Presenting a live 110‐minute teleconference with interactive Q&A IRC Sect. 704(b): Allocations to Partners Navigating Complex Rules on Determining Validity of Partnership Allocations 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific WEDNESDAY, MARCH 2, 2011 Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Amanda Wilson Lowndes Drosdick Doster Kantor & Reed Orlando Fla Amanda Wilson, Lowndes Drosdick Doster Kantor & Reed, Orlando, Fla. Jeremy Naylor, Partner, White & Case, New York Jorge Otoya, Senior Manager, KPMG, Washington, D.C. For this program, attendees must listen to the audio over the telephone. Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at1-800-926-7926 ext. 10.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presenting a live 110‐minute teleconference with interactive Q&A

IRC Sect. 704(b): Allocations to Partners Navigating Complex Rules on Determining Validity of Partnership Allocations

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, MARCH 2, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Amanda Wilson Lowndes Drosdick Doster Kantor & Reed Orlando FlaAmanda Wilson, Lowndes Drosdick Doster Kantor & Reed, Orlando, Fla.

Jeremy Naylor, Partner, White & Case, New York

Jorge Otoya, Senior Manager, KPMG, Washington, D.C.

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-871-8924 and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

IRC S t (b) All ti t P t IRC Sect. 704(b): Allocations to Partners Webinar

March 2, 2011

Jeremy Naylor, White & [email protected]

Amanda Wilson, Lowndes Drosdick Doster

Kantor & Reedd il @l d [email protected]

Jorge Otoya, KPMG [email protected] y p g

Today’s Program

Material Aspects Of 704(b) Rules[Amanda Wilson and Jeremy Naylor]

Slide 7 – Slide 35

Associated Regulatory Sections[Jeremy Naylor and Jorge Otoya]

Slide 36 – Slide 69

Relevant And Recent IRS Administrative Guidance[Jorge Otoya]

Slide 70 – Slide 72

A d Wil L d D di k D K & R d

MATERIAL ASPECTS OF 704(b)

Amanda Wilson, Lowndes Drosdick Doster Kantor & ReedJeremy Naylor, White & Case

MATERIAL ASPECTS OF 704(b) RULES

Orlando, Florida | www.lowndes-law.com

Allocations

One of the key benefits of a partnership is the flexibility in allocatingpartnership items among the partners.

Allocations of a partner’s distributive share of partnership income, gain,loss, deductions or credit will be respected if they:

(1) Are either in accordance with the partners’ interests in the(1) Are either in accordance with the partners interests in thepartnership, or

(2) Have substantial economic effect.

Allocations are not the same as distributions.

IRC Sect. 704(b): Allocations to Partners Webinar 8

Orlando, Florida | www.lowndes-law.com

Partners’ Interest In The Partnershipp

Allocations are generally in accordance with the partners’ interests inthe partnership if all allocations are being made in accordance with therespective contributions of the partners.

For example, if A and B each contributed $100, allocations would be inaccordance with the partners’ interests in the partnership if allaccordance with the partners interests in the partnership if allpartnership items are shared 50-50.

Liquidating distributions can be made in accordance with the partners’respective interests in the partnership.

IRC Sect. 704(b): Allocations to Partners Webinar 9

Orlando, Florida | www.lowndes-law.com

Substantial Economic EffectAB is a partnership that owns 3 properties. All income allocated 50% toA, except 60% of income from property 1 is allocated to A. This is aspecial allocation.

Special allocations will be respected if they have substantial economiceffect. Substantial economic effect is a safe harbor.

Under a two-part analysis, allocations must :

(1) Have economic effect, and

(2) The economic effect must be substantial.

IRC Sect. 704(b): Allocations to Partners Webinar 10

Orlando, Florida | www.lowndes-law.com

Economic Effect

General principle: If there is an economic benefit or burden thatp pcorresponds to an allocation, then the partner to whom the allocationis made must receive the economic benefit or burden.

More simply if a partner gets the benefit of an allocation of $100 of taxMore simply, if a partner gets the benefit of an allocation of $100 of taxloss, the partner must suffer the $100 economic loss. If a partnersuffers the burden of $100 of tax gain, the partner must get the $100of cash This is accomplished by maintaining capital accounts andof cash. This is accomplished by maintaining capital accounts andliquidating in accordance with those accounts.

IRC Sect. 704(b): Allocations to Partners Webinar 11

Orlando, Florida | www.lowndes-law.com

Basic Test For Economic Effect

(1) Capital account requirement: The partnership must maintain itscapital accounts in accordance with the rules of Reg. §1.704-1(b)(2)(iv).1(b)(2)(iv).

(2) Liquidation requirement: Upon liquidation of the partnershipagreement, the liquidating distributions must be made in

d ith th iti b l f th t ’ it laccordance with the positive balances of the partner’s capitalaccount.

(3) Deficit make-up requirement: If a partner has a deficit in his(3) Deficit make up requirement: If a partner has a deficit in hiscapital account upon liquidation of the partnership, the partnermust have an unconditional obligation to restore the deficit.

IRC Sect. 704(b): Allocations to Partners Webinar 12

Orlando, Florida | www.lowndes-law.com

Capital Account Maintenance Rules

A partner’s capital account reflects the partner’s equity investment. It must be adjusted as follows:

• Increased by (1) FMV of contributions and (2) allocable share of partnership income

D d b (1) FMV f di t ib ti d (2) ll bl• Decreased by (1) FMV of distributions and (2) allocable share of partnership loss

For economic effect liquidating distributions to the partners mustFor economic effect, liquidating distributions to the partners must be made based on capital accounts adjusted according to these rules.

IRC Sect. 704(b): Allocations to Partners Webinar 13

Orlando, Florida | www.lowndes-law.com

Deficit Restoration Obligation

The deficit restoration obligation (DRO) may be provided for inthe partnership agreement or by state law.

A DRO may be imposed to the extent of any outstandingprincipal balance of a promissory note (if the partner is the

k ) th t i t ib t d t th t hi d th t fmaker) that is contributed to the partnership and the amount ofany unconditional obligation of the partner (whether imposed bythe partnership agreement of state law) to make subsequentcontributions to the partnership.

A partner can have a limited DRO.

IRC Sect. 704(b): Allocations to Partners Webinar 14

Orlando, Florida | www.lowndes-law.com

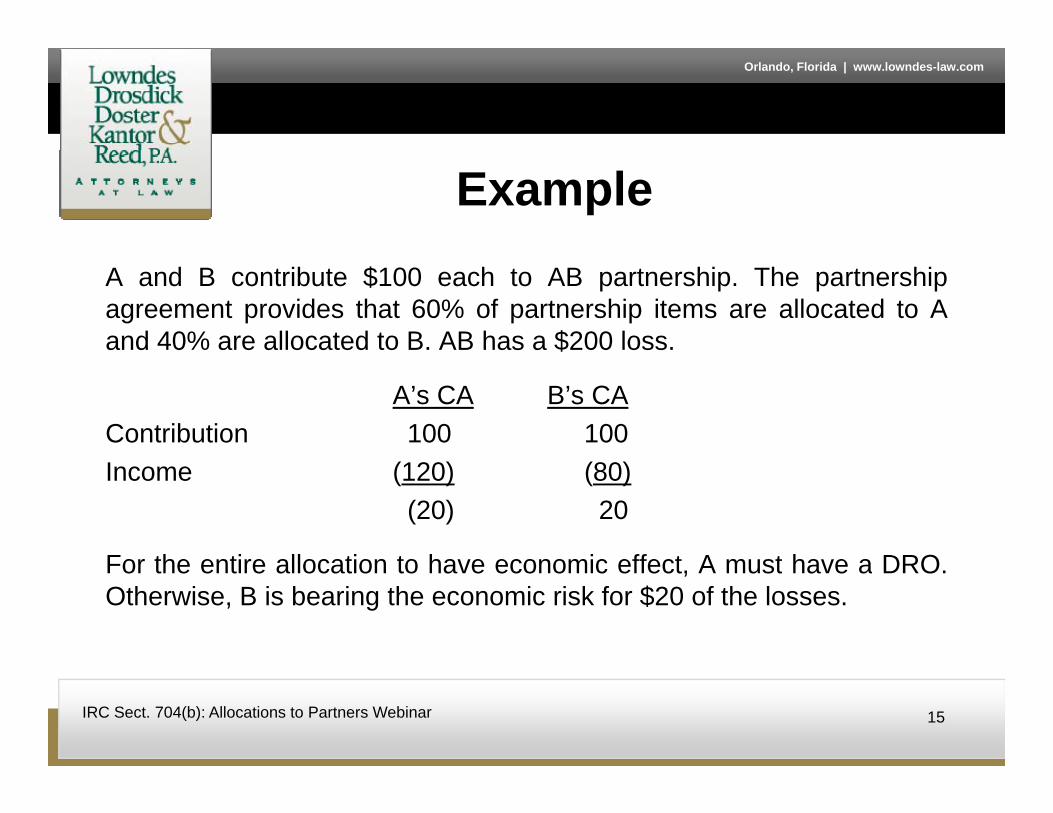

ExampleA and B contribute $100 each to AB partnership. The partnershipagreement provides that 60% of partnership items are allocated to Aand 40% are allocated to B. AB has a $200 loss.

A’s CA B’s CAContribution 100 100Income (120) (80)

(20) 20

For the entire allocation to have economic effect A must have a DROFor the entire allocation to have economic effect, A must have a DRO.Otherwise, B is bearing the economic risk for $20 of the losses.

IRC Sect. 704(b): Allocations to Partners Webinar 15

Orlando, Florida | www.lowndes-law.com

Planning Opportunity

Treas. Reg. §1.761-1(c) provides that a “partnership agreement” canTreas. Reg. §1.761 1(c) provides that a partnership agreement canbe modified or amended with respect to a taxable year after the closeof the taxable year, as long as the amendment occurs on or before thedue date for the partnership return (without extension).

This gives partners a planning opportunity to amend how they allocateincome and losses after the close of the year, in particular to providefor a limited DRO to the extent necessary to support a loss allocationfor a limited DRO to the extent necessary to support a loss allocation.

IRC Sect. 704(b): Allocations to Partners Webinar 16

Orlando, Florida | www.lowndes-law.com

Alternate Test For Economic Effect

(1) Capital account requirement

(2) Liquidation requirement(2) Liquidation requirement

(3) Partnership agreement has a qualified income offset (QIO)provision. The QIO must require that any partner with an

t d ti it l t b ll t d ll f th tunexpected negative capital account be allocated all of the nextitems of partnership income, so as to eliminate the negativebalances as quickly as possible.

(4) The allocation does not create or increase a deficit in a partner’scapital account in excess of the partner’s obligation to restore adeficit.

IRC Sect. 704(b): Allocations to Partners Webinar 17

Orlando, Florida | www.lowndes-law.com

Substantiality

The economic effect of an allocation is substantial if there is areasonable possibility that the allocation will affect substantially thedollar amounts to be received by the partners from the partnership,independent of tax consequences.

In short, an allocation lacks substantiality if the allocation hasfavorable tax consequences to one partner without correspondingq p p gdetrimental tax consequences to the other partners and no overallchange on the partners’ capital accounts.

If the only effect of an allocation is to reduce taxes withoutsubstantially affecting the partners’ pre-tax distributive shares, thenthe economic effect is not substantial.

IRC Sect. 704(b): Allocations to Partners Webinar 18

Orlando, Florida | www.lowndes-law.com

Substantiality (Cont.)

Even if the general rule is satisfied, the economic effect is notsubstantial in the following cases:

(1) Shifting tax consequences

(2) Transitory allocations(2) Transitory allocations

(3) After-tax effect

IRC Sect. 704(b): Allocations to Partners Webinar 19

Orlando, Florida | www.lowndes-law.com

Shifting Tax AllocationsOccurs if there is a strong likelihood that:

(1) The net increases and decreases that will be recorded in thepartners’ respective capital accounts for such taxable year willp p p ynot differ substantially from the net increases and decreasesthat would be recorded in the partners’ capital accounts if theallocations were not contained; and

(2) The total tax liability of the partners will be less than if theallocations were not contained in the partnership agreementp p g(taking into account the tax consequences that result from theinteraction of the allocation with the partner’s tax attributeseven if unrelated to the partnership).

IRC Sect. 704(b): Allocations to Partners Webinar 20

Orlando, Florida | www.lowndes-law.com

Shifting Tax Allocations (Cont.)(Cont.)

Example

A d B l t b t A i t t tit T thA and B are equal partners, but A is a tax-exempt entity. To theextent that there is any, B is allocated all of the tax-exempt incomeup to an amount that equals 50% of the partnership income. Thislacks substantiality under the shifting tax consequences rulelacks substantiality under the shifting tax consequences rule.

ExceptionValue-equals-basis rule: A partnership’s assets are irrebuttablya ue equa s bas s u e pa t e s p s assets a e ebuttab ypresumed to have a value equal to their basis (or book value ifdifferent from basis).

IRC Sect. 704(b): Allocations to Partners Webinar 21

Orlando, Florida | www.lowndes-law.com

Transitory Allocations

If a partnership agreement provides for a possibility that one or moreallocations (original allocation) will be largely offset by one or moreallocations (offsetting allocation), and there is a strong likelihood that:

(1) The net increases and decreases that will be recorded in thepartners’ respective capital accounts for such taxable year willpartners respective capital accounts for such taxable year willnot differ substantially from the net increases and decreasesthat would be recorded in the partners’ capital accounts if theallocations were not contained; andallocations were not contained; and

IRC Sect. 704(b): Allocations to Partners Webinar 22

Orlando, Florida | www.lowndes-law.com

Transitory Allocations (Cont.)( )

(2) The total tax liability of the partners will be less than if theallocations were not contained in the partnership agreement(taking into account the tax consequences that result from theinteraction of the allocation with the partner’s tax attributeseven if unrelated to the partnership).

Example A and B are equal partners, but A has NOLs that are expiring inthe next two years A is therefore allocated all partnership incomethe next two years. A is therefore allocated all partnership incomefor the first two years, then all to B for the next two years, thenequally between them. This is a transitory allocation and lackssubstantiality

IRC Sect. 704(b): Allocations to Partners Webinar 23

substantiality.

Orlando, Florida | www.lowndes-law.com

Transitory Allocations (Cont.)( )

Exceptions

• Five year rule: If at the time of allocation there is a strong• Five-year rule: If at the time of allocation, there is a stronglikelihood that the original allocation will not be largely offsetwithin five years, then presumption that economic effect ofallocation is not transitoryallocation is not transitory.

• Value-equals-basis rule

• Risky ventures: Because a risky venture is speculative in nature• Risky ventures: Because a risky venture is speculative in nature,there is not a strong likelihood that the offsetting profits/incomewill ever materialize.

IRC Sect. 704(b): Allocations to Partners Webinar 24

Orlando, Florida | www.lowndes-law.com

After-Tax Rule

An allocation does not have substantial economic effect if, at the timethe allocation is added to the partnership agreement:

(1) The after-tax economic consequences of at least one partnermay be enhanced compared to such consequences if theallocation were not contained in the partnership agreement,and

(2) There is a strong likelihood that the after-tax consequences ofno partner will be substantially diminished compared with theno partner will be substantially diminished compared with theconsequences if the allocation were not in the partnershipagreement.

IRC Sect. 704(b): Allocations to Partners Webinar 25

Orlando, Florida | www.lowndes-law.com

After-Tax Rule (Cont.)

The focus of this rule is on after-tax consequences, not pre-tax capitalt Th t id l k f b t ti lit b iaccounts. Thus, you cannot avoid lack of substantiality by using an

unequal number of years.

ExceptionsExceptions

• Value-equals-basis rule

• Risky venture• Risky venture

IRC Sect. 704(b): Allocations to Partners Webinar 26

Orlando, Florida | www.lowndes-law.com

No Substantial Economic EffectEffect

If there is no substantial economic effect, a reallocation will occur inaccordance with the partners’ interest in the partnership. Presumption isaccordance with the partners interest in the partnership. Presumption isthat partners share per capita (i.e., 50-50 if two partners).

Factors to consider in rebutting this presumption• The partners’ relative contributions to the partnership• The interests of the partners in economic profits and losses (if

different from taxable income and loss)• Interests in cash flow or other non-liquidating distributions• Rights to distribution on liquidation

IRC Sect. 704(b): Allocations to Partners Webinar 27

Partnership Agreement Drafting ApproachesD fti ll ti i i Drafting allocations provisions Liquidating in accordance with capital accounts Can qualify for the “safe harbor” Either tranched allocation provisions or forced allocation provisions

Liquidating in accordance with the “business deal” (i.e., the distribution provisions)p ) Cannot qualify for the “safe harbor” May be able to have SEE (economic equivalency test) Generally use forced or “targeted” allocations Generally use forced or targeted allocations Many parties to the business deal prefer this approach.

WHITE & CASE LLP 28

Partnership Agreement Drafting Approaches (Cont.)

D fti ll ti i i (C t ) Drafting allocations provisions (Cont.) Tranched allocations Limited Partner puts up 90% of capital, General Partner puts up 10%

of capital; cumulative profit shared 50%/50% (assume no LP DRO). Partnership gains allocated (i) first 90%/10% to offset prior losses;

(ii) second, 50% to each partner. Partnership losses allocated (i) first 50%/50% to offset prior gains

allocated per tranche (ii) above; (ii) second, 90%/10% until each partner’s capital account reduced to zero; (iii) last 100% to the general partner.

The more complicated the business deal (e.g., preferred returns, IRR hurdles, profits interests, other flipping allocations), the more

WHITE & CASE LLP 29

complicated the allocations will be to draft.

Partnership Agreement Drafting Approaches (Cont.)

Drafting allocations provisions (Cont ) Drafting allocations provisions (Cont.) Targeted/forced allocations

Typical (but not perfect!) provision Partnership profits, losses, deductions and credits shall be allocated among the

t i h th t th it l t f h t i di t l partners in a manner such that the capital account of each partner, immediately after making such allocation, is as nearly as possible equal (proportionately) to the distributions that would be made to such partner pursuant to (the distribution provision of the agreement), if the partnership were dissolved, its affairs wound up and its assets sold for cash equal to their book value (as adjusted under this and its assets sold for cash equal to their book value (as adjusted under this agreement), all partnership liabilities were satisfied (limited with respect to each non-recourse liability to the book values of the assets securing such liability), and the net assets of the partnership were distributed in accordance with (the distribution section) to the partners immediately after making such allocation, minus(i) such partner’s share of minimum gain and (ii) any amount such partner is obligated (or deemed obligated) to restore to the partnership.

Intent is to cause the capital accounts to equal the distributions partners would receive upon a liquidation of the partnership

WHITE & CASE LLP 30

Partnership Agreement Drafting Approaches (Cont.)

D fti ll ti i i (C t ) Drafting allocations provisions (Cont.) Pros and cons of the various approaches Liquidating in accordance with capital accounts allow an allocation to

qualify for the safe harbor However, parties to the deal often do not want to rely on the

allocations producing the right business deal. Incorrect capital accounts could distort cash partners ultimately expect to receive.

Tranched allocations provide a “road map” for the accountants who need to implement the agreement However, even when tranched allocations are used, often the tax

director/CFO will “back into” the tranched allocations by doing forced allocations.

WHITE & CASE LLP 31

Partnership Agreement Drafting Approaches (Cont.) Drafting allocations provisions (Cont ) Drafting allocations provisions (Cont.) Pros and cons of the various approaches (Cont.) Forced allocations and liquidating in accordance with the business deal generally

minimize likelihood of “practitioner error.” However, even forced allocation provisions must be drafted with care to

guard against unintended consequences. Non-recourse deductions don’t affect bottom line cash distributions, so

the m st be car ed o t of pro ision or speciall allocated (not entirel they must be carved out of provision or specially allocated (not entirely clear that NRD safe harbor can be complied with under a target allocation approach). Similarly, minimum gain charge-backs need to be backed out of the y g g

targeted amount. Or, a partner is only supposed to receive a particular amount upon the

occurrence of a particular event.O t hi i t d t l ith th “f ti l ”

WHITE & CASE LLP 32

Or, a partnership intends to comply with the “fractions rule.”

Additional 704(b) Requirements: RevaluationsAdditi l 704(b) it l t i t l Additional 704(b) capital account maintenance rules Revaluations (“book-ups” and “book-downs”) Upon admission of new partners, non-pro rata distributions Assets revalued (marked-to-market) Gain/loss is “booked” to capital accounts of existing partners. Subsequent allocations of depreciation etc made with respect to Subsequent allocations of depreciation, etc. made with respect to

“new” book value (as opposed to historical cost). Reverse 704(c) allocations will apply to take into account the

book-tax difference created by the book-upbook tax difference created by the book up. Note: Newly admitted partner will want input into 704(c)

method partnership uses in order to ensure, e.g., that it receives its “fair share” of subsequent depreciation deductions

WHITE & CASE LLP 33

receives its fair share of subsequent depreciation deductions.

Revaluations (Cont.)E l f l ti Example of revaluation Partnership AB owns property with a cost of 100 and a fair value of 200. A and B each originally contributed 50 and currently share all items 50/50. C is admitted for a 100 capital contribution and will share 1/3 in partnership C is admitted for a 100 capital contribution and will share 1/3 in partnership

property. Absent revaluation of capital accounts, if the property were immediately

sold, the 100 gain in the property would be allocated 1/3 to each partner, so: A capital account: 50 + 33 = 83 B capital account: 50 + 33 = 83 C capital account: 100 + 33 = 133 C capital account: 100 + 33 = 133

Without revaluing the property and “booking” the built-in gain to A and B’s capital account, the business deal is distorted.

WHITE & CASE LLP 34

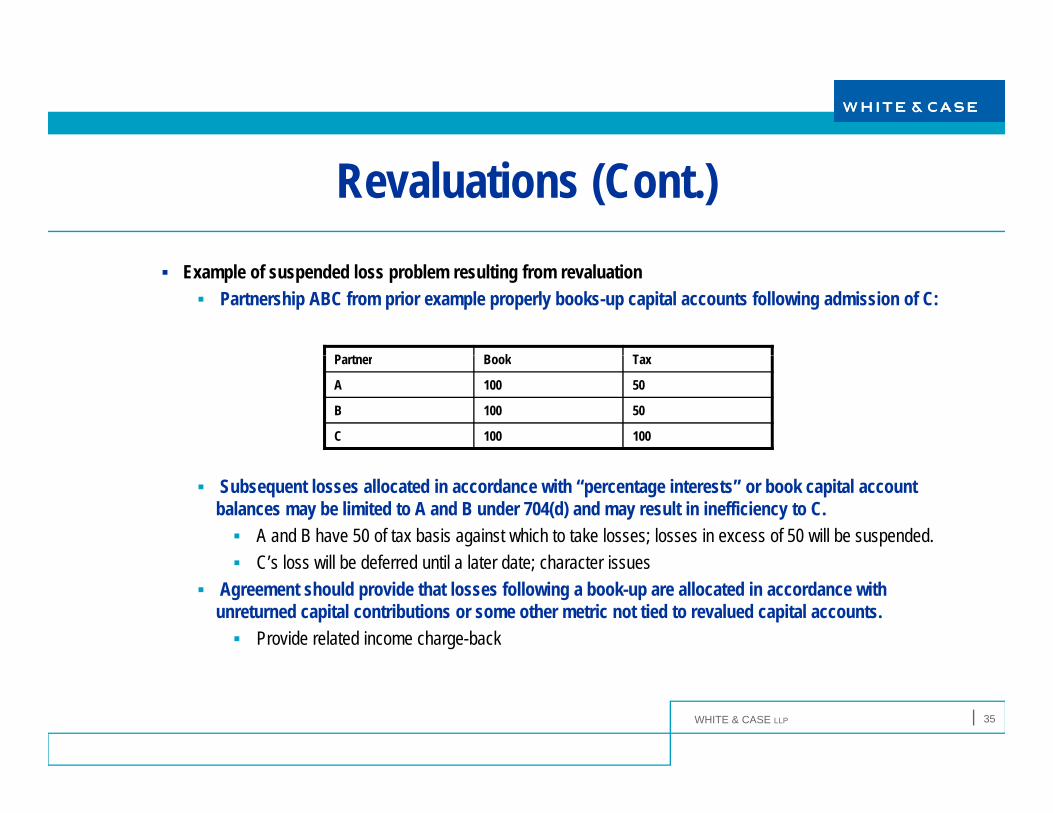

Revaluations (Cont.) Example of suspended loss problem resulting from revaluation

Partnership ABC from prior example properly books-up capital accounts following admission of C:

P t B k TPartner Book Tax

A 100 50

B 100 50

C 100 100

Subsequent losses allocated in accordance with “percentage interests” or book capital account balances may be limited to A and B under 704(d) and may result in inefficiency to C. A and B have 50 of tax basis against which to take losses; losses in excess of 50 will be suspended. C’s loss will be deferred until a later date; character issues C s loss will be deferred until a later date; character issues

Agreement should provide that losses following a book-up are allocated in accordance with unreturned capital contributions or some other metric not tied to revalued capital accounts. Provide related income charge-back

WHITE & CASE LLP 35

Jeremy Naylor White & Case

ASSOCIATED REGULATORY

Jeremy Naylor, White & CaseJorge Otoya, KPMG

ASSOCIATED REGULATORY SECTIONS

Non-Recourse Deductions: Brief Review Of General Rules

Substantial economic effect Substantial economic effect Each allocation of income, gain, loss and deduction must have

“substantial economic effect.”P t i i ll ti b th i b fit d Partner receiving allocations bears the economic benefits and burdens. Reflected in capital accounts Scorecard Positive capital accounts = partner entitlement to partnership capital Negative capital accounts = partner obligation to restore partnership g p p g p p

capital Assuming no unlimited deficit restoration obligation, a partner’s

capital account should not be driven negative by more than the

WHITE & CASE LLP 37

p g ypartner has agreed to restore (or is deemed to have agreed to restore) to the partnership’s capital.

Non-Recourse Deductions (Cont.)“l d d ti tt ib t bl t t hi “losses, deductions … attributable to partnership nonrecourse liabilities” Non-recourse liability Determined under Sect. 752 Generally, a partnership liability where no partner/member bears the

“economic risk of loss”I di i f i i k f l i l d Indicia of economic risk of loss include: Obligation to make payment on debt or contribute capital Express in agreement or required under state law

P t l t d i l d t t hi Partner or related person is lender to partnership Guarantees of principal or interest repayment Pledges/other security provided for borrowing

WHITE & CASE LLP 38

Non-Recourse Deductions (Cont.)

How are they allocated? General rule: Allocations are required to have “substantial

economic effect.” Essentially, the partner receiving the allocation has the economic

benefit or burden of such allocation. If no partner bears the economic burden of a partnership non-

recourse liability (because no partner is individually required to repay the liability), how can an allocation of a non-recourse deduction have substantial economic effect? Safe harbor

WHITE & CASE LLP 39

Non-Recourse Deductions (Cont.)H th ll t d? How are they allocated? Principles of 1.704-2 regulations When property subject to a non-recourse debt is sold, the full

amount of the debt must be included in amount realized (regardless of its FMV) (principles of Tufts) Thus, the partnership will be required to include in income the

difference between the basis of property and the amount of the outstanding non-recourse liability. So long as such income is allocated (or charged back) to the

partners who were allocated the corresponding non-recourse deductions (i.e., the deductions that caused the basis of the property to decrease), then the allocations of the non-recourse deductions will b d d t h b t ti l i ff t

WHITE & CASE LLP 40

be deemed to have substantial economic effect.

Non-Recourse Deductions (Cont.)H th ll t d? How are they allocated? Safe harbor for allocations of non-recourse deductions Allocations under LPA generally have SEE. Non-recourse deductions are allocated in a manner that is

reasonably consistent with allocations of some other significant partnership item associated with the mortgaged property. LPA contains a “minimum gain chargeback” provision.

Allocations of non-recourse deductions must bear some relation to the overall business deal (can be in a range between two different ( gallocation ratios), and the partner receiving the tax benefit of the deduction will be charged back an equivalent amount of income at a later date (when the minimum gain chargeback is triggered).

WHITE & CASE LLP 41

Minimum Gain Charge-BacksSeveral concepts in one Several concepts in one Minimum gain: The excess of the principal amount of non-recourse debt

over the tax basis of the property securing it I.e., the “minimum” amount of gain the owner of the property would be , g p p y

required to recognize upon a taxable sale of the property Minimum gain increases when basis decreases below the principal amount

of the non-recourse debt, or principal amount of debt increases (and typically the borrowed proceeds are distributed to the partners)typically the borrowed proceeds are distributed to the partners). E.g., depreciation deductions drive basis below principal amount of debt.

Minimum gain decreases when there are certain basis increases, or when the property is disposed of Non-recourse deductions for a particular year will generally equal the

increase in partnership minimum gain for that year. I.e., deductions from property secured by non-recourse loan will not be “non-

recourse deductions ” unless partnership minimum gain has increased

WHITE & CASE LLP 42

recourse deductions, unless partnership minimum gain has increased.

Minimum Gain Charge-Backs (Cont.) Partner’s share of minimum gain Partner s share of minimum gain Tracked separately for each partner – generally will equal such partner’s

share of non-recourse deductions previously allocated Minimum gain charge-back

T i d h t hi h t d i i i i Triggered when partnership has a net decrease in minimum gain E.g., upon sale of property – minimum gain goes to zero (because the debt

has been repaid upon sale) Any other transaction that results in a decrease in minimum gain triggers the

h b k tchargeback, except: Refinancings of debt or conversion of debt into recourse debt – partners

who become recourse on debt should not then have the minimum gain chargeback triggeredC f Capital contributions, if used to repay principal on non-recourse debt or improve property This does not trigger charge-back, because the partner is actually

coming out of pocket to improve property; there is no gain going untaxed by reason of this transaction

WHITE & CASE LLP 43

untaxed by reason of this transaction. Revaluation

Minimum Gain Charge-Backs (Cont.)

Result of minimum gain charge-back Partners are charged back income equal to their respective shares

of decreases in the partnership minimum gain. Recapturep Undoing tax benefits of deductions previously taken

WHITE & CASE LLP 44

Minimum Gain Charge-Backs (Cont.) Example Example A and B form a partnership and each contributes $0. AB borrows $100 on a non-recourse basis to acquire depreciable property. A and B each have outside basis of $50. Partnership has $100 basis in property.

P t d i t $10 E h f A d B i ll t d $5 f Property depreciates $10 per year. Each of A and B is allocated $5 of depreciation deductions.

After year 5, each of A and B’s basis is reduced to $25, and they each have a negative capital account of $(25).At end of year 5 AB puts the property back to the lender (assume no previous At end of year 5, AB puts the property back to the lender (assume no previous principal repayments).

What happens to A & B AB’s minimum gain at the end of year 5 was: $50 (difference between the $100

principal amount and $50 adjusted basis of property)principal amount and $50 adjusted basis of property). Upon foreclosure, AB has net decrease in minimum gain of $50 (because

principal amount of debt is $0 and AB no longer owns property). Each of A and B must be allocated $25 of income under the minimum gain

chargeback reflecting prior non-recourse deductions they have taken.

WHITE & CASE LLP 45

chargeback reflecting prior non recourse deductions they have taken.

Minimum Gain Charge-Backs (Cont.)Complicating factors Complicating factors Partners may share in operating losses in a manner different than non-

recourse deductions. Non-recourse deductions = net increase in partnership minimum gain, so Non recourse deductions net increase in partnership minimum gain, so

you need to analyze each year whether depreciation deductions are sufficient to result in a net increase in PMG; otherwise, partners may share in losses in a different manner.

Need to pay careful attention to drafting other charge-back provisions in Need to pay careful attention to drafting other charge-back provisions in allocation clauses in agreements – ensure that income related to non-recourse deductions is not being charged back already before the minimum gain charge-back

S h b k f l ll ti i i d t ifi ll l d Some charge-back of loss allocation provisions do not specifically exclude charge-backs of non-recourse deductions previously taken. Can result in double-counting

WHITE & CASE LLP 46

Recent Transactional Examples Structuring to minimize minimum gain charge back Structuring to minimize minimum gain charge-back

Client is interested in acquiring debt or equity from bankrupt entity However, entity is partner in real estate partnership with several underwater

properties.Mi i i h b k ld b t i d if l d f l lti i t Minimum gain charge-back would be triggered if lender forecloses resulting in tax liability.

What to do? Make debt recourse Provide guarantee Transaction would trigger charge-back for those partners who remained non-

recourse to the debt. Trigger COD income rather than minimum gain charge-back COD income is excluded from income of bankrupt debtor; income from minimum

gain chargeback is not. Putting property to lender in satisfaction of non-recourse loan does not trigger

COD (because borrower was never “on the hook” for the debt),

WHITE & CASE LLP 47

Negotiating a reduction in principal while retaining the property can result in COD (because borrower retains property).

Recent Transactional Examples (Cont.)St t i t i i i i i i h b k Structuring to minimize minimum gain charge-back Briarpark case Lender agreed to release liens on property, if borrower would sell the

property for specified price and assign the proceeds to the lender. 5th circuit noted transactions intertwined; transaction did not result in

COD income. Transaction would need to be structured in a manner that bifurcated

the lender’s agreement from the sale of the property. It may be difficult to get a buyer to agree to provide funds prior to the date borrower has full control of property.

WHITE & CASE LLP 48

Recent Transactional Examples (Cont.) Allocating non recourse deductions from specific assets to new partner Allocating non-recourse deductions from specific assets to new partner

Existing partnership plans to acquire assets with borrowed funds that are entitled to accelerated depreciation.

Existing partners cannot fully use depreciation deductions.P t hi h th ti d th li biliti Partnership has other properties and other liabilities.

Third-party investor can use depreciation deductions. Can deductions from specific assets in partnership that secure multiple liabilities be

allocated specifically to new partner? Sect. 1.704-2 regulations look at non-recourse deductions and partnership minimum

gain as aggregate concepts. Under 752 regulations, it is unclear that basis attributable to specific assets can be

allocated to a particular partner. Even if depreciation deductions on specific assets could be allocated to a particular

partner, you may not be able to control timing of minimum gain charge-back. Exculpatory liabilities?

Solutions?

WHITE & CASE LLP 49

New partner provides guarantee and makes liability recourse. Series partnership?

Scenario 1: Capital Accounts And Economic

Effect

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 50

50

Scenario 1: Capital Accounts And Economic Effect

LLC is a potential compliance client for its 2010 Form 1065. We have been charged with reviewing its partnership agreement and prior year returns in order to prepare a fee estimateand prior-year returns in order to prepare a fee estimate.

From our review, we determine the following facts:Partners A and B formed LLC in 2008 Partners A and B formed LLC in 2008. Each contributed the same amount of cash to form LLC and have agreed to share in all partnership items, including non-recourse deductions on a 50/50 basis.recourse deductions on a 50/50 basis.

The partnership agreement meets the alternate test for economic effect. The partnership had a $3,000 loss in 2008.p p The partnership has a $13,000 loss in 2009. We are provided a copy of the partnership’s capital account roll-forward.

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5151

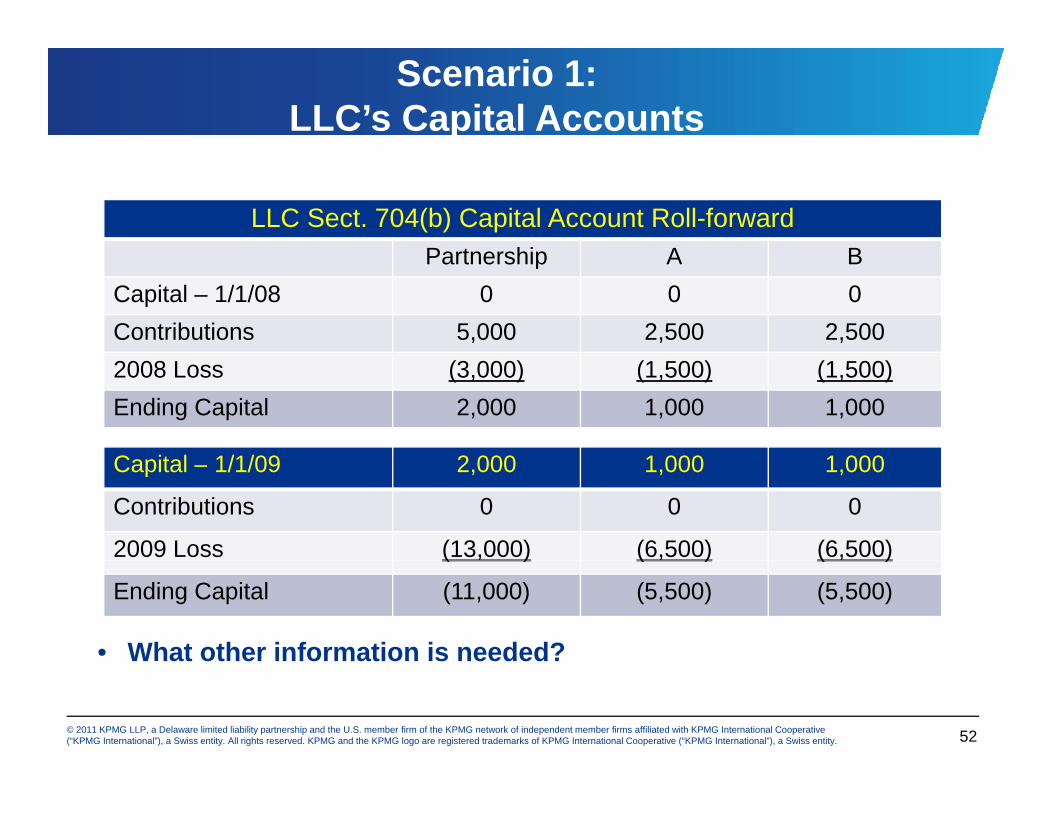

Scenario 1:LLC’s Capital Accounts

LLC Sect. 704(b) Capital Account Roll-forwardPartnership A BPartnership A B

Capital – 1/1/08 0 0 0Contributions 5,000 2,500 2,5002008 Loss (3,000) (1,500) (1,500)Ending Capital 2,000 1,000 1,000

C it l 1/1/09 2 000 1 000 1 000Capital – 1/1/09 2,000 1,000 1,000

Contributions 0 0 0

2009 Loss (13,000) (6,500) (6,500)( ) ( ) ( )

Ending Capital (11,000) (5,500) (5,500)

• What other information is needed?

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5252

Scenario 1:LLC’s Capital Accounts (Cont.)

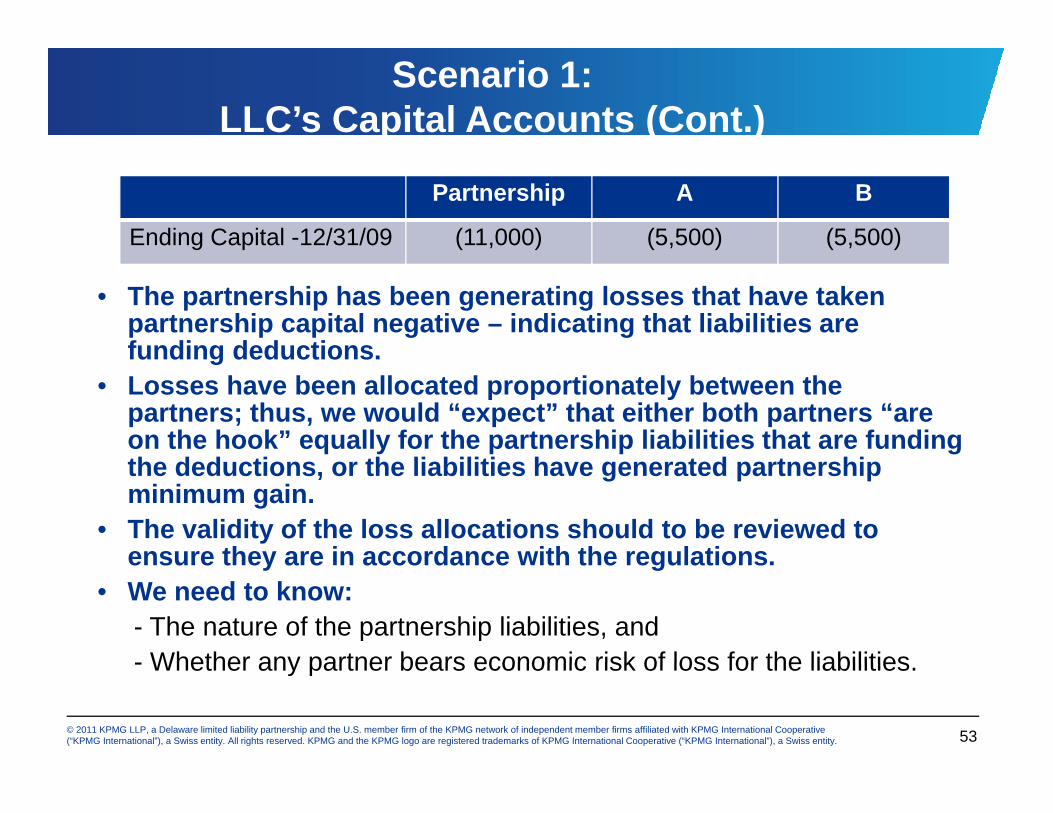

Partnership A B

Ending Capital -12/31/09 (11,000) (5,500) (5,500)

• The partnership has been generating losses that have taken partnership capital negative – indicating that liabilities are funding deductionsfunding deductions.

• Losses have been allocated proportionately between the partners; thus, we would “expect” that either both partners “are on the hook” equally for the partnership liabilities that are funding th d d ti th li biliti h t d t hithe deductions, or the liabilities have generated partnership minimum gain.

• The validity of the loss allocations should to be reviewed to ensure they are in accordance with the regulationsensure they are in accordance with the regulations.

• We need to know:- The nature of the partnership liabilities, and- Whether any partner bears economic risk of loss for the liabilities

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5353

- Whether any partner bears economic risk of loss for the liabilities.

What Do We Know About The LLC?

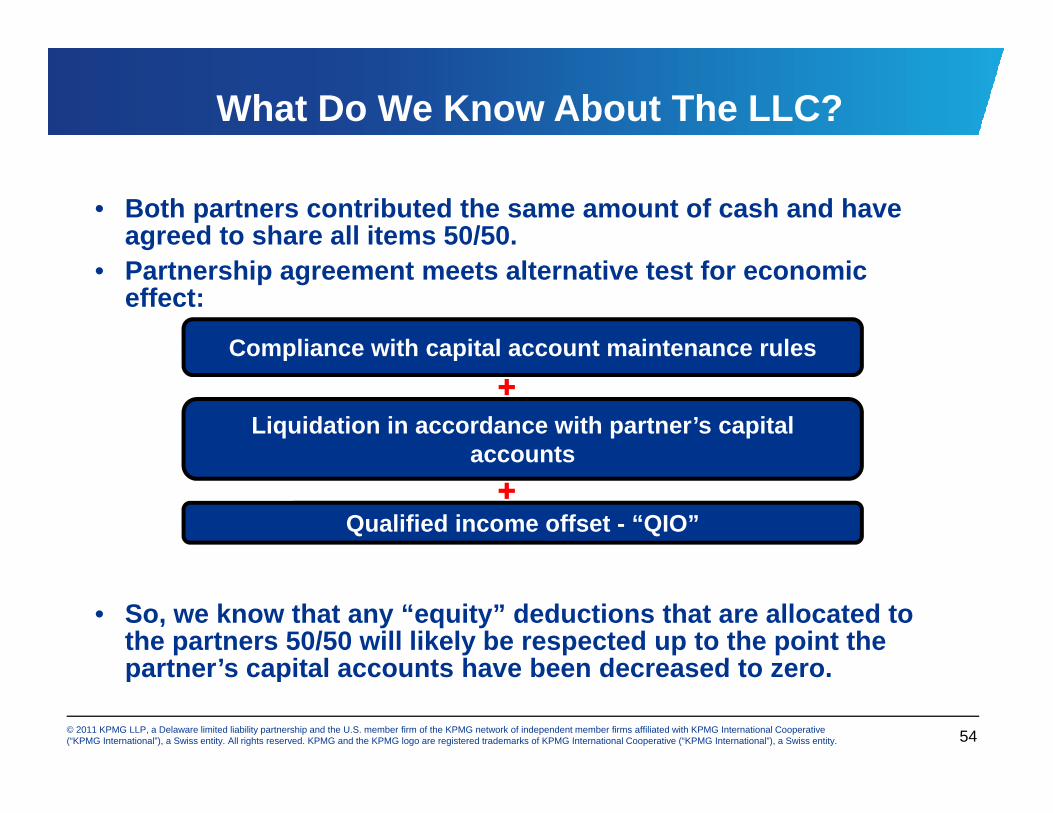

• Both partners contributed the same amount of cash and have agreed to share all items 50/50.

• Partnership agreement meets alternative test for economic effect:

Compliance with capital account maintenance rulesCompliance with capital account maintenance rules

Liquidation in accordance with partner’s capital accountsaccounts

Qualified income offset - “QIO”

• So, we know that any “equity” deductions that are allocated to the partners 50/50 will likely be respected up to the point the partner’s capital acco nts ha e been decreased to ero

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 54

partner’s capital accounts have been decreased to zero.

Scenario 1: More Facts

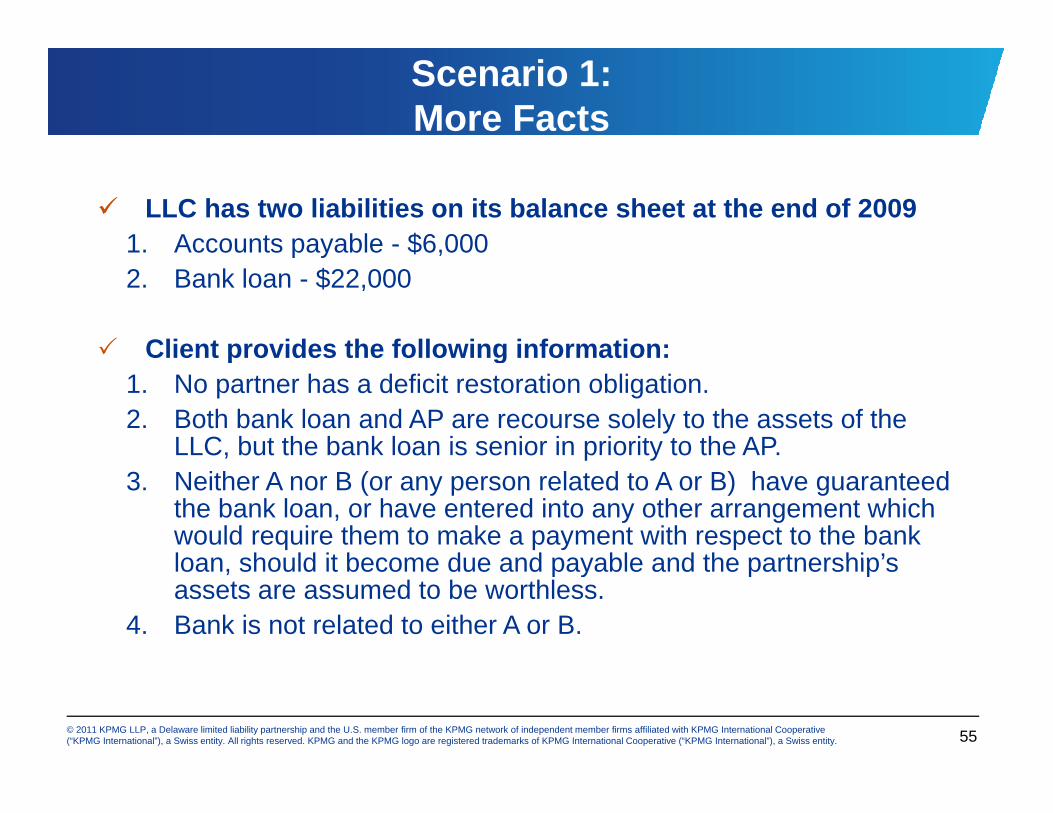

LLC has two liabilities on its balance sheet at the end of 20091. Accounts payable - $6,000p y $ ,2. Bank loan - $22,000

Client provides the following information:Client provides the following information:1. No partner has a deficit restoration obligation.2. Both bank loan and AP are recourse solely to the assets of the

LLC, but the bank loan is senior in priority to the AP., p y3. Neither A nor B (or any person related to A or B) have guaranteed

the bank loan, or have entered into any other arrangement which would require them to make a payment with respect to the bank loan should it become due and payable and the partnership’sloan, should it become due and payable and the partnership s assets are assumed to be worthless.

4. Bank is not related to either A or B.

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5555

Scenario 1: More Facts (Cont.)

• Based on these facts, the capital accounts appear correct, and the prior year loss allocations are also likely correctthe prior year loss allocations are also likely correct.

• Why?y

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5656

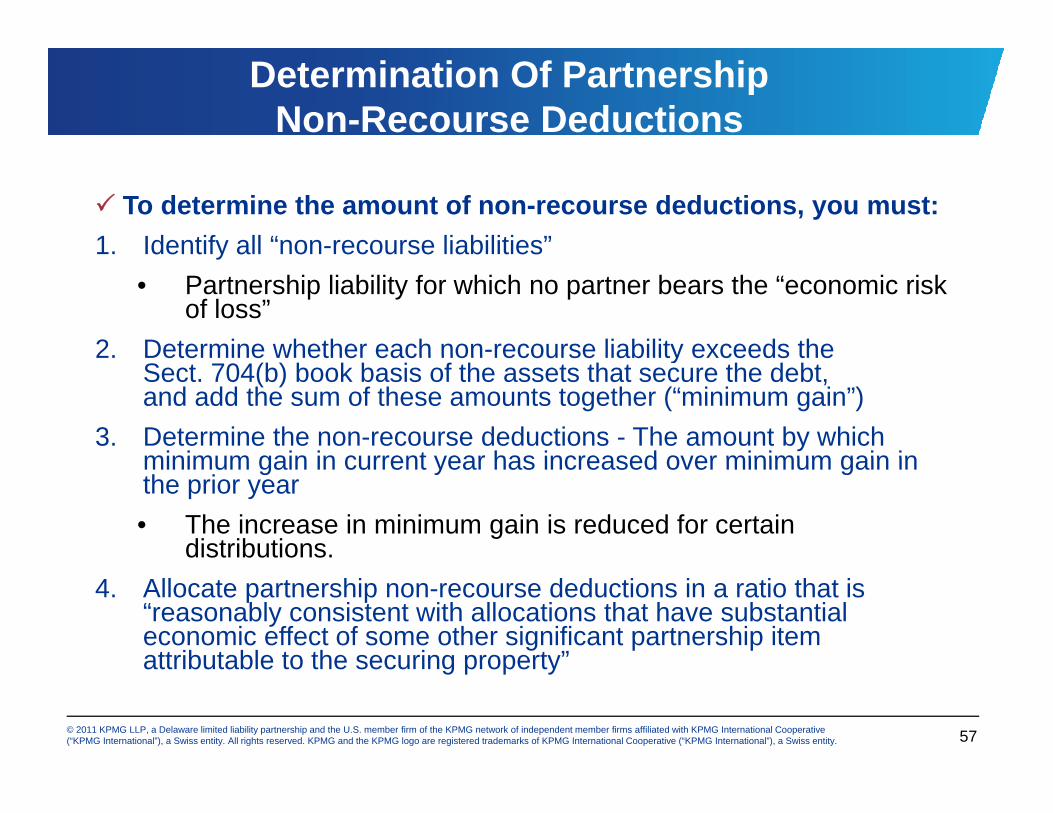

Determination Of Partnership Non-Recourse Deductions

To determine the amount of non-recourse deductions, you must:1. Identify all “non-recourse liabilities”1. Identify all non recourse liabilities

• Partnership liability for which no partner bears the “economic risk of loss”

2. Determine whether each non-recourse liability exceeds the2. Determine whether each non recourse liability exceeds the Sect. 704(b) book basis of the assets that secure the debt,and add the sum of these amounts together (“minimum gain”)

3. Determine the non-recourse deductions - The amount by which minimum gain in current year has increased over minimum gain inminimum gain in current year has increased over minimum gain in the prior year• The increase in minimum gain is reduced for certain

distributions.4. Allocate partnership non-recourse deductions in a ratio that is

“reasonably consistent with allocations that have substantial economic effect of some other significant partnership item attributable to the securing property”

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5757

attributable to the securing property

Scenario 1: Non-Recourse Deduction Calculations

Partnership’s Sect. 704(b) Balance Sheets

12/31/08 12/31/09Net Depreciable Assets 12,000 17,000

Accounts Payable 0 6,000

Bank Loan 10,000 22,000

Partner Capital 2,000 (11,000)

Liabilities & Capital 12,000 17,000

Tax Year 2009 Partnership Minimum GainBank Loan Accounts Payable

A/R 22,000 6,000

A/B: Sec. 704(b) Basis (17,000) (-0-)S/T: Partnership MG 5,000 6,000Less Prior Year MG (-0-) -0-

$

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5858

Increase in MG $5,000 6,000

Example Of LLC Non-Recourse Deduction Calculations

The increase in partnership minimum gain is $11,000 in total (partnership minimum gain of zero in 2008).

Therefore of the total $16 000 losses in 2008 and 2009 $11 000 are non- Therefore, of the total $16,000 losses in 2008 and 2009, $11,000 are nonrecourse deductions and $5,000 are allocated under the partnership agreement loss-sharing provisions (also 50/50).

Under the partnership agreement, the non-recourse deductions are allocable 50/50 between the partners and would be allocated to A and B 50/50.p

Based on the facts as we know them, do the capital accounts appear correct?

P t hi A BPartnership A BCapital – 1/1/09 2,000 1,000 1,000

Contributions 0 0 0

2009 Loss (13,000) (6,500) (6,500)

Ending Capital (11,000) (5,500) (5,500)

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 5959

Example Of LLC Non-Recourse Deduction Calculations (Cont.)

In fact, if we add back each partner’s share of minimum gain, their capital accounts should equal zero (or be above zero). “Adjusted capital account deficit” = Zero. Adjusted capital account deficit Zero. This is a good cross-check to set up between the capital account roll-

forward workpapers and the minimum gain workpapers. Another good practice is to setup the capital account roll-forwards to

illustrate the allocations by partnership provision.y p p p

Partnership A BCapital – 1/1/09 2,000 1,000 1,000C t ib ti 0 0 0Contributions 0 0 02009 Non-Recourse Deductions (11,000) (5,500) (5,500)

2009 “Equity” Losses (2,000) (1,000) (1,000)Ending Capital Account (11,000) (5,500) (5,500)Plus share of PRS MG +11,000 +5,500 +5,500“Adjusted Capital Account” -0- -0- -0-

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6060

j

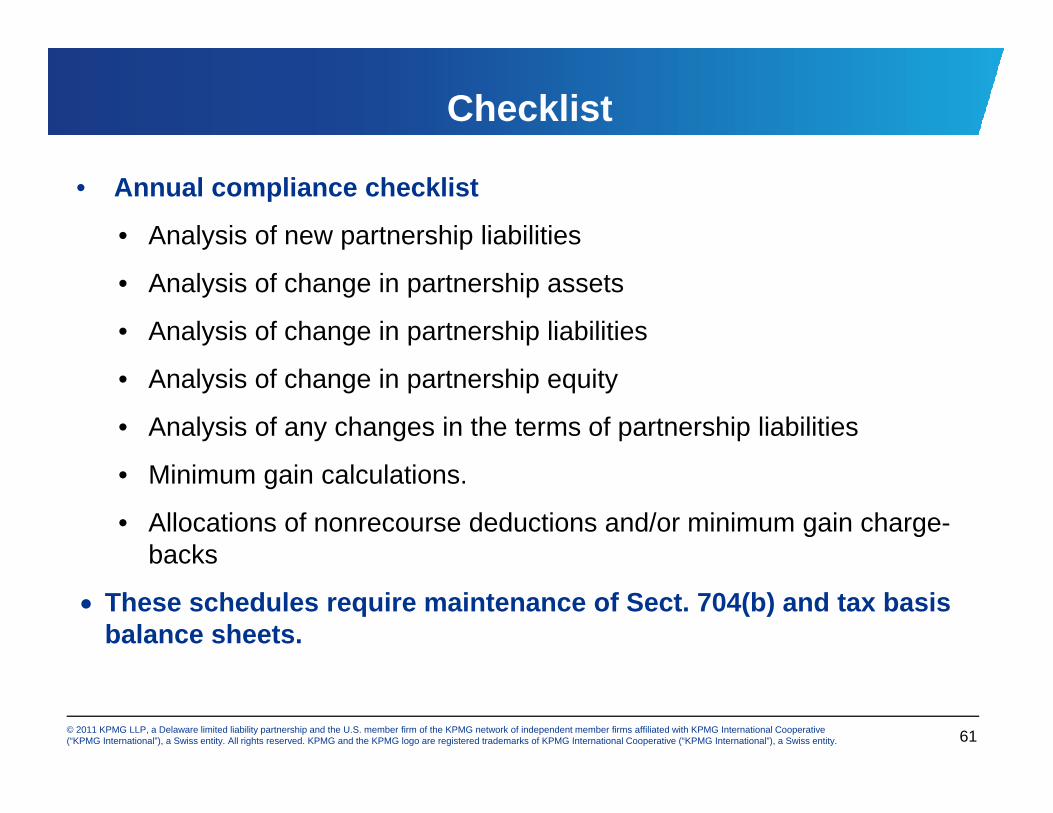

Checklist

• Annual compliance checklist

• Analysis of new partnership liabilities

• Analysis of change in partnership assets

• Analysis of change in partnership liabilities

• Analysis of change in partnership equity

• Analysis of any changes in the terms of partnership liabilities

• Minimum gain calculations.

• Allocations of nonrecourse deductions and/or minimum gain charge-backsbacks

These schedules require maintenance of Sect. 704(b) and tax basis balance sheets.

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6161

Scenario 2:Partner Non Recourse DeductionsPartner Non-Recourse Deductions

Debts With Multiple Priorities

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 62

62

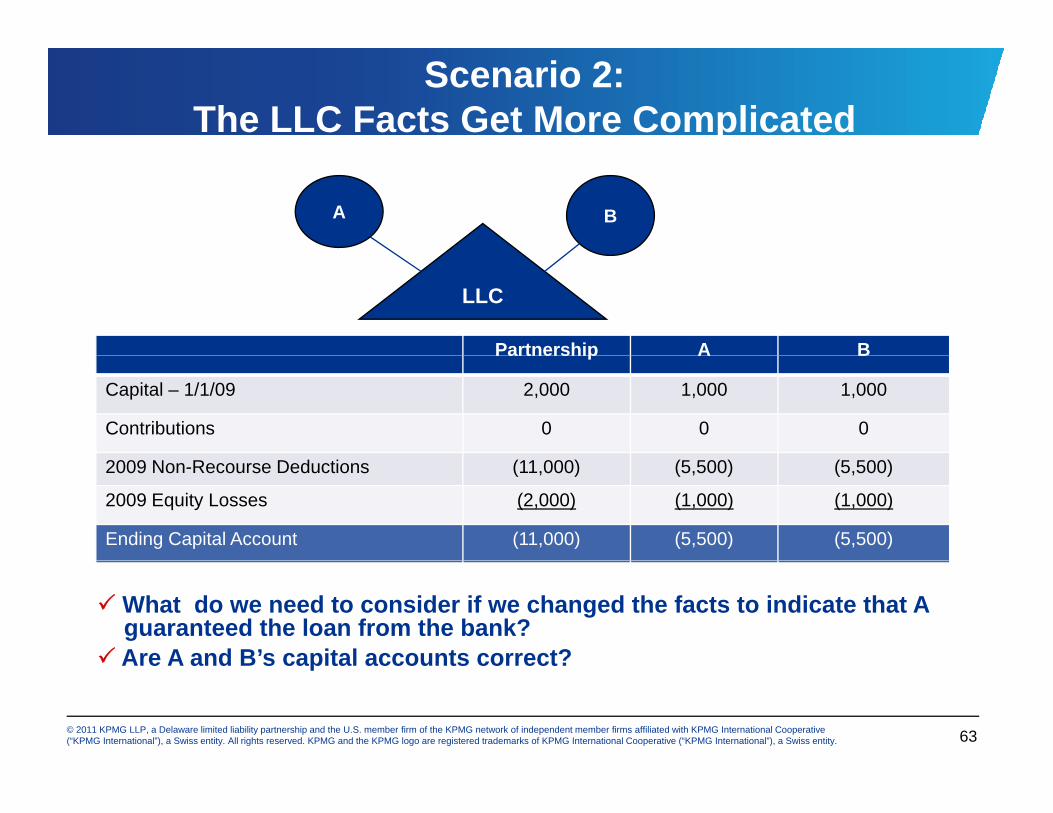

Scenario 2: The LLC Facts Get More Complicated

A B

LLC

Partnership A BPartnership A B

Capital – 1/1/09 2,000 1,000 1,000

Contributions 0 0 0

2009 Non-Recourse Deductions (11,000) (5,500) (5,500)

2009 Equity Losses (2,000) (1,000) (1,000)

Ending Capital Account (11,000) (5,500) (5,500)

What do we need to consider if we changed the facts to indicate that Aguaranteed the loan from the bank?

Are A and B’s capital accounts correct?

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6363

Are A and B s capital accounts correct?

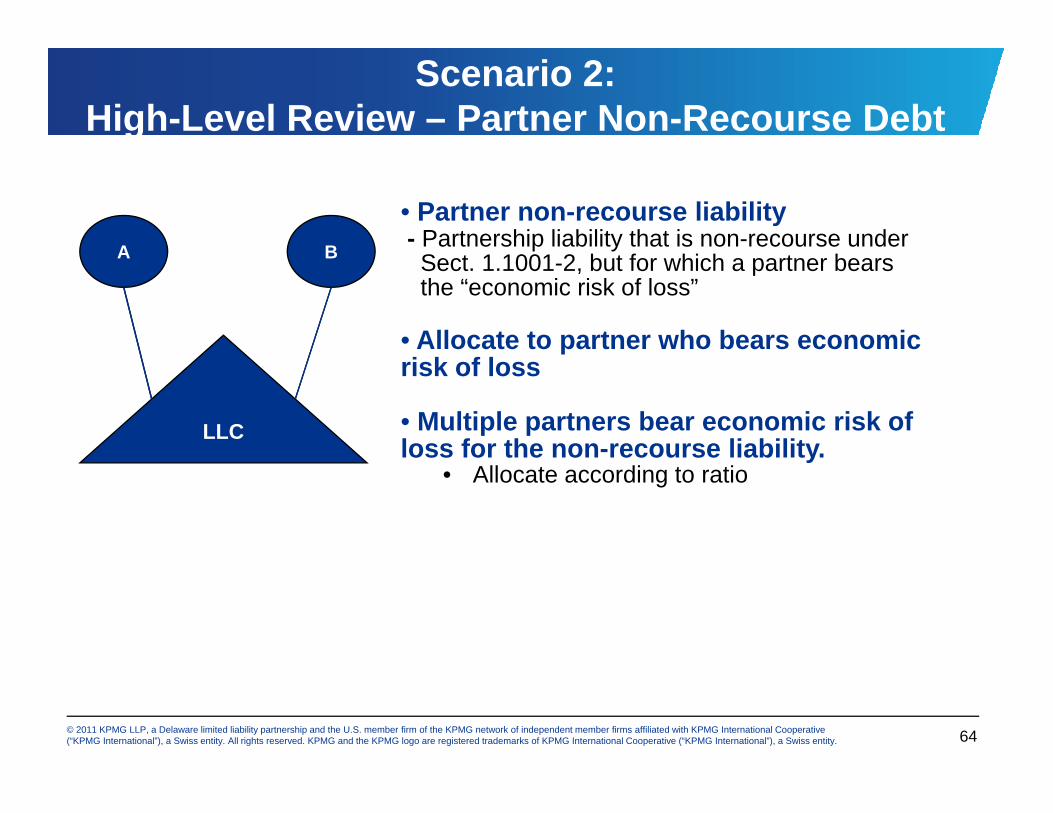

Scenario 2: High-Level Review – Partner Non-Recourse Debt

A B

• Partner non-recourse liability- Partnership liability that is non-recourse under A B Sect. 1.1001-2, but for which a partner bears

the “economic risk of loss”

• Allocate to partner who bears economic

LLC

risk of loss

• Multiple partners bear economic risk of loss for the non-recourse liability.y

• Allocate according to ratio

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6464

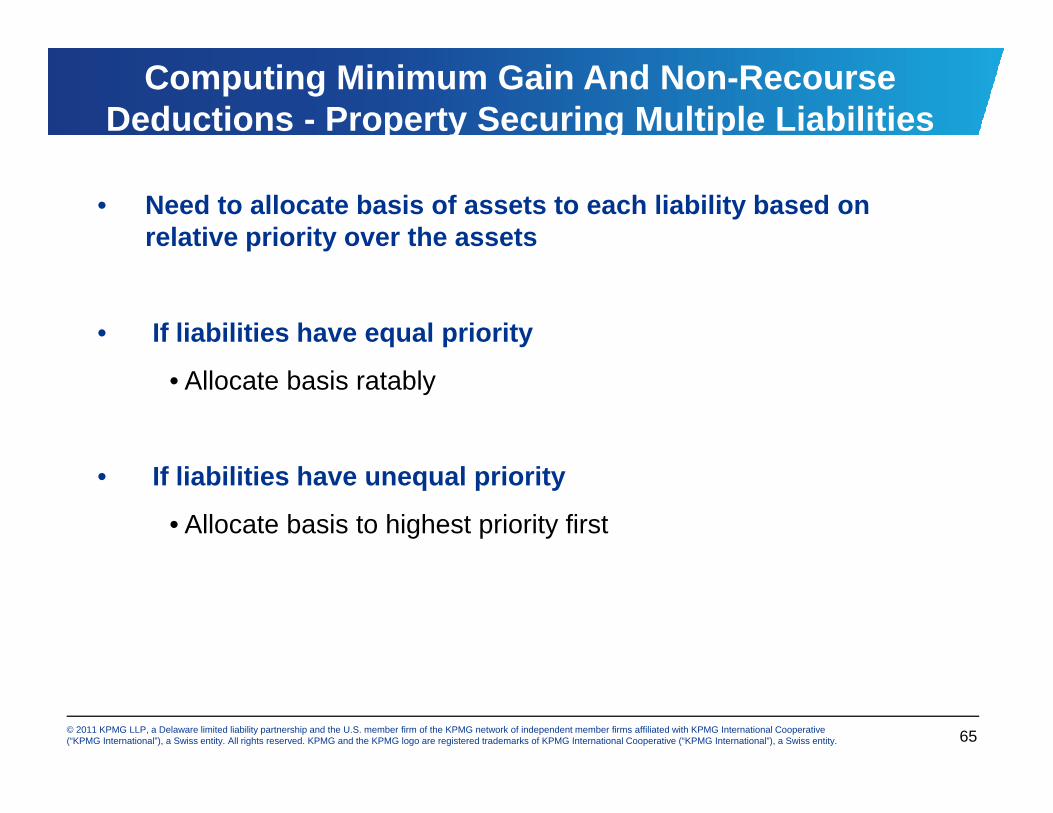

Computing Minimum Gain And Non-Recourse Deductions - Property Securing Multiple Liabilities

• Need to allocate basis of assets to each liability based on relative priority over the assets

• If liabilities have equal priority

• Allocate basis ratably

• If liabilities have unequal priority

• Allocate basis to highest priority first

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6565

Scenario 2: Calculating Minimum Gain With Multiple Debts (Cont.)

Partnership’s Sect. 704(b) Balance Sheets12/31/08 12/31/09

Net Depreciable Assets 12,000 17,000

Accounts Payable 0 6,000Bank Loan 10,000 22,000

2009 Minimum Gain Calculation Partner MG Partnership MGB k L A t P blBank Loan Accounts Payable

A/R: Liabilities (Bank Loan & A/P) 22,000 6,000

A/B: Sect. 704(b) Basis (17,000) (0)

• Increase in partner minimum gain is $5 000 Therefore partner non recourse

S/T: Partnership MG 5,000 6,000Less Prior Year MG 0 0Increase in MG 5,000 6,000

• Increase in partner minimum gain is $5,000. Therefore, partner non-recourse deductions for 2009 equals $5,000.

• These deductions would be allocated 100% to A, as he bears all of the economic risk of loss for the liability . • Losses of $6,000 are funded by partnership non-recourse debt, which are allocated 50/50.

Th i i $2 000 i l it l ll bl d th t hi t

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6666

• The remaining $2,000 in losses are equity losses allocable under the partnership agreement (also 50/50).

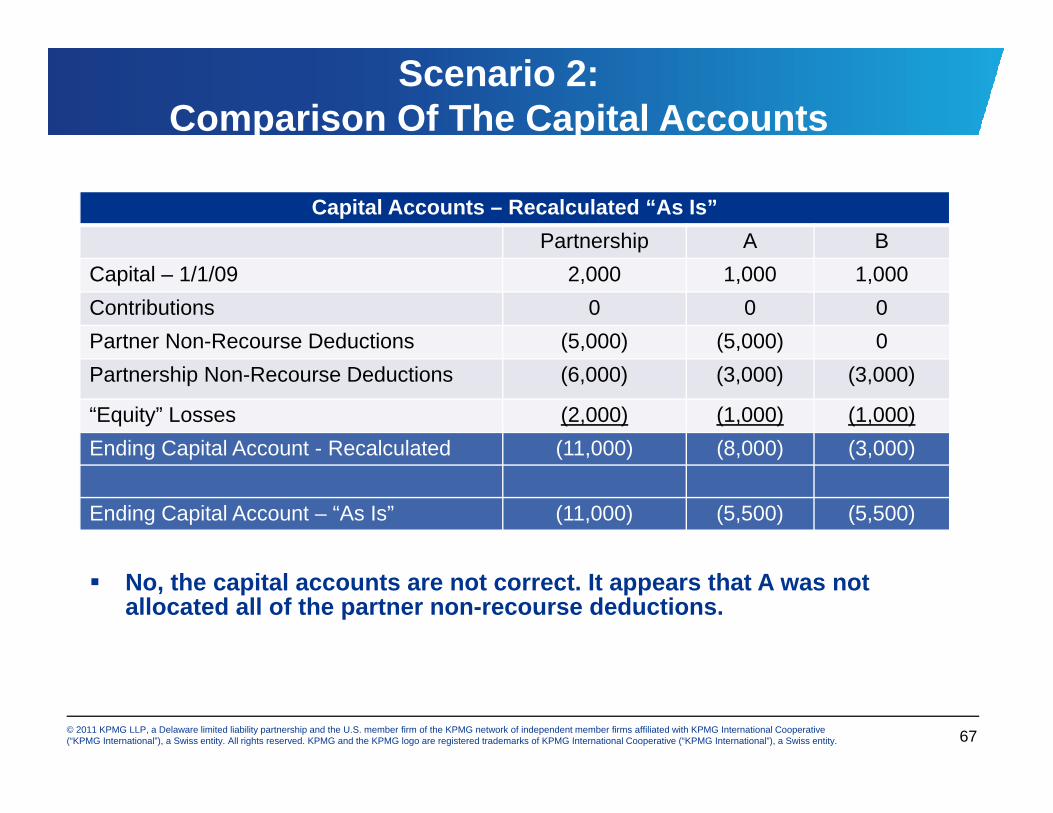

Scenario 2: Comparison Of The Capital Accounts

Capital Accounts – Recalculated “As Is”Partnership A B

Capital – 1/1/09 2,000 1,000 1,000Contributions 0 0 0Partner Non-Recourse Deductions (5,000) (5,000) 0Partnership Non-Recourse Deductions (6,000) (3,000) (3,000)

“Equity” Losses (2,000) (1,000) (1,000)Ending Capital Account - Recalculated (11,000) (8,000) (3,000)g p ( , ) ( , ) ( , )

Ending Capital Account – “As Is” (11,000) (5,500) (5,500)

No, the capital accounts are not correct. It appears that A was not allocated all of the partner non-recourse deductions.

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6767

Scenario 2: Comparison Of The Capital Accounts (Cont.)

Sect. 704(b) Capital Accounts12/31/09 12/31/09 Difference12/31/09

As prepared12/31/09

As recalculatedDifference

A (5,500) (8,000) (2,500)

B (5,500) (3,000) 2,500

Total (11,000) (11,000) 0

• Exposure: A was under-allocated deductions by $2,500. B received $2,500 deductions to which he was not entitled.

• What are the tax considerations?• Duty to inform?• Requirement to amend?• Effect(s) on compliance engagement, if the partnership decides to not amend?• Is this an audit client?

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 6868

• Is this an audit client?

Capital Account Maintenance

Tip: Where non-recourse deductions are shared in the same manner as other partnership items, the minimum gain

t ti till d t b d t i dcomputations still need to be determined.Consider partner debt.Consider debt priorities and collateral.

Tip: Non-recourse deductions may occur even when the partnership aggregate capital is positive.p p gg g p p

Tip: A partner’s negative Sect. 704(b) capital account plus share of minimum gain should generally equal zero (or more than zero).g g y q ( )

Not always true – consider effect of deficit restoration obligations and allocations attributable to recourse debts.

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 69

RECENT AND RELEVANT Jorge Otoya, KPMG

REGULATORY GUIDANCE

Recent Updates With Respect To Sect. 704

• Final regulations under Sect. 704(c)• Direct and indirect partners are considered in determiningDirect and indirect partners are considered in determining

whether a Sect. 704(c) method is reasonable/

• Notice 2010-52 – Foreign tax credit guidance under Sect 909Notice 2010 52 Foreign tax credit guidance under Sect. 909

• Renkemeyer v. Commissioner, 136 TC No 7 • Special allocations• SE tax

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 71

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OFCLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any p y g ytax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be j g pp y pdetermined through consultation with your tax adviser.

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 72

Related Documents