INVENTORY MANAGEMENT Presented by: Ram babu Amit Kumar Ankit sharma

Inventory management

Jul 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INVENTORY MANAGEMENT

Presented by: Ram babuAmit KumarAnkit sharma

In dictionary meaning of inventory is a “detailed list of goods, furniture etc.” Many understand the word inventory, as a stock of goods, but the generally accepted meaning of the word ‘goods’ in the accounting language, is the stock of finished goods only. In a manufacturing organization, however, in addition to the stock of finished goods, there will be stock of partly finished goods, raw materials and stores. The collective name of these entire items is ‘inventory’.

Inventory is material that the firm obtains in advance of need, holds until it is needed, and then used, consumes, incorporates into a product, sells, or otherwise disposes it of. A business inventory is temporary in nature.

Inventories are stock of any kind like fuel and lubricants, spare parts and semi-processed materials to be stored for future use mainly in the process of production or it can be known as the ideal resource of any kind having some economic values.

Independent Demand

A

B(4) C(2)

D(2) E(1) D(3) F(2)

Dependent Demand

Independent demand is uncertain. Dependent demand is certain.

Inventory

Inventory management supervises the flow of goods from manufacturers to warehouses and from these facilities to point of sale. A key function of Inventory management is to keep a detailed record of each new or returned product as it enters or leaves a warehouse or point of sale

The primary objectives of inventory management are:

To minimize the possibility of disruption in the production schedule of a firm for want of raw material, stock and spares.

maintain sufficient stock of raw material in the period of short supply and anticipate price changes.

ensure a continuous supply of material to production department facilitating uninterrupted production.

minimize the carrying cost and time.

+maintain sufficient stock of finished goods for smooth sales operations.

• ensure that materials are available for use in production and production services as and when required.

• ensure that finished goods are available for delivery to customers to fulfill orders, smooth sales operation and efficient customer service.

• minimize investment in inventories and minimize the carrying cost and time.

• protect the inventory against deterioration, obsolescence and unauthorized use.

• maintain sufficient stock of raw material in period of short supply and anticipate price changes.

Functions of inventory management

To meet anticipated customer demand (to meet the anticipated stocks, average demand)

To smooth production requirements (create seasonal inventories to meet seasonal demand).

To decouple operations (eliminate sources of disruptions).To protect against stock outs (hold safety stocks to prevent

the risk of shortages)To take advantages order cycle (buys more quantities then

immediate requirements –cycle stock, periodic orders or order cycles).

To hedge against price increases (purchase larger order to hedge future price increase or implement volume discount).

To take advantage of quantity discount( supplies may give discount on large orders).

1.Direct inventories: The inventories which play a direct role in the manufacture of a product and become an integral part of the finished product are called direct inventories. Direct inventories are classified as:

(a) Raw materials: theses are the materials which are machined or before they are ready to be used in assembly of the finished products. They include items like steel, copper, tin,lead,cotton,rubber,forgins,leather,wood.

(b) Work in progress: in this process inventories are the semi finished goods at various stages of manufacture. The output of one machine is fed to another machine for further processing. Raw materials becomes work in progress at the end of first operation and remain in that classification until they become piece parts or finish goods. Work in progress can be found on the conveyors, pallets in and around the machine and in temporary storage and waiting for the next operations.

(c) purchased parts: these are some purchased items.(components, sub assemblies, finished parts etc.),purchased from outside suppliers instead of manufacturing in the factory itself. For example, ball bearings,screws,nuts,bolts,tyres required in automobile industries.

(d) Finished goods: finished goods inventories contain the output the production process. These are the finished (final) products ready for dispatching to the customer products usually leave work in progress classification and enter in the classification of finished goods at the point of final inspection they are ready for delivery to the customers or to finished goods store.

2.Indirect inventories: are those materials which help the raw materials to get converted into the finished product, but do not become an integral part of the finished products. Indirect inventories are further classified as:

(a) Tools: various tools used for processing are classified as:(i)Standard tools used on machines such as lathe tools, milling

cutters,drill,reamers taps,hobs,broaches,chasers,form tool etc.(ii)Hand tools such as hand saws,chisels,drill

guns,hammers,mallets,pliers,spanners,wrenches,punches etc.

(b) Supplies: it includes materials used in running the plant but do not go into the product. Supplies include:

(i)miscellaneous consumable stores such as brooms, cottons waste, toilet paper, vim powder, jute etc.

(ii) welding, soldering, and tinning materials such as electrodes,welding rods,

solder,spelter etc..(iii)abrasive materials such as emery cloth,emery belts, and paper emery,

graphite etc.

(iv) empties such as bags ,glass, bottles, card board boxes, drums jarstins etc.

CLASSIFICATION OF INVENTORIESCOST:

Inventories’ cost are traditionally categorized into four basic types:

Purchase cost:

For items that are purchased from outside the firms, this is usually the unit price that the firm pays to its vendor. As an item moves through the logistics system of the firms, it purchase cost in the inventory analysis should reflect its fully landed cost, by which is meant the cost to acquire and moves the item to that point in the system.

ORDERING COST:

In addition to the per unit purchase cost, there is usually an additional cost which is incurred whenever we order, reorder or replenish the inventory. If we produce items internally then there will be an organization set up cost. This happens because we have to shut down the manufacturing line and change over, reconfigure the line to make a specific item. This is the cost involved with processing the order, involving paying the bill, auditing, and so forth.

HOLDING COST:

The cost that accrue due to the actual holding of the inventory over a time period. Many different kinds of cost can be considered as holding cost. The key characteristics of holding cost varies with the amount of inventory being held and the time that the inventory is held. The holding cost can further be classified as follows:

• Storage cost• Service cost• Risk cost •Capital cost.

SHORTAGE COST:

When a demand arises which cannot be satisfied from available inventory an inventory shortage occurs. Purchase, ordering and holding cost can be thought of as the cost of having inventories, while shortage cost result for not having inventory, or for not having enough inventory at the right place at the right time

Four specific case where shortage cost may exist are:

Back orders

Lost sales

Lost customer cost

Disruption cost

Inventory control:

Inventory control is the means by which materials of the correct quality and in correct quantity are made available as and when required with due regard to economic in storage and ordering cost. Hear the desired level of inventory can neither be high or low because high level inventory will lead to increase in carrying cost while low level of inventory will lead to increase in ordering cost

• To ensure smooth flow of stock.

• To provide for required quality of materials.

• To control investments in stock.

• Protection against fluctuating demand.

• Protection against fluctuations in output.

• Minimization of risk and uncertainty.

• Risk of obsolescence.

• Minimization of material cost.

Economic order quantity

Inventory level

Perpetual inventory control

ABC system of control

Inventory turnover ratio

We want to determine the optimal number of units to order so that we minimize the total cost associated with the purchase, delivery and storage of the product.

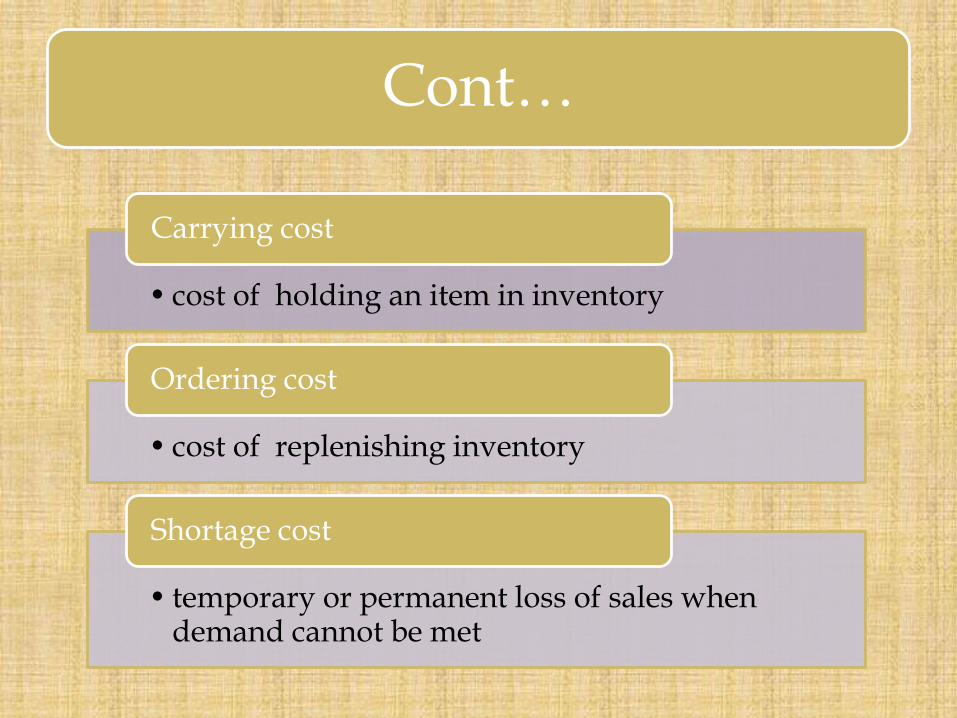

Cont…

• cost of holding an item in inventory

Carrying cost

• cost of replenishing inventory

Ordering cost

• temporary or permanent loss of sales when demand cannot be met

Shortage cost

E.O.Q = √(2*UP)/C OR =√2RCp/CH = √2AS/I

E.O.Q=Economic order quantity

U or A or= annual usage in unit

P or Cp or S = cost of placing an order

Ch or C or I = cost of storage of one unit in inventory for one year.

Re order level

Reorder level= maximum usage*maximum reorder period

Or RL=minimum level +(normal usage*normal delivery time)

Minimum stock level

MSL=reorder level – (normal usage)*normal delivery time

Maximum stock level

MSL= reorder level + reorder quantity(minimum usage )*minimum delivery time

Average stock level

ASL=(minimum level +maximum level)/2

It is implies maintenance of up to date stock records and in its board sense it covers both continuous stock tacking as well as up to date recording of stores books

Divides inventory into three classes based on Consumption Value

Consumption Value = (Unit price of an item) (No. of units consumed per annum)

Class A - High Consumption Value

Class B - Medium Consumption Value

Class C - Low Consumption Value

ABC Classification System

Classifying inventory according to some measure of importance and allocating control efforts accordingly.

A - very important

B - mod. important

C - least important

According to this approach to inventory control high value items are more closely controlled than low value items. Each item of inventory is given A, B or C denomination depending upon the amount spent for that particular item. “A”

or the highest value items should be under the tight control and under responsibility of the most experienced personnel, while “C” or the lowest value may be under simple physical control. It may also be clear with the help of the following examples:

“A” Category – 5% to 10% of the items represent 70% to 75% of the money value. “B” Category – 15% to 20% of the items represent 15% to 20% of the money. “C” Category – The remaining number of the items represent 5% to 10% of the money value. The

Advantages of ABC Analysis

1. It ensures a closer and a more strict control over such items, which are having a sizable investment in there. 2. It releases working capital, which would otherwise have been locked up for a more profitable channel of investment. 3. It reduces inventory-carrying cost. 4. It enables the relaxation of control for the ‘C’ items and thus makes it possible for a sufficient buffer stock to be created. 5. It enables the maintenance of high inventory turn over rate.

ITR= cost of goods sold /average inventory

cost of goods sold = sales –gross profit

average stock = (opening stock+closeing stock)/2

THANK YOU

Related Documents