IIEA Conference, Marburg, Germany 17-18 June 2016 IRAN’S OIL & GAS POTENTIAL AND CHALLENGES Manouchehr Takin* * International Oil & Energy Consultant E-mail: [email protected]. Tel: +44 (0) 7896 809 365 Takin 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IIEA Conference, Marburg, Germany 17-18 June 2016

IRAN’S OIL & GAS

POTENTIAL AND CHALLENGES

Manouchehr Takin*

* International Oil & Energy Consultant E-mail: [email protected]. Tel: +44 (0) 7896 809 365

Takin 1

2

• Doom and gloom, or shining success and growth?

• In this presentation: The historical context An overall view Considerable potential Challenges

EXAMINING IRAN’S OIL & GAS INDUSTRY

3

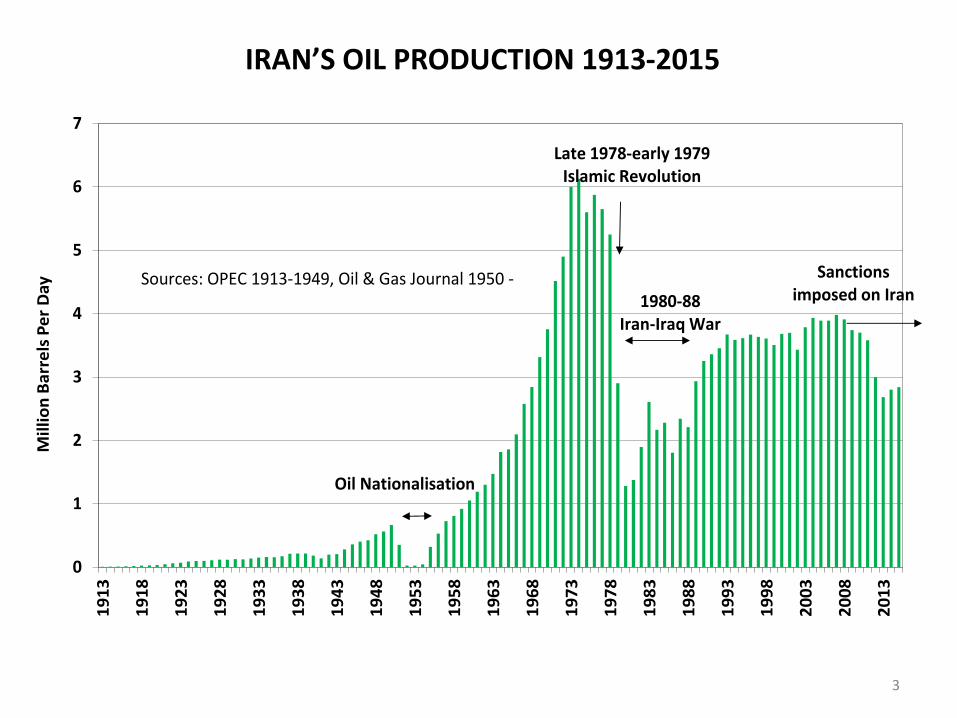

IRAN’S OIL PRODUCTION 1913-2015

0

1

2

3

4

5

6

71

91

3

19

18

19

23

19

28

19

33

19

38

19

43

19

48

19

53

19

58

19

63

19

68

19

73

19

78

19

83

19

88

19

93

19

98

20

03

20

08

20

13

Mil

lio

n B

arr

els

Pe

r D

ay

Sources: OPEC 1913-1949, Oil & Gas Journal 1950 -

Late 1978-early 1979 Islamic Revolution

1980-88Iran-Iraq War

Oil Nationalisation

Sanctions imposed on Iran

4

IRAN’S OIL PRODUCTION 1988-2014 (from two sources) IMPORTANCE OF LIQUIDS FROM GAS FIELDS

2

2.5

3

3.5

4

4.519

88

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

OGJ BP

Million Barrels Per Day

Sources: Oil & Gas Journal and BP Statistical Review of World Energy

Natural gas liquids

5

MORE ON NATURAL GAS

6

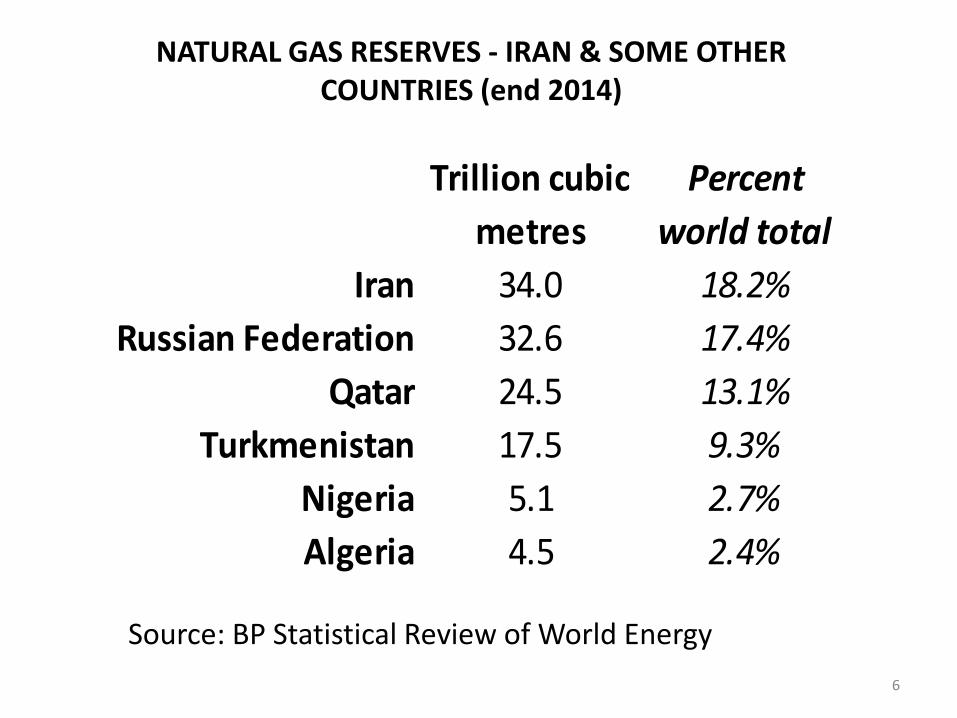

NATURAL GAS RESERVES - IRAN & SOME OTHER COUNTRIES (end 2014)

Source: BP Statistical Review of World Energy

Trillion cubic

metres

Percent

world total

Iran 34.0 18.2%

Russian Federation 32.6 17.4%

Qatar 24.5 13.1%

Turkmenistan 17.5 9.3%

Nigeria 5.1 2.7%

Algeria 4.5 2.4%

7

IRAN: NATURAL GAS PRODUCTION, EXPORTS & IMPORTS (BILLION CUBIC METRES PER YEAR)

0

2

4

6

8

10

12

14

0

50

100

150

200

250

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014

Marketed production

Gas exports

Gas imports

Marketed production Exports and imports

Source: OPEC

8

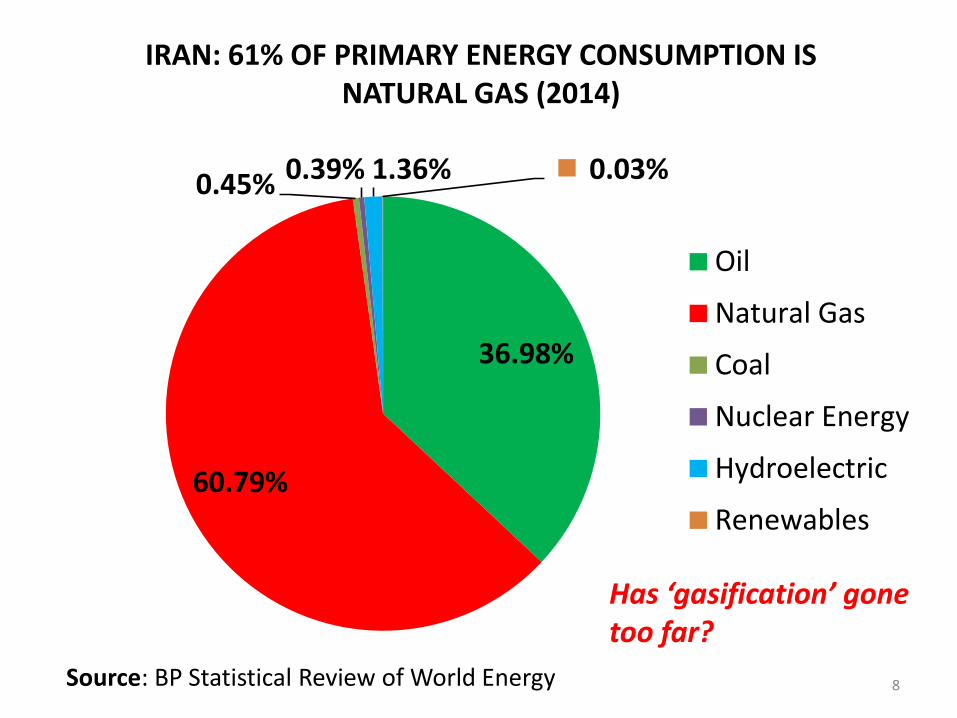

IRAN: 61% OF PRIMARY ENERGY CONSUMPTION IS NATURAL GAS (2014)

Source: BP Statistical Review of World Energy

36.98%

60.79%

0.45% 0.39% 1.36% 0.03%

Oil

Natural Gas

Coal

Nuclear Energy

Hydroelectric

Renewables

Has ‘gasification’ gone too far?

9

IRAN’S OIL & GAS PRODUCTION POTENTIAL

10

OIL RESERVES & PRODUCTION - 2015

0

2

4

6

8

10

12

0

50

100

150

200

250

300Ir

an

Iraq

Ku

wai

t

UA

E

Sau

di A

rab

ia

Om

an

Un

ited

Sta

tes

No

rway UK

Production Reserves

Billion barrels of remaining reserves

Million barrels per day of production

Source: Oil & Gas Journal

11

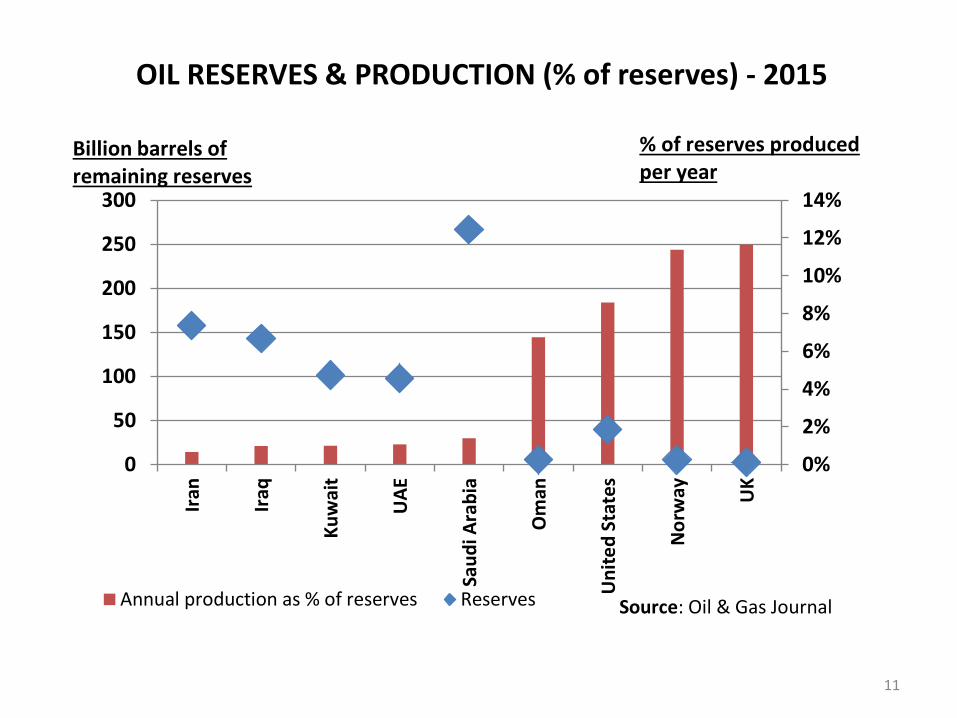

OIL RESERVES & PRODUCTION (% of reserves) - 2015

0%

2%

4%

6%

8%

10%

12%

14%

0

50

100

150

200

250

300Ir

an

Iraq

Ku

wai

t

UA

E

Sau

di A

rab

ia

Om

an

Un

ite

d S

tate

s

No

rway UK

Annual production as % of reserves Reserves

Billion barrels of remaining reserves

% of reserves producedper year

Source: Oil & Gas Journal

12

0

100

200

300

400

500

600

700

800

0

5

10

15

20

25

30

35

40

Turk

men

ista

n

Iran

Qat

ar

Russ

ian

Fede

ratio

n

Alge

ria US

Cana

da

Production

Reserves

Trillion cubic metres of remaining reserves

Billion cubic metres of production

Source: BP Statistical Review of World Energy

NATURAL GAS RESERVES & PRODUCTION - 2014

13

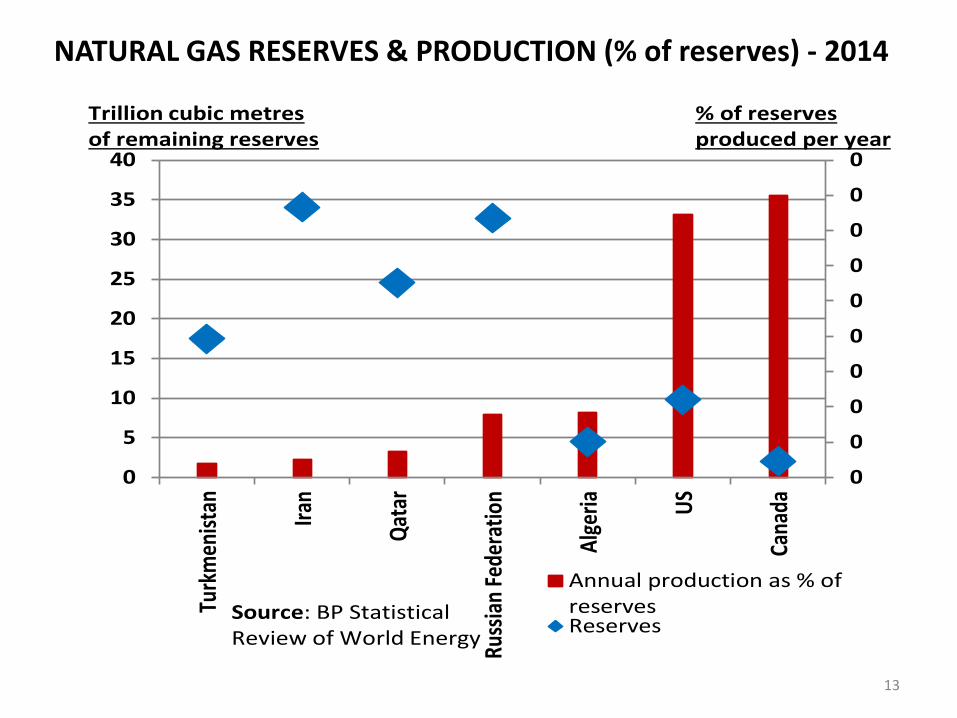

NATURAL GAS RESERVES & PRODUCTION (% of reserves) - 2014

0

0

0

0

0

0

0

0

0

0

0

5

10

15

20

25

30

35

40

Turk

men

ista

n

Iran

Qat

ar

Russ

ian

Fede

ratio

n

Alg

eria US

Cana

da

Annual production as % ofreservesReserves

Trillion cubic metres of remaining reserves

% of reserves produced per year

Source: BP Statistical Review of World Energy

14

HOLDERS OF HIGH RESERVES (including IRAN) PRODUCE AT RELATIVELY LOW RATES IN COMPARISON WITH HOLDERS OF

LOW RESERVES

IRAN HAS THE POTENTIAL TO INCREASE ITS OIL AND GAS PRODUCTION

15

IRAN OIL & GAS

SOME CHALLENGES

16

Example of an old field: Forties Field in the UK sector of the North Sea Discovered in 1970, first production 1975, reached 520 thousand barrels per day (tbpd) in 1978. By 2003 had produced more than 2 billion barrels and production had declined to 40 tbpd. BP estimated field decommissioning in 2013. Apache took over in 2003. In 2013 Forties was the second largest producing field (after Buzzard). Forties Field is expected to produce beyond 2030 (20 years longer than the 2003 estimate)

DEVELOPMENT WORK IN OLD FIELDS

17

Average well production 16,000 bpd (early 1970s) down to 2,000-3,000 bpd (recent). Remaining reserves of Iran’s old fields: about 30 billion barrels (cf. current reserves of Kazakhstan with 1.6 mbpd production) Efficient production of the old reserves requires systematic field/reservoir monitoring, detailed studies & analysis, implementation of IOR, EOR, ….e.g. expansion of gas injection. Development projects in old fields are profitable, but they are: capital-intensive and ‘expert-intensive’

IRAN’S OLD OIL/GAS FIELDS

18

‘The elderly need much greater medical care and treatment than the young’, especially those that did not pay attention to their health, diet and life style when they were young’! Most Iranian oil fields have fractured reservoirs with low permeability in the matrix and high production from the fractures; decades of ‘primary’ production (falling reservoir pressure, declining production and significant quantities of oil trapped in matrix blocks); years of NIOC / Consortium debate: water or gas injection!

EXAMPLE OF TECHNICAL CHALLENGES IN OLD FIELDS

19

Example: Haftkel, on stream 1928, peak production 200,000 bpd, had fallen to 14,000 bpd in 1976 when gas injection commenced; resulted in the expansion of the oil column, production rose to 34,000 bpd by the mid-1990s; estimated extra recoverable oil 500-600 million barrels (Saidi SPE 1996). However, an oil field gas-injection programme is a billion Dollar project and should not be blindly implemented in all Iranian oil fields. Detailed reservoir studies, proper monitoring and planning are necessary for each of the reservoirs in each of the fields and should also evaluate water-injection and other IOR/EOR methods. These projects are CAPITAL & EXPERT INTENSIVE!

GAS INJECTION INTO OIL FIELDS

20

Onshore: Aghajari (1939), Ahvaz (1961), Bibi Hakimeh (1964), Gachsaran (1941), Karanj (1965), Kupal (1971), Mansuri (1974), Marun (1966), Parsi (1966), Rag-e Safid (1966) & others. Offshore: Abuzar (1976), Dorud-Kharg (1964), Salman (1968) & others. (figures in brackets): year of first production

EXAMPLES OF OLD PRODUCING IRANIAN OIL FIELDS STILL HOLDING CONSIDERABLE RESERVES

21

The Islamic Republic of Iran has priority for developing cross-border fields. The preferred method of developing shared fields is unitisation, though many problems will be faced: Different (foreign) companies operating in the neighbouring country Different regulatory regimes on the two sides Political differences between governments Better chance for fields on the Iraqi border?

SHARED FIELDS

22

Some examples of fields shared with: Iraq: Azadegan, Danan, Dehloran, Khorramshahr, Naft Shahr, West Paydar, Yadavaran, Yaran Kuwait & Saudi Arabia: Arash, Esfandiar, Foruzan Oman: Hengam Qatar: South Pars The UAE: Salman, Nosrat

DEVELOPING OIL/GAS FIELDS SHARED WITH NEIGHBOURING COUNTRIES

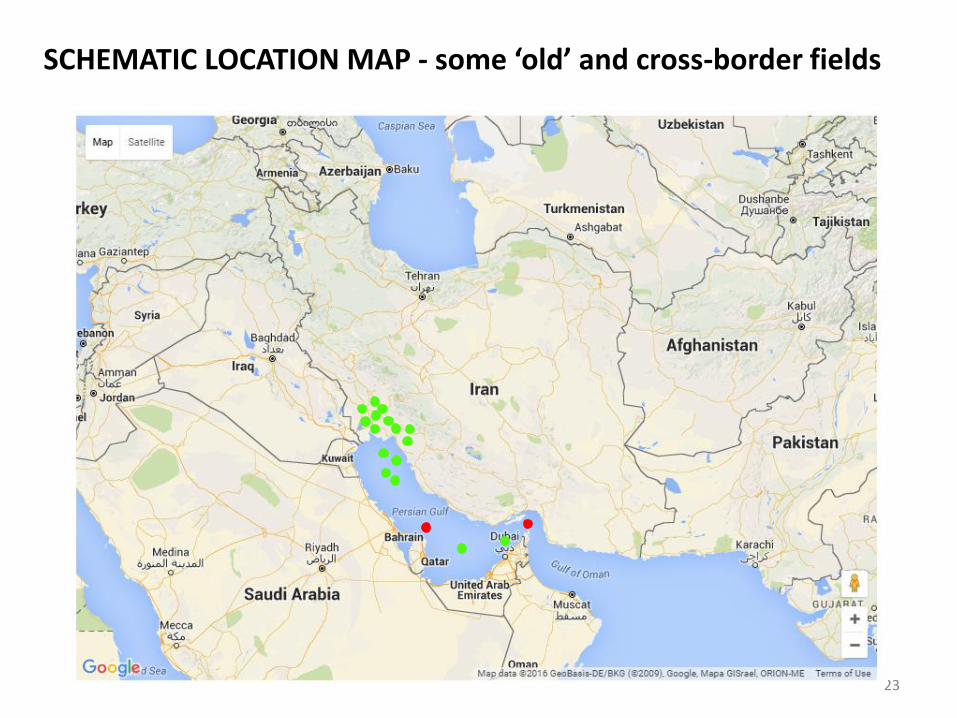

23

SCHEMATIC LOCATION MAP - some ‘old’ and cross-border fields

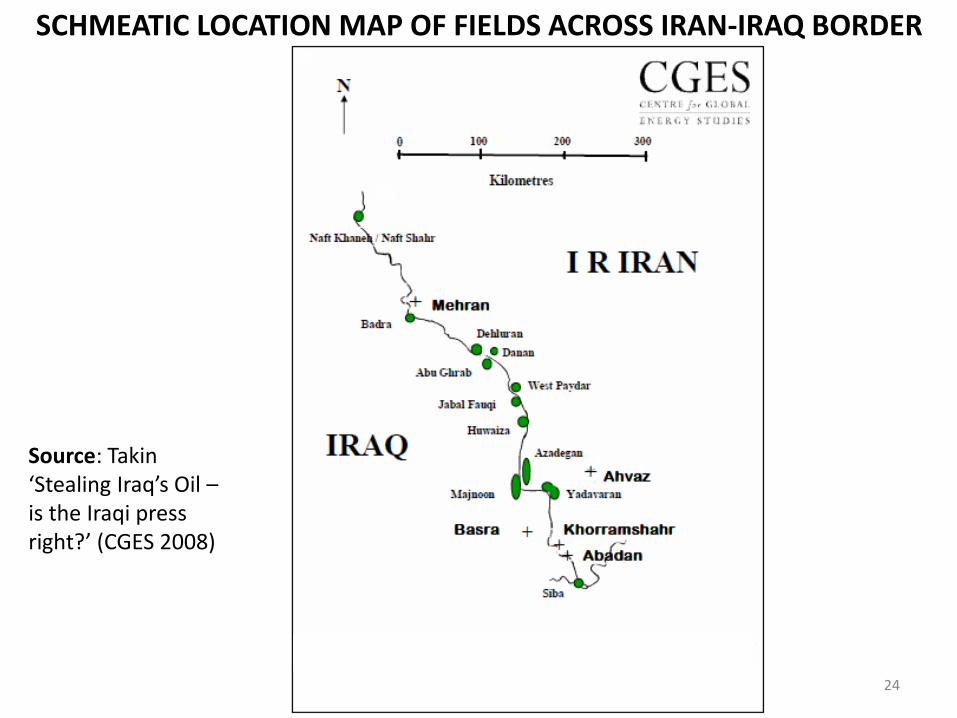

24

SCHMEATIC LOCATION MAP OF FIELDS ACROSS IRAN-IRAQ BORDER

Source: Takin ‘Stealing Iraq’s Oil – is the Iraqi press right?’ (CGES 2008)

25

Majnoon (on the Iraqi side): Several billion barrels of recoverable reserves, multi-reservoir field, requiring complex production systems and heavy investment. Foreign companies are Shell (operator) and Petronas. Operations started 2009, first export of oil 2014. Azadegan (on the Iranian side): We are far behind.

EXAMPLE OF A FIELD ON THE IRAQI BORDER

26

Has been under preparation since 2013. Is expected to be a major improvement on the former Buy-Back model. It is still to be finally approved. Already negotiations and provisional agreements are being made with international oil companies. More than 50 projects are said to be offered, investment requirements: $100-$300 bn

IRAN PETROLEUM CONTRACT (a new contract model)

27

In the Middle East and in Iran, public opinion is still strong about the excesses of the old ‘oil concessionaires’, their unfair practices, acting almost as ‘a state within the state’, influencing governments, etc. Foreign operators, their management and staff still face resentment. They should emphasise their professional responsibility, technical expertise, provision of capital, long-term commitment and the expectation of a ‘win-win’ outcome from their involvement in Iran.

LEGACIES FROM THE FORMER OIL CONCESSIONAIRES OPERATING IN THE MIDDLE EAST

28

Politicisation of Iranian hydrocarbon industry and repeated personnel changes since the Revolution Breaking the National Iranian Oil Company & ‘Privatisation’ Many sanctions still remain Finalisation of the new ‘Iran Petroleum Contract’

SOME OTHER CHALLENGES

29

THANK YOU FOR YOUR ATTENTION

Related Documents