2017 Journal of Innovative Research in Business & Economics - ISSN - 2456-7868 JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April http://sijitcs.com ISSN - 2456-7868 ISSN - 2456-7868 ISSN - 2456-7868 http://sijitcs.com Assessment of Professional Ethics’ Practice among Professional Accountants in the Nigerian Public Sector Mubaraq Sanni Department of Accounting and Finance Kwara State University, Malete, Nigeria ABSTRACT: High profile corruption and fraud in public sector with which accountants have been asso- ciated as auditors, executives and directors have prompted searching questions to be asked as to the integ- rity of the professional accountants engaged particularly in public services. Consequently, the study aim to assess the practice of professional ethics among professional Accountants in Nigerian public service. The study use purposively sampling techniques to select chartered Accountant of Institute of Chartered Ac- countants (ICAN) and Association Of National Accountant of Nigeria (ANAN) in the ministry of Finance, particularly the office of the Accountant General and auditor General of the Federation. The Kolmogorov- Smirnov and the Shapiro-Wilk tests were used to determine the normality of the data. One sample t test was employed to assess the application of professional ethics among professional Accountants, while Mann- Whitney U test was employed in testing whether significant difference exists between the perception of ICAN and ANAN member as well as between professional Accountants and Auditors. The results of statis- tical tests show that there is no significant difference in the application of professional ethics among the professionals implying that professional Accountants in the public sector comply with the professional ethics of the professional bodies in their official dealing and that cadre of the professionals does not influ- ence the application of professional ethics. Therefore, the study recommends that the government should provide financial support to an ordinarily Accountant to become member of a reputable professional bodies and to encourage the professional to further intensify efforts on high level compliance with professionals ethics. KEY WORDS: Ethics, Accountants, Auditors, Public Sector, Nigeria 1.0 INTRODUCTION Scandals involving public officials have captured world attention and the public are debating on the accelerating level of corruption and unprofessional behaviour in government (Tivelli & Masini, 2007). The root cause was the gradual but ultimately complete collapse of ethical behavior across the sectors of the econaomy. Once a sector of the economy became unmoored from its ethical base, the sectors were free to behave in ways detriments to the achievement of set objectives. For instance, what happened to Enron Company and their auditors, Arthur Anderson, was not due to the default of the international accounting criteria or auditing criteria, but the problem falls in the ethics of the profession itself (Al-Qashi, 2005). Unethical practices kill and neutralize organizational values and consequently relegate the organizational objectives to the background. Every citizen suffers from it including those living outside the country (Dukor, 2015). Davis (2009) observed that increasingly governments all over the world are recognizing that ethics is not just an issue for others but necessary tool for them to clean up their own doorstep, often in the aftermath of revelations about the alleged unethical behavior of both civil servants and politicians in order to ensure fair and honest behavior of individuals and organizations acting in the public domain. This has influence International organizations such as the World Bank to take a strong interest in ethics and have become a key concern to the European Union because the result of distrust by citizens on the public sector was apathy to democratic activity. This has impacted negatively upon the economic performance of many Organisations for Economic Co-operation and Development (OECD) countries (Davis, 2009). In Nigeria, many institutions has been established to enforce the ethical codes such as codes of conduct bureau, courts, EFCC, ICPC, ICAN, ANAN etc but the more the institutions, the more the growth of 29

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll Aprilhttp

://sijitcs.comIS

SN

- 2

456-

7868

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

Assessment of Professional Ethics’ Practice among Professional Accountants inthe Nigerian Public Sector

Mubaraq Sanni

Department of Accounting and Finance

Kwara State University, Malete, Nigeria

ABSTRACT: High profile corruption and fraud in public sector with which accountants have been asso-ciated as auditors, executives and directors have prompted searching questions to be asked as to the integ-rity of the professional accountants engaged particularly in public services. Consequently, the study aim toassess the practice of professional ethics among professional Accountants in Nigerian public service. Thestudy use purposively sampling techniques to select chartered Accountant of Institute of Chartered Ac-countants (ICAN) and Association Of National Accountant of Nigeria (ANAN) in the ministry of Finance,particularly the office of the Accountant General and auditor General of the Federation. The Kolmogorov-Smirnov and the Shapiro-Wilk tests were used to determine the normality of the data. One sample t test wasemployed to assess the application of professional ethics among professional Accountants, while Mann-Whitney U test was employed in testing whether significant difference exists between the perception ofICAN and ANAN member as well as between professional Accountants and Auditors. The results of statis-tical tests show that there is no significant difference in the application of professional ethics among theprofessionals implying that professional Accountants in the public sector comply with the professionalethics of the professional bodies in their official dealing and that cadre of the professionals does not influ-ence the application of professional ethics. Therefore, the study recommends that the government shouldprovide financial support to an ordinarily Accountant to become member of a reputable professional bodiesand to encourage the professional to further intensify efforts on high level compliance with professionalsethics.KEY WORDS: Ethics, Accountants, Auditors, Public Sector, Nigeria

1.0 INTRODUCTION

Scandals involving public officials have capturedworld attention and the public are debating on theaccelerating level of corruption and unprofessionalbehaviour in government (Tivelli & Masini, 2007).The root cause was the gradual but ultimatelycomplete collapse of ethical behavior across thesectors of the econaomy. Once a sector of theeconomy became unmoored from its ethical base,the sectors were free to behave in ways detrimentsto the achievement of set objectives. For instance,what happened to Enron Company and their auditors,Arthur Anderson, was not due to the default of theinternational accounting criteria or auditing criteria,but the problem falls in the ethics of the professionitself (Al-Qashi, 2005). Unethical practices kill andneutralize organizational values and consequentlyrelegate the organizational objectives to thebackground. Every citizen suffers from it includingthose living outside the country (Dukor, 2015). Davis

(2009) observed that increasingly governments allover the world are recognizing that ethics is not justan issue for others but necessary tool for them toclean up their own doorstep, often in the aftermathof revelations about the alleged unethical behaviorof both civil servants and politicians in order toensure fair and honest behavior of individuals andorganizations acting in the public domain. This hasinfluence International organizations such as theWorld Bank to take a strong interest in ethics andhave become a key concern to the European Unionbecause the result of distrust by citizens on the publicsector was apathy to democratic activity. This hasimpacted negatively upon the economic performanceof many Organisations for Economic Co-operationand Development (OECD) countries (Davis, 2009).

In Nigeria, many institutions has been establishedto enforce the ethical codes such as codes of conductbureau, courts, EFCC, ICPC, ICAN, ANAN etc butthe more the institutions, the more the growth of

29

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April 2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

ISS

N -

245

6-78

68http

://sijitcs.com

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

unethical behaviours. The governance in Nigeria’spublic sector becomes more problematic andethically tasking as a result of endemic corruption.The lack of an effective ethical organizationalframework to coordinate the civil servants hasastronomically worsened unethical practices inpublic services (Scott, 2004). Unethical and corruptpractices are sources of negative image to agovernment which is even worse than corruption.

Evidence has shown that noncompliance with theprofessional ethics has led to various forms of fraudand corruption which has heavily harm the economy,lower investment levels and reduce public finances.Damages done to public institutions and their budgetsby fraud and corruption were enormous ranging fromfinancial loss to reduction of organizationalperformance, reputation, credibility and publicconfidence. Consequently, the level of relationshipof ethical requirements to ethical behavior is centralto criticisms over the past 30 years because theprofession has claimed to be both moral and ethicalin their dealings but this assertion has beenquestioned in the public sectors.

However, the above circumstances lead to theformulation of the following research questions.

i. Are professional accountants in the Nigerianpublic sector complying with the professional ethics?

ii. Is there any difference in perception betweenprofessional auditors and accountants in the Nigerianpublic sector with regard to level of compliance withprofessional ethics?

iii. Is there disparity in perception betweenANAN and ICAN professional member with regardto compliance with the professional ethics?

iv. Are there challenges affecting the professionalethics practices in the Nigerian public services?

These research hypotheses were developed for thestudy

H1: The public sector professional accountants are

not complying significantly with the professionalethics.

H2: There is no significance difference in the

perception of professional auditor and accountantsin the level of compliance with professional ethics

H3: The perception of ANAN and ICAN

professional accountant do not significantly differson the practice of professional ethics in the Nigerianpublic sector.

H4: There is no significant challenges affecting

the practice of professional ethics in the Nigerianpublic services

2.0 LITERATURE REVIEW

This section is structured into three dimensionalissues of conceptual, theoretical and empirical

2.1 Conceptual issues

2.1.1 Ethics and Profession

The word ‘Ethics’ is derived from the Ancient Greekword ‘ethikos’ means customs and habits. It coversthe analysis and employment of concepts such asright and wrong, good and evil and do’s and don’ts(Saeed, 2007). Ethics is defined as the branches ofphilosophy concerns value regarding humanbehavior pertaining to the rightness and wrongnessof actions and to the goodness and badness of theintent and consequences of such actions (Asif, 2010and ACCA, 2014). Ethics can be defined broadly asa set of moral principles or values. Each of us hassuch a set of values, although we may or may nothave considered them explicitly. Philosophers,religious organizations and other groups have definedethics in various ways as an ideal set of moralprinciples or values such as laws and regulations,religious doctrine, codes of business, ethics forprofessional and industry groups and codes of

30

2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll Aprilhttp

://sijitcs.comIS

SN

- 2

456-

7868

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

conduct within individual organizations (Kabir,2009). In other words, ethics is the set of moralstandards for judging whether something is right orwrong (Gitman & McDaniel, 2002). It has beenfound that there exists an overlap between ethics andthe law. Nevertheless ethics and law are notequivalent. The law can be seen as the minimumacceptable standards of behaviour and many ethicalissues are not explicitly covered by law (Larsson,2006).

Saeed (2007) explains that a profession in anoccupation requires extensive training and masteryof specialized knowledge and usually has aprofessional association, ethical code and processof certification or licensing such as Engineering,Medicine, Social Work, Teaching, Law, Finance,Military, Nursing, Accountancy etc. Each of theseprofessions holds to a specific code of ethics andmembers are almost universally required to swearsome form of oath to uphold those ethics, therefore‘professing’ to a higher standard of accountability.Each of these professions also provides and requiresextensive training in the meaning, value andimportance of its particular oath in practice of thatprofession.

Acting in the public interest involves having regardto the legitimate interests of clients and others whorely upon the objectivity and integrity of theprofessional to support the propriety and orderlyfunctioning of an entity which can only be achievedwith existence of good professional conduct(Institute of Chartered Accountant in England andWales (ICAEW). The professional conductrepresents a set of ethical rules and virtues whichare binding to all the individuals and groups whowork in the society through the performance of theirduties (Al qtaish, Baker & Othman, 2014). Theimportance of professional conducts by professionalsis to perform their profession fully with sincerity,objectivity and integrity lies on the organizers of theprofession to legislate laws, regulations andprinciples guiding the professional conduct.

The society places even higher expectations onprofessionals. People need to have confidence in thequality of the complex services provided byprofessionals. Ethics in accountancy profession areinvaluable to accounting professionals and to thosewho rely on their services such as clients, creditgrantors, governments, taxation authorities,employees, investors, the business and financialcommunity. These users perceive the professionalaccountants as highly competent, reliable, objectiveand neutral people. Professional accountantstherefore, must not only be well qualified but alsopossess a high degree of professional integrity. Theprofessional ethical codes call for their members tomaintain a level of self-discipline that goes beyondthe requirements of laws and regulations (Thunaibat,2010).

2.1.2 Need for Professional Ethics forProfessional Accountants

Each of the major professional association foraccountants has a code of ethics. Now as the businessand financial world is adopting internationalaccounting and auditing standards, it is becomingmore necessary to adhere to certain Code of ethicsprescribed by international and national accountancybodies. A code of ethics is often a formal statementof the organization’s values on certain ethical andsocial issues relating to the profession and practiceof the professional knowledge. This also includesthe principles and procedures for specific ethicalsituations. Regardless of the role of accountants, itis mandatory to adhere specifically to professionalcode of ethics applicable to their profession (IFAC,2015).

Asif (2010) discuss the reasons why ethics is so muchimportant in accounting and auditing profession. Hehighlighted the following reasons:

i. Professional accountants have a responsibilityto consider the public interest and maintain thereputation of the accounting profession (ICAEW,2009 and 2010).

31

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April 2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

ISS

N -

245

6-78

68http

://sijitcs.com

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

ii. Professional accountants give an independentview on a range of issues on behalf of clients. Theyoften have access to confidential and sensitiveinformation (ICAEW, 2009 and 2010).

iii. The professional sees himself or herself asresponsible to the customer; the mission is to solvethe problem of the customer, to create the value thatthe customer requires. If that value is not created, ifproblem is not solved, the professional has not donehis or her job (Kabir, 2009).

iv. Technically, the professional accountantsshould carry out professional services in accordancewith the relevant technical and professionalstandards. This must be compatible with therequirements of integrity, objectivity and in the caseof professional accountants in public practice,independence (Kabir, 2009).

Mehran, Masoud, Abbas & Mohammad (2014)asserts that ethics is require in the accountingprofession due to fraud, misappropriation of assets,neglection of internal controls to abuse, forcingsubordinates to record transactions incorrectly,collusion with the auditor for non-disclosure offinancial irregularities, Use of improper accountingpractices, Disclosure of confidential information ofthe employer competitors and failure to provideadequate storage for inventory and depreciationexpense recorded.

2.1.3 Professional Code of Ethics forAccountants

ACCA (2014) opine that Professional ethics is aboutprofession obligation to the public. Everyprofessional accountancy body has issued a code ofconduct and code of ethics for its members andstudent members (ICAN, 2014). The board saddledwith responsibility of issuing professional ethics foraccountants is ‘The International Ethics StandardsBoard for Accountants (IESBA)’ located withinthe International Federation of Accountants(IFAC). The IFAC is a federation of all accountancybodies throughout the world. All the major

international and national associations like ACCA,AICPA, ICMA, ICAP, IASB, ICAN, ANAN etc aremember of the organizations. The mission of IFAC,as set out in its constitution, is “the worldwidedevelopment and enhancement of an accountancyprofession with harmonized standards, able toprovide services of consistently high quality in thepublic interest” (IFAC, 2015).

The IESBA Code sets out the ethical requirementsfor professional accountants and states that anymember body of IFAC (such as ICAN) or anyindividual firm of accountants may not apply ethicalstandards that are less strict than those in the IESBACode. The IESBA Code therefore establishes aminimum world-wide code of ethical conduct foraccountants (IFAC, 2015 and ACCA, 2014). TheIESBA Code is divided into three parts: Generalprinciples and application of the code; Guidelinesfor accountants in public practice and Guidelines foraccountants in business. IFAC (2015) and IESBA(2015) code of ethics for professional accountantson General Fundamental Principles has prescribedfive (5) fundamental principles which member shallcomply with and this establishes the fundamentalethical principles that apply to all members as wellas guidance on the threats and safeguards relating tothose fundamental principles.

i. Integrity: A professional accountant should bestraightforward and honest in all professional andbusiness relationships.

ii. Objectivity: A professional accountant shouldnot allow bias, conflict of interest or undue influenceof others to override professional or businessjudgments.

iii. Professional Competence and Due Care: Aprofessional accountant has a continuing duty tomaintain professional knowledge and skill at thelevel required to ensure that a client or employerreceives competent professional service based oncurrent developments in practice, legislation andtechniques.

32

2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll Aprilhttp

://sijitcs.comIS

SN

- 2

456-

7868

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

iv. Confidentiality: A professional accountantshould respect the confidentiality of informationacquired as a result of professional and businessrelationships and should not disclose any suchinformation to third parties without proper andspecific authority unless there is a legal orprofessional right or duty to disclose.

v. Professional Behaviour: A professionalaccountant should comply with relevant laws andregulations and should avoid any action thatdiscredits the profession.

According to IESAB (2015), AAT (2014) and Asif(2010), it may be possible that the circumstances inwhich members operate give rise to specific threatsto compliance with the fundamental principles. Thesethreats may include self-interest threats; self-reviewthreats; advocacy threats; familiarity threats andintimidation threats. AAT (2014) and Asif (2010)assert safeguards are actions or other measures thatmay eliminate threats or reduce them to an acceptablelevel. These fall into safeguards created by theprofession, legislation or regulation and safeguardsin the work environment.

The part B of the Code illustrates how the conceptualframework is to be applied and is not intended to be,nor should they be interpreted as, an exhaustive listof all circumstances experienced by a member inpractice that may create threats to compliance withthe fundamental principles. Therefore, it is notsufficient for a member in practice merely to complywith the examples presented; rather, the frameworkmust be applied to the particular circumstances faced.

The areas cover by this section includes theProfessional Appointment; Conflicts of Interest;Second Opinions; Fees and Other Types ofRemuneration; Marketing Professional Services;Gifts and Hospitality; Custody of Client Assets;Objectivity and Independence of assuranceengagements.

Finally, part C of the Code illustrates how theconceptual framework contained in Part A is to be

applied in specific situations relevant to members inbusiness. Investors, creditors, employers and othersectors of the business community, as well asgovernments and the public at large, all may rely onthe work of members in business. Some of thosecircumstances include: Threats and safeguards;Conflicts of interest; Preparation and reporting ofinformation; Financial interests, compensation andincentives linked to financial reporting and decision-making and Inducements through Receiving offersand Making offers.

2.2. Theoretical Background

Based on the literature reviews, theory of institutionand theory of profession are adopted for the study.

2.2.1 Theory of Institution

Institutional theory is not really a coherent systemof rules. It is rather a collection of ideas that togetherform a, somewhat consistent, perspective of themechanisms supporting and restricting socialbehaviour for an excellent attempt to integratedifferent institutional perspectives into a singleanalytic framework (Scott 2001). The institutionalperspective is adopted for research within disciplinesas diverse as economics, political science, sociology,and business studies (Johansson 2002).

Since the 1970s public administration institutionsas a research domain has increasingly opened up tocontributions from other social sciences such ashistory, political science and sociology oforganizations. Potentially the most importantimpediment to a more central position forinstitutionalism is that the term means so many thingsto different scholars, and that some of the alternativeapproaches are not only different but evencontradictory (Hall and Taylor, 1996; Kato, 1995).If one adopts some versions of the institutionalapproach he or she may have very different empiricalevidence, and make very different predictions aboutbehavior, than if one were doing research usinganother version (Peters, 2000).

33

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April 2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

ISS

N -

245

6-78

68http

://sijitcs.com

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

Different new schools of thought have emerged inacademic circles. Institutional theory is a label thatoversimplifies the fact that such schools are notexactly alike: they do not share the same agenda. Ithas become less normative and more empirical,considering institutions as dependent variables aswell as autonomous actors (Thoenig, 2011).Institutional theorists believe that institutions notonly offer and constrain behavioral alternatives, butthey also, up to a certain extent model individualpreferences (March & Olsen, 1995). This means thatinstitutions, directly and indirectly determine themotives guiding individual behavior but these canbe achieve in different ways/approaches whichcollectively include normative institutionalism,rational choice institutionalism, historicalinstitutionalism, sociological institutionalism, newinstitutionalism, and local order or actorinstitutionalism

However, this study adopts the rational choiceapproach. The rational choice institutionalism is thatinstitutions are arrangements of rules and incentives,and the members of the institutions behave inresponse to those basic components of institutionalstructure (Peters, 2000). The preferences of themembers are not modified by their membership inthe institution. In the rational choice approach,institutions are conceptualized as exogenous to thevalues of the individuals functioning within them.This statement means that it is assumed thatindividual values will not be altered by involvementwith the institution (Peters, 2000). Behavior willchange in response to the assortment of opportunitiesand constraints presented by the structure, but thevalues that condition behavior are assumed to beunaffected by the institution (Lawton & Macaulay,2009). In Nigeria, there are several institutions suchas ICPC, EFCC, Public Complaints Commission,NAFDAC, ANAN, ICAN etc. that work differentlyin ensuring high standards of behavior in publicservice and position. These institutions are supposedto affect and influence the behavior of individuals

working in the public service. However, from therational choice approach, the values of theindividuals are not altered by the institution.

2.2.2 Theory of Profession

While there is no agreed definition of a profession,the Australian Council of Professions (ACP) definesit as a disciplined group of individuals who adhereto high ethical standards and uphold themselves to,and are accepted by, the public as possessing specialknowledge and skills in a widely recognised,organized body of learning derived from educationand training at a high level, and who are prepared toexercise this knowledge and these skills in theinterest of others (Australian Competition andConsumer Commission (ACCC), 2011). There aremany categories of traditional professions such asdoctors, pharmacists, lawyers, architects andengineers.

Acknowledged as a leading researcher on the Theoryof Profession, Abbott (1988) suggests three potentialrights for a profession to claim jurisdiction: withinthe legal framework, through public opinion and inthe workplace. He defines a profession’s socialstructure as including groups, controls and worksitesthat work cohesively to create an improvedprofessional model. This structure influencesprofessions in the following ways: The moreorganized a profession, the more effective the claimof jurisdiction; Organization into a single,identifiable association is a pre-requisite to anypublic/legal claim of jurisdiction; Level of formalityof organizational structure may provide advantage/flexibility in workplace competition and highlyorganized, resilient internal structures.

Fournier (1999), in describing the profession ofaccounting, presents a model of professionalism asa disciplinary logic that includes criteria oflegitimacy, public good, social welfare, as well asprofessional competence based on knowledge,conduct and control. Theory of Profession providesan analytical lens with which to

34

2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll Aprilhttp

://sijitcs.comIS

SN

- 2

456-

7868

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

understand the characteristics, attributes andstructure of any profession.

In an accounting context, the Theory of Professionis described as the power and reputation granted bysociety to the profession in terms of protecting publicinterest where professionals acquire a body ofknowledge, which is connected to the major needsand values of the social and accounting system(Pollock & Amernic, 1981). Professions are expectedto commit their services to the interest of the publicrather than the interests of their clients or self-interest(Pollock & Amernic, 1981). Therefore, accountingprofessionals are regarded as a mechanism to protectpublic interest as they are required to act above andbeyond material incentives (Larson, 1977). In thecontext of this study, the Theory of Professionprovides a useful framework for identifying thefunctions and attributes of the profession (Canning& O’Dwyer, 2001), which is consistent with thenecessary requirements and qualifications to workin the field of accountancy. They present the Theoryof Profession framework under five attributes thatcontribute to accounting ‘professionalism’ andultimately, the protection of public interest. Theseattributes are test of competence; further study andrelevant training; a register of qualified members;enforcement of a high standard of professionalconduct and organisation within a specificoccupation (Candilis, 2009; Gaffikin, 2009 andKranacher, Riley, & Wells, 2011)

2.3 Empirical Evidences

Asif (2010) conducts study on Ethics in Auditingand Ethical Studies in different Accounting Bodies.The study discusses the various ethical dilemmas,threats, safeguard and steps of avoiding ethicalthreats in selecting auditing engagement. This wasachieved through the explanation of concepts ofethics and studies of degrees of ethical studies invarious public accountants’ bodies around the world.To fulfill the requirement of the study data arecollected mainly from different books, studymaterials and journals on ethics and auditing. IFACCode of Conduct for professional accountant andwebsites of the various professional bodies around

the world. The study found clearly that all theaccounting bodies are maintaining high level ofethical studies for their candidates. The studytherefore recommends that practitioners shouldobserve the code of ethics and maintain theirindependence while certifying and expressingopinion on the financial statements becauseaccounting profession has important publicresponsibilities.

Al Qtaish, Baker & Othman (2014) investigate theethical rules of auditing and the impact of compliancewith the ethical rules on auditing quality. The studydeveloped questionnaire with 37 questionsdistributed to a sample of (59) auditors practitionersof the audit profession but (54) were recovered andwere analysis using one sample t-test and regressionanalysis. The study found that there is a high degreeof commitment to the auditors professional ethicson the quality of the audit. The study recommendsthat supervisory authorities and the Organization forthe audit profession hold training courses, workshopsand seminars on auditing standards and rules ofethics of the audit profession to further strengthenedthe compliance.

Casimir, Izueke & Nzekwe (2014) examine theimperatives of good ethical conduct in the conductof government business in Nigeria. Usinginstitutional theory suggests that moralcontradictions in institutional behavior expectationfrom the public deepen daily. The perceived lack ofan effective ethical organizational framework tocoordinate the activities of various institutions hasastronomically worsened unethical practices such ascorruption in the Nigerian public service. The studyconclude that the behavioral and errant departure ofcivil servants and Nigeria’s public service from thecore human values that ensure transparent privateand public conduct of individuals have resulted inunderperformance and underdevelopment and inorder to move towards good ethical conduct ingovernment and reduce corruption, it stronglyrecommend the integration of theistic humanism andcore African values in both individual and publicconduct of civil servants in Nigeria. A more realistic

35

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April 2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

ISS

N -

245

6-78

68http

://sijitcs.com

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

African traditional approach to ethical restraint ofpublic servants from indulging in corrupt behaviorby subjecting them to customary oath taking basedupon the theistic values of fear of sin against motherearth should be employed.

Mehran, Masoud, Abbas & Mohammad (2014) writean essay on Professional Ethics in Accounting andAuditing. They assert that Ethics is a subject that isinclusive to all aspects of human life. The paperdescribe moral and ethical paradigms andprofessional ethics and the history of ethics isreferenced in the following basic features andelements of ethics; ethical decision-making models,standing ethics and its role in advancement,professional growth and development, professionalethics and ethical guidelines in accounting andauditing.

3.0 SECTION THREE:METHODOLOGY

3.1 Research Design

The study adopts survey research design methodwhich involves the use of questionnaire surveytechnique that requires rigorous research planning,execution and often involves testing of hypothesisor answering research questions. This technique wasadopted because of its advantages over other methodsin terms of relatively high population and thegeneralizability of the sample selected to thepopulation (Pallant, 2007).

3.2 Population and Sampling Techniques

A survey research design was used. The justificationfor the use of survey research for this study accordingto Asika (2004) is that convenience with which thesurvey can be conducted and inferences for largerpopulation can be made from the result.

All the Accountants and Auditors in the officeAccountant general and Auditor general of federationare the population of this study. The study adopts apurposive sampling technique to select all charteredand certified Accountants, who belong to arecognized professional body by IFAC, because they

Source: Author’s review

This study focuses on primary data which wasobtained through the use of carefully wordedquestionnaire administered on all the professionalchartered accountants of ANAN and ICAN inAccountant General Office and Auditor generaloffice.

Consequently, a total of One thousand, one hundredand twenty seven (1,127) questionnaires wereadministered but only seven hundred and Eight five(785) were returned constituting about 70% responserate. The high reduction in response rate is not asurprise because more than 40% of their staffers werein all the state of federation which time does notallow the study to cover. However, the response rateobtain perhaps be attributed to the fact that theresearcher is also a member and the questionnaireswere delivered by hands.

3.3 Data analysis and Reporting

Descriptive and inferential statistical techniqueswere used to analyze the data collected. Thedescriptive statistics include mean, maximum,minimum and standard deviation which measures thelevel of dispersion of mean distribution were usedto provide a snap shot of the variables in the study.While kurtosis, skewness, Kolmogorov-Smirnov andthe

36

were expected to apply professional ethics in all theirofficial dealings. Out of the population of 3,827,1,127 were professionals representing 30% of thetargeted population. The sample is even more thanthe sample size specified by Krejcie and Morgan(1970) which affirm that appropriate sample size forpopulation of 3,500 is 346. The detail is as follow intable 1:

2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll Aprilhttp

://sijitcs.comIS

SN

- 2

456-

7868

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

Shapiro-Wilk tests were used to determine thenormality of the data. In addition, independentsample t test, a parametric test will be used to testfor data that does not violate the assumptions ofparametric test while an equivalent non-parametrictest, Mann-Whitney U test, will be used to test datathat violate the normal distribution assumptions(Field, 2006).

4.0 SECTION FOUR

4.1 Presentation of Data and DescriptionStatistics

4.1.1 Socio-demographic Characteristics ofRespondents

The demographic characteristic of the respondentswere presented in table 4

Table 2: Demographic Characteristics ofRespondents

Source: Authors’ Survey, 2014

The survey result shown in Table 2 revealed that allthe professional Accountants and Auditors wereabove the age groups of 30 and 74.7% was betweenthe age group of 30-40 years while 41 years aboverepresent the balance of 25.3%. It is clear indication

that professional in the Nigerian public sector werein their active year of service and will result to betterachievement of state goal and objectives. The surveyalso showed that 69.5% of the respondents were malewhile 30.5% were female. On the distribution of themanagement level of respondents, 15.7%, 79.0% and5.2% were Top, Middle and Lower managementrespectively. The result implies that most of theprofessional accountants were still in operationalmanagement level where all the statutory financialactivities are carried out. In addition, the surveyindicates that respondents with working experiencebetween 5-10 years were 69.5% while 11-15years,15-20 years and above 21 years working experienceconstitute 5.2%, 10.5% and 14.8% respectively. Thisimplies that more than half of the respondents(85.1%) have a current working experience. Thesurvey also revealed that most of the respondentshave a sound formal education as 90% above of therespondents have first degree and possess a reputableprofessional qualification. It is obvious that theAccountant will be much higher than the Auditor,consequently, the result reveal that 55.3% areAccountants while 44.7% represent the professionalauditors in the state public services. This implies thataccountants do embrace professional body than theauditors. Overall, the result of the survey indicatesthat the respondents have the versatile requisiterequirement to provide the required answers to thequestionnaire.

4.1.2 Descriptive Statistics

Table 3 present the descriptive statistic with respectto the mean, Maximum, minimum, standarddeviation, skewness and kurtosis of the data.

Table 3: Descriptive Statistics of the Data

37

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April 2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

ISS

N -

245

6-78

68http

://sijitcs.com

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

Source: Author’s Computation

Table 3 shows the minimum and maximum of thescores obtained from the questionnaire and the scoreobtained were within the boundary of likert scale inthe questionnaire. The mean results of theprofessional ethics and the threat among charteredAccountants is above average for all respondentswhile the mean for principle of ethic shows thehighest compare to other fundamental principles. Themean on the use of government property reveal thehighest average mean for the identified threats toprofessionals in the public sector while the mean forinducement was not only among the lowest but alsoreveal the highest standard deviation of 1.22implying that it constitutes the highest threats to theapplication of professional ethics in public sector.

Kolmogorov-Smirnov and the Shapiro-Wilk testswas used to determine if the sample came from anormally distributed population. This becameexpedient in order to determine the appropriatestatistical tests to use for the significant of thedifferences in the perception. The results of the testswere presented in table 4.

Table 4: Result of Data Distribution NormalityTest

Source: Author’s Computation.

Table 4 presents the results of the Kolmogorov-Smirnov Test and Shapiro-Wilk normality test ofdistribution for the variables on the professional ethicand the threats. Normality assumption is assumed ifthe significant level is greater than 5% level ofsignificant. Independent sample t test will be usedto test the variables that do not violate the assumption

of parametric test. While Man-Whitney U test willbe used to test the variables if otherwise. The resultin table 4 reveals that the level of significant for bothKolmogorov-Smirnov and Shapiro-Wilk test is lessthan 5%. This implies that the data from the variablesare not normally distributed and consequently, Man-Whitney U test is used to test for the differences inthe professional ethics practices betweenProfessional Accountants and Auditor and the ICANand ANAN members in public services.

4.2 Restatement of Hypothesis and Discussionof Findings

Hypothesis One

H01

: The public sector professional accountants arenot complying significantly with the professionalethics.

Table 5. One-Sample Test on the professionalethics practice in Public Sector

Source: Authors’ computation

Table 5 show the result of the one sample t-test onthe professional ethics practices in public sector. Theresult shows that the mean of all the fundamentalprinciples apply by professionals Accountants ishigher than 3.0. This implies that all professionalAccountants comply with professional codes of ethicin all their business and official dealings. This isevidence with the lowest mean score of 4.14 with ap-value of 0.000 which indicates a significance levelof 1%.

Since the population mean shows a mean score ofabove 3.0, the null hypothesis was rejected andrestated that public sector professional

38

2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll Aprilhttp

://sijitcs.comIS

SN

- 2

456-

7868

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

Accountants are complying with professional ethicsin their official dealings.

The findings is confirmed by the theory of professionwhich emphasis that individuals in a disciplinedgroup of profession must adhere to high ethicalstandards and uphold themselves to the public aspossessing special knowledge and skills to beexercised in the interest of others (AustralianCompetition and Consumer Commission (ACCC),2011). The finding of the study also shows that themembers of the professional bodies behave inresponse to those basic requirements of theprofession as stipulated in the rational choiceinstitutional theory. The theory affirms thatinstitutions are conceptualized as exogenous to thevalues of the individuals functioning within them inorder to achieve the stated goal and objectives(Peters, 2000). The result is also in line with theconclusion of Al Qtaish, Baker & Othman (2014)who assert that there is a high degree of commitmentto the professional ethics which make the degree ofinfluence of commitment to professional ethics onthe quality of the audit uneven. The independenceof the auditor came in first, while the auditor’sstraightening and integrity is the second and the thirdis characterized with efficiency of the auditor,commitment to professional conduct is the fourth,then the auditor’s commitment to the confidentialityof information. Asif (2010) support this withevidence that the professional accounting bodieshave provide adequate ethical studies to theprofessional and therefore, it is the duty of themembers to implement these studies in their practicaldealings in order to ensure accountability andreliability of their outputs.

Hypothesis Two

H02

: There is no significance difference in theperception of professional auditor and accountantsin the level of compliance with the professionalethics

Table 6: Result of Mann-Whitney U test fordifferences between professional accountant andauditor in professional ethics practices in publicsector

Source: Author’s Computation.

Table 6 shows the result of the Mann-Whitney Utest. Analysis of the data reveals generally that theprofessional ethics practices is not differ betweenthe Accountants and Auditors in the public sectorregardless of the slight differences observed in themean rank of the professionals. The median of allthe fundamental principles employed by theprofessional are the same for both Accountants andAuditors while the Mann-Whitney U statistics, zstatistics and significant level are as follow: Integrity(U=2686, Z=-0.111 and sig = 0.912); Honesty(U=2628.5, Z=-0.296 and sig = 0.765) ; Objectivity(U=2655.5, Z=-0.192 and sig = 0.848) ;Confidentiality of Information (U=2686, Z=-0.195and sig = 0.845) ; Professional behaviour (U=2654.0,Z=-0.200 and sig = 0.841) and ProfessionalCompetence (U=2633.0, Z=-0.268 and sig = 0.788).Therefore, the study accepts the null hypothesiswhich states that there are no significance differencesin the professional ethics practices amongAccountants and Auditors in Nigeria public services.

It can be deduced that the Accountants and Auditorswere professionals and must comply with rules andregulations of their professional body regardless ofduties and responsibility assigned because theprofession’s social structure includes groups,controls and worksites that work cohesively to createan improved professional model as proclaimed inthe theory of profession. This shows that

39

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April 2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

ISS

N -

245

6-78

68http

://sijitcs.com

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

professionals behave in a disciplinary logic thatincludes criteria of legitimacy, public good, socialwelfare, as well as professional competence basedon knowledge, conduct and control (Fournier, 1999).Therefore, being a professional implies commitmentto services to the interest of public rather thanpersonal interest (Pollock & Amernic, 1981).

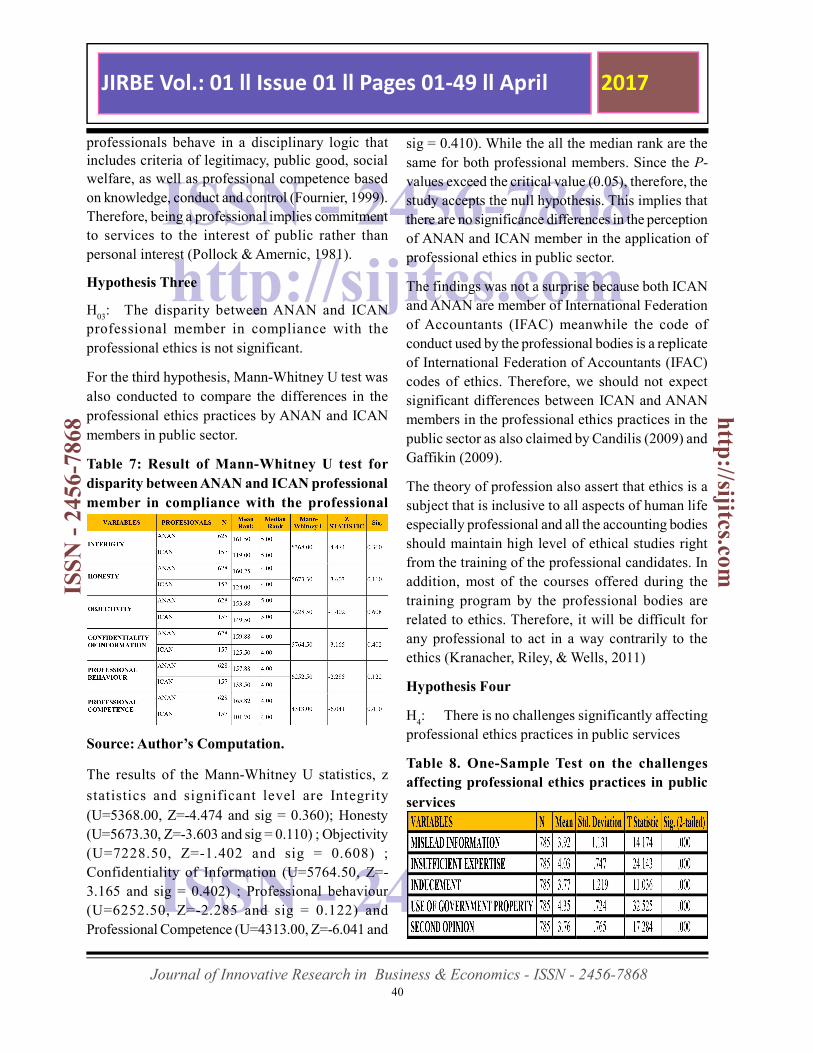

Hypothesis Three

H03

: The disparity between ANAN and ICANprofessional member in compliance with theprofessional ethics is not significant.

For the third hypothesis, Mann-Whitney U test wasalso conducted to compare the differences in theprofessional ethics practices by ANAN and ICANmembers in public sector.

Table 7: Result of Mann-Whitney U test fordisparity between ANAN and ICAN professionalmember in compliance with the professionalethics is not significant

Source: Author’s Computation.

The results of the Mann-Whitney U statistics, z

statistics and significant level are Integrity(U=5368.00, Z=-4.474 and sig = 0.360); Honesty(U=5673.30, Z=-3.603 and sig = 0.110) ; Objectivity(U=7228.50, Z=-1.402 and sig = 0.608) ;Confidentiality of Information (U=5764.50, Z=-3.165 and sig = 0.402) ; Professional behaviour(U=6252.50, Z=-2.285 and sig = 0.122) andProfessional Competence (U=4313.00, Z=-6.041 and

sig = 0.410). While the all the median rank are thesame for both professional members. Since the P-values exceed the critical value (0.05), therefore, thestudy accepts the null hypothesis. This implies thatthere are no significance differences in the perceptionof ANAN and ICAN member in the application ofprofessional ethics in public sector.

The findings was not a surprise because both ICANand ANAN are member of International Federationof Accountants (IFAC) meanwhile the code ofconduct used by the professional bodies is a replicateof International Federation of Accountants (IFAC)codes of ethics. Therefore, we should not expectsignificant differences between ICAN and ANANmembers in the professional ethics practices in thepublic sector as also claimed by Candilis (2009) andGaffikin (2009).

The theory of profession also assert that ethics is asubject that is inclusive to all aspects of human lifeespecially professional and all the accounting bodiesshould maintain high level of ethical studies rightfrom the training of the professional candidates. Inaddition, most of the courses offered during thetraining program by the professional bodies arerelated to ethics. Therefore, it will be difficult forany professional to act in a way contrarily to theethics (Kranacher, Riley, & Wells, 2011)

Hypothesis Four

H4: There is no challenges significantly affecting

professional ethics practices in public services

Table 8. One-Sample Test on the challengesaffecting professional ethics practices in publicservices

40

2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll Aprilhttp

://sijitcs.comIS

SN

- 2

456-

7868

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

Source: Author’s computation

Table 8 show the result of the one sample t-test onchallenges affecting professional ethics practices inpublic services. The benchmark for decision rulesfor accepts or rejects the hypothesis rest on middlevalue (3) which stands for indifferences by therespondent. Since all the threats/challenges have amean value higher than 3.0, the study conclude thatthe all the challenges hinder professional ethicspractices in public services. Therefore, the nullhypothesis is rejected as the population mean showsa mean score of above 3.0. This implies thatprofessional Accountants regardless of professionalbodies or schedule of duties face challenges whichserve as threats to professional ethics practices inpublic services. This influence their business andofficial dealings in the office.

The findings is also in line with the ICAN (2014)which affirms that professionals will find it difficultto comply with professional ethics if threats arepresent and consequently, his work cannot be replyupon. The existence of these threats can be attributedto be the major reason why Professionals involve infinancial malpractices.

5.0 SECTION FIVE

5.1 SUMMARY AND CONCLUSION

Based on the overall results of this study, theprofessional Accountants in the public sector complywith the professional ethics in their official dealing.This implies that the schedule of duties and cadre ofthe professionals does not influence the professionalethics practices in public sector. All the professionalbodies, that are members, must comply with theInternational Federation of Accountants (IFAC)codes of ethics. This perhaps reveals in theinsignificant differences in the professional ethicspractices among the professional Accountants in thepublic sector and that ethics is a subject that isinclusive to all aspects of human life. In addition,all the accounting bodies maintain high level ofethical studies right from the training of theprofessional candidates and all the courses offeredduring the professional training relate to ethics.

Therefore, it will be difficult for any professional toact in a way contrarily to the ethics as confirmed bythe findings of the study.

However, adherence alone to the Professional ethicscannot solve the problems of accounting scandalsthat occur around the world as a result of variouschallenges hinder professional ethics practices inpublic sector identified in the study. Apart from these,the review of institutional measures and codes ofconduct puts in place to ensure high standard ofbehavior, using institutional theory suggests thatmoral contradictions by public office holders deependaily. The perceived lack of an effective ethicalorganizational framework to coordinate the activitiesof various institutions has astronomically worsenedunethical practices in public sector. This has resultedin underperformance of professionals andunderdevelopment in the public sector.

5.2 Recommendations

In view of the above findings and for the public sectorto benefits from professional ethics practices, thestudy provides the following recommendations.

i. The government should provide financialsupport to Accountant to become member of areputable professional body.

ii. The government needs to encourage theprofessional to strengthen their compliance inprofessional ethics practices.

iii. The professional bodies and government needto strengthen the sanctions to any erring member whocommit or aid in financial misappropriation.

iv. In the event existence of threats, theprofessionals were encourage to evaluate andembrace all safeguards available to deal with thesituation.

v. The professional bodies and government werealso encouraged to introduce and embrace thetraditional oath taking in public services in order tohinder the occurrence of financial malpractices bypublic office holder.

41

JIRBE Vol.: 01 ll Issue 01 ll Pages 01-49 ll April 2017

Journal of Innovative Research in Business & Economics - ISSN - 2456-7868

ISS

N -

245

6-78

68http

://sijitcs.com

ISSN - 2456-7868

ISSN - 2456-7868http://sijitcs.com

Finally, future researches are encourage to beconducted on impact of entity’s ethic on theperformance of employees in order to confirmwhether the same conclusion will be reached withthis study.

REERENCES

1. Abbott, A. (1988) The System of Professions: AnEssay on the Division of Expert Labor. Chicago:University of Chicago Press.

3. Al-Qashi, Z. S. (2005). The collapse of someinternational companies and their impact on the

4. accounting environment. Arab Journal ofAdministration, the Arab Organization forAdministration, the Arab League, 25(II), 1-9.

5. Al Qtaish, H.F., Baker, A.A.M. & Othman H.O. (2014). The Ethical Rules of Auditing AndThe

6. Impact Of Compliance With The Ethical RulesOn Auditing Quality. Isra University, Jordan(IJRRAS), 18(3),1-12.

7. Ani Casimir, K. C. (2009). The Role ofTraditional Institutions and Intangible Resourcesin

8. Cultural Development among AfricanIndigenous Peoples: A Religion-PhilosophicalExploration of the Ezeagu Wawa IndigenousAfrican People. Journal of African Studies,24(2), 1-11.

9. Ani Casimir, K. C., Izueke, E. M., & Nzekwe,I. F. (2014). Public Sector and Corruption in

10. Nigeria: An Ethical and InstitutionalFramework of Analysis. Open Journal ofPhilosophy, 4(2), 216-224. http://dx.doi.org/10.4236/ojpp.2014.43029

11. Association of Accounting Technicians (AAT)(2014). AAT Code of Professional

12. Ethics. New York, USA. Published by IFAC,529 Fifth Avenue,

13. Association of Chartered CertifiedAccountants (ACCA) (2008). Corporatereporting Essential

14. text; UK Wokingham, Kaplan Publishing ,Berkshire.

15. Asif A. (2010) Ethics in Auditing and Base ofEthical Studies in Different Accounting Bodies.

16. Department of Accounting & InformationSystems, Faculty of Business Studies, Universityof Dhaka, Bangladesh.

17. Asika, N. (2004). Research Methodology: AProcess Approach, Lagos, Mukugamu and

18. Brothers Enterprises19. Candilis, P.J. (2009). The Revolution in

Forensic Ethics: Narrative, Compassion and aRobust

20. Professionalism. Psychiatr Clin North Am,32(6), 423–435.

21. Collste, G. (1996). Inledning till etiken. Lund:Studentlitteratur

22. Davis, H. (2009). Ethics and Standards ofConduct. In T. Bovaird, & E. Loffler (Eds.),Public

23. Management and Government. New York:Routledge.

24. Dukor, M. (2010). African Philosophy in theGlobal Village: Theistic PanpsychicRelationship,

25. Axiology and Science. USA: LAP LAMBERTAcademic Publishing.

26. Field, A. (2006). Discovery Statistic UsingSPSS. (2nd Edition) Sage Publication; London,

27. New Delhi.28. Fournier, V. (1999). The Appeal to

Professionalism as a Disciplinary Mechanism.The

29. Sociological Review, 47(2), 280–307.30. Gaffikin, M. (2009). Commentary Education

for an Accounting Profession’, PacificAccounting

31. Review, 21(2), 170-185.32. Gitman, L. I. & McDaniel, C, (2002). The

Future of Business. Interactive Edition, South-33. Western College Publishing USA.34. Hall, P. A. & Taylor, R. C. R. (1996). Political

Science and the Three New Institutionalisms,35. Journal of Political Studies, 44(7), 952–973.36. Institute of Chartered Accountants of England

and Wales (ICAEW) (2009). Assurance Study37. Manual, ACA Professional Stage Knowledge

Level.38. Institute of Chartered Accountants of England

and Wales (ICAEW) (2010). Assurance Study39. Manual, ACA Professional Stage Knowledge

Level.40. Institute of Chartered Accountants of Nigerian

(ICAN) (2014). Management, Governance and

42

Related Documents

![Indian Constitutional Law Review [ISSN: 2456-8325] Edition V …iclrq.in/editions/jul18/Art6.pdf · Indian Constitutional Law Review [ISSN: 2456-8325] Edition V [July 2018] Published](https://static.cupdf.com/doc/110x72/5f81a2116ed8d010624d4b00/indian-constitutional-law-review-issn-2456-8325-edition-v-iclrqineditionsjul18art6pdf.jpg)

![Indian Constitutional Law Review [ISSN: 2456-8325] …iclrq.in/editions/jul18/Art3.pdfIndian Constitutional Law Review [ISSN: 2456-8325] Edition V [July 2018] Published by Agradoot](https://static.cupdf.com/doc/110x72/5e757292f8b9e5405c52d8c6/indian-constitutional-law-review-issn-2456-8325-iclrqineditionsjul18art3pdf.jpg)