Investor & analyst presentation June 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Investor & analyst presentationJune 2016

Redefine International P.L.C. Investor & analyst presentation

June 2016

Redefine International P.L.C.Who we are and what we do

Redefine International is a FTSE 250 UK Real Estate Investment Trust focused on income driven total returns and committed to delivering superior distributions to its shareholders throughout the property cycle.

Redefine International holds a primary listing on the London Stock Exchange and a secondary listing on the Johannesburg Stock Exchange. The Company is included within the EPRA and FTSE 250 indices.

Introduction

2Redefine International P.L.C.

Investor & analyst presentationJune 2016

Redefine International P.L.C. Investor & analyst presentation

June 2016

09:30 – 10:00 Welcome and registration

10:00 – 10:30 Charing Cross Road, Central London

10:30 – 11:30 Transit; Presentation

11:30 – 12:30 Priory Retail Park, Merton, London

12:30 – 13:30 Transit; Lunch

13:30 – 14:00 Camino Park, Crawley

14:00 Transport to Gatwick Express

15:00 Arrive at London Victoria

3

Itinerary

Redefine International P.L.C. Investor & analyst presentation

June 2016

4

Redefine International P.L.C. Investor & analyst presentation

June 2016

Redefine International P.L.C. Investor & analyst presentation

June 2016

Schloss Strassen Shopping Centre, Berlin

Investment

Proposition

Redefine International P.L.C. Investor & analyst presentation

June 2016

Continued transformation

delivering valueTransformed corporate structure and asset base offer foundation to drive

further value

Market-leading dividends

Proven track record of delivering superior dividends throughout the

property cycle

Secure income stream

Diversified portfolio and tenant base, with WAULT of 8.1 years

complemented by a debt maturity of 7.4 years of which >90% interest cost is

fixed

Lean but intensive management

structureHands on and transparent

management style, allowing for fast and effective reaction to opportunities

Effective, opportunistic capital

allocationInvestment philosophy to efficiently recycle capital to sectors/ locations with strong occupier fundamentals

and assets with realisable upside

Further income and value opportunities

Strategy to continue enhancing the portfolio quality and deliver occupier

led assets management initiatives

6

Focused on income driven total returns in a market where reliable income is increasingly attractive

Income driven total returns are underpinned by a diversified portfolio and efficient capital structure

Redefine International Investment Proposition

Redefine International P.L.C. Investor & analyst presentation

June 2016Delivered value throughout a five year transformation

(1) Market cap of £830m as at 10 June 2016

Committed to delivering superior distributions to shareholders

Annualised total shareholder returns of c.25% since 2012 equity raise

Significant efforts over last 5 years have transformed both the corporate structure and asset base

Reverse takeover of Wichford P.L.C.

Admitted to Premium listing

UK REIT conversion Internalisation of management

JSE secondary listing

Acquisition of Weston Favell Shopping Centre

for £84m

Repayment of over£250m of legacy financing facilities£127m equity raise

German shopping centre acquisition

€189m

Included in the FTSE 250 and EPRA indices£55m equity raise

German Retail Portfolio (“Leopard”) €157m Sold

non-core assets, including Cromwell and

Swiss portfolio

£70m equity raise

£115m equity raise

£490m AUK acquisition

2011 2012 2013 2014 2015 2016

31 August 2011

Market Cap (£m) 227

Portfolio Value (£m) 1,077

Underlying distributable earnings (£m) 20.3

LTV (%) 75.4

29 February 2016 (HY)

Market Cap(1) (£m) 626

Portfolio Value (£m) incl non-core 1,524

Underlying distributable earnings (£m) 25.4

Pro-forma LTV (%) 52.5

7

Redefine International P.L.C. Investor & analyst presentation

June 2016

8

Committed to maintain a superior dividend yield across UK listed real estate sector

Targeting dividend growth of 1-2% over the medium term whilst simultaneously reducing payout ratio to 90%

Market-leading dividends

0%

1%

2%

3%

4%

5%

6%

7%

8%

2016E Dividend yield (%)

Source: Factset as at 17 June 2016

Redefine International (>7%)

London Specialists (1.3%)

Developers (3.0%)

UK Majors (3.9%)

Mid-cap Income Specialists (5.6%)

Redefine International P.L.C. Investor & analyst presentation

June 2016

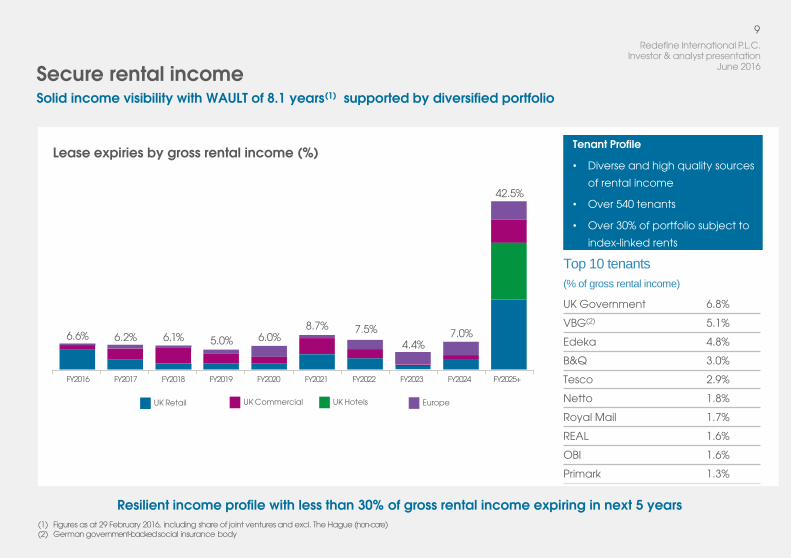

Tenant Profile

• Diverse and high quality sources

of rental income

• Over 540 tenants

• Over 30% of portfolio subject to

index-linked rents

UK Government 6.8%

VBG(2) 5.1%

Edeka 4.8%

B&Q 3.0%

Tesco 2.9%

Netto 1.8%

Royal Mail 1.7%

REAL 1.6%

OBI 1.6%

Primark 1.3%

Top 10 tenants

(% of gross rental income)

9

Solid income visibility with WAULT of 8.1 years(1) supported by diversified portfolio

Resilient income profile with less than 30% of gross rental income expiring in next 5 years

(1) Figures as at 29 February 2016, including share of joint ventures and excl. The Hague (non-core)(2) German government-backed social insurance body

Secure rental income

Lease expiries by gross rental income (%)

UK Retail UK Hotels EuropeUK Commercial

6.6% 6.2% 6.1% 5.0% 6.0%4.4%

42.5%

8.7% 7.5% 7.0%

FY2016 FY2017 FY2018 FY2019 FY2020 FY2021 FY2022 FY2023 FY2024 FY2025+

Redefine International P.L.C. Investor & analyst presentation

June 2016

10

AUK acquisition enhances ability to more actively allocate & recycle capital into new opportunities to deliver the

best risk adjusted returns

Effective, opportunistic capital allocation

Recycled

Streamlined geographical footprint which is nowfocused in Europe’s two largest economies

Realised capital from mature assets which have met their business plan

AUK opportunity

Off-market transaction

Achieved in a highly completive UK property market, owing to flexible

two tranche deal structure

Investment philosophy to invest in assets with resilient income returns and realisable growth opportunities

Clear value-add opportunities

Business plan attached to each asset

Early success

Early progress on income-led asset management initiatives with significant scope to continue

through the cycle

Redefine International P.L.C. Investor & analyst presentation

June 2016

• Enhanced exposure to assets with stronger property

fundamentals providing income-led asset management

opportunities

• More active capital recycling

• Investment market remains strong for secure income

• Disposals to focus on mature and underperforming

assets

11

AUK improves portfolio exposure to sub-sectors with good income and value growth prospects

Outlook supports our targeted sectors with clearly identified opportunities to add value and capitalise on current

occupational market trends

Portfolio repositioned for further income growth

th

c

cc

Market value by geography Market value by sector

Hotels

15%29%

9%

10%12%

18%

22%

12%

11%23%

21%

6%5%5%

2%Retail Parks

Regional Offices

Distribution

London Offices

Industrial & Automotive

Germany

Shopping Centres

Other

Greater London

Big 6 UK cities

Big 5 German cities

UK South

Dominant regional shopping centres

Other

Redefine International P.L.C. Investor & analyst presentation

June 2016

12

Flexible AUK facility presents further capital structure efficiencies and even lower cost of debt opportunities

Capitalising on low interest rate environment and utilising lower leverage on refinancing to attract lower cost of

debt

All figures as at 29 February 2016

Efficient capital structure

Positive direction of travel

52.5%Pro-forma LTV

Target LTV 40% - 50%

3.6%Cost of debt %

Post half year results cost of debt reduced

to 3.4% with opportunities to decrease

further

7.4 yearsDebt maturity

All near term maturities extended or under negotiations with no significant maturities until 2020

>90%Debt at fixed or capped rates

19.5%Principal debt with no LTV

covenants

20bpsFurther reduction in cost of debt %

Recent extensions and AUK Tranche II drawdown reduced

cost of debt to 3.4% (2016HY 3.6%)

Flexible funding£148m revolving credit facility providing opportunity to consolidate

debt and reduce interest costs further

Opportunity to reduce margin on all AUK debt by 15bps if LTV reduced to <50%

Camino Park Distribution Centre, Crawley

Portfolio

Redefine International P.L.C. Investor & analyst presentation

June 2016

14

Geographical focus in Europe’s two largest economies

Balanced exposure to retail, commercial and hotel sectors, supported by

in-house sector specialist asset managers

Secure income returns underpinned by diversified portfolio

UK

London

Redefine International P.L.C. Investor & Analyst Presentation

June 2016

15

All low yielding AUK offices with high vacancies were strategically weighted to Tranche 2

AUK adds high quality offices with immediate upside in filling vacancies which are progressing well

All figures as at 29 February 2016

UK Commercial - Offices

Gross annualised rental income

Latest asset management successes include:

• Charing Cross, London renewals average +29% on passing rent

• Swindon 15 year lease signed with OBU >40% above ERV

94.1%

Occupancy by lettable space:

Majority of vacancies in the high quality AUK regional

offices

4.7 yearsWAULT

Early stage renegotiation of 8 UK government leases totalling gross rent of £3.8m due to expire 31 March 2018

and considering alternate uses

5.2%Net initial yield

5.9% Topped up yield6.9% Reversionary yield

24Total number of UK offices:

4 in Greater London, 8 in Big 6 UK Cities, 3 in UK

South East

94,975Square metres

Average gross rent £17.2 per sqft vs ERV of

£17.4 per sqft

£16.5m

Redefine International P.L.C. Investor & Analyst Presentation

June 2016

16

Progress in filling vacancies, current occupancy at 86% (+590bps since acquisition)

AUK Offices - Income opportunities

Remaining 14% voids in Manchester, Leeds and

Reigate

+£1.2mERV

Vacancies filled to date

+£0.5mGross rent

Market evidence

£80-£100Per sqft

Rental achieved on latest rent reviews +29% on passing

<£40Per sqftCurrent rent for 1st/2nd floor tenant; rent review

Oct 2016

127-133 Charing Cross Road, LondonPositive direction of travel

+9 floors

Immediate neighbours to Charing Cross Road office recently secured planning

permission

£60Per sqft

<£40Per sqft

Redefine International P.L.C. Investor & Analyst Presentation

June 2016

99.2%

9.0 years

6.3%

14

237,621

17

Latest leasing transactions in shopping centres reflect rents at or ahead pre-downturn rental values

All figures as at 29 February 2016

UK Retail

Gross annualised rental income

Opportunity for modest rental growth, reconfiguration of existing space and further development activity

Occupancy by lettable space:

Shopping centres nearlyfully occupied at 98.9%

WAULT

Good quality tenants weighted towards non-discretionary food

retailers, discounters and leisure

Net initial yield

6.6% topped up andreversionary yield

Total number of UK retail assets:

Including 3 in Greater London and 5 regionally

dominant shopping centres

Square metres

Supply demand imbalance combined with long leases

presents opportunity to eliminate Retail Park over- rent

£41.4m

Redefine International P.L.C. Investor & Analyst Presentation

June 2016

18

National retail park vacancy at a 14 year low, reflected in our fully occupied retail parks

Strong tenant demand at retail parks creating opportunities to add additional space and enhance tenant mix to

drive footfall

AUK Retail – Priory Retail Park income opportunities

+17 floors Neighbouring Brown and Root

Tower refurbishment

Significant potential residential development on the Carphone

Warehouse site

Offer received from discount food

retailer will improve tenant mix and

ultimately drive higher footfall

Footfall

Offers received on potential reconfigured

6,000 sqft leisure unit with passing rent of £23 per sqft

Commercialisation

£35-£37.5Per sqft offers

Several initiatives and negotiations underway,

including creating advertising space and

Amazon lockers

Expansion opportunities

Redefine International P.L.C. Investor & Analyst Presentation

June 2016

5.8%

40

121,689

8.2 years

97.9%

19

Distribution sector currently experiencing strong demand and rental growth potential

Consumer shopping patterns with more focus on convenience and online shopping will continue to underpin

strong sector demand

All figures as at 29 February 2016

UK Commercial - Logistics and automotive

Gross annualised rental income

Latest asset management successes include:

• Camino Park, Crawley vacant unit in solicitors’ hands +22% on passing rent. Royal Mail 10 year reversionary lease, with 5 year break, complete

• Express Park, Bridgewater 5 year lease regear in solicitors’ hands at passing and ERV

Occupancy by lettable space:

Demand > Availablespace

WAULT

11.6 years on industrial and automotive sector with long defensive largely indexed income

Distribution asset WAULT +36% in last 6 months

Net initial yield

6.6% Reversionary yieldon distribution assets

Total number of properties:

>50% in Greater London, Big 6 UK cities

and UK South East

Square metres

Distribution asset average gross rent £6.2 per sqft vs

ERV of £6.8 per sqft

£10.5m

Redefine International P.L.C. Investor & Analyst Presentation

June 2016

20

Demand for space exceeding availability

AUK Distribution – Camino Park income opportunities

Royal Mail 10 year reversionary leases concluded with 5 year break option

10 yearsReversionary

lease

Vacant unit in solicitors’ hands at 22% above passing rent

15 yearsNew lease

Recently achieved or targeted at neighbouring estates

£11-£13Per sqft

Achieved on latest agreed lease

<£40Per sqft

As reported at acquisition

Camino Park, CrawleyPositive direction of travel

Online retail

c.15% share of current total retail sales and

gaining share at a rapid

pace

>£10Per sqft

£7.5Per sqft

3.4 years WAULTAs reported 29 February 2016

7.1 years WAULTPost completion of two recent lease activities

Redefine International P.L.C. Investor & analyst presentation

June 2016

Double Tree by Hilton, Edinburgh

Final Thoughts

22

Income focus is in our DNA and defines who we are as a company

Income focused total returns are core to our business

Investment philosophyAcquire secure

income streams, exposed to

strong property fundamentals, with realisable

income and value-add opportunities

Income

Capital structureOptimising debt levels to

capitalise on low interest rate environment and focused on high yielding debt pay down

DevelopmentOptimising existing

space and selective high yielding expansions

DiversifiedIncome security

supported by diversified portfolio

tenant base

Active asset management

Income-led asset management

initiatives informed by occupational market

26Redefine International

P.L.C. Investor & analyst presentation June 2016

Divider page titleDivider page subhead

City Point, Leeds

Appendices

Redefine International P.L.C. Investor & analyst presentation

June 2016Portfolio summary & analysis

Summary (incl. share of joint ventures)

% of portfolio by

market value

Market value 29 February

2016

Properties Area (m2) Annualised gross rental

income

ERV Net initialyield

Reversionaryyield

Weighted average

lease length

Voids (by lettable

area)

%Indexed

Like-for-like retail 22.7% 346.6 6 157,102 27.1 27.4 6.5% 7.0% 8.6 1.1% 20.9%

AUK retail 13.7% 207.8 8 80,519 14.3 13.0 6.0% 5.9% 9.8 0.4% 0.0%

UK Retail 36.4% 554.4 14 237,621 41.4 40.4 6.3% 6.6% 9.0 0.8% 13.7%

Like-for-like commercial 10.4% 157.9 53 79,947 12.7 11.0 7.2% 6.7% 6.8 0.2% 48.0%

AUK commercial 16.9% 257.6 11 136,718 14.3 17.0 4.5% 6.2% 5.3 5.8% —

UK Commercial 27.3% 415.5 64 216,665 27.0 28.0 5.5% 6.4% 6.0 3.8% 22.6%

UK Hotels 15.4% 235.4 9 41,323 15.0 15.0 6.0% 6.0% 10.8 — 5.4%

Total UK 79.1% 1,205.3 87 495,609 83.3 83.4 6.0% 6.4% 8.4 2.0% 15.1%

Europe 20.6% 314.1 87 198,621 20.9 20.8 5.6% 5.6% 6.8 1.8% 97.7%

Total (excl. The Hague) 99.7% 1,519.4 174 694,230 104.2 104.2 5.9% 6.2% 8.1 2.0% 31.7%

The Hague (non-core) 0.3% 5.0 1 12,878 1.9 1.1 33.3% 19.7% 0.3 — 100.0%

Total 100.0% 1,524.4 175 707,108 106.1 105.3 6.0% 6.3% 7.9 1.9% 32.9%

Wholly owned 91.5% 1,395.3 99 598,177 95.9 96.2 5.9% 6.3% 7.8 2.0% 26.7%

Joint ventures (share) 8.5% 129.1 76 108,931 10.2 9.1 6.9% 6.0% 8.6 1.8% 91.2%

Like-for-like portfolio 69.5% 1,059.0 156 489,870 77.6 75.4 6.4% 6.4% 8.1 1.1% 45.0%

AUK portfolio 30.5% 465.4 19 217,238 28.6 29.9 5.0% 6.1% 7.2 3.0% 0.0%

Redefine International P.L.C. Investor & analyst presentation

June 2016

Top 20 assets make up >60% of total portfolio

Top 20 assets

Top 20 assets

% of portfolio by

market value

Market value 29 February

2016

Area (m2) Annualised gross rental

income

Net initialyield

Weighted average

lease length

Voids (by lettable

area)

%Indexed

Grand Arcade, Wigan 6.6% 100.5 43,491 7.9 6.4% 9.5 0.8% 17.0%

Weston Favell, Northampton 5.7% 87.4 28,451 6.5 6.9% 7.8 0.8% 48.7%

St Georges, Harrow 4.8% 73.2 20,202 4.6 5.2% 5.0 0.9% 18.9%

Schloss Centre, Berlin 4.6% 69.6 18,181 4.0 5.0% 5.4 0.9% 98.3%

Bahnhoff Altona, Hamburg 4.0% 60.3 15,074 3.6 5.2% 5.4 0.7% 97.8%

Banbury Cross Retail Park, Banbury 3.3% 50.3 15,845 3.8 7.0% 5.5 — 0.1%

Charing Cross Road, London 3.2% 49.0 3,776 1.8 2.6% 5.7 — —

The Arches Retail Park, Watford 3.1% 48.0 11,443 3.0 6.0% 10.9 — —

Camino Park Distribution Center, Crawley 2.8% 42.0 32,664 2.4 5.3% 3.4 7.8% —

Express Park Distribution Center, Bridgewater 2.7% 41.5 46,961 2.7 6.3% 5.8 — —

Top 10 40.8%

Priory Retail Park, Merton 2.6% 39.0 6,533 2.2 5.2% 9.7 0.0% —

Southwark 2.5% 38.4 3,936 2.4 5.9% 9.8 — —

Birchwood, Warrington 2.3% 35.2 34,583 2.9 7.0% 15.0 2.2% 3.5%

Earl’s Court 2.2% 33.9 2,781 2.2 6.1% 9.8 — —

West Orchards, Coventry 2.0% 30.4 19,656 3.6 8.4% 6.4 0.9% —

Limehouse 2.0% 30.2 5,747 2.1 6.6% 9.8 — —

Edinburgh 1.8% 28.1 7,250 2.0 6.7% 10.0 — 4.4%

Royal Docks 1.7% 26.3 4,561 1.8 6.3% 9.8 — —

Deansgate Office, Manchester 1.7% 26.0 7,775 1.4 3.2% 4.6 24.2% —

Sytner Vehicle Dealership, High Wycombe 1.6% 24.9 6,028 1.4 5.3% 9.1 — —

Top 20 61.3%

Redefine International P.L.C. Investor & analyst presentation

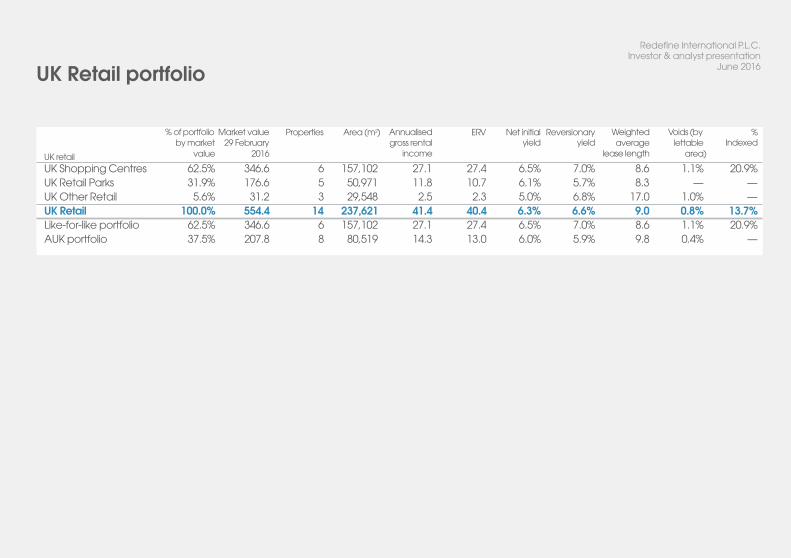

June 2016UK Retail portfolio

UK retail

% of portfolio by market

value

Market value 29 February

2016

Properties Area (m2) Annualised gross rental

income

ERV Net initialyield

Reversionaryyield

Weighted average

lease length

Voids (by lettable

area)

%Indexed

UK Shopping Centres 62.5% 346.6 6 157,102 27.1 27.4 6.5% 7.0% 8.6 1.1% 20.9%

UK Retail Parks 31.9% 176.6 5 50,971 11.8 10.7 6.1% 5.7% 8.3 — —

UK Other Retail 5.6% 31.2 3 29,548 2.5 2.3 5.0% 6.8% 17.0 1.0% —

UK Retail 100.0% 554.4 14 237,621 41.4 40.4 6.3% 6.6% 9.0 0.8% 13.7%

Like-for-like portfolio 62.5% 346.6 6 157,102 27.1 27.4 6.5% 7.0% 8.6 1.1% 20.9%

AUK portfolio 37.5% 207.8 8 80,519 14.3 13.0 6.0% 5.9% 9.8 0.4% —

Redefine International P.L.C. Investor & analyst presentation

June 2016UK Commercial portfolio

UK Commercial (incl. share of joint ventures)

% of portfolio Market value by market 29 February

value 2016

Properties Area (m2) Annualised gross rental

income

ERV Net initial Reversionary yield yield

Weighted average

lease length

Voids (by lettable

area)

%Indexed

UK Offices– GreaterLondon 21.1% 87.7 4 15,706 4.2 4.8 3.9% 5.4% 4.6 — 23.4%

UK Offices – Regions 38.8% 161.1 20 79,269 12.4 13.0 6.0% 7.7% 4.7 7.1% 18.5%

UK Offices 59.9% 248.8 24 94,975 16.5 17.8 5.2% 6.9% 4.7 5.9% 19.7%

UK Distribution 20.1% 83.5 2 79,625 5.2 5.8 5.8% 6.6% 4.7 3.2% —

UK Industrialand Automotive

20.0% 83.2 38 42,065 5.3 4.4 5.9% 4.8% 11.6 — 53.7%

UK Commercial 100.0% 415.5 64 216,665 27.0 28.0 5.5% 6.4% 6.0 3.8% 22.6%

Wholly owned 97.2% 403.7 63 213,912 26.2 27.2 5.4% 6.4% 5.9 3.8% 23.3%

Joint ventures (share) 2.8% 11.8 1 2,753 0.8 0.8 6.7% 6.6% 8.3 — —

Like-for-like portfolio 38.0% 157.9 53 79,946 12.7 11.0 7.2% 6.7% 6.8 0.2% 48.0%

AUK portfolio 62.0% 257.6 11 136,719 14.3 17.0 4.5% 6.2% 5.3 5.8% —

Redefine International P.L.C. Investor & analyst presentation

June 2016UK Hotel portfolio

UK Hotels

% of portfolio by market

value

Market value 29 February

2016

Properties Area (m2) Annualised gross rental

income

ERV Net initialyield

Reversionaryyield

Weighted average

lease length

Voids (by lettable

area)

%Indexed

Greater London &

UK South portfolio

82.2% 193.6 7 29,426 12.3 12.3 6.0% 6.0% 9.8 — —

Edinburgh 12.0% 28.1 1 7,250 2.0 2.0 6.7% 6.7% 10.0 — 4.4%

RBDL Managed Hotels 94.2% 221.7 8 36,676 14.3 14.3 6.1% 6.1% 9.8 — 0.6%

Enfield Travelodge 5.8% 13.7 1 4,647 0.7 0.7 5.0% 5.0% 31.3 — 100.0%

UK Hotels 100.0% 235.4 9 41,323 15.0 15.0 6.0% 6.0% 10.8 — 5.4%

Redefine International P.L.C. Investor & analyst presentation

June 2016European portfolio

Europe (incl. share of joint ventures)

% of portfolio Market value by market 29 February

value 2016

Properties Area (m2) Annualised gross rental

income

ERV Net initial Reversionary yield yield

Weighted average

lease length

Voids (by lettable

area)

%Indexed

German Shopping Centres 46.2% 145.0 3 44,537 7.9 8.8 4.5% 5.2% 5.4 0.8% 98.1%

GermanSupermarkets andRetail Parks

42.4% 133.3 80 131,963 9.9 10.0 6.2% 6.3% 7.9 2.1% 96.9%

German Retail 88.6% 278.3 83 176,500 17.8 18.8 5.3% 5.7% 6.7 1.7% 97.4%

German Offices 11.4% 35.8 4 22,121 3.1 2.0 8.0% 5.0% 7.4 1.9% 99.4%

Europe (excl. non-core) 100.0% 314.1 87 198,621 20.9 20.8 5.6% 5.6% 6.8 1.8% 97.7%

Wholly owned 62.6% 196.9 12 92,442 11.6 12.5 4.8% 5.4% 5.4 1.8% 96.4%

Joint ventures (share) 37.4% 117.2 75 106,179 9.3 8.3 6.9% 6.0% 8.7 1.9% 99.3%

Redefine International P.L.C. Investor & analyst presentation

June 2016Redefine International Team

30

Mike WattersCEOt: +44 (0) 20 7811 0102e: [email protected]

Stephen Oakenfull

Deputy CEO

t: +44 (0) 20 7811 0104

Donald Grant

CFO

t: +44 (0) 20 7811 0106

Adrian Horsburgh

Property Director

t: +44 (0) 20 7808 3992

Janine Ackermann

Head of Investor Relations

t: +44 (0) 20 7808 3998

Redefine International P.L.C.

2nd Floor, 30 Charles II Street

London SW1Y 4AE

Visit us online

www.redefineinternational.com

@RedefinePLC

Redefine International

Related Documents