Islamic Accounting - An Overview

Aug 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Have you heard about..

Tahwid Khalifa

AdalahIkhtisab

Shari'ah

Introducing: Islamic Accounting

• an alternative accounting system,

• It aims to provide users with information enabling them to operate businesses and organizations according to Shari'ah, or Islamic law.

Key Factors of Islamic Accounting

Interest-free Loans Zakat

Conventional accounting, considered insufficient to accommodate these unique characteristics of Islamic Financial Institutions [IFIs].

Why do I need to know this?

The Emergence of Islamic Financial Institutions

• The Islamic funds in global financial institutions is estimated to be at US$1.3 trillion.

• The Islamic financial market is estimated to be worth US$400 billion in size, with annual growth rate of 12-15%.

• There are over 300 Islamic financial institutions currently operating in about 75 countries.

Some Important Islamic Organisations

Takaful Companies

Awqaf

Insurance Company

Charitable Trust

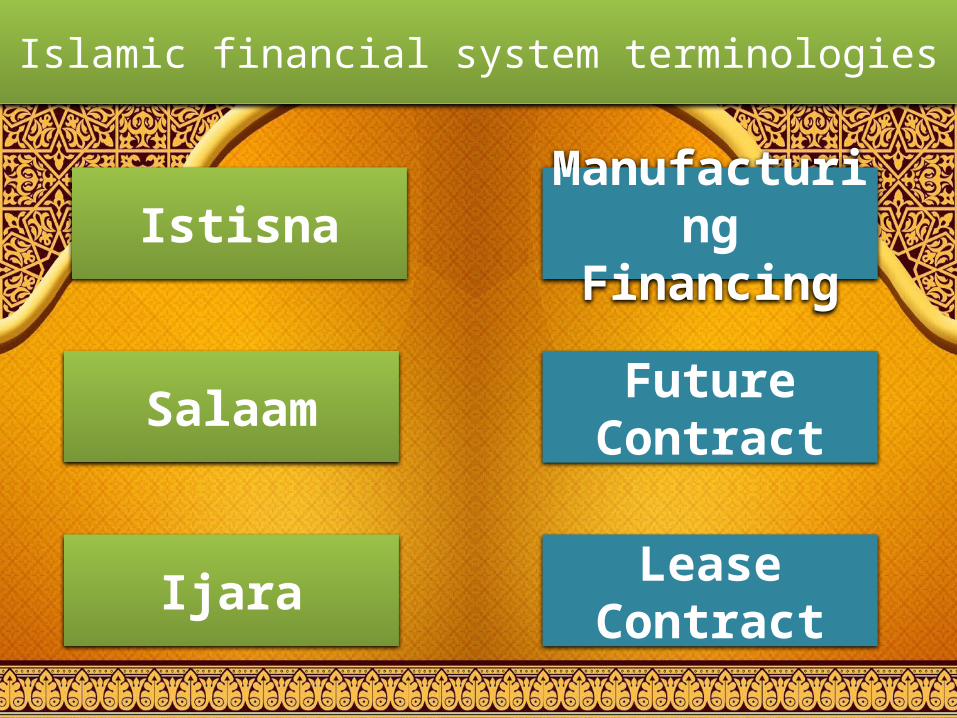

Ijara

Salaam Future Contract

Lease Contract

Istisna Manufacturing Financing

Islamic financial system terminologies

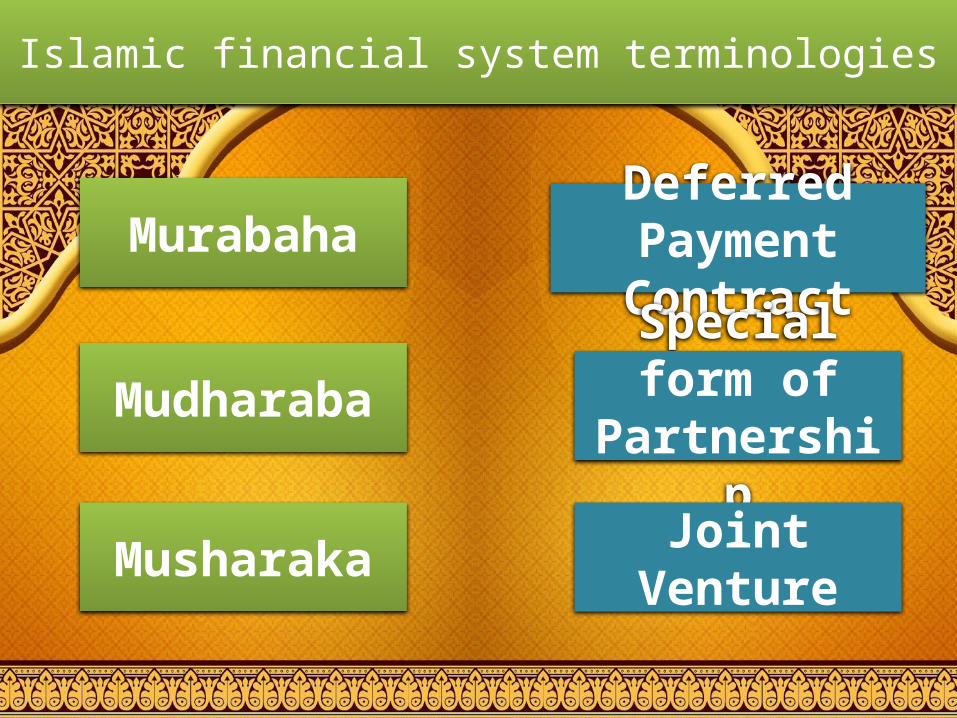

Murabaha

Mudharaba

Musharaka

Deferred Payment Contract

Special form of Partnership

Joint Venture

Islamic financial system terminologies

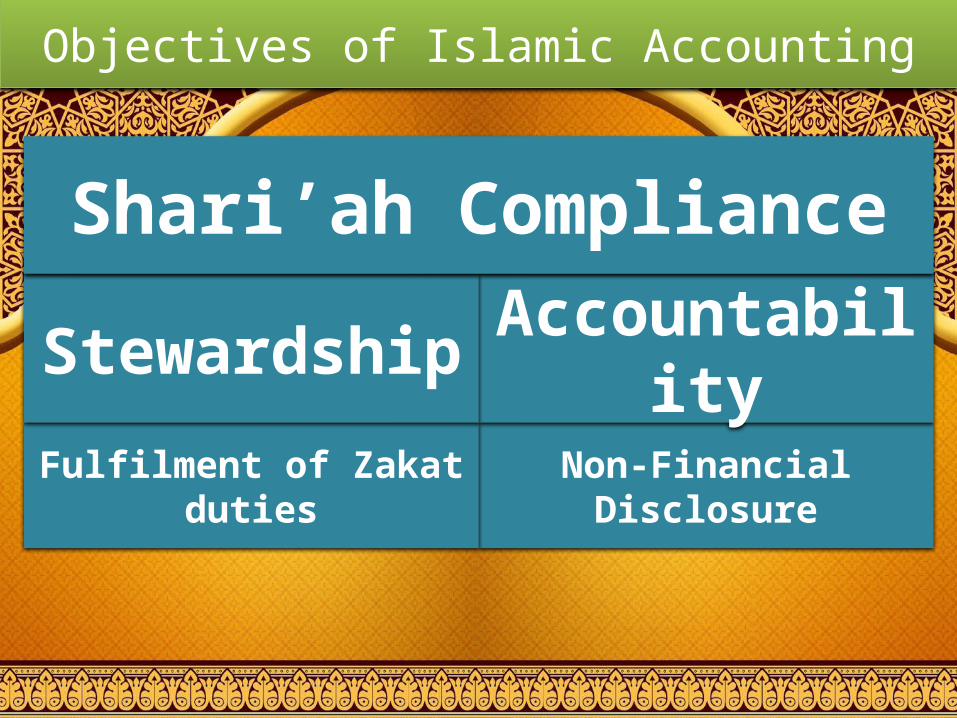

Objectives of Islamic Accounting

Non-Financial DisclosureFulfilment of Zakat duties

AccountabilityStewardship

Shari’ah Compliance

Accounting and Auditing Organization for Islamic Financial Institutions

• Established to maintain and promote Shari'ah standards for Islamic financial institutions.

• Issued o 25 accounting standards, o 7 auditing standards,o 6 governance standards, o 41 Shari'ah standards,o 2 codes of ethics.

USERS OF ISLAMIC ACCOUNTING INFORMATION

• Zakat payers and the Government authority in charge of Zakat assessment and monitoring.

Zakat Beneficiaries

• Local community and employees and employees have an important stake in the organisation as in Western society.

Local Community and Employees

• Good and services must be halal (permitted) under the Shari’ahConsumers

Bibliography

• Dr. Shahul Hameed bin Mohamed IbrahimPhD Dissertation (UK: University of Dundee, 2000)

http://www.iium.edu.my/iaw/phdcontents.htm

• Islamic banking and finance

https://en.wikipedia.org/wiki/Islamic_banking_and_finance

• Perceptions of Muslim Accounting Academicians By : Rizal Yaya

http://www.iium.edu.my/iaw/Articles/Objectives%20and%20Characteristics%20of%20Islamic%20Accounting.htm

• Islamic Accounting: Challenges, Opportunities and Terror

http://www.accountingweb.com/aa/auditing/islamic-accounting-challenges-opportunities-and-terror

• Islamic Accounting Systems and Practices By Dr. Syed Mohammad Ather FCMA and Md. Hafij Ullah

http://www.academia.edu/7624898/Islamic_Accounting_Systems_and_Practices

• AAOIFI

http://www.aaoifi.com/

THANK YOU

Shari’ah

• Shari'ah, is the Islamic legal system derived from the religious precepts of Islam, particularly the Quran and the Hadith.

• The term Shari'ah comes from the Arabic language, which means a body of moral and religious law.

Tawhid (Unity and Oneness of God)

The concept of Tawhid implies

• there is only One God who is the creator and sovereign of all,

• Islam requires total submission to Him in all aspects of life.

Economics – therefore is part of religion.

Khalifa (Vicegerancy)

The concept of Khalifa implies

• Man is the agent of God,• implies trust and responsibility, authority and

duty, election and service,• This puts some restriction on the use of economic

resources. PROPERTY – belongs to God, accessible to everyone.

Ikhtisab(Accountability)

The concept of Ikhtisab implies

• every act in this world will have to be accounted for to Allah

• associated with this concept is the belief in rewards and punishments.

Man is answerable to God for his wealth - how he acquired and spent it.

Adalah (Justice)

The concept of Adalah implies• the objective of individual and social welfare and

public benefit as the objective of an Islamic state.

• distributive equity is sought in an Islamic economic framework

Transactions need to be SOCIALY JUSTIFIED

The Problem of Riba

• ‘Riba has been translated into English as usury or interest.

• The Qur’an specifically prohibits Riba.

• To charge interest from someone who is constrained to borrow to meet his essential requirements is considered an exploitative practice in Islam.

• Riba is also said to lead to the concentration of wealth by transferring wealth from the poor to the rich.

WHY?

INTEREST = EXPLOITATION

Zakat Collection and Distribution

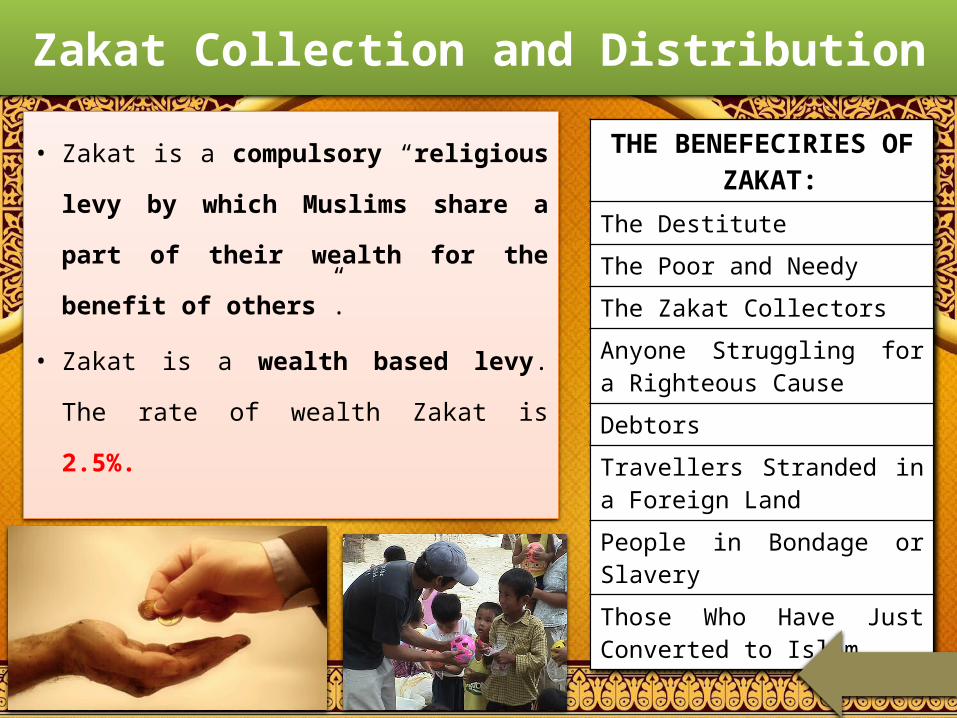

• Zakat is a compulsory “religious levy

by which Muslims share a part of

their wealth for the benefit of

others”.

• Zakat is a wealth based levy. The

rate of wealth Zakat is 2.5%.

THE BENEFECIRIES OF ZAKAT:

The Destitute

The Poor and Needy

The Zakat Collectors

Anyone Struggling for a Righteous Cause

Debtors

Travellers Stranded in a Foreign Land

People in Bondage or Slavery

Those Who Have Just Converted to Islam

Awqaf

• It is the setting aside of certain assets usually land, buildings etc. for the exclusive use for specific charitable/religious purposes under a legal deed.

• The asset cannot be sold, inherited or expropriated by the government.

Takaful Companies

• Conventional insurance is prohibited by Islamic Shari’ah due to the element uncertainty in contingent contracts as well the elements of gambling especially in relation to life insurance.

• In addition, the practice of investing premiums in interest-bearing securities is also prohibited.

• Takaful operates as a co-operative savings and mutual help scheme.

• Premiums paid by the policyholders are not recorded as income.

Murabaha and Bai al-Mu’ajjal

• Originated in the deferred sale (Bai al-Mu'ajjal) contract.

• In this contract, a buyer of goods requests an agent to buy the goods for him, on the understanding that the agent will charge a mark-up on the cost of the goods which will be sold to the buyer.

• The Islamic banks saw this as an opportunity in financing a purchase.

Mudharaba

• Mudharaba is a labour-capital partnership,

• The profit sharing ratio between the entrepreneur and the investor is pre-determined in advance,

• In case of losses, the investor bears the entire loss, the entrepreneur loses his labour as he is not paid a salary.

Musharaka

• This is plain partnership financing.

• In case the bank does not play an active part in the business, then the entrepreneur may charge management salary or expenses to the business account.

• the bank has full rights of administration in Musharaka contracts.

Ijara

• Ijara is rent or leasing of assets.

• Only operational leases are allowed in Islam, wherein the owner permits the user to use of an asset for a particular period which is shorter than the economic life of the asset without any transfer of ownership rights.

Salaam

• an advance purchase contract, where the goods of a particular quality and quantity which is not yet in existence can be the subject of a contract.

• This is an important means of financing agricultural or fishing activities.

Istisna

• Istisna is the payment for commissioned manufacture,

• Unlike salaam, payment is at delivery or according to manufacturing or construction progress. Thus, this instrument can be used to finance construction or manufacturing projects.

Stewardship

• not only means the custody and safekeeping of resources but also for their efficient and profitable use and for protecting them from the greatest extent possible from an unfavourable economic impact,

• Concept of stewardship arose from the Islamic concept of Khilafa (Vicegerancy) and Amanah (Trusteeship).

Accountability

• From an Islamic perspective, accountability is a basic ingrained concept in the Muslim community,

• it forms one of the core concepts of belief i.e. the belief in the hereafter, heaven and hell, accounting and punishment.

Shari’ah Compliance

• To enable the activities of the entity to be controlled to be in line with the Shari’ah.

• Here, not only is the immediate Shari’ah meaning of (halal) permitted activities and avoidance of prohibited (haram) activities meant, but also a broader more comprehensive view of the Shari’ah, including the protection of the environment.

Assessment and Distribution of Zakat

• Under conventional accounting, tax avoidance is a major activity for accountants. No consideration is given to the fact that less tax means less wealth distribution and less money for public benefit,

• Under the Islamic economic system, Zakat is a cornerstone of public fiscal policy of in Islamic State. Even in the absence of a truly Islamic government, many Muslim countries have departments to collect Zakat and distribute them.

Non-Financial Disclosure

• Islamic banks must account to their owners and other stakeholders as to the extent to which they have complied with the ethical dictates.

• Islamic bank would have to disclose:• The avoidance of prohibited transactions• The extent to which their activities have contributed to the economic and

social development of various poor sectors of society• The ethical treatment of employees and depositors and entrepreneurs.• The extent to which they have safeguarded the environment and

conserved energy. • The collections and disbursement of Zakat from the bank’s operations

Related Documents