Investor Roadshow | February 28, 2018 Investor Roadshow | February 28, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Investor Roadshow | February 28, 2018

Investor Roadshow | February 28, 2018

Investor Roadshow | February 28, 2018

Forward-Looking Statements

2

Certain statements in these slides and made during this presentation may be considered forward-looking

statements. These statements reflect management’s current views and are subject to risks and uncertainties

that could cause actual results to differ materially from those expressed or implied in these statements.

Factors which could cause actual results to differ include but are not limited to: (i) the level of our

indebtedness and changes in interest rates; (ii) industry conditions, including but not limited to changes in

the cost or availability of raw materials, energy and transportation costs, competition we face, cyclicality and

changes in consumer preferences, demand and pricing for our products; (iii) global economic conditions and

political changes, including but not limited to the impairment of financial institutions, changes in currency

exchange rates, credit ratings issued by recognized credit rating organizations, the amount of our future

pension funding obligation, changes in tax laws and pension and health care costs; (iv) unanticipated

expenditures related to the cost of compliance with existing and new environmental and other governmental

regulations and to actual or potential litigation; (v) whether we experience a material disruption at one of our

manufacturing facilities; (vi) risks inherent in conducting business through joint ventures; and (vii) our ability

to achieve the benefits we expect from strategic acquisitions, divestitures and restructurings. These and

other factors that could cause or contribute to actual results differing materially from such forward-looking

statements are discussed in greater detail in the Company’s Securities and Exchange Commission filings.

We undertake no obligation to publicly update any forward-looking statements, whether as a result of new

information, future events or otherwise.

Investor Roadshow | February 28, 2018

Statements Relating to Non-GAAP Financial Measures

3

During the course of this presentation, certain non U.S. GAAP financial measures

will be presented, such as Adjusted Operating EPS, Adjusted EBIT, Adjusted

EBITDA, Adjusted EBITDA Margin, Free Cash Flow, Cash Conversion and Adjusted

ROIC.

A reconciliation of all presented non-GAAP measures (and their components) to

U.S. GAAP financial measures is available on the company’s website at

internationalpaper.com under Performance/Investors.

Investor Roadshow | February 28, 2018

Ilim JV and GPK Investment Information

4

All financial information and statistical measures regarding our 50/50 Ilim joint

venture in Russia (“Ilim”) and our 20.5% ownership interest in a subsidiary of

Graphic Packaging Holding Company (“GPK”), other than historical International

Paper Equity Earnings and dividends received by International Paper, have been

prepared by the management of Ilim and GPK, respectively. Any projected

financial information and statistical measures reflect the current views of Ilim and

GPK management and are subject to risks and uncertainties that could cause

actual results to differ materially from those expressed or implied by such

projections. See “Forward-Looking Statements.”

Investor Roadshow | February 28, 2018

Investment Thesis

Investor Roadshow | February 28, 2018

IP Investment Thesis

6

Our Vision

To be among the most successful,

sustainable and responsible

companies in the world

Our Mission

To improve people’s lives, the planet and

our company’s performance by transforming

renewable resources into products people

depend on every day

Investor Roadshow | February 28, 2018

IP Investment Thesis | About Us

7

We are one of the world’s leading producers of fiber-

based packaging, pulp and paper

We transform renewable resources into recyclable

products people depend on every day

We do the right things, in the right ways,

for the right reasons, all of the time.

Who We

Are

What

We Do

How We

Do It

Investor Roadshow | February 28, 2018

IP Investment Thesis | The IP Way Forward

8

“The IP Way Forward is how we

go beyond just doing the right

things; it’s how we create long-

term value for all IP stakeholders.”

Mark S. Sutton,

Chairman and Chief Executive Officer

Investor Roadshow | February 28, 2018

IP Investment Thesis | Leveraging Selective Choices

9

Cost Positions

• Low-cost asset base

− Mill footprint on cost curve

− Disciplined capital

investment

• Sustained low-cost

positions through

operational excellence

and optimization

• Fiber-based Packaging, Pulp and Paper

• Advantaged positions in Attractive markets

Strategy

Renewable

Natural Resources

Availability and access to

low-cost, sustainable fiber

in key manufacturing

regions

Channels to Market

• Strong market positions

• Sell products in markets

where they are valued

• Winning with the right

customers and segments

Investor Roadshow | February 28, 2018

IP Investment Thesis | Delivering Shareholder Value

10

Capital Allocation

Strong and sustainable free cash flow to:

Fund dividends (40-50% of FCF)

Maintain healthy balance sheet and

credit rating

Enable opportunistic share buybacks

Reinvest in the businesses and

strengthen portfolio

• Strong and sustainable Free Cash Flow

• Increase value creation

• Exceed shareholders’ TSR expectations

Shareholder Value

Value Creation Levers

Improve what we have:

Manufacturing excellence efforts

Commercial optimization

Targeted investments (IRR>WACC):

Integrate newly-acquired pulp business

and deliver synergies

N.A. Industrial Packaging projects

Riverdale 15 conversion

Madrid mill acquisition / conversion

Investor Roadshow | February 28, 2018

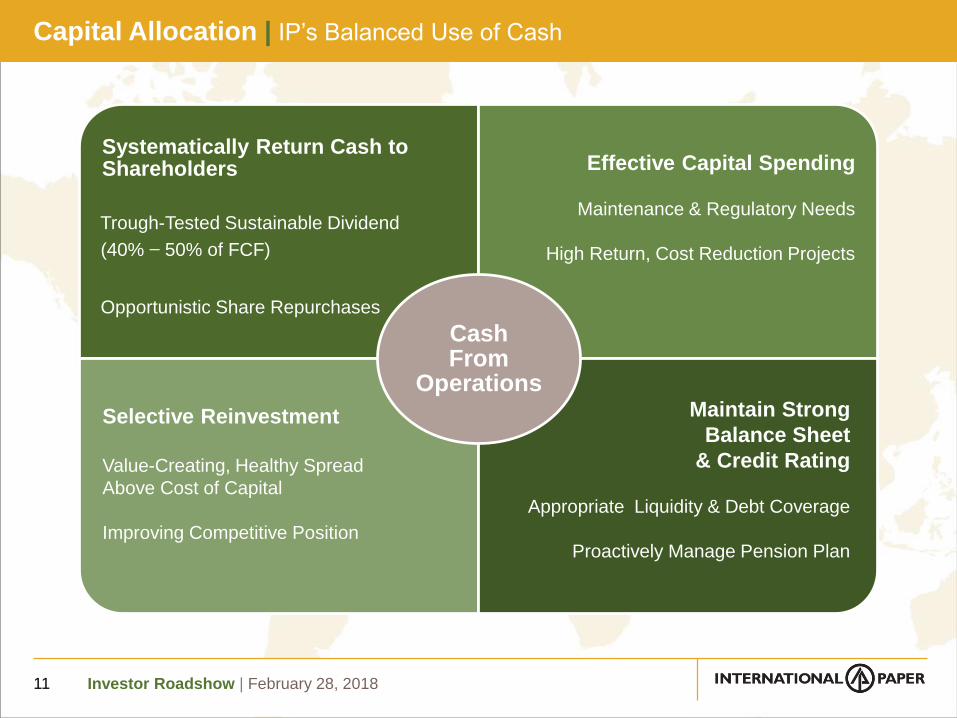

Capital Allocation | IP’s Balanced Use of Cash

11

Systematically Return Cash to Shareholders

Trough-Tested Sustainable Dividend

(40% − 50% of FCF)

Opportunistic Share Repurchases

CashFrom

OperationsMaintain Strong

Balance Sheet

& Credit Rating

Appropriate Liquidity & Debt Coverage

Proactively Manage Pension Plan

Selective Reinvestment

Value-Creating, Healthy Spread

Above Cost of Capital

Improving Competitive Position

Effective Capital Spending

Maintenance & Regulatory Needs

High Return, Cost Reduction Projects

Investor Roadshow | February 28, 2018

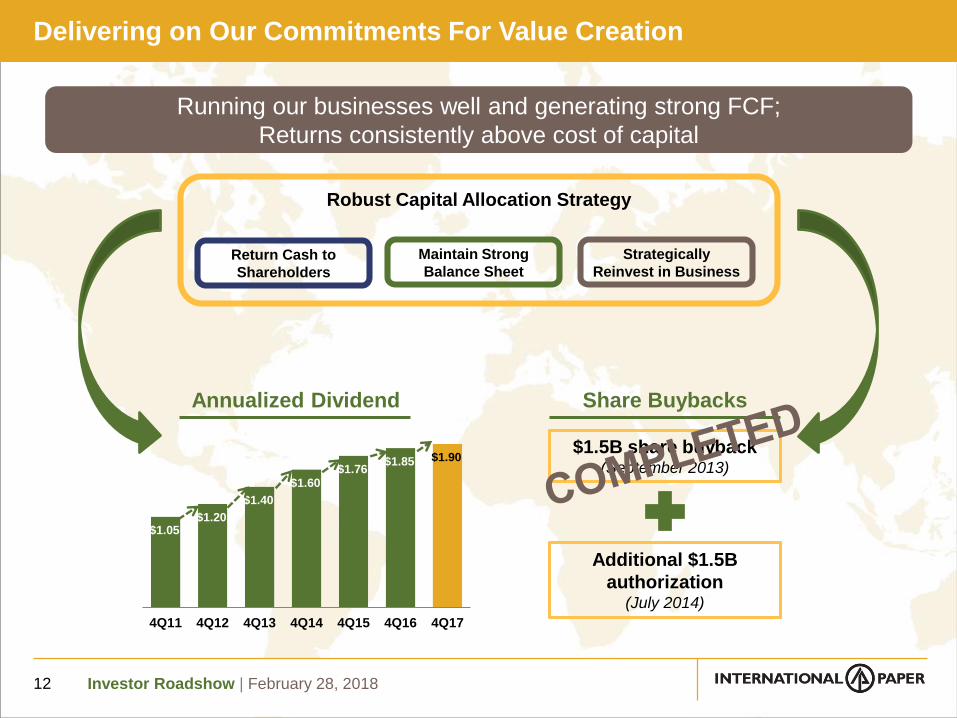

Delivering on Our Commitments For Value Creation

12

Strategically

Reinvest in BusinessReturn Cash to

Shareholders

Maintain Strong

Balance Sheet

Robust Capital Allocation Strategy

Annualized Dividend Share Buybacks

$1.5B share buyback (September 2013)

Additional $1.5B

authorization(July 2014)

Running our businesses well and generating strong FCF;

Returns consistently above cost of capital

$1.05 $1.20

$1.40

$1.60 $1.76

$1.85 $1.90

4Q11 4Q12 4Q13 4Q14 4Q15 4Q16 4Q17

Investor Roadshow | February 28, 2018

Global Economic

Recession

$1.8

$2.1

$1.8 $1.9$2.0

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ B

illi

on

sStrong, Sustainable Free Cash Flow

13

Free Cash Flow, a non U.S. GAAP measure, reflects cash provided by continuing operations for 2005 – 2011, based on data in the 10-K for each year at the time of filing. Free Cash

Flow reflects cash provided by operations for 2012 onward.

Excludes net cash pension contributions impacting 2006, 2010, 2011, 2013, 2014, 2015, 2016 & 2017, cash flows under European accounts receivable securitization beginning in 2009

and ending in 2011, and cash received from Black Liquor Tax Credits in 2009 and 2010. 2012 excludes $120MM cash paid for Temple-Inland change-in-control agreements, $251MM

cash received from unwinding a timber monetization, $44MM cash paid for Temple-Inland pension plan contribution, and $80MM cash paid for Guaranty Bank settlement. 2013 excludes

$30MM cash received from Guaranty Bank insurance reimbursements. For 2015 onward, see slide #64 for a reconciliation of cash provided by operations to Free Cash Flow.

Transformation:

$0.5 Billion (average)

5-Year Average

$1.9 Billion

Investor Roadshow | February 28, 2018

Global

Economic

Recession

4.5%

6.3%7.5%

6.5%

5.0%

8.1%

9.5%

8.3%

9.7%9.2%

11.4%

10.0% 9.9%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Expanded Spread of Adj. ROIC1 Above Cost of Capital | Increasing Shareholder Value

14

5-Year Average

10.0%

WACC for 2017

Years 2013-2017 restated to reflect N.A. Consumer Packaging and xpedx as discontinued operations. Years 2005-2012 are as reported in the 10-K for each year at time of filing1 Adjusted ROIC = Adjusted Operating Earnings before Interest / Average Invested Capital [Equity (adjusted to remove pension related amounts in OCI, net of tax) + Interest-bearing Debt]

Investor Roadshow | February 28, 2018

2018 Outlook | Momentum Continues

15

Confident in Another Year of 10%+ Growth in EBITDA

Free Cash FlowStrong cash generation

and conversion

Strong outlook in

core businessesDemand

Catalysts

Cost reduction initiatives

GCF optimization

Madrid Mill start-up

MarginFull-year price flow through

of 2017 increases

$3.7

2017 2018E

Adjusted EBITDA1

($MM)

10%+

1 From continuing operations before special items and non-operating pension expense

Investor Roadshow | February 28, 2018

Business Overview

Investor Roadshow | February 28, 2018

2005 - 2007 2008 - 2010 2011+

IP Transformation Timeline/Plan

Transformation Plan

Divestitures & Strategic

Reinvestment

Global Recession IP Achieves Cost of Capital Returns

N.A. Weyco Pkg.

Acquisition

Russia

Ilim JV

India APPM

AcquisitionChina

Sun JV

Brazil

VCP Land / Mill Swap

Coated Papers

Wood Products

Forestland

Kraft Paper

Chemicals

Beverage Pkg.

$11B

Asset Sales

China

SCA Pkg.

Brazil

Grupo Orsa Pkg.

N.A. TIN

Acquisition

Turkey

Olmuksan Pkg.

17

Franklin Fluff

Pulp

Conversion

TIN Bldg.

Products

Sale

xpedx

Spin-Off

Riegelwood

Fluff Pulp

ConversionValliant

PM3

Sun JV

& Asia

Box Sale

Madrid mill

Acquisition

Weyco Pulp

Business

Acquisition

N.A. Consumer

Pkg Transfer

Investor Roadshow | February 28, 201818

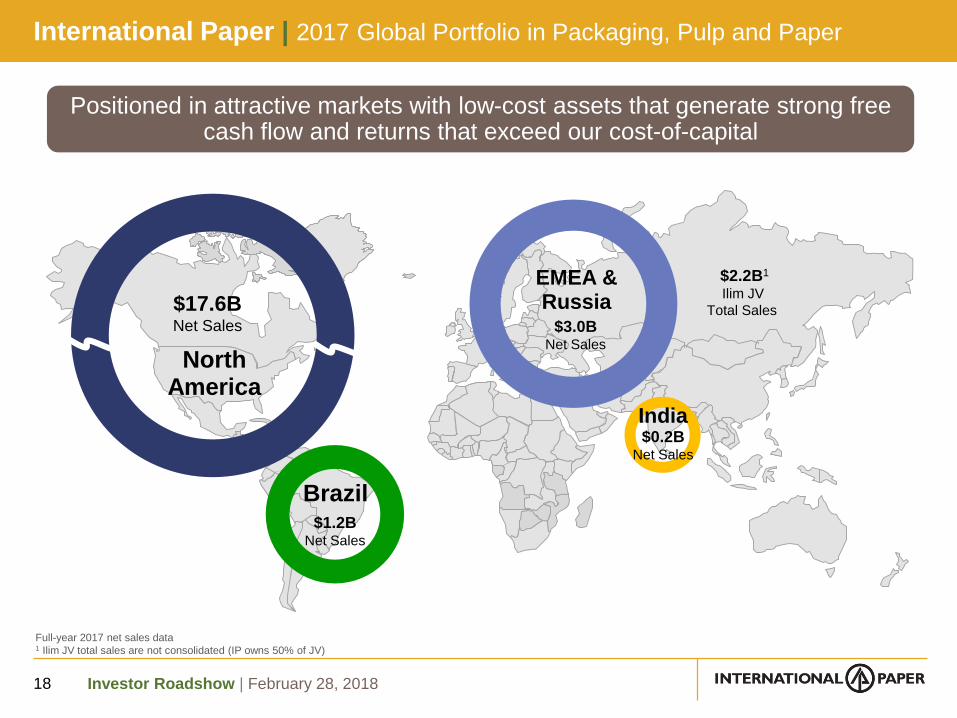

NorthAmerica

Brazil

EMEA &Russia

India

Positioned in attractive markets with low-cost assets that generate strong free cash flow and returns that exceed our cost-of-capital

$17.6BNet Sales

$1.2BNet Sales

$3.0BNet Sales

$0.2BNet Sales

Full-year 2017 net sales data1 Ilim JV total sales are not consolidated (IP owns 50% of JV)

International Paper | 2017 Global Portfolio in Packaging, Pulp and Paper

$2.2B1

Ilim JV

Total Sales

Investor Roadshow | February 28, 201819

Strong Domestic Market Positions

1st

1st

North America

Latin America

EMEA3

NorthAmerica

84%

Brazil8%

EMEA5%

Russia3%

% Total

Adjusted

EBITDA4

2nd

India

Industrial

Packaging

Revenue by

Business1Printing

Papers

69% 19%

Russia

1st 1st

Ilim

Pulp

* Fluff pulp & specialties grades1 Based on 2017 sales2 From continuing operations before special items and non-operating pension expense; does not reflect equity earnings from Ilim JV3 Excludes Russia4 Based on 2017 Adj. EBITDA Margins

Global

Cellulose

Fibers

12%

1st*

Investor Roadshow | February 28, 2018

N.A. Exports | Leveraging Strategic Export Opportunities

20

Fluff Pulp(~90% of N.A. production)

Containerboard(~10% of N.A. production)

EMEA

Asia

Latin America

~50%~40%

~15%

~45%

~40%~10%

% of export volume shipped to select regions

Investor Roadshow | February 28, 201821

Brazil & Russia Exports | Leveraging Strategic Export Opportunities

Softwood Pulp(~50% of Russia production)

Uncoated Freesheet(~50% of Brazil production)

EMEA

Asia

Latin America ~40%

~55%

~5%

~80%~20%

% of export volume shipped to select regions

Investor Roadshow | February 28, 2018

Global

Recession

N.A. Industrial Packaging | Track Record of Success

22

Bu

sin

ess

Ad

j. EB

ITD

A ($

B)

Weyco Packaging

Acquisition & IntegrationAdj.

EBITDA %

IP Adjusted EBITDA margins based on North American Industrial Packaging operating profit before special items

Excludes the Recycling Business and revenue from trade volumes

0.3 0.4 0.5

0.8

1.3 1.31.6

2.0

2.52.7 2.7

2.42.6

9%

13%15% 15%

19%18%

20%19%

22%24% 24%

22% 22%

0%

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Th

ou

san

ds

TIN Acquisition

& Integration

Growth and Margin Expansion through Strategic Acquisitions

and Successful Integrations

Investor Roadshow | February 28, 2018

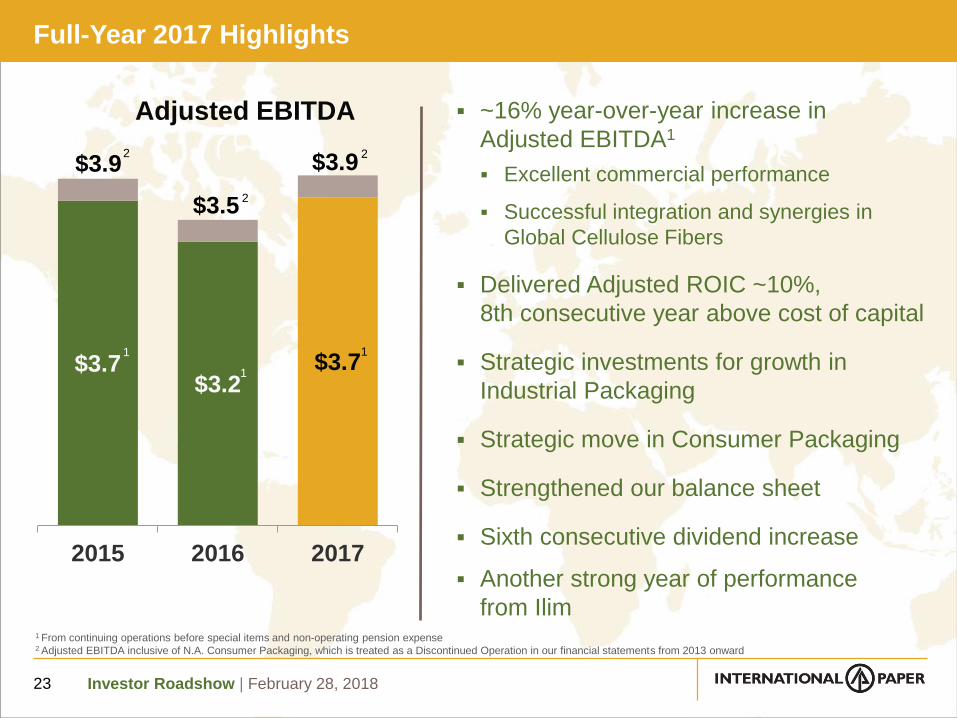

$3.7$3.2

$3.7

2015 2016 2017

Adjusted EBITDA

$3.9

Full-Year 2017 Highlights

~16% year-over-year increase in

Adjusted EBITDA1

Excellent commercial performance

Successful integration and synergies in

Global Cellulose Fibers

Delivered Adjusted ROIC ~10%,

8th consecutive year above cost of capital

Strategic investments for growth in

Industrial Packaging

Strategic move in Consumer Packaging

Strengthened our balance sheet

Sixth consecutive dividend increase

Another strong year of performance

from Ilim

23

1 From continuing operations before special items and non-operating pension expense2 Adjusted EBITDA inclusive of N.A. Consumer Packaging, which is treated as a Discontinued Operation in our financial statements from 2013 onward

1

1

1

$3.5

$3.92

2

2

Investor Roadshow | February 28, 2018

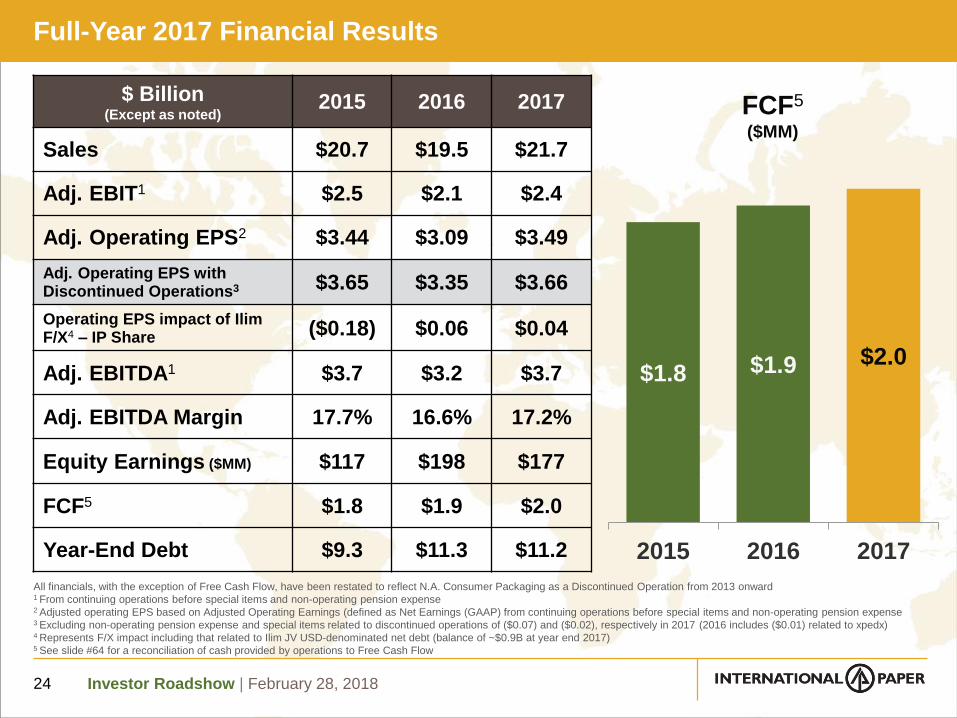

Full-Year 2017 Financial Results

24

$ Billion(Except as noted)

2015 2016 2017

Sales $20.7 $19.5 $21.7

Adj. EBIT1 $2.5 $2.1 $2.4

Adj. Operating EPS2 $3.44 $3.09 $3.49

Adj. Operating EPS with Discontinued Operations3 $3.65 $3.35 $3.66

Operating EPS impact of IlimF/X4 – IP Share ($0.18) $0.06 $0.04

Adj. EBITDA1 $3.7 $3.2 $3.7

Adj. EBITDA Margin 17.7% 16.6% 17.2%

Equity Earnings ($MM) $117 $198 $177

FCF5 $1.8 $1.9 $2.0

Year-End Debt $9.3 $11.3 $11.2

All financials, with the exception of Free Cash Flow, have been restated to reflect N.A. Consumer Packaging as a Discontinued Operation from 2013 onward1 From continuing operations before special items and non-operating pension expense2 Adjusted operating EPS based on Adjusted Operating Earnings (defined as Net Earnings (GAAP) from continuing operations before special items and non-operating pension expense3 Excluding non-operating pension expense and special items related to discontinued operations of ($0.07) and ($0.02), respectively in 2017 (2016 includes ($0.01) related to xpedx)4 Represents F/X impact including that related to Ilim JV USD-denominated net debt (balance of ~$0.9B at year end 2017)5 See slide #64 for a reconciliation of cash provided by operations to Free Cash Flow

$1.8 $1.9 $2.0

2015 2016 2017

FCF5

($MM)

Investor Roadshow | February 28, 2018

4Q17 Financial Results

25

4Q16 3Q17 4Q17

Sales ($B) $5.0 $5.5 $5.7

Adj. EBIT1 ($MM) $461 $665 $831

Adj. Operating EPS2 $0.67 $1.01 $1.27

Adj. Operating EPS with Discontinued Operations3 $0.73 $1.08 $1.34

Operating EPS impact of Ilim F/X4 – IP Share

$0.01 $0.02 $0.01

Adj. EBITDA1 ($MM) $0.8 $1.0 $1.2

Adj. EBITDA Margin1 15.3% 18.2% 20.5%

Equity Earnings ($MM) $47 $45 $64

Free Cash Flow5 ($MM) $467 $624 $732

All financials, with the exception of Free Cash Flow, have been restated to reflect N.A. Consumer Packaging as a Discontinued Operation from 2013 onward1 From continuing operations before special items and non-operating pension expense2 Adjusted operating EPS based on Adjusted Operating Earnings (defined as Net Earnings (GAAP) from continuing operations before special items and non-operating pension expense3 Excluding non-operating pension expense and special items related to discontinued operations of $0.00, $0.00 and $0.09 for 4Q16, 3Q17 and 4Q17, respectively4 Represents F/X impact including that related to Ilim JV USD-denominated net debt (balance of ~$0.9B at end of 4Q17)5 See slide #64 for a reconciliation of cash provided by operations to free cash flow

Record Operating EPS in 4Q17

Healthy industry conditions

Record volume in N.A. Industrial

Packaging and Global Cellulose

Fibers

Full realization of first half 2017

price increases

Successful realization of

Global Cellulose Fibers synergies

Strong performance from Ilim;

IP equity earnings of $64MM

Investor Roadshow | February 28, 2018

Appendix

Investor Roadshow | February 28, 2018

Appendix - Table of Contents

Industrial Packaging……………….………………………………….…..28-39

Global Cellulose Fibers………………………………………………......40-46

Printing Papers..……….…………………………………………………..47-57

IP Russia & Ilim Group.………….….……………………………….……58-61

Graphic Packaging Investment…………………………………….……62

Other Financial Information…..………………………………….….......63-81

Global Citizenship………….…..………………………………….….......82-84

Contact Information……………….………………………………….……85

Slides

27

Investor Roadshow | February 28, 2018

N.A. Containerboard | Supply Positions

28

Source: 2018 estimated effective containerboard capacity based on RISI Capacity Reports, SEC Filings, and IP data and analysis

2018 Producer Position

Top 5 = 75%

IP32%

WRK19%

GP10%

PCA9%

KapStone4%

Others26%

Stone13%

Smurfit7%

GP 9%

WY 7%

IP 7%TIN7%

Others 50%

1995 Producer Position

Top 5 = 43%

Investor Roadshow | February 28, 2018

IP N.A. Industrial Packaging | Balanced Global Strategy

29

1 Includes Saturating Kraft /Gypsum Liner

Source: 2018 estimates based on IP data and analysis

IP Box Plants~80%

Open Market~20%

U.S.~90%

Non-U.S.~10%

Export~65%

Domestic~35%

EMEA~45%

Lat Am~40%

Asia~15%

N.A. Mill System Capacity~13.5 Million Tons

Containerboard~13.0 Million Tons

Other Uses1

~0.5 Million Tons

IP’s channels to market provide choices for maximizing value

Investor Roadshow | February 28, 2018

Global Containerboard Industry | Total Containerboard Trade Flows

Estimated 2018 Global Demand = 189MM tons

30

Net Export, Tons

Net Import, Tons

Countries with Net Import or

Export greater than 100M tons…

Source: 2018 RISI trade estimates and IP Analysis

`

Europe

5.1MM

Europe

4.6MM

N America

5.1MMAfrica

1.6MM

S America

0.3MMS America

1.1MM

C America

2.6MM

Africa

0.4MM

Mid East

1.1MM

Asia

1.5MM

Oceania

0.8MM

Investor Roadshow | February 28, 2018

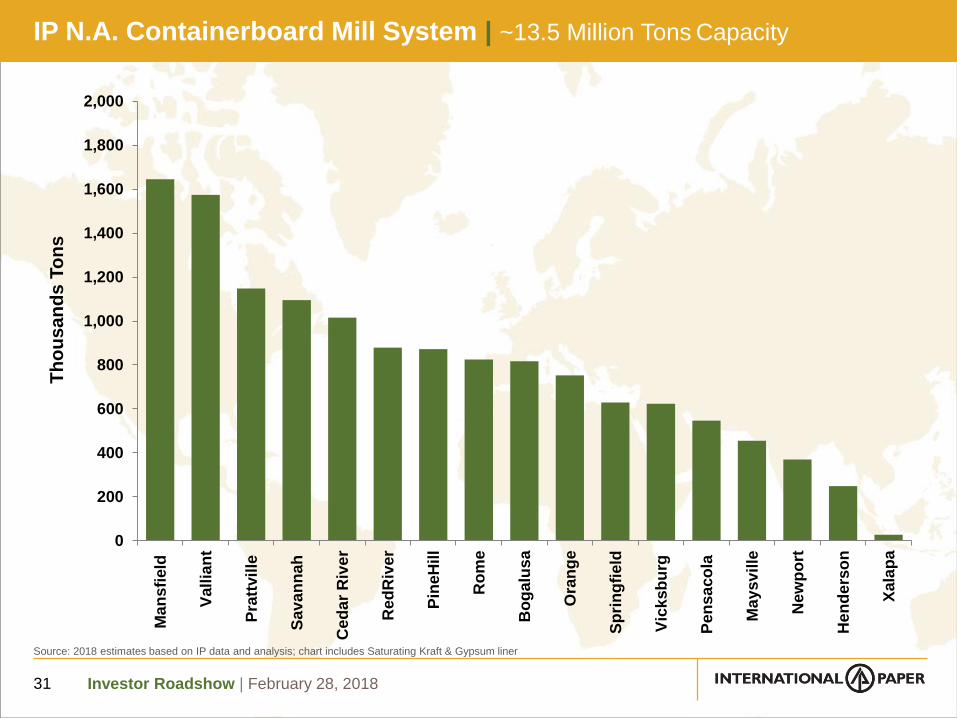

IP N.A. Containerboard Mill System | ~13.5 Million Tons Capacity

31

Source: 2018 estimates based on IP data and analysis; chart includes Saturating Kraft & Gypsum liner

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Ma

ns

field

Vall

ian

t

Pra

ttvil

le

Sav

an

nah

Ced

ar

Riv

er

Red

Riv

er

Pin

eH

ill

Ro

me

Bo

ga

lus

a

Ora

ng

e

Sp

rin

gfi

eld

Vic

ksb

urg

Pen

sa

co

la

Ma

ysv

ille

New

po

rt

He

nd

ers

on

Xala

pa

Th

ou

sa

nd

s T

on

s

Investor Roadshow | February 28, 2018

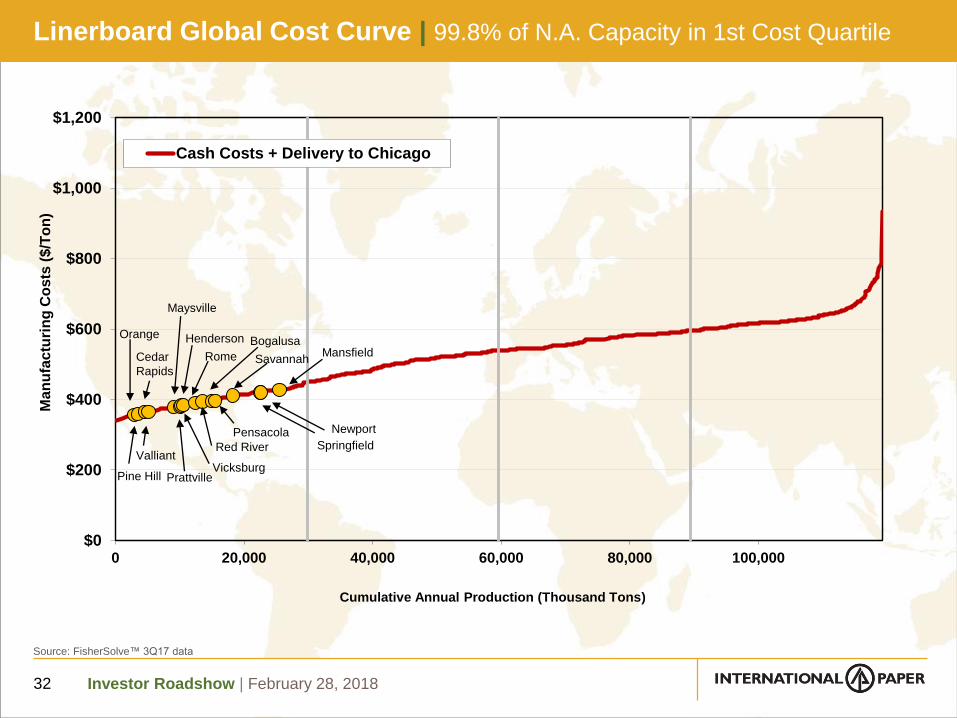

$0

$200

$400

$600

$800

$1,000

$1,200

0 20,000 40,000 60,000 80,000 100,000

Ma

nu

fac

turi

ng

Co

sts

($

/To

n)

Cumulative Annual Production (Thousand Tons)

Cash Costs + Delivery to Chicago

Linerboard Global Cost Curve | 99.8% of N.A. Capacity in 1st Cost Quartile

32

Source: FisherSolve™ 3Q17 data

Orange

Pine Hill

Valliant

Cedar

Rapids

Maysville

Prattville

Henderson

Vicksburg

Rome

Red River

Bogalusa

Pensacola

Savannah

Springfield

Newport

Mansfield

Investor Roadshow | February 28, 2018

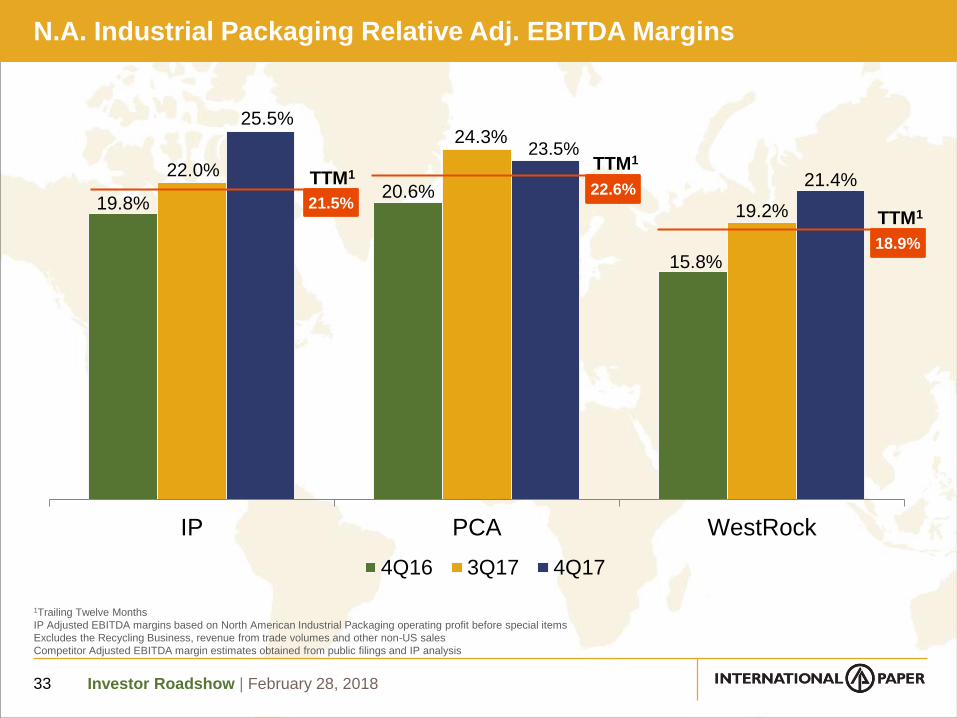

N.A. Industrial Packaging Relative Adj. EBITDA Margins

33

19.8%20.6%

15.8%

22.0%

24.3%

19.2%

25.5%

23.5%

21.4%

IP PCA WestRock

4Q16 3Q17 4Q17

1Trailing Twelve Months

IP Adjusted EBITDA margins based on North American Industrial Packaging operating profit before special items

Excludes the Recycling Business, revenue from trade volumes and other non-US sales

Competitor Adjusted EBITDA margin estimates obtained from public filings and IP analysis

TTM1

21.5%22.6%

TTM1

18.9%

TTM1

Investor Roadshow | February 28, 2018

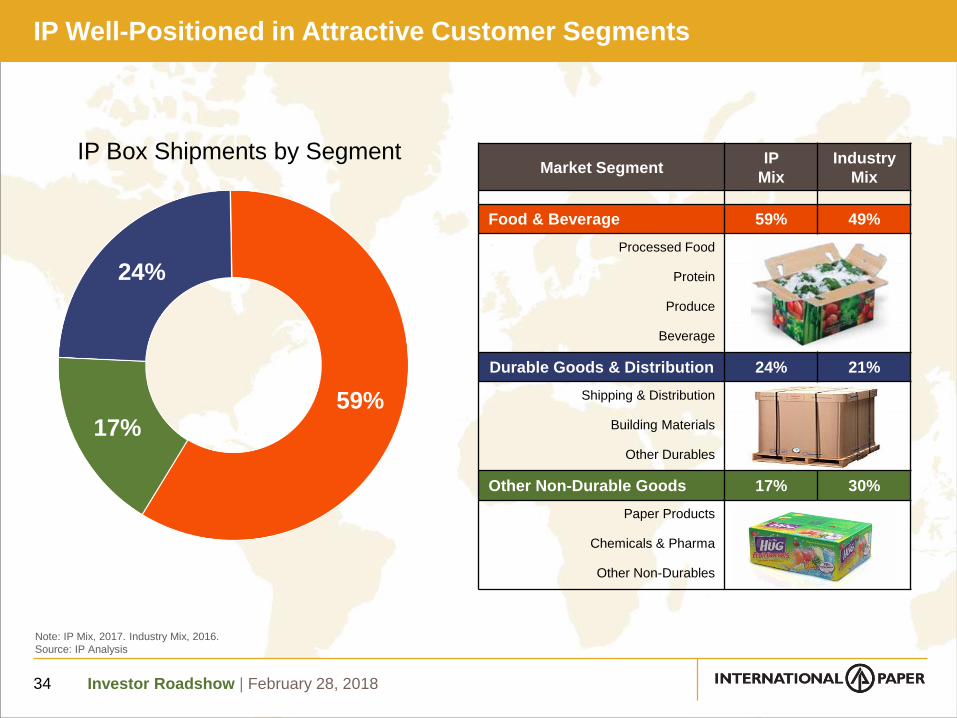

Note: IP Mix, 2017. Industry Mix, 2016.

Source: IP Analysis

IP Well-Positioned in Attractive Customer Segments

34

59%17%

24%

IP Box Shipments by SegmentMarket Segment

IP

Mix

Industry

Mix

Food & Beverage 59% 49%

Processed Food

Protein

Produce

Beverage

Durable Goods & Distribution 24% 21%

Shipping & Distribution

Building Materials

Other Durables

Other Non-Durable Goods 17% 30%

Paper Products

Chemicals & Pharma

Other Non-Durables

Investor Roadshow | February 28, 2018

Riverdale Mill Conversion | Investment Overview

35

Strategic Rationale:

Supports growth in our strategic markets

Enhances world-class mill system and significantly improves our whitetop linerboard cost

Improves system flexibility

Improves our whitetop linerboard product offering

Investment: $300MM to convert No. 15 paper machine from uncoated freesheet to high quality whitetop virgin containerboard; will add 450k tons of capacity

Timing: Targeting to complete conversion mid-2019

N.A. Containerboard Mill System

Investor Roadshow | February 28, 2018

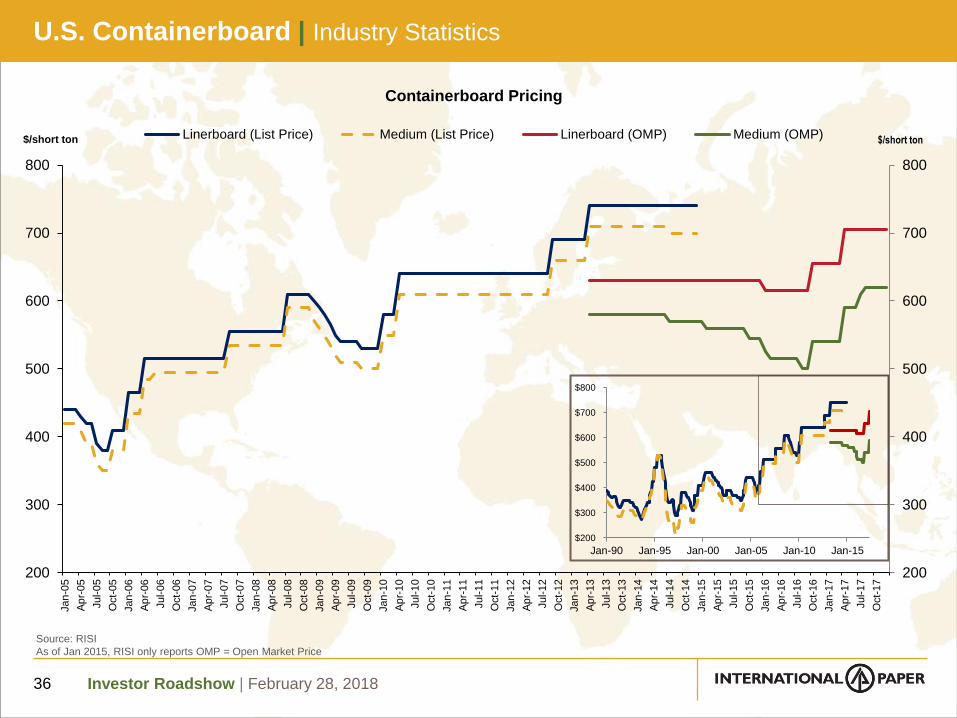

U.S. Containerboard | Industry Statistics

36

200

300

400

500

600

700

800

200

300

400

500

600

700

800

Jan

-05

Ap

r-05

Jul-0

5

Oct-

05

Jan

-06

Ap

r-06

Jul-0

6

Oct-

06

Jan

-07

Ap

r-07

Jul-0

7

Oct-

07

Jan

-08

Ap

r-08

Jul-0

8

Oct-

08

Jan

-09

Ap

r-09

Jul-0

9

Oct-

09

Jan

-10

Ap

r-10

Jul-1

0

Oct-

10

Jan

-11

Ap

r-11

Jul-1

1

Oct-

11

Jan

-12

Ap

r-12

Jul-1

2

Oct-

12

Jan

-13

Ap

r-13

Jul-1

3

Oct-

13

Jan

-14

Ap

r-14

Jul-1

4

Oct-

14

Jan

-15

Ap

r-15

Jul-1

5

Oct-

15

Jan

-16

Ap

r-16

Jul-1

6

Oct-

16

Jan

-17

Ap

r-17

Jul-1

7

Oct-

17

$/short ton$/short ton

Containerboard Pricing

Linerboard (List Price) Medium (List Price) Linerboard (OMP) Medium (OMP)

Source: RISI

As of Jan 2015, RISI only reports OMP = Open Market Price

$200

$300

$400

$500

$600

$700

$800

Jan-90 Jan-95 Jan-00 Jan-05 Jan-10 Jan-15

Investor Roadshow | February 28, 2018

Economic Indicators and U.S. Box Demand

37

Source: Oxford Economics; RISI North America Containerboard Historical Data

70

80

90

100

110

120

130

140

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7In

dexed 1

00 =

2001

US Box Shipments US Nondurable Industrial Production US GDP US Industrial Production

Investor Roadshow | February 28, 2018

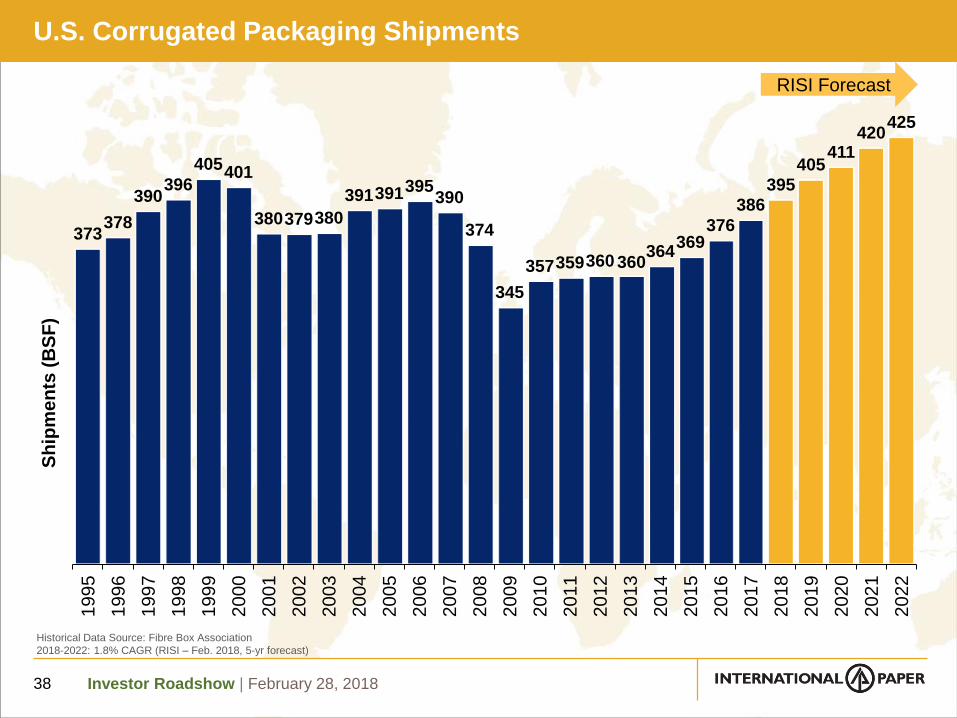

373378

390396

405401

380379380

391391395390

374

345

357359360 360364

369376

386395

405411

420425

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Sh

ipm

en

ts (

BS

F)

U.S. Corrugated Packaging Shipments

38

Historical Data Source: Fibre Box Association

2018-2022: 1.8% CAGR (RISI – Feb. 2018, 5-yr forecast)

RISI Forecast

Investor Roadshow | February 28, 2018

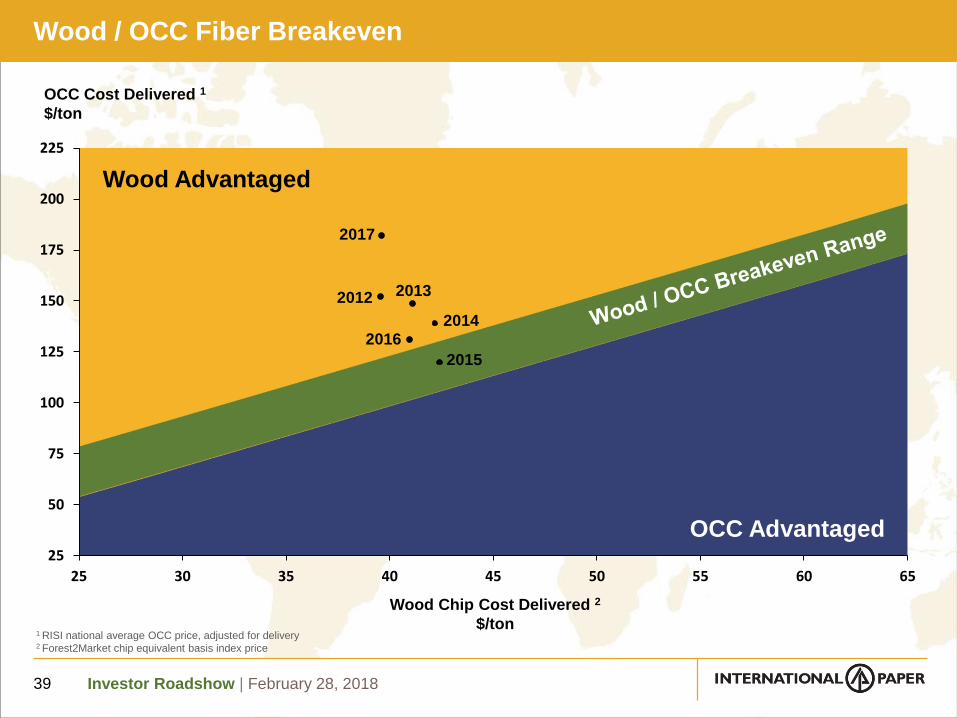

Wood / OCC Fiber Breakeven

39

25

50

75

100

125

150

175

200

225

25 30 35 40 45 50 55 60 65

OCC Cost Delivered 1

$/ton

Wood Chip Cost Delivered 2

$/ton

Wood Advantaged

OCC Advantaged

2012

2014

2013

1 RISI national average OCC price, adjusted for delivery2 Forest2Market chip equivalent basis index price

2015

2016

2017

Investor Roadshow | February 28, 2018

Global Cellulose Fibers | Business Overview

40

~75%

~25%

Current Product Mix1

Fluff Pulp & Specialties Market Pulp

Total Capacity ~3.6MM MTPY Targeted Mix

Fluff Pulp & Specialties 3.0MM 85%

Market Pulp 0.6MM 15%

1 North American production. Combined businesses, with Riegelwood PM18 running SW market pulp

Market Pulp Mill

Fluff Pulp Mill

Converting facilities

Investor Roadshow | February 28, 2018

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1995 2000 2005 2010 2015 2020

An

nu

al G

DP

(U

SD

/cap

ita)

MEA Asia-Pacific Eastern Europe Latin America

Source: Euromonitor, 3Q14

Absorbent Hygiene Products (AHP) Outlook | Demand and Growth

41

AHP demand linked to GDP growth in emerging markets

Investor Roadshow | February 28, 2018

Global Market Pulp Demand Outlook | Bleached Softwood

42

North America North America

Latin America Latin America

Western Europe Western Europe

Eastern Europe Eastern Europe

Asia Asia

Rest of WorldRest of World

0

5

10

15

20

25

30

2018 2021

2018 – 2021

CAGR

0.5%

2.1%

1.9%

(1.2%)

0.2%

0.5%

Source: PPPC; IP Analysis

25.8MM MTPY 26.8MM MTPYCAGR = 1.3%

Investor Roadshow | February 28, 2018

Global Cellulose Fibers | Advantaged Position in Attractive Markets

43

Well-Positioned to Serve Growing Demand with Global, Strategic Customers

Source: Poyry World Fibre Outlook up to 2030, IP Analysis

North America

Latin America

EMEA

Asia

2018

2018 - 2022

CAGR

2.1%

3.1%

7.6%

3.1%Airlaid

11%

Adult

Incontinence

35%

Feminine

Care

22%

Baby

Diapers

32%

6.2MM MTPY

CAGR = 4.3%

Fluff Demand by Region and End Use

2.3%

3.6%

6.3%

1.6%

2018 - 2022

CAGR

Investor Roadshow | February 28, 2018

Pulp mill

IP Global Pulp Capacity | Total of 4.1 MM MTPY1

44

Ilim JV

2.0 MM

Europe / Russia

0.3 MM N. America

3.6 MM

L. America

0.2 MM

1 Does not include llim JV

Investor Roadshow | February 28, 201845

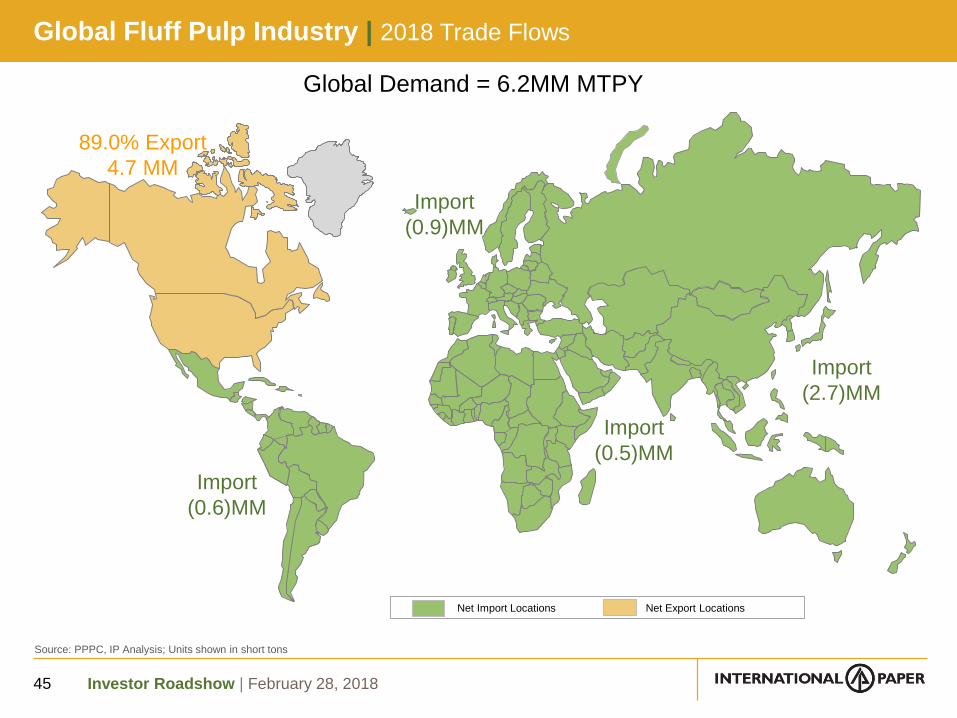

Global Fluff Pulp Industry | 2018 Trade Flows

Net Import Locations Net Export Locations

Global Demand = 6.2MM MTPY

Import

(0.9)MM

89.0% Export

4.7 MM

Import

(0.5)MM

Import

(0.6)MM

Import

(2.7)MM

Source: PPPC, IP Analysis; Units shown in short tons

Investor Roadshow | February 28, 2018

Pulp | Industry Statistics

46

0

200

400

600

800

1,000

1,200

1,400

Jan

-06

Ma

r-06

Ma

y-0

6Jul-0

6S

ep-0

6N

ov-0

6Jan

-07

Ma

r-07

Ma

y-0

7Jul-0

7S

ep-0

7N

ov-0

7Jan

-08

Ma

r-08

Ma

y-0

8Jul-0

8S

ep-0

8N

ov-0

8Jan

-09

Ma

r-09

Ma

y-0

9Jul-0

9S

ep-0

9N

ov-0

9Jan

-10

Ma

r-10

Ma

y-1

0Jul-1

0S

ep-1

0N

ov-1

0Jan

-11

Ma

r-11

Ma

y-1

1Jul-1

1S

ep-1

1N

ov-1

1Jan

-12

Ma

r-12

Ma

y-1

2Jul-1

2S

ep-1

2N

ov-1

2Jan

-13

Ma

r-13

Ma

y-1

3Jul-1

3S

ep-1

3N

ov-1

3Jan

-14

Ma

r-14

Ma

y-1

4Jul-1

4S

ep-1

4N

ov-1

4Jan

-15

Ma

r-15

Ma

y-1

5Jul-1

5S

ep-1

5N

ov-1

5Jan

-16

Ma

r-16

Ma

y-1

6Jul-1

6S

ep-1

6N

ov-1

6Jan

-17

Ma

r-17

Ma

y-1

7Jul-1

7S

ep-1

7N

ov-1

7Jan

-18

USD/admt Global Pulp Prices

NBSK (dne) BEK (dne) Fluff (dne)

Source: RISI

Global pulp prices delivered to Northern Europe; Units shown in metric tons

Investor Roadshow | February 28, 201847

IP Global Papers Footprint | Total of 4.5 Million Short Tons1

1 Does not include llim JV. NA includes Uncoated Bristols, Bag and other Non UFS

Brazil

1.1 MM

N. America

2.0 MM

Europe

0.8 MM

Russia

0.4 MM

Uncoated paper mill

India

0.2 MM

ILIM

0.3 MM

Investor Roadshow | February 28, 2018

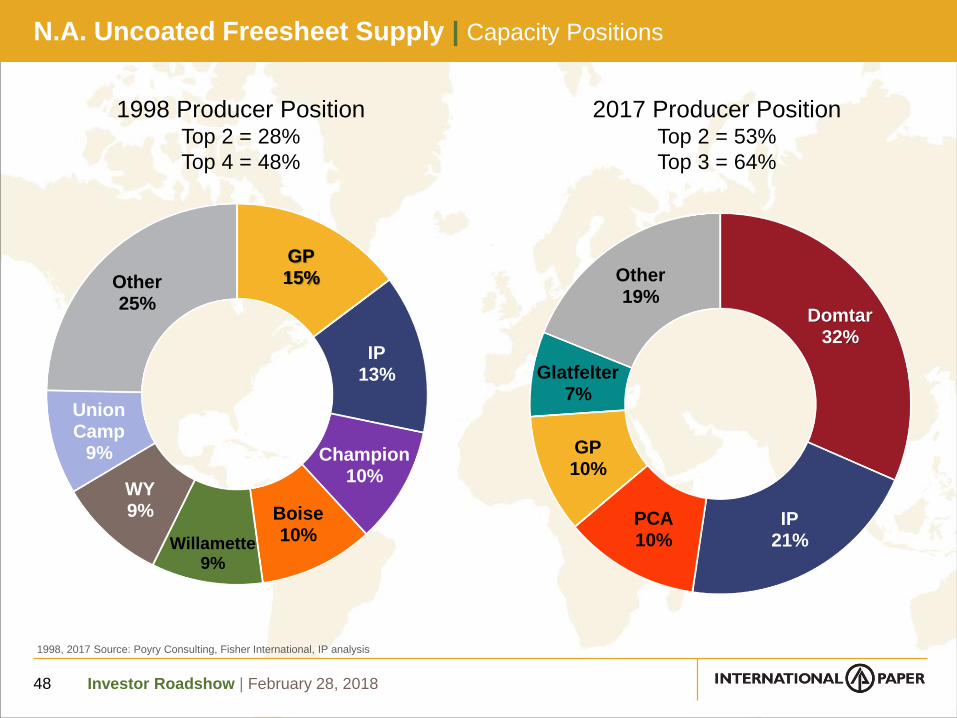

GP15%

IP13%

Champion10%

Boise10%Willamette

9%

WY9%

Union Camp

9%

Other 25%

1998 Producer PositionTop 2 = 28%

Top 4 = 48%

2017 Producer PositionTop 2 = 53%

Top 3 = 64%

1998, 2017 Source: Poyry Consulting, Fisher International, IP analysis

N.A. Uncoated Freesheet Supply | Capacity Positions

48

Domtar32%

IP21%

PCA10%

GP10%

Glatfelter7%

Other 19%

Investor Roadshow | February 28, 2018

0%

20%

40%

60%

80%

100%

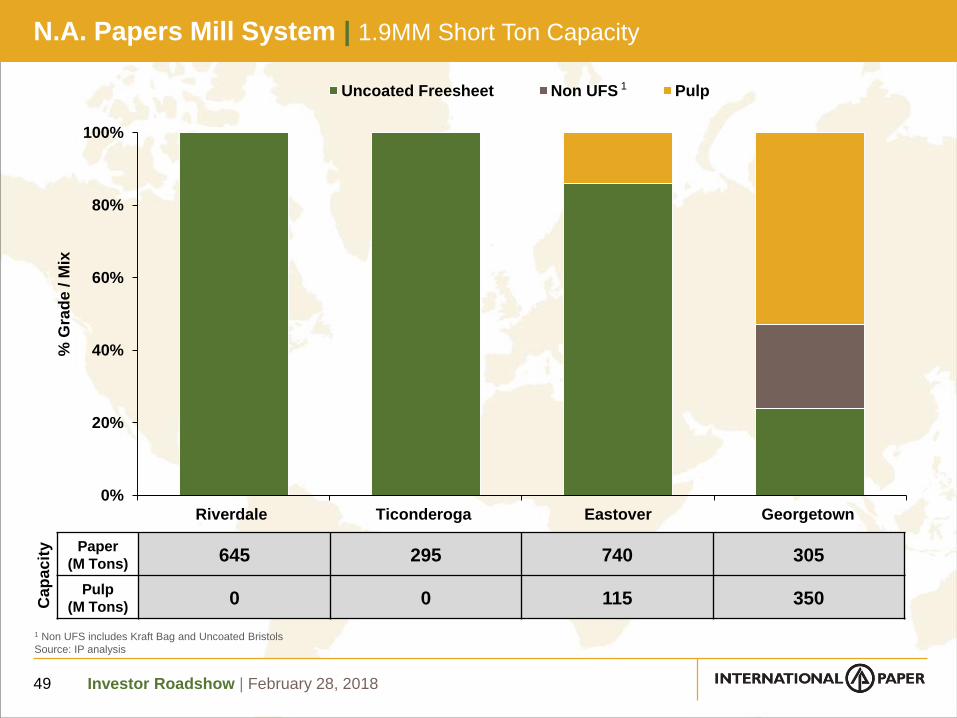

Riverdale Ticonderoga Eastover Georgetown

% G

rad

e / M

ix

Uncoated Freesheet Non UFS Pulp1

N.A. Papers Mill System | 1.9MM Short Ton Capacity

49

1 Non UFS includes Kraft Bag and Uncoated Bristols

Source: IP analysis

Paper

(M Tons) 645 295 740 305

Pulp

(M Tons) 0 0 115 350C

ap

ac

ity

Investor Roadshow | February 28, 2018

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

0 10,000 20,000 30,000 40,000 50,000

Ma

nu

fac

turi

ng

Co

sts

$/T

on

Cumulative Annual Production (Thousand Tons)

Cash Costs + Delivery to Chicago

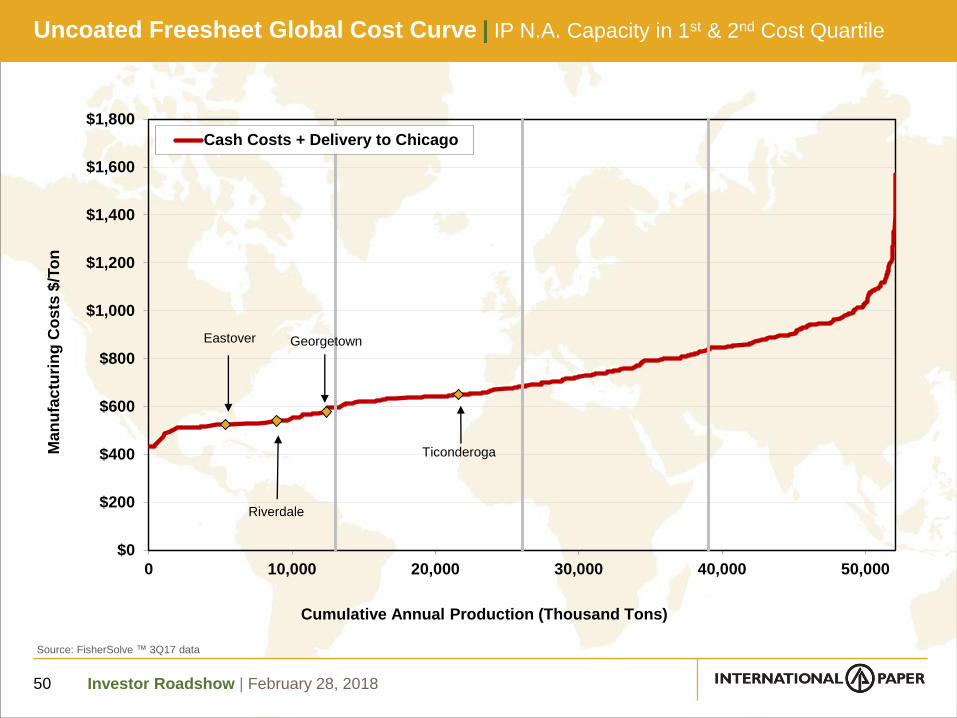

Uncoated Freesheet Global Cost Curve | IP N.A. Capacity in 1st & 2nd Cost Quartile

50

Source: FisherSolve ™ 3Q17 data

Georgetown

Riverdale

Ticonderoga

Eastover

Investor Roadshow | February 28, 2018

314

575657 657

513 539598

499

310253 261 316

213

10%

16%

19% 19%18%

20%

22%

18%

12% 12%13%

17%

12%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Adj.EBITDA1

%

Adj.EBITDA1

$ MM Papers Only

N.A. Printing Papers | Margin History

51

Tons (MM)

4.0 4.1 3.9 3.5 3.0 2.8 2.7 2.7 2.6 2.0 2.0 1.9 1.9

1 From continuing operations before special items and non-operating pension expense

Investor Roadshow | February 28, 2018

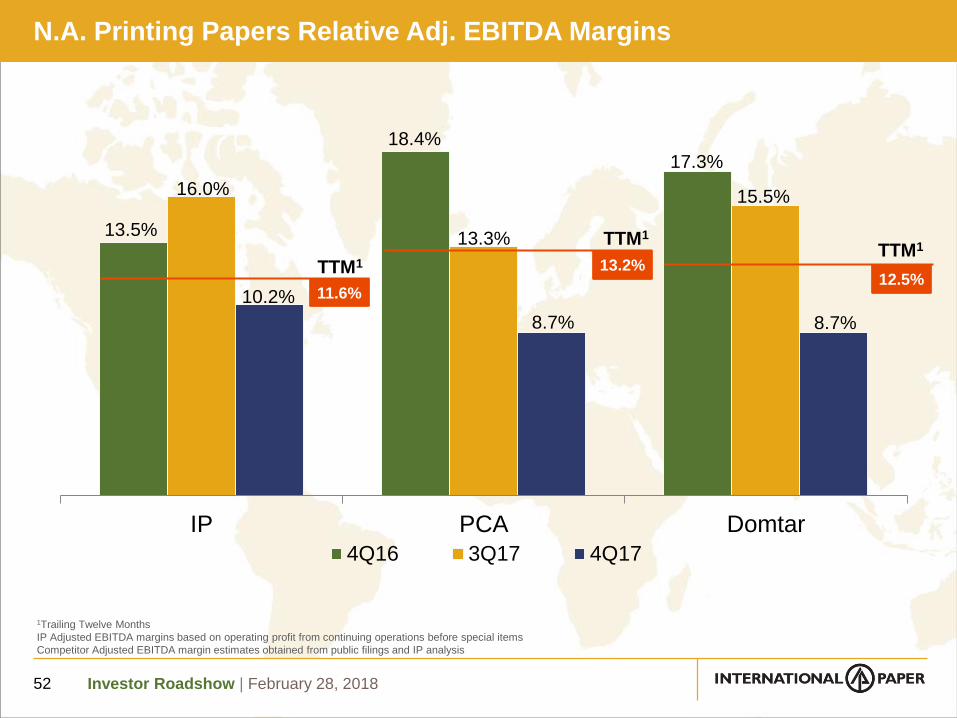

N.A. Printing Papers Relative Adj. EBITDA Margins

52

13.5%

18.4%

17.3%

16.0%

13.3%

15.5%

10.2%

8.7% 8.7%

IP PCA Domtar

4Q16 3Q17 4Q17

1Trailing Twelve Months

IP Adjusted EBITDA margins based on operating profit from continuing operations before special items

Competitor Adjusted EBITDA margin estimates obtained from public filings and IP analysis

TTM1

11.6%

TTM1

13.2%12.5%

TTM1

Investor Roadshow | February 28, 2018

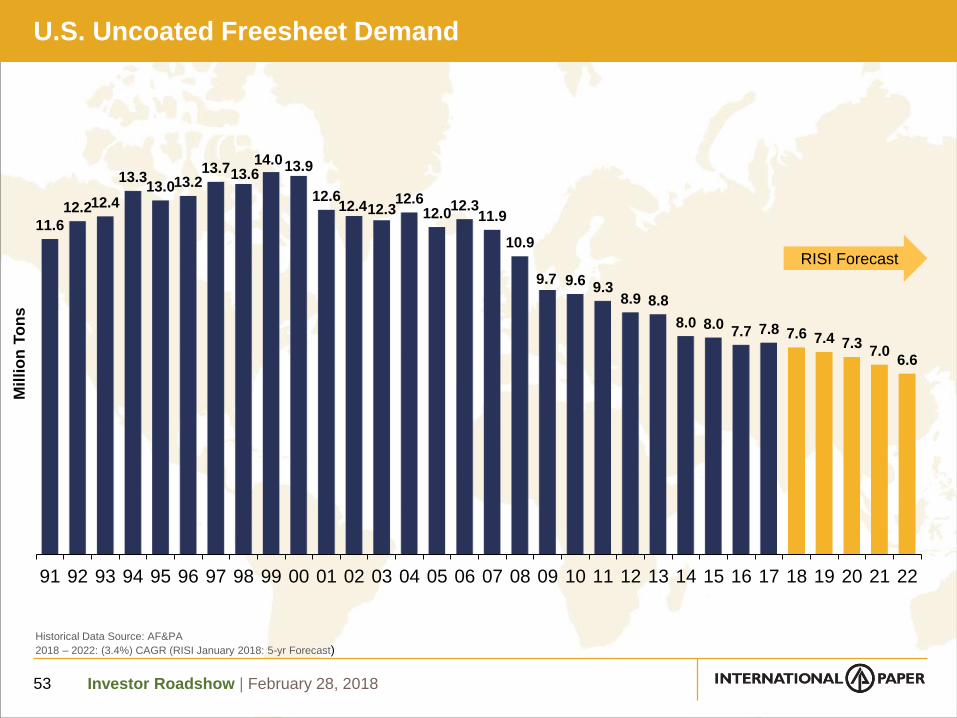

U.S. Uncoated Freesheet Demand

53

Historical Data Source: AF&PA

2018 – 2022: (3.4%) CAGR (RISI January 2018: 5-yr Forecast)

11.6

12.212.4

13.313.013.2

13.713.614.013.9

12.612.412.3

12.612.0

12.311.9

10.9

9.7 9.69.3

8.9 8.8

8.0 8.07.7 7.8 7.6 7.4 7.3

7.06.6

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22

Mil

lio

n T

on

s

RISI Forecast

Investor Roadshow | February 28, 2018

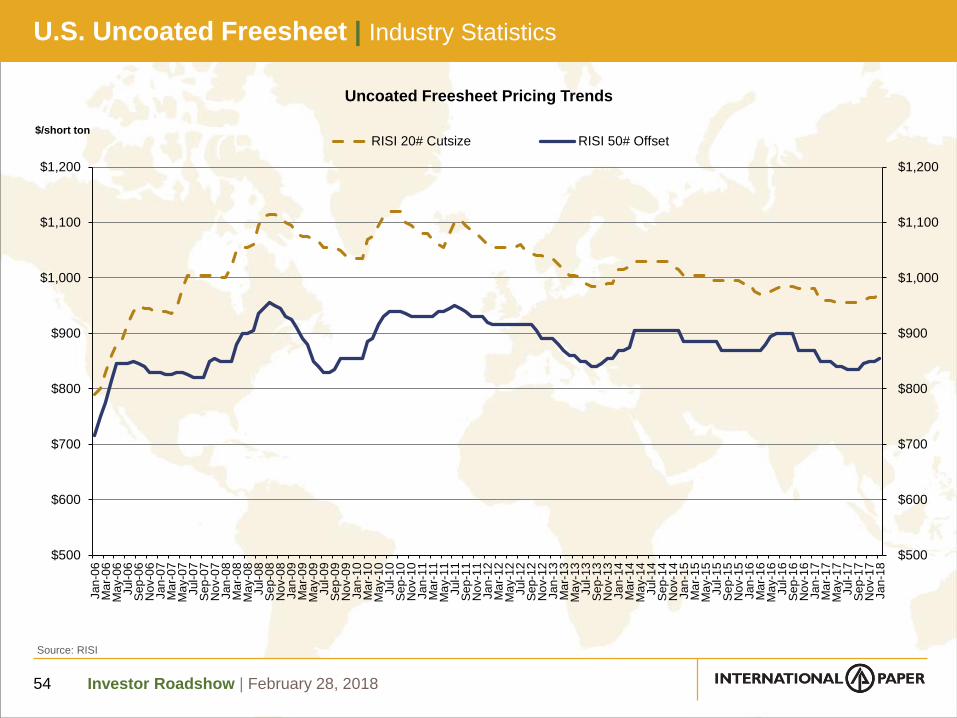

U.S. Uncoated Freesheet | Industry Statistics

54

$500

$600

$700

$800

$900

$1,000

$1,100

$1,200

$500

$600

$700

$800

$900

$1,000

$1,100

$1,200

Jan

-06

Ma

r-0

6M

ay-0

6Jul-

06

Se

p-0

6N

ov-0

6Jan

-07

Ma

r-0

7M

ay-0

7Jul-

07

Se

p-0

7N

ov-0

7Jan

-08

Ma

r-0

8M

ay-0

8Jul-

08

Se

p-0

8N

ov-0

8Jan

-09

Ma

r-0

9M

ay-0

9Jul-

09

Se

p-0

9N

ov-0

9Jan

-10

Ma

r-1

0M

ay-1

0Jul-

10

Se

p-1

0N

ov-1

0Jan

-11

Ma

r-1

1M

ay-1

1Jul-

11

Se

p-1

1N

ov-1

1Jan

-12

Ma

r-1

2M

ay-1

2Jul-

12

Se

p-1

2N

ov-1

2Jan

-13

Ma

r-1

3M

ay-1

3Jul-

13

Se

p-1

3N

ov-1

3Jan

-14

Ma

r-1

4M

ay-1

4Jul-

14

Se

p-1

4N

ov-1

4Jan

-15

Ma

r-1

5M

ay-1

5Jul-

15

Se

p-1

5N

ov-1

5Jan

-16

Ma

r-1

6M

ay-1

6Jul-

16

Se

p-1

6N

ov-1

6Jan

-17

Ma

r-1

7M

ay-1

7Jul-

17

Se

p-1

7N

ov-1

7Jan

-18

$/short ton

Uncoated Freesheet Pricing Trends

RISI 20# Cutsize RISI 50# Offset

Source: RISI

Investor Roadshow | February 28, 2018

Latin American Uncoated Freesheet Market

55

0

500

1,0

00

1,5

00

2,0

00

2,5

00

3,0

00

Brazil

Argentina

Colombia

Chile

Peru

Other LatAm

Thousand Short Tons

Demand

Capacity

Latin America is a Net Exporter

DemandCapacity @

88% Op. RateNet Exports

2.6 MM 2.9 MM -0.2 MM

Supply & Demand

LatAm analysis excludes Mexico

Source: Ibá / AFCP / RISI / Fisher / IP Estimates

Top 6 Producers > 80%

Suzano

37%

30%

7%

4%

4%

4%

14%Smurfit

Kappa

Ledesma

Celulosa

Argentina

Propal

IP

Others

Suzano

3.3MM

tons

Investor Roadshow | February 28, 2018

IP Brazil Uncoated Freesheet | At a Glance

56

Mogi Guacu Luiz Antonio Três Lagoas IP Brazil

UFS Paper

Machines4 2 1 7

UFS Capacity (thousand tons)

460 410 260 1,130

Market Pulp (thousand tons)

45 130 - 175

Source: RISI

Investor Roadshow | February 28, 2018

IP Brazil Uncoated Freesheet | Historical Financials

57

280

317

228

296 320

293

334 326

275 264297

33% 33%

24%

27% 27% 26%

31% 31% 31%29%

31%

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Adj.

EBITDA1

US $ MM

Adj.

EBITDA1

Margin

Tons

(MM) 0.9 1.0 1.2 1.2 1.3 1.3 1.3 1.3 1.2 1.3

1 From continuing operations before special items and non-operating pension expense

Investor Roadshow | February 28, 2018

IP Russia & Ilim JV | Manufacturing Overview

Ilim JV Production1 2016 2017

Bratsk Mill

Total 1,140 1,162

• Softwood bleached pulp 686 653

• Hardwood bleached pulp 266 316

• KLB 188 193

Koryazhma Mill

Total 1,244 1,270

• PM7 paper 181 188

• PM7 CFS 45 48

• Pulp (BHKP, UKP) 299 286

• KLB and others 719 748

Ust-Ilimsk Mill

Total 793 797

• Pulp (BSKP, UKP) Total 769 720

• Hardwood bleached pulp 24 77

IP Russia Production1

Svetogorsk 2017

Total 719

• Coated Paperboard 118

• Pulp (soft/hardwood) 166

• Fine Papers 435

1 Volumes shown in thousand metric tons

Koryazhma

BratskUst-Ilimsk

China

Kazakhstan Mongolia

Svetogorsk

Well-Positioned to Serve Target Markets

58

Investor Roadshow | February 28, 2018

Ilim Joint Venture | Well-Positioned to Serve Growing Pulp Markets

59

China will account for more than 60% of world’s incremental market pulp growth

1st / 2nd quartile cost positions with favorable access to China NBSK market

Access to significant Russian wood basket

1 Source: FisherSolve™ 3Q17 data

$0

$200

$400

$600

$800

$1,000

0 5,000 10,000 15,000 20,000

Ma

nu

fac

turi

ng

Co

sts

($/T

on

)

Cumulative Capacity (Thousand Tons)

Cash Cost + Delivery to Beijing, China1

Ust-Ilimsk

Bratsk

Investor Roadshow | February 28, 2018

Ilim Joint Venture | Full Year Financials

60

2013 2014 2015 2016 2017

Sales Volume (Million metric tonnes) 2.4 2.9 3.0 3.2 3.1

Sales ($B) 1.9 2.1 1.9 1.9 2.2

Debt ($B) 1.5 1.4 1.2 1.5 1.6

Adj. Operating EBITDA ($MM) 203 459 694 680 695

F/X Gain (Loss)1 ($MM) (80) (674) (188) 63 37

EBITDA ($MM) 123 (215) 506 743 732

Depreciation ($MM) 176 188 128 121 151

EBIT ($MM) (53) (403) 378 622 581

Interest Expense ($MM) 39 69 52 81 $88

Net Income / (Loss) ($MM) (72) (359) 237 385 362

IP Equity Earnings / (Loss) ($MM) (46) (194) 131 199 183

Dividends (to IP) ($MM) 0 56 35 60 134

Ilim JV results are US GAAP basis 1 Represents F/X impact including that related to Ilim JV USD-denominated net debt (balance of ~$0.9B at year end 2017)

Investor Roadshow | February 28, 2018

Ilim Joint Venture | 4Q17 vs. 3Q17

61

$ Millions 4Q16 3Q17 4Q17 2016 2017

Sales Volume (thousand metric tonnes)

895 772 843 3,195 3,110

Sales $539 $523 $632 $1,927 $2,150

EBITDA $194 $184 $236 $743 $732

F/X (Impact of USD Net Debt)1 $14 $18 $7 $63 $37

Adj. Operational EBITDA2 $180 $166 $229 $680 $695

IP Equity Earnings (Loss)3 $45 $48 $64 $199 $183

Higher pricing and strong sales volume in 4Q17

F/X gain (non-cash) on USD denominated net debt driven by ruble strengthening

1Q18 equity earnings projected to be $80M-$90MM4 on continued strong, demand-

driven market fundamentals

Ilim JV results are on U.S. GAAP basis 1 Represents F/X impact including amounts related to Ilim JV USD-denominated net debt (balance of ~$0.9B at end of 4Q17); Ilim Group’s functional currency is the

Ruble (RUB); Non-functional-denominated currency balances are measured monthly using the month-end exchange rate2 Before F/X impact including USD-denominated net debt3 IP Equity Earnings (Loss) for 4Q16, 3Q17 and 4Q17 include after-tax F/X gains (losses) (primarily on USD-denominated net debt) of $6MM, $7MM and $3MM, respectively4 At December 31, 2017 RUB/USD exchange rate

Investor Roadshow | February 28, 2018

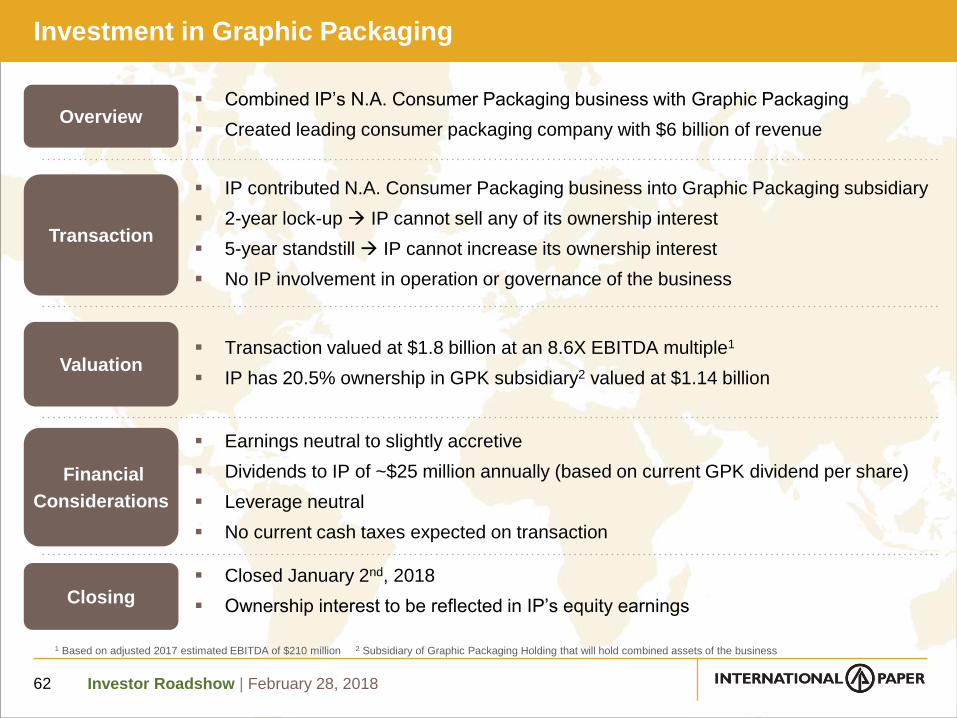

Investment in Graphic Packaging

62

1 Based on adjusted 2017 estimated EBITDA of $210 million 2 Subsidiary of Graphic Packaging Holding that will hold combined assets of the business

Combined IP’s N.A. Consumer Packaging business with Graphic Packaging

Created leading consumer packaging company with $6 billion of revenue

IP contributed N.A. Consumer Packaging business into Graphic Packaging subsidiary

2-year lock-up IP cannot sell any of its ownership interest

5-year standstill IP cannot increase its ownership interest

No IP involvement in operation or governance of the business

Transaction valued at $1.8 billion at an 8.6X EBITDA multiple1

IP has 20.5% ownership in GPK subsidiary2 valued at $1.14 billion

Earnings neutral to slightly accretive

Dividends to IP of ~$25 million annually (based on current GPK dividend per share)

Leverage neutral

No current cash taxes expected on transaction

Closed January 2nd, 2018

Ownership interest to be reflected in IP’s equity earnings

Overview

Transaction

Financial

Considerations

Valuation

Closing

Investor Roadshow | February 28, 2018

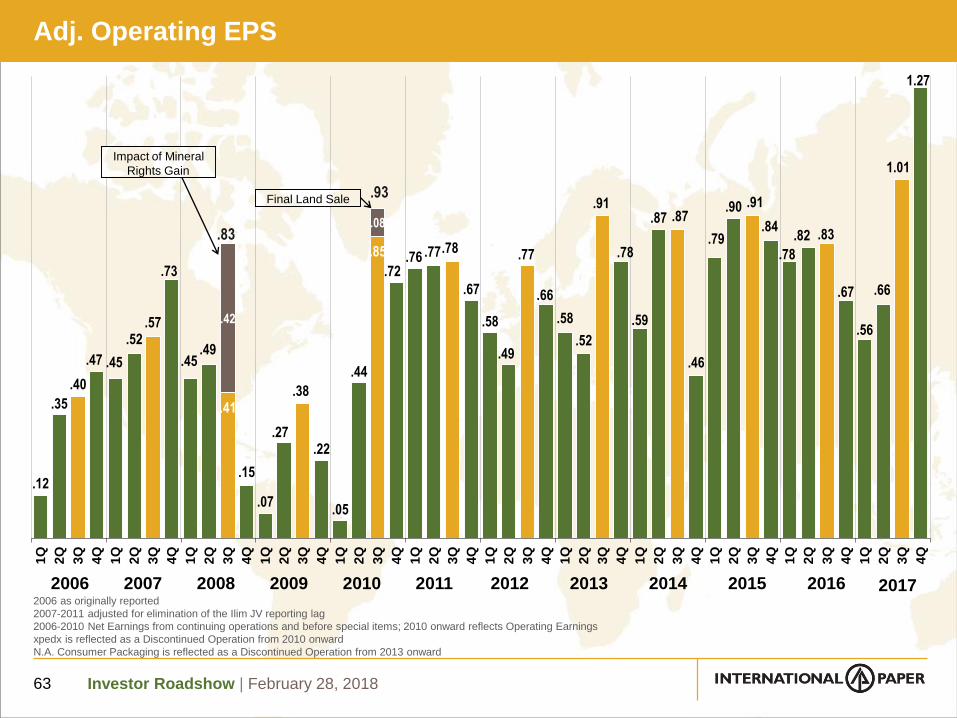

Adj. Operating EPS

63

2006 as originally reported

2007-2011 adjusted for elimination of the Ilim JV reporting lag

2006-2010 Net Earnings from continuing operations and before special items; 2010 onward reflects Operating Earnings

xpedx is reflected as a Discontinued Operation from 2010 onward

N.A. Consumer Packaging is reflected as a Discontinued Operation from 2013 onward

.12

.35

.40

.47 .45

.52.57

.73

.45.49

.41

.15

.07

.27

.38

.22

.05

.44

.85

.72.76 .77.78

.67

.58

.49

.77

.66

.58

.52

.91

.78

.59

.87 .87

.46

.79

.90 .91

.84

.78

.82 .83

.67

.56

.66

1.01

1.27

.42

.08

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

20172006 2007 20102008

Impact of Mineral

Rights Gain

2009

.83

2011

.93Final Land Sale

2012 2013 2014 2015 2016

Investor Roadshow | February 28, 2018

$ Million 2015 4Q16 2016 1Q17 2Q17 3Q17 4Q17 2017

Cash Provided by Operations

$2,580 $912 $2,478 $633 $645 ($709) $1,188 $1,757

Cash Invested in Capital Projects

($1,487) ($445) ($1,348) ($374) ($290) ($271) ($456) ($1,391)

Cash Contribution to Pension Plan

$750 - $750 - - $1,250 - $1,250

Kleen Products Settlement

- - - - - $354 - $354

Free Cash Flow $1,843 $467 $1,880 $259 $355 $624 $732 $1,970

Free Cash Flow

64

Investor Roadshow | February 28, 2018

Balance Sheet | Financial Strength

65

$ B

illio

n

3.2x

$9.3Balance

Sheet

Debt

$0.5 Op. Lease Adj. $0.5 Op. Lease Adj.

$3.4Pension Gap

20162015 2017

3.3x

[2.4x]1

Moody’s Target: Adjusted Debt < 3X Adjusted EBITDA

Pension gap decreased by $1.4B

Made $1.25B voluntary pension

contribution

Took meaningful measures to further

de-risk our pension plan

Year-end discount rate decreased

from 4.1% (2016) to 3.6% (2017)

Attractive $1.0B debt issuance partly

funded pension contribution

$ 1.0B cash balance at year end

$11.3Balance

Sheet

Debt

[3.2x]2

$0.5 Op. Lease Adj.

$3.6Pension Gap

4.0x

$11.2Balance

Sheet

Debt

$2.0Pension Gap

[3.0x]3

2017 Highlights

Moody’s methodology adjusted to exclude N.A. Consumer Packaging in 20171 Simple Debt Coverage: Balance Sheet Debt / 2015 IP’s Adjusted EBITDA of $3.9B2 Simple Debt Coverage: Balance Sheet Debt / 2016 IP’s Adjusted EBITDA of $3.5B3 Simple Debt Coverage: Balance Sheet Debt / 2017 IP’s Adjusted EBITDA of $3.7B

Investor Roadshow | February 28, 2018

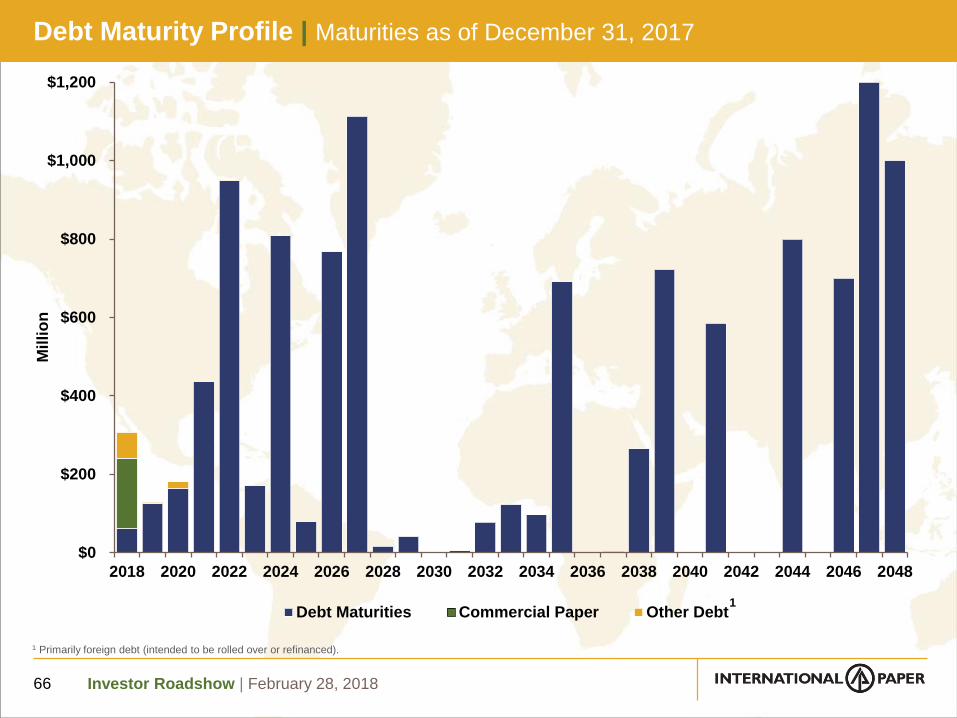

1 Primarily foreign debt (intended to be rolled over or refinanced).

Debt Maturity Profile | Maturities as of December 31, 2017

66

$0

$200

$400

$600

$800

$1,000

$1,200

2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048

Mil

lio

n

Debt Maturities Commercial Paper Other Debt1

Investor Roadshow | February 28, 2018

De-Risking the Company

67

Taking additional measures to reduce risk in our pension plan

– Making changes to the plan's asset allocation to emphasize more fixed income

– Reallocating the plan’s fixed income investments to longer duration maturities

– Expanding certain hedging strategies

– Transferred ~$1.3B of pension benefit obligations to Prudential (2H 2017)

IP is taking meaningful and deliberate steps to de-risk our pension plan

2004

Pension plan

closed to new

entrants

2014

Decision made to freeze

defined benefit pension plan

for active salary participants

effective 12/31/18

2016

Voluntary term-vested

buy out program

reduced plan size by

~10% and introduced

new LDI1 policy

Contributions2014

$353MM

2015

$750MM

2016

$750MM

2017

$1.25B

De-Risking

2017+

1 Liability Driven Investment

Investor Roadshow | February 28, 2018

Pension Plan Update | As of December 31, 2017

68

No contribution 1960-2005;

$2.5B contribution 2006-2013

$1.1B contribution made in

2014-2015

$750MM voluntary

contributions for 2016

$1.25B voluntary contribution

for 2017

No contribution required in

2018

($2.8)

($1.5)

($2.4)

($4.1)

($2.2)

($3.9)

($3.6)($3.4)

($2.0)

Billio

n

Year-End Funded Status1

1 Reflects status as of December 31

Investor Roadshow | February 28, 2018

Pension Plan Update1 | As of December 31, 2017

69

342

545

387

447

364

290

167

$0

$150

$300

$450

$600

$750

2012 2013 2014 2015 2016 2017 2018

Mil

lio

n

Annual Pension Expense2

Key Variables 2016 2017 2018

Assumed Rate of Return

7.75% 7.50% 7.50%

Discount Rate4 4.40% 4.10% 3.60%

Average Annualized Returns3

2017 19.3%

Past Five Years 9.4%

Past Ten Years 7.2%

Portfolio Asset Allocation at 12-31-17

Target Actual

Equity 42% - 53% 49%

Fixed Income 32% - 44% 36%

Real Estate 7% - 13% 10%

Other 3% - 8% 5%1 2013 and onward include Temple-Inland pension plan2 Non-cash expense for U.S. qualified and nonqualified plans 3 Through December 20174 Rate used to calculate pension expense

Pension expense reflects service cost, interest cost, amortization of actuarial losses and expected return on plan assets

For the past 10 years, IP Pension Plan performance ranked in the top decile of the State Street Bank Corporate and Public Master Trust Universe of approx. 125 observations

Investor Roadshow | February 28, 2018

25%

50%

75%

100%

125%

$0

$300

$600

$900

$1,200

$1,500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Maintenance Regulatory Strategic Cost Reduction % of Depreciation

$ Million% of

Depreciation

Years 2010-2017 continuing operations only

Capital Spending

70

~$1,500

Investor Roadshow | February 28, 2018

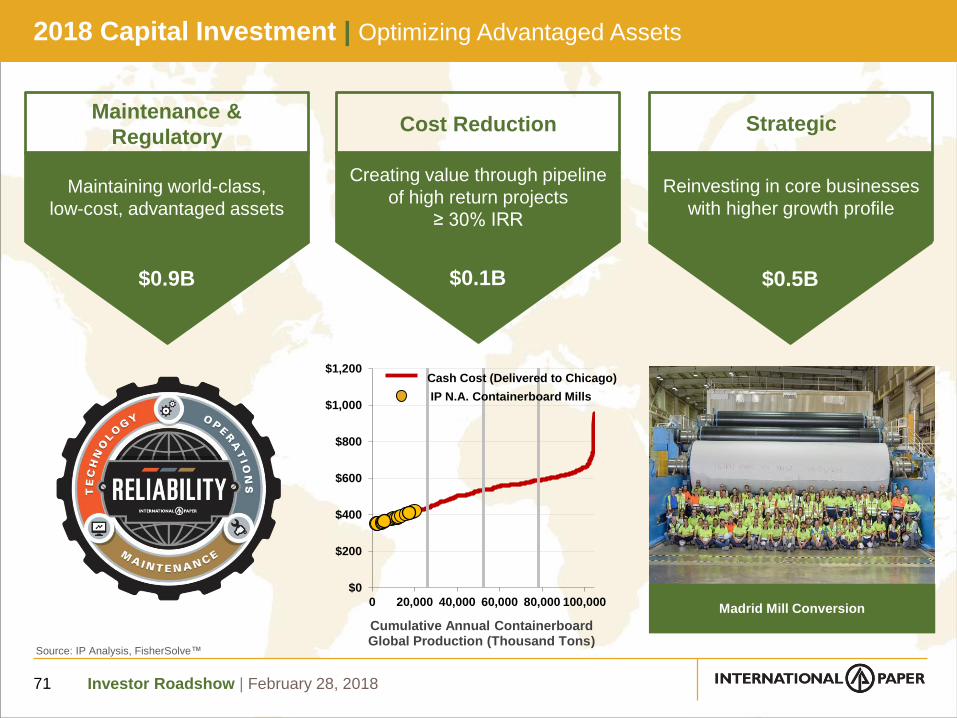

2018 Capital Investment | Optimizing Advantaged Assets

71

$0

$200

$400

$600

$800

$1,000

$1,200

0 20,000 40,000 60,000 80,000 100,000

Cumulative Annual Containerboard Global Production (Thousand Tons)

IP N.A. Containerboard Mills

Cash Cost (Delivered to Chicago)

Source: IP Analysis, FisherSolve™

Maintenance &

Regulatory

Maintaining world-class,

low-cost, advantaged assets

Madrid Mill Conversion

$0.9B $0.2B $0.4B

Cost Reduction Strategic

Creating value through pipeline

of high return projects

≥ 30% IRR

Reinvesting in core businesses

with higher growth profile

$0.1B $0.5B

Investor Roadshow | February 28, 2018

Maintenance Outages Expenses | 2017 Actual

72

$ Million 1Q17A 2Q17A 3Q17A 4Q17A 2017A

Industrial Packaging $71 $102 $38 $28 $239

North America 69 100 38 28 235

Europe 0 0 0 0 0

Europe Coated Paperboard 0 2 0 0 2

Brazil 2 0 0 0 2

Global Cellulose Fibers $50 $44 $7 $9 $110

North America 50 43 7 9 109

Europe 0 1 0 0 1

Printing Papers $23 $43 $1 $10 $77

North America 23 34 0 10 67

Europe 0 6 0 0 6

Brazil 0 3 0 0 3

India 0 0 1 0 1

Total Impact $144 $189 $46 $47 $426

Investor Roadshow | February 28, 2018

Maintenance Outages Expenses | 2018 Forecast

73

$ Million 1Q18F 2Q18F 3Q18F 4Q18F 2018F

Industrial Packaging $87 $122 $77 $22 $308

North America 81 117 77 22 297

Europe 0 0 0 0 0

Europe Coated Paperboard 5 3 0 0 8

Brazil 1 2 0 0 3

Global Cellulose Fibers $61 $44 $9 $36 $150

North America 59 37 9 36 141

Europe 2 7 0 0 9

Printing Papers $45 $50 $4 $9 $108

North America 32 29 0 9 70

Europe 8 17 0 0 25

Brazil 5 4 2 0 11

India 0 0 2 0 2

Total Impact $193 $216 $90 $67 $566

Investor Roadshow | February 28, 2018

North American Downtime

74

92141 125

86117 93

157

8546

230

85107 41

35

Maintenance Economic

30

11

25

010

24 25

111

3617

4

2918

0

55

7 11

13190

Containerboard

Uncoated Papers

Cellulose Fibers

Th

ou

sa

nd

To

ns

Th

ou

sa

nd

To

ns

322353

210193

158

13

212

128

Th

ou

sa

nd

To

ns

Investor Roadshow | February 28, 2018

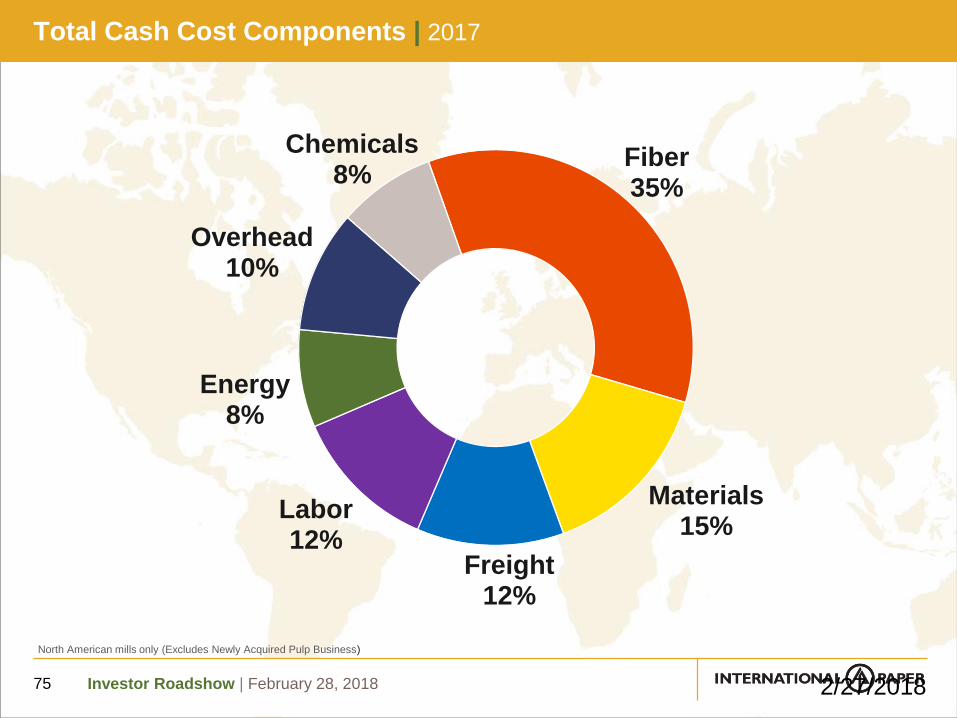

Total Cash Cost Components | 2017

75

Fiber35%

Materials15%

Freight12%

Labor12%

Energy8%

Overhead10%

Chemicals8%

2/27/2018

North American mills only (Excludes Newly Acquired Pulp Business)

Investor Roadshow | February 28, 2018

90

95

100

105

110

115

120

125

130

2017

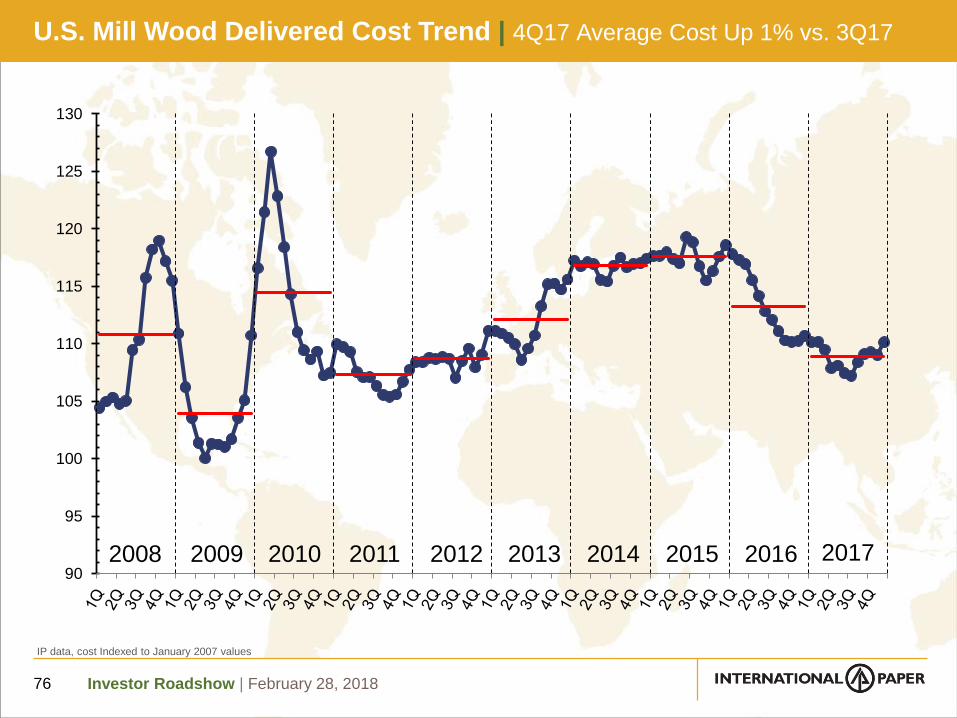

U.S. Mill Wood Delivered Cost Trend | 4Q17 Average Cost Up 1% vs. 3Q17

76

IP data, cost Indexed to January 2007 values

2008 2009 2010 2011 2012 2013 2014 2015 2016

Investor Roadshow | February 28, 2018

40

60

80

100

120

140

160

180

200

220

IP data, cost Indexed to January 2007 values

U.S. OCC Delivered Cost Trend | 4Q17 Average Cost Down 25% vs. 3Q17

77

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Investor Roadshow | February 28, 2018

U.S. Natural Gas Cost Trend | 4Q17 Average Cost Down 2% vs. 3Q17

78

0

50

100

150

200

250

IP data, cost Indexed to January 2007 values

NYMEX Natural Gas closing prices

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Investor Roadshow | February 28, 2018

0

50

100

150

200

250

300

U.S. Fuel Oil Cost Trend | 4Q17 Average Cost Up 16% vs. 3Q17

79

IP data, cost Indexed to January 2007 values

WTI Crude prices

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Investor Roadshow | February 28, 2018

75

100

125

150

175

200

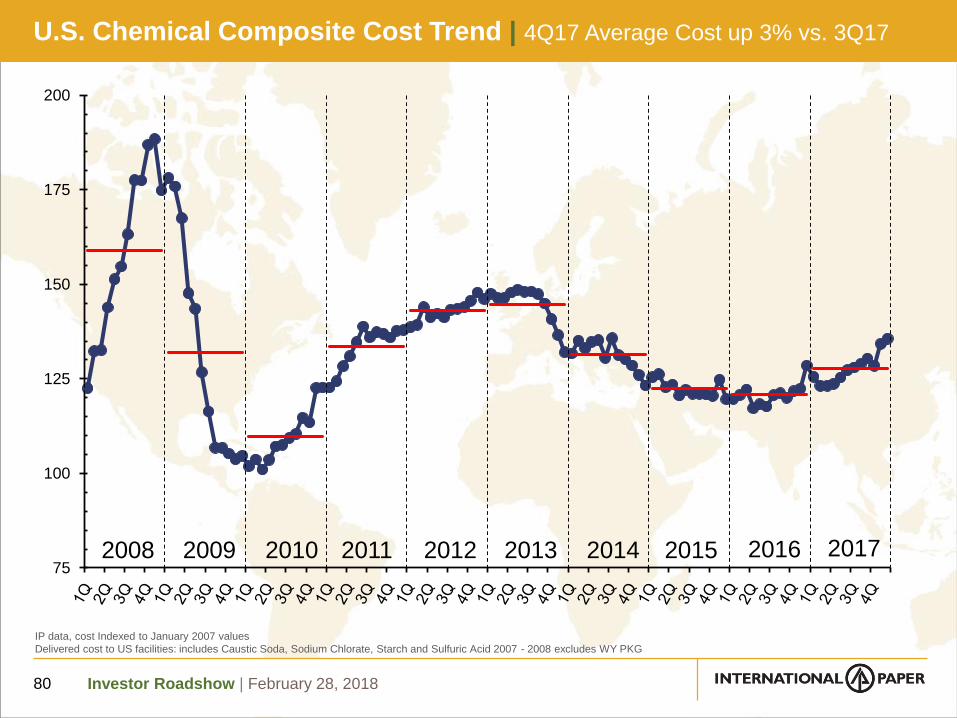

U.S. Chemical Composite Cost Trend | 4Q17 Average Cost up 3% vs. 3Q17

80

IP data, cost Indexed to January 2007 values

Delivered cost to US facilities: includes Caustic Soda, Sodium Chlorate, Starch and Sulfuric Acid 2007 - 2008 excludes WY PKG

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Investor Roadshow | February 28, 2018

2017 Global Consumption | Annual Purchases for Key Inputs

81

CommodityNorth

AmericaNon – North

America

Energy

Natural Gas (MMBTUs) 80,000,000 11,000,000

Fuel Oil (Barrels) 450,000 400,000

Coal (Tons) 85,000 550,000

FiberWood (Tons) 55,000,000 8,000,000

Old Corrugated Containers / DLK (Tons) 4,900,000 250,000

Chemicals

Caustic Soda (Tons) 420,000 70,000

Starch (Tons) 340,000 110,000

Sodium Chlorate (Tons) 170,000 50,000

LD Polyethylene (Tons) - -

Latex (Tons) - 10,000

Annual purchases exclude N.A. Consumer Packaging

Investor Roadshow | February 28, 2018

Global Citizenship | Sustainability throughout the Value Chain

82

Investor Roadshow | February 28, 20188383

Global Citizenship | The IP Way Forward

Investor Roadshow | February 28, 2018

Global Citizenship | Progress Toward our Vision 2020 Goals

8484

* Includes $3 million raised through employee giving and fundraising

WATER QUALITY PROGRESS

28% improvementin effluent water quality

SOLID WASTE PROGRESS

11% reductionin manufacturing waste to landfills

WATER STEWARDSHIP PROGRESS

Mapped water use and risk by location, identified priority mills and initiated annual stakeholder and facility assessments

SUPPLY CHAIN PROGRESS

Established baseline supply chain performance and implemented improvement plans

AIR EMISSIONS PROGRESS

23% reductionin air emissions(PM, SO2, NOx)

GHG EMISSIONS PROGRESS

19% reductionin greenhouse gas emissions

FIBER EFFICIENCY PROGRESS

0.79% fiber lossfrom reporting mills

SAFETY PROGRESS

39% reductionin serious safety incidents

COMMUNITY INVOLVEMENT PROGRESS

$17.3 milliondonated to charitable organizations in 2016*

ENERGY EFFICIENCY PROGRESS

6.4% improvementin purchased energy efficiency

FIBER CERTIFICATION PROGRESS

31% increasein certified fiber volume

RECYCLING PROGRESS

17% increasein recovery of OCC

Investor Roadshow | February 28, 2018

Investor Relations | Contact Information

85

Guillermo GutierrezVice President, Investor Relations

+1-901-419-1731

Michele VargasDirector, Investor Relations

+1-901-419-7287

Betty GroomFinancial & Administrative Analyst

+1-901-419-4250

Investor Roadshow | February 28, 2018

International Paper Brazil

Graphic Paper

Manufacture 2015

International Paper Russia

Corporate Social

Responsibility Award 2015

Named by the Ethisphere

Institute as one of the

“World’s Most Ethical

Companies®” 2018

2015 AF&PA Better

Practices, Better Planets

2020 Sustainability Award

International Paper India

Parivartan Award 2015

International Paper Awards & Recognitions

IDG’s Computerworld

“100 Best Places to

Work in IT” 2017

1 From FORTUNE Magazine, March 1, 2017. © 2017 Time Inc. Used under license2 From Commercial Appeal (Memphis, TN)

FORTUNE’S “World’s

Most Admired

Companies®” 2017

1

Commercial Appeal’s

“Top Workplace 2017”

2

Institutional Investor’s

“Most Honored Company” 2017

in the Paper & Packaging sector

Related Documents