 cents per litre to 6 cents per litre with effect from 1 July 2017.

4) Petroleum or Engine Fuel Monitoring Levy (PEFML)

The PEFML levy was increased from 0.2 cents per litre to 0.3 cents per litre with effect from 1 July 2017. This levy applies to petroleum or engine fuel that is specified as a type of motor spirit, diesel, biodiesel and ethyl alcohol.

32 PwC

Philippines

Alex Saborio

+65 6236 4192 [email protected]

The implementation of AHTN 2017

On 27 June 2017, The Philippines National Economic and Development Authority (NEDA) Board approved the adoption of the ASEAN Harmonized Tariff Nomenclature 2017 (AHTN 2017), effective from 28 July 2017. Consequently, all tariff commodity classification rulings issued under Section 1313-a of the Tariff and Customs Code of the Philippines (TCCP) and Advance Rulings issued under Section 1100 of the Customs Modernization and Tariff Act (CMTA) that are based on AHTN 2012 are no longer considered valid starting 28 July 2017.

Modification of the Philippine tariff schedule

The tariff schedule is regularly updated to keep Philippine industries internationally competitive and to comply with international agreements entered into by the country. In line with this, the following Executive Orders were signed to modify the Most Favoured Nation (MFN) tariff schedule of the Philippines:

Executive Order No. 20 (s. 2017)This was signed to amend the schedule set out by Executive Order No. 61 (s. 2011) which was applied from 2011 to 2016. It provides the MFN rates for 2017 to 2020, effective on 17 July 2017.

Executive Order No. 21 (s. 2017)The WTO’s Information Technology Agreement (ITA) was signed in 1996 to eliminate or bind tariffs on certain IT products by year 2000, or by year 2005 for developing countries. In 2015, the Agreement was expanded to cover another 201 products. In line with this, the President signed an Executive Order to implement the Philippine ITA Expansion Schedule, eliminating the tariff rates of identified IT products by 1 July 2017, with flexibility on some products until 1 July 2023.

Executive Order No. 22 (s. 2017)Companies registered with the Board of Investments (BOI) were entitled to import capital equipment, spare parts and accessories at zero percent duty until 9 May 2017 to promote investments. With the same purpose, the President extended this privilege for products classified under Chapters 40, 59, 68, 69, 70, 73, 76, 82, 83, 84, 85, 86, 87, 88, 89, 90, 91, and 96. This took effect on 18 May 2017 and is valid for one year or until the Omnibus Investments Code is amended, whichever comes earlier.

33Trade Intelligence Asia Pacific June / July 2017

Executive Order No. 23 (s. 2017)The World Trade Organization temporarily allowed the Philippines to impose quantitative restrictions on rice, on the condition that the MFN rates on certain agricultural products will be reduced until the expiration of the special treatment on 30 June 2017. This Executive Order was signed to extend the reduced MFN rates until 30 June 2020 or until the Agricultural Tariffication Act is amended, whichever comes earlier.

Clearance procedure of postal items

Customs recently released the rules and regulations on the clearance procedure of postal items to implement the related provisions of the new Philippines Customs and Tariff Law. It prescribed the filing of a Postal Customs Declaration and a non-intrusive inspection for all postal items, whether subject to import charges or not. Items with Free Carrier (FCA) or Free on Board (FOB) value of up to approximately USD 1,000 will be cleared through an informal entry process, while those over approximately USD 1,000 will be cleared through a formal entry process requiring the lodgment of goods declaration. Postal items refer to anything dispatched under postal services including mail-letter post, parcel post, money orders, etc.

Creation of a Customs Special Inspection Team on valuation

The Bureau of Customs created a “Special Inspection Team”, dedicated to examine shipments issued with alert orders due to valuation concerns. It fast-tracks customs valuation inquiries, as the team must finish the examination and submission of reports within 24 hours for perishable goods and 48 hours for non-perishable goods, from the issuance of the alert order.

Importation of petroleum products by registered free zone enterprises

One of the incentives for registered free zone enterprises is the exemption from payment of import taxes, on the condition that the goods imported do not enter the customs territory of the Philippines.

Despite this, the Bureau of Internal Revenue (BIR) issued a regulation in 2012 imposing VAT and excise tax on all importations of petroleum and petroleum-based products, requiring an Authority to Release Imported Goods (ATRIG) from the BIR for customs clearance, including those of free zone enterprises. The regulation provided that since free zone enterprises are entitled to tax exemption, they may later apply for refund upon proof that the products did not enter the Philippines customs territory.