Macroeconomic Outlook for 2015 Samir Rath (CAIA) MBA (Brown[USA] & IE[Spain]) +1 312 985 7570 +65 9750 6842 [email protected] Financial Consultant Global Financial Consultants

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Macroeconomic Outlook for 2015

Samir Rath (CAIA)!MBA (Brown[USA] & IE[Spain]) !+1 312 985 7570 +65 9750 6842 [email protected] !Financial Consultant Global Financial Consultants

What has come before in 2014

US equities have been the source of best risk-adjusted returns for the past three years

Risk Adjusted Returns: 2011 - 2014

-0.18

0.00

0.18

0.35

0.53

0.70

iSha

res

Cor

e S&

P 50

0 ET

F

iSha

res

U.S

. Pre

ferre

d St

ock

ETF

iSha

res

MSC

I Den

mar

k C

appe

d ET

F

iSha

res

MSC

I Ire

land

Cap

ped

ETF

iSha

res

MSC

I Bel

gium

Cap

ped

ETF

iSha

res

MSC

I Sw

itzer

land

Cap

ped

ETF

iSha

res

MSC

I New

Zea

land

Cap

ped

ETF

iSha

res

MSC

I Phi

lippi

nes

ETF

iSha

res

Glo

bal H

igh

Yiel

d C

orpo

rate

Bon

d ET

F

iSha

res

Cor

e U

.S. A

ggre

gate

Bon

d ET

F

iSha

res

MSC

I Hon

g Ko

ng E

TF

iSha

res

MSC

I Net

herla

nds

ETF

iSha

res

MSC

I Ger

man

y ET

F

iSha

res

MSC

I Tai

wan

ETF

iSha

res

MSC

I Fin

land

Cap

ped

ETF

iSha

res

MSC

I Jap

an E

TF

iSha

res

Japa

n La

rge-

Cap

ETF

iSha

res

MSC

I Uni

ted

King

dom

ETF

iSha

res

MSC

I Sin

gapo

re E

TF

iSha

res

MSC

I Sw

eden

ETF

iSha

res

MSC

I Chi

na E

TF

iSha

res

MSC

I Fra

nce

ETF

iSha

res

MSC

I Ind

ia E

TF

iSha

res

MSC

I Isr

ael C

appe

d ET

F

iSha

res

MSC

I Tha

iland

Cap

ped

ETF

iSha

res

MSC

I Tur

key

ETF

iSha

res

Emer

ging

Mar

kets

Hig

h Yi

eld

Bond

ETF

iSha

res

MSC

I Spa

in C

appe

d ET

F

iSha

res

MSC

I Can

ada

ETF

iSha

res

7-10

Yea

r Tre

asur

y Bo

nd E

TF

iSha

res

MSC

I Aus

tralia

ETF

iSha

res

MSC

I Pol

and

Cap

ped

ETF

iSha

res

MSC

I Ita

ly C

appe

d ET

F

iSha

res

MSC

I Sou

th A

frica

ETF

iSha

res

MSC

I Aus

tria

Cap

ped

ETF

iSha

res

MSC

I Mex

ico

Cap

ped

ETF

iSha

res

MSC

I Mal

aysi

a ET

F

iSha

res

MSC

I Sou

th K

orea

Cap

ped

ETF

iSha

res

MSC

I Nor

way

Cap

ped

ETF

iSha

res

Emer

ging

Mar

kets

Div

iden

d ET

F

iSha

res

MSC

I Ind

ones

ia E

TF

iSha

res

MSC

I All

Peru

Cap

ped

ETF

iSha

res

MSC

I Bra

zil C

appe

d ET

F

iSha

res

MSC

I Rus

sia

Cap

ped

ETF

iSha

res

MSC

I Chi

le C

appe

d ET

F

Most Assets currently at their Historical High Valuations

Data from 1969 for developed equities to Emerging Debt from 2004

US Dollar Appreciation Cycle has just started

US Dollar Appreciation cycles normally last six to seven years !This means a de-facto tightening of global financial conditions given that about 80% of international trade finance is settled in U.S. dollars. !Emerging markets typically bear the brunt of a stronger dollar as their funding sources dry up.

Greater Growth & Policy Divergence in the years ahead

US: On a strong growth path and will start tightening financial conditions UK: The UK having made some strong reforms has growth back on track and is looking to normalise monetary conditions Japan: Despite the loosest financial conditions, Japan is loosening further to spark growth China and India: To soften their slowing structural growth cycles, they are both loosening financial conditions. Reserve Bank of India tends to be very wary of inflation and despite having the tightest financial conditions it is being quite cautious. Eurozone: Finally, ECB has started appreciating the impact of Quantitative Easing and has jumped into the bandwagon with a Eur 1.2 trillion intervention in 2015. Brazil: Despite a big step towards easing financial conditions, we do not expect growth to pick up

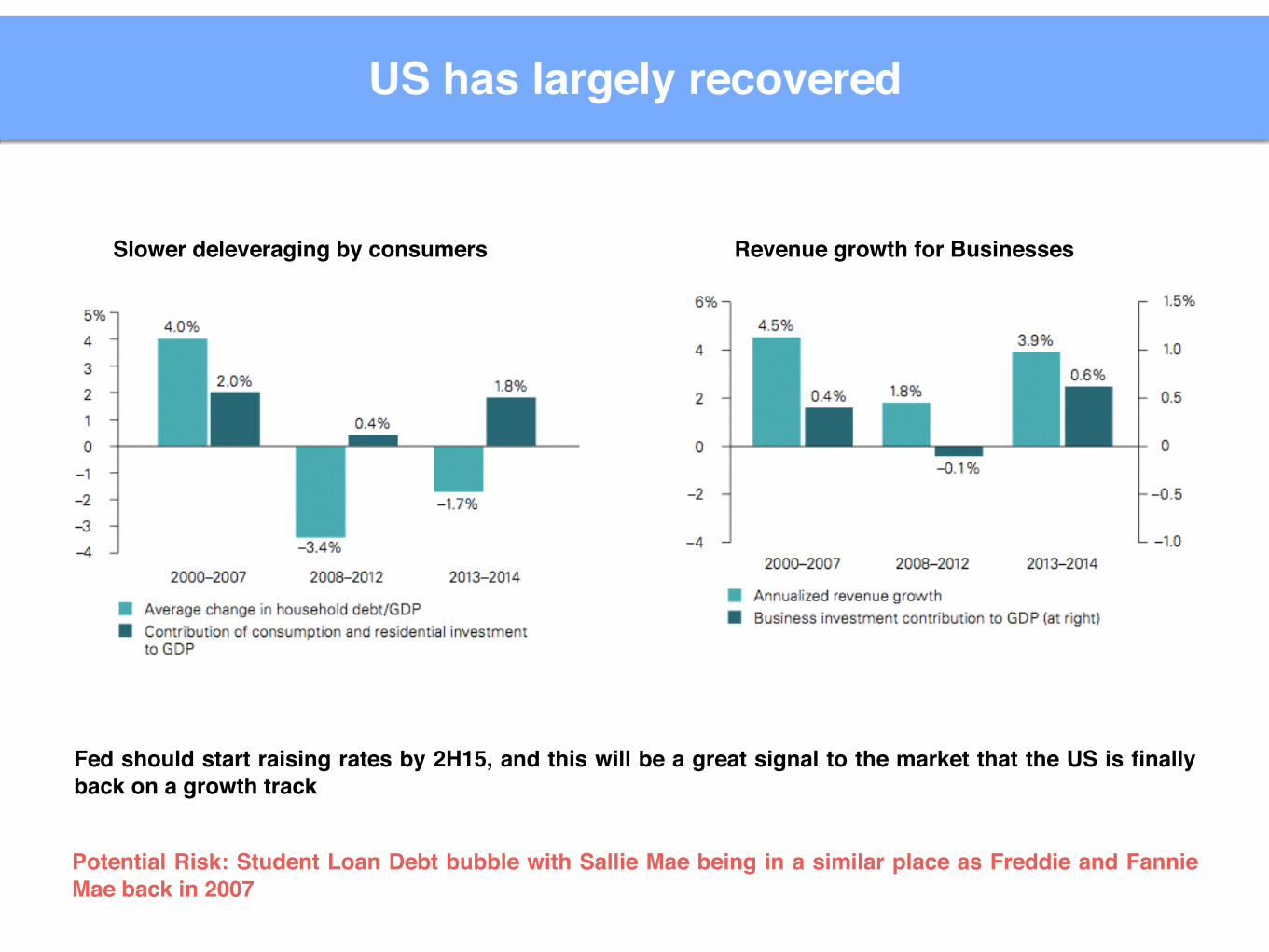

US has largely recovered

Slower deleveraging by consumers Revenue growth for Businesses

Fed should start raising rates by 2H15, and this will be a great signal to the market that the US is finally back on a growth track

Potential Risk: Student Loan Debt bubble with Sallie Mae being in a similar place as Freddie and Fannie Mae back in 2007

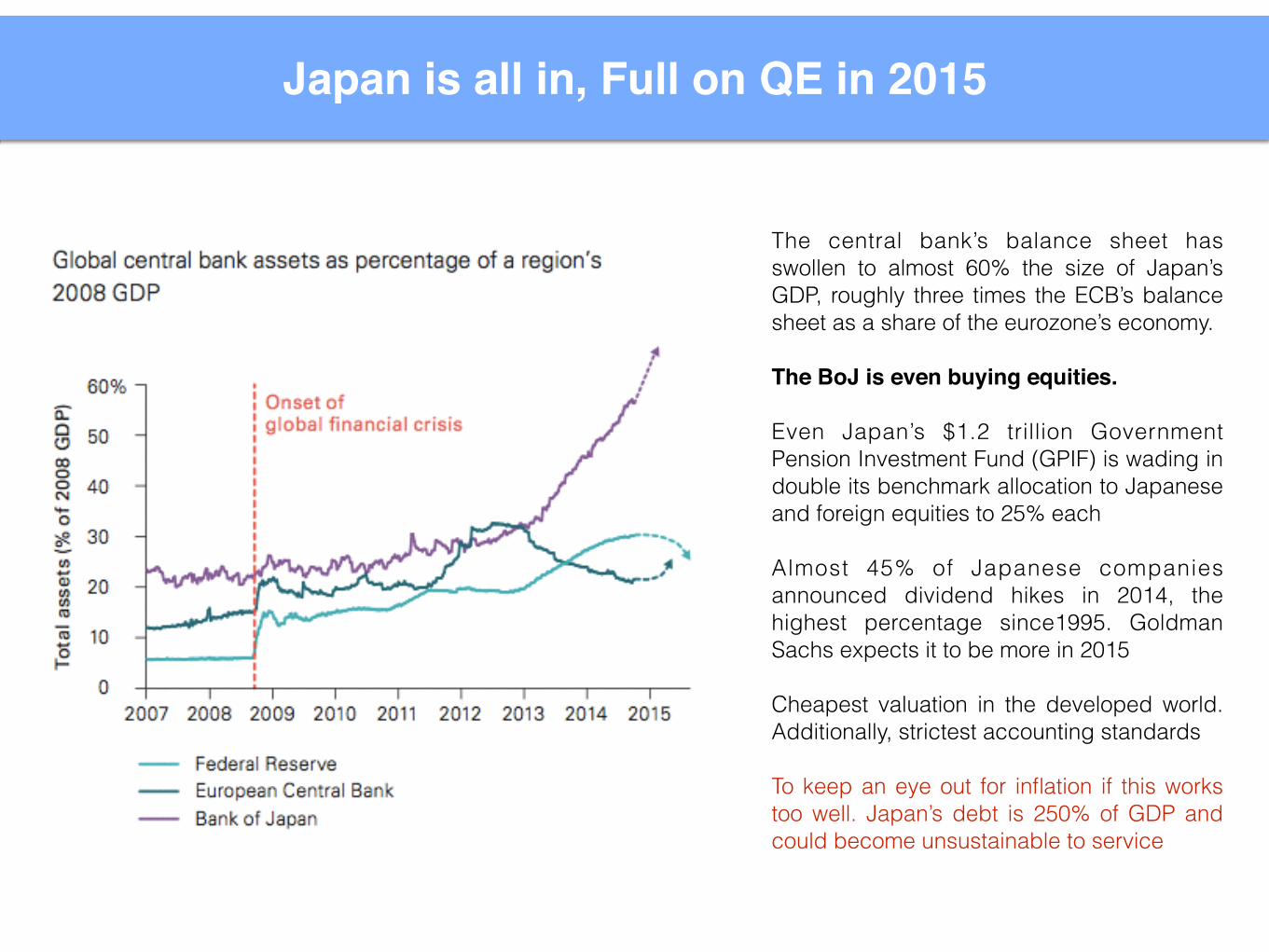

Japan is all in, Full on QE in 2015

The central bank’s balance sheet has swollen to almost 60% the size of Japan’s GDP, roughly three times the ECB’s balance sheet as a share of the eurozone’s economy. !The BoJ is even buying equities. !Even Japan’s $1.2 trillion Government Pension Investment Fund (GPIF) is wading in double its benchmark allocation to Japanese and foreign equities to 25% each !Almost 45% of Japanese companies announced dividend hikes in 2014, the highest percentage since1995. Goldman Sachs expects it to be more in 2015 !Cheapest valuation in the developed world. Additionally, strictest accounting standards !To keep an eye out for inflation if this works too well. Japan’s debt is 250% of GDP and could become unsustainable to service

Europe muddles through & avoids hard questions

QEs knock on wealth effect in Europe will be much lower than in the US given that Europeans have much lower ownership rates of equity and homes. !• For example, only 22% of Germans own equities compared to 47% in the USA!!Imbalances growing with Germany having 2% of Eurozone surplus and 7% of its own GDP. So has a hopelessly underpriced currency.

China’s growth seems to be stabilizing in a new range

China is likely to grow at a 6%–7% pace over the next two to three years. Its maturing as an economy!!- tepid recovery in the global economy, - significant appreciation of the renminbi in REER3 terms - the government’s anticorruption and austerity campaign - regulators’ stricter control on credit growth and curbs on speculative housing demand

India has been re-rated upwards post elections

There is a tendency of markets to be over optimistic right after elections in India, but structurally the current government should be more supportive of growth in the medium term

Commodity super cycle over, depressed prices to continue

Bloomberg Commodity Index has touched 2009 lows!!WTI Crude is at US$ 47.09 !(Shale Oil producers could go virtually bankrupt, Saudi can continue to produce with no issues) !Copper prices just broke below $6000/mt for the first time in 5 years.!!Iron ore, Steel, Aluminum have also hit all time cycle lows.

Bloomberg Commodity Index

Impact of further Oil Price Drop

Countries with exposed trade balances and subsidies will benefit - India - Indonesia - Thailand !Oil will support consumer spending in - USA - UK - Europe !Exporters will be hurt - Nigeria - Russia - Norway

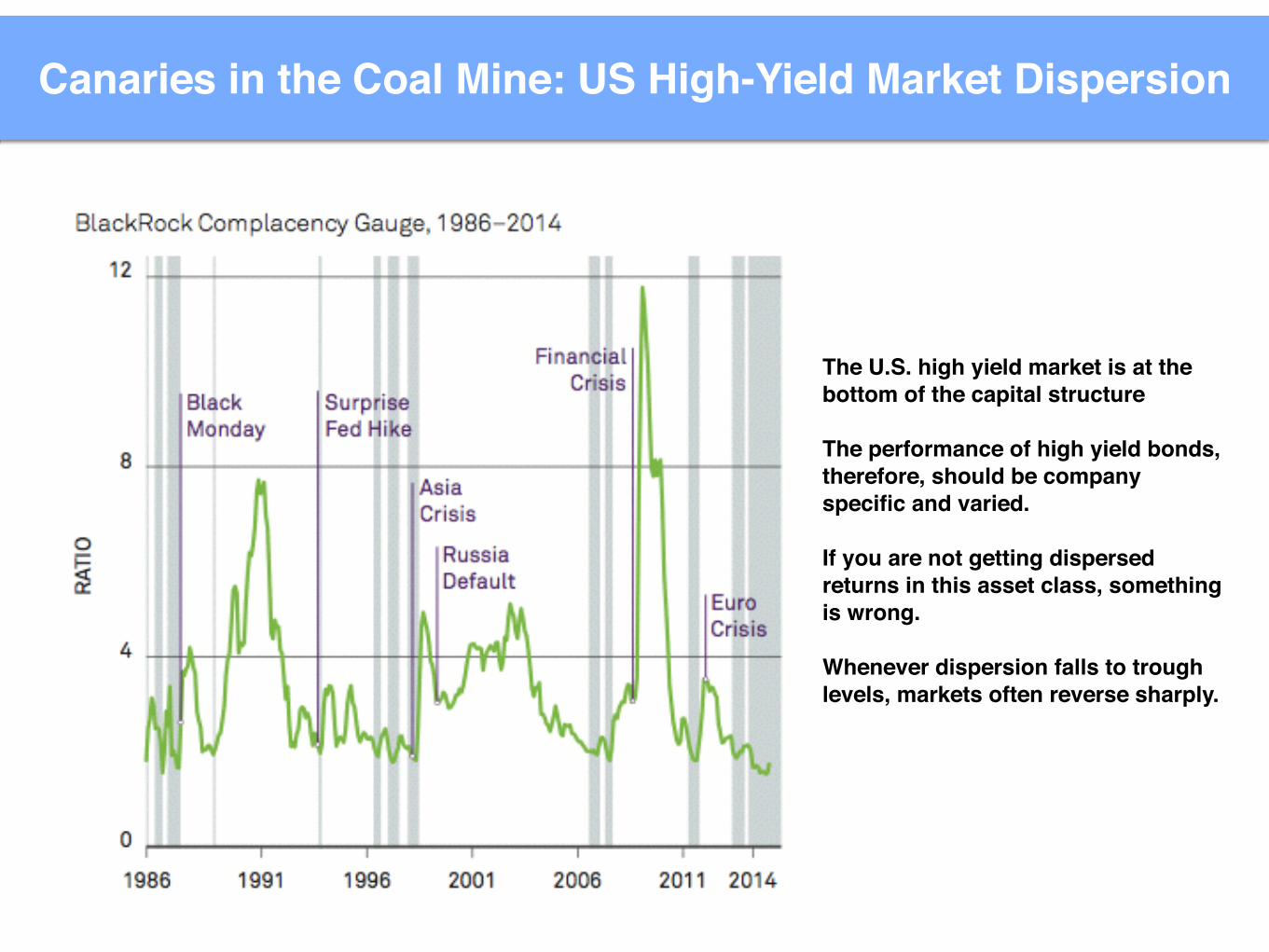

Canaries in the Coal Mine: US High-Yield Market Dispersion

The U.S. high yield market is at the bottom of the capital structure !!The performance of high yield bonds, therefore, should be company specific and varied. !!If you are not getting dispersed returns in this asset class, something is wrong.!!Whenever dispersion falls to trough levels, markets often reverse sharply.

Canaries in the Coal Mine: Lumber is Flashing Red

Lumber is the most economically correlated commodity, even more than WTI Crude and Copper!!Less manipulation and less financialization than crude oil

Political Events to Keep an Eye On

The left-wing party Syriza just won the elections and PM Alexis Tsipras is about to lock horns with the EU on debt repayment and ending austerity

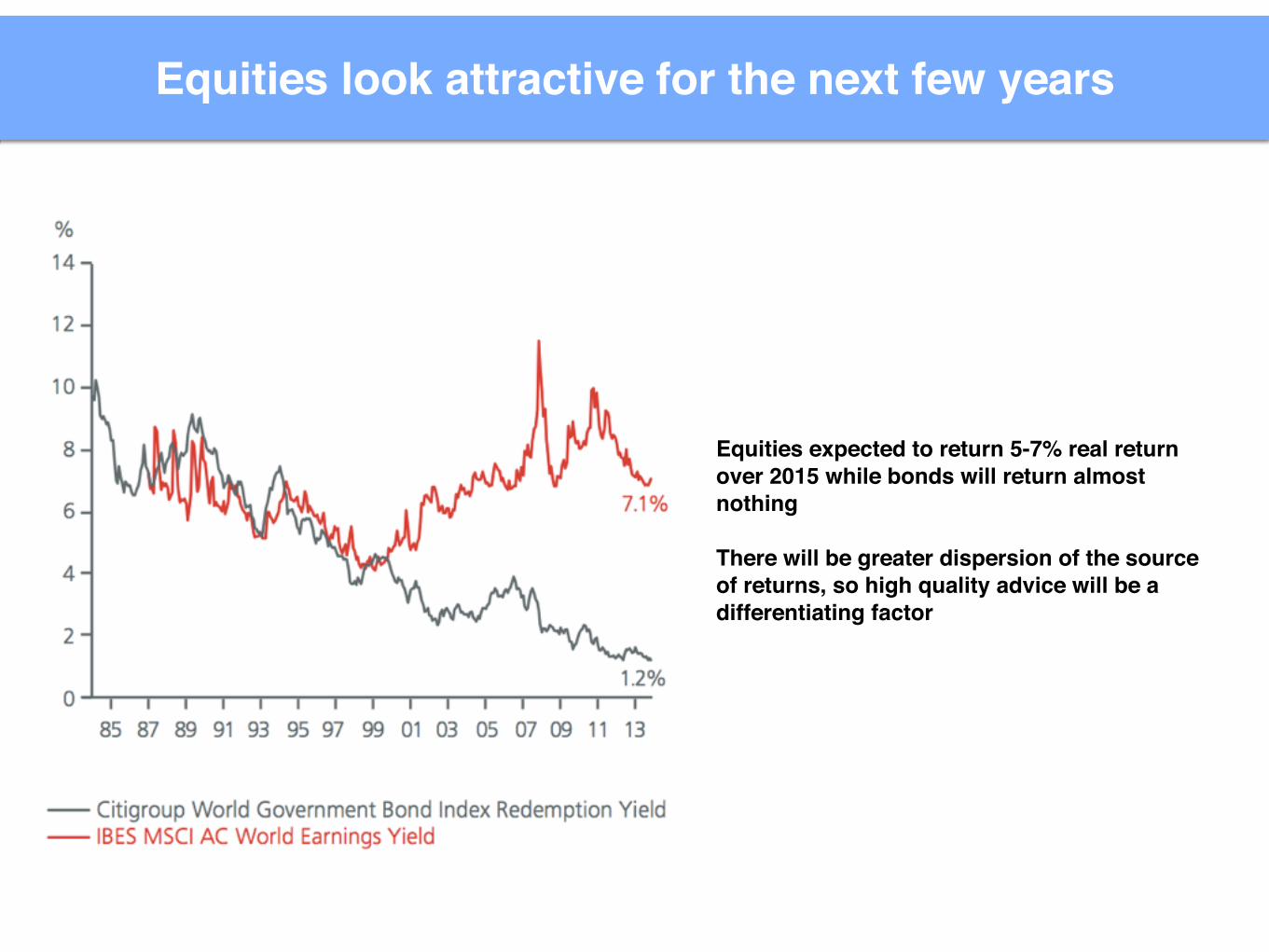

Equities look attractive for the next few years

Equities expected to return 5-7% real return over 2015 while bonds will return almost nothing !There will be greater dispersion of the source of returns, so high quality advice will be a differentiating factor

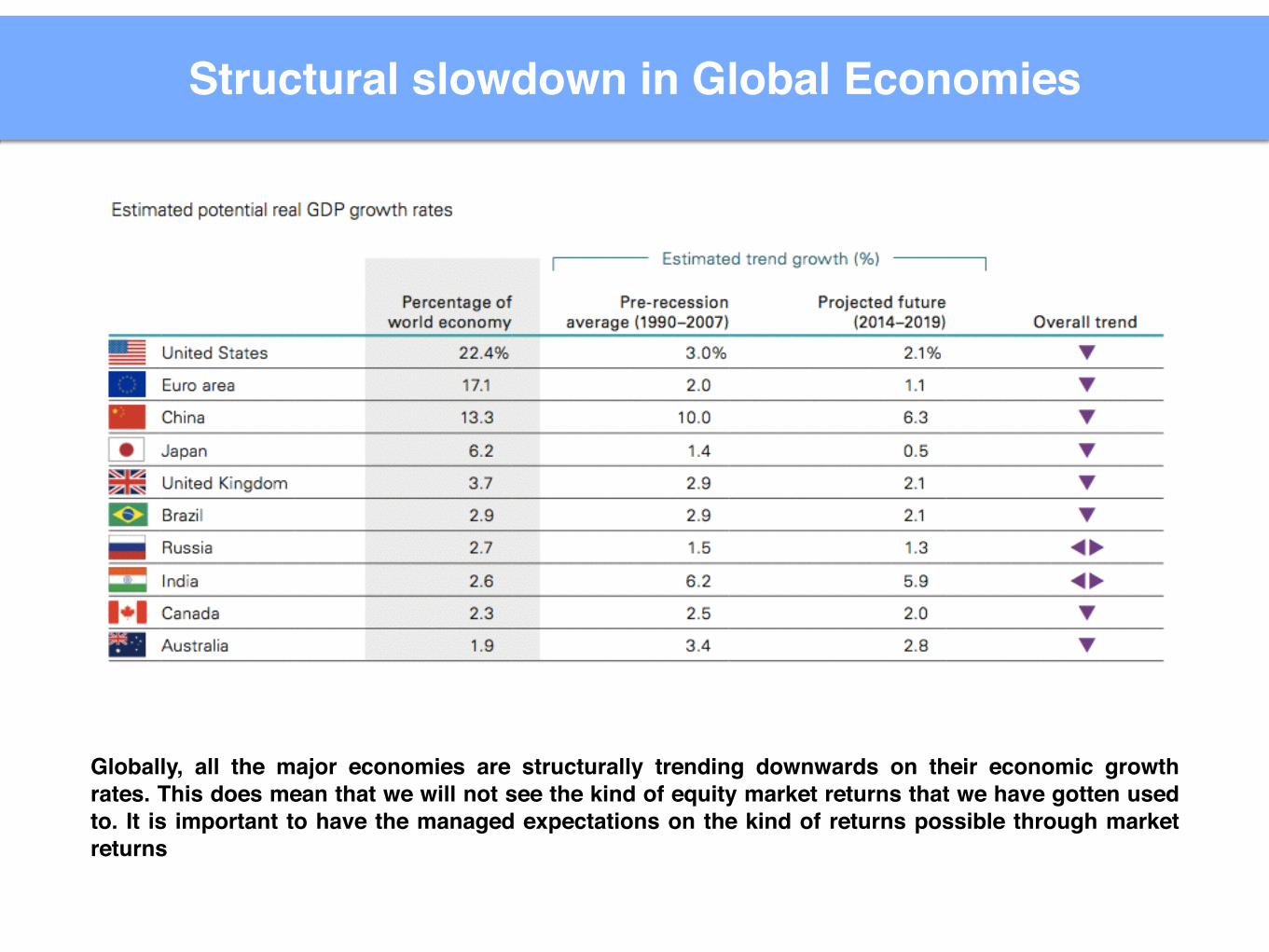

Structural slowdown in Global Economies

Globally, all the major economies are structurally trending downwards on their economic growth rates. This does mean that we will not see the kind of equity market returns that we have gotten used to. It is important to have the managed expectations on the kind of returns possible through market returns

Related Documents