Is the demand of the index- based livestock insurance and informal insurance network substitute or complement? Kazushi Takahashi (with Chris Barrett and Munenobu Ikegami)

Is the demand of the index-based livestock insurance and informal insurance network substitute or complement?

Aug 06, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Is the demand of the index-based livestock insurance and informal insurance network substitute or complement?

Kazushi Takahashi(with Chris Barrett and Munenobu Ikegami)

Motivation Index insurance attracts attention as the next financial

revolution. Several studies discuss that formal insurance may crowd

out informal insurance networks (de Janvry et al. 2013 ; Boucher and Delpierre, 2014;) Free-riding: well-connected individuals can free-ride on their

group-members' insurance payout, resulting in a socially suboptimal level of coverage

Moral hazard: a greater degree of formal insurance allows for excessive risk-taking, which informal networks should absorb, imposing a negative externality on network members- crowding-out of informal risk-sharing

Motivation Counterargument is also provided to explain that the

demand of the index insurance can be complementary to informal insurance networks (Berhane, et al., 2014: Chemin, 2014; Dercon et al., 2014; Mobarak and Rosenzweig, 2013;) . Basis risk and crowed-in: the difference between the losses

actually incurred and the losses insured= idiosyncratic risk of incomplete compensation pooled and managed within an informal risk-sharing group

Increased trust: social learning in groups from early adopters who have tested the system before, and thus alleviate fears of non-reimbursement

Motivation Empirical evidence on whether the index insurance

crowed-in or crowed-out informal risk-sharing networks when sold to individuals is scarce, and it is theoretically ambiguous.

Our paper aims to provide empirical evidence to this issue, by using the data collected in Borena, Ethiopia.

Data 17 Study sites in Borena-Southern Ethiopia (near to Kenya Boundary)

514 households from Round 3

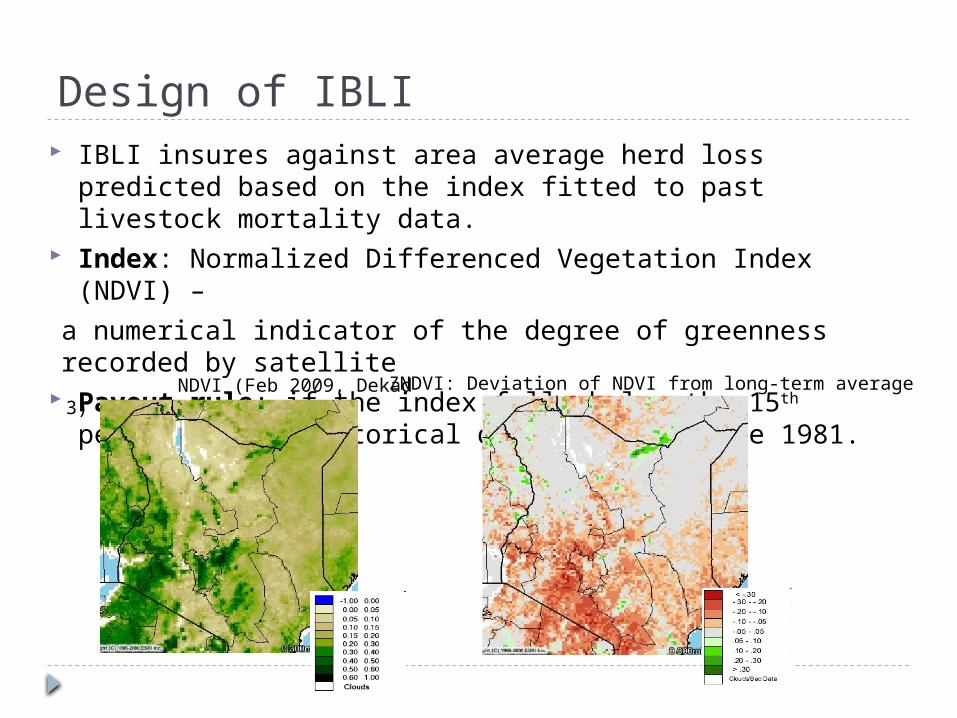

Design of IBLI IBLI insures against area average herd loss predicted based on the index

fitted to past livestock mortality data. Index: Normalized Differenced Vegetation Index (NDVI) – a numerical indicator of the degree of greenness recorded by satellite

Payout rule: if the index falls below the 15th percentile of historical distribution since 1981.

ZNDVI: Deviation of NDVI from long-term average NDVI (Feb 2009, Dekad 3)

Design of IBLI Insurance contract Timing of Purchase: before rainy seasons (two times in a year) Coverage: 1 year Timing of Payout: after dry seasons (two times in a year)

Design of IBLI

Premium payment:

(9.75% for Dilo, 8.71% for Teltele, 7.54% for Yabello, 9.49% for Dire, 8.58% for Arero, 9.36% for Dhas, and 11.05% for Miyo and Moyale, depending on differences in expected mortality risk)

Total insured herd value (TIHV):

Indemnity Payout: Max: 0.5*TIHV Min: Premium payment (depending on the severity of the drought)

Empirical strategy We want to explore the impact of informal insurance on the

uptake of IBLI or vice versa. Potential problems

Formation of informal networks/uptake of IBLI is clearly endogenous Measuring informal network is often problematic (Santos and Barrett,

2011; Maertens and Barrett, 2013) Census is costly, and infeasible Network within sampling method (either list up certain number or not)

artificially truncates the network, and resultant network data are non-representative

Open question tends to elicit only strong network link Remedy

Apply “random matching within a sample” method

Empirical strategy A household is randomly matched with 5 near neighbors and 3

non-near neighbors within a sample Two questions: (1) Do you know (the match)? (2) If yes, are you

willing to transfer cattle as a loan if the match asked for it. A dummy, representing a link, equal to 1 if the answer to (2) is

yes This is a hypothetical question, but hopefully, this may not be a

problem as informal asset transfers among Boran pastoralists are generally small. Also, there is evidence that the inferred determinants of insurance networks derived from this approach closely match those obtained from analysis of real insurance relations among the same population (Santos and Barrett, 2011).

Empirical strategy Basic model (via ivprobit)

LINK: 1 if there is the possibility of transferring cattle as a loan if the match asked for it between a household i and j,

Xi: characteristics of household i, Xj: characteristics of matched household j, Τ: characteristics to replect relationships between i and j : the predicted IBLI uptake of previous one year (instrumented with some

exogenous variables, such as the discount coupon recipient (assigned randomly: RCT) dummy)

>0 is complementary; <0 is supplement

Empirical strategy Some extension

Assuming that individual knows others’ purchase decision. Individuals strategically decide whether to purchase IBLI given

others’ decisions . Set of recursive equations via multivariate probit:

= =

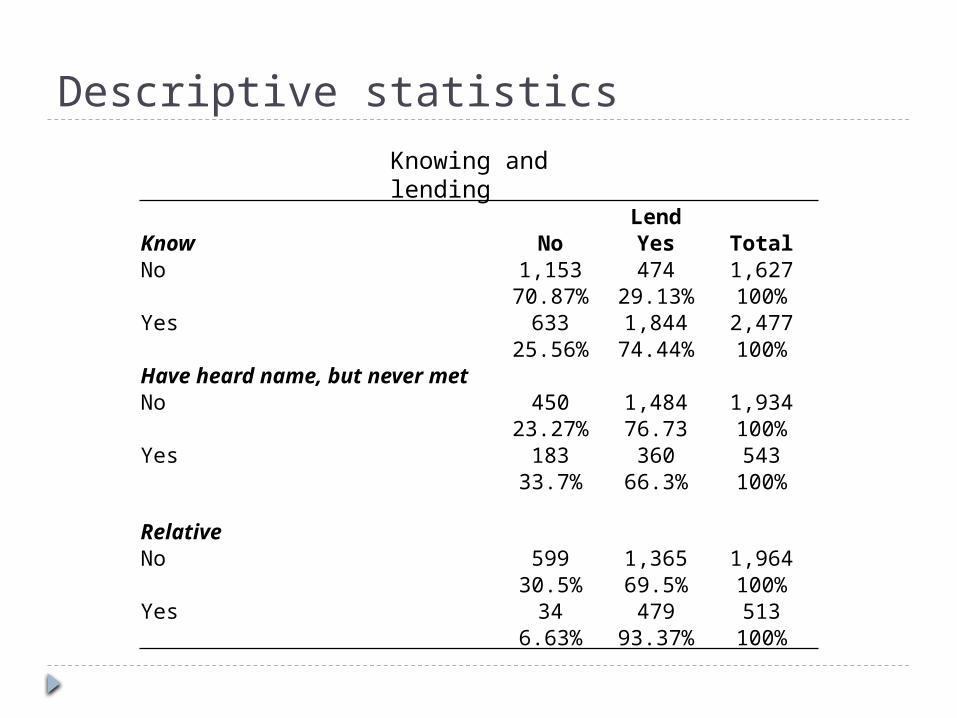

Descriptive statistics

Knowing and lending

LendKnow No Yes TotalNo 1,153 474 1,627

70.87% 29.13% 100%Yes 633 1,844 2,477

25.56% 74.44% 100%Have heard name, but never metNo 450 1,484 1,934

23.27% 76.73 100%Yes 183 360 543

33.7% 66.3% 100%

RelativeNo 599 1,365 1,964

30.5% 69.5% 100%Yes 34 479 513

6.63% 93.37% 100%

Preliminary results Basic model (IVprobit)

IBLI: =1 if purchase IBLI at either 3 or 4 sales periodControl: HHsize, Head male (=1), Head age and its squared, Head’s completed years of education, risk preference dummies, same clan (=1), study site fixed effect for both own and mathedIV: dummy to receive discount coupons at either 3 or 4 sales period

(1) (2)VARIABLES Link Link

far -0.968***

(0.045)

-0.057 -0.022(0.233) (0.243)

Preliminary results Extension (IV+multivariate probit)

(1) (2) (3) (4)

Link Link

far -0.971***

(0.081)

0.136 0.139

(0.284) (0.311)

0.248* -0.229*** 0.163 -0.240***

(0.138) (0.068) (0.143) (0.068)

*** p<0.01, ** p<0.05, * p<0.1

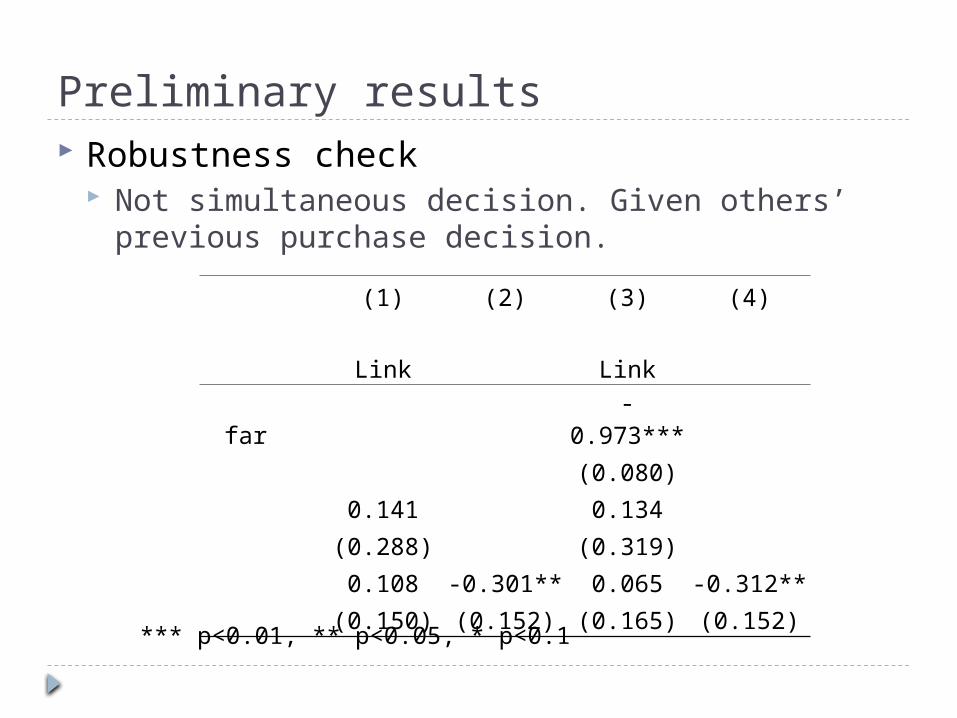

Preliminary results Robustness check

Not simultaneous decision. Given others’ previous purchase decision.

(1) (2) (3) (4)

Link Link

far -0.973***

(0.080)

0.141 0.134

(0.288) (0.319)

0.108 -0.301** 0.065 -0.312**

(0.150) (0.152) (0.165) (0.152)

*** p<0.01, ** p<0.05, * p<0.1

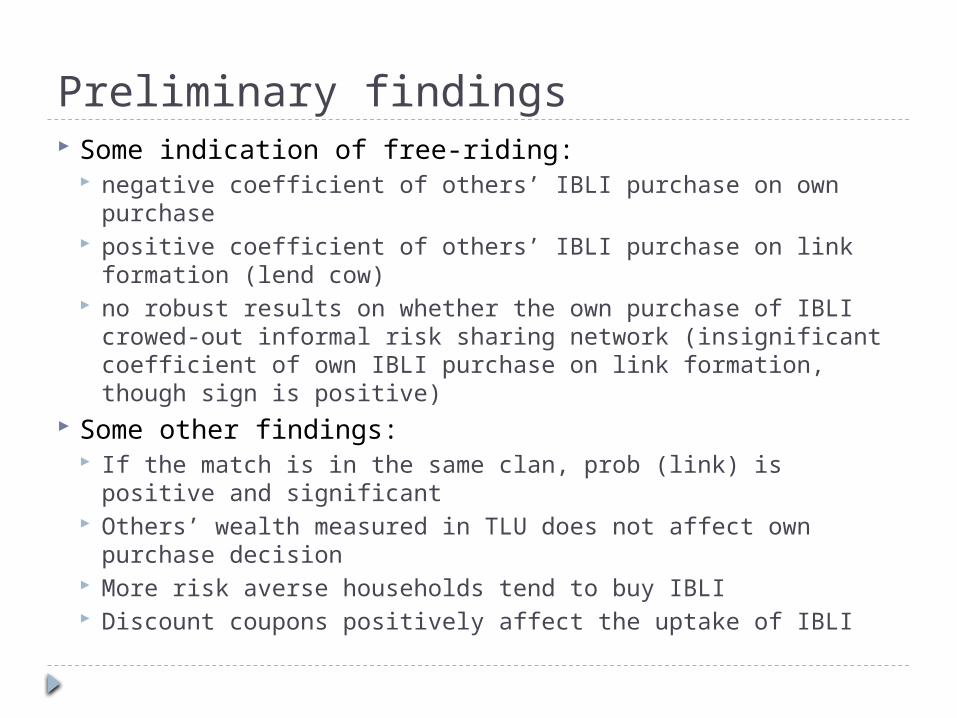

Preliminary findings Some indication of free-riding:

negative coefficient of others’ IBLI purchase on own purchase positive coefficient of others’ IBLI purchase on link formation (lend

cow) no robust results on whether the own purchase of IBLI crowed-out

informal risk sharing network (insignificant coefficient of own IBLI purchase on link formation, though sign is positive)

Some other findings: If the match is in the same clan, prob (link) is positive and significant Others’ wealth measured in TLU does not affect own purchase

decision More risk averse households tend to buy IBLI Discount coupons positively affect the uptake of IBLI

Future work It seems important to investigate whether the free-riding is

driven by the fact that the subject knows very well about the economic conditions of the matches.

Cai et al. (2015) show positive network effects are driven by the diffusion of insurance knowledge rather than purchase decision.

Vasilaky et al. (2014) show groups in which individuals knew of one another's assets were less likely to purchase their insurance within a group (in line with Boucher and Delpierre, 2014)

We will add two questions in R4: (1) do you think the match bought IBLI six month ago? (2) how many cows do you think the match herds?

Related Documents