Inventories: Additional Issues Chapter 9

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Inventories:Additional Issues

Chapter 9

Reporting —Lower of Cost or Market

Inventories are valued at the lower of cost or market (LCM).

LCM is a departure from historical cost. The method causes losses to be recognized in the period the value of inventory declines below its cost rather than in the

period that the goods ultimately are sold.

LCM is a departure from historical cost. The method causes losses to be recognized in the period the value of inventory declines below its cost rather than in the

period that the goods ultimately are sold.

Determining Market Value

Market Should Not Exceed Net Realizable

Value (Ceiling)

Market Should Not Be Less Than Net Realizable Value less Normal Profit

(Floor)

GAAP defines GAAP defines “market value” in “market value” in terms of current terms of current replacement cost.replacement cost.

Market should not be Market should not be greater than the greater than the “ceiling” or less than “ceiling” or less than the “floor.”the “floor.”

GAAP defines GAAP defines “market value” in “market value” in terms of current terms of current replacement cost.replacement cost.

Market should not be Market should not be greater than the greater than the “ceiling” or less than “ceiling” or less than the “floor.”the “floor.”

Determining Market Value

CeilingCeilingNRVNRV

CeilingCeilingNRVNRV

ReplacementReplacementCostCost

ReplacementReplacementCostCost

NRV – NPNRV – NPFloorFloor

NRV – NPNRV – NPFloorFloor

DesignatedDesignatedMarketMarket

DesignatedDesignatedMarketMarket

CostCostCostCostNot More Than

Not Less Than

Or

Step 1Determine Designated Market

Step 2Compare Designated Market with Cost

Lower of CostLower of Costor Marketor Market

Lower of CostLower of Costor Marketor Market

Lower of Cost or Market

An item in inventory has a historical cost of $20 per unit. At year-end we gather the following per unit information: • Current replacement cost = $21.50• Selling price = $30• Cost to complete and dispose = $4 • Normal profit margin = $5

How would we value this item in the balance sheet?

Lower of Cost or Market

ReplacementCost =$21.50

ReplacementCost =$21.50

$21.50DesignatedMarket?

Historical cost of Historical cost of $20.00 is less than $20.00 is less than

designated market of designated market of $21.50, so this $21.50, so this

inventory item will be inventory item will be valued at cost of valued at cost of

$20.00.$20.00.

1. Apply LCM to 1. Apply LCM to each individual itemeach individual item in in inventory such as printers. inventory such as printers.

1. Apply LCM to 1. Apply LCM to each individual itemeach individual item in in inventory such as printers. inventory such as printers.

Applying Lower of Cost or Market

Lower of cost or market can be applied 3 different ways.

1. Apply LCM to 1. Apply LCM to each individual itemeach individual item in in inventory. inventory.

1. Apply LCM to 1. Apply LCM to each individual itemeach individual item in in inventory. inventory.

2. Apply LCM to logical inventorycategories, such as desktop and laptop

computers.

2. Apply LCM to logical inventorycategories, such as desktop and laptop

computers.

Applying Lower of Cost or Market

Lower of cost or market can be applied 3 different ways.

1. Apply LCM to 1. Apply LCM to each individual itemeach individual item in in inventory. inventory.

1. Apply LCM to 1. Apply LCM to each individual itemeach individual item in in inventory. inventory.

2. Apply LCM to logical inventorycategories.

2. Apply LCM to logical inventorycategories.

3. Apply LCM to the entire inventory as a group.

3. Apply LCM to the entire inventory as a group.

Applying Lower of Cost or Market

Lower of cost or market can be applied 3 different ways.

Adjusting Cost to Market1. Record the loss as a separate item in

the income statement

Loss on write-down of inventory XX Inventory XX

2. Record the loss as part of cost of goods sold.

Cost of goods sold XX Inventory XX

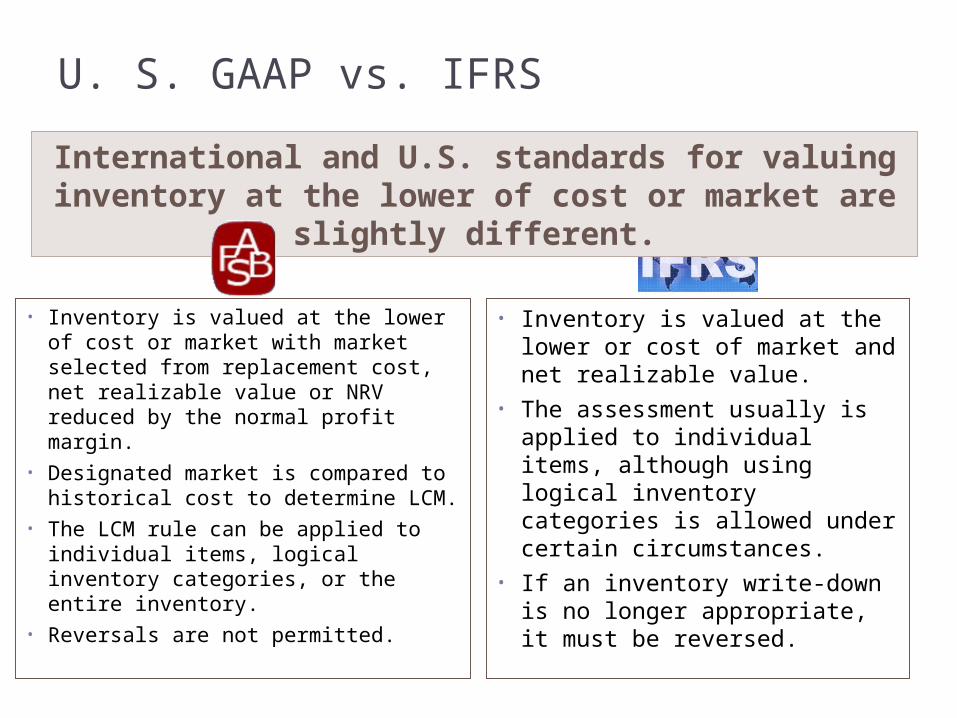

U. S. GAAP vs. IFRS

• Inventory is valued at the lower of cost or market with market selected from replacement cost, net realizable value or NRV reduced by the normal profit margin.

• Designated market is compared to historical cost to determine LCM.

• The LCM rule can be applied to individual items, logical inventory categories, or the entire inventory.

• Reversals are not permitted.

• Inventory is valued at the lower or cost of market and net realizable value.

• The assessment usually is applied to individual items, although using logical inventory categories is allowed under certain circumstances.

• If an inventory write-down is no longer appropriate, it must be reversed.

International and U.S. standards for valuing inventory at the lower of cost or market are slightly different.

Inventory Estimation Techniques (NOT COVERED)

Estimate instead of taking physical inventory 1. Less costly 2. Less time-consuming

Two popular methods of estimating ending inventory are the . . .

1. Gross profit method2. Retail inventory method

End of Chapter 9

Related Documents