Nicola Miglietta and Enrico Battisti 1 ISLAMIC AND TRADITIONAL CORPORATE FINANCE: A COMPARATIVE STUDY ON WACC Miglietta Nicola, University of Turin, Italy, [email protected] Battisti Enrico, University of Turin, Italy, [email protected] Turin, 9 th September 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Nicola Miglietta and Enrico Battisti 1

ISLAMIC AND TRADITIONAL

CORPORATE FINANCE:

A COMPARATIVE STUDY ON WACC

Miglietta Nicola, University of Turin, Italy, [email protected]

Battisti Enrico, University of Turin, Italy, [email protected]

Turin, 9th September 2016

Nicola Miglietta and Enrico Battisti 2

Summary

1. Capital structure

2. Purpose of the study

3. Introduction to Islamic Finance

4. Theoretical Background

5. Methodology

6. Discussion

7. Conclusions

Nicola Miglietta and Enrico Battisti 3

1. Capital structure

Nicola Miglietta and Enrico Battisti 4

1) What is the financial goal of a firm?

2) What is the capital structure of a firm?

Is the choice of leverage and ratio beetwen risk capital and debt

Maximize the value of the firm

1. Capital structure

Financing choices has to reflect the risk profile of a firm and the characteristics of projects

Nicola Miglietta and Enrico Battisti 5

MAXIMIZE THE VALUE OF THE FIRM

VALUE OF THE FIRM

EQUITY

DEBT

V

E

D

V = E + D CAPITAL STRUCTURE

1. Capital structure

Nicola Miglietta and Enrico Battisti 6

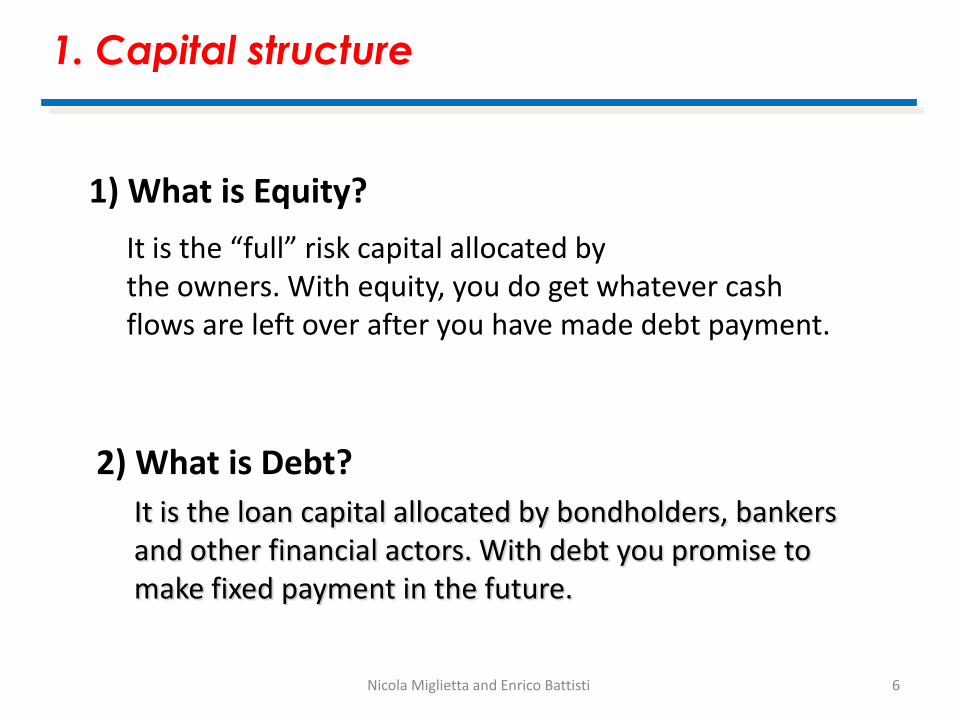

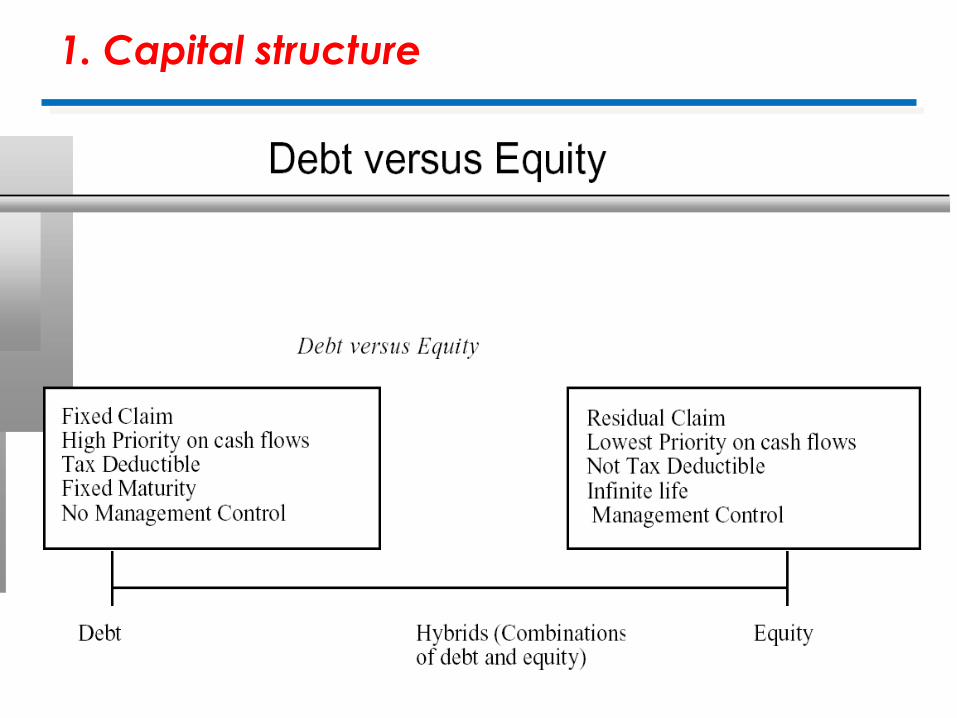

1) What is Equity?

2) What is Debt?

It is the loan capital allocated by bondholders, bankers and other financial actors. With debt you promise to make fixed payment in the future.

It is the “full” risk capital allocated by the owners. With equity, you do get whatever cash flows are left over after you have made debt payment.

1. Capital structure

Nicola Miglietta and Enrico Battisti 7

1. Capital structure

Nicola Miglietta and Enrico Battisti 8

Is there a relation between capital structure and value?

Modigliani and Miller in their famous First proposition say…

… The value of a firm is independent from its capital structure

?????

1. Capital structure

Nicola Miglietta and Enrico Battisti 9

Modigliani & Miller Hypothesis:

1. No taxes

2. Efficient market theory

3. No expected bankruptcy costs

4. No agency costs

There is not a relation between the capital structure and the value of a firm.

1. Capital structure

Nicola Miglietta and Enrico Battisti 10

1. No taxes: mean no taxation. But is it realistic???

2. Efficient Market theory: means that the market function well. All the operator have the same access to information.

3. No expected bankruptcy cost: as you borrow more, you

increase the probability of bankruptcy and hence the expected BC.

4. No agency cost: an agency cost arises whenever you hire

someone else to do something for you. It arise because the interest of principal may deviate from those of the person you hired.

1. Capital structure

Nicola Miglietta and Enrico Battisti 11

FINANCIAL POLICY

Is Our Capital Structure the optimal mix of financing? Is our financial policy correct? It could be different?

1. Capital structure

Nicola Miglietta and Enrico Battisti 12

ASSETS LIABILITIES

Net fixed assets

Inventory

Credits

Cash

Shareholders’ founds

Long Term Liabilities

Current Liabilities

NET

ASSETS

E

QU

ITY

D

EBT

1. Capital structure

Nicola Miglietta and Enrico Battisti 13

WACC (Weighted Average Cost of Capital) is the traditional view of capital structure, risk and return.

It will depend upon:

- the components of financing;

- the cost of each components.

1. Capital structure

THE COST OF CAPITAL APPROACH

Nicola Miglietta and Enrico Battisti 14

WACC = ke*[E/(D+E)] + kd*[D/(D+E)]

Where: - ke = cost of equity - kd = cost of debt - E/(D+E) = Equity to capital ratio - D/(D+E) = Debt to capital ratio

1. Capital structure

WACC is the cost of each component weighted by its relative market value; it is the average rate of return that a firm expects to compensate all its different investors.

Nicola Miglietta and Enrico Battisti 15

ke = Rf + levered [ Rm - Rf ]

1. Capital structure

Where: - Rf = risk free rate - levered = measure of market risk - Rm = market yield - Rm – Rf = expected additional return for making a risky investment rather than a safe one

The cost of equity is the required rate of return given the risk, inclusive of both dividend yield and price appreciation.

Nicola Miglietta and Enrico Battisti 16

kd = i x ( 1 - t )

1. Capital structure

Where: - i = interest rate - t = tax shield

The cost of debt is the market interest rate that has to pay on its borrowing. It will depend on three components: the general level of interest rate, the default premium and the tax rate.

Nicola Miglietta and Enrico Battisti 17

Consider the following numbers…

A) 10%

B) 5%

C) 8,5%

Without knowing other information….

What is the cost of equity? And cost of debt? Finally, the WACC?

1. Capital structure

Nicola Miglietta and Enrico Battisti 18

Following the WACC method the optimal capital

structure is the mix of debt and equity that

maximize firm’s value having, at the same time,

the minimum WACC…..

…. minimum WACC means higher firm value

1. Capital structure

Nicola Miglietta and Enrico Battisti 19

1. Capital structure

Nicola Miglietta and Enrico Battisti 20

2. Purpose of the study

• This study is based on the comparison between the Weighted Average Cost of Capital of a sample of companies listed on Malaysian Stock Exchange, classified and shared according to the principles of Islamic finance.

• The purpose is to provide some preliminary evidences of the potential effect on the risk (measured by Beta) as result of the principles used to divide the companies between Shari’ah Compliant (LCSC) and not Shari’ah Compliant (LCnotSC).

20

Nicola Miglietta and Enrico Battisti 21

3. Introduction to Islamic finance

First ….

the traditional principles of Corporate Finance postulate that each firm carries out some choices related to (Damodaran, 2015):

– where to get the funds;

– how to invest it;

– when to return the excess cash;

The same choices can be referred to an Islamic firm.

21

Nicola Miglietta and Enrico Battisti 22

3. Introduction to Islamic finance

Second….

the financial goal of the firm is to maximize the Shareholder Value.

This goal is widely accepted in both theory and practice (e.g. Copeland, Weston & Shastri, 2004; Van Horne and Wachovicz, 2008; Vernimmen et al., 2014; Brealey et al., 2014) and can be applied also to Islamic firms (e.g. Aggarwal & Yousef, 2000; Habib, 2007; Nagano, 2010; Salvi & Miglietta, 2013).

22

Nicola Miglietta and Enrico Battisti 23

What is really different? And why?

The principles that a Shari’ah Compliant company must follow with reference to its capital structure diverge from a traditional firm.

Islamic finance is a financial institution and product designed to comply with the central principles of Shari’ah.

What are the main principles of Islamic finance?

23

3. Introduction to Islamic finance

Nicola Miglietta and Enrico Battisti 24

The main principles of Islamic finance are (Gait & Worthington, 2007): - the prohibition of Riba (generally translated as usury or interest) and the exclusion of debt-based financing from the economy; - the prohibition of Gharar (generally translated as risk, uncertainty or hazard) encompassing the full disclosure of information and elimination of any asymmetrical information in a contract; - the prohibition of Maysir (generally translated as gambling or other games of chance) encompassing the exclusion of financing and dealing in sinful and socially irresponsible activities and commodities such as gambling, drugs and pork or the production of alcohol and other games of chance (i.e. casino-type games, lotteries);

3. Introduction to Islamic finance

Nicola Miglietta and Enrico Battisti 25

Islamic finance rejects that it can be realized a gain without taking a risk. This means that the funding to the business entity is prohibited? No, the funding to the business entity is permitted but the return, be tied exclusively to the results linked to the use of capital. This is the base of the Profit and Loss Sharing (PLS) that is a form of partnership where partners share profits and losses based on their capital share and work. Profit and Loss Sharing, in addition to legal-religious principles, could play a significant role on the system of capital structure puzzle and, consequently, on the WACC.

3. Introduction to Islamic finance

Nicola Miglietta and Enrico Battisti 26

4. Theoretical Background

According to the traditional corporate finance, the Weighted Average

Cost of Capital and the theories (“trade-off theory”, “pecking order

theory” and “agency theory”) on the capital structure have determined

the principles that underpin the system of the financial decisions for

the:

- Traditional firm (e.g. Fama & French, 1999; Damodaran, 2011; Dallocchio &

Salvi, 2011; Tardivo, Schiesari & Miglietta 2012; Brealey et al., 2014)

- Islamic firm (e.g. Habib, 2007; Mohamad & Saad, 2012; Shafizal & Mansur,

2013).

According to the Traditional corporate finance, the company’s cost of

capital is usually estimated as a WACC.

26

Nicola Miglietta and Enrico Battisti 27

4. Theoretical Background

• The cost of capital for Islamic Corporate finance based on mark-up tends to assume a structure similar to the Traditional Corporate finance.

• The process of formation of the cost of debt in Islamic finance provides a mechanism based on a benchmark derived from the traditional finance and equivalent to the “base cost” the same source on which, through the application of the Mark-up, it forms a “cost complement”. Although in the process of estimating the cost of equity in Islamic finance can be associated a “hurdle yield of return” that the lender is expected from the investment.

27

Nicola Miglietta and Enrico Battisti 28

5. Methodology

• Research strategy: to provide some preliminary evidences of

the potential effect on the risk as result of the principles used

to divide the companies between Shari’ah Compliant and not

Shari’ah Compliant.

28

Nicola Miglietta and Enrico Battisti 29

5. Methodology

• Data collection: three research phases 1. We have identified an important stock markets that contained Shari’ha

Compliant e not Shari’ah Compliant firms: Bursa Malaysian;

2. The companies on Bursa Malaysia listed under the Main Market are 814.

We have recognized 598 listed companies Shari’ah Compliant (LCSC) and

216 listed companies not Shari’ah Compliant (LCnotSC).

3. We have defined some items relevant to the purpose of our comparative

analysis on WACC. We have considered the three following selection

criteria of the listed companies: • Company profile: Macro sector.

• Key Statistics: Beta levered.

• Financial Health: Debt/equity ratio.

29

Nicola Miglietta and Enrico Battisti 30

5. Methodology

In this phase, we have evaluated as “not relevant”, and consequently

excluded from the final dataset, the listed companies that do not have at

least two of the three parameters mentioned above or some listed

companies in which it was not possible to identify a single sector.

779 listed companies were our eligible target:

569 LCSC and 210 LCnotSC.

30

Nicola Miglietta and Enrico Battisti 31

5. Methodology

• Data analysis: we have divided the listed companies for macro sectors:

– 8 for the listed companies Shari’ah Compliant;

– 9 for the listed companies not Shari’ah Compliant.

31

Nicola Miglietta and Enrico Battisti 32 32

Figure: Sectors for listed

companies Shari’ah Compliant

Figure: Sectors for listed

companies not Shari’ah Compliant

Nicola Miglietta and Enrico Battisti 33

5. Methodology

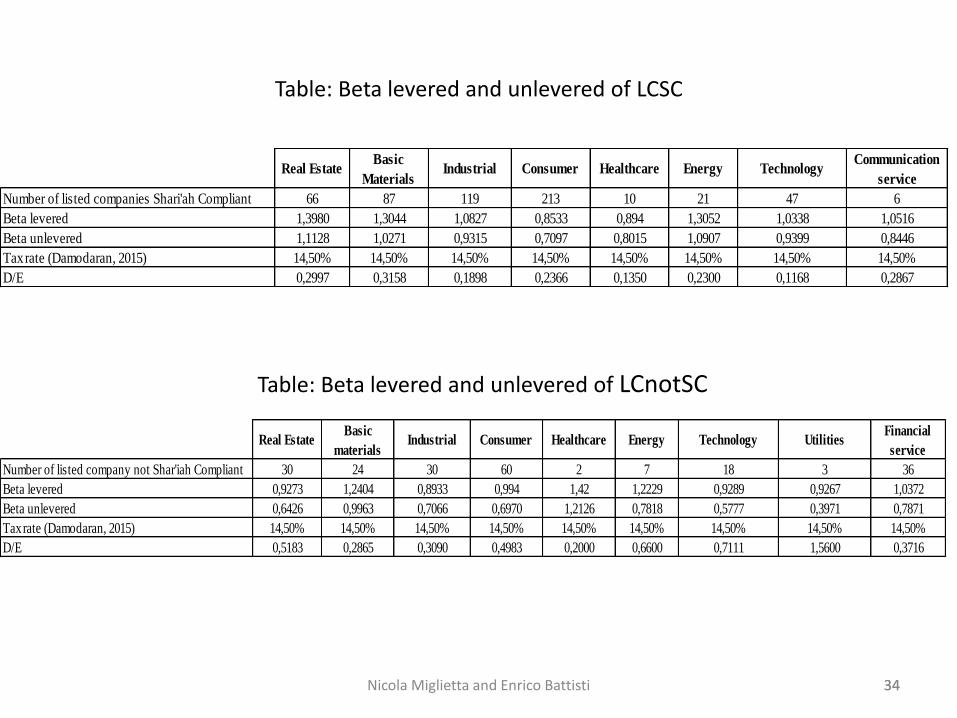

In this phase we have decided to analyse for each listed companies the following elements needed to calculate the average WACC of the sector:

- Beta levered;

- Debt/equity ratio.

Starting from these two elements, considered a Malaysian tax rate of 14,50% (Damodaran, 2015), we have calculated for each sector the

a) beta levered Betalevered = Betaunlevered * [1 + (1 – t) * D/E]

b) unlevered beta Betaunlevered = Betalevered / [1 + (1 – t) * D/E]

33

Nicola Miglietta and Enrico Battisti 34 34

Table: Beta levered and unlevered of LCSC

Table: Beta levered and unlevered of LCnotSC

Real EstateBasic

MaterialsIndustrial Consumer Healthcare Energy Technology

Communication

service

Number of listed companies Shari'ah Compliant 66 87 119 213 10 21 47 6

Beta levered 1,3980 1,3044 1,0827 0,8533 0,894 1,3052 1,0338 1,0516

Beta unlevered 1,1128 1,0271 0,9315 0,7097 0,8015 1,0907 0,9399 0,8446

Tax rate (Damodaran, 2015) 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50%

D/E 0,2997 0,3158 0,1898 0,2366 0,1350 0,2300 0,1168 0,2867

Real EstateBasic

materialsIndustrial Consumer Healthcare Energy Technology Utilities

Financial

service

Number of listed company not Shar'iah Compliant 30 24 30 60 2 7 18 3 36

Beta levered 0,9273 1,2404 0,8933 0,994 1,42 1,2229 0,9289 0,9267 1,0372

Beta unlevered 0,6426 0,9963 0,7066 0,6970 1,2126 0,7818 0,5777 0,3971 0,7871

Tax rate (Damodaran, 2015) 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50%

D/E 0,5183 0,2865 0,3090 0,4983 0,2000 0,6600 0,7111 1,5600 0,3716

Nicola Miglietta and Enrico Battisti 35 35

The results of comparative analysis on Beta levered and unlevered are the

following:

Table: A comparative analysis on Beta levered and unlevered

Listed companies Shari’ah compliant are generally more risky than those not Shari’ah Compliant.

LCSC LCnotSC LCSC LCnotSC

Real Estate 1,3980 0,9273 1,1128 0,6426 LCSC LCSC

Basic Materials 1,3044 1,2404 1,0271 0,9963 LCSC LCSC

Industrial 1,0827 0,8933 0,9315 0,7066 LCSC LCSC

Consumer 0,8533 0,9940 0,7097 0,6970 LCnotSC LCSC

Healthcare 0,8940 1,4200 0,8015 1,2126 LCnotSC LCnotSC

Energy 1,3052 1,2229 1,0907 0,7818 LCSC LCSC

Technology 1,0338 0,9289 0,9399 0,5777 LCSC LCSC

Higher beta

unlevered

Beta levered Beta unlevered Higher beta

levered

Nicola Miglietta and Enrico Battisti 36

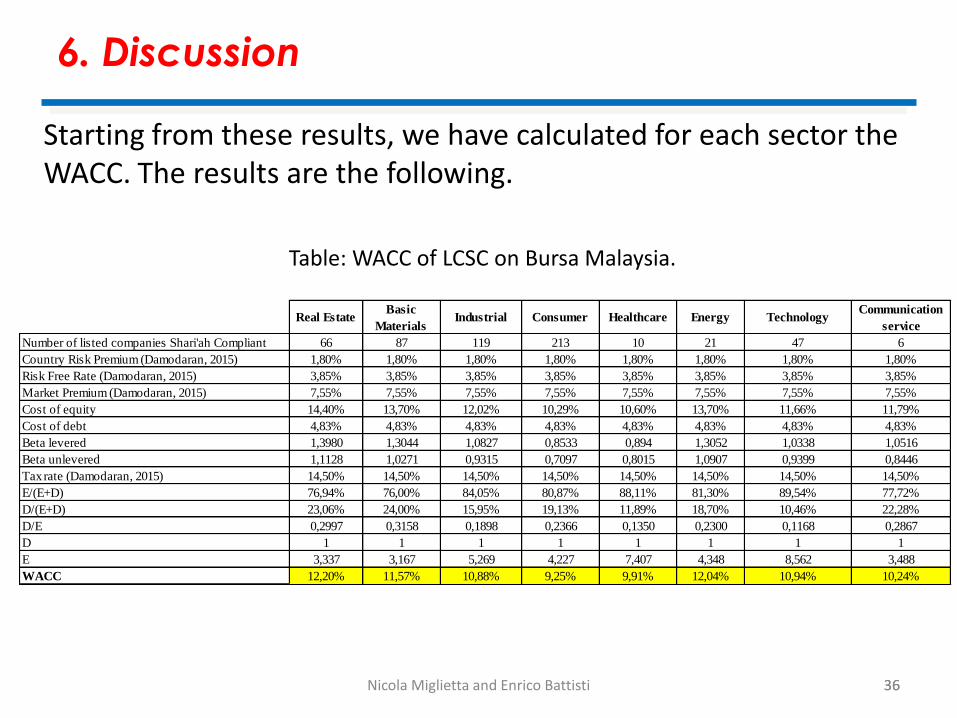

6. Discussion

Starting from these results, we have calculated for each sector the WACC. The results are the following.

Table: WACC of LCSC on Bursa Malaysia.

36

Real EstateBasic

MaterialsIndustrial Consumer Healthcare Energy Technology

Communication

service

Number of listed companies Shari'ah Compliant 66 87 119 213 10 21 47 6

Country Risk Premium (Damodaran, 2015) 1,80% 1,80% 1,80% 1,80% 1,80% 1,80% 1,80% 1,80%

Risk Free Rate (Damodaran, 2015) 3,85% 3,85% 3,85% 3,85% 3,85% 3,85% 3,85% 3,85%

Market Premium (Damodaran, 2015) 7,55% 7,55% 7,55% 7,55% 7,55% 7,55% 7,55% 7,55%

Cost of equity 14,40% 13,70% 12,02% 10,29% 10,60% 13,70% 11,66% 11,79%

Cost of debt 4,83% 4,83% 4,83% 4,83% 4,83% 4,83% 4,83% 4,83%

Beta levered 1,3980 1,3044 1,0827 0,8533 0,894 1,3052 1,0338 1,0516

Beta unlevered 1,1128 1,0271 0,9315 0,7097 0,8015 1,0907 0,9399 0,8446

Tax rate (Damodaran, 2015) 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50%

E/(E+D) 76,94% 76,00% 84,05% 80,87% 88,11% 81,30% 89,54% 77,72%

D/(E+D) 23,06% 24,00% 15,95% 19,13% 11,89% 18,70% 10,46% 22,28%

D/E 0,2997 0,3158 0,1898 0,2366 0,1350 0,2300 0,1168 0,2867

D 1 1 1 1 1 1 1 1

E 3,337 3,167 5,269 4,227 7,407 4,348 8,562 3,488

WACC 12,20% 11,57% 10,88% 9,25% 9,91% 12,04% 10,94% 10,24%

Nicola Miglietta and Enrico Battisti 37 37

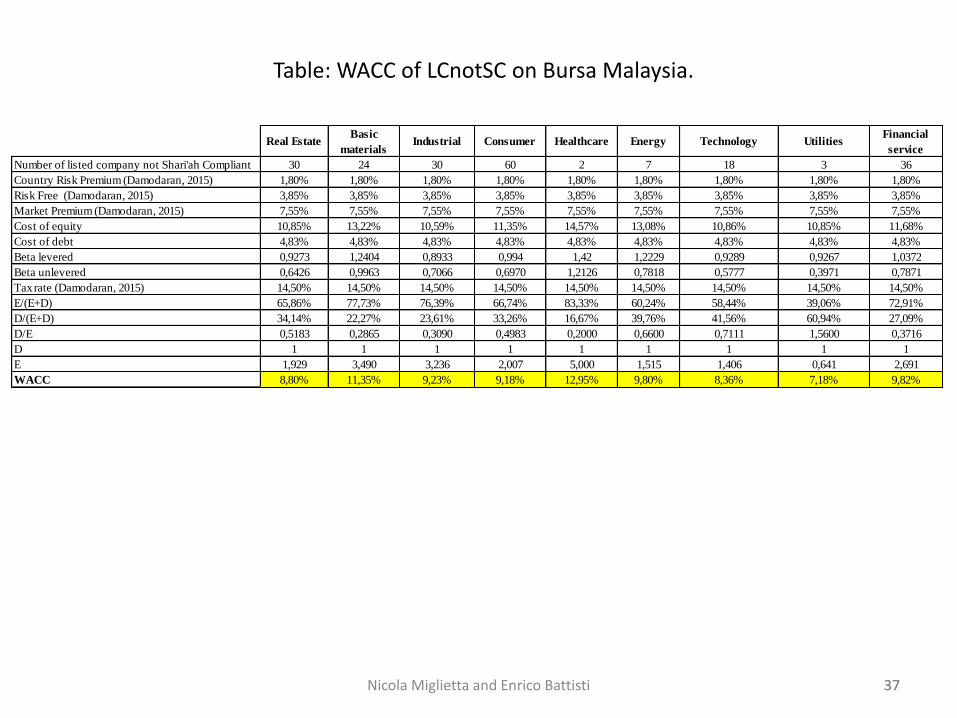

Table: WACC of LCnotSC on Bursa Malaysia.

Real EstateBasic

materialsIndustrial Consumer Healthcare Energy Technology Utilities

Financial

service

Number of listed company not Shari'ah Compliant 30 24 30 60 2 7 18 3 36

Country Risk Premium (Damodaran, 2015) 1,80% 1,80% 1,80% 1,80% 1,80% 1,80% 1,80% 1,80% 1,80%

Risk Free (Damodaran, 2015) 3,85% 3,85% 3,85% 3,85% 3,85% 3,85% 3,85% 3,85% 3,85%

Market Premium (Damodaran, 2015) 7,55% 7,55% 7,55% 7,55% 7,55% 7,55% 7,55% 7,55% 7,55%

Cost of equity 10,85% 13,22% 10,59% 11,35% 14,57% 13,08% 10,86% 10,85% 11,68%

Cost of debt 4,83% 4,83% 4,83% 4,83% 4,83% 4,83% 4,83% 4,83% 4,83%

Beta levered 0,9273 1,2404 0,8933 0,994 1,42 1,2229 0,9289 0,9267 1,0372

Beta unlevered 0,6426 0,9963 0,7066 0,6970 1,2126 0,7818 0,5777 0,3971 0,7871

Tax rate (Damodaran, 2015) 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50% 14,50%

E/(E+D) 65,86% 77,73% 76,39% 66,74% 83,33% 60,24% 58,44% 39,06% 72,91%

D/(E+D) 34,14% 22,27% 23,61% 33,26% 16,67% 39,76% 41,56% 60,94% 27,09%

D/E 0,5183 0,2865 0,3090 0,4983 0,2000 0,6600 0,7111 1,5600 0,3716

D 1 1 1 1 1 1 1 1 1

E 1,929 3,490 3,236 2,007 5,000 1,515 1,406 0,641 2,691

WACC 8,80% 11,35% 9,23% 9,18% 12,95% 9,80% 8,36% 7,18% 9,82%

Nicola Miglietta and Enrico Battisti 38

7. Conclusions

38

The results of comparative analysis on WACC are the following: Table: A comparative analysis on WACC

We can assert that, for the sample analysed, LCSC collected using the application of the principles of Islamic finance, shows an higher level or risk, measured by Beta levered, and higher value of the WACC.

LCSC LCnotSC

Real Estate 12,20% 8,80% LCSC

Basic Materials 11,57% 11,35% LCSC

Industrial 10,88% 9,23% LCSC

Consumer 9,25% 9,18% LCSC

Healthcare 9,91% 12,95% LCnotSC

Energy 12,04% 9,80% LCSC

Technology 10,94% 8,36% LCSC

WACC Higher

WACC

Nicola Miglietta and Enrico Battisti 39

Thank you very much

for your attention

39

Related Documents