INVESTOR PRESENTATION 09.14

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

I N V E S T O R P R E S E N T A T I O N 0 9 . 1 4

DISCLAIMER AND OTHER MATTERS

SAFE HARBOR: Some statements contained in this presentation are forward-looking statements within the meaning of the Private Securities LitigationReform Act of 1995 and applicable Canadian securities laws. Investors are cautioned that forward-looking statements are inherently uncertain and involverisks and uncertainties that could cause actual results to differ materially. Such statements include comments regarding: the timing for closing higher costrefractory operations; transformation of Golden Star to a low cost underground gold producer and the timing thereof; our production expectations for 2014,including our production guidance for 2014; the timing for completing mining at Bogoso North and Chujah; predictions regarding cash operating costs perounce for 2014 and over the life of mine target; estimated capital expenditures; anticipated all-in sustaining costs over the life of mine target; expectedcash flow over the remainder of 2014 and the life of mine targets; timing of drilling, the acceleration of cash flows due ot underground mining at Wassa;anticipated blended head grades at Wassa and Wassa Underground; life of mine for Wassa and Wassa Underground; use of the existing Wassa processingplant and Bogoso oxide and sulfide processing plants; estimated post-tax internal rate of return and net present value (including assumed discount rate) atWassa Underground; estimated capital expenditures and timing of capital expenditures at Wassa Underground; sensitivities of the Wassa undergroundeconomic model; timing of Wassa Underground construction; timing of Wassa underground to commercial production; the sufficiency of funding to advancethe development of Wassa Underground; timing for completion of mining at Bogoso; timing of revised preliminary economic assessment at PresteaUnderground; timing of Prestea Underground to commercial production; operational risk of mining in Ghana; and our expectations regarding explorationand development upside. Factors that could cause actual results to differ materially include timing of and unexpected events at the Bogoso oxide andsulfide processing plants and/or at the Wassa processing plant; variations in ore grade, tonnes mined, crushed or milled; variations in relative amounts ofrefractory, non-refractory and transition ores; delay or failure to receive board or government approvals and permits; the availability and cost of electricalpower; timing and availability of external financing on acceptable terms; technical, permitting, mining or processing issues, including difficulties inestablishing the infrastructure for Wassa Underground; changes in U.S. and Canadian securities markets; and fluctuations in gold price and input costs andgeneral economic conditions. There can be no assurance that future developments affecting the Company will be those anticipated by management. Pleaserefer to the discussion of these and other factors in our Annual Information Form for the year ended December 31, 2013. The forecasts contained in thispresentation constitute management's current estimates, as of the date of this presentation, with respect to the matters covered thereby. We expect thatthese estimates will change as new information is received and that actual results will vary from these estimates, possibly by material amounts. While wemay elect to update these estimates at any time, we do not undertake to update any estimate at any particular time or in response to any particular event.Investors and others should not assume that any forecasts in this presentation represent management's estimate as of any date other than the date of thispresentation.

NON-GAAP FINANCIAL MEASURES: In this presentation, we use the terms "cash operating cost per ounce” and “all-in sustaining cost per ounce”. Theseterms should be considered as Non-GAAP Financial Measures as defined in applicable Canadian and United States securities laws and should not beconsidered in isolation or as a substitute for measures of performance prepared in accordance with GAAP. “Cash operating cost per ounce” for a period isequal to the cost of sales excluding depreciation and amortization for the period less royalties and production taxes, minus the cash component of metalsinventory net realizable value adjustments divided by the number of ounces of gold sold during the period. “All-in sustaining costs per ounce” commenceswith cash operating costs and then adds sustaining capital expenditures, corporate general and administrative costs, mine site exploratory drilling andgreenfield evaluation costs and environmental rehabilitation costs. This measure seeks to represent the total costs of producing gold from operations Thesemeasures are not representative of all cash expenditures as they do not include income tax payments or interest costs. These measures are not necessarilyindicative of operating profit or cash flow from operations as would be determined under International Financial Reporting Standards. Changes in numerousfactors including, but not limited to, mining rates, milling rates, gold grade, gold recovery, and the costs of labor, consumables and mine site general andadministrative activities can cause these measures to increase or decrease. We believe that these measures are the same or similar to the measures ofother gold mining companies, but may not be comparable to similarly titled measures in every instance.INFORMATION: The information contained in this presentation has been obtained by Golden Star from its own records and from other sources deemedreliable, however no representation or warranty is made as to its accuracy or completeness. The technical information relating to Golden Star’s materialproperties disclosed herein is based upon technical reports prepared and filed pursuant to National Instrument 43-101 Standards for Disclosure of MineralProperties (“NI 43-101”) and other publicly available information regarding the Company, including the following: (i) “NI 43-101 Technical Report onMineral Resources and Mineral Reserves Golden Star Resources Ltd, Wassa Gold Mine, Ghana Effective Date December 31, 2012”, prepared by SRKConsulting (UK) Limited and prepared under the supervision of Martin P. Raffield and S. Mitchel Wasel; (ii) Golden Star’s press release dated February 10,2014; (iii) Golden Star’s Annual Report for 2013; and (iv) Golden Star’s press release dated September 15, 2014. Additional information is included inGolden Star’s Annual Information Form for the year ended December 31, 2013 which is filed on SEDAR. Mineral Reserves were prepared under thesupervision of Dr. Martin Raffield, Senior Vice President Technical Services for the Company. Dr. Raffield is a "Qualified Person" as defined by Canada'sNational Instrument 43-101. The Qualified Person reviewing and validating the estimation of the Mineral Resources is S. Mitchel Wasel, Golden StarResources Vice President of Exploration.

CURRENCY: All monetary amounts refer to United States dollars unless otherwise indicated.

Golden Star Resources September 20142

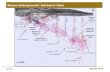

— 15 year history in Ghana— Three mines – Wassa, Bogoso

and Prestea— Located on Ashanti gold belt

close to major gold producers — 3.9M oz. Reserves and further

2.1M oz. of M & I Resources1, 2

— Total processing capacity of 6.9 mtpa

— Historical production circa 300,000 oz. per annum

— Listed on the NYSE, TSX and in Ghana

INTRODUCTION TO GOLDEN STAR

Golden Star Resources September 20143

1. Please refer to the relevant disclosure on Mineral Reserve and Mineral Resource Estimates contained in the Company’s Annual Report for the year ended December 31, 2013.

2. All Mineral Resources for Wassa Main and Wassa Underground are as at September 15, 2014. Please refer to the to the relevant disclosure on Mineral Resource Estimates contained in Company’s announcement of the same date.

— Major cost reductions being achieved at existing operations — Higher cost refractory operations to close in late 2015— Significant high grade underground reserve at Prestea with extensive

exploration upside— Major new underground discovery at Wassa— Capital expenditure of less than $100 million on these two low cost

projects unlocks significant value — Golden Star will transform to a low cost gold producer by 2017

STRATEGIC DIRECTION

Golden Star Resources September 20144

BOGOSO MINE

— 2.0M oz. of Mineral Reserves1 at 3.17 g/t Au— Significant portion are in high grade

refractory deposits

— Mining in Bogoso North and Chujah pits only, 400,000 oz. in Mineral Reserves1

— 2014E production of 145-155,000 oz.

— Mining complete end 2015

— Major pushbacks recently completed, now cash flow positive

— Tailings retreatment continues— FY2014E cash costs $1,100-1,200— Tarred road to site and power supplied by

national grid— Strategic value in two processing plants

— Tailings retreatment

— Third party ore treatment

— Prestea Underground

1. Based on December 31, 2013 Mineral Reserve and Resource estimate. Please refer to Company's press release dated 10 February 2014.

Golden Star Resources September 20145

PRESTEA UNDERGROUND

— Existing high grade underground mine, suspended in 2002

— Historical production of over 9M oz.

— High grade ore body, 18 g/t Au in situ

— 440,000 oz. Mineral Reserves1 with scope to grow with further drilling

— Non refractory free milling ore

— M & I Mineral Resource of 630,000 oz.1

— Ore to be processed at Bogoso plant

— Mine located 15 km’s from plant along dedicated haul road

— Full support from Government and community to develop

Golden Star Resources September 20146

1. Based on December 31, 2013 Mineral Reserve and Resource estimate. Please refer to Company's press release dated 10 February 2014.

PRESTEA UNDERGROUND

— 2013 Feasibility Study demonstrated positive economics

— Lower capex, quicker production alternative evaluated in Q2 2014

— Shrinkage mining = less dilution

— Significantly lower capex

— Quicker to production

— Similar cash operating costs per ounce to Feasibility Study

— Progressing to PEA, expected to be complete Q4 2014

— 2.0M oz. of Mineral Reserves at 1.75 g/t Au1

— One large open pit - Wassa Main— Non-refractory plant with 2.7 mtpa

capacity performing well— 500 meters from Wassa Main pit

— Easy access by road and on national power grid

— 2014E production of 115-125,000 oz.— Closure of high grade, high cost

satellite pit

— FY2014E cash costs $925-1,000/oz.— Operating cash costs and expenses

reducing

1. Based on December 31, 2013 Mineral Reserve and Resource estimate. Please refer to Company's press release dated 10 February 2014.

WASSA MINE

Golden Star Resources September 20148

Indicated Resource Inferred Resource

WASSA RESOURCE DEVELOPMENT 2013

Golden Star Resources September 20149

— Two year LOM in 2011, two year drilling campaign increased this by 148%, despite reducing gold price

— Steady and deliberate drill programme undertaken as understanding of deposit evolved

— Higher grade appeared at depth

Indicated Resource Inferred Resource

WASSA RESOURCE DEVELOPMENT H1 2014

Golden Star Resources September 201410

— Decision taken to do step out drilling to determine strike length

— Longer strike length allows for higher underground tonnage

— PEA delayed to allow for assessment of larger scale underground mine

Indicated Resource Inferred Resource

WASSA RESOURCE DEVELOPMENT H2 2014

Golden Star Resources September 201411

— Deposit remains open in all directions

— Concession extends for over 5 kilometers to the south in the direction of strike

— Further open pit and underground optimisation possible in Feasibility Study

WASSA MINERAL RESOURCE UPDATE

— Total M&I Mineral Resources of 35,7 Mt @ 2.22 g/t Au for 2,5M oz.

— Open pit constrained to 200 m depth with underground below that, thus eliminating lower grade deep material from block model

— Increase in grade of 18%

— Includes 7 months of depletion from mining since end 2013

— Inferred Mineral Resources increased substantially to 9 Mt @ 3.88 g/t Au for 1.1M oz.

— Updated resource model includes infill at depth and step out to south

— $1,400 gold price assumption used to derive cutoff grade and optimised pit shell

— Open pit cutoff grade of 0.58 g/t Au for oxide and 0.61 g/t Au for fresh

— Underground cutoff grade of 2.27 g/t Au

Golden Star Resources September 201412

OPEN PIT VS. UNDERGROUND RESOURCE ESTIMATE AND MINE DESIGN

— Open pit constrained to 200 m depth in $1,000/ oz. pit shell

— Decline will be developed from starter pit

— All ore feed will be from within 500 metres of plant

Golden Star Resources September 2014

OpenPit

Under-ground

13

WASSA PEA KEY FINDINGS @ AU PRICE $1,300

— Post-tax IRR of 129% — Post-tax NPV5% of $350 million— Underground pre-production capex estimated at $41 million — Average combined annual production 174,000 ounces for first 5 years of

combined production, 120,000 ounces per annum thereafter— First production from Wassa underground expected early 2016, 10 year

LOM thereafter— LOM cash operating costs of US$684/ oz.— LOM all-in sustaining costs of US$778/ oz.

14 Golden Star Resources September 2014

WASSA PEA KEY FINDINGS SENSITIVITY

Golden Star Resources September 201415

— Robust economics

— At Au price of $1,230, IRR is 90% and post tax NPV5% is $295 million

— Returns most sensitive to Au price, less so to costs

— Low capex makes sensitivity of returns negligible

Post - Tax NPV5% NPV10% IRR

Gold Price

$ 1,000 $111 $67 25%$ 1,100 $191 $136 47%$ 1,200 $271 $203 78%$ 1,300 $350 $269 129%$ 1,400 $433 $338 234%$ 1,500 $515 $407 615%$ 1,600 $597 $476 n/a

WASSA PRODUCTION AND COSTS

Golden Star Resources September 201416

400

500

600

700

800

900

1,000

1,100

1,200

-

50

100

150

200

250

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

Cos

ts p

er O

unce

US$

Gol

d Pr

oduc

tion

–O

unce

s 00

0’s

Gold Production CoC AiC

CATALYSTS FOR VALUE CREATION

Wassa decline construction begins

PEA on underground mining at Wassa complete

Establish Wassa Main pit

Complete push back at Bogoso

Updated Mineral Resource estimate for Wassa

Q3 2014 Q4 2014Q2 2014 2015 2016

Operational cost savings achieved

Revised PEA for Prestea Underground

First production Wassa Underground

First production from Prestea Underground

* Development of projects dependent on positive study results and adequate access to finance

Golden Star Resources September 201417

Wassa Feasibility complete

Investment Case

Established gold mining company with 15 years of production history in Ghana

3.9M oz. in Mineral Reserves & a further 2.1M oz. in Measured & Indicated Mineral Resources

Successfully reduced overall operating costs over last two years

Delivering on stated strategy of low cost, low capex growth

Offers investors leveraged, un-hedged exposure to the gold price

Low operational risk in a stable African mining jurisdiction

Significant exploration & development upside development

Golden Star Resources May 201418

INTRODUCTION TO GHANA

Golden Star Resources September 201419

— Attractive investment destination and top African mining jurisdiction

— Stable inclusive democracy — S&P credit rating of B — Second largest producer of gold in Africa— Strong mining culture and trained

personnel

— Golden Star well positioned in country— Large property positions and excellent

geological knowledge base— Solid and longstanding relationships with

the government and communities — COO is former President of the Ghana

Chamber of Mines

(1) Includes US$55.1M of 5% Convertible Debentures at fair value(2) As accessed on September 3, 2014 from Bloomberg(3) As a group, beneficially owned, or controlled or directed, directly or indirectly as at June 30, 2014

Major Shareholders2

Heartland Advisors Inc. 12.1%

Sentry Select Capital Corp. 10.9%

Van Eck Associates Corp. 8.7%

Directors and Executive Officers3 2.8%

Sprott Inc 2.5%

BNP Paribas 1.7%

Share Price (Last close) (US$) (as of September 12, 2014) 47 cents

Shares Outstanding 259.1M

Market Capitalization (US$) 121M

Cash and Equivalents (US$) (June 30, 2014) 43M

Total Debt (US$) (June 30, 2014)1 115.8M

Enterprise Value (US$) 194.2M

Daily Average Volume TSX: 145KNYSE MKT: 1.8M

STRONG SPONSORSHIP, GOOD LIQUIDITY

Golden Star Resources September 201420

— Listed on NYSE AMEX, TSX and Ghana Stock Exchange

MANAGEMENT AND BOARD

Sam CoetzerPresident and CEO

Sam was appointed CEO in January 2013 after joining Golden Star in March 2011 as COO. Sam is a mining engineer and a member of the World Gold Council. He has over 26 years of international mining experience with Kinross, Xstrata, Xstrata Coal and Placer Dome.

André van NiekerkEVP and CFO

André joined Golden Star in 2006 and spent five years in Ghana as the head of finance and business operations, after which he transferred to the corporate office as Controller. André was appointed to the role of CFO in 2014. Prior to joining Golden Star, André spent six years with KPMG serving clients in the mining and oil and gas industries

Daniel OwireduEVP and COO

Daniel was appointed COO in January 2013, after joining Golden Star in September 2006 as VP, Ghana Operations. He has more than 20 years of experience in the mining sector in Ghana and West Africa. Most recently, Daniel was Deputy Chief Operating Officer for AngloGold Ashanti where he successfully managed the construction and operation of the Bibiani, Siguiri, and the Obuasi mines.

Tim BakerChairman

Tim was appointed Chairman in January 2013. Tim most recently served as the COO of Kinross. He is a geologist with over 30 years of global project development and operational experience in Chile, Tanzania, United States, Venezuela, Kenya and Liberia.

Tony JensenDirector

Tony has over 25 years of mining industry experience and is CEO of Royal Gold Inc. Prior to joining Royal Gold, Tony was the Mine General Manager of the Cortez Joint Venture and spent eighteen years with Placer Dome. Tony has extensive experience in operations in the United States and Chile where he held several senior management positions.

Chris ThompsonDirector

Chris has 40 years of experience in international mining. Chris formerly served as Chairman and CEO of Gold Fields Limited, Chairman of the World Gold Council and Founder, President and CEO of Castle Group Inc. Chris has held directorships at over 25 public gold mining companies

Anu is the Managing Director of MiniqsLimited, a private group primarily interested in developing resource projects. She is also a Director of Atlatsa Resources, Frontier Rare Earths, and of EnergulfResources. Prior to founding Miniqs, Anu was VP, Corporate Development and Company Secretary at Katanga Mining.

Anu DhirDirector

MANAGEMENT AND BOARD

Craig is a geologist with over 30 years of experience in the mining business. He is Founder, CEO and Director of Avanti Mining. Formerly, Craig was EVP, Exploration of Gold Fields Limited; Founder, CEO and Chairman of the former Metallica Resources (now New Gold), and held a variety of strategic positions at Lac Minerals.

Robert has more than 30 years of mining; from international resource exploration, development, and fundraising, to production. Most recently, he was Founder, and CEO of Medoro Resources, now Gran Colombia Gold Corp. Prior to this, he served as CFO of Pacific Stratus Energy, CFO of Coalcorp Mining and CFO of Bolivar Gold Corp. Currently, Robert serves as a Director of Mandalay Resources and Detour Gold

Craig NelsonDirector

Rob DoyleDirector

Bill YeatesDirector

Bill was one of the founding partners of Hein & Associates LLP where he served on the Executive Committee and was their National Director of Auditing and Accounting. Bill has over 40 years of auditing experience working with public companies specializing in extractive industries. From 2005 to 2009, he served on the Financial Accounting Standards Advisory Council.

PROVEN AND PROBABLE RESERVES

Dec 31, 2013 Proven

Mineral Reserve

Dec 31, 2013 Probable

Mineral Reserve

Dec 31, 2013 Proven and Probable

Mineral Reserve

tonnes(000)

gradeg/t Au

ounces(000)

tonnes(000)

gradeg/t Au

ounces(000)

tonnes(000)

gradeg/t Au

ounces(000)

Wassa Main - - - 33,721 1.72 1,863 33,721 1.72 1,863

Father Brown - - - 694 4.31 96 694 4.31 96

Stockpiles 438 0.68 10 59 0.54 1 497 0.67 11

Subtotal Wassa 438 0.68 10 34,473 1.77 1,960 34,911 1.75 1,970

Bogoso 2,930 2.65 250 1,731 2.59 144 4,662 2.63 394

Dumasi 3,116 2.39 239 5,826 2.36 443 8,941 2.37 682

Mampon - - - 1,133 5.24 191 1,133 5.24 191

Prestea South 969 2.74 85 2,170 2.52 176 3,139 2.59 261

Prestea Underground - - - 1,434 9.61 443 1,434 9.61 443

Stockpiles 106 1.79 6 - - - 106 1.79 6

Subtotal Bogoso 7,122 3 581 12,294 4 1,397 19,415 3 1,977

Total 7,559 2.43 590 46,767 2.23 3,357 54,327 2.26 3,947

* Please refer to the relevant disclosure on Mineral Reserve and Mineral Resource Estimates contained in our Annual Report for the year ended December 31, 2013

Golden Star Resources September 201423

MEASURED AND INDICATED MINERAL RESOURCES1

Dec 31, 2013 Measured

Mineral Resources

Dec 31, 2013 Indicated

Mineral Resources

Dec 31, 2013 Measured and Indicated

Mineral Resources

tonnes(000)

gradeg/t Au

ounces(000)

tonnes(000)

gradeg/t Au

ounces(000)

tonnes(000)

gradeg/t Au

ounces(000)

Wassa Main2 - - - 25,582 1.41 1,160 25,582 1.41 1,160

Wassa Underground2 - - - 10,116 4.27 1,389 10,116 4.27 1,389

Father Brown - - - 692 3.86 86 692 3.86 86

Father Brown Underground - - - 1,000 6.47 208 1,000 6.47 208

Wassa Other - - - 2,115 2.40 163 2,115 2.40 163

Subtotal Wassa - - - 39,505 2.37 3,007 39,505 2.37 3,007

Bogoso 2,697 2.94 255 1,856 2.95 176 4,553 2.94 431

Dumasi 3,255 2.56 268 9,868 2.41 764 13,123 2.45 1,032

Mampon - - - 1,553 4.79 239 1,553 4.79 239

Prestea South 986 2.87 91 3,318 2.62 279 4,304 2.67 370

Prestea Underground - - - 1,356 14.50 632 1,356 14.50 632

Bogoso Other - - - 3,835 2.64 325 3,835 2.64 325

Subtotal Bogoso 6,938 2.75 614 21,786 3.45 2,415 28,724 3.28 3,029

Total 6,938 2.75 614 61,291 2.75 5,422 68,229 2.75 6,036 1. Please refer to the relevant disclosure on Mineral Reserve and Mineral Resource Estimates contained in the Company’s Annual Report for the year ended December 31,

2013. 2. All Mineral Resources for Wassa Main and Wassa Underground are as at September 15, 2014. Please refer to the to the relevant disclosure on Mineral Resource

Estimates contained in Company’s announcement of the same date.

Golden Star Resources September 201424

INFERRED MINERAL RESOURCES1

Dec 31, 2013 Inferred Mineral Resources

tonnes(000)

gradeg/t Au

ounces(000)

Wassa Main2 237 1.56 12

Wassa Underground2 8,841 3.95 1,122

Father Brown 40 1.85 2

Father Brown Underground 881 6.35 180

Wassa Other 85 2.93 8Subtotal Wassa 10,084 4.08 1,324

Bogoso 288 2.08 19

Dumasi - - -

Mampon 221 1.79 13

Prestea South 581 6.00 112

Prestea Underground 3,289 8.02 848

Bogoso Other 892 2.37 68

Subtotal Bogoso 5,271 6.25 1,060

Total 15,355 4.83 2,384

Golden Star Resources September 201425

1. Please refer to the relevant disclosure on Mineral Reserve and Mineral Resource Estimates contained in the Company’s Annual Report for the year ended December 31, 2013.

2. All Mineral Resources for Wassa Main and Wassa Underground are as at September 15, 2014. Please refer to the to the relevant disclosure on Mineral Resource Estimates contained in Company’s announcement of the same date.

Related Documents