Electronic copy available at: http://ssrn.com/abstract=2535224 Investigating liquidity in a frontier government bond market: the case of Bucharest Stock Exchange Prof.dr. Cornelia Pop, Department of Business, Faculty of Business, Babes-Bolyai University, Cluj-Napoca, Romania, [email protected] Assoc.Prof.dr. Maria-Andrada Georgescu, Department of Economics and Public Policies, National University of Political Studies and Public Administration, Bucharest, Romania Lecturer dr. Iustin Atanasiu Pop, Department of Business, Faculty of Business, Babes-Bolyai University, Cluj-Napoca, Romania (version August 10 th 2014) Abstract: Liquidity is an important feature for any domestic bond market, being associated with a well organized market. A liquid secondary government bond market must be of interest for any frontier economy policy-makers given the important benefits. The present paper is the first to investigate the liquidity of government bond secondary market in Romania, included in the subgroup of frontier securities market. The paper use multivariate empirical analysis using the data set available at Bucharest Stock Exchange for the period August 2008, when the secondary market for government bonds was launched, and December 2013. Since this is the first paper trying to measure the liquidity of BVB government bond market segment, a high number of proxies were first selected in order to capture all the liquidity dimensions. Also five factors were identified to influence the majority of these proxies. In the end, four factors of the initial five proved to have an increased explanatory power over the liquidity proxies. Further, the number of twelve liquidity proxies should be reduced and a PCA was conducted in order to extract a smaller number. The final result indicates a number of four liquidity proxies that captured in a satisfactory manner all the liquidity dimensions. The results suggests that the Romanian Ministry of Finance should pay a special attention to these four proxies and to the idemtfied factors influencing them in order to increase the government bond segment liquidity at Bucharest Stock Exchange. Key words: government bonds, liquidity, factors, liquidity proxy, Principal-Component Analysis JEL Classification: G100, G190 1. Introduction The ability of emerging economies to develop domestic debt markets was documented by recent studies of Jaramillo & Weber (2013), Comelli (2012), and Burger et al. (2012) and highlighted by Global Financial Stability Reports of 2005, 2006 and 2013. The subgroup of frontier economies, smaller and less developed, seems to follow the same trend in establishing local currency-denominated bond markets, nevertheless this phenomenon and related topics, like liquidity, remained of low interest for academic studies. Liquidity is an important feature for any domestic bond market, being associated with a well organized market. A liquid secondary government bond market must be of interest for any frontier economy policy-makers given the important benefits. The importance of liquidity and liquidity functions for government bond markets were documented and underlined by McCauley & Remolona (2000), Mohanty (2002), Anderson & Lavoie (2004), Luengnaruemitchai & Ong (2005), Burger & Warnok (2006), Burger & Warnok (2007), Peiris (2010), Daniel (2008), and Ebeke & Lu (2014). A brief synthesis of what the mentioned studies underscored is presented as follow.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Electronic copy available at: http://ssrn.com/abstract=2535224

Investigating liquidity in a frontier government bond market:

the case of Bucharest Stock Exchange

Prof.dr. Cornelia Pop, Department of Business, Faculty of Business, Babes-Bolyai University,

Cluj-Napoca, Romania, [email protected]

Assoc.Prof.dr. Maria-Andrada Georgescu, Department of Economics and Public Policies,

National University of Political Studies and Public Administration, Bucharest, Romania

Lecturer dr. Iustin Atanasiu Pop, Department of Business, Faculty of Business, Babes-Bolyai

University, Cluj-Napoca, Romania

(version August 10th

2014)

Abstract:

Liquidity is an important feature for any domestic bond market, being associated with a well organized market. A

liquid secondary government bond market must be of interest for any frontier economy policy-makers given the

important benefits. The present paper is the first to investigate the liquidity of government bond secondary market in

Romania, included in the subgroup of frontier securities market. The paper use multivariate empirical analysis using

the data set available at Bucharest Stock Exchange for the period August 2008, when the secondary market for

government bonds was launched, and December 2013. Since this is the first paper trying to measure the liquidity of

BVB government bond market segment, a high number of proxies were first selected in order to capture all the

liquidity dimensions. Also five factors were identified to influence the majority of these proxies. In the end, four

factors of the initial five proved to have an increased explanatory power over the liquidity proxies. Further, the

number of twelve liquidity proxies should be reduced and a PCA was conducted in order to extract a smaller

number. The final result indicates a number of four liquidity proxies that captured in a satisfactory manner all the

liquidity dimensions. The results suggests that the Romanian Ministry of Finance should pay a special attention to

these four proxies and to the idemtfied factors influencing them in order to increase the government bond segment

liquidity at Bucharest Stock Exchange.

Key words: government bonds, liquidity, factors, liquidity proxy, Principal-Component Analysis

JEL Classification: G100, G190

1. Introduction

The ability of emerging economies to develop domestic debt markets was documented by recent

studies of Jaramillo & Weber (2013), Comelli (2012), and Burger et al. (2012) and highlighted

by Global Financial Stability Reports of 2005, 2006 and 2013. The subgroup of frontier

economies, smaller and less developed, seems to follow the same trend in establishing local

currency-denominated bond markets, nevertheless this phenomenon and related topics, like

liquidity, remained of low interest for academic studies.

Liquidity is an important feature for any domestic bond market, being associated with a well

organized market. A liquid secondary government bond market must be of interest for any

frontier economy policy-makers given the important benefits. The importance of liquidity and

liquidity functions for government bond markets were documented and underlined by McCauley

& Remolona (2000), Mohanty (2002), Anderson & Lavoie (2004), Luengnaruemitchai & Ong

(2005), Burger & Warnok (2006), Burger & Warnok (2007), Peiris (2010), Daniel (2008), and

Ebeke & Lu (2014). A brief synthesis of what the mentioned studies underscored is presented as

follow.

Electronic copy available at: http://ssrn.com/abstract=2535224

First, a domestic government security market provides a basis for a robust and efficient financial

system as a whole. Burger & Warnok (2006) documented the correlation between the issuance of

domestic debt and the quality improvement of financial systems. A liquid market allows lower

financing cost for government deficits, and also plays an important role in the implementation

and transmission of monetary policies by absorbing a share of liquid savings.

Second, a local currency-denominated bond market reduces the reliance on overseas financing in

foreign currency, and helps reducing the financial fragility and vulnerabilities associated with

currency mismatches. Through a liquid domestic government bond market, a frontier economy is

able to borrow ‘abroad’ (Daniel 2008) in its own currency, and by attracting foreign investors

that could act as catalysts for further development mainly by diversifying the investor base, and

increasing the demand for local debt securities (Peiris 2010, Ebeke & Lu 2014). Moreover, such

and evolution can create room for countercyclical domestic policy response to adverse external

shocks (Miyajima et al. 2012).

Third, a local government bond market generates a yield curve that reflects market-determined

interest rates that reveal the opportunity costs of funds for a wider range of maturities, providing

the policy-makers with a source of information on financial market interest expectations.

Fourth, a liquid secondary market for government bonds can represent a credible benchmark,

facilitating the pricing of other riskier assets, the hedging of other types of assets, encouraging

the use of government bonds as collateral for other financial transactions, having an important

impact on other financial market segments developments.

Given the importance of liquidity for a domestic government bond market development in a

frontier economy, it is critical to measure the liquidity of such a market in order to allow further

studies regarding the liquidity determinants and liquidity premium.

Liquidity is an elusive, amorphous, complex, an abstract feature for any market, difficult to

capture by a single measure given its multifaceted nature associated with multiple dimensions

Amihud (2002), Mohanty (2002), Anderson & Lavoie (2004), Diaz et al. (2006), Schaeffer &

Schmalz (2009). As highlighted by Borio (2000), and Jankowitsch et al. (2002), many market

participants and academic researchers have a general sense of what liquidity means, being more

easily recognized than defined and measured.

The concept of liquidity and various aspects of this concept were discussed and investigated by a

large number of academic studies and papers. In recent years the following authors Jankowitsch

et al.(2002), Kay (2008), Goyenko et al.(2011), Schaeffer & Schmalz (2009), provided

comprehensive literature reviews and discussions regarding liquidity concept and it will be

pointless to repeat their ideas. However, a synthesis of liquidity dimensions and their potential

measures along with a series of stylized facts regarding liquidity was seldom or never done and

is of interest for the present paper.

While the academic literature investigating liquidity in developed and emerging government

bond markets is extensive, little attention was concentrated on frontier markets either due to

absence of such markets or the lack of data.

The present paper is the first to investigate the liquidity of government bond secondary market in

Romania, included in the subgroup of frontier securities market. The paper use multivariate

empirical analysis using the data set available at Bucharest Stock Exchange for the period

August 2008, when the secondary market for government bonds was launched, and December

2013. Through the investigations regarding the presence of stylized facts on government bond

liquidity, and by revealing the liquidity proxies that can be calculated for this market, along with

their determinants, the paper further reveals a low to moderate level of liquidity and points out

that the main problem lays with the government bond issuer, Romanian Ministry of Finance,

which after five years is still struggling to grasp the significant role government bonds play as

benchmarks for the domestic market, including the importance of liquidity for these securities’

secondary market. In addition to this contribution to the academic literature, the paper proposes a

synthesis of liquidity dimensions and their potential measures or proxies, identifies and present a

series of six stylized facts regarding government bond liquidity, and proposes that several of

former liquidity proxies (outstanding quantity, coupon and time to maturity) to be considered

rather liquidity determinants/ factors since they are given characteristics established by the

issuer.

Further, the paper is structured as follow: subparagraphs 1.1. and 1.2. are related to introduction

and present a synthesis of liquidity dimensions and their proposed proxies, as the academic

literature discuss and use them, and respectively a selection of stylized facts regarding

government bond liquidity. Part 2 presents briefly the data and methodology. Part 3 offers an up

to date survey of the government bond market segment at Bucharest Stock Exchange. Part 4

presents the findings and discussions and part 5 concludes.

1.1. Liquidity dimensions

As mentioned above, the difficulty in measuring liquidity arises from its complex and

multifaceted nature associated with its multiple dimensions. Table 1 below presents a synthesis

of these dimensions’ definitions and the measures or liquidity proxies that can be associated with

the respective dimensions.

Table 1: Liquidity dimensions and corresponding measures/ proxies

Liquidity dimension1)

Liquidity measures/ proxies2)

Tightness: refers to the cost efficiency of any

transactions; the lower the cost, the higher the

liquidity. Note: Anderson & Lavoie (2004) citing Gravelle 1999,

names this dimension width.

Traditionally measured by bid-ask spread.

Alternative measures: Roll measure, gamma,

zero return days (or LOT), Imputed Roundtrip

Trades, dispersion or unique round trip cost.

Depth: refers to transaction dimensions

(abundant number of orders and order volume)

that can be absorbed by the market without

causing sharp changes in price. Note: most of the sources above imply that depth

includes breadth. Breadth is mentioned only by Sarr &

Lybeck (2002) and Baker (1996) as cited by Gabrielsen

et al.(2011)

Traditionally associated mainly with volume

based liquidity measures like trading volume,

size of trade, volume per trade, order volume,

turnover ratio, liquidity ratio, index of Martin,

Amihud illiquidity measure1, latent liquidity,

volume-weighted difference measure, Hui-

Heubel liquidity ratio.

Resiliency or resilience: refers to the market

capacity to absorb random shocks by

correcting order imbalances and/ or dissipating

price fluctuations with the highest speed

possible.

There is no consensus regarding the proxies

capturing this liquidity dimension. However,

the following proxies might capture it: liquidity

ratio, index of Martin Marsh and Rock

liquidity ratio, Amihud illiquidity measure,

trading frequency, frequency of trade, volume-

weighted difference measure, Hui-Heubel

liquidity ratio, market efficiency coefficient or

1 Since Amihud illiquidity measure (Amihud 2002) is related to price impact coefficient or lambda proposed by

Kyle (1985), Kyle’s coefficient was not mentioned distinctly.

variance ratio, non-trading-day adjusted

Amihud (illiquidity) measure or illiq_zero.

Immediacy: refers to the time needed for an

order to be processed; it considers the time

elapsed between the moment one order was

placed until it was settled

This is the most elusive liquidity dimension

and almost impossible to be captured with the

proxies proposed until now by the academic

literature.

Nevertheless, one can consider that the

liquidity proxies that capture resiliency

indirectly capture immediacy also. The simple

reasoning is: a high speed in absorbing the

random shocks must be supported by a fast

order processing activity. Note 1): The definitions of above presented liquidity dimensions represent authors’ compilation based on the

following sources: CGFS (1999), Borio (2000), Upper 2000, Mohanty (2002), Sarr & Lybeck (2002), Anderson &

Lavoie (2004), Schaeffer & Schmalz (2009), Turner (2012)

Note 2): The measures were compiled based on the following sources: Roll (1984), CGFS (1999), Lesmond et

al.(1999), Amihud (2002), Fleming (2003), Anderson & Lavoie (2004), Christodoulopoulos & Grigoratou (2005),

Mahanti et al.(2007), Bao et al.(2009), Jankowitsch et al.(2008), Dick-Nielsen et al.(2012), Schaeffer & Schmalz

(2009), Zhang (2010), Bushman et al.(2010), Gabrielsen et al.(2011).

The following academic studies provide further literature review and in depth discussions

regarding the liquidity measures: Sarr & Lybeck (2002), Goyenko et al.(2009), Dick-Nielsen et

al.(2012), Schaeffer & Schmalz (2009), Bushman et al.(2010), Zhang (2010), Gabrielsen et

al.(2011). The ideas expressed within these papers were considered and embedded in the

investigations of the current paper.

Most of the papers cited above also consider that coupon, outstanding quantity or inventory and

the age of the bond, as proposed by Sarig & Warga (1989), can stand as proxies for government

bond liquidity. Thus, these three measures do not capture any of the liquidity dimensions

presented above. Moreover, these three proposed proxies are in fact (government) bond given

characteristics, established by the issuer and should be considered rather factors that influence

the liquidity measures presented in Table 1, as the stylizes facts below suggest. Within this

paper, coupon, outstanding quantity and bond age will be considered liquidity factors and not

liquidity proxies.

1.2. Selected stylized facts regarding government bond liquidity

The abundant academic literature concerning the topic of government bond liquidity allow the

selection of the following features that can be currently considered stylized facts due to the

existing documented works and there are commonly accepted as such by numerous academic

papers. The further presentation of selected stylized facts was based on the following sources:

Amihud & Mendelson (1991), Gravelle (1999), Mohanty (2002), Jankowitsch et al.(2002), Sarig

& Warga (1989), Longstaff et al.(2004), Das et al.(2005), Kamara (1994), Fleming (2003),

Christodoulopoulos & Grigoratou (2005).

First, the benchmark2 (Treasury) bonds are often considered more liquid than other bonds. The

benchmark bonds also tend to trade close to par. Hence, the benchmarks are preferred by active

2 A benchmark bond, according to Banks (2005, pp.33), is a a market leading bond, generally featuring significant

liquidity and narrow bid-ask spread. It used to be also bellwether. Because a benchmark is used as a standard against

traders. In the US Treasury market, the benchmark property is closely related to the on-the-run

property and a concentration of liquidity can be seen in on-the-run and near maturity

benchmarks. Also in connection with the benchmark property, it is underscored that benchmark

bonds tend to cover particular maturity buckets and that there a strategy of concentrating the

issuance on a few important maturities is taking shape and is followed by many countries. This

strategy is used in order to avoid the problem of market fragmentation arising from issuing a

large number of maturities with small issue size.

Second, the ‘on-the-run’3 long term government bonds are considered to enjoy higher liquidity

before they are absorbed into investors’ portfolios. The phenomenon of trading concentration on

the most recently issued government bonds is described by mainly by Warga (1992) and Amihud

et al.(2005) showing that the availability of the on-the-run T-bonds through various investment

houses and banks make them more attractive for traders and investors.

Third, bond liquidity tends to decrease with age and the older bonds may be less liquid than more

recent issue bonds. This fact is related with (and might be considered a corollary of) the on-the-

run property and the trading behavior toward the newly issued bonds as mentioned within the

second stylized fact. Moreover, as stressed by Sarig & Warga (1989), once a bond becomes

illiquid, it tends to stay illiquid until it matures.

Fourth, the notional amount outstanding for a bond is used as an indicator of the general

availability of the respective bond in the market. Hence, it is expected that the bond issue size to

affect its liquidity in a positive way. The corollary is that the T-bonds with larger issues are

(expected to be) more liquid than the bonds with smaller issuers, and are expected to register

larger turnovers.

Fifth, more liquid bonds are expected to have higher prices (lower yields) than less liquid bonds.

Sixth, academic literature reports that high coupon bonds tend to be more liquid than the bonds

with low coupons.

2. Data, research questions and methodology

The main data set used for the present paper is represented by the daily information provided by

Bucharest Stock Exchange through the respective daily trading reports, including a dedicate

section for government bond trading. This data set was used, when appropriate, as end of period

data and as daily averages. The main data set was completed, when necessary, by information

provided through their official websites by Romanian Ministry of Finance and Romanian

National Bank.

The following research questions were addressed: 1) Do the six selected stylized facts regarding

government bond liquidity hold for Bucharest Stock Exchange? 2) The calculation of a set of

liquidity proxies based on the main data set available. 3) Verifying the general hypothesis: do the

identified liquidity factors have a combined influence over each liquidity proxy that could be

calculated? 4) Selecting of the calculated liquidity proxies a smaller number that captures better

all the liquidity dimensions at Bucharest Stock Exchange.

which other bonds are measured, T-bonds or government bonds are almost always used as benchmark

(Investopedia). The government benchmark bonds might have the reopening feature, meaning that a secondary

offering of a new tranche of securities under an existing issue with a defined coupon and maturity might be made.

For the secondary market, mainly in US, a benchmark T-bond is the most recently auctioned Treasury issue for each

maturity (Investopedia). 3 The ‘on-the-run’ property refers to the most recently issued bond for a given maturity bucket and are considered

more liquid than off-the-run bonds Jankowitsch et al.(2002).

The multivariate analysis was used, along with multiple regressions in order to address the first

three research questions. The answer to the fourth research question was obtained by using the

Pricipal-Component Analysis.

3. Government bond market segment at Bucharest Stock Exchange: August 2008- December

2013

The domestic government bonds were introduced for trading at Bucharest Stock Exchange (BVB

hereafter4) August 4

th 2008. They were the last newcomers of the BVB bond sector which was

launched in November 2001 with the listing of municipal bonds. Further, in May 2003, the

domestic corporate bonds were introduced, followed by the international (corporate) bonds in

September 2006. However, the bond sector had a relative low profile within BVB, as Graph 1

and Graph 2 below show. Before the introduction of T-bonds, the bond sector represented around

6% of BVB turnover, more than half due to the bond public offerings, thus infrequent, of large

value compared with daily bond turnover. The listing of T-bonds increased the bond sector share

to about 10%, while the importance of the bond public offerings remained over 3%. It must be

mentioned that none of the BVB bond public offerings included T-bonds.

Graph 1: BVB main market structure as of

December 2007

Graph 2: BVB main market structure as of

December 2013

Source: authors’ calculations based on BVB data

Source: authors’ calculations based on BVB data

The evolution of bond sector at BVB and its structure presented in the Table 2 show a very thin

market between the end of 2001 and 2003 revealing the low interest the domestic municipal

bonds attracted. After the introduction of corporate bonds, the bulk of the trading activity

gravitated around them and moved toward the international bonds segment in 2007 and 2008.

Since 2009, the domestic government bonds are the main focus of bond trading, a situation

generated not only by the importance of T-bonds for domestic institutional investor portfolios,

but also by the complete absence of listed domestic corporate bond since the beginning of 2010

4 BVB abbreviation was chosen over BSE in order to keep the identity of the main Romanian security market. BVB

is the abbreviation of Romanian name: Bursa de Valori Bucuresti. The BSE abbreviation for Bucharest Stock

Exchange might generate confusions with Budapest Stock Exchange, Bulgarian Stock Exchange, Bratislava Stock

Exchange, and Belgrade Stock Exchange, all functioning in the same region of Central and Eastern Europe.

shares, 93.87%

bond-public offerings,

3.65%

bonds (municipals,

intl., corporate),

2.25%

other securities

(rights, futures),

0.23%

shares, 87.20%

T-bonds, 5.53%

bond-public offerings,

3.27%

bonds (municipals,

intl., corporate),

1.56%

other securities

(rights, futures, ETFs,

structured products),

2.44%

until the fourth quarter of 2012. The more intense trading activity of 2009 and 2010 was almost

entirely generated by the ‘flight to safety’ behavior as a response to global financial crisis

influence on shares. However, this interest toward domestic government bonds was abruptly

stopped by the sovereign bond crisis in Greece and the lack of investor confidence in the

sovereign bonds of several European Union countries. While Romanian economy was suffering,

the Romanian domestic government bonds never showed signs of distress. Thus, the general

mistrust in sovereign bonds mainly issued by emerging/ frontier economies left its imprint on

BVB bond market sector also.

Table 2: BVB bond sector trading and structure (without public offerings) Year No. of

trades

Volume Trading

value

(mil.EUR)

No.of

listed

issues

(end of

period)

New

listed

issues

% of

municipal

bonds

% of

corporate

bonds

% of

intl

bonds

% of T-

bonds

2001 5 45 0.00 2 2 100 - - -

2002 10 59,050 0.25 4 2 100 - - -

2003 37 29,870 0.36 10 9 95.66 4.34 - -

2004 274 118,136 13.15 25 17 10.02 89.98 - -

2005 334 197,107 29.67 19 6 2.38 97.62 - -

2006 319 603,208 53.88 18 5 3.80 49.38 46.82 -

2007 233 3,652,467 147.99 22 11 2.00 10.03 87.97 -

2008 547 862,927 53.47 50 34 15.92 22.30 52.09 9.69

2009 958 1,822,908 277.75 60 16 1.65 5.15 15.80 77.40

2010 540 591,511 552.87 55 7 0.99 0.00 0.59 98.42

2011 245 857,248 105.21 59 6 1.91 0.00 16.55 81.54

2012 368 220,238 264.87 63 8 0.04 0.00 0.91 99.05

2013 475 106,048 95.21 67 7 0.65 9.44 0.05 89.86 Source: Source: authors’ calculations based on BVB data

Note: the exchange rate used is the one reported by EUROSTAT, available at

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&language=en&pcode=tec00033&plugin=1

Table 3 presents only the government bond (T-bond) market segment evolution at BVB.

As mentioned above, the intense trading activity of 2009 and 2010 took place under the influence

of the global financial crisis on shares and the alternative offered by the newly listed T-bonds

represented a welcomed investment alternative. The year 2011 suffered from the influence of

successive outburst of Greece sovereign bond crisis and its effects were still present during 2012

when the market reached only half the level of 2010. The 2013 decrease indicates a lack of

interest toward T-bonds since the equity market recovered and offers better returns.

Table 3: BVB T-bond market segment Year No. of trades Volume Trading value

(mil.EUR)

No.of listed

issues

(end of period)

New listed

issues

2008 17 2,069 5.18 24 25

2009 346 85,689 241.98 26 2

2010 435 203,724 544.13 18 2

2011 181 35,889 85.78 21 4

2012 358 114,245 262.37 24 7

2013 337 35,575 86.56 26 4 Source: Source: authors’ calculations based on BVB data

Note: the exchange rate used is the one reported by EUROSTAT, available at

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&language=en&pcode=tec00033&plugin=1

It is interesting to observe that there seems to be a constant reluctance of Romanian Ministry of

Finance in listing the domestic government bond issues. With the exception of 2012, when 7 new

issues were listed, the newly introduced issues are scarce and they are just enough to keep the

number of total listed T-bonds around 25, as many as they were when this sector was launched.

In fact, this situation of newly listed T-bond issues at BVB only confirms the general non-

collaborative attitude of Romanian Ministry of Finance representatives who were asked since

1998 by BVB representatives to list the domestic government bonds. The reluctance manifested

by the Ministry of Finance combined with the Romanian National Bank lack of willingness to

lose a share of the secondary interbank government bond market it organize and supervise

(Pandele 2007).

The “change of heart” of 2008 might took place under the requirements/ recommendations of

European Union (EU), after Romania became an EU member, rather than of internal willingness.

Another factor that pressured the listing of T-bonds was the launch, at the beginning of 2008, of

the second pillar’s private pension funds which had limited investment options and the domestic

government bonds represent the main recommended placements. Under these two impulses, the

transparency regarding Romanian sovereign debt increased abruptly from non existent through a

dedicated link on Romanian Ministry of Finance website.

Further, several selected facts regarding the listed T-bonds will be presented.

As Table 4 shows, while the internal debt financed through government bonds grew between

2008 and 2013, the outstanding listed T-bonds at BVB decrease from 70% of the issued

government bonds at the end of 2008 to 17% at the end of 2013. Also, the listed T-bonds barely

overpass 4% of GDP in 2009 and were less than 3% in 2013. This only support the observation

above regarding the fact that only a small number of the issued government bonds are introduced

to the secondary market provided by BVB.

Table 4: BVB listed T-bonds within domestic internal debt and GDP (mil.EUR and %)

2008 2009 2010 2011 2012 2013

Internal debt of central

public administration

financed through

government bonds

( % of internal debt)

4,762.18

(63.06)

10,841.95

(75.30)

15,108.76

(77.74)

19,114.62

(82.56)

21,358.67

(87.04)

21,828.81

(87.90)

Outstanding listed

T-bonds

as % of internal debt

financed through

government bonds

68.58 44.58 32.07 23.87 18.33 17.28

Outstanding listed

T-bonds

as % of GDP

2.34 4.09 3.90 3.47 2.98 2.64

Source: authors’ calculations based on the data available at:

http://www.mfinante.ro/trezorengl.html?pagina=domenii

Note: the exchange rate used is the one reported by EUROSTAT, available at:

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&language=en&pcode=tec00033&plugin=1

No government bon public offer was launched through BVB system for the period under

scrutiny; the primary dealers system of the primary market was preferred instead.

Since August 2008 until December 2013, a number of 44 government bond issues were listed at

BVB, of which 19 reached the maturity; 7 of the matured bonds were never traded during the

listing period.

The situation of listed and traded T-bonds at BVB is presented in Graph 3 below and reflects that

between one third and half of the listed T-bonds were traded, with the exception of a slow first

year and the decrease of 2011, due to the sovereign crisis.

Graph 3: Listed and traded T-bonds at BVB between August 2008 and December 2013

Source: authors’ calculations based on the data available at BVB, http://www.bvb.ro/Companies/DGovBonds.aspx

The general profile of BVB listed government bonds includes the following features: they are

vanilla (bullet) bonds, with medium to long-term maturities, a nominal/ face value of 10,000

RON or about 2,376 EUR (average value for the period 2008 to December 2013). The coupon is

fix and paid annually.

The BVB listed government bonds are of two types: common (symbol starting with letter F) and

benchmark (symbol starting with letter B). The listed benchmark government bonds were issued

starting with 2007, according to the data offered by BVB. However, the Romanian Ministry of

Finance did not ‘capture’ the international meaning of benchmark bonds. The brief definition

that exists (available in Romanian only on BVB website) emphasizes the reopening feature of the

benchmark bonds. Until now, this feature was never used by Romanian authorities in order to

concentrate liquidity on a given maturity. The differences between the common bonds and

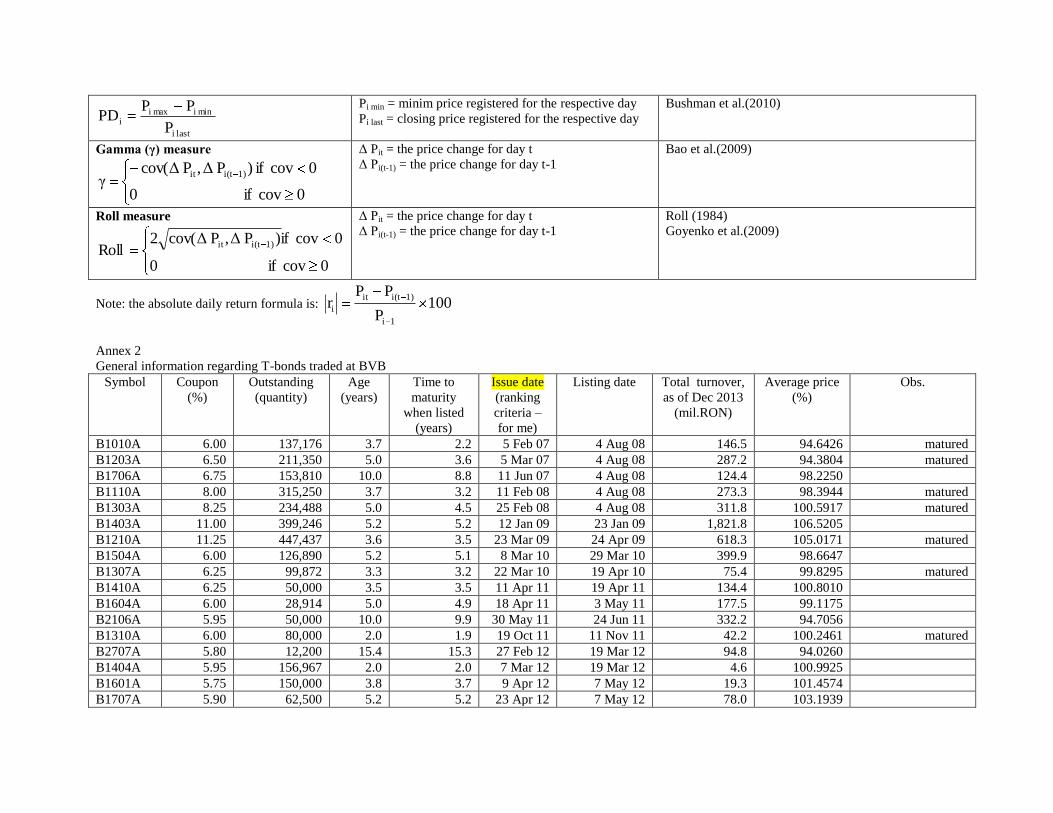

benchmark bonds can be observed in Annex 2 and the main difference is given by the issue

dimension: benchmark issues are larger, while common issues ranged between 1,000 and 20,000

0

5

10

15

20

25

30

Au

g-0

8

No

v-0

8

Feb

-09

May

-09

Au

g-0

9

No

v-0

9

Feb

-10

May

-10

Au

g-1

0

No

v-1

0

Feb

-11

May

-11

Au

g-1

1

No

v-1

1

Feb

-12

May

-12

Au

g-1

2

No

v-1

2

Feb

-13

May

-13

Au

g-1

3

No

v-1

3

listed issues traded issues

bonds. Another ‘difference’ is the fact that no new common bond issue was listed at BVB

starting with 2009. Therefore, the benchmark is rather a label than an active feature.

Nevertheless, the benchmark bonds are the most traded.

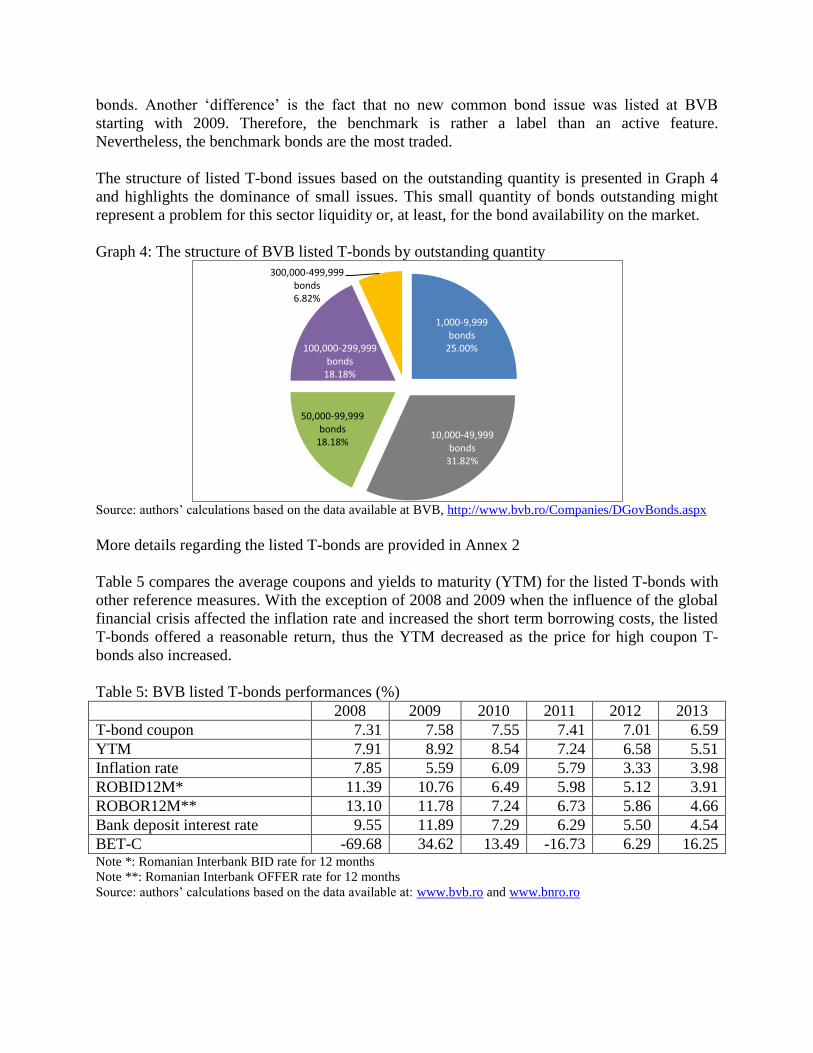

The structure of listed T-bond issues based on the outstanding quantity is presented in Graph 4

and highlights the dominance of small issues. This small quantity of bonds outstanding might

represent a problem for this sector liquidity or, at least, for the bond availability on the market.

Graph 4: The structure of BVB listed T-bonds by outstanding quantity

Source: authors’ calculations based on the data available at BVB, http://www.bvb.ro/Companies/DGovBonds.aspx

More details regarding the listed T-bonds are provided in Annex 2

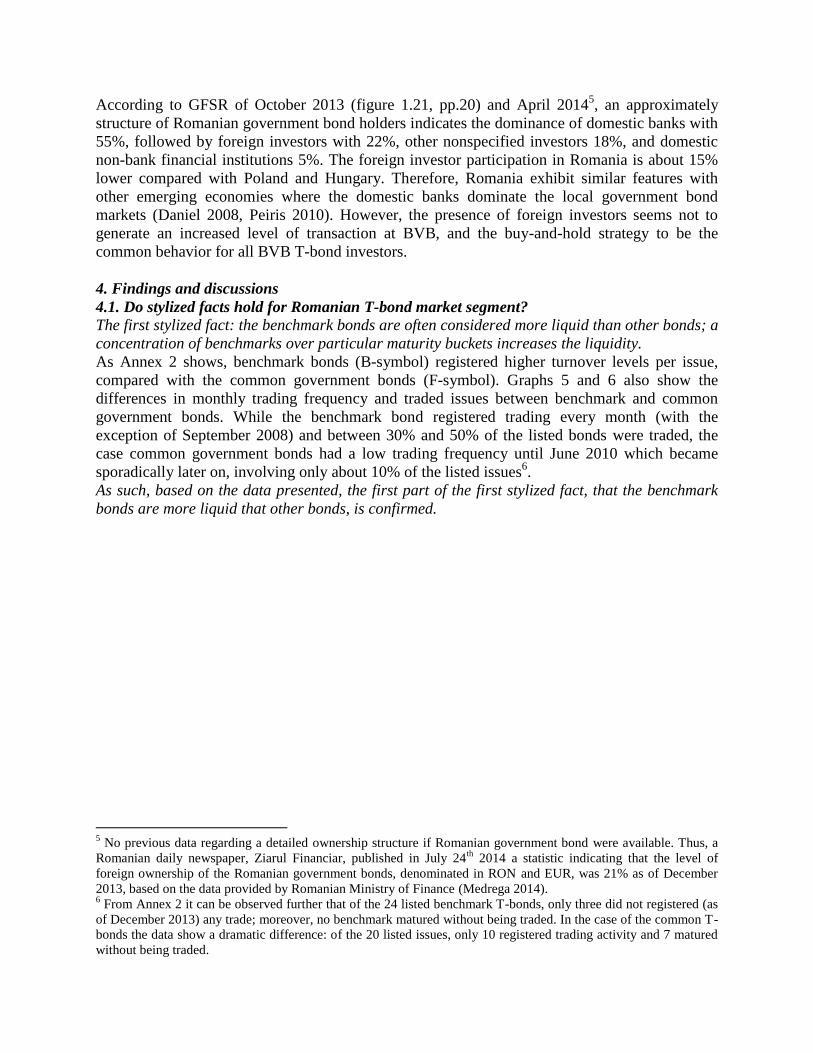

Table 5 compares the average coupons and yields to maturity (YTM) for the listed T-bonds with

other reference measures. With the exception of 2008 and 2009 when the influence of the global

financial crisis affected the inflation rate and increased the short term borrowing costs, the listed

T-bonds offered a reasonable return, thus the YTM decreased as the price for high coupon T-

bonds also increased.

Table 5: BVB listed T-bonds performances (%)

2008 2009 2010 2011 2012 2013

T-bond coupon 7.31 7.58 7.55 7.41 7.01 6.59

YTM 7.91 8.92 8.54 7.24 6.58 5.51

Inflation rate 7.85 5.59 6.09 5.79 3.33 3.98

ROBID12M* 11.39 10.76 6.49 5.98 5.12 3.91

ROBOR12M** 13.10 11.78 7.24 6.73 5.86 4.66

Bank deposit interest rate 9.55 11.89 7.29 6.29 5.50 4.54

BET-C -69.68 34.62 13.49 -16.73 6.29 16.25 Note *: Romanian Interbank BID rate for 12 months

Note **: Romanian Interbank OFFER rate for 12 months

Source: authors’ calculations based on the data available at: www.bvb.ro and www.bnro.ro

1,000-9,999 bonds

25.00%

10,000-49,999 bonds

31.82%

50,000-99,999 bonds

18.18%

100,000-299,999 bonds

18.18%

300,000-499,999 bonds 6.82%

According to GFSR of October 2013 (figure 1.21, pp.20) and April 20145, an approximately

structure of Romanian government bond holders indicates the dominance of domestic banks with

55%, followed by foreign investors with 22%, other nonspecified investors 18%, and domestic

non-bank financial institutions 5%. The foreign investor participation in Romania is about 15%

lower compared with Poland and Hungary. Therefore, Romania exhibit similar features with

other emerging economies where the domestic banks dominate the local government bond

markets (Daniel 2008, Peiris 2010). However, the presence of foreign investors seems not to

generate an increased level of transaction at BVB, and the buy-and-hold strategy to be the

common behavior for all BVB T-bond investors.

4. Findings and discussions

4.1. Do stylized facts hold for Romanian T-bond market segment?

The first stylized fact: the benchmark bonds are often considered more liquid than other bonds; a

concentration of benchmarks over particular maturity buckets increases the liquidity.

As Annex 2 shows, benchmark bonds (B-symbol) registered higher turnover levels per issue,

compared with the common government bonds (F-symbol). Graphs 5 and 6 also show the

differences in monthly trading frequency and traded issues between benchmark and common

government bonds. While the benchmark bond registered trading every month (with the

exception of September 2008) and between 30% and 50% of the listed bonds were traded, the

case common government bonds had a low trading frequency until June 2010 which became

sporadically later on, involving only about 10% of the listed issues6.

As such, based on the data presented, the first part of the first stylized fact, that the benchmark

bonds are more liquid that other bonds, is confirmed.

5 No previous data regarding a detailed ownership structure if Romanian government bond were available. Thus, a

Romanian daily newspaper, Ziarul Financiar, published in July 24th

2014 a statistic indicating that the level of

foreign ownership of the Romanian government bonds, denominated in RON and EUR, was 21% as of December

2013, based on the data provided by Romanian Ministry of Finance (Medrega 2014). 6 From Annex 2 it can be observed further that of the 24 listed benchmark T-bonds, only three did not registered (as

of December 2013) any trade; moreover, no benchmark matured without being traded. In the case of the common T-

bonds the data show a dramatic difference: of the 20 listed issues, only 10 registered trading activity and 7 matured

without being traded.

Graph 5: Benchmark listed and traded T-bonds at BVB

Source: authors’ calculations based on the data available at BVB, http://www.bvb.ro/Companies/DGovBonds.aspx

Graph 6: Common listed and traded T-bonds at BVB

Source: authors’ calculations based on the data available at BVB, http://www.bvb.ro/Companies/DGovBonds.aspx

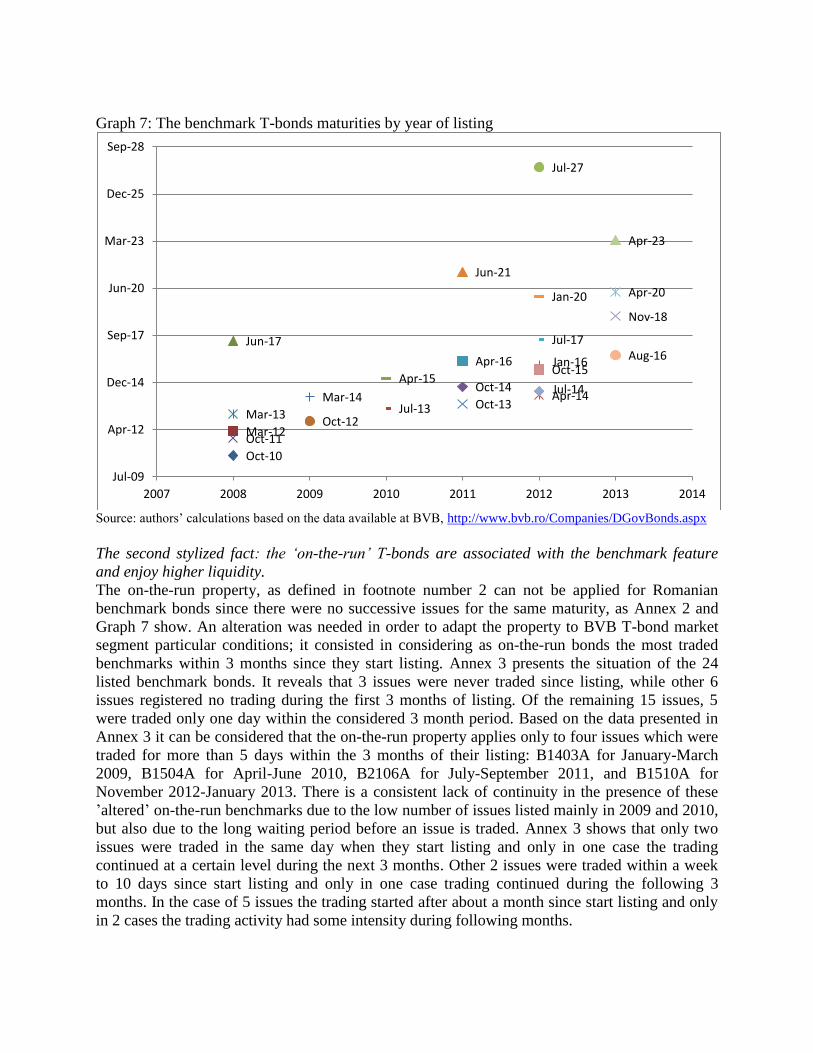

Further, Graph 7 shows the distribution of benchmark maturities by year of listing. There is no

tendency to concentrate on several maturities, which indicates that, at least for the last 5 years

since the launch of T-bond segment at BVB, there existed no strategy regarding the T-bonds’

maturities. As mentioned before, the reopening feature of benchmark issues was never used and

as the listed maturities multiplied, the trading spread thin among these maturities, as Annex 2

also shows.

Based on this finding, the second part of the first stylized fact, referring to the concentration of

benchmarks on several maturity buckets can not be confirmed for BVB T-bond market segment.

As such, the trading at BVB is fragmented covering most of the maturities of listed T-bonds.

0

2

4

6

8

10

12

14

16

18

20 A

ug-

08

Oct

-08

Dec

-08

Feb

-09

Ap

r-0

9

Jun

-09

Au

g-0

9

Oct

-09

Dec

-09

Feb

-10

Ap

r-1

0

Jun

-10

Au

g-1

0

Oct

-10

Dec

-10

Feb

-11

Ap

r-1

1

Jun

-11

Au

g-1

1

Oct

-11

Dec

-11

Feb

-12

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

B listed issues B traded issues

0

5

10

15

20

25

Au

g-0

8

No

v-0

8

Feb

-09

May

-09

Au

g-0

9

No

v-0

9

Feb

-10

May

-10

Au

g-1

0

No

v-1

0

Feb

-11

May

-11

Au

g-1

1

No

v-1

1

Feb

-12

May

-12

Au

g-1

2

No

v-1

2

Feb

-13

May

-13

Au

g-1

3

No

v-1

3

F traded issues F listed issues

Graph 7: The benchmark T-bonds maturities by year of listing

Source: authors’ calculations based on the data available at BVB, http://www.bvb.ro/Companies/DGovBonds.aspx

The second stylized fact: the ‘on-the-run’ T-bonds are associated with the benchmark feature

and enjoy higher liquidity.

The on-the-run property, as defined in footnote number 2 can not be applied for Romanian

benchmark bonds since there were no successive issues for the same maturity, as Annex 2 and

Graph 7 show. An alteration was needed in order to adapt the property to BVB T-bond market

segment particular conditions; it consisted in considering as on-the-run bonds the most traded

benchmarks within 3 months since they start listing. Annex 3 presents the situation of the 24

listed benchmark bonds. It reveals that 3 issues were never traded since listing, while other 6

issues registered no trading during the first 3 months of listing. Of the remaining 15 issues, 5

were traded only one day within the considered 3 month period. Based on the data presented in

Annex 3 it can be considered that the on-the-run property applies only to four issues which were

traded for more than 5 days within the 3 months of their listing: B1403A for January-March

2009, B1504A for April-June 2010, B2106A for July-September 2011, and B1510A for

November 2012-January 2013. There is a consistent lack of continuity in the presence of these

’altered’ on-the-run benchmarks due to the low number of issues listed mainly in 2009 and 2010,

but also due to the long waiting period before an issue is traded. Annex 3 shows that only two

issues were traded in the same day when they start listing and only in one case the trading

continued at a certain level during the next 3 months. Other 2 issues were traded within a week

to 10 days since start listing and only in one case trading continued during the following 3

months. In the case of 5 issues the trading started after about a month since start listing and only

in 2 cases the trading activity had some intensity during following months.

Oct-10

Mar-12

Jun-17

Oct-11

Mar-13 Oct-12

Mar-14 Jul-13

Apr-15 Oct-14

Apr-16

Jun-21

Oct-13 Apr-14

Jul-27

Jan-16

Jul-17

Jan-20

Jul-14

Oct-15

Apr-23

Nov-18

Apr-20

Aug-16

Jul-09

Apr-12

Dec-14

Sep-17

Jun-20

Mar-23

Dec-25

Sep-28

2007 2008 2009 2010 2011 2012 2013 2014

Based on these facts and on the data presented in Annex 3 only 3 issues (B1504A, B2106A and

B1510A) exhibit some features of on-the-run bonds. These three were selected based on the

trading volume and turnover registered during the 3 month period after listing. In Annex 4 can be

seen that these issues considered on-the-run rank 6th

, 4th

and 11th

when the average daily turnover

and the average daily volume are considered.

Hence, it can be reckoned that in an altered form the on-the-run property can be found in a

sporadically manner among the Romanian benchmaks7. However, it has no practical value since

there is not followed by frequent trading of the newly listed benchmarks.

The findings presented above indicate that the on-the-run property (even in a modified form) can

not be automatically associated with benchmark bonds at BVB and the identified on-the-run T-

bonds do not exhibit higher liquidity compared with the other benchmarks. The second stylized

fact is not confirmed at BVB.

The third stylized fact: bond liquidity tends to decrease with age and the older bonds may be less

liquid than more recent issue bonds.

In relation with on-the-run property, comes the age of the bond. While the third stylized fact

states that the older bonds may be less liquid than those more recently issued, Graphs 8 and 9

shows something different for BVB government bond market segment.

Graph 8: Benchmark bonds B1403A, B1203A and B1210A position in T-bond segment turnover

Source: authors’ calculations based on the data available at BVB, http://www.bvb.ro/Companies/DGovBonds.aspx

7 While the on-the-run property does not apply to the common T-bonds, it is interesting to mention that none of the

10 ordinary government bonds that registered trading activity was traded during the first 3 months since start listing.

B1203A, 26.94

B1203A, 12.67

B1203A, 4.65

B1203A, 12.34

B1203A, 1.29

B1403A, 43.43

B1403A, 54.88

B1403A, 0.23

B1403A, 10.05 B1403A, 13.14

B1210A, 23.56

B1210A, 14.55 B1210A, 13.50

B1210A, 1.79 0.00

10.00

20.00

30.00

40.00

50.00

60.00

2008 2009 2010 2011 2012 2013

%

B1203A B1403A B1210A

Graph 9: Benchmark bonds B1010A, B1504A, B1604A and B2106A position in T-bond

segment turnover

Source: authors’ calculations based on the data available at BVB, http://www.bvb.ro/Companies/DGovBonds.aspx

The most traded maturities (considered as percentage of the total T-bond market turnover of the

respective year) are the medium term ones. Thus, between 2011 and 2013, a long term maturity

(B2106A) was also intensely traded. Only in the case of the matured bonds B1010A and B1210A

the trading activity decreased as they approached their respective maturities. This might have

happened because their maturities were shorter than 5 years when they start trading. The other 5

most traded bonds show oscillations of the trading activity. They seem to become illiquid during

one year, just to come back the next year among the traded T-bonds (mainly the case of

B1403A). Also, the following cases must be mentioned: B1706A issue seemed to be an illiquid

one, while no trading was registered for almost one year and a half after listing; since January

2010 is traded with some frequency. In other two cases a similar pattern appeared; the bonds

start trading after more than 6 month after start listing.

Taking into consideration these observations, the third stylized fact does not hold for BVB T-

bond market segment. The most newly issued bonds do not trade immediately, and older issues,

which might seem illiquid, can start trading after a (long) waiting period. The combined causes

of this situation are: the relative low number of listed benchmark bonds and their spread among a

relative wide range of maturities. In this situation, the investors might start trading a T-bond that

was illiquid in the absence of other alternatives, without paying too much attention to the

maturity.

The fourth stylized fact: the T-bonds with larger issues are more liquid and are expected to

register larger turnovers.

As showed in paragraph 3 and presented in Annex 2, the outstanding amount of benchmark

bonds is considerably higher than that of the common bonds. The BVB benchmarks exhibit an

average of 141,400 bonds per issue, compared with an average of about 8,000 bonds per issue

B1010A, 65.40

B1010A, 6.81 B1010A, 3.14 B1504A, 2.26

B1504A, 15.64

B1504A, 24.75

B1504A, 0.43

B1604A, 14.19

B1604A, 5.06

B1604A, 17.64

B2106A, 8.26

B2106A, 23.59

B2106A, 6.89

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

2008 2009 2010 2011 2012 2013

%

B1010A B1504A B1604A B2106A

for the common T-bonds. As highlighted previously and presented in Annex 2, the benchmark

bonds registered higher turnover compared with common bonds.

Based on these observations the fourth stylized fact is confirmed for T-bond market segment at

BVB. The T-bond issues with larger outstanding amount registered, in general, higher turnover.

The fifth stylized fact: more liquid bonds have higher prices.

Annex 2 shows that the average closing price of benchmark bonds is higher and almost at par

than the average closing price of common bonds. As shown above, the BVB benchmarks are

more liquid than the common bonds. However, when details are considered, the data from Annex

2 are not conclusive. Hence, the daily averages were taken into consideration and presented in

Annex 4 The new data show more consistently that higher (supra par) prices are related to more

liquid T-bonds. While in the majority cases of the top 20 T-bonds, the fifth stylized fact is

verified, exceptions occur often and they are related to the coupon of the respective T-bonds, the

period when were issued and traded. The most obvious situation is that of the several illiquid

common (F symbol) T-bonds which registered high prices. This exception might have been

generated by fact that common bond coupons are at the level of 2005 when they were issued and

currently exhibit 200 to 300 basis points above the level of newly issued benchmark bonds.

Based on the facts presented above, it can be stated that, in general, the fifth stylized fact is

confirmed at BVB; more liquid bonds tend to have higher prices.

The sixth stylized fact: high coupon bonds tend to be more liquid than low-coupon bonds.

The data in Annex 2 show that at the level of total turnover, all the benchmark bonds with a

coupon higher than 6.00% registered trading values over 100 mil.RON. Thus, the common

bonds, with coupons ranging from 6.50% to 8.00% were seldom traded or never traded at all.

This situation can be explained by their low outstanding quantities combined with the fact that

being so scarce, the investors rather preferred to keep them in their portfolio than to trade them

even at a supra par price. When coupon is under scrutiny, the period when the T-bond was issued

and became available for trading should be considered, due to the fact that Romania exhibited a

decrease in inflation rate and a general decrease of interest rates, including the interest rates for

T-bonds.

It can be considered that, in general, the sixth stylized fact is confirmed for BVB T-bonds; thus

the peculiarities of this frontier market should be taken into consideration.

4.2. The liquidity factors and liquidity proxies for BVB T-bond market segment

4.2.1. The liquidity factors

Based on the ideas presented in paragraphs 3 and 4.1., and considering the data available at BVB

for the government market segment, the following five liquidity factors were identified: a) the

coupon (C), b) the outstanding quantity (Q), c) the time to maturity when listing (TM), d) the

listing period, and e) the retail trading (R).

While several of these factors are usually regarded as liquidity proxies, within this paper it was

chosen to take into consideration their role as liquidity determinants since the coupon, the

outstanding quantity and the time to maturity are given characteristics decided by the T-bond

issuer. Time to maturity when listing was taken into consideration instead of the time to

maturity, since in the case of T-bonds first listed in August 2008 the gap between the initial

maturity and the remaining life of the bond is important, mainly for common bonds (F-symbol),

as Annex 2 reveals. Starting with 2009 listed T-bonds, the gap decreased. Thus, in some cases

one month or more elapsed before the respective T-bond issue was listed. Time to maturity when

listed is strongly correlated with time to maturity and is a characteristics upon which investors

have no influence. Moreover, this factor considers the T-bond life span available to interested

investors. The listing period was considered as factor based on the observation related to the

third stylized fact which revealed that previously never traded issues might become active when

the number of listed issues decreases due to expiration, or when their coupon is considered

interesting enough to generate a high price. Also, the listing period might be considered a

substitute for on/off the run characteristic of T-bonds, which could not be highlighted at BVB, as

mentioned in paragraph 4.1.. For the fifth factor, retail trading, a proxy was considered due to the

absence of detailed information regarding the general investors’ structure (namely the percentage

of individual investors) for listed T-bond issues from the official custodian. The proxy capturing

the retail trading is the percentage of days (out of total number of days when trade occurred)

when only 1 to 5 bonds were traded. This proxy was chosen based on data availability and on the

reasoning that an institutional investors is highly unlikely to trade such small quantities. To this

assumption, the high nominal (face) value of a T-bond, of 10,000 RON, was added. It is unlikely

that a Romanian individual investor will spend more than 50,000 RON for an individual security,

due to the low level of resources available for investments.

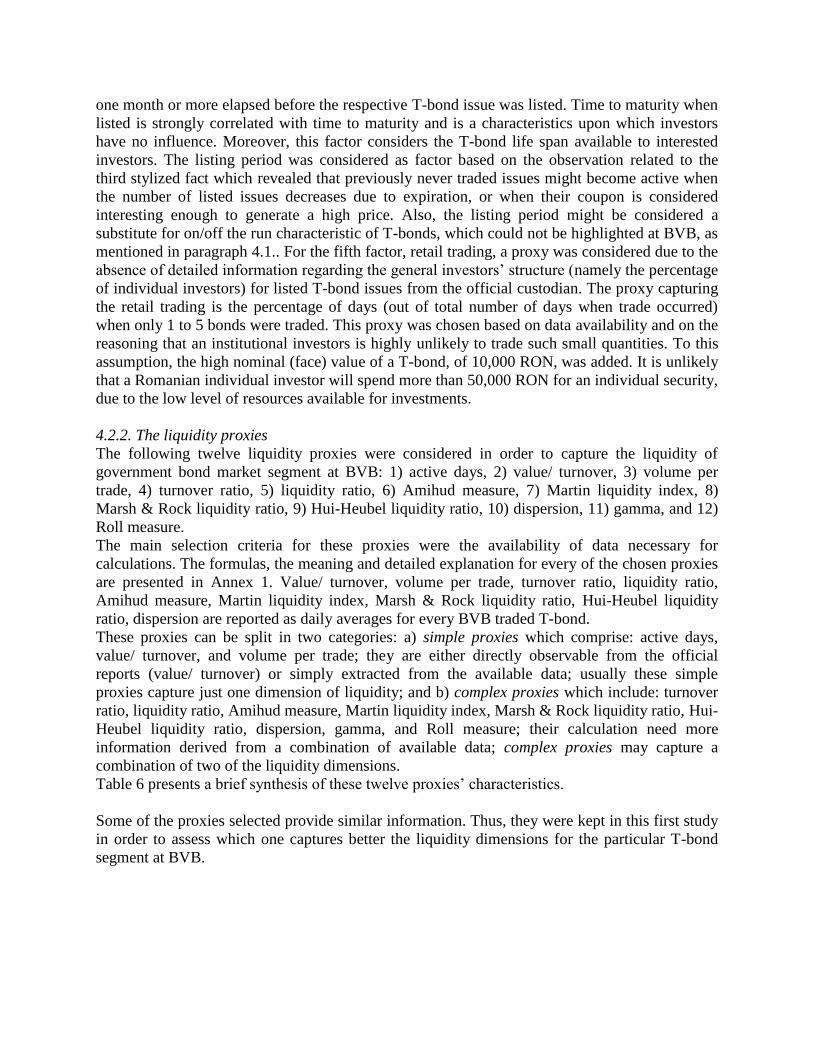

4.2.2. The liquidity proxies

The following twelve liquidity proxies were considered in order to capture the liquidity of

government bond market segment at BVB: 1) active days, 2) value/ turnover, 3) volume per

trade, 4) turnover ratio, 5) liquidity ratio, 6) Amihud measure, 7) Martin liquidity index, 8)

Marsh & Rock liquidity ratio, 9) Hui-Heubel liquidity ratio, 10) dispersion, 11) gamma, and 12)

Roll measure.

The main selection criteria for these proxies were the availability of data necessary for

calculations. The formulas, the meaning and detailed explanation for every of the chosen proxies

are presented in Annex 1. Value/ turnover, volume per trade, turnover ratio, liquidity ratio,

Amihud measure, Martin liquidity index, Marsh & Rock liquidity ratio, Hui-Heubel liquidity

ratio, dispersion are reported as daily averages for every BVB traded T-bond.

These proxies can be split in two categories: a) simple proxies which comprise: active days,

value/ turnover, and volume per trade; they are either directly observable from the official

reports (value/ turnover) or simply extracted from the available data; usually these simple

proxies capture just one dimension of liquidity; and b) complex proxies which include: turnover

ratio, liquidity ratio, Amihud measure, Martin liquidity index, Marsh & Rock liquidity ratio, Hui-

Heubel liquidity ratio, dispersion, gamma, and Roll measure; their calculation need more

information derived from a combination of available data; complex proxies may capture a

combination of two of the liquidity dimensions.

Table 6 presents a brief synthesis of these twelve proxies’ characteristics.

Some of the proxies selected provide similar information. Thus, they were kept in this first study

in order to assess which one captures better the liquidity dimensions for the particular T-bond

segment at BVB.

Table 6: Proposed liquidity proxies’ characteristics

Liquidity proxy Liquidity dimension

captured

Type of proxy8

Level needed for

showing liquidity

Active days Indirectly: resilience &

immediacy9

Frequency based measure High

Value/ turnover Depth Volume based measure High

Volume per trade Depth Volume based measure High

Turnover ratio Depth Volume based measure High

Liquidity ratio Depth Volume based measure High

Amihud measure Resiliency (price

impact) and depth

Volume based measure Low

Martin liquidity index Tightness and depth Volume based measure Low

Marsh & Rock

liquidity ratio

Tightness and

resilience

Price based measure Low

Hui-Heubel liquidity

ratio

Depth and resiliency Price and volume based

measure

Low

Dispersion Tightness Price based measure Low

Gamma Tightness Price based measure Low

Roll measure Tightness Price based measure Low

Note: To mention from which source/ paper I took this classification

4.3. Findings regarding the liquidity factors and liquidity proxies for BVB T-bond market

segment

4.3.1. The liquidity factors

The general hypothesis verified in this section is: the identified liquidity factors have a combined

influence over each liquidity proxy considered.

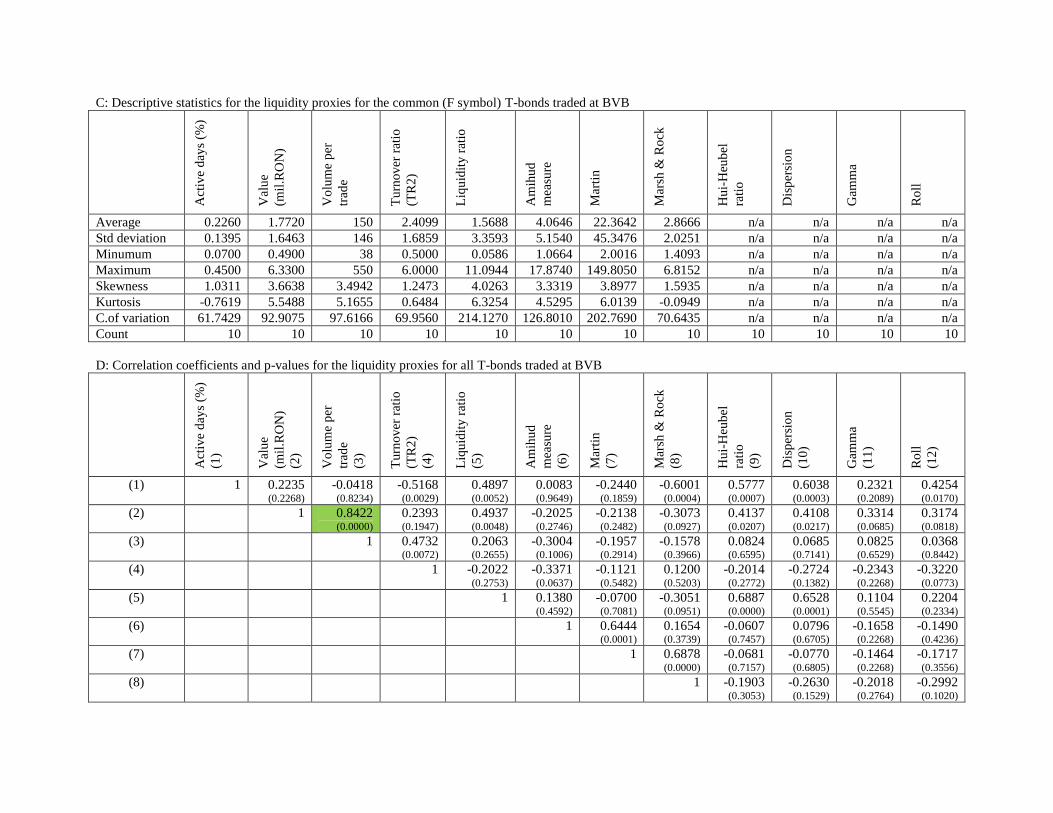

Annex 5 contains the descriptive statistics and the correlation matrices for the identified five

liquidity factors for the traded T-bonds.

The small number of observations provided data series far from normal distributions and with

high coefficients of variations. The closest to a normal distribution are the data series for

common bonds (F-symbol); since in all the common bond cases only 10 observations are

available, this situation is rather accidental. Moreover, the fifth factor – retail trading or R –

could not be calculated for common bonds since they registered only sporadic transactions, all

above 100 bonds per trade. The most important differences between benchmarks and common

bonds arise from a) the outstanding quantities, larger in the case of benchmarks; b) the coupon,

larger in the case of common bonds, since they were all issued in 2005 under the financing

conditions of that year; c) the time to maturity and listing period, longer for the common bonds,

and d) the retail trading, present only on the case of benchmarks. The data confirm the idea

expressed in paragraph 4.1. suggesting that the common bonds are rather treasured mainly in

institutional investors’ portfolios.

The correlations between coupon and outstanding quantities, moderate for all T-bonds and strong

for benchmark bonds, are generated by the way Romanian Ministry of Finance was issuing

8 Based on Schaeffer & Schmalz (2009), and Gabrielsen et al.(2011)

9 The frequency of trading measures, like the active days measure proposed here, can suggest the presence of

resilience and immediacy since the more frequent a T-bond is traded, the more likely the market can absorb random

shocks.

bonds: during 2008 and 2009 the increased financial needs triggered larger issues while the

borrowing costs increased under the global financial crisis influence; starting with 2010, the

borrowing costs decreased and, it seems, financial needs decreased also as the new issues’

dimensions indicate. These correlations might also be under the influence of the small number of

traded issues.

A moderate correlation can be also observed between the outstanding quantity and the listing

period for benchmark bonds. This correlation is generated by the same reason presented

previously: the largest listed and traded issues were introduced at BVB during 2008 and 2009.

The most interesting correlation for benchmark bonds is the moderate negative one between the

time to maturity and the retail trading, indicating that individual investors seem to prefer shorter

maturities when trading.

The moderate to strong correlations which occurred in the case of common bonds are under the

influence of Romanian Ministry of Finance decisions to issue T-bonds; thus, the small number of

observations also impairs the results accuracy.

Based on the reasons presented above, for all T-bonds and benchmark bonds all the five

identified factors were taken into consideration in order to test the general hypothesis. The

common bonds were eliminated form this test due to low correlation accuracy and by the fact

that four of the twelve proxies could not be calculated, as Annex 6 show.

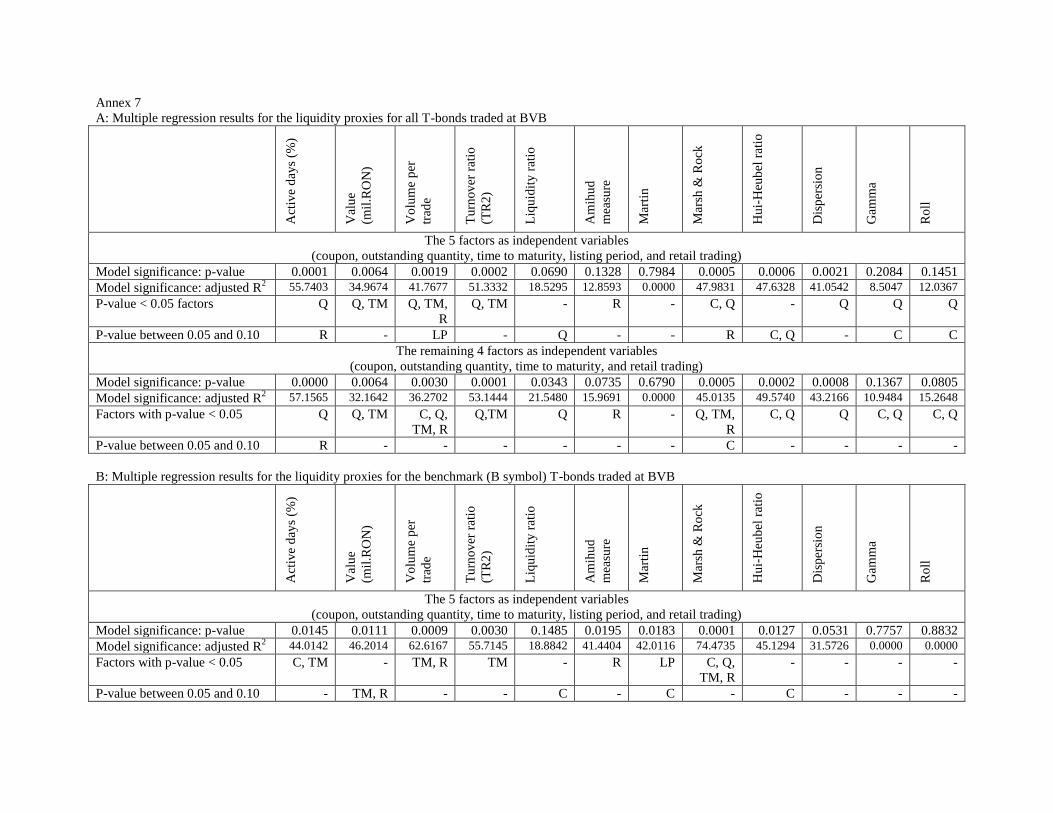

Further, the multiple regression was chosen in order to asses the influence of the considered

liquidity factors over the liquidity proxies. The general model used is:

n

1i

iii0 εXbbY (1)

Where:

Y represents the dependent variable

X represent the independent variables

b0 represents the constant

bi represent the estimates for the independent variables

εi represents the residuals.

The results were considered valid for a p-value of < 0.05, at a standard confidence level of 95%.

Every one of the twelve liquidity proxies that could be calculated was considered the dependent

variable, while the liquidity factors were the independent variables. The multiple regression

results are presented in Annex 7

For all traded T-bonds, the combination of the five identified factors explains about 35% or more

of seven proxies’ variability at a confidence level of 95%; in other three cases the combination

explains between 12% and 19% of the respective proxy variability at a confidence level of 85%

or more. Only one liquidity proxy, the Martin index, remained unexplained. Of the five factors,

the outstanding quantity is significant for 8 proxies at a confidence level of 95% and for 2

proxies at a confidence level between 90% and 95%. Coupon appears to have significance

mainly for the price related proxies, while time to maturity is significant for only three proxies.

The factor least significant is the listing period.

The significance of the outstanding quantity indicates that it plays an important role in the

trading decision, hence its importance and influence over liquidity proxies.

For the traded benchmark bonds (B-symbols), the five factor combination explains about 32% or

more of nine proxies’ variability at a confidence level of 95%; in one case it explains 18.9% of

the proxy variability at a confidence level of 85%. In two cases (Gamma and Roll, both price

related proxies) the five factors have no explanatory power. Time to maturity seems to become

the most significant factor at 95% confidence level, while the significance of coupon is lower, at

90% confidence level. As in the case of all traded T-bonds, the listing period seems to be the

least significant factor.

These multiple regression results indirectly confirm also the 1st, 4

th, and 5

th stylized facts at BVB.

Based on the findings presented above, the general hypothesis formulated at the beginning of

this paragraph can be accepted; for the majority of the considered liquidity proxies, the

combination of identified liquidity factors explains a satisfactory level of variability at a

confidence level of 95%.

However, the investigation was continued by eliminating the least significant factor of the five:

the listing period. The combination of the remaining four factors has an increased explanatory

power for all the traded T-bonds and for the traded benchmark bonds. The importance of

outstanding quantity in the case of all T-bonds and of time to maturity for benchmark bonds

remained unchanged.

The modified form of the general hypothesis is: a combination of four of the five identified

factors explains at an improved level the variability for the majority of the liquidity proxies at a

confidence level of 95%.

4.3.2 The liquidity proxies

The descriptive statistics for the twelve liquidity proxies are available in Annex 6 and in a brief

synthesis in Table 7. In most cases the values are far from a normal distribution and the

coefficient of variation tends to be high, due to wide value intervals.

Table 7: Average from descriptive statistics

Proxy All traded T-bonds Traded B symbols Traded F symbols

Active days 4.5623 6.6271 0.2260

Value/ turnover 3.7516 4.6943 1.7720

Volume per trade 236 277 150

Turnover ratio 1.3642 0.8662 2.4099

Liquidity ratio 93.9917 138.0030 1.5688

Amihud measure 5.1489 5.6652 4.0646

Martin liquidity index 12.4198 7.6844 22.3642

Marsh & Rock

liquidity ratio

1.3186 0.5815 2.8666

Hui-Heubel liquidity

ratio

*0.9878 1.4582 n/a

Dispersion *0.0001 0.0001 n/a

Gamma *0.0544 0.0804 n/a

Roll measure *0.2549 0.3763 n/a

Note*: The Hui-Heubel liquidity ratio, dispersion, gamma and Roll measure were considered zero for the common

(F-symbol) bonds when the average of respective measures was calculated for all traded T-bonds.

Since no previous paper measured the BVB T-bond segment liquidity, there is no benchmark for

the results presented above and the evaluation of the meaning of high and low is relative. Thus,

in combination with what was already revealed regarding BVB T-bond segment, the general

picture provided by the liquidity proxies show a relative low level of liquidity.

One set of proxies confirm this low liquidity. The trading frequency, measured by the number of

active days, is low; similarly low is the trading intensity, measured by daily value/ turnover,

volume per trade and turnover ratio. The Amihud measure indicates that the absolute return

varies 5 % for every daily million traded, which can be considered a relative high variation

indicating a low resilience, hence a low liquidity.

Another set of proxies seems to indicate a rather moderate level of liquidity; this set includes the

liquidity ratio, Hui-Heubel liquidity ratio, dispersion, and gamma and Roll measure. Thus, the

intimacy of available data should be considered when the significance of these proxies is

regarded. Hui-Heubel liquidity ratio and dispersion are based on the dispersion between the

maximum and minimum price registered. At daily level, often, this dispersion is zero for BVB

traded T-bonds; this situation is generated by the low trading frequency and the low number of

investors in the T-bond market. Both ratios rather show the relative lack of investors’ interest

toward the T-bond segment rather than a moderate level of liquidity. Gamma and Roll measure

are based on the negative correlation of only 12 benchmark traded bonds; for all traded T-bonds

this number represent less than half, while for the benchmark bonds it is close to 60%. Thus,

when combined with other information available, the relative moderate liquidity that seems to be

depicted by these four proxies should be rather ignored. Only the liquidity ratio level remains,

for now, unexplained and needs further investigation. Thus, since the other volume based proxies

indicate a relative low level of liquidity, the information offered by the liquidity ratio should be

adapted to the general picture resulted by combining all the information available.

Also from Table 7 it can be observed that in most cases the calculated proxies indicate that the

benchmark (B-symbol) bonds are more liquid that the common (F-symbol) bonds. Thus, two

proxies: the turnover ratio and Amihud measure point that the common bonds are more liquid. In

the case of turnover ration this somewhat distorted information is generated by the fact that the

outstanding quantity of these bond is low (see Graph 4 and Annex 2) and, while seldom traded,

the traded quantity had the tendency to represent a higher percentage of the outstanding volume

than in the case of benchmark bonds. In the case of Amihud measure, the distortion in

information comes from the fact that, thus seldom traded, the common (F-symbol) bonds prices

varied less than the benchmark bond prices.

Based on the combined information available, the proxies indicate a low level of liquidity for

the BVB T-bond market segment. The liquidity is slightly higher for the benchmark bonds,

while for the common bonds the liquidity can be considered very low.

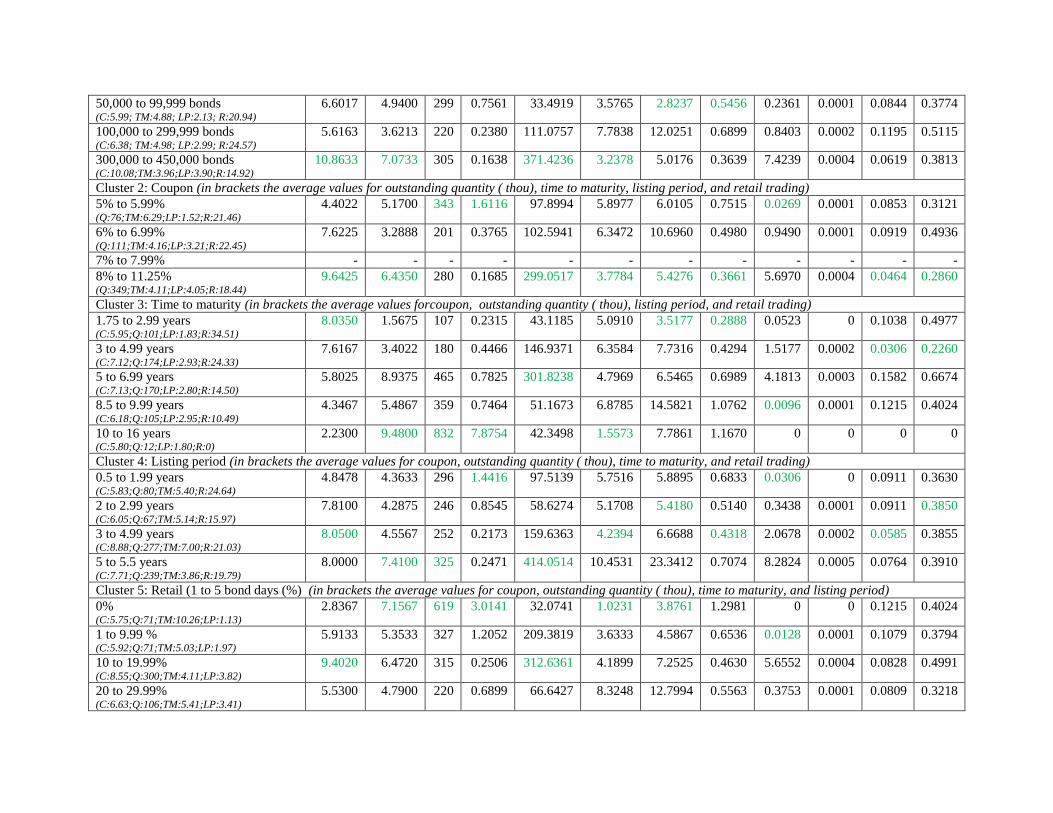

Annex 8 presents the proxies grouped by clusters. The T-bonds were grouped using the five

identified factors as reference in order to enhance their explanatory power. From Annex 8 (A and

B) it is obvious that the most liquid (benchmark) T-bonds are those with the larger outstanding

quantity, highest coupon, a listing of over 3 years, and which registered less than 20% retail

trading. The decrease in turnover ratio as the outstanding quantity increases only confirms the

low level of trading activity, hence the general low level of liquidity of BVB T-bond market

segment. The mix results for time to maturity cluster indicate that other reasons (factors) have a

stronger influence over the decision to trade. For the common bonds (F-symbol), the results even

by clusters do not reveal a clear pattern for liquidity; this situation arises from the very low

trading frequency for this T-bond group and reveals insolated decisions of institutional investors

to sell/ buy the respective common bonds.

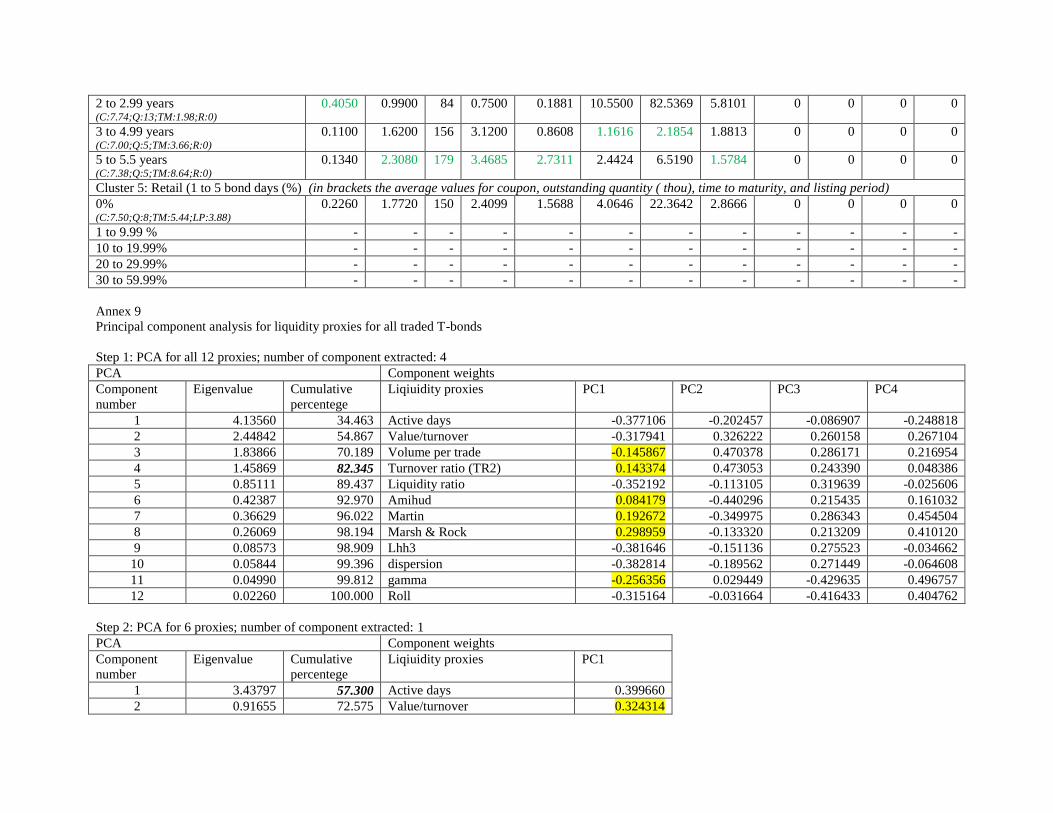

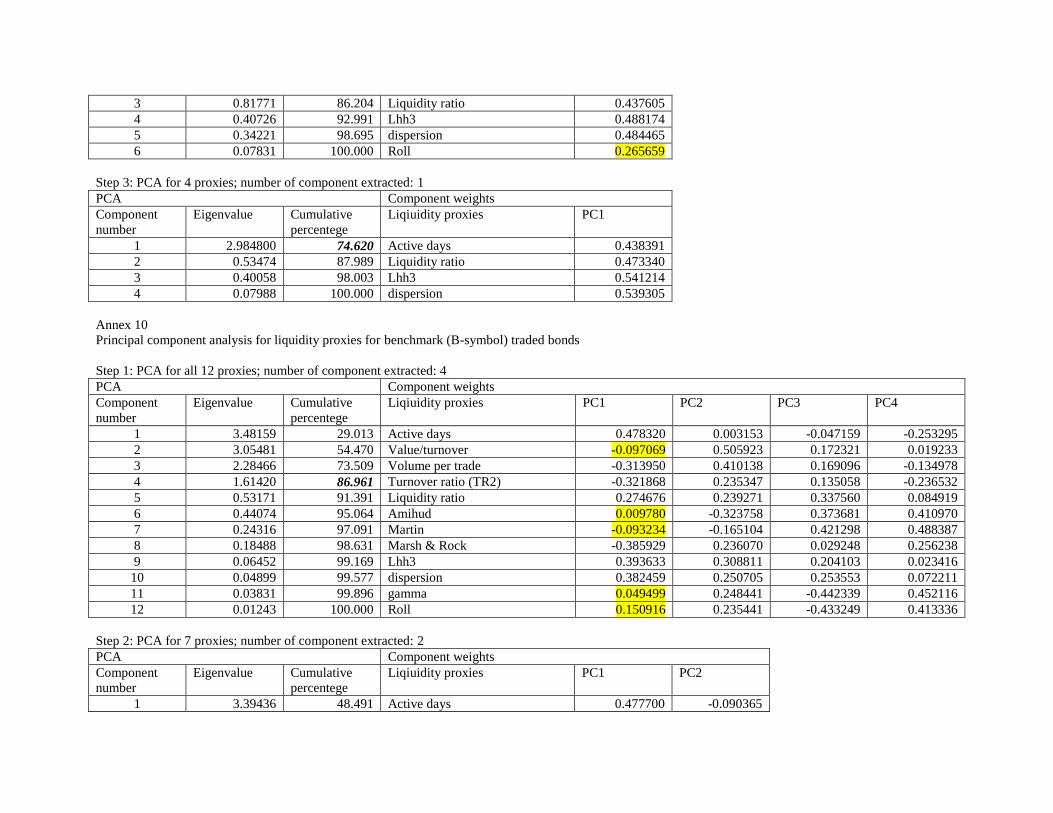

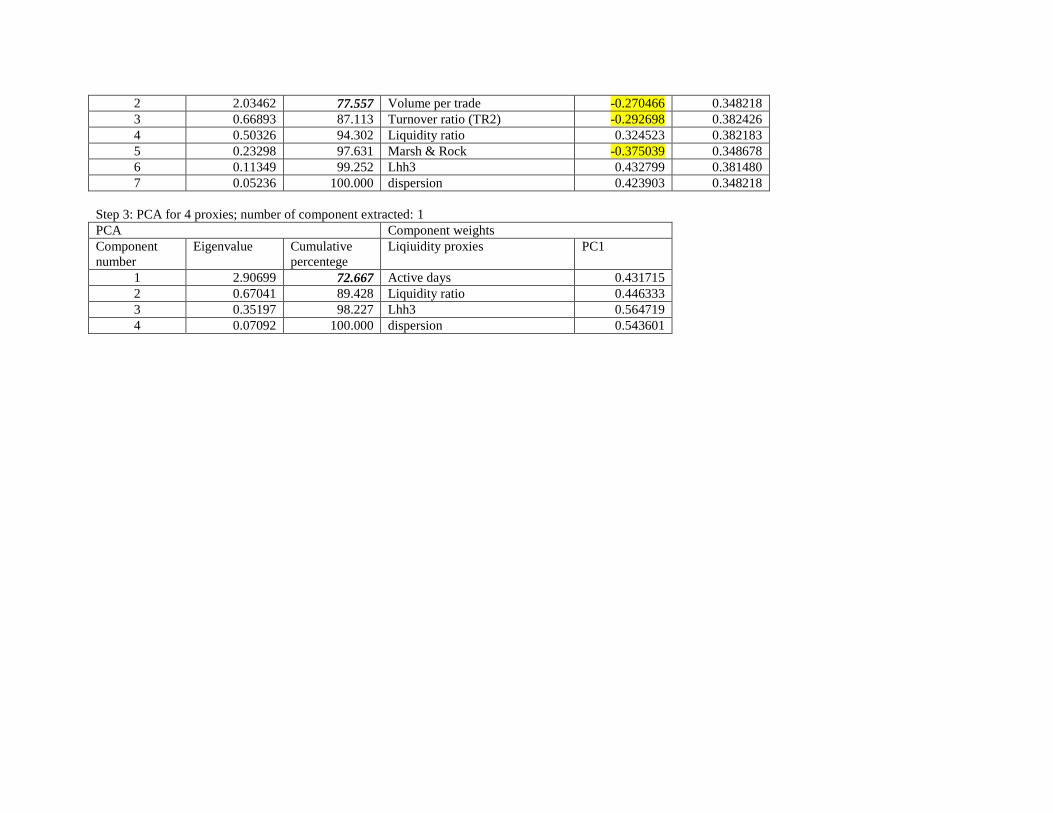

4.3.3. Principal-Component Analysis

The twelve liquidity proxies calculated in for BVB T-bond sector are too many and in some

cases they describe the same liquidity dimension(s), as presented in Table 6. In other cases, they

exhibit moderate to strong significant correlations, as Annex 6 show. A Principal-Component

Analysis (PCA) was conducted in order to extract a smaller number a proxies that capture the

BVB T-bond sector liquidity, while retaining as much as possible of the variation in the original

set of proxies. Since the measures for the twelve proxies are different and of different scale, the

Principal Components (PCs) were extracted from the correlation matrix.

PCA was performed in three steps. First, PCA was conducted for all the twelve proxies and four

PCs resulted, as presented in Annexes 9 and 10. These four PCs capture 82.35% of the original

proxies’ variation. The result is to be expected since no proxy was eliminated.

Further, the loading of PC1 was considered and all the components with a weight lower than 0.3,

in absolute value, were eliminated. In the case of all T-bonds, the remaining six proxies

generated just one PC which captures 57.3% of the original variation. For benchmark bonds, the

remaining seven proxies generated two PCs resulted, capturing 77.56% of the original variation.

The results seem satisfactory. Thus, a closer look at the six proxies’ PC1 loading for all T-bonds

revealed that four proxies have a weight closer or higher than 0.4. Hence, two more proxies with

a loading less than 0.39 were eliminated and the remaining four proxies were combined in one

PC which captures 74.62% of the original variation. In the case of benchmark bonds, the

remaining seven proxies, within the two PCs, were considered too many. While the PC1 loading

rather suggest the elimination of liquidity ratio instead of Marsh & Rock10

, it was chosen to test

the explanatory power of the same four proxies that were extracted at all T-bond level. The

combination of these four proxies captures a satisfactory 72.67% of the original variation11

.

Based on these results, the following four proxies satisfactory capture the various liquidity

dimensions for all BVB traded T-bonds and benchmark bonds: i) active days – based on

frequency which indirect describes resiliency and immediacy, ii) liquidity ratio which is seizing

depth, iii) Hui-Heubel ratio capturing depth and resiliency, and iv) dispersion capturing

tightness. The four proxies indicate a moderate to low liquidity for T-bond market segment at

BVB, dominated by benchmark bonds.

All four proxies are significantly influenced by the 4 remaining factors identified to influence

liquidity, respectively: outstanding quantity, coupon, time to maturity and the retail trading. For

all T-bonds and for benchmark bonds only, the multiple regression models are significant and

explain between 21% and 57% of the respective proxies’ variance (Annex 7).

10

If the liquidity ratio was eliminated and the four remaining proxies were: active days, Marsh & Rock, Hui-Heubel

ratio and dispersion, their combination results in two PCs seize 93.83% of the initial variation. Thus, it was tested

further if a combination of other four proxies can generate only one PC and the result presented in Annex 10

emerged. 11

A closer look at the PC1 loading in Annex 10 step 2 indicates, in fact, the necessity of eliminating both liquidity

ratio and Marsh & Rock. In this case, the three remaining proxies generate one PC that seizes 81.17% of the

original variation. Thus, the depth is only marginally described by the combination of the three remaining proxies

(active days, Hui-Heubel ratio, and dispersion). Based on this fact it the combination of the four proxies presented in

text was chosen.

These combined results indicate that liquidity as measured by the four proxies can be improved

if the Romanian government authorities will pay more attention to the four factors highlighted

above.

5. Conclusions

Within the present paper several aspects of T-bond segment liquidity within a frontier security

market, Bucharest Stock Exchange (BVB), were under scrutiny. The general presentation of

BVB government bond segment permitted a first glance of a low liquidity. Further, the holding

of six stylized facts regarding liquidity was investigated. The results showed that while three

stylized facts could be confirmed, at general level, other two were rejected and one only partially

confirmed. An in-depth look at the causes revealed that the benchmark feature for the traded

bonds is superficially understood by the bonds’ issuer, the Romanian Ministry of Finance, and no

concentration on specific maturity buckets can be found. This situation had a direct influence

over on/off the run feature which can not be confirmed even in a modified form. Moreover, the

three confirmed stylized facts should be considered under the peculiarities of T-bond segment at

BVB.

Since this is the first paper trying to measure the liquidity of BVB government bond market

segment, a high number of proxies were first selected in order to capture all the liquidity

dimensions. Also five factors were identified to influence the majority of these proxies. In the

end, four factors of the initial five proved to have an increased explanatory power over the

liquidity proxies. Further, the number of twelve liquidity proxies should be reduced and a PCA

was conducted in order to extract a smaller number. The final result indicates a number of four

liquidity proxies that captured in a satisfactory manner all the liquidity dimensions. One is a

simple proxy, directly observable, the other three are complex proxies. The data regarding these

four proxies indicate a low to moderate liquidity for the BVB government bond market segment

currently dominated by the trading of the benchmark bonds. The four proxies are under the

combined influence of four factors in the following order of importance: outstanding quantity,

time to maturity, coupon and retail trading. This suggests that the Romanian Ministry of Finance

should pay a special attention to these factors in order to increase the government bond segment

liquidity at BVB.

This finding is confirmed by suggestions of McCauley & Remolona (2000) and Daniel (2008).

Also, a previous general survey of the Romanian government bond market by Pop & Georgescu

(2012) suggested also the need of an increased issue size for the traded government bonds and

their availability for retail investors. A timid step was made by Romanian Ministry of Finance

during 2014 when it announced its intention to launch, through public offer, several issues with a