Investing in Russian Power Sector Adam Smith International Conference 24 November 2010 Adam Smith International Conference. RUSSIAN POWER: FINANCE AND INVESTMENT 1 22.11.2010 Moscow, Russia

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Investing in Russian Power SectorAdam Smith International Conference

24 November 2010

Adam Smith International Conference.

RUSSIAN POWER: FINANCE AND INVESTMENT

122.11.2010

Moscow, Russia

Introduction

Content

Introduction• Investment Opportunity: Russian Electricity DistributionDistribution

• Investment Opportunity: Russian Electricity G tiGeneration

• Appendix

222.11.2010

I t t Th R iInvestment Theme: Russian Electricity DistributionElectricity Distribution

322.11.2010

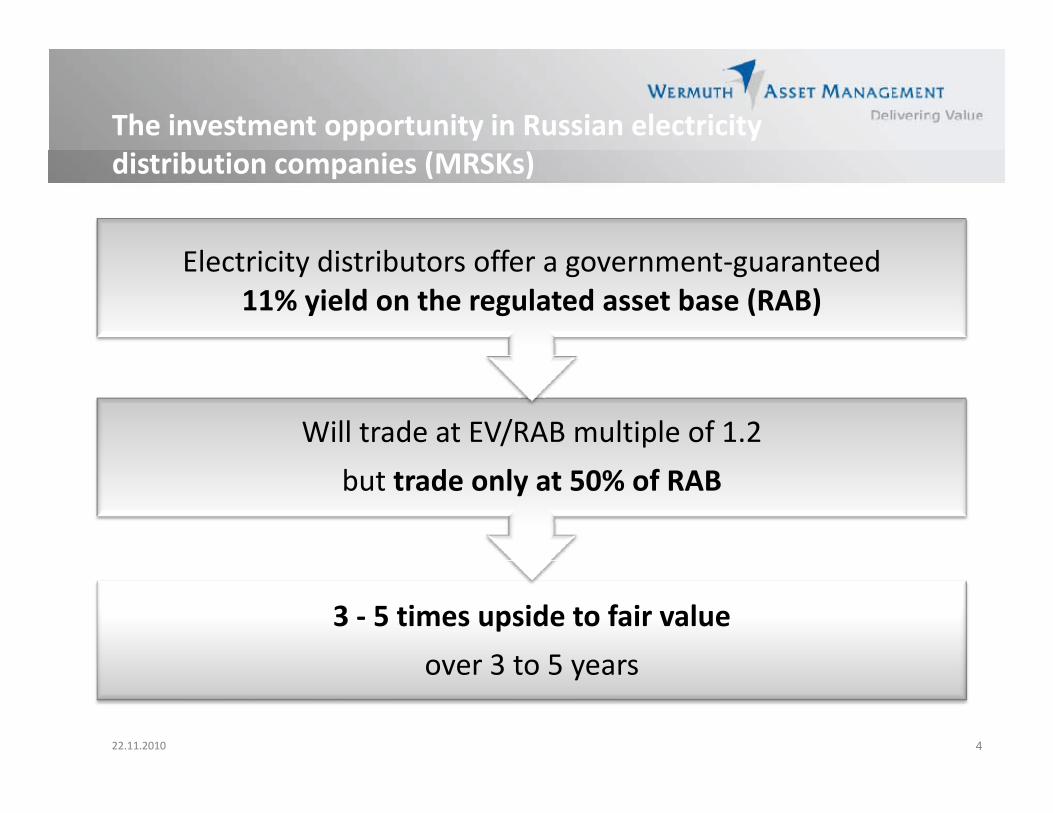

The investment opportunity in Russian electricity

El t i it di t ib t ff t t d

distribution companies (MRSKs)

Electricity distributors offer a government‐guaranteed 11% yield on the regulated asset base (RAB)

Will trade at EV/RAB multiple of 1.2but trade only at 50% of RAB

3 ‐ 5 times upside to fair valueover 3 to 5 years

422.11.2010

over 3 to 5 years

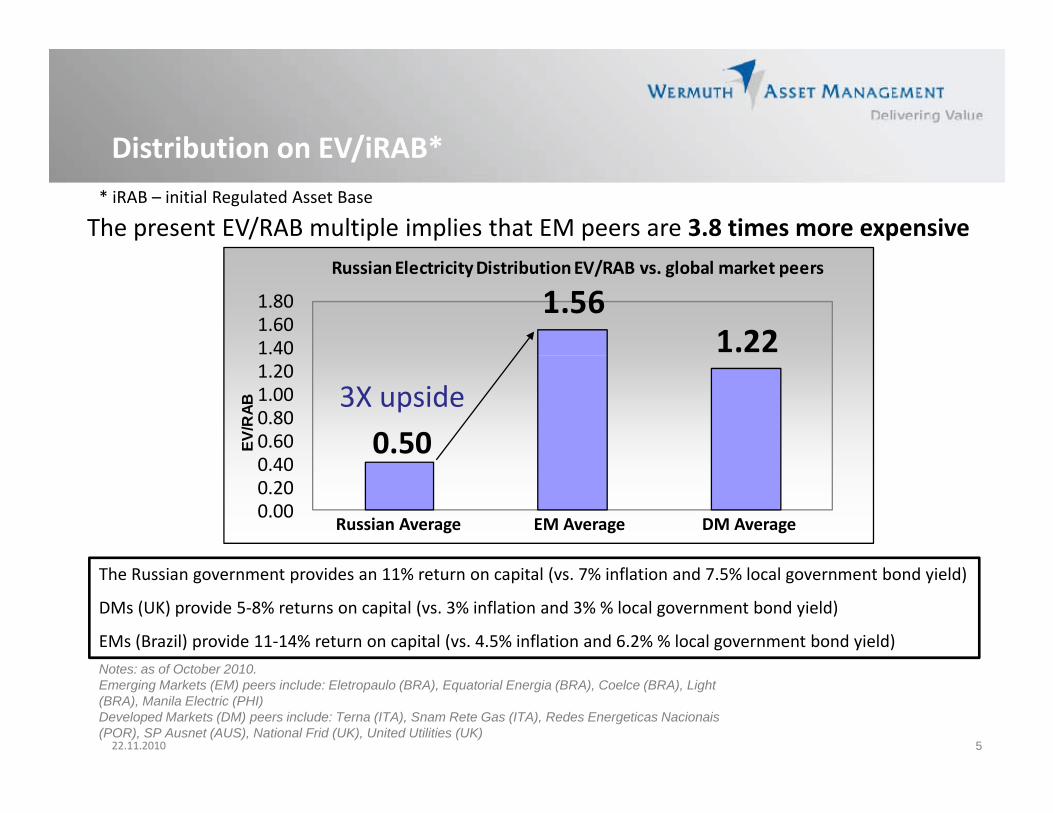

Distribution on EV/iRAB*Distribution on EV/iRAB* iRAB – initial Regulated Asset Base

The present EV/RAB multiple implies that EM peers are 3.8 times more expensive

1.561.221.40

1.601.80

Russian Electricity Distribution EV/RAB vs. global market peers

0 400.600.801.001.20

EV/R

AB 3X upside0.50

0.000.200.40

Russian Average EM Average DM Average

Source: Troika DialogThe Russian government provides an 11% return on capital (vs. 7% inflation and 7.5% local government bond yield)

DMs (UK) provide 5‐8% returns on capital (vs. 3% inflation and 3% % local government bond yield)

EMs (Brazil) provide 11‐14% return on capital (vs. 4.5% inflation and 6.2% % local government bond yield)

522.11.2010

Notes: as of October 2010. Emerging Markets (EM) peers include: Eletropaulo (BRA), Equatorial Energia (BRA), Coelce (BRA), Light (BRA), Manila Electric (PHI)Developed Markets (DM) peers include: Terna (ITA), Snam Rete Gas (ITA), Redes Energeticas Nacionais (POR), SP Ausnet (AUS), National Frid (UK), United Utilities (UK)

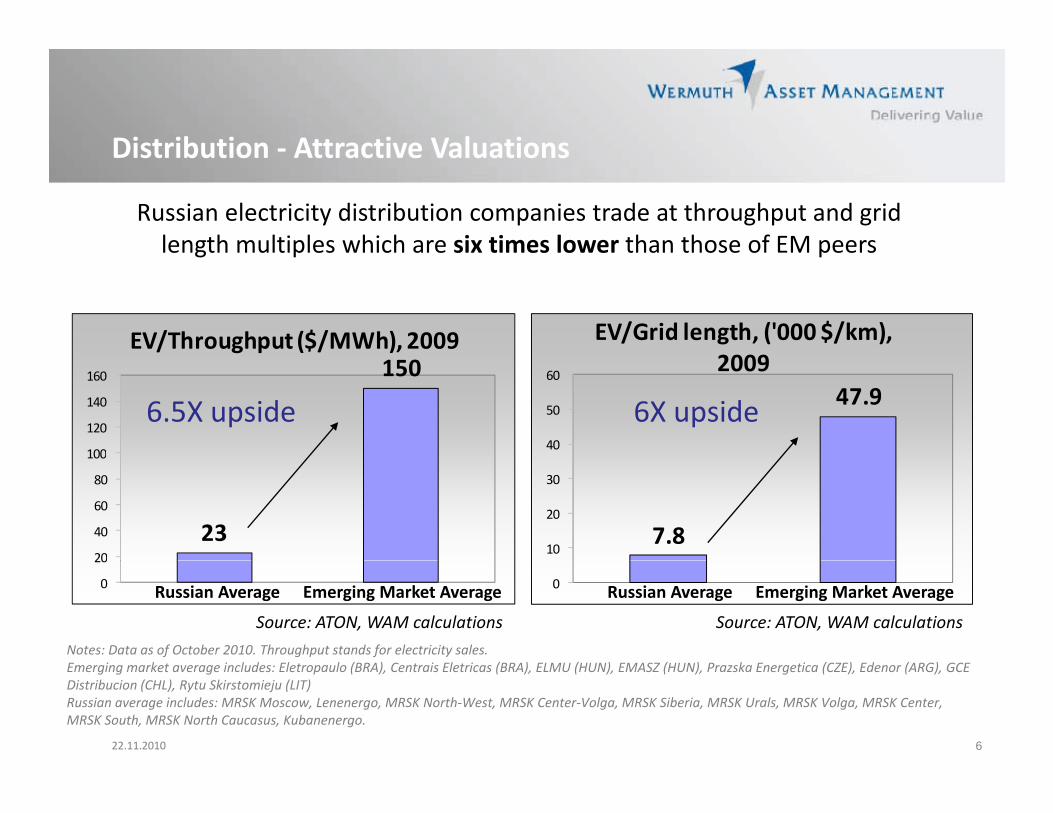

Distribution ‐ Attractive Valuations

Russian electricity distribution companies trade at throughput and grid length multiples which are six times lower than those of EM peers

Distribution ‐ Attractive Valuations

g p p

EV/Throughput ($/MWh), 2009 EV/Grid length, ('000 $/km), 2009150

100

120

140

160

47.9

40

50

60 2009

6.5X upside 6X upside

2320

40

60

80

100

7.810

20

30

Notes: Data as of October 2010. Throughput stands for electricity sales. E i k i l d El l (BRA) C i El i (BRA) ELMU (HUN) EMASZ (HUN) P k E i (CZE) Ed (ARG) GCE

0

20

Russian Average Emerging Market Average 0

Source: ATON, WAM calculations Source: ATON, WAM calculations

Emerging Market AverageRussian Average

622.11.2010

Emerging market average includes: Eletropaulo (BRA), Centrais Eletricas (BRA), ELMU (HUN), EMASZ (HUN), Prazska Energetica (CZE), Edenor (ARG), GCE Distribucion (CHL), Rytu Skirstomieju (LIT) Russian average includes: MRSK Moscow, Lenenergo, MRSK North‐West, MRSK Center‐Volga, MRSK Siberia, MRSK Urals, MRSK Volga, MRSK Center, MRSK South, MRSK North Caucasus, Kubanenergo.

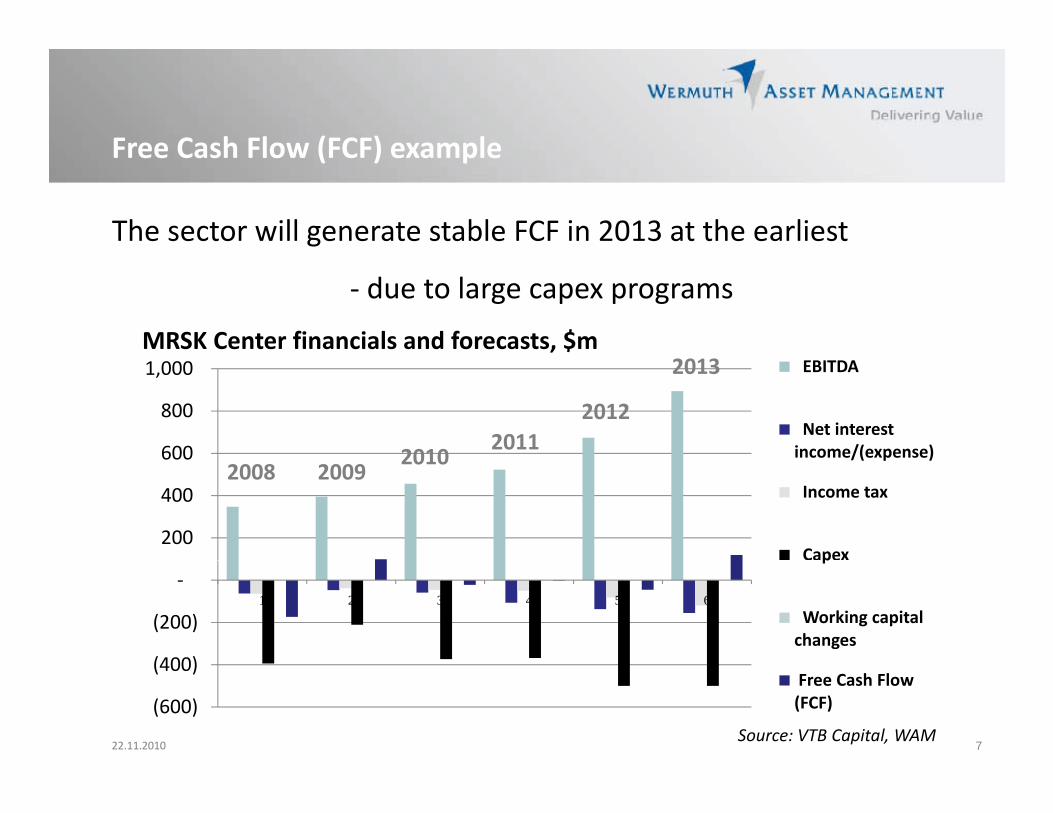

Free Cash Flow (FCF) exampleFree Cash Flow (FCF) example

The sector will generate stable FCF in 2013 at the earliest

MRSK Center financials and forecasts, $m

‐ due to large capex programs

600

800

1,000 EBITDA

Net interest income/(expense) 2010 2011

2012

2013

200

400

600 /( p )

Income tax

Capex

20082010

2009

(400)

(200)

‐1 2 3 4 5 6

p

Working capital changes

722.11.2010

(600)

(400)Free Cash Flow (FCF)

Source: VTB Capital, WAM

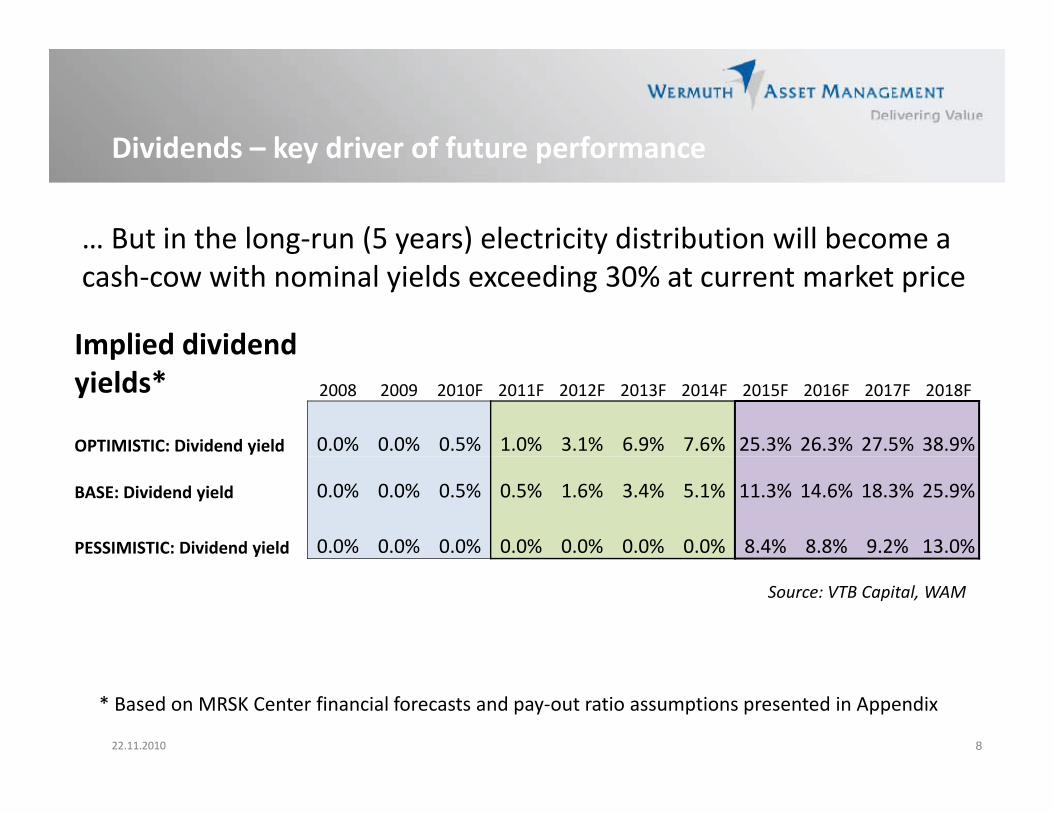

Dividends – key driver of future performanceDividends – key driver of future performance

… But in the long‐run (5 years) electricity distribution will become a g ( y ) ycash‐cow with nominal yields exceeding 30% at current market price

Implied dividend pyields* 2008 2009 2010F 2011F 2012F 2013F 2014F 2015F 2016F 2017F 2018F

OPTIMISTIC: Dividend yield 0.0% 0.0% 0.5% 1.0% 3.1% 6.9% 7.6% 25.3% 26.3% 27.5% 38.9%

BASE: Dividend yield 0.0% 0.0% 0.5% 0.5% 1.6% 3.4% 5.1% 11.3% 14.6% 18.3% 25.9%

PESSIMISTIC: Dividend yield 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 8.4% 8.8% 9.2% 13.0%

Source: VTB Capital, WAM

822.11.2010

* Based on MRSK Center financial forecasts and pay‐out ratio assumptions presented in Appendix

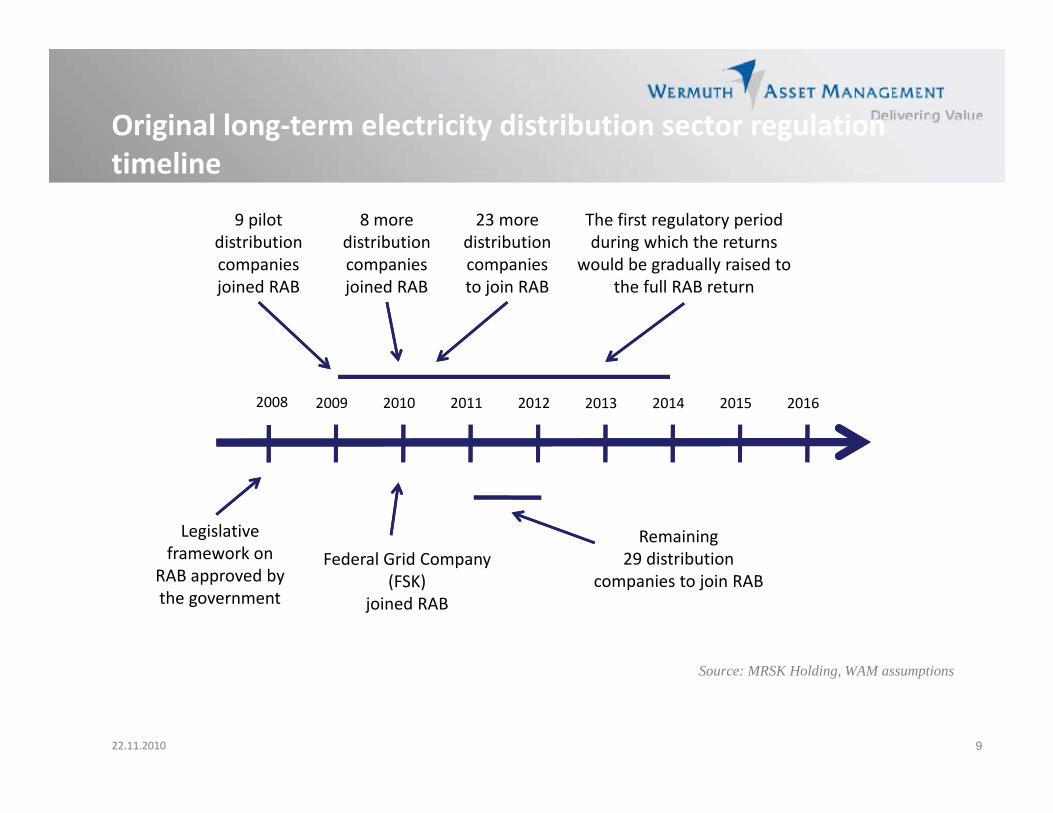

Original long‐term electricity distribution sector regulation

9 pilot distribution

The first regulatory period during which the returns

timeline

8 more distribution

23 more distribution

companies joined RAB

would be gradually raised to the full RAB return

companies joined RAB

companies to join RAB

2008 20132009 2010 2011 2012 2014 2015 2016

Legislative framework on Federal Grid Company

Remaining29 distribution

RAB approved by the government

Federal Grid Company (FSK)

joined RAB

29 distribution companies to join RAB

922.11.2010

Source: MRSK Holding, WAM assumptions

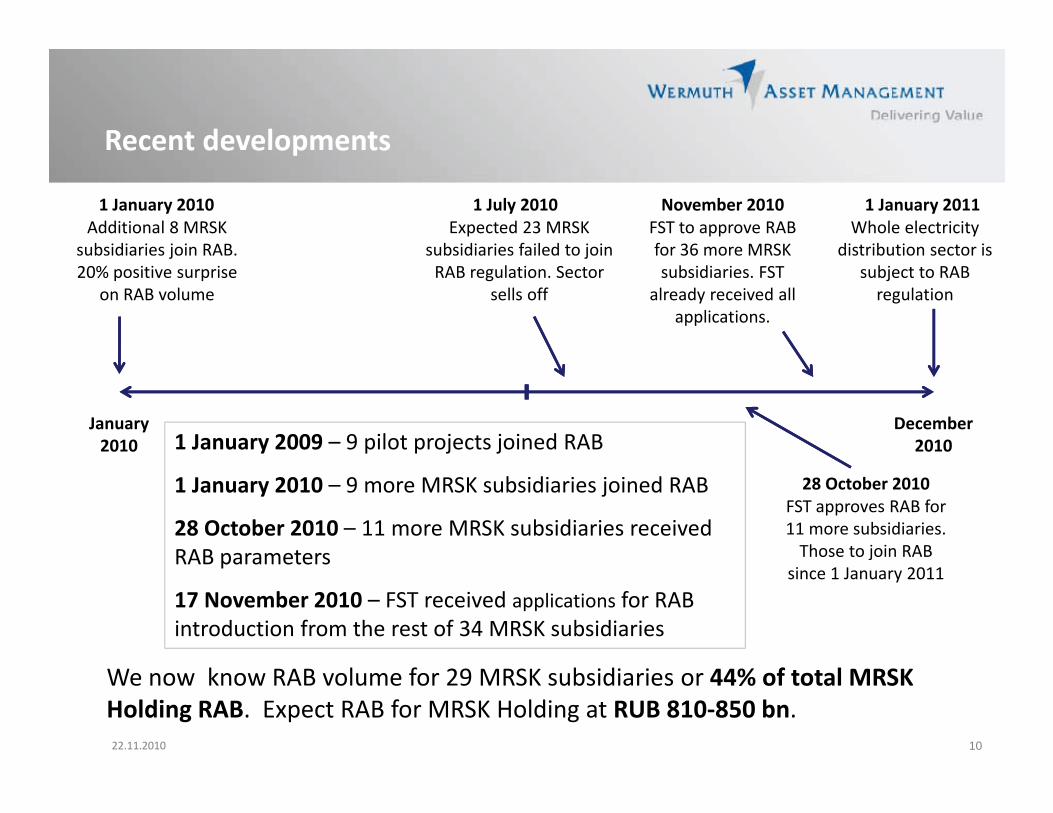

Recent developmentsece t de e op e ts

Expected 23 MRSK subsidiaries failed to join

1 July 2010Whole electricity

distribution sector is

1 January 2011Additional 8 MRSK

subsidiaries join RAB

1 January 2010FST to approve RAB for 36 more MRSK

November 2010

subsidiaries failed to join RAB regulation. Sector

sells off

distribution sector is subject to RAB regulation

subsidiaries join RAB. 20% positive surprise

on RAB volume

for 36 more MRSK subsidiaries. FST

already received all applications.

January 2010

December 20101 January 2009 – 9 pilot projects joined RAB

FST approves RAB for 11 more subsidiaries. Those to join RAB

28 October 20101 January 2010 – 9 more MRSK subsidiaries joined RAB

28 October 2010 – 11 more MRSK subsidiaries received RAB parameters

since 1 January 2011RAB parameters

17 November 2010 – FST received applications for RAB introduction from the rest of 34 MRSK subsidiaries

1022.11.2010

We now know RAB volume for 29 MRSK subsidiaries or 44% of total MRSK Holding RAB. Expect RAB for MRSK Holding at RUB 810‐850 bn.

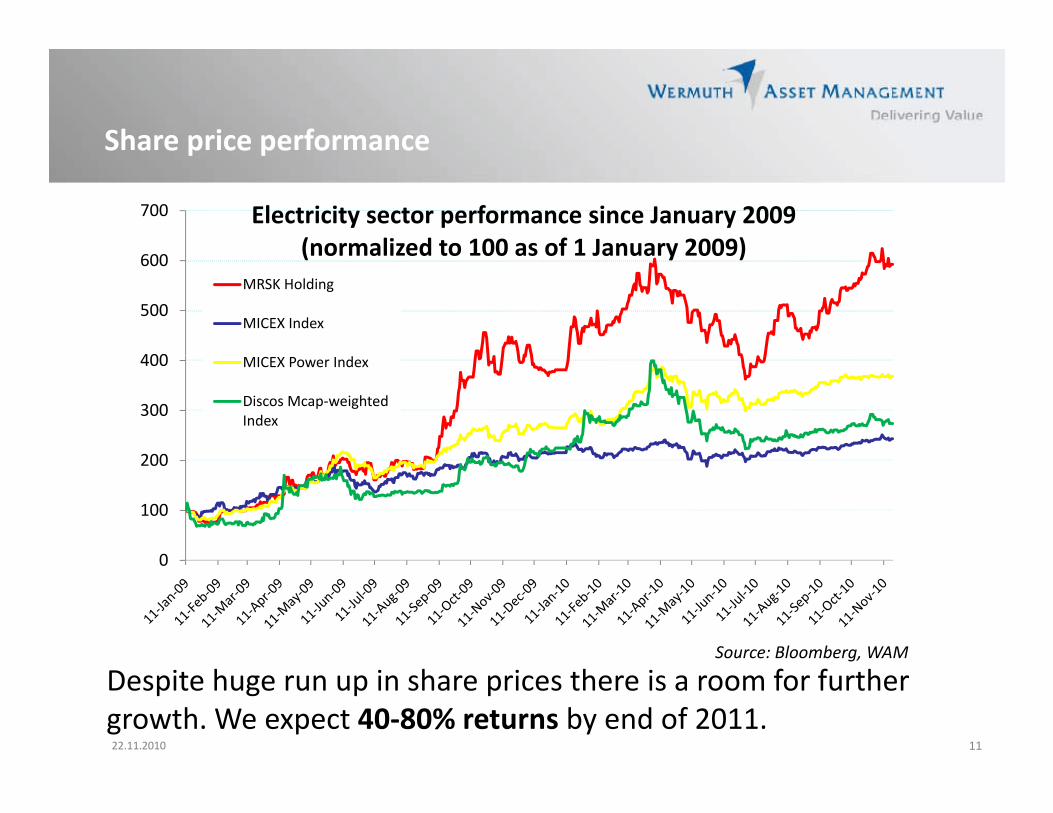

Share price performanceS a e p ce pe o a ce

700 Electricity sector performance since January 2009 (normalized to 100 as of 1 January 2009)

400

500

600 (normalized to 100 as of 1 January 2009)MRSK Holding

MICEX Index

200

300

400 MICEX Power Index

Discos Mcap‐weighted Index

0

100

200

0

Source: Bloomberg, WAM

1122.11.2010

Despite huge run up in share prices there is a room for further growth. We expect 40‐80% returns by end of 2011.

Distribution bottom linest but o botto e

‐ Risk profile of the sector improved much after RAB adoption for 50%f h Wi d f i l i J h 100% fof the sector. Window of opportunity closes in January when 100% of

distribution sector is subject to RAB regulation. MRSKs will followtrading pattern of FSK (which switched to RAB in January 2010 withRAB parameters known back in August 2009),

‐MRSK Holding not necessarily best exposure due to rights issue in 2011‐2013 potential RAB delays/surprises in certain regions 20%2011 2013, potential RAB delays/surprises in certain regions, 20% premium to SOTP.

‐ Next big driver: M&A/consolidation in certain regions. Privatization,

‐ Time to focus on regional MRSKs. We like MRSK Urals, MRSK Volga, MRSK South and Lenenergo.

1222.11.2010

I t t Th R iInvestment Theme: Russian Electricity GenerationElectricity Generation

1322.11.2010

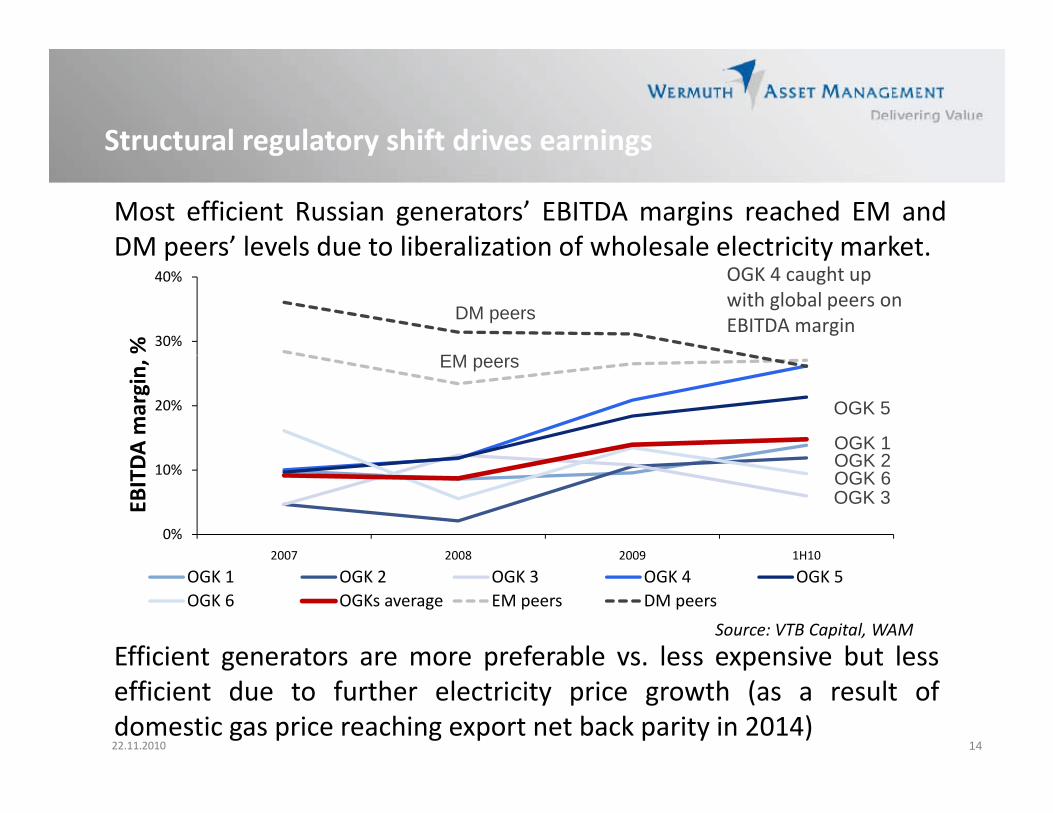

Structural regulatory shift drives earningsSt uctu a egu ato y s t d es ea gs

Most efficient Russian generators’ EBITDA margins reached EM andDM peers’ levels due to liberalization of wholesale electricity market.DM peers levels due to liberalization of wholesale electricity market.

30%

40%

%

EM

DM peers

OGK 4 caught up with global peers on EBITDA margin

20%

DA m

argin, EM peers

OGK 5

OGK 1OGK 2

0%

10%

2007 2008 2009 1H10

EBITD OGK 2

OGK 6OGK 3

Efficient generators are more preferable vs. less expensive but less

OGK 1 OGK 2 OGK 3 OGK 4 OGK 5OGK 6 OGKs average EM peers DM peers

Source: VTB Capital, WAM

1422.11.2010

Efficient generators are more preferable vs. less expensive but lessefficient due to further electricity price growth (as a result ofdomestic gas price reaching export net back parity in 2014)

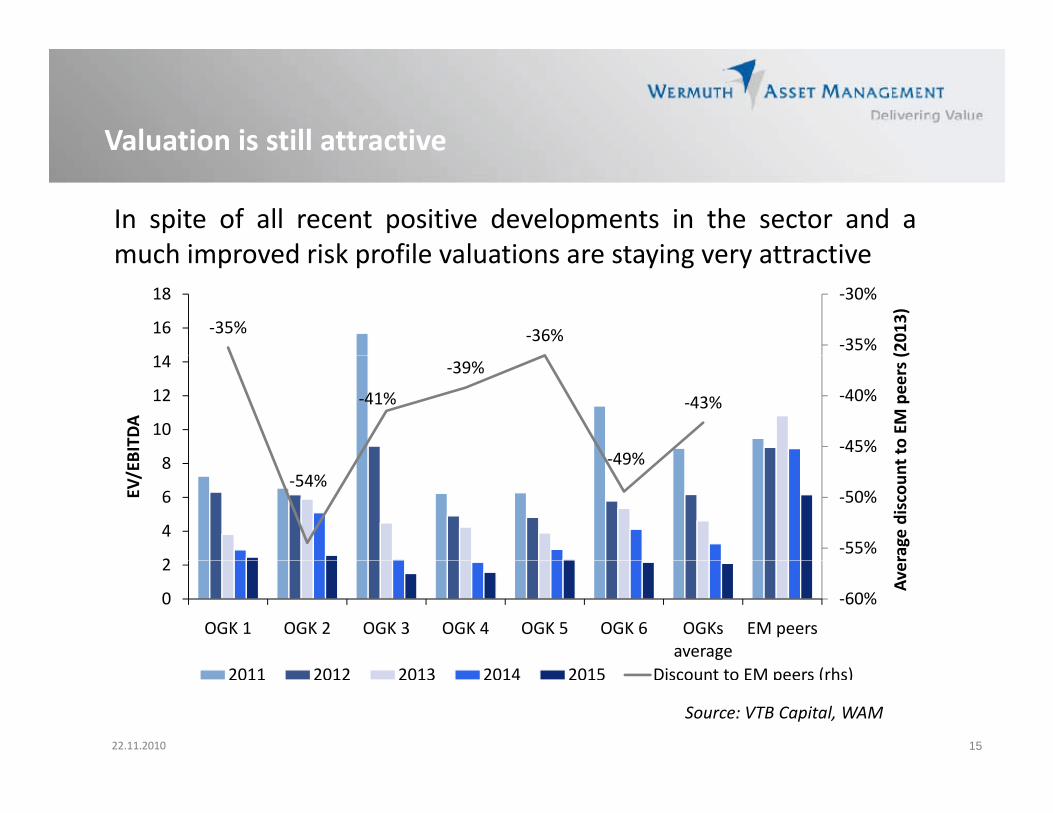

Valuation is still attractivea uat o s st att act e

In spite of all recent positive developments in the sector and amuch improved risk profile valuations are staying very attractivemuch improved risk profile valuations are staying very attractive

‐35% ‐36% ‐35%

‐30%

14

16

18

(2013)

‐41%

‐39%

49%

‐43%

‐45%

‐40%

8

10

12

14

to EM peers (

BITD

A

‐54%‐49%

‐55%

‐50%

2

4

6

8

rage discoun

t

EV/EB

‐60%0

2

OGK 1 OGK 2 OGK 3 OGK 4 OGK 5 OGK 6 OGKs average

EM peers

Aver

1522.11.2010

2011 2012 2013 2014 2015 Discount to EM peers (rhs)

Source: VTB Capital, WAM

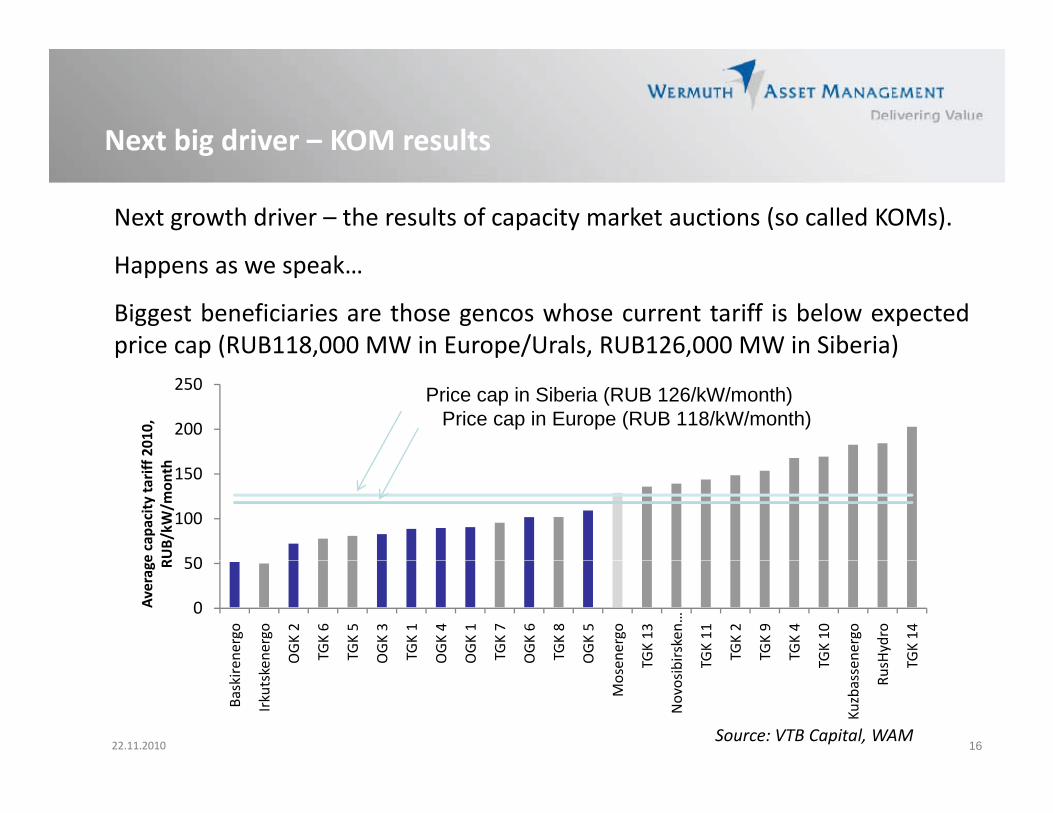

Next big driver – KOM resultse t b g d e O esu ts

Next growth driver – the results of capacity market auctions (so called KOMs).

Happens as we speak…

Biggest beneficiaries are those gencos whose current tariff is below expectedprice cap (RUB118,000 MW in Europe/Urals, RUB126,000 MW in Siberia)p p ( , p / , , )

200

250

2010,

Price cap in Siberia (RUB 126/kW/month)Price cap in Europe (RUB 118/kW/month)

50

100

150

e capa

city ta

riff

RUB/kW

/mon

th

0

50

energo

energo

OGK 2

TGK 6

TGK 5

OGK 3

TGK 1

OGK 4

OGK 1

TGK 7

OGK 6

TGK 8

OGK 5

energo

TGK 13

birsken…

TGK 11

TGK 2

TGK 9

TGK 4

TGK 10

energo

sHydro

TGK 14

Average R

1622.11.2010

Baskire

Irkutske

Mose T

Novosib T T

Kuzbasse

Rus T

Source: VTB Capital, WAM

Generation bottom lineGe e at o botto e

‐ Risk profile of the sector improved after capacity marketparameters and returns for Capacity commissioningparameters and returns for Capacity commissioningagreements (so called DPM) have been approved by theregulator. New investment is value accretive, no more valuedestructivedestructive,

‐ Russian electricity generation market regulation is mostfavorable among BRIC countries Opposed to commonfavorable among BRIC countries. Opposed to commonperception,

‐ Not only value but also growth story. Russian gencos have ay g y gunique earnings growth profile,

‐ Sector is now cheap not only on EV/capacity multiples but also

1722.11.2010

on financial multiples with earnings profile significantlyimproved. Our top‐picks: OGK‐2, TGK‐1, RusHydro, OGK‐4

Contact detailsCo tact deta s

Sergey EzimovPortfolio AdviserPortfolio [email protected]+7‐495‐580‐7300

1822.11.2010

+7 495 580 7300

APPENDIX

1922.11.2010

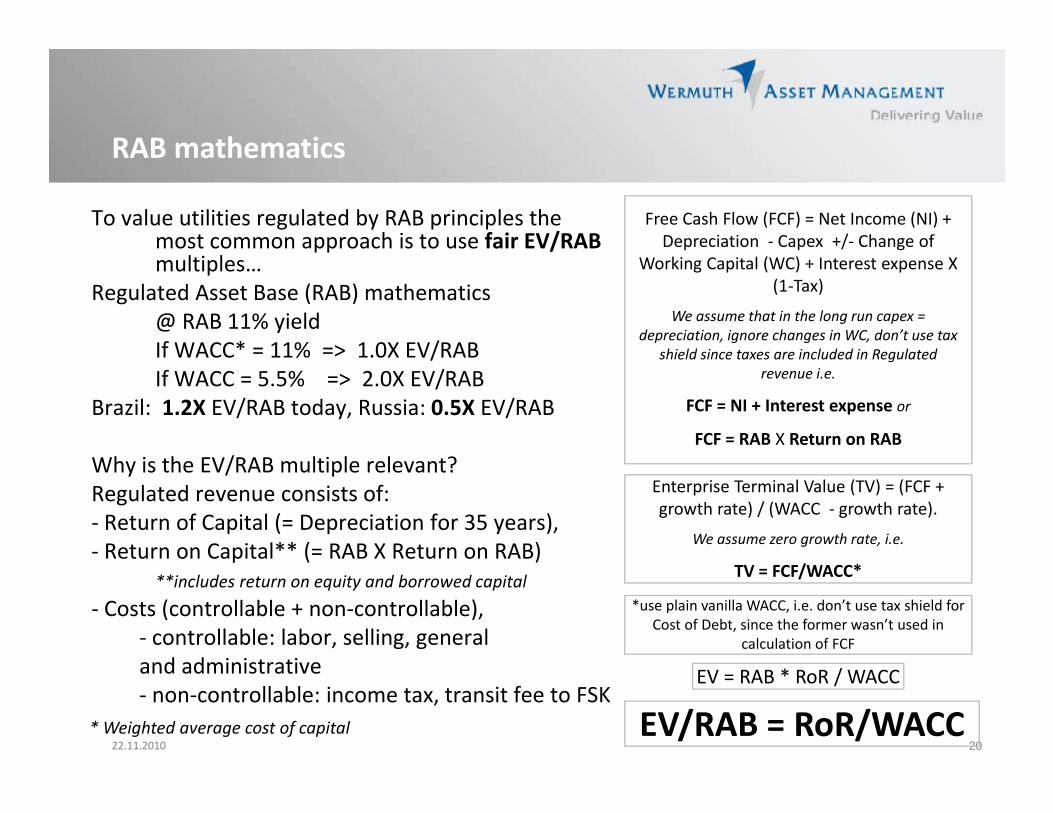

RAB mathematics

To value utilities regulated by RAB principles the most common approach is to use fair EV/RAB

RAB mathematics

Free Cash Flow (FCF) = Net Income (NI) + Depreciation ‐ Capex +/‐ Change of

multiples…Regulated Asset Base (RAB) mathematics

@ RAB 11% yieldIf WACC* = 11% => 1.0X EV/RAB

Working Capital (WC) + Interest expense X (1‐Tax)

We assume that in the long run capex = depreciation, ignore changes in WC, don’t use tax

shield since taxes are included in RegulatedIf WACC 11% > 1.0X EV/RABIf WACC = 5.5% => 2.0X EV/RAB

Brazil: 1.2X EV/RAB today, Russia: 0.5X EV/RAB

Wh i h EV/RAB l i l l ?

shield since taxes are included in Regulated revenue i.e.

FCF = NI + Interest expense or

FCF = RAB X Return on RABWhy is the EV/RAB multiple relevant?Regulated revenue consists of: ‐ Return of Capital (= Depreciation for 35 years),‐ Return on Capital** (= RAB X Return on RAB)

Enterprise Terminal Value (TV) = (FCF + growth rate) / (WACC ‐ growth rate).

We assume zero growth rate, i.e.p ( )**includes return on equity and borrowed capital

‐ Costs (controllable + non‐controllable),‐ controllable: labor, selling, general and administrative

TV = FCF/WACC*

*use plain vanilla WACC, i.e. don’t use tax shield for Cost of Debt, since the former wasn’t used in

calculation of FCF

2022.11.2010

and administrative‐ non‐controllable: income tax, transit fee to FSK

EV = RAB * RoR / WACC

EV/RAB = RoR/WACC* Weighted average cost of capital

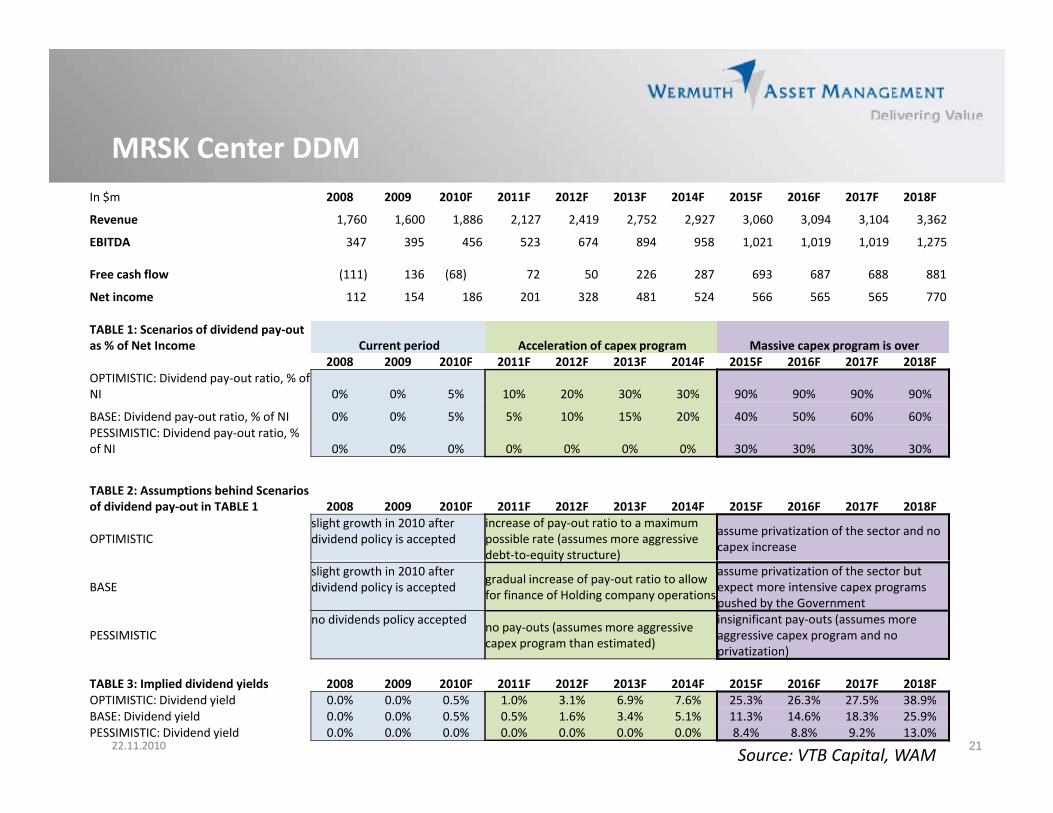

MRSK Center DDMIn $m 2008 2009 2010F 2011F 2012F 2013F 2014F 2015F 2016F 2017F 2018F

Revenue 1,760 1,600 1,886 2,127 2,419 2,752 2,927 3,060 3,094 3,104 3,362

EBITDA 347 395 456 523 674 894 958 1,021 1,019 1,019 1,275

MRSK Center DDM

Free cash flow (111) 136 (68) 72 50 226 287 693 687 688 881

Net income 112 154 186 201 328 481 524 566 565 565 770

TABLE 1: Scenarios of dividend pay‐out as % of Net Income Current period Acceleration of capex program Massive capex program is over

2008 2009 2010F 2011F 2012F 2013F 2014F 2015F 2016F 2017F 2018FOPTIMISTIC: Dividend pay‐out ratio, % of NI 0% 0% 5% 10% 20% 30% 30% 90% 90% 90% 90%

BASE: Dividend pay‐out ratio, % of NI 0% 0% 5% 5% 10% 15% 20% 40% 50% 60% 60%PESSIMISTIC: Dividend pay‐out ratio, % of NI 0% 0% 0% 0% 0% 0% 0% 30% 30% 30% 30%

TABLE 2: Assumptions behind Scenarios of dividend pay‐out in TABLE 1 2008 2009 2010F 2011F 2012F 2013F 2014F 2015F 2016F 2017F 2018F

OPTIMISTICslight growth in 2010 after dividend policy is accepted

increase of pay‐out ratio to a maximum possible rate (assumes more aggressive debt‐to‐equity structure)

assume privatization of the sector and no capex increaseq y )

BASEslight growth in 2010 after dividend policy is accepted gradual increase of pay‐out ratio to allow

for finance of Holding company operations

assume privatization of the sector but expect more intensive capex programs pushed by the Government

PESSIMISTICno dividends policy accepted no pay‐outs (assumes more aggressive

capex program than estimated)

insignificant pay‐outs (assumes more aggressive capex program and no privatization)

2122.11.2010

TABLE 3: Implied dividend yields 2008 2009 2010F 2011F 2012F 2013F 2014F 2015F 2016F 2017F 2018FOPTIMISTIC: Dividend yield 0.0% 0.0% 0.5% 1.0% 3.1% 6.9% 7.6% 25.3% 26.3% 27.5% 38.9%BASE: Dividend yield 0.0% 0.0% 0.5% 0.5% 1.6% 3.4% 5.1% 11.3% 14.6% 18.3% 25.9%PESSIMISTIC: Dividend yield 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 8.4% 8.8% 9.2% 13.0%

Source: VTB Capital, WAM

Related Documents

![[Nahu] - An wa3ul 'Irab (arabic)](https://static.cupdf.com/doc/110x72/549a225eac7959132e8b5af1/nahu-an-wa3ul-irab-arabic.jpg)