International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network 115 PRICE FORECASTING FOR DAY – AHEAD ELECTRICITY MARKET USING RECURSIVE NEURAL NETWORK 1 N. SAI PAVN KUMAR, 2 B. SIVA NAGARAJU 1,2 Asst. Professor, EEE Department, G.V.R&S College of Engineering & Technology, Budampadu, Guntur (Dt) AP, India. E-mail: 1 [email protected], 2 [email protected] Abstract- Price forecasting has becomes a very valuable tool in the current upheaval of electricity market deregulation. It plays an important role in power system planning and operation, risk assessment and other decision making. This paper provides a method for predicting hourly prices in the day-ahead electricity marketusing Recursive Neural Network (RNN) technique, which is based on one output node, which uses the previous prediction as input for the subsequent forecasts. In this way, it is carried out recursively for twenty four steps to preict next 24 hour prices. Comparison of forecasting performance of the proposed RNN model with similar days along with other literature is presented. The proposed method is examined on the PJM electricity market. The result obtained through the simulation show that the proposed RNN model can provide efficient, accurate and better results. Index Terms- Electricity market, price forecasting, recursive neural networks, similar days. I. INTRODUCTION During the last two decades, the electric power industry around the world has undertaken significant restructuring. With the introduction of restructuring into the power industry, two major objectives remain same in establishing an electricity market. First one is ensuring a secured operation and second one is facilitating an economical operation. Security could be ensured by utilizing the diverse services available to market. The price of electricity has become the focus of all activities in the power market as price forecasting that plays a crucial role in establishing proper economical operation is still an issue. Electricity has its own complexities as it cannot be stored economically and is affected by power network limitation. Thus, the existing price forecasting methodology of other commodities cannot be utilized for electricity price forecasting methodology of other commodities cannot be utilized for electricity price forecasting. Many factors could impact the electricity price in which some factors are more dominant than others. Some of the factors are more dominant than others. Some of the factors considered in electricity price in literatures are: (a) Time (hour of the day, day of the week, month, year, and special days); (b) Reserve (historical and forecasted reserve); (c) price (historical price); (d) Load (historical and forecasted load). In general, the main factor driving the electricity price is power demand. In the USA, PJM Interconnection plays a vital role in the U.S, electric system and responsible for the operation of the largest centrally dispatched electric system in North America. The PJM market is co- ordinated byan independent system operator (ISO). The ISO ensures a secured, economical and efficient operation as well as determining all locational marginal price (LMP) according to voluntary bids and bilateral transactions. Forecasting these LMPs is essential in a deregulated market as it does not only give theimportant information that is helpful for the market participants to develop their bidding strategies, but also, if more accuracy in forecasting is obtained, it provides better risk management.In the PJM market, it is observed that daily power demand curves have similar patterns, whereas the daily LMP curves are fluctuating. There exists some abrupt changes in the LMP curves. The LMP and load values are low at night. The LMP and load values are low at night. The LMP values usually reach their peaks around 9 a.m. and 8 p.m. A lot of methods have been reported for price prediction of the electricity market, especially in the last decade. Some of these methods are basically the short-term load forecasting (STLF) methods. However, electricity prices are usually more volatile than hourly loads. Hence, the price prediction is more complex than the STLF. Methods based on time series or neural networks (NN) aremore common for electricity price forecasting due to their more flexibility and ease of implementation. Time series model, i.e., autoregressive integrated moving average (ARIMA), has been used to predict price in Spanish and Californian electricity markets. Nogales et al. have proposed time series models, including dynamic regression and linear transfer function models for short-term price forecasting. The main drawback of time-series model is that they are usually based on the hypothesis of stationarity; however, the price series violate this assumption. Another kind of time-series models like generalized Autoregressive Conditional Heteroskedastic (GARCH) and input-output Hidden Markov models (IOHMM) have been developed in order to solve the

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

115

PRICE FORECASTING FOR DAY – AHEAD ELECTRICITY MARKET USING RECURSIVE NEURAL NETWORK

1N. SAI PAVN KUMAR, 2B. SIVA NAGARAJU

1,2 Asst. Professor, EEE Department, G.V.R&S College of Engineering & Technology, Budampadu, Guntur (Dt) AP, India.

E-mail: [email protected], [email protected]

Abstract- Price forecasting has becomes a very valuable tool in the current upheaval of electricity market deregulation. It plays an important role in power system planning and operation, risk assessment and other decision making. This paper provides a method for predicting hourly prices in the day-ahead electricity marketusing Recursive Neural Network (RNN) technique, which is based on one output node, which uses the previous prediction as input for the subsequent forecasts. In this way, it is carried out recursively for twenty four steps to preict next 24 hour prices. Comparison of forecasting performance of the proposed RNN model with similar days along with other literature is presented. The proposed method is examined on the PJM electricity market. The result obtained through the simulation show that the proposed RNN model can provide efficient, accurate and better results. Index Terms- Electricity market, price forecasting, recursive neural networks, similar days. I. INTRODUCTION During the last two decades, the electric power industry around the world has undertaken significant restructuring. With the introduction of restructuring into the power industry, two major objectives remain same in establishing an electricity market. First one is ensuring a secured operation and second one is facilitating an economical operation. Security could be ensured by utilizing the diverse services available to market. The price of electricity has become the focus of all activities in the power market as price forecasting that plays a crucial role in establishing proper economical operation is still an issue. Electricity has its own complexities as it cannot be stored economically and is affected by power network limitation. Thus, the existing price forecasting methodology of other commodities cannot be utilized for electricity price forecasting methodology of other commodities cannot be utilized for electricity price forecasting. Many factors could impact the electricity price in which some factors are more dominant than others. Some of the factors are more dominant than others. Some of the factors considered in electricity price in literatures are: (a) Time (hour of the day, day of the week, month, year, and special days); (b) Reserve (historical and forecasted reserve); (c) price (historical price); (d) Load (historical and forecasted load). In general, the main factor driving the electricity price is power demand. In the USA, PJM Interconnection plays a vital role in the U.S, electric system and responsible for the operation of the largest centrally dispatched electric system in North America. The PJM market is co-ordinated byan independent system operator (ISO). The ISO ensures a secured, economical and efficient

operation as well as determining all locational marginal price (LMP) according to voluntary bids and bilateral transactions. Forecasting these LMPs is essential in a deregulated market as it does not only give theimportant information that is helpful for the market participants to develop their bidding strategies, but also, if more accuracy in forecasting is obtained, it provides better risk management.In the PJM market, it is observed that daily power demand curves have similar patterns, whereas the daily LMP curves are fluctuating. There exists some abrupt changes in the LMP curves. The LMP and load values are low at night. The LMP and load values are low at night. The LMP values usually reach their peaks around 9 a.m. and 8 p.m. A lot of methods have been reported for price prediction of the electricity market, especially in the last decade. Some of these methods are basically the short-term load forecasting (STLF) methods. However, electricity prices are usually more volatile than hourly loads. Hence, the price prediction is more complex than the STLF. Methods based on time series or neural networks (NN) aremore common for electricity price forecasting due to their more flexibility and ease of implementation. Time series model, i.e., autoregressive integrated moving average (ARIMA), has been used to predict price in Spanish and Californian electricity markets. Nogales et al. have proposed time series models, including dynamic regression and linear transfer function models for short-term price forecasting. The main drawback of time-series model is that they are usually based on the hypothesis of stationarity; however, the price series violate this assumption. Another kind of time-series models like generalized Autoregressive Conditional Heteroskedastic (GARCH) and input-output Hidden Markov models (IOHMM) have been developed in order to solve the

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

116

above problem. However, their application to electricity price prediction encounters difficulty. A rapid variation in load can have a sudden impact on the hourly price. The time-series techniques are successful in the areas where the frequency of the data is low, such as weekly patterns, but they can be problematic when there are rapid variations and high-frequency changes of the target signal. Hence, there is a need of more efficient forecast tool capable of learning complex and non-linear relationships that are difficult to model with conventional techniques. In recent years, forecasting method based on artificial intelligence techniques have been reported in many papers, and especially, NNs have received much attention as they provide good solutions to model complex non-linear relationships much better than the traditional linear models. NNs were used for solving the short-term loadforecast problems. NNs were also used to forecast system marginal price, market clearing price (MCP). Szkutaet al. proposed a three layered feed-forward NN for short term price forecasting in the Victorian Electricity market Rodrigucz and Anders proposed back propagation (BP) NN with one hidden layer and one output layer and Neuro Fuzzy system for predicting hourly MCP in the Ontario energy market, where the latter showed better forecasting accuracy than the former. Doulai and Cahill have proposed fully connected multi layer perception (MLP) neural network for forecasting electricity price in Australian electricity market (New South Wales). Hong and Hsiao have proposed recurrent neural network structure to forecast LMP in the PJM electricity market. In this paper, new approach is proposed to forecast hourly electricity prices in the PJM day-ahead market using Recursive Neural Network (RNN), which is based on similar days method. RNN is a multi-step approach based on one output node, forecasting price a single step ahead (t+1), and the network is applied recursively using the previous prediction as input for the subsequent forecasts. In this way, it is carried out recursively for twenty four steps to predict next 24 hour electricity prices. RNN used input data obtained by averaging selected number of similar price days corresponding to forecast day, i.e., two procedures are analyzed: (a) forecasting based on averaging prices of similar days and (b) forecasting based on averaging prices of similar days plus RNN refinement. The advantages of the proposed price forecasting technique with respect to other techniques reported in the technical literatures are; better accuracy; simplified neural network with lesser number of inputs; good in volatility cases; and performs well for multiple seasons. This paper contributes to forecast electricity prices in the day-ahead electricity market using RNN. The main contribution of this paper lies in the choice of

some input factors based on similar days technique for better accuracy and simplified neural network. To evaluate the performance of the proposed RNN model, mean absolute percentage error (MAPE) and forecast mean square error (FMSE) are calculated. These values show that the proposed RNN model is capable of forecasting electricityprice efficiently and accurately for any day of the week. The rest of the paper is organized as follows. Section II described price forecasting based on similar days method. The proposed recursive neural network architecture is presented in section III, which is followed by results and discussion in section IV. Section V concludes the paper.

Price Prediction Based On Similar Days Method According to similarday’s method, we select similar price days corresponding to forecast day based on Euclidean norm. Euclidean norm with weighted factors are used in order to evaluate the similarity between forecast day and searched previous days. The evaluation determined by the Euclidean norm makes us understand the similarity by using an expression based on the concept of norm. smaller the Euclidean, better the evaluation of similar days. Selection of similar price days is described below. A. Selection of Similar Price Days In general, the main variable that drives the price is the demand. To minimize the number of input data, while maximizing the accuracy of the proposed algorithm, authors did comprehensive statistical analysis of historical data. It wasobserved that load and price at same hour and previous hour are appropriate input to find similar days based on correlation analysis. Fig. 1 shows the relationship between load and price, which is simply an example to show the correlation between demand and price for the period January-May, 2006. Correlation coefficient of determination (R2) value is obtained as 0.6744, and correlation coefficient ® of 0.822 is reasonable topredict electricity price. Note that correlation coefficient is with approximate curve fitting of third degree equation. Hence, load is a natural choice as a parameter to be used to predict electricity price. Other factors such as transmission line congestion, generator availability, generator bidding strategy on

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

117

the generation side, outages, spinning reserves, etc. have also impact on electricity price. The only explicative variable that has been considered in this study is the power demand. Explicative variable data (temperature, hydro resources, equipment outages, etc) for day d, if available, can be easily and fruitfully included in the model presented, Note, unit outage information is generally not available to all market agents. Note also that the effect of temperature is embodied in the demand forecasts. Nevertheless, for the sake of simplicity of our built-in-house C-programming, explicative variables other than demand have not been included in this study. However, these aspects would be explored in our future work. In general, the following equation is used as Euclidean norm with weighted factors for the selection of similar price days: Fig. 2 Time framework for the selection of similar days corresponding to forecast day. ||D|| = (1) Where

2 (2)

2 (3) 2 (4)

2 (5)

(6)

(7)

(8)

(9) Where and are load and price on forecast day

and are load and price on similar day in past,

respectively. is the load deviation between

forecast day and similar day; is the price deviation between forecast day and similar day;

is the deviation of price at (t-1) on forecast day and similar day. The weighted factor is determined by using least square method based on regression model that is constructed by using historical load and price data. In our previous work, only three variables (load at same hour, price at same and previous hour) have been considered in Euclidean norm equation, whereas in the current study, load at previous hour has also been considered as shown in (1). Accordingly, regression model has been created and then simplified. Error was calculated based on difference of regression analysis based predicted value and actual value. Least cost square method was used to minimize this error. Detail of regression model can be found in reference.

Therefore, a selection of similar price days that considers a trend of price and load is performed. The above equations give the hourly calculation of Euclidean norm. Equation (1) is a very important equation for the selection of similar price days based on historical data. Combining weighted factor obtained with regression model in Euclidean norm improved the performance of similar days method and Euclidean norm equation finally evolved as given in (1). The time frame work for the selection of similar price days corresponding to forecast day is shown in Fig.2. The past 30 days from the day before a forecast day, and past 30 days before and after the forecast day in the previous year are considered for the selection of similar days. If the forecast day is changed, similar days are selected in the same manner. We select similar price days by calculating ||D|| (Euclidean norm) from (1). Price data of similar days at time

Are obtained from (1) and assumed to be

forecasted price. Then, it is assume to be actual price and selected similar price day at . II. PROPOSED RECURSIVE NEURAL NETWORK ARCHITECTURE Neural network are a class of flexible non-linear models that can discover patterns adaptively from the data. Theoretically, it has been shown that given an appropriate number of non-linear processing units, NN can learn from experience and estimate any complex functional relationship with high accuracy. In power systems, NNs have been used to solve problems such as load forecasting, component and system fault diagnosis, security assessment, unit commitment, etc. in price forecasting applications, the main function of NN is to predict Price for the next half-hour, hour(s), day(s) or week(s). Although many types of NN models have been reported in Papers, the most popular one for price forecasting is the feed forward model.In this paper, we propose a typical three-layer feed-forward model, recursive neural network, for forecasting the next 24h Electricity prices. The architecture of the proposed RNN is illustrated schematically in Fig.3. The network model is Composed of one input layer, one hidden layer, and one output layer. The input variable of the proposed RNN structure for price forecasting as shown in Fig.3 are meansimilar days price data , which is an average of 5 similar price days; actual hourly price ; actual hourly load

. Since RNN is a multistep approach based on one output node, price is forecasted a single step ahead

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

118

to obtain , and the network is applied recursively using the previous prediction as input for the subsequent forecasts. For the price forecast of the lead time of second step to obtain as

shown in Fig.3, the input to RNN-2 are: , and

, where is the forecasted load for next hour and this paper assumes that forecasted values are available; is similar price day data. In this way, it is carried out recursively for twenty four steps to predict next 24th prices. In the proposed price prediction method, we forecast hourly prices by using RNN (Fig.3) to modify the price curve obtained by averaging 5 similar price days corresponding to forecast day, i.e., NN corrects the output obtained from the similar days approach. Hence, in this paper, the prices based on several selected similar days are averaged in order to improve the accuracy of price forecasting. The proposed neural network uses the nominal values of load and price as learning data. A. Back-Propagation Training Algorithm for

RNN

In this paper, the proposed NN uses the back-propagation (BP) training algorithm. In the Fig.3 Proposed recursive neural network model for price forecasting. General, the error at the output layer in the BP model propagates backward to the input layer through the

hidden layer in the network to obtain the final desired output. The steepest gradient descent method is utilized to calculate the weight of the network and adjusts the weight of interconnections to minimize the output error. The error minimization process is repeated until the error converges to a predefined small value. The error function at the output neuron is defined as.

2 (10)

Where and represent the target and actual values of output neuron, k, respectively. In training, the network learn by adjusting the weights connecting the input and hidden layer and the weights connecting the hidden and output, by the gradient multiplied by the learning rate parameter. The correction applied to the synaptic weight at iteration n is defined by the deltarule.

(11)

Where η is a constant that determines the rate of learning. It is called learning rate parameter of the BP algorithm, denotes the synaptic weight connecting the output of neuron i to the input of neuron j at iteration n; is the local gradient. The learning rate is the proportion of error gradient by which the weights are adjusted. Large value of η can give a faster convergence to the gradient minimum but may produce oscillation around the minimum. Hence, in order to accelerate the learning process and yet avoiding the danger of instability, we modify (11) by including a momentum term as shown by

(12) Where is usually a positive numbercalled the momentum constant. The momentum determines the proportion of the change of past weights that is used in the calculation of new weights. Both and η affect the error gradient minimization process. In this paper, the proposed neural network is trained by using the data of past 45 days from the day before the forecast day, and past 45 days before and after the forecast day in the previous year, i.e., total available learning days are 135 days. If the forecast time is changed, neural network is retrained to obtain the relationship between ‘load and price’ around the forecast day. B. Design Of Network The proposed neural network structure as shown in Fig.3 consists of three layers; an input layer, one hidden layer and an output layer. In the present work,

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

119

sigmoid function has been used as the activation function. The hiddenlayer and neurons play very important roles for many successful applications of neural networks. It is the neurons in the hidden layer that allow neural networks to detect the feature, to capture the pattern in the data, and to perform complicated nonlinear mapping between input and output variables. It has been proved that only one layer of hidden units is sufficient for NNs to approximate any complex nonlinear function with any desired accuracy. In this paper, 2n+1 hidden neurons are chosen for better forecasting accuracy, where n is the number of input nodes. The network is trained by repeating the BP learning set for 1500 times. For the proposed neural network, the values for learning rate (η) and momentum () are chosen as 0.8 and 0.1, respectively. III. RESULTS AND DISCUSSION This paper focuses on price prediction technique based on averaging the prices of similar days and refining the results through recursive neural network procedure. The proposed recursive neural network model has been applied to predict electricity prices of day-ahead PJM electricity market. Extensive testing has been carried out using data during January 2004-may 2006 derived from the PJM electricity market. Sets of data include hourly price and load data. One day per month (January-May) of year 2006 is studied to validate the performance of the proposed RNN model. Weekdays and weekends are selected for daily forecasts. To evaluate the performance of the proposed model, the most widely used mean absolute percentage error (MAPE) is adopted in this paper. However, when used in its present form for electricity price forecasting, MAPE could create errors because of the perceived behavior of electricity price. For example, the price of electricity is too volatile. It can rise to tens of or even hundreds of times its normal value during some periods, or drop to zero and even to negative values in other periods. Accordingly, MAPE could reach the extreme values in those cases. Hence, to avoid this adverse effect, the following MAPE definition has been used.

(13)

(14)

Where is the actual price, is the predicted

price, N is the number of data points, and is the average true price. Fig. 4-8 show the comparison of forecast prices obtained from similar days (SD)

method and the proposed recursive neural network (RNN) model with actual price.

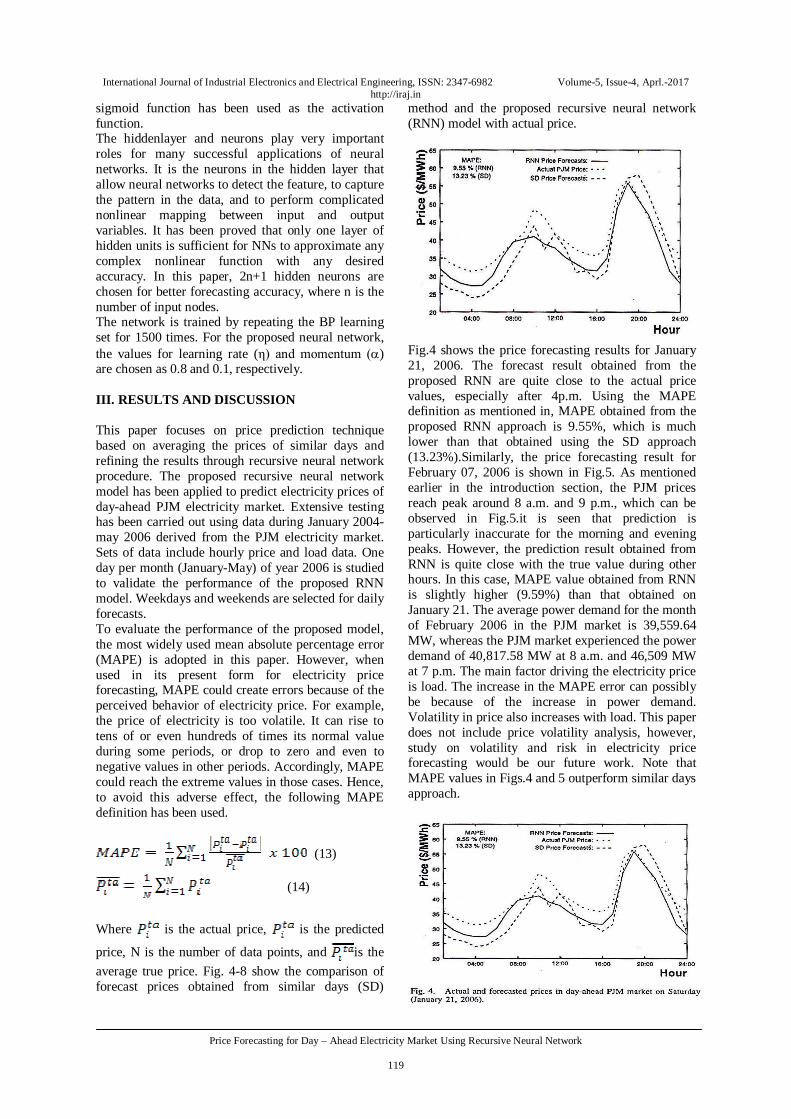

Fig.4 shows the price forecasting results for January 21, 2006. The forecast result obtained from the proposed RNN are quite close to the actual price values, especially after 4p.m. Using the MAPE definition as mentioned in, MAPE obtained from the proposed RNN approach is 9.55%, which is much lower than that obtained using the SD approach (13.23%).Similarly, the price forecasting result for February 07, 2006 is shown in Fig.5. As mentioned earlier in the introduction section, the PJM prices reach peak around 8 a.m. and 9 p.m., which can be observed in Fig.5.it is seen that prediction is particularly inaccurate for the morning and evening peaks. However, the prediction result obtained from RNN is quite close with the true value during other hours. In this case, MAPE value obtained from RNN is slightly higher (9.59%) than that obtained on January 21. The average power demand for the month of February 2006 in the PJM market is 39,559.64 MW, whereas the PJM market experienced the power demand of 40,817.58 MW at 8 a.m. and 46,509 MW at 7 p.m. The main factor driving the electricity price is load. The increase in the MAPE error can possibly be because of the increase in power demand. Volatility in price also increases with load. This paper does not include price volatility analysis, however, study on volatility and risk in electricity price forecasting would be our future work. Note that MAPE values in Figs.4 and 5 outperform similar days approach.

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

120

Fig.6 corresponds to weekend in March with forecast prices computed using SD method and the proposed RNN model. The forecast results obtained from the proposed RNN are quite close to the actual values. Using the MAPE definition as mentioned in, the prediction behavior of the proposed RNN technique for this day is very appropriate with a daily MAPE error of only 6.24%, which is lower than that obtained using the similar days (SD) approach (8.14%).

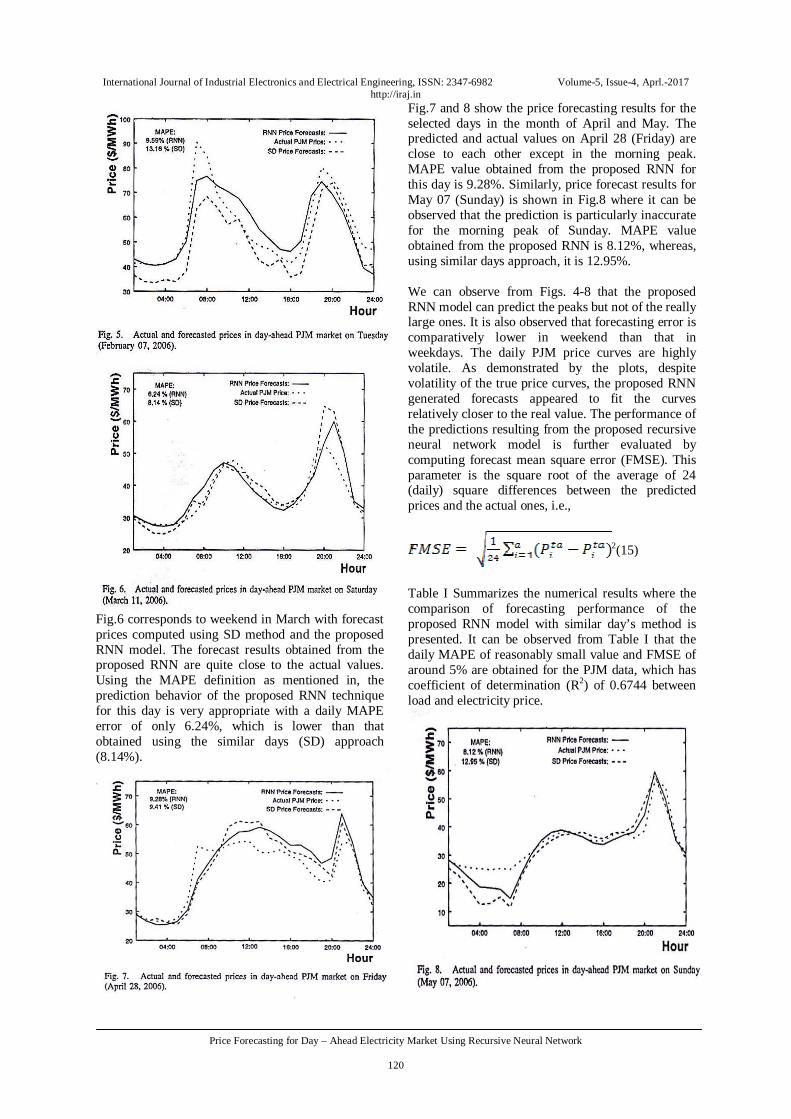

Fig.7 and 8 show the price forecasting results for the selected days in the month of April and May. The predicted and actual values on April 28 (Friday) are close to each other except in the morning peak. MAPE value obtained from the proposed RNN for this day is 9.28%. Similarly, price forecast results for May 07 (Sunday) is shown in Fig.8 where it can be observed that the prediction is particularly inaccurate for the morning peak of Sunday. MAPE value obtained from the proposed RNN is 8.12%, whereas, using similar days approach, it is 12.95%. We can observe from Figs. 4-8 that the proposed RNN model can predict the peaks but not of the really large ones. It is also observed that forecasting error is comparatively lower in weekend than that in weekdays. The daily PJM price curves are highly volatile. As demonstrated by the plots, despite volatility of the true price curves, the proposed RNN generated forecasts appeared to fit the curves relatively closer to the real value. The performance of the predictions resulting from the proposed recursive neural network model is further evaluated by computing forecast mean square error (FMSE). This parameter is the square root of the average of 24 (daily) square differences between the predicted prices and the actual ones, i.e.,

2(15)

Table I Summarizes the numerical results where the comparison of forecasting performance of the proposed RNN model with similar day’s method is presented. It can be observed from Table I that the daily MAPE of reasonably small value and FMSE of around 5% are obtained for the PJM data, which has coefficient of determination (R2) of 0.6744 between load and electricity price.

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

121

Furthermore, in order to show the effectiveness of the proposed Recursive NN model, the proposed price prediction

Table – I. Comparison of forecasting performance of the

proposedRecursive NN with similar Days Method.

Table II. Comparison of forecasting performance of the performance of the proposed Recursive NN model with other method based on

NN.

Method is compared with reference where the authors have proposed multilayer perceptron with one hidden layer neural network along with other statistical methods for forecasting electricity prices of the PJM market and same MAPE definition has been used. It can be seen from Table II that the MAPE values obtained for the weekday (February) in reference range from 6.08% - 14.07%, whereas in the current study, MAPE value is around 9% for the weekday. Similarly, for the weekend (May), the MAPE value obtained in our study is much lower (8%) than that obtained in their study. Hence, the proposed RNN method compare favorably well with their approach in weekend and weekday. This paper contributes to solve an important problem of electricity price forecasting in which the authors have proposed a technique based on recursive NN model with applying similar days approach to forecast electricity price in day-ahead PJM market. Weekdays and weekends are selected for daily

forecasts and the obtained test results show that the proposed algorithm could provide a considerable improvement of the forecasting accuracy for any day of the week very well. CONCLUSIONS This paper has proposed a technique based on Recursive Neural Network (RNN) and similar days approach to forecast hourly prices in the PJM electricity market. RNN is a multistep approach based on one output node, forecasting price a single step ahead (t+1), and the network is applied recursively using the previous predication as input for the subsequent forecasts. In this way, it is carried out recursively for twenty four steps to predict next 24 hour prices. Appropriate examples based on data pertaining to the PJM electricity were used to demonstrate the functioning of the proposed RNN method based on similar days approach. According to which, the price curves are forecasted by using the information of the days being similar to that of the forecast day. Two procedures were analyzed, i.e., prediction based on averaging the prices of similar days, and prediction based on averaging the prices of similar days plus neural network refinement. The price forecasting results obtained from the proposed RNN outperforms the direct use of similar days approach. The factors impacting electricity price forecasting, including time factors demand factors and historical price factor are discussed. It is confirmed that the demand is the most important variable influencing the electricity price. For the selected days, daily MAPE values obtained from the proposed RNN model are acceptable taking into account the complex time series nature of electricity price data in the highly volatile PJM market. In the PJM market, the main challenging issue is that the daily PJM price curves are highly volatile and the proposed algorithm could solve the volatility problem very well as the fest results obtained through the simulation demonstrate the efficiency, accuracy, and high adequacy of the proposed technique. REFERENCES

[1] S. Stoft. Power System Economics: Designing Market for Electricity. John Wiley & Sons Inc., New York, 2002.

[2] H.Y. Yamini, S. M. Shahidehpour, and Z.Li, “Adaptive short-term electricity price forecasting using artificial neural networks in the restructured power markets”, Electrical power and energy Systems, vol.26, pp. 571-581, 2004.

[3] N. Amjady, “Day – ahead price forecasting of electricity markets by a new fuzzy neural network,” IEEE Trans, on Power Syst., vol. 21, no.2, pp. 887 -896, May 2006.

[4] C.P. Rodriguez and G.J. Anders, “Energy Price forecasting in the Ontario competitive power system

International Journal of Industrial Electronics and Electrical Engineering, ISSN: 2347-6982 Volume-5, Issue-4, Aprl.-2017 http://iraj.in

Price Forecasting for Day – Ahead Electricity Market Using Recursive Neural Network

122

market”, IEEE Trans, on Power Syst., vol.19, no.3, pp. 366-374, Feb. 2004.

[5] PJM Web Site, http://www.pjm.com, Active March 2006.

[6] M. Shahidehpour. H. Yamin, and Z.Li, Market operations in electric power systems: forecasting, scheduling, and risk assessment, John Wiley & Sons, Inc., New York, 2002.

[7] Y.Y. Hong, C.Y.Hsiao, “Locational marginal price forecasting in deregulated electricity Markets using artificial intelligence,” IEE ProcGener. Transm. Distrib. Vol.149, no.5, pp. 621-626, Sept.2002.

[8] J. Contreras, R. Espinola,F.. Nogales, and A..Conejo, “ARIMA models to predict next-day electricity prices,” IEEE Trans. On Power Syst., vol.18, no. 3, pp. 1014-1020, Aug. 2003.

[9] F.J. Nogales, J. Contreras, A.J. Conejo, and R. Espinola, “Forecasting next-day electricity prices by Time Series Model”, IEEE Trans, on Power Syst., vol. 17, no.2, pp. 342 – 348, Aug. 2002.

[10] R.C. Garcia, J. Contreras, M. Akkeren, and J.C. Garcia, “A GARCH forecasting model to predict day-ahead electricity Prices,” IEEE Trans. On power Syst. Vol. 20, no.2 pp. 867-874, 2005.

[11] A.M. Gonzalez, A.M.S. Roque, J. Gargia-Gonzalez, “Modeling models”, IEEE Trans. On power syst. vo. 20, no.1, pp. 13-24, 2005.

[12] S. Haykin, Neural network: A comprehensive foundation. Macmillan College Publishing Company, Inc., 1994.

[13] P. Mandal, T. Senjyu, and T.Funabashi, “Neural networks approach to forecast several hour ahead electricity prices and loads in deregulated market”, Energy Conversion and Management, vol.47, Issues 15-16, pp. 2128-2142, Sept. 2006.

[14] B.R. Szkuta, L.A. Sanabria, and T.S.Dillon, “Electricity price shorttermforecasting using ANN,” IEEE Trans. On Power Syst., vol.14, no.3, pp. 851-857, Aug. 1999

[15] M. Biaqnchini, M. Maggini, L. Sarti, and F. Scarselli, “Recursive neural networks for processing graphs with labeled edges: theory and applications,” Neural Networks, vol.18, Issue 8, PP. 1040-1050, Oct. 2005.

[16] H.S. Hippert, C.E. Pedreira, and R.C. Souza, “Neural networks for short-term load forecasting: A review and evaluation,” IEEE Trans. On Power Syst., vol.16,no.1, pp. 44-55, 2001.

[17] T. Senjyu, P. Mandal, K. Uezato, and T. Funabashi, “Next day load curve forecasting using hybrid correction method,” IEEE Trans. On Power syst., vol. 20,no. 1, pp. 102-109, 2005.

[18] T. Senjyu, P. Mandal, K. Uezato, and T. Funabashi, “Next day load curve forecasting using recurrent neural network structure,” IEEE Proc,-Gener, Transm. Distrib., vol.151, no.3,pp.388-394, may 2004.

[19] E. Ni and P.B. Luh, “Forecasting power market cleaning price and its discrete PDF using a Bayesian-based classification method”, IEEEPES winter meeting, vol. 3, pp. 1518-1523,Colombus, OH, USA, 2001.

[20] F. Gao, X.Guan X.R. Cao, and A, Papalexopoulos, “Forecasting power market cleaning price and quantity thing a neural network”, IEEE PES summer meeting, vol.4, pp.2138-2188, Seattle, WA, 2000.

[21] A.J. Conejo, J. Contreras, R. Espinola, and M.A. Plazas, “Forecasting electricity prices for a day-ahead pool-based electric energy market”, Int. Journal of forecasting. Vol. 21, no.pp.435-462, 2005.

[22] P. Doulai and W. Cahill, “Short-term price forecasting in electricity energy market,” In Proceedings of the international power engineering Conference (IPEC2001). PP.749-754, May 17-19, 2001.

Related Documents