Internet Of things And the Insurance industry Suman Chatterjee, PGPM1114, Roll: 127

Io t and the insurance industry suman chatterjee-pgpm1114-127

Aug 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Internet Of thingsAnd the Insurance industry

Suman Chatterjee,PGPM1114, Roll: 127

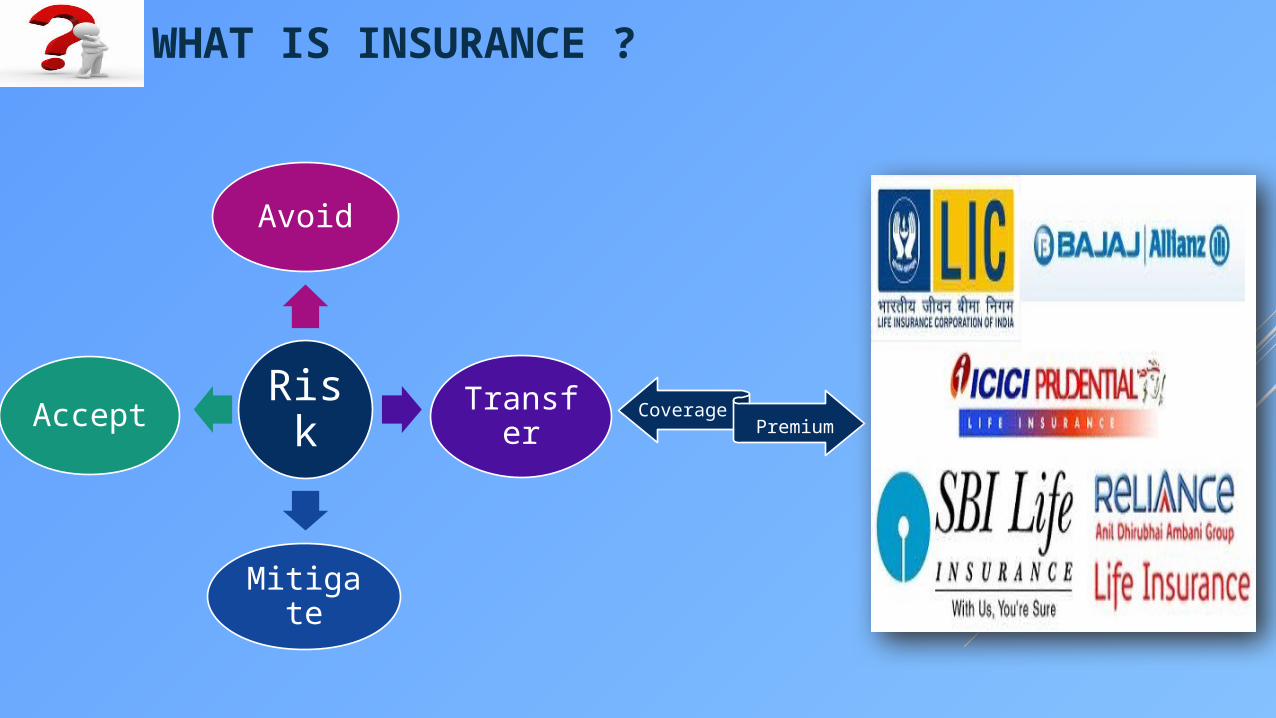

WHAT IS INSURANCE ?

Risk

Avoid

Transfer

Mitigate

Accept CoveragePremium

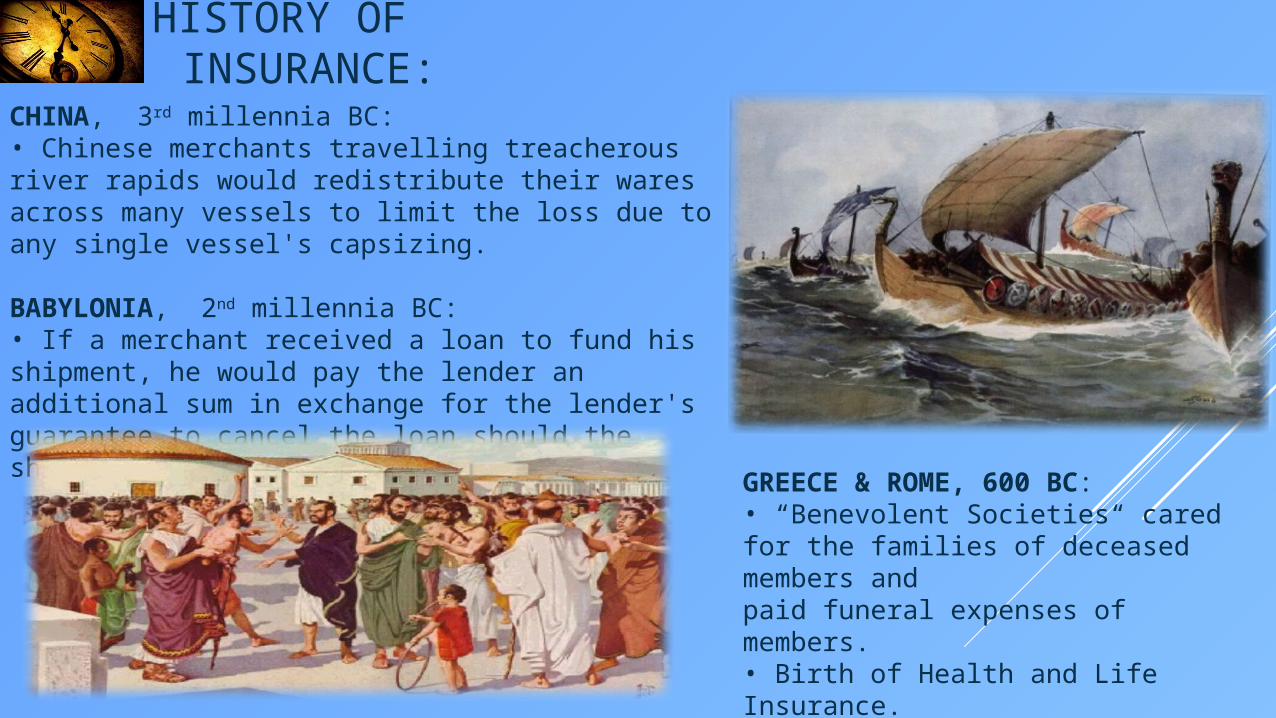

HISTORY OF INSURANCE:

CHINA, 3rd millennia BC:• Chinese merchants travelling treacherous river rapids would redistribute their wares across many vessels to limit the loss due to any single vessel's capsizing.

BABYLONIA, 2nd millennia BC:• If a merchant received a loan to fund his shipment, he would pay the lender an additional sum in exchange for the lender's guarantee to cancel the loan should the shipment be stolen or lost at sea.

GREECE & ROME, 600 BC:• “Benevolent Societies“ cared for the families of deceased members and paid funeral expenses of members.• Birth of Health and Life Insurance.

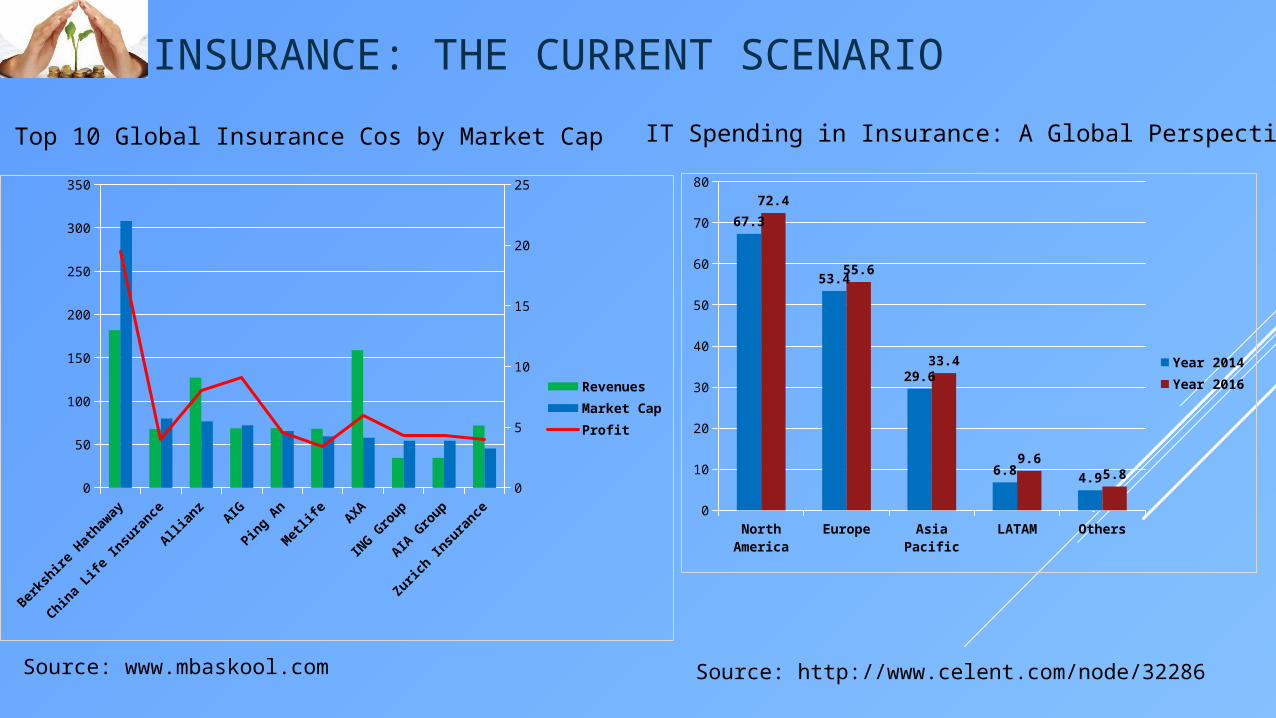

INSURANCE: THE CURRENT SCENARIO

Berks

hire

Hat

haway

China

Life

Insu

ranc

e

Allian

zAIG

Ping

An

Met

life

AXA

ING G

roup

AIA G

roup

Zuric

h In

sura

nce

0

50

100

150

200

250

300

350

0

5

10

15

20

25

RevenuesMarket CapProfit

Source: www.mbaskool.com

North America

Europe Asia Pacific

LATAM Others0

10

20

30

40

50

60

70

80

67.3

53.4

29.6

6.84.9

72.4

55.6

33.4

9.65.8

Year 2014Year 2016

Source: http://www.celent.com/node/32286

Top 10 Global Insurance Cos by Market Cap IT Spending in Insurance: A Global Perspective

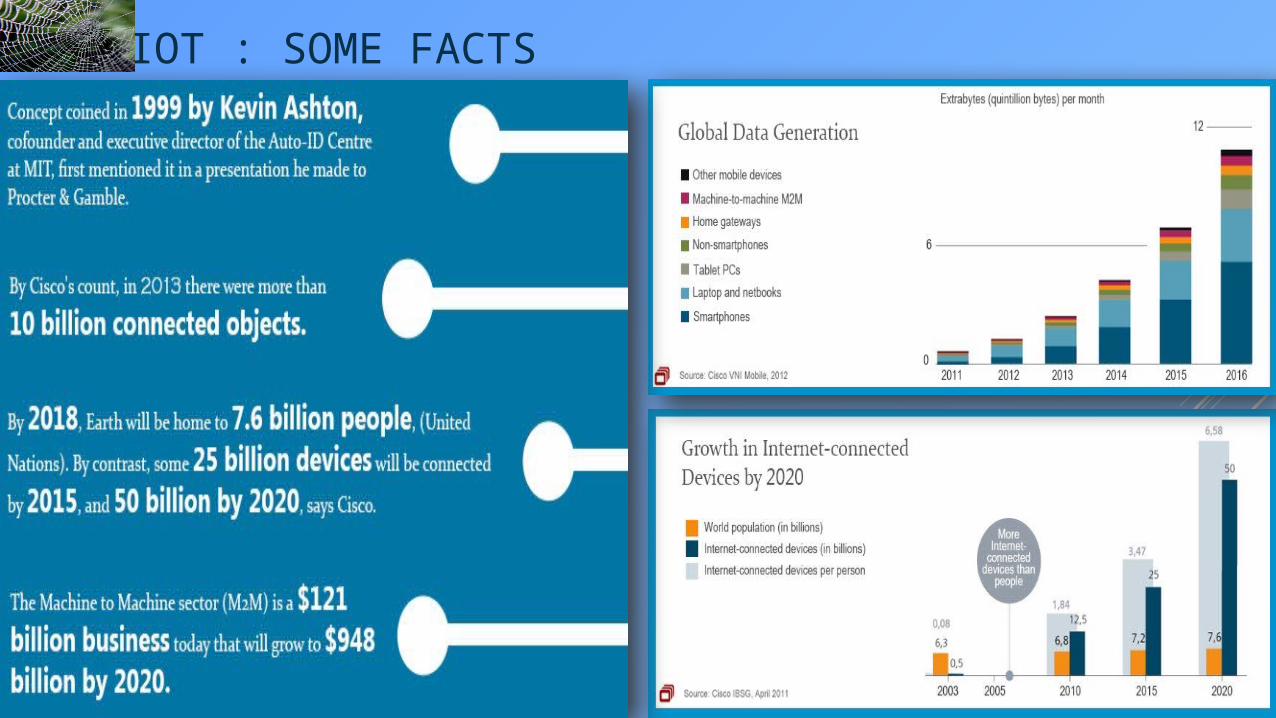

IOT : SOME FACTS

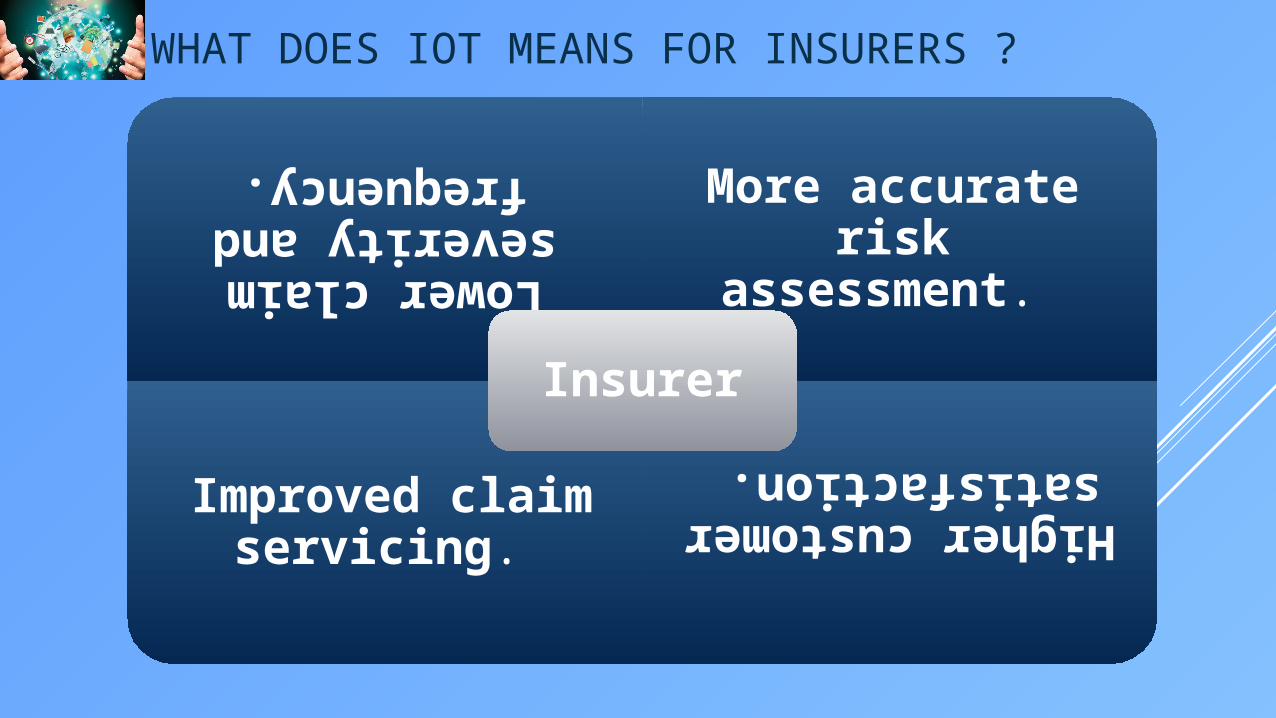

WHAT DOES IOT MEANS FOR INSURERS ?

Lower

claim sever

ity and

frequency.

More accurate risk assessment.

Improved claim servicing.

Higher

customer

satisfaction. Insurer

Continuous monitoring of Risk. Change in any lifestyle event like marital status or occupation will be reflected in policy premium.

IoT wearable devices capture significant measures, like heartbeat, temperature, blood sugar, exercise duration and report them to insurers.

LIFE AND HEALTH INSURANCE

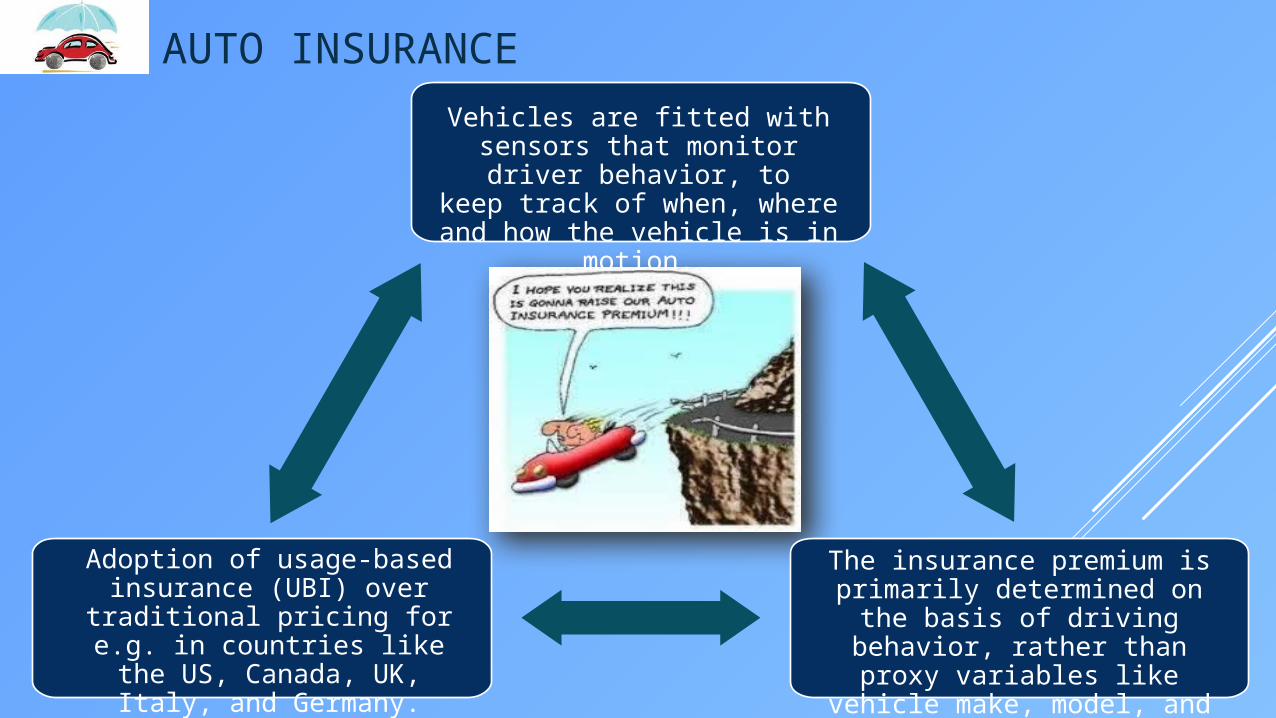

AUTO INSURANCE

Vehicles are fitted with sensors that monitor driver behavior, to keep track of when, where and how the vehicle is in motion.

The insurance premium is primarily determined on the

basis of driving behavior, rather than proxy variables like vehicle make, model, and year.

Adoption of usage-based insurance (UBI) over

traditional pricing for e.g. in countries like the US, Canada, UK, Italy, and

Germany.

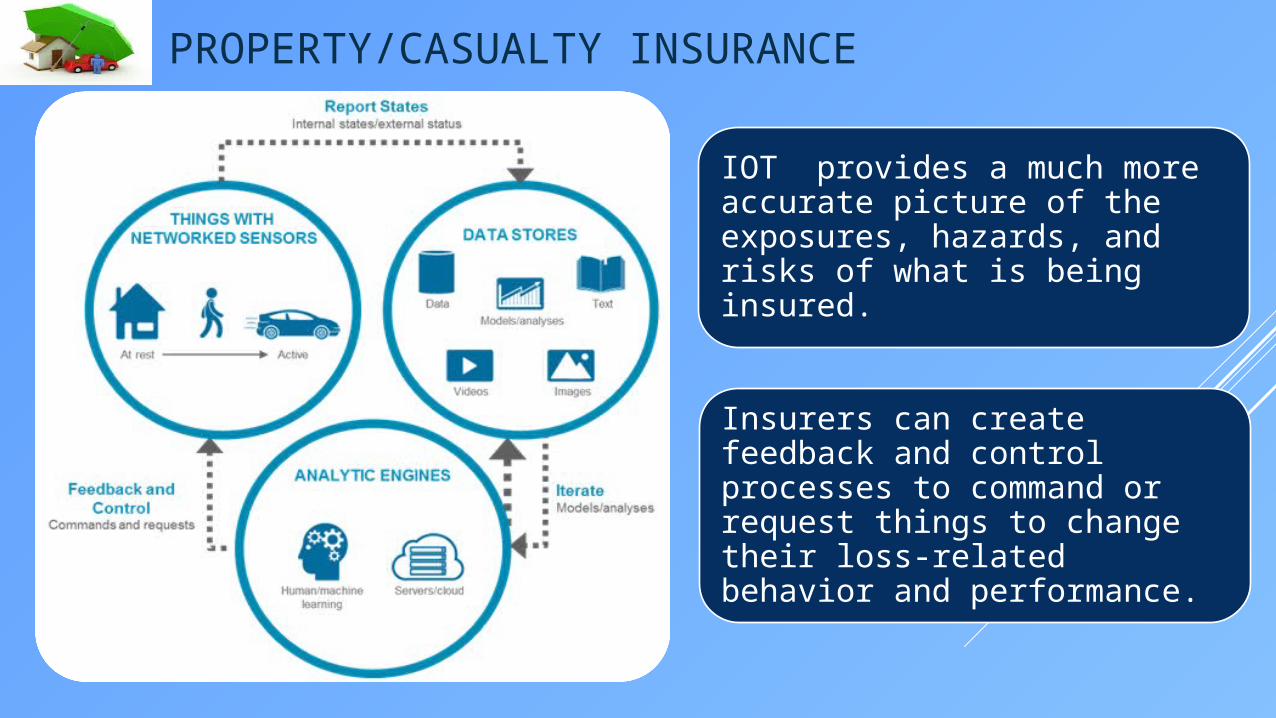

PROPERTY/CASUALTY INSURANCE

Insurers can create feedback and control processes to command or request things to change their loss-related behavior and performance.

IOT provides a much more accurate picture of the exposures, hazards, and risks of what is being insured.

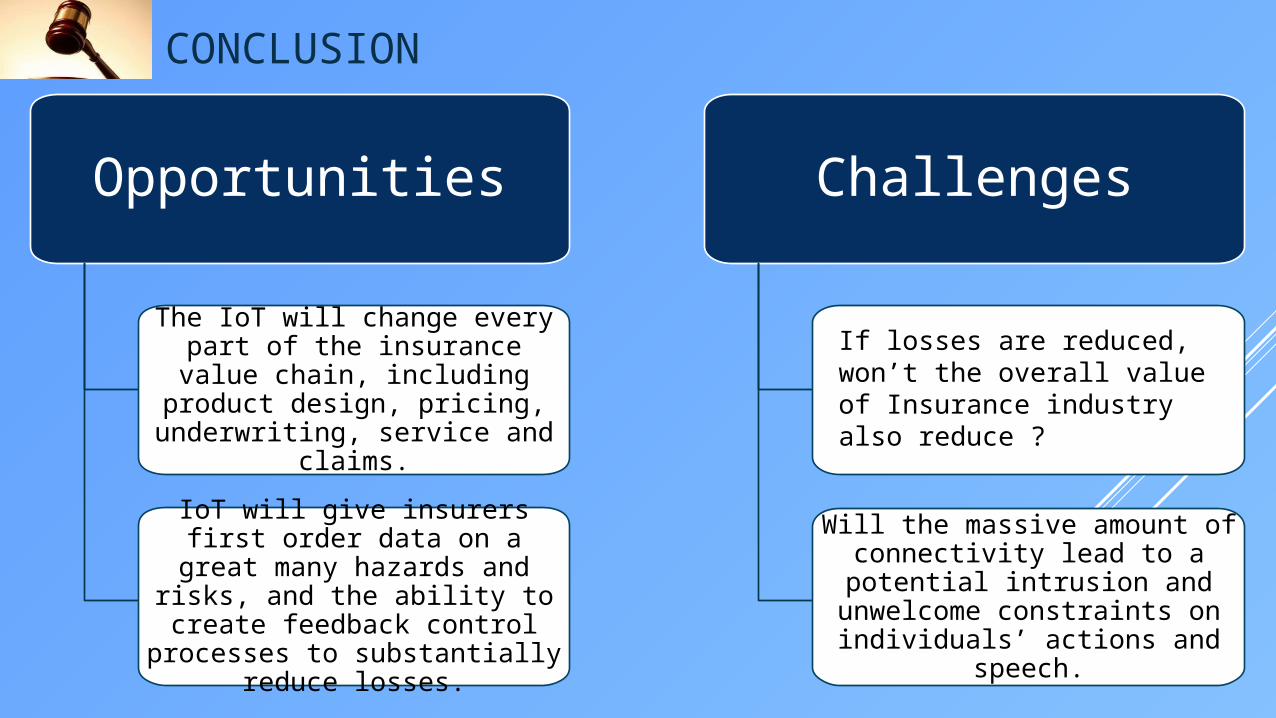

CONCLUSION

Opportunities

The IoT will change every part of the insurance value chain,

including product design, pricing, underwriting, service

and claims.

IoT will give insurers first order data on a great many hazards

and risks, and the ability to create feedback control

processes to substantially reduce losses.

Challenges

Will the massive amount of connectivity lead to a potential

intrusion and unwelcome constraints on individuals’

actions and speech.

If losses are reduced, won’t the overall value of Insurance industry also reduce ?

Related Documents

![[XLS]merinoindia.commerinoindia.com/pdf/MEIL-2017.xls · Web view1914 LADIKIALON KI GALI SOTHLI WALO KA RASTA S M S JAIPUR P0000000000000000810 SUMAN P0000000000000001972 SUMITA CHATTERJEE](https://static.cupdf.com/doc/110x72/5ad279127f8b9a482c8c7934/xls-view1914-ladikialon-ki-gali-sothli-walo-ka-rasta-s-m-s-jaipur-p0000000000000000810.jpg)