Inventory Management Chapter 13 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Inventory Management Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Inventory Management

Chapter 13

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

13-2

You should be able to:LO 13.1 Define the term inventoryLO 13.2 List the different types of inventoryLO 13.3 Describe the main functions of inventory LO 13.4 Discuss the main requirements for effective managementLO 13.5 Explain periodic and perpetual review systemsLO 13.6 Describe the costs that are relevant for inventory managementLO 13.7 Describe the A-B-C approach and explain how it is usefulLO 13.8 Describe the basic EOQ model and its assumptions and solve typical

problemsLO 13.9 Describe the economic production quantity model and solve typical

problemsLO 13.10 Describe the quantity discount model and solve typical problemsLO 13.11 Describe reorder point models and solve typical problemsLO 13.12 Describe situations in which the fixed-order interval model is

appropriate and solve typical problemsLO 13.12 Describe situations in which the single-period model is

appropriate, and solve typical problems

Chapter 13: Learning Objectives

13-3

InventoryA stock or store of goods

Independent demand itemsItems that are ready to be sold or used

Inventory

Inventories are a vital part of business: (1) necessary for operations and (2) contribute to customer satisfaction

A “typical” firm has roughly 30% of its current assets and as much as 90% of its working capital invested in inventory

LO 13.1

13-4

Inventories serve a number of functions such as:1. To meet anticipated customer demand2. To smooth production requirements3. To decouple operations4. To protect against stockouts5. To take advantage of order cycles6. To hedge against price increases7. To permit operations8. To take advantage of quantity discounts

Inventory Functions

LO 13.3

13-5

Inventory management has two main concerns:1. Level of customer service

Having the right goods available in the right quantity in the right place at the right time

2. Costs of ordering and carrying inventories The overall objective of inventory management is to

achieve satisfactory levels of customer service while keeping inventory costs within reasonable bounds1.Measures of performance2. Customer satisfaction

Number and quantity of backorders Customer complaints

3. Inventory turnover

Objectives of Inventory Control

LO 13.3

13-6

Requires:1. A system keep track of inventory2. A reliable forecast of demand3. Knowledge of lead time and lead time variability4. Reasonable estimates of

holding costs ordering costs shortage costs

5. A classification system for inventory items

Effective Inventory Management

LO 13.4

13-7

Periodic SystemPhysical count of items in inventory made at

periodic intervalsPerpetual Inventory System

System that keeps track of removals from inventory continuously, thus monitoring current levels of each itemAn order is placed when inventory drops to a

predetermined minimum levelTwo-bin system

Two containers of inventory; reorder when the first is empty

Inventory Counting Systems

LO 13.5

13-8

Purchase costThe amount paid to buy the inventory

Holding (carrying) costsCost to carry an item in inventory for a length of time,

usually a yearOrdering costs

Costs of ordering and receiving inventorySetup costs

The costs involved in preparing equipment for a jobAnalogous to ordering costs

Shortage costsCosts resulting when demand exceeds the supply of

inventory; often unrealized profit per unit

Inventory Costs

LO 13.6

13-9

A-B-C approach Classifying inventory according to some measure of

importance, and allocating control efforts accordingly A items (very important)

10 to 20 percent of the number of items in inventory and about 60 to 70 percent of the annual dollar value

B items (moderately important) C items (least important)

50 to 60 percent of the number of items in inventory but only about 10 to 15 percent of the annual dollar value

ABC Classification System

LO 13.7

13-10

How Much to Order: EOQ ModelsEconomic order quantity models identify the

optimal order quantity by minimizing the sum of annual costs that vary with order size and frequency1. The basic economic order quantity model2. The economic production quantity model3. The quantity discount model

LO 13.8

13-11

The basic EOQ model is used to find a fixed order quantity that will minimize total annual inventory costs

Assumptions:1. Only one product is involved

2. Annual demand requirements are known

3. Demand is even throughout the year

4. Lead time does not vary

5. Each order is received in a single delivery

6. There are no quantity discounts

Basic EOQ Model

LO 13.8

13-12

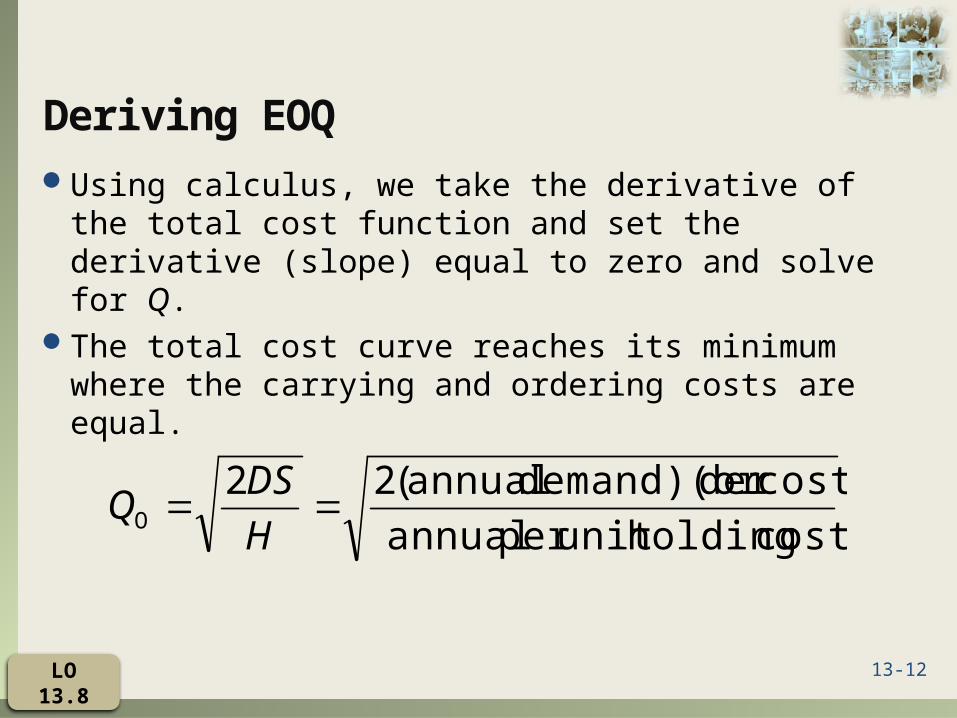

Using calculus, we take the derivative of the total cost function and set the derivative (slope) equal to zero and solve for Q.

The total cost curve reaches its minimum where the carrying and ordering costs are equal.

Deriving EOQ

cost holdingunit per annual

cost)der demand)(or annual(22O

H

DSQ

LO 13.8

13-13

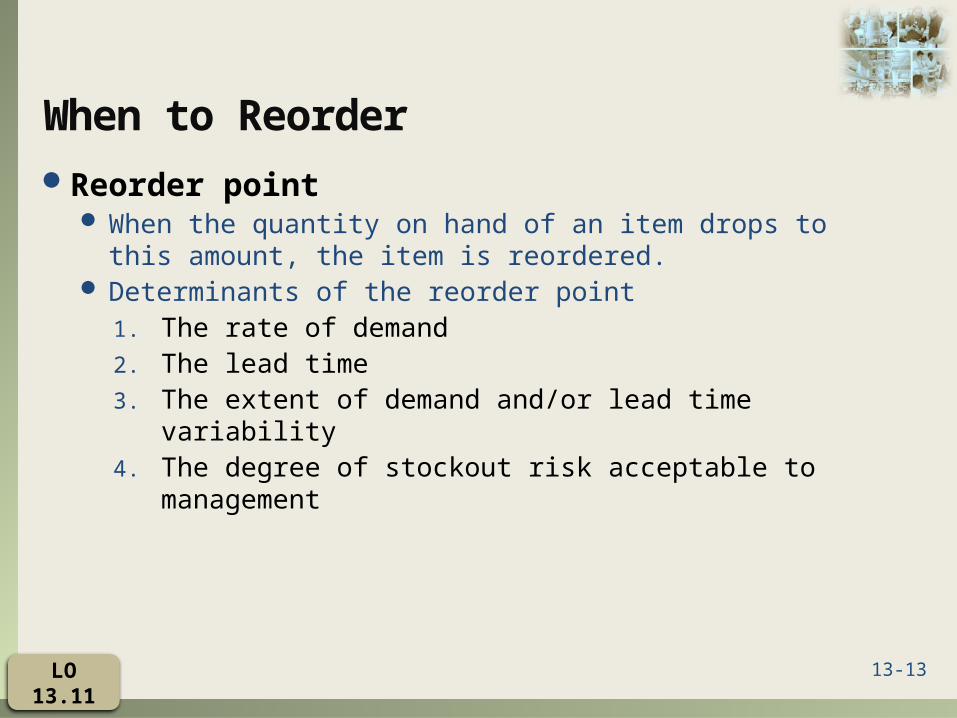

When to ReorderReorder point

When the quantity on hand of an item drops to this amount, the item is reordered.

Determinants of the reorder point1. The rate of demand2. The lead time3. The extent of demand and/or lead time variability4. The degree of stockout risk acceptable to

management

LO 13.11

13-14

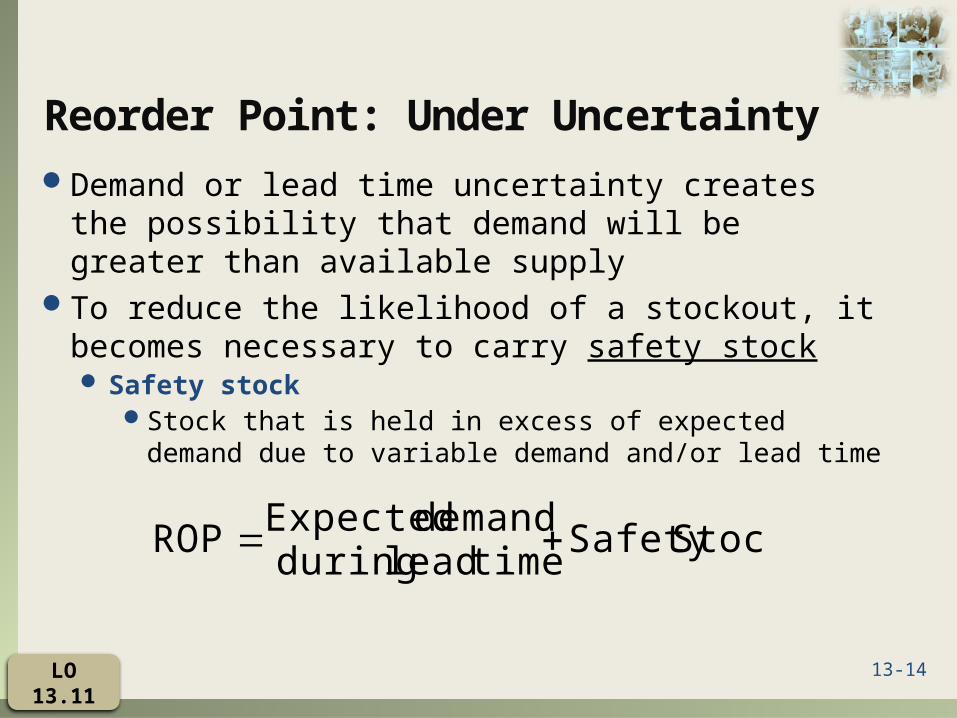

Demand or lead time uncertainty creates the possibility that demand will be greater than available supply

To reduce the likelihood of a stockout, it becomes necessary to carry safety stock Safety stock

Stock that is held in excess of expected demand due to variable demand and/or lead time

Reorder Point: Under Uncertainty

StockSafety timelead during

demand Expected ROP

LO 13.11

13-15

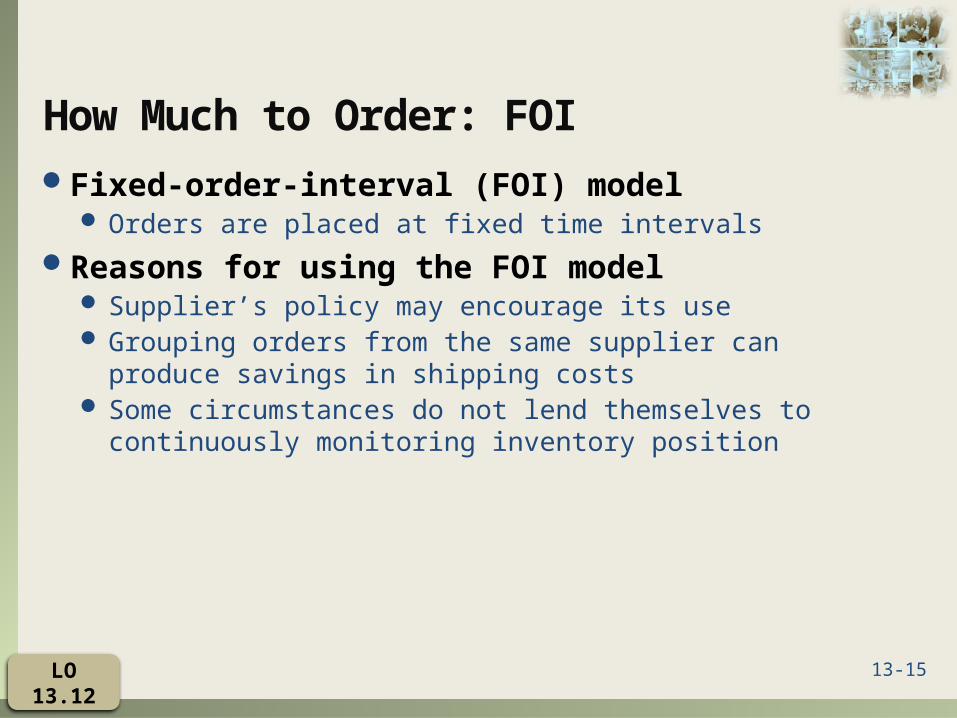

Fixed-order-interval (FOI) model Orders are placed at fixed time intervals

Reasons for using the FOI model Supplier’s policy may encourage its use Grouping orders from the same supplier can produce

savings in shipping costs Some circumstances do not lend themselves to

continuously monitoring inventory position

How Much to Order: FOI

LO 13.12

Related Documents