Introduction to options & Introduction to options & option valuation option valuation FIN 441 FIN 441 Prof. Rogers Prof. Rogers Spring 2012 Spring 2012

Introduction to options & option valuation FIN 441 Prof. Rogers Spring 2012.

Jan 01, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Introduction to options & option Introduction to options & option valuationvaluation

FIN 441FIN 441

Prof. RogersProf. Rogers

Spring 2012Spring 2012

What are option contracts What are option contracts (“options”)?(“options”)?

• Definition:– Right (but not obligation) to buy or sell underlying

asset.– Forwards/Futures are obligations to buy or sell!

• Most options are formal contracts– Every option has a “buyer” and a “seller.”– “It takes two to tango” but it takes at least two to

create an option contract!– In some cases, “options” don’t have to involve formal

contract (example, “real options”).

Basic option terminologyBasic option terminology• Call

– Right to buy underlying.• Put

– Right to sell underlying.• Writer (of option)

– Options do not magically appear. “Writer” = seller.– Writer has an obligation to perform IF the option is exercised.

• Premium– How much does writer receive from buyer?

• Exercise price– What is the fixed price at which option buyer buys or sells

underlying (if option is exercised)?• Expiration

– At what date does the option contract expire?

The basics of option payoffsThe basics of option payoffs

• Hockey stick diagrams– Call– Put– Writer of call– Writer of put

• What do forward and futures contract payoffs look like?

• More terminology:– At-the-money.– In-the-money.– Out-of-the-money

““Where” does option trading Where” does option trading happen?happen?

• Organized exchanges– Standardized contracts– See “Major Options Exchanges” (Table 2.1) in

Chance & Brooks.– Example: Chicago Board Options Exchange (

http://www.cboe.com)• Over-the-counter (OTC)

– Privately negotiated options– Data sources (ISDA & BIS surveys)

• Why do the two venues coexist?– Users differ in their need for contract standardization.– Advantages to each venue.

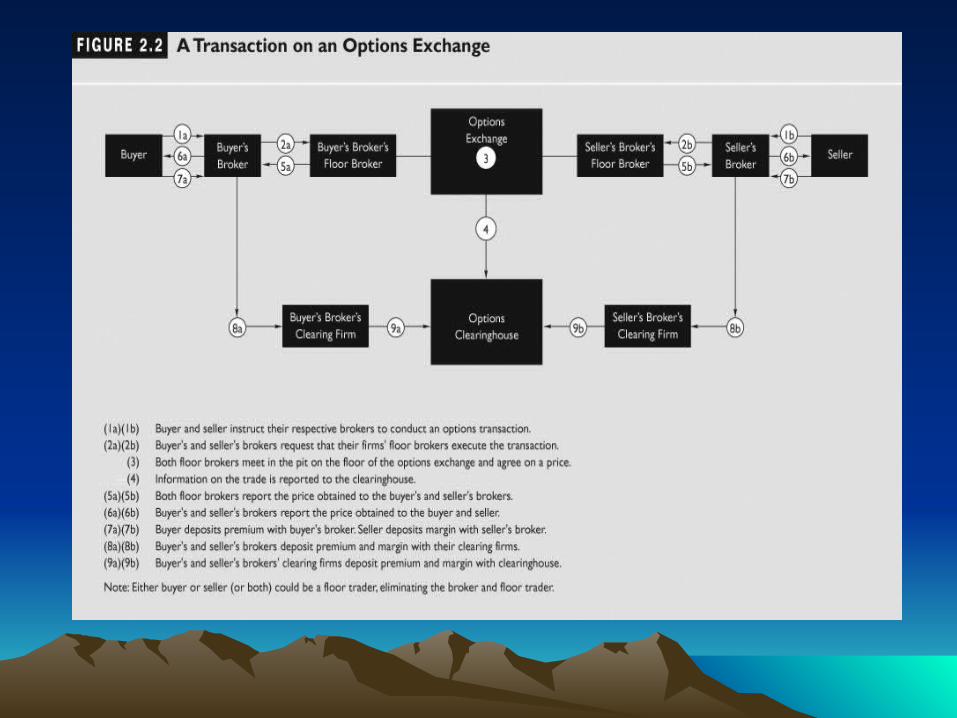

Option quotes & order processOption quotes & order process

• CBOE example– Look at MSFT options

• Expiration dates• Exercise prices• Premiums

• Order process (see Figure 2.2)– Writing options & margin deposits

Exiting an option transactionExiting an option transaction

• Placing an offsetting order– Buy, then sell (or sell, then buy).– Exchange-traded options are more conducive to engaging in

offsetting trades than OTC options.

• Exercising an option– Buyer chooses if and when to exercise (writer has no say).– Physical settlement vs. cash settlement.– Realizing option’s “intrinsic value” (NOTE: this is NOT the same

“intrinsic value” mentioned by stock market investors!)

• Letting it expire– Not feasible unless option is out of the money at expiration date.– Good broker should have policy of not letting “valuable” option

expire if it’s in the money!

What are the underlying assets on What are the underlying assets on which options are traded? which options are traded?

• Individual stocks (most popular example)• Stock indices• Currencies, interest rates, and commodities

(primarily OTC-traded)• Credit quality• Options on futures contracts (see Chapter 9 for

discussion of differences from other options)• Real assets (“real options” will receive some

discussion when we cover the applications of option valuation)

Basic Notation and TerminologyBasic Notation and Terminology

• Symbols– S0 (stock price)

– X (exercise price)– T (time to expiration = (days until

expiration)/365)– r (see below)

– ST (stock price at expiration)

– C(S0,T,X), P(S0,T,X)

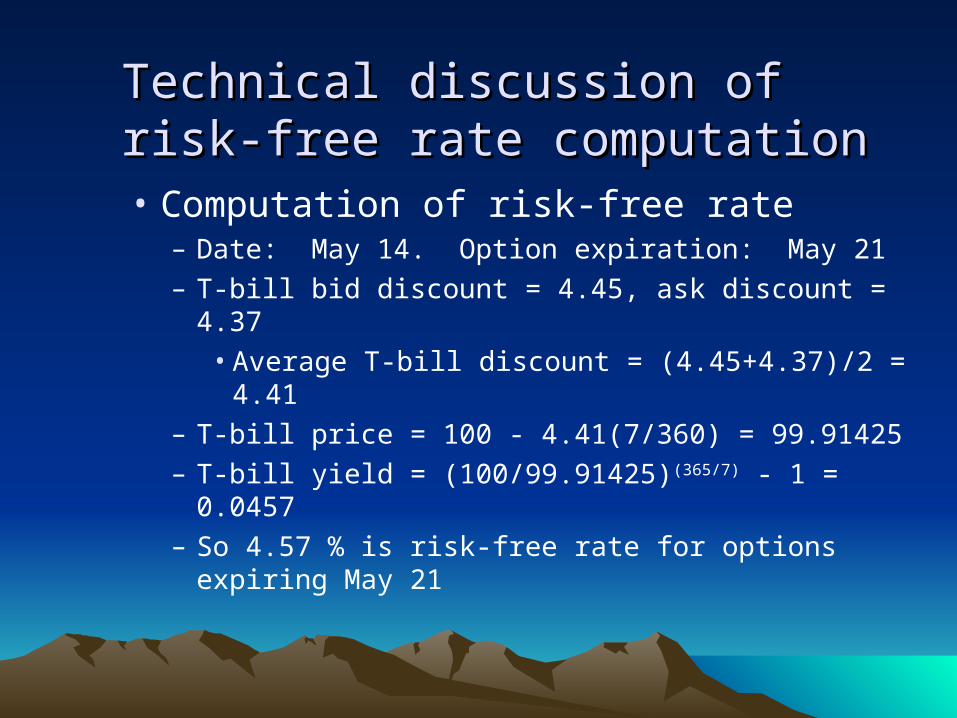

Technical discussion of risk-free rate Technical discussion of risk-free rate computationcomputation• Computation of risk-free rate

– Date: May 14. Option expiration: May 21– T-bill bid discount = 4.45, ask discount = 4.37

• Average T-bill discount = (4.45+4.37)/2 = 4.41– T-bill price = 100 - 4.41(7/360) = 99.91425– T-bill yield = (100/99.91425)(365/7) - 1 = 0.0457– So 4.57 % is risk-free rate for options expiring May

21

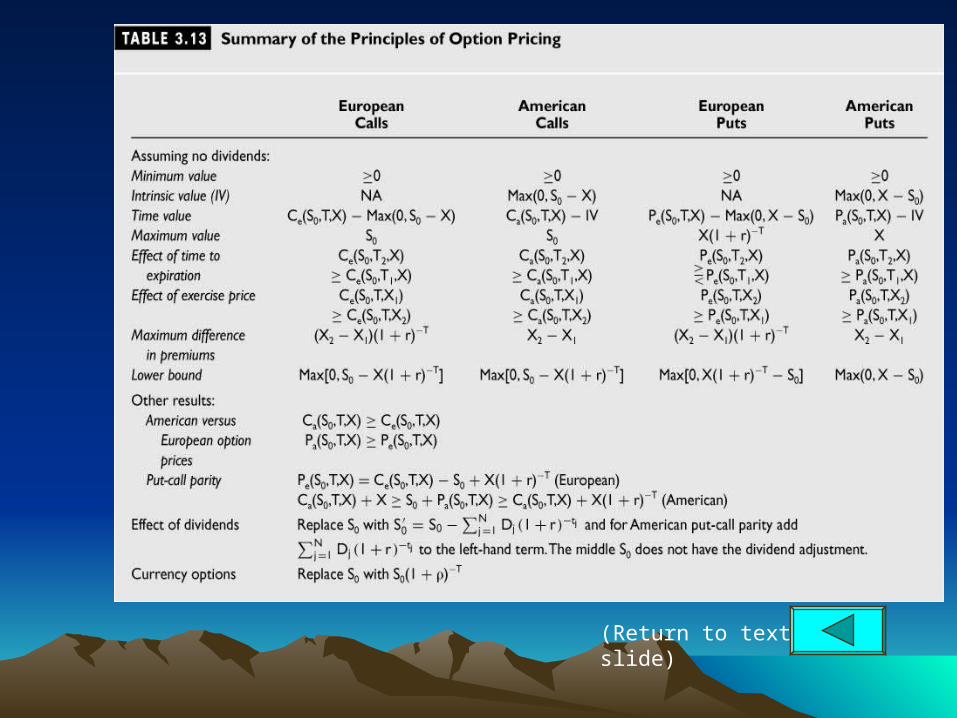

Principles of Call Option PricingPrinciples of Call Option Pricing

• Minimum Value of a Call– C(S0,T,X) 0 (for any call)

– For American calls:• Ca(S0,T,X) Max(0,S0 - X)

– Concept of intrinsic value: Max(0,S0 - X)

– Concept of time value of option• C(S,T,X) – Max(0,S – X)

Principles of Call Option Pricing Principles of Call Option Pricing (continued)(continued)

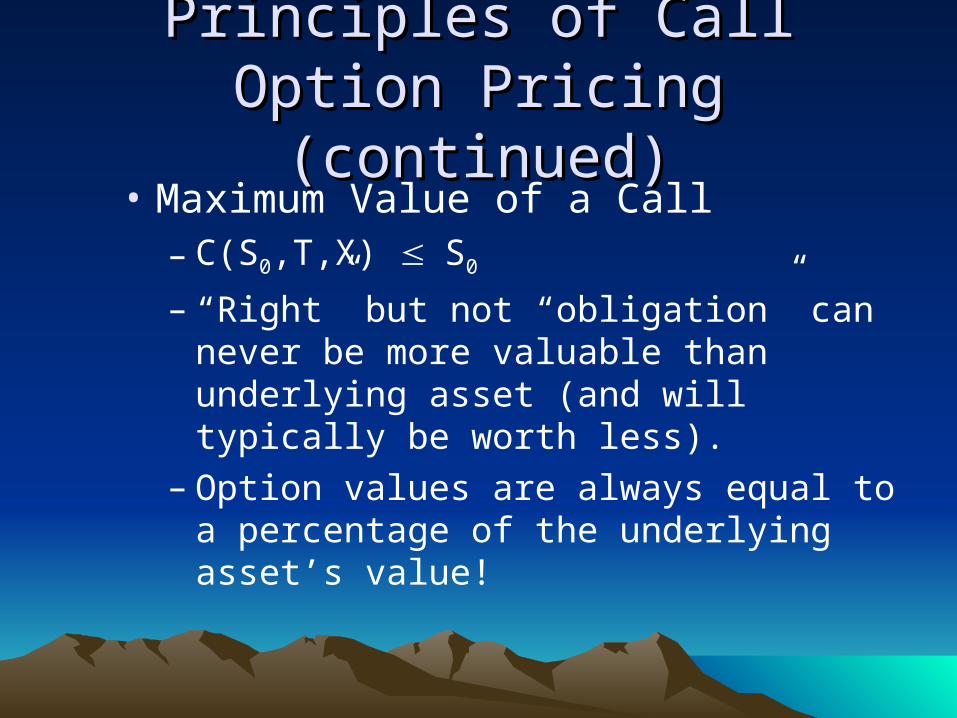

• Maximum Value of a Call– C(S0,T,X) S0

– “Right” but not “obligation” can never be more valuable than underlying asset (and will typically be worth less).

– Option values are always equal to a percentage of the underlying asset’s value!

Principles of Call Option Pricing Principles of Call Option Pricing (continued)(continued)

• Effect of Time to Expiration– More time until expiration, higher option

value!• Volatility is related to time (we’ll see this in

binomial and Black-Scholes models).• Calls allow buyer to invest in other assets, thus

a pure time value of money effect.

Principles of Call Option Pricing Principles of Call Option Pricing (continued)(continued)

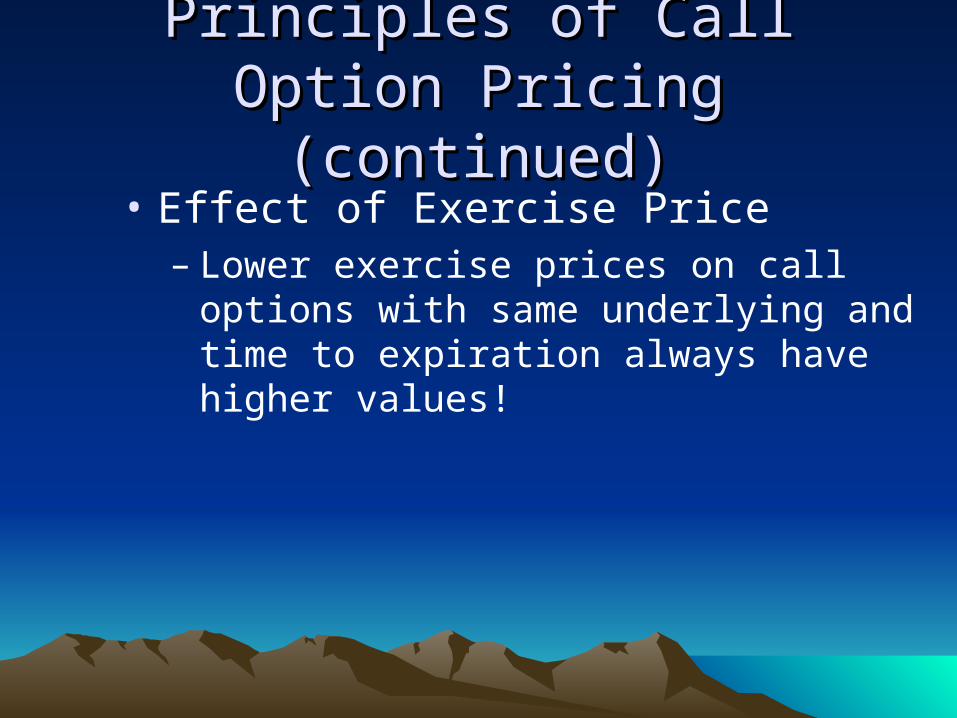

• Effect of Exercise Price– Lower exercise prices on call options with

same underlying and time to expiration always have higher values!

Principles of Call Option Pricing Principles of Call Option Pricing (continued)(continued)

• Lower Bound of a European Call– Ce(S0,T,X) Max[0,S0 - X(1+r)-T]

– This is the lower bound for a European call

Principles of Call Option Pricing Principles of Call Option Pricing (continued)(continued)

• American Call Versus European Call– Ca(S0,T,X) Ce(S0,T,X)– If there are no dividends on the stock, an

American call will never be exercised early.– It will always be better to sell the call in the

market.– In such cases, the value of the American call

and identical European call should be equal.

Principles of Put Option PricingPrinciples of Put Option Pricing

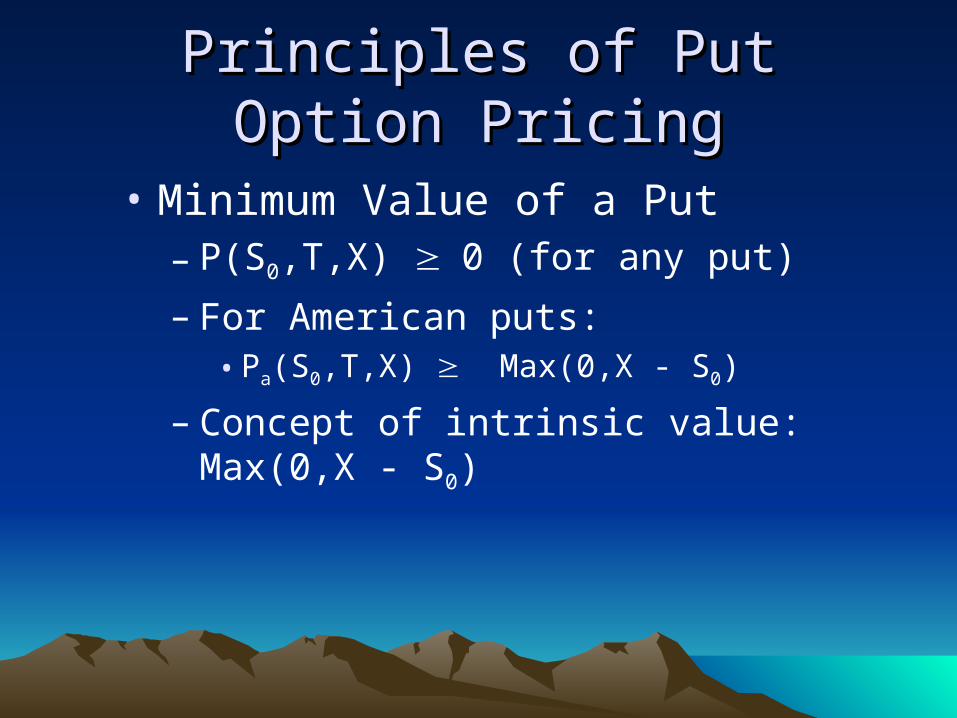

• Minimum Value of a Put– P(S0,T,X) 0 (for any put)

– For American puts:• Pa(S0,T,X) Max(0,X - S0)

– Concept of intrinsic value: Max(0,X - S0)

Principles of Put Option Pricing Principles of Put Option Pricing (continued)(continued)

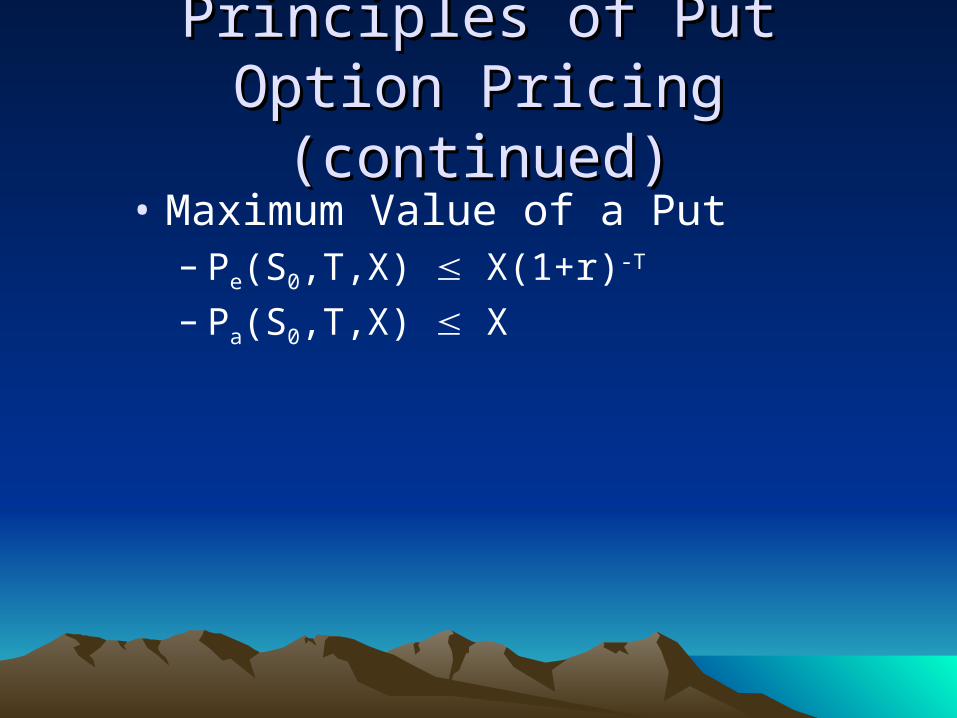

• Maximum Value of a Put– Pe(S0,T,X) X(1+r)-T

– Pa(S0,T,X) X

Principles of Put Option Pricing Principles of Put Option Pricing (continued)(continued)

• The Effect of Time to Expiration– Same effect as call options: more time, more

value!

Principles of Put Option Pricing Principles of Put Option Pricing (continued)(continued)

• Effect of Exercise Price– Raising exercise price of put options

increases value!

Principles of Put Option Pricing Principles of Put Option Pricing (continued)(continued)

• Lower Bound of a European Put– Pe(S0,T,X) Max(0,X(1+r)-T - S0)

– This is the lower bound for a European put

Principles of Put Option Pricing Principles of Put Option Pricing (continued)(continued)

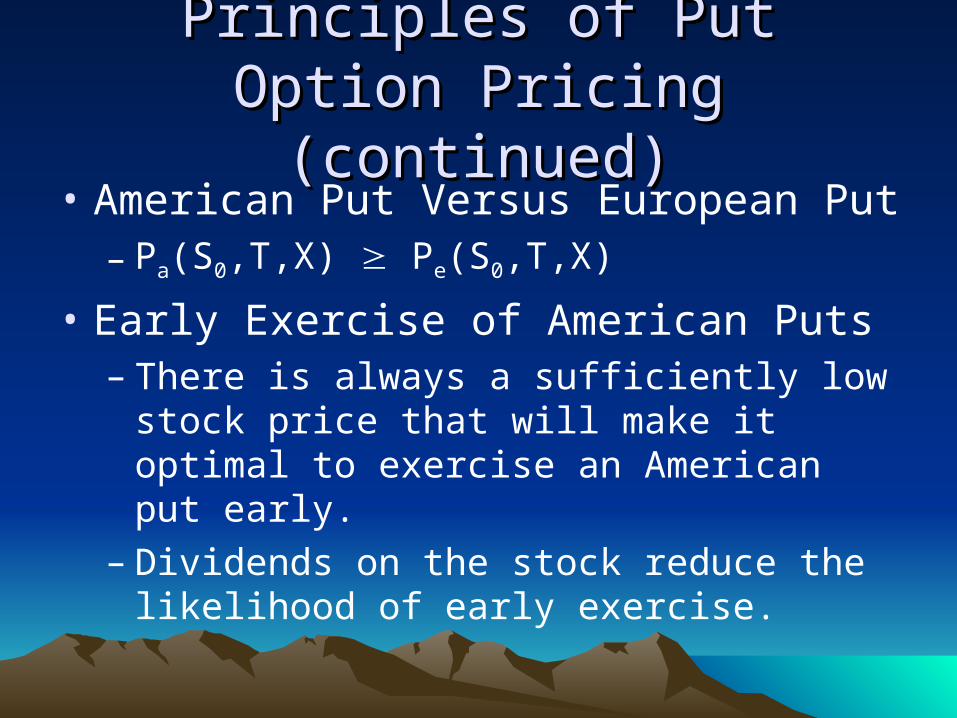

• American Put Versus European Put– Pa(S0,T,X) Pe(S0,T,X)

• Early Exercise of American Puts– There is always a sufficiently low stock price

that will make it optimal to exercise an American put early.

– Dividends on the stock reduce the likelihood of early exercise.

European put-call parityEuropean put-call parity

– Form portfolios A and B where the options are European. See Table 3.11.

– The portfolios have the same outcomes at the options’ expiration. Thus, it must be true that

• S0 + Pe(S0,T,X) = Ce(S0,T,X) + X(1+r)-T

• This is called put-call parity.• It is important to see the alternative ways the

equation can be arranged and their interpretations.

(Return to text slide)

One-Period Binomial ModelOne-Period Binomial Model

• Conditions and assumptions– One period, two outcomes (states)– S = current stock price– u = 1 + return if stock goes up– d = 1 + return if stock goes down– r = risk-free rate

• Value of European call at expiration one period later– Cu = Max(0,Su - X) or– Cd = Max(0,Sd - X)

One-Period Binomial Model One-Period Binomial Model (continued)(continued)

• This is the theoretical value of the call as determined by the stock price, exercise price, risk-free rate, and up and down factors.

• The probabilities of the up and down moves were never specified. They are irrelevant to the option price.

d)-d)/(u-r(1=p

wherer1

p)C(1pCC du

One-Period Binomial Model One-Period Binomial Model (continued)(continued)

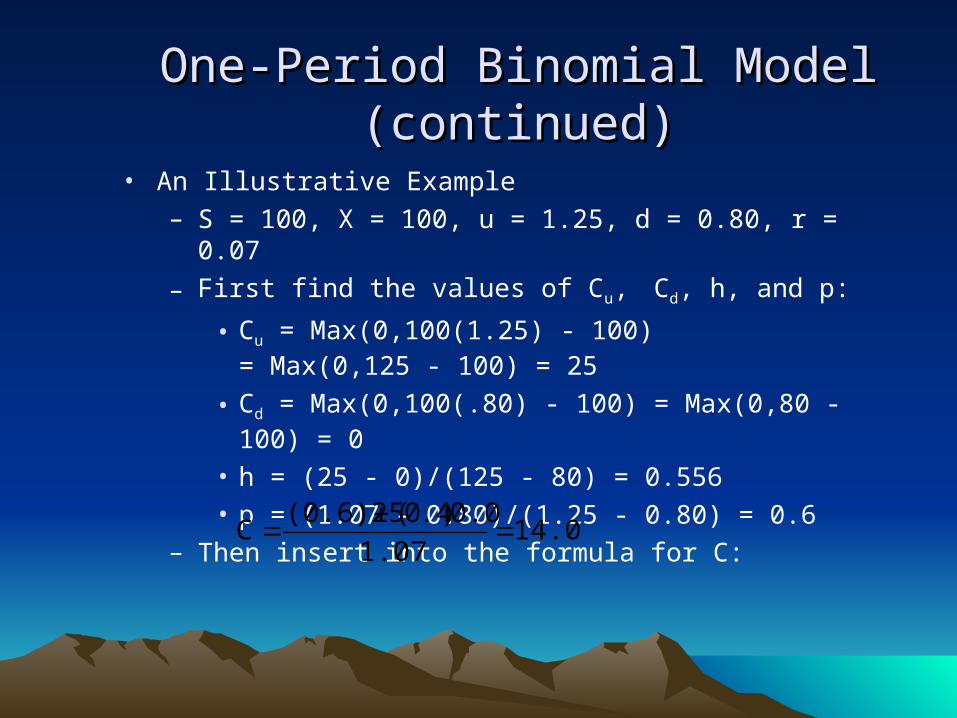

• An Illustrative Example– S = 100, X = 100, u = 1.25, d = 0.80, r = 0.07

– First find the values of Cu, Cd, h, and p:

• Cu = Max(0,100(1.25) - 100) = Max(0,125 - 100) = 25

• Cd = Max(0,100(.80) - 100) = Max(0,80 - 100) = 0

• h = (25 - 0)/(125 - 80) = 0.556• p = (1.07 - 0.80)/(1.25 - 0.80) = 0.6

– Then insert into the formula for C: 14.02

1.07

0.0).40((0.6)25C

Next class!Next class!

• Valuing options with a two-period binomial model

• The concept of a hedged portfolio using options and the underlying asset (no-arbitrage model).– Show using both one and two-period binomial

models.

• Extensions of the two-period binomial model.– Put options– Binomial models and early exercise (difference

between American and European values)

Related Documents