Inventory and Accounting for Merchandisers Module 6

Inventory and Accounting for Merchandisers Module 6.

Jan 02, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Inventory and Accounting for Merchandisers

Module 6

SAP 2007 / SAP University Alliances Introductory Accounting

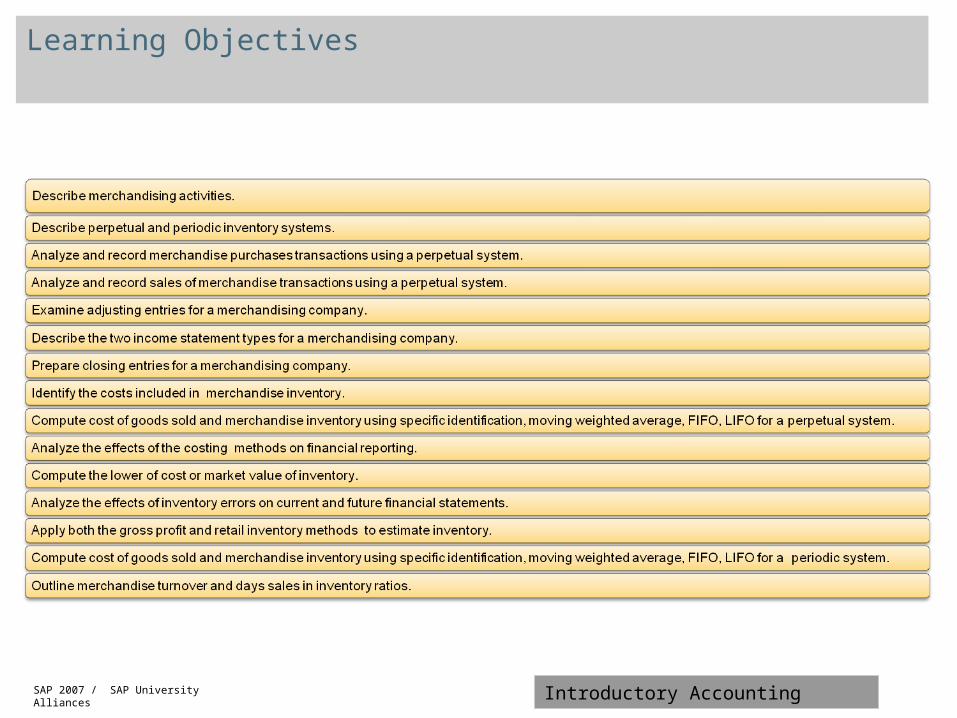

Learning Objectives

SAP 2007 / SAP University Alliances Introductory Accounting

Merchandising Activities

SAP 2007 / SAP University Alliances Introductory Accounting

Computing Net Income

Net Sales

Cost of Goods Sold

Gross Profit

Operating Expenses

Net Income Net Income

Operating Expenses

Revenue

Merchandiser Service Company

SAP 2007 / SAP University Alliances Introductory Accounting

Inventory

SAP 2007 / SAP University Alliances Introductory Accounting

Inventory

SAP 2007 / SAP University Alliances Introductory Accounting

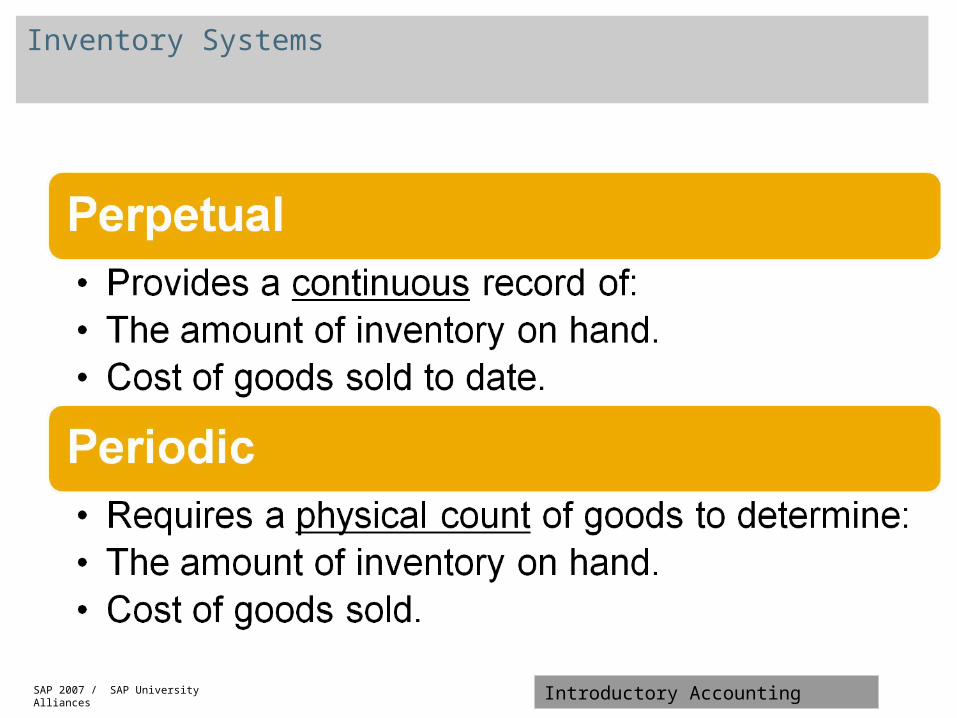

Inventory Systems

SAP 2007 / SAP University Alliances Introductory Accounting

May. 1 Inventory 66,000 Accounts Payable 6,000 Purchased inventory on account

May. 4 Accounts Payable 2,000 Inventory 2,000

Defective merchandise returned to supplier.

Purchases

Purchase Returns and Allowances

Perpetual System-Example

SAP 2007 / SAP University Alliances Introductory Accounting

Terms

Time

Due

Discount Period = 10 days

(Full amount minus 2% discount) due between

May.1 and May.11

Credit Period = 30 days

Full amount due anytime between

Mayt.12 and May.31

Purchase or Sale

May.1 May.11 May.31

Purchase/Sales Discounts

SAP 2007 / SAP University Alliances Introductory Accounting

Purchase Discounts- Assume the purchase of inventory on May 1 was on the terms 2/10,n30.

Case 1-Discount takenMay.11 Accounts Payable 644,000 Inventory 80 Cash 3,920 2% x (6,000 - 2,000) = 80 Case 2-Discount not taken Oct.31 Accounts Payable 4,000 Cash 4,000

Perpetual System — Example

SAP 2007 / SAP University Alliances Introductory Accounting

FOB Shipping Point(Buyer pays

shipping charges)

FOB Destination(Seller pays for

shipping charges)

Goods

Seller Buyer

Carrier

Transportation Charges — Perpetual System

SAP 2007 / SAP University Alliances Introductory Accounting

Transportation Charges

May. 2 Inventory 100 Accounts Payable 100

Transportation charges on goods purchased FOB shipping point.

Perpetual System — Example

SAP 2007 / SAP University Alliances Introductory Accounting

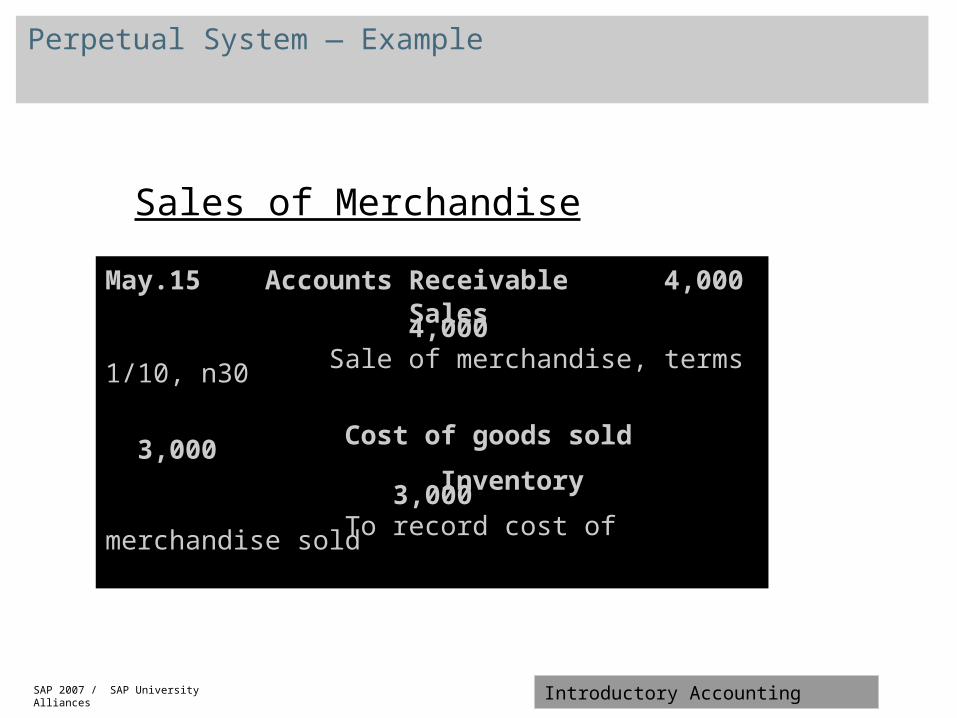

Sales of Merchandise

May.15 Accounts Receivable 4,000 Sales 4,000 Sale of merchandise, terms 1/10, n30

Cost of goods sold 3,000 Inventory 3,000 To record cost of merchandise sold

Perpetual System — Example

SAP 2007 / SAP University Alliances Introductory Accounting

Sales Returns and Allowances

Msy.17 Sales Returns & Allowance 400 Accounts Receivable 400 Defective merchandise returned

Inventory 300 Cost of Goods Sold 300 To record return of inventory

Perpetual System — Example

SAP 2007 / SAP University Alliances Introductory Accounting

Sales Discounts

Case 1- Discount taken

Perpetual System — Example

May.25 Cash 3,564 Sales Discounts 36 Accounts Receivable 3,600

1% X (4,000 - 400) = 36

Case 2- Discount not takenMay.25 Cash 3,600 Accounts Receivable 3,600

(4,000- 400)

SAP 2007 / SAP University Alliances Introductory Accounting

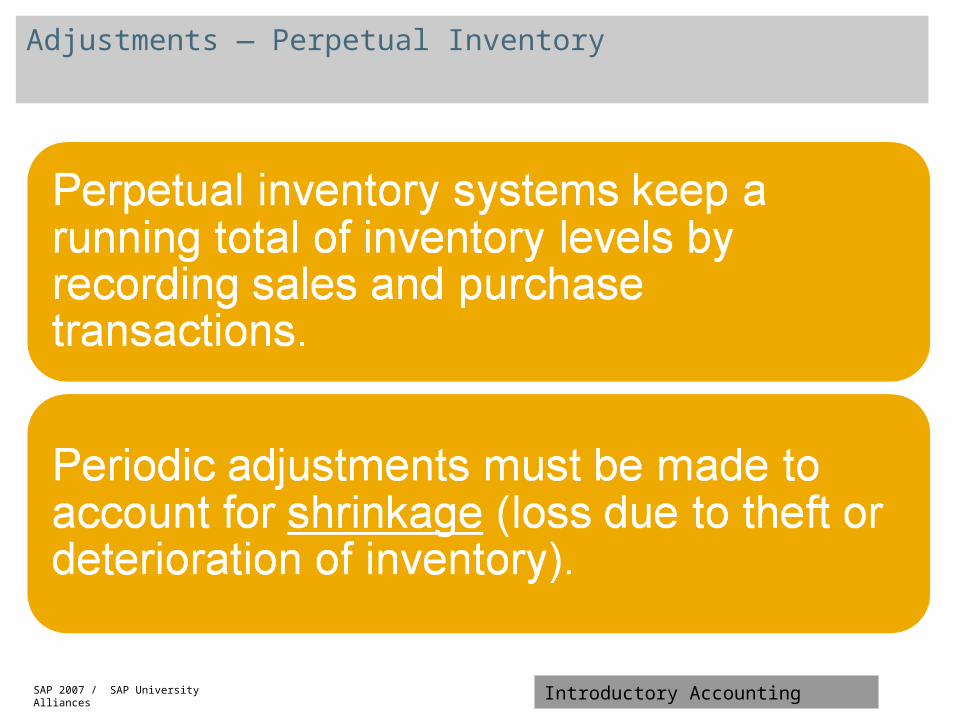

Adjustments — Perpetual Inventory

SAP 2007 / SAP University Alliances Introductory Accounting

Inventory per accounting records: $187,000

Inventory per physical count: $184,200

Difference (shrinkage) $2,800

Adjustment required:

Perpetual System — Example

May.31 Cost of Goods Sold 2,800 Inventory 2,800

To record inventory shrinkage revealed by physical count.

SAP 2007 / SAP University Alliances Introductory Accounting

Income Statement Formats

SAP 2007 / SAP University Alliances Introductory Accounting

Sales 335,000$ Less: Sales discounts 4,250$

Sales returns and allowances 2,200 6,450 Net sales 328,550 Cost of goods sold 233,200 Gross profit 95,350 Operating expenses: Selling expenses:

Amortization expense, store 2,800$ Sales salaries expense 19,200 Rent expense 8,500 Store supplies expense 950 Advertising expense 12,600 44,050

General and administrative expenses:Amortization expense, office 800 Office salaries expense 26,500 Insurance expense 500 Rent expense 850 Office supplies 1,950 30,600

Total operating expenses 74,650 Income from operations 20,700 Other revenues and expenses:

Rent revenue 2,000 Interest expense (250) 1,750

Net income 22,450$

Samle CoIncome Statement

For Year Ended December 31, 2005Classified Multi-step

Format

SAP 2007 / SAP University Alliances Introductory Accounting

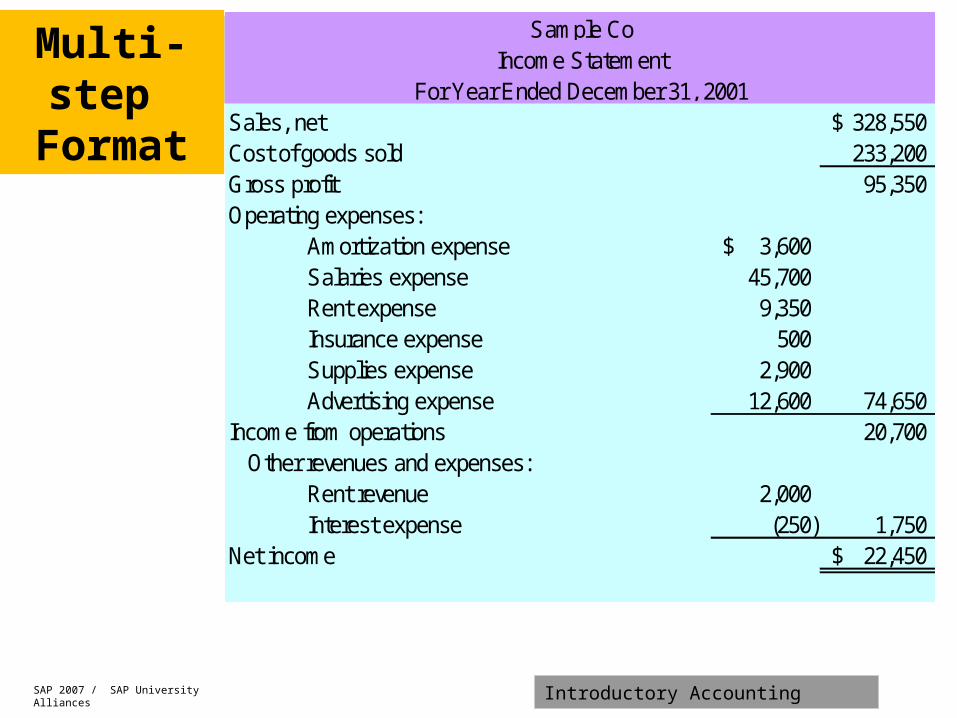

Sales, net 328,550$ Cost of goods sold 233,200 Gross profit 95,350 Operating expenses:

Amortization expense 3,600$ Salaries expense 45,700 Rent expense 9,350 Insurance expense 500 Supplies expense 2,900 Advertising expense 12,600 74,650

Income from operations 20,700 Other revenues and expenses:

Rent revenue 2,000 Interest expense (250) 1,750

Net income 22,450$

Sample CoIncome Statement

For Year Ended December 31, 2001

Multi-step

Format

SAP 2007 / SAP University Alliances Introductory Accounting

Revenues:Sales, net 328,550$ Rent revenue 2,000 Total revenues 330,550

Expenses:Cost of goods sold 233,200$ Selling expense 44,050 General and administrative expense 30,600 Interest expense 250 Total expenses 308,100

Net income 22,450$

Sample CoIncome Statement

For Year Ended December 31, 2005

Single- step

Format

SAP 2007 / SAP University Alliances Introductory Accounting

Closing Entries — Perpetual System

SAP 2007 / SAP University Alliances Introductory Accounting

Periodic and Perpetual Inventory Systems Compared

Example

Purchases 5,000 Inventory 5,000

Accounts Payable 5,000 Accounts Payable 5,000

Purchase of Merchandise

Return of Merchandise

Accounts Payable 1,000 Accounts Payable 1,000

Purchase Returns 1,000 Inventory 1,000

Periodic System Perpetual System

SAP 2007 / SAP University Alliances Introductory Accounting

Example

Accounts Payable 4,000 Accounts Payable 4,000

Purchase Discounts 80 Inventory 80

Cash 3,920 Cash 3,920

Purchase Discount Taken (2/10, n30)

Transportation Charges

Transportation-in 100 Inventory 100

Accounts Payable 100 Accounts Payable 100

Periodic System Perpetual System

SAP 2007 / SAP University Alliances Introductory Accounting

Example

Accounts Receivable 4,000 Accounts Receivable 4,000

Sales 4,000 Sales 4,000

Cost of Goods Sold 3,000

Inventory 3,000

Sale of merchandise

Periodic System Perpetual System

SAP 2007 / SAP University Alliances Introductory Accounting

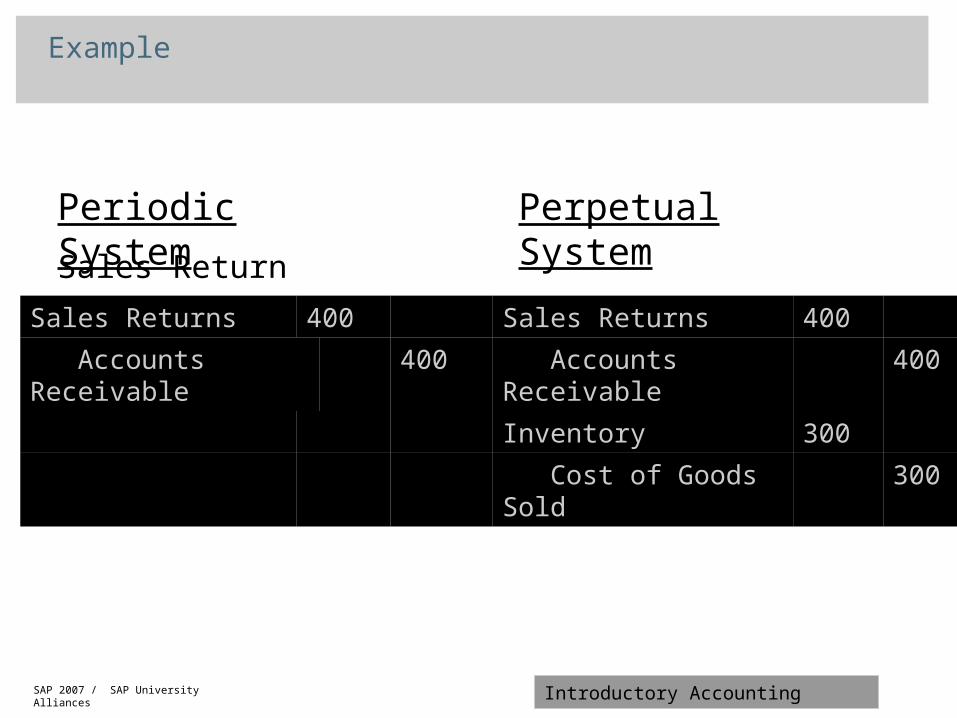

Example

Sales Returns 400 Sales Returns 400

Accounts Receivable 400 Accounts Receivable 400

Inventory 300

Cost of Goods Sold 300

Sales Return

Periodic System Perpetual System

SAP 2007 / SAP University Alliances Introductory Accounting

Assigning Costs to Inventory

SAP 2007 / SAP University Alliances Introductory Accounting

Items in Merchandise Inventory

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

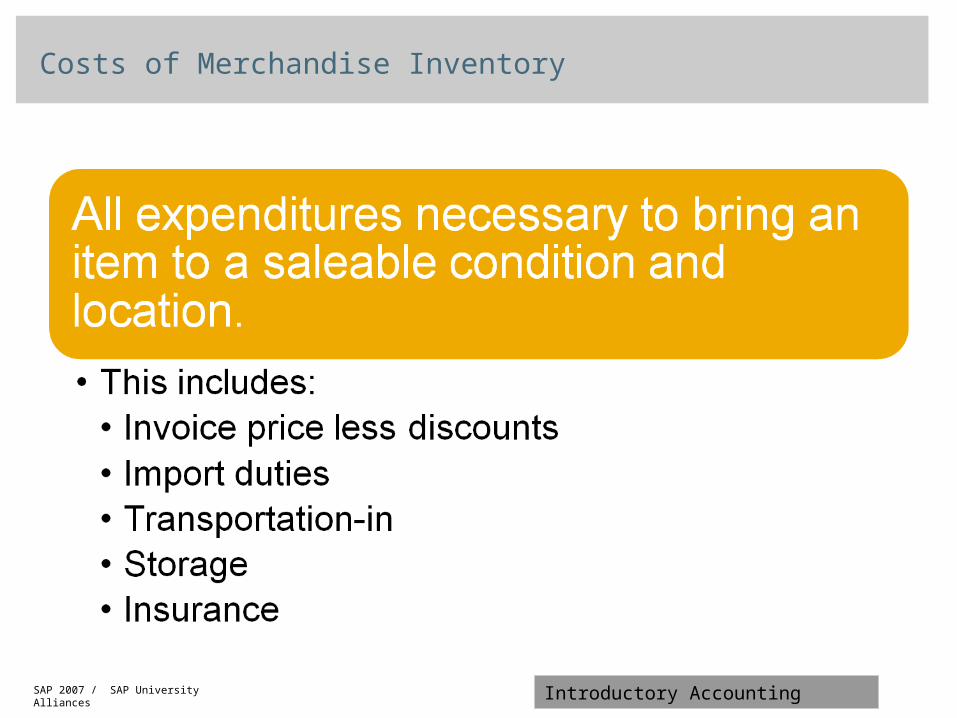

Costs of Merchandise Inventory

SAP 2007 / SAP University Alliances Introductory Accounting

Assigning Costs to Inventory

MerchandiseAvailable

for Sale

Net Costof Purchases

Cost ofGoods Sold

BeginningInventory

EndingInventory

Balance SheetBalance Sheet Income StatementIncome Statement

Merchandising Cost Flows

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

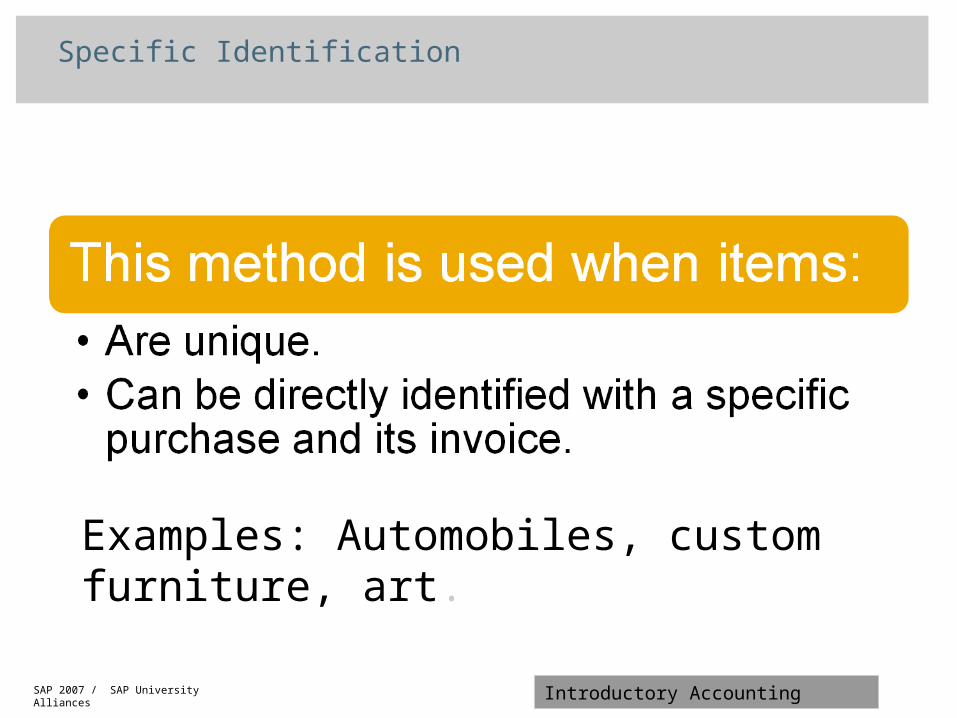

Specific Identification

Examples: Automobiles, custom furniture, art.

SAP 2007 / SAP University Alliances Introductory Accounting

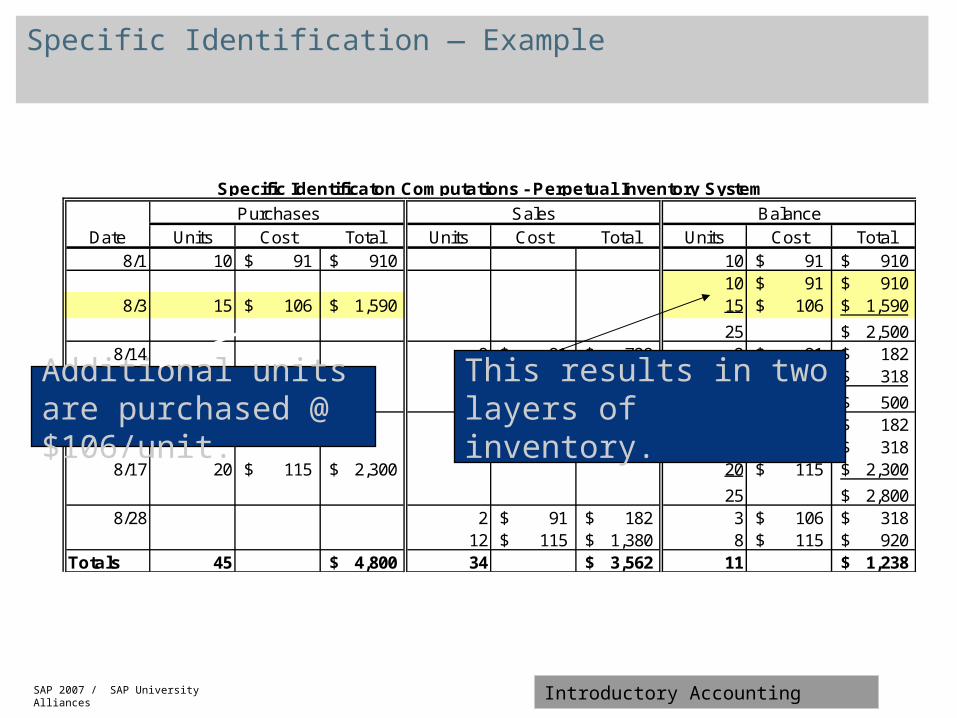

Specific Identification — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 8 91$ 728$ 2 91$ 182$

12 106$ 1,272$ 3 106$ 318$

5 500$ 2 91$ 182$ 3 106$ 318$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,800$ 8/28 2 91$ 182$ 3 106$ 318$

12 115$ 1,380$ 8 115$ 920$ Totals 45 4,800$ 34 3,562$ 11 1,238$

Specific Identificaton Computations - Perpetual Inventory System

The opening inventory consists of 10 units @ $91/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

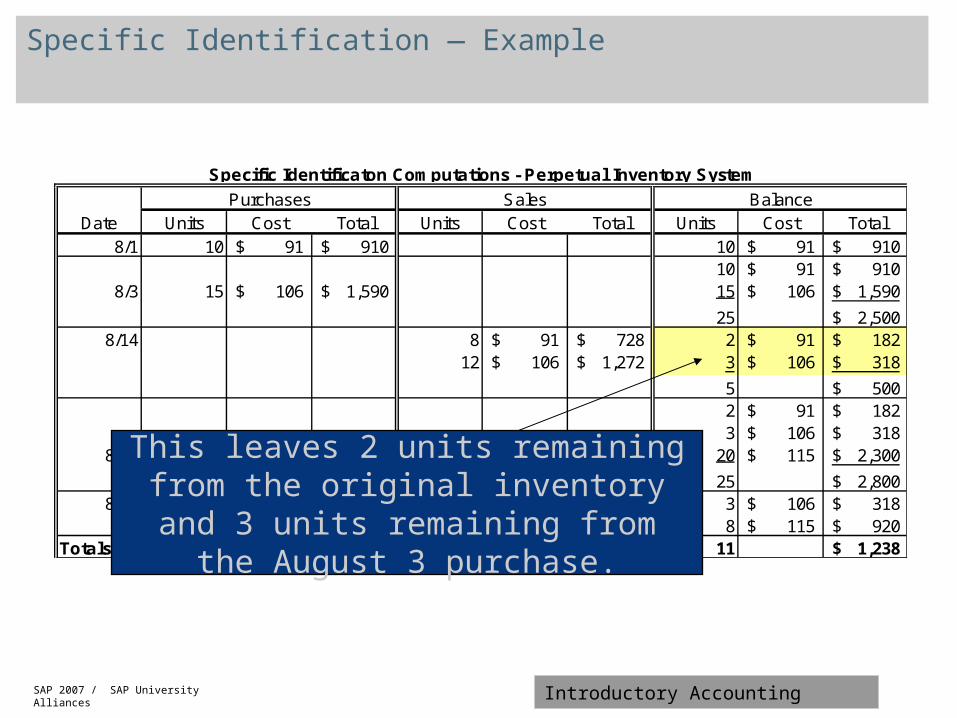

Specific Identification — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 8 91$ 728$ 2 91$ 182$

12 106$ 1,272$ 3 106$ 318$

5 500$ 2 91$ 182$ 3 106$ 318$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,800$ 8/28 2 91$ 182$ 3 106$ 318$

12 115$ 1,380$ 8 115$ 920$ Totals 45 4,800$ 34 3,562$ 11 1,238$

Specific Identificaton Computations - Perpetual Inventory System

This results in two layers of inventory.

Additional units are purchased @ $106/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

Specific Identification — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 8 91$ 728$ 2 91$ 182$

12 106$ 1,272$ 3 106$ 318$

5 500$ 2 91$ 182$ 3 106$ 318$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,800$ 8/28 2 91$ 182$ 3 106$ 318$

12 115$ 1,380$ 8 115$ 920$ Totals 45 4,800$ 34 3,562$ 11 1,238$

Specific Identificaton Computations - Perpetual Inventory System

On August 14, 20 units are sold. Eight of these units came from the opening inventory and the remaining 12

units came from the August 3 purchase.

SAP 2007 / SAP University Alliances Introductory Accounting

Specific Identification — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 8 91$ 728$ 2 91$ 182$

12 106$ 1,272$ 3 106$ 318$

5 500$ 2 91$ 182$ 3 106$ 318$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,800$ 8/28 2 91$ 182$ 3 106$ 318$

12 115$ 1,380$ 8 115$ 920$ Totals 45 4,800$ 34 3,562$ 11 1,238$

Specific Identificaton Computations - Perpetual Inventory System

This leaves 2 units remaining from the original inventory and 3 units remaining

from the August 3 purchase.

SAP 2007 / SAP University Alliances Introductory Accounting

First-In, First-Out (FIFO)

SAP 2007 / SAP University Alliances Introductory Accounting

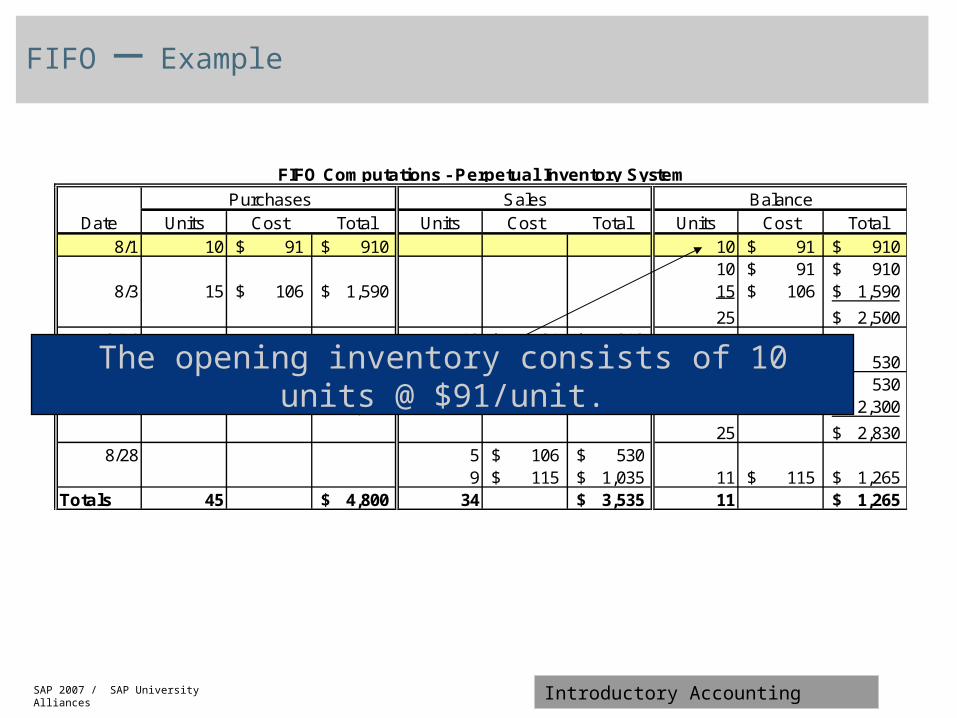

FIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 10 91$ 910$

10 106$ 1,060$ 5 106$ 530$ 5 106$ 530$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,830$ 8/28 5 106$ 530$

9 115$ 1,035$ 11 115$ 1,265$ Totals 45 4,800$ 34 3,535$ 11 1,265$

FIFO Computations - Perpetual Inventory System

The opening inventory consists of 10 units @ $91/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

FIFO — Example

Additional units re purchased @ $106/unit.

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 10 91$ 910$

10 106$ 1,060$ 5 106$ 530$ 5 106$ 530$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,830$ 8/28 5 106$ 530$

9 115$ 1,035$ 11 115$ 1,265$ Totals 45 4,800$ 34 3,535$ 11 1,265$

FIFO Computations - Perpetual Inventory System

This results in two layers of inventory.

Additional units are purchased @ $106/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

FIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 10 91$ 910$

10 106$ 1,060$ 5 106$ 530$ 5 106$ 530$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,830$ 8/28 5 106$ 530$

9 115$ 1,035$ 11 115$ 1,265$ Totals 45 4,800$ 34 3,535$ 11 1,265$

FIFO Computations - Perpetual Inventory System

Under FIFO, units are assumed to be sold in the order acquired. Therefore, of the 20 units sold on August 14, the first 10 units come

from beginning inventory. Therefore, those 10 units are removed from the inventory record based on the cost of those units of $91.

SAP 2007 / SAP University Alliances Introductory Accounting

FIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 10 91$ 910$

10 106$ 1,060$ 5 106$ 530$ 5 106$ 530$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,830$ 8/28 5 106$ 530$

9 115$ 1,035$ 11 115$ 1,265$ Totals 45 4,800$ 34 3,535$ 11 1,265$

FIFO Computations - Perpetual Inventory System

The remaining 10 units sold on August 14th come from the next purchase, made on August 3rd. Therefore, these units are removed

from the inventory record based on their cost of $106.

SAP 2007 / SAP University Alliances Introductory Accounting

FIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 10 91$ 910$

10 106$ 1,060$ 5 106$ 530$ 5 106$ 530$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,830$ 8/28 5 106$ 530$

9 115$ 1,035$ 11 115$ 1,265$ Totals 45 4,800$ 34 3,535$ 11 1,265$

FIFO Computations - Perpetual Inventory System

The ending inventory consists of the 5 remaining units from the August 3 purchase.

SAP 2007 / SAP University Alliances Introductory Accounting

Last-In, First-Out (LIFO)

SAP 2007 / SAP University Alliances Introductory Accounting

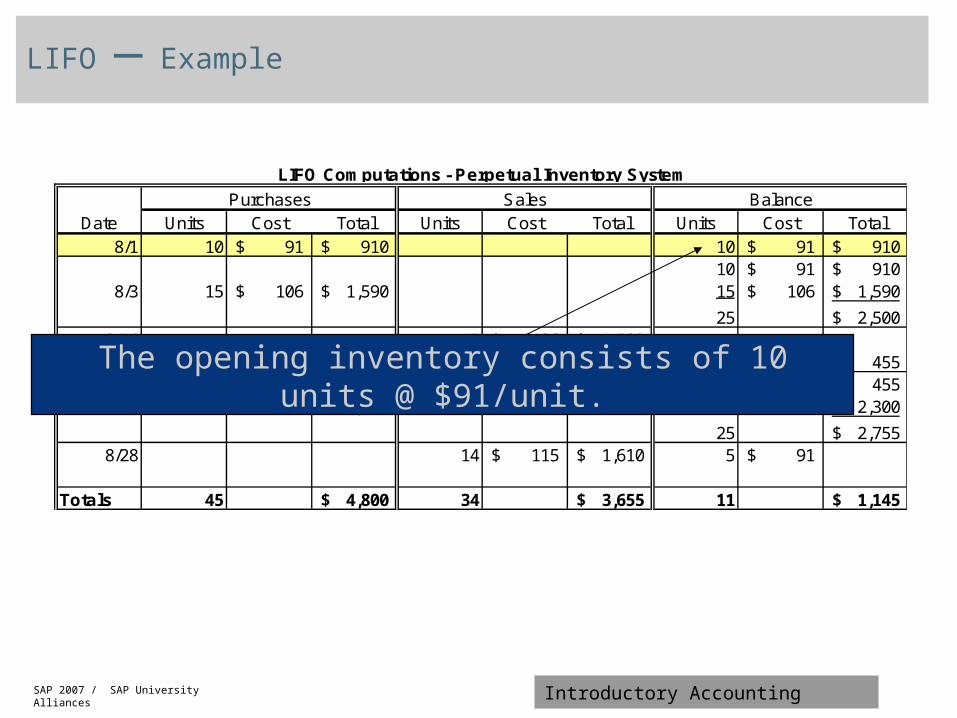

LIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 15 106$ 1,590$

5 91$ 455$ 5 91$ 455$ 5 91$ 455$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,755$ 8/28 14 115$ 1,610$ 5 91$

Totals 45 4,800$ 34 3,655$ 11 1,145$

LIFO Computations - Perpetual Inventory System

The opening inventory consists of 10 units @ $91/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

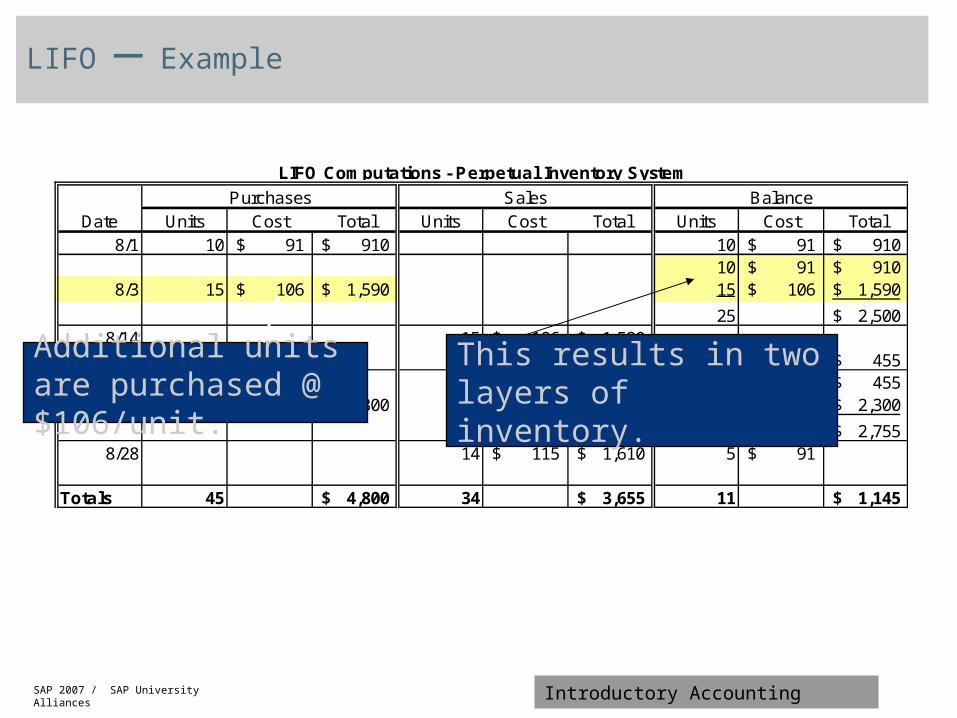

LIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 15 106$ 1,590$

5 91$ 455$ 5 91$ 455$ 5 91$ 455$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,755$ 8/28 14 115$ 1,610$ 5 91$

Totals 45 4,800$ 34 3,655$ 11 1,145$

LIFO Computations - Perpetual Inventory System

Additional units are purchased @ $106/unit.

This results in two layers of inventory.

SAP 2007 / SAP University Alliances Introductory Accounting

LIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 15 106$ 1,590$

5 91$ 455$ 5 91$ 455$ 5 91$ 455$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,755$ 8/28 14 115$ 1,610$ 5 91$

Totals 45 4,800$ 34 3,655$ 11 1,145$

LIFO Computations - Perpetual Inventory System

Of the 20 units sold, these units are assumed to be sold

first.

SAP 2007 / SAP University Alliances Introductory Accounting

LIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 15 106$ 1,590$

5 91$ 455$ 5 91$ 455$ 5 91$ 455$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,755$ 8/28 14 115$ 1,610$ 5 91$

Totals 45 4,800$ 34 3,655$ 11 1,145$

LIFO Computations - Perpetual Inventory System

Once the latest units purchased are sold, units are sold from the

previous purchase.

SAP 2007 / SAP University Alliances Introductory Accounting

LIFO — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 10 91$ 910$

8/3 15 106$ 1,590$ 15 106$ 1,590$

25 2,500$ 8/14 15 106$ 1,590$

5 91$ 455$ 5 91$ 455$ 5 91$ 455$

8/17 20 115$ 2,300$ 20 115$ 2,300$

25 2,755$ 8/28 14 115$ 1,610$ 5 91$

Totals 45 4,800$ 34 3,655$ 11 1,145$

LIFO Computations - Perpetual Inventory System

This leaves 5 units remaining from the first purchase.

SAP 2007 / SAP University Alliances Introductory Accounting

Cost of goods available for sale

Number of units available for sale

Moving Weighted Average Method

Average cost per unit

=

SAP 2007 / SAP University Alliances Introductory Accounting

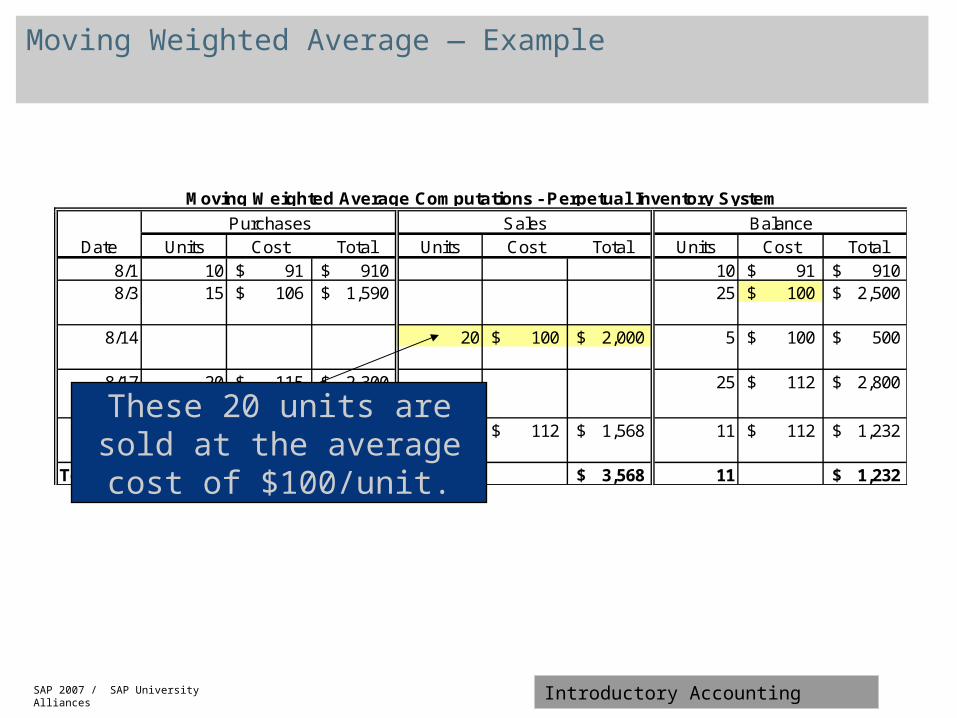

Moving Weighted Average — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 8/3 15 106$ 1,590$ 25 100$ 2,500$

8/14 20 100$ 2,000$ 5 100$ 500$

8/17 20 115$ 2,300$ 25 112$ 2,800$

8/28 14 112$ 1,568$ 11 112$ 1,232$

Totals 45 4,800$ 34 3,568$ 11 1,232$

Moving Weighted Average Computations - Perpetual Inventory System

The opening inventory consists of 10 units @ $91/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

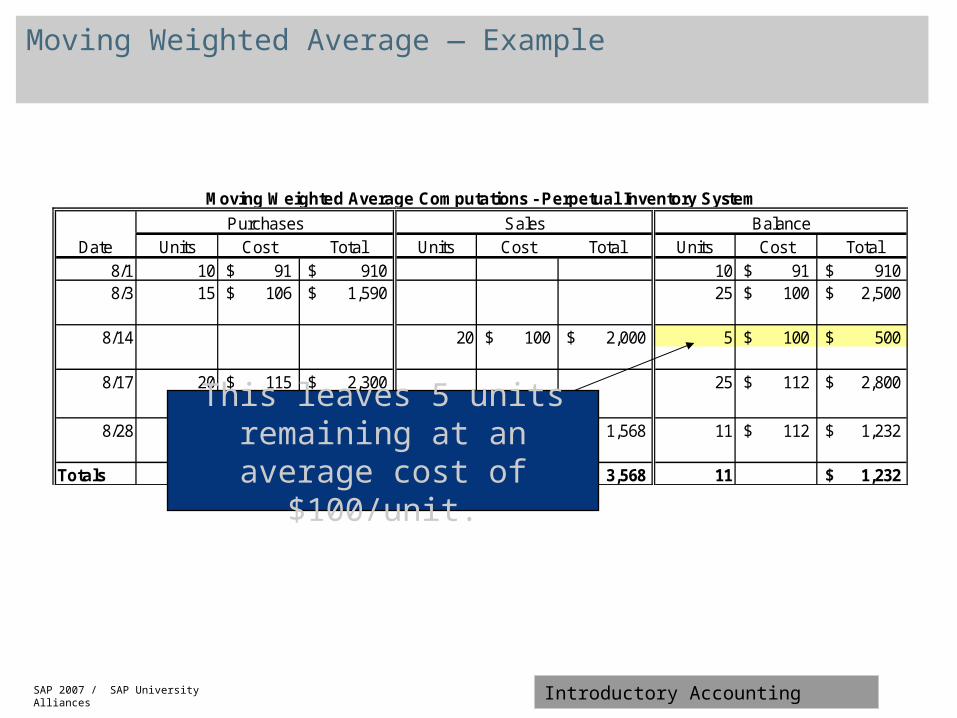

Moving Weighted Average — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 8/3 15 106$ 1,590$ 25 100$ 2,500$

8/14 20 100$ 2,000$ 5 100$ 500$

8/17 20 115$ 2,300$ 25 112$ 2,800$

8/28 14 112$ 1,568$ 11 112$ 1,232$

Totals 45 4,800$ 34 3,568$ 11 1,232$

Moving Weighted Average Computations - Perpetual Inventory System

Additional units are purchased @ $106/unit. This results in an average cost of

$100/unit.

(10 x $91) + (15 x $106) 25 units

SAP 2007 / SAP University Alliances Introductory Accounting

Moving Weighted Average — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 8/3 15 106$ 1,590$ 25 100$ 2,500$

8/14 20 100$ 2,000$ 5 100$ 500$

8/17 20 115$ 2,300$ 25 112$ 2,800$

8/28 14 112$ 1,568$ 11 112$ 1,232$

Totals 45 4,800$ 34 3,568$ 11 1,232$

Moving Weighted Average Computations - Perpetual Inventory System

These 20 units are sold at the average cost of $100/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

Moving Weighted Average — Example

Purchases Sales BalanceDate Units Cost Total Units Cost Total Units Cost Total

8/1 10 91$ 910$ 10 91$ 910$ 8/3 15 106$ 1,590$ 25 100$ 2,500$

8/14 20 100$ 2,000$ 5 100$ 500$

8/17 20 115$ 2,300$ 25 112$ 2,800$

8/28 14 112$ 1,568$ 11 112$ 1,232$

Totals 45 4,800$ 34 3,568$ 11 1,232$

Moving Weighted Average Computations - Perpetual Inventory System

This leaves 5 units remaining at an average cost of $100/unit.

SAP 2007 / SAP University Alliances Introductory Accounting

Financial Reporting

Sample Company

Segment Income Statement - Mountain BikesMonth ending August 31, 2005

Specific Identification

Moving Weighted Average FIFO LIFO

Sales 4,760$ 4,760$ 4,760$ 4,760$ Cost of Goods Sold 3,562$ 3,568$ 3,535$ 3,655$

Gross Profit 1,198 1,192 1,225 1,105Operating expenses 374 374 374 374 Income from operations 824$ 818$ 851$ 731$

Merchandise Inventory 1,238$ 1,232$ 1,265$ 1,145$

August 31, 2001Balance Sheet

SAP 2007 / SAP University Alliances Introductory Accounting

Advantages of Each MethodAdvantages of Each Method

First-In, First-Out

First-In, First-Out

Ending inventory approximates

current replacement cost.

Ending inventory approximates

current replacement cost.

Weighted Average

Weighted Average

Smoothes out purchase price

changes.

Smoothes out purchase price

changes.

Last-In, First-Out

Last-In, First-Out

Better matches current costs in

cost of goods sold with revenues.

Better matches current costs in

cost of goods sold with revenues.

Financial Reporting

Reporting

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

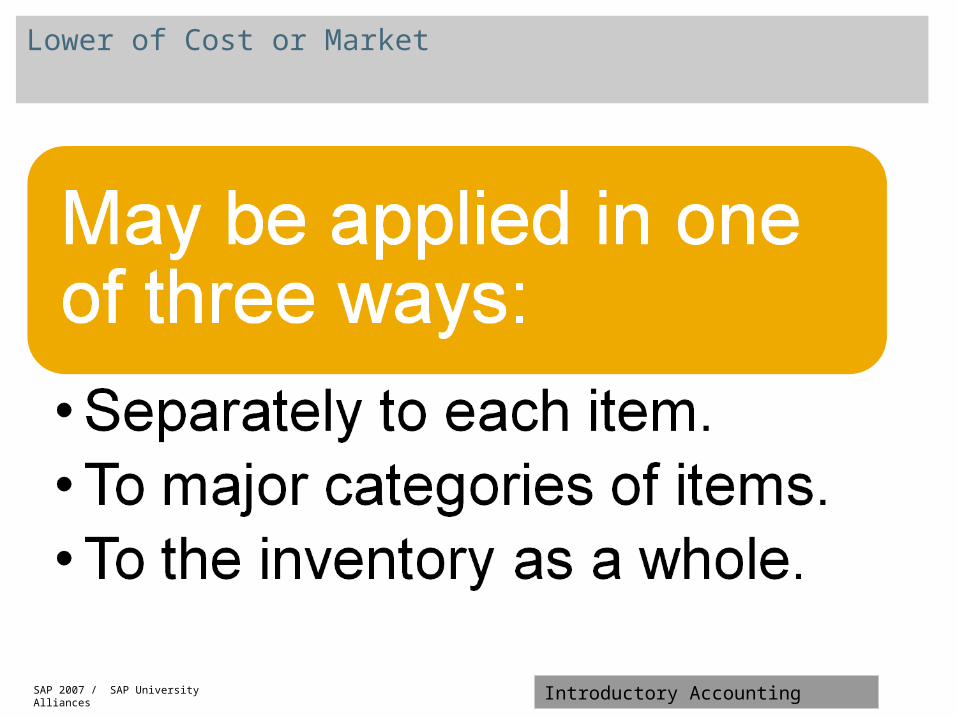

Lower of Cost or Market

SAP 2007 / SAP University Alliances Introductory Accounting

Lower of Cost or Market

SAP 2007 / SAP University Alliances Introductory Accounting

Inventory Errors

SAP 2007 / SAP University Alliances Introductory Accounting

Inventory Errors — Effects on the Income Statement

SAP 2007 / SAP University Alliances Introductory Accounting

Inventory Errors — Effects on the Balance Sheet

SAP 2007 / SAP University Alliances Introductory Accounting

Gross Profit Method

SAP 2007 / SAP University Alliances Introductory Accounting

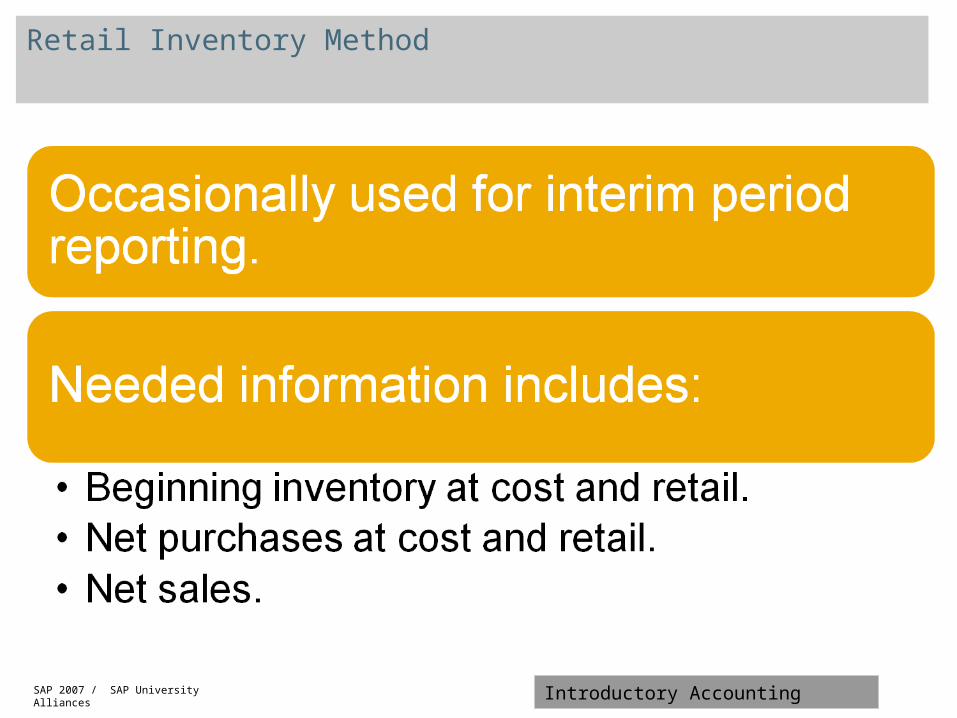

Retail Inventory Method

SAP 2007 / SAP University Alliances Introductory Accounting

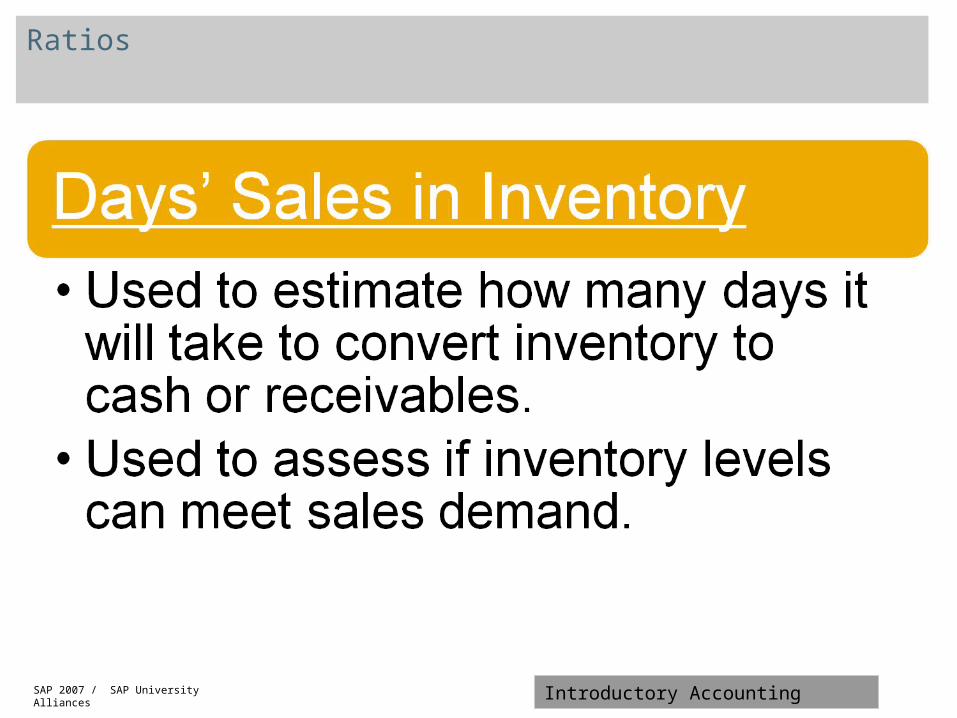

Ratios

SAP 2007 / SAP University Alliances Introductory Accounting

Ratios

Related Documents