ISM Mid-winter Conference ISM Mid-winter Conference Short Term Perspectives for Natural Short Term Perspectives for Natural Gas Gas February 2006 February 2006 knowledge to bridge the gap

ISM Mid-winter Conference Short Term Perspectives for Natural Gas February 2006 knowledge to bridge the gap.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ISM Mid-winter ConferenceISM Mid-winter ConferenceShort Term Perspectives for Natural GasShort Term Perspectives for Natural Gas

February 2006February 2006

knowledge to bridge the gap

Page # 2 Petral Consulting Companyknowledge to bridge the gap

Page # 3 Petral Consulting Companyknowledge to bridge the gap

Katrina & RitaKatrina & RitaThrough the heart of the Gulf of MexicoThrough the heart of the Gulf of Mexico

Page # 4 Petral Consulting Companyknowledge to bridge the gap

Shut-in Natural Gas ProductionShut-in Natural Gas ProductionKatrina/Rita ImpactKatrina/Rita Impact

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,000

29-A

ug 6 14 22 30 8 16 24

1-N

ov 9 17 25 3 11 19 27 3 11

Mill

ion

Cu

bic

Ft

per

Day

Katrina/Rita S-I Ivan S-I

Page # 5 Petral Consulting Companyknowledge to bridge the gap

What Happened after Katrina & Rita?What Happened after Katrina & Rita?

With 5-8 Bcfd of GOM production shut-in, forecasts of $20 per MM Btu were prevalent in the fourth quarter of 2005

Gas inventory reports were generally ignored during October/November

How did we avoid a price spike to $20 per MM Btu?» Rules of curtailment were very important» Price premiums versus resid triggered fuel switching

Page # 6 Petral Consulting Companyknowledge to bridge the gap

Gas Pricing DifferentialsGas Pricing Differentials

Usually, gas prices in Louisiana average 5-10 ¢ per MMBtu above Houston Ship Channel. During the 4th quarter, the premium average $2.00 per MMBtu. Why were pricing differentials so much wider than normal?» Rules of curtailment ARE very important» Consumers who were curtailed were willing to pay very

high prices to buy gas away from consumers who were not curtailed

Page # 7 Petral Consulting Companyknowledge to bridge the gap

Natural Gas Price InfluencesNatural Gas Price Influences

Other than hurricanes, natural gas prices respond to three fundamental influences:» Trends in crude oil and resid pricing» Weekly inventory report & year-to-year

comparisons» Demand in the power generation market

Page # 8 Petral Consulting Companyknowledge to bridge the gap

Gas Fired Power GenerationGas Fired Power GenerationPeak Demand SeasonPeak Demand Season

10

12

14

16

18

20

22

24

1999

2000

2001

2002

2003

2004

2005

2006

Bill

ion

Cub

ic F

t per

Day

Page # 9 Petral Consulting Companyknowledge to bridge the gap

Gas Fired Power Generation:Gas Fired Power Generation:Share of Total GenerationShare of Total Generation

1011

121314

151617

1819

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

% o

f Tot

al P

ower

Gen

erat

ion

History Forecast High Range

Page # 10 Petral Consulting Companyknowledge to bridge the gap

Residential/Commercial Demand:Residential/Commercial Demand:Winter SeasonWinter Season

0

5

10

15

20

25

30

35

40

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Bill

ion

Cu

bic

Ft

per

Day

History Forecast High Case

Page # 11 Petral Consulting Companyknowledge to bridge the gap

Injections into Working Gas StorageInjections into Working Gas Storage

-5

0

5

10

15

20

Ap

ril

May

Jun

Jul

Au

g

Sep Oct

No

v

Bill

ion

Cu

bic

Fee

t p

er D

ay

Avg 01-03 2005 pre Katrina 2005 post Katrina

Page # 12 Petral Consulting Companyknowledge to bridge the gap

Working Gas StorageWorking Gas StorageExplanations for Weak Injection RatesExplanations for Weak Injection Rates

Railroad maintenance in Wyoming began in July and coal deliveries were curtailed – by some amount. Some power generators switched to gas // demand was 3-5 Bcfd higher than in 2004

Hot weather pushed electric power demand sharply higher. Katrina & Rita disrupted short term supply plans for many

power generators and industrial consumers. Despite the loss of 5-8 Bcfd for 2 months, natural gas

storage injections were sufficient to push inventories to a peak of 3.25 Tcf by mid-November – gas pipelines affected by supply losses invoked “rules of curtailment”

Page # 13 Petral Consulting Companyknowledge to bridge the gap

Injections into Working Gas StorageInjections into Working Gas Storage

0

2

4

6

8

10

12

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Bill

ion

Cu

bic

Fee

t p

er D

ay

History Base Case High Case

Page # 14 Petral Consulting Companyknowledge to bridge the gap

Working Gas In StorageWorking Gas In StorageSeasonal MinSeasonal Min

00.20.4

0.60.8

11.21.4

1.61.8

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Tri

llio

n C

ub

ic F

eet

History Forecast High Case

Page # 15 Petral Consulting Companyknowledge to bridge the gap

Natural Gas In Working StorageNatural Gas In Working StorageSeasonal PeakSeasonal Peak

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Tri

llio

n C

ub

ic F

eet

History Forecast High Case

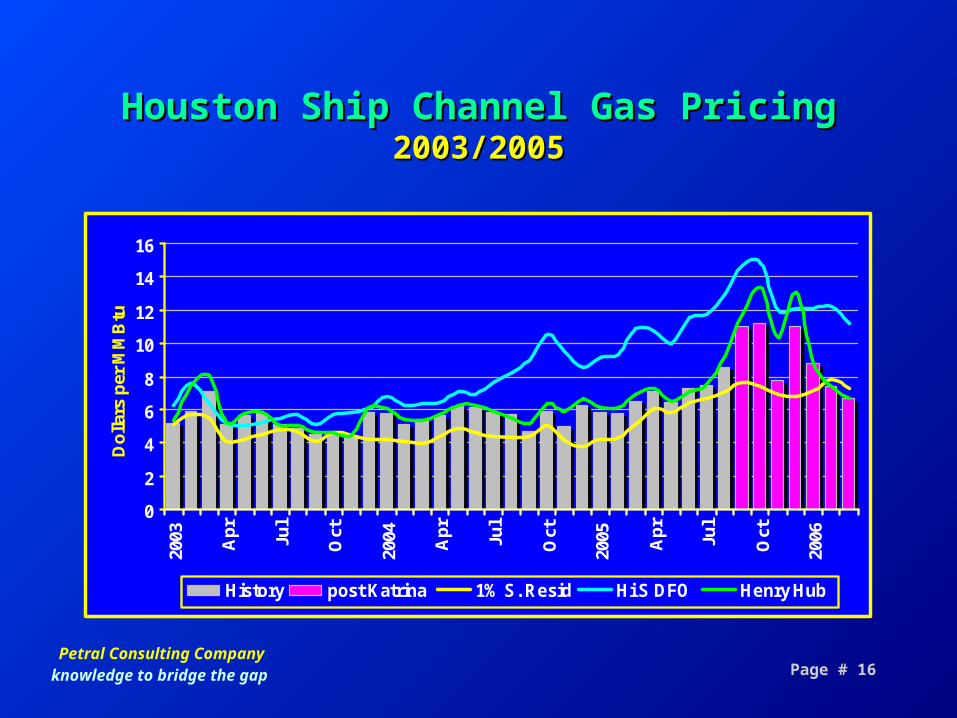

Page # 16 Petral Consulting Companyknowledge to bridge the gap

Houston Ship Channel Gas PricingHouston Ship Channel Gas Pricing2003/20052003/2005

0

2

4

6

8

10

12

14

16

2003 Ap

r

Jul

Oct

2004 Ap

r

Jul

Oct

2005 Ap

r

Jul

Oct

2006

Do

llars

per

MM

Btu

History post Katrina 1% S. Resid Hi S DFO Henry Hub

Page # 17 Petral Consulting Companyknowledge to bridge the gap

Cash Market Henry Hub Natural GasCash Market Henry Hub Natural GasWinter AveragesWinter Averages

0

2

4

6

8

10

12

14

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Do

llars

per

MM

Btu

History Forecast 1% S. Resid Hi S DFO

Page # 18 Petral Consulting Companyknowledge to bridge the gap

Cash Market Natural Gas PricesCash Market Natural Gas PricesShort Term ForecastShort Term Forecast

0

2

4

6

8

10

12

14

03:1

04:1

05:1

06:1

Do

llars

per

MM

Btu

Henry Hub Forecast 1% S. Resid Hi S DFO HSC

Page # 19 Petral Consulting Companyknowledge to bridge the gap

Cash Market Henry Hub Gas PricesCash Market Henry Hub Gas PricesLong Term ForecastLong Term Forecast

0

1

2

3

4

56

7

8

9

10

1990

1995

2000

2005

2010

2015

Dol

lars

per

MM

Btu

History Forecast Coal Dlvd. LNG Breakeven 1%S Resid

Related Documents