Introduction to Accounting and Business Unit 2 Laurie Hopkins Chapter 1 1

Introduction to Accounting and Business Unit 2 Laurie Hopkins

Dec 30, 2015

Chapter 1. Introduction to Accounting and Business Unit 2 Laurie Hopkins. Generally Accepted Accounting Principles p 7. Financial accountants follow generally accepted accounting principles (GAAP) in preparing reports. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Introduction toAccounting and Business

Unit 2Laurie Hopkins

Chapter 1

1

• Financial accountants follow generally accepted accounting principles (GAAP) in preparing reports.

Generally Accepted Accounting Principles p 7

• Within the United States, the Financial Accounting Standards Board (FASB) has the primary responsibility for developing accounting principles.

2

Why and How

Those accounting principles along with accounting concepts are the how and why behind accounting.

So let’s look at some concepts.

Under the Under the business entity concept, the activities of a the activities of a business are recorded business are recorded separately from the activities separately from the activities of its owners, creditors, or of its owners, creditors, or other businesses.other businesses.

Business Entity Concept p 8

4

Under the cost concept, amounts are initially recorded in the accounting records at their cost or purchase price.

Cost Concept p 8

5

The objectivity concept requires that the amounts recorded in the accounting records be based on objective evidence.

In other words, what it actually cost.

Objectivity Concept p 9

6

The unit of measure concept requires that economic data be recorded in dollars.

In other words we use money as our measuring stick.

Unit of Measure Concept p9

7

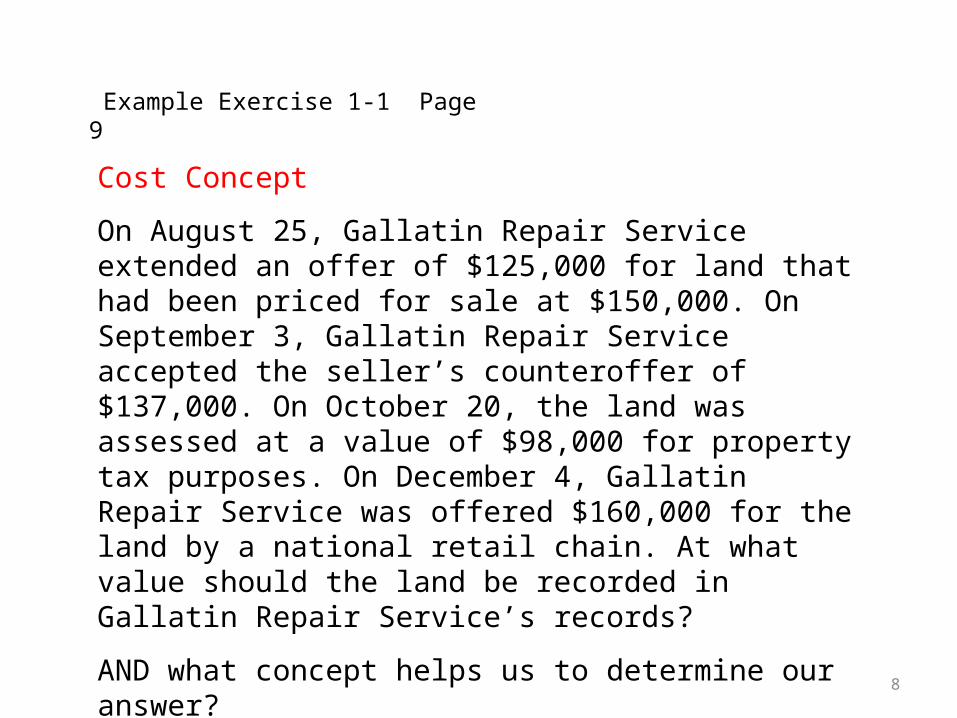

Cost Concept

On August 25, Gallatin Repair Service extended an offer of $125,000 for land that had been priced for sale at $150,000. On September 3, Gallatin Repair Service accepted the seller’s counteroffer of $137,000. On October 20, the land was assessed at a value of $98,000 for property tax purposes. On December 4, Gallatin Repair Service was offered $160,000 for the land by a national retail chain. At what value should the land be recorded in Gallatin Repair Service’s records?

AND what concept helps us to determine our answer?

Example Exercise 1-1 Page 9

8

$137,000. Under the cost concept, the land should be recorded at the cost to Gallatin Repair Service.

Example Exercise 1-1 (continued)

9

State the accounting equation and define each element of the equation.

Assets=Liabilities + Owner’s Equity

Objective 3

10

The resources owned by a

business

Assets = Liabilities + Owner’s Equity

The Accounting Equation

11

The rights of the creditors are

the debts of the business.

Assets = Liabilities + Owner’s Equity

The Accounting Equation

12

The rights of the owners

Assets = Liabilities + Owner’s Equity

The Accounting Equation

13

Laurie’s Definitions:

• Assets – what we own• Liabilities – what we owe• Equity – the difference between the two

If I own a $50K house and owe $40K on it, what is the difference between the two?

$10K – my equity or worth in the business

Accounting Equation

John Joos is the owner and operator of You’re A Star, a motivational consulting business. At the end of its accounting period, December 31, 2009, You’re A Star has assets of $800,000 and liabilities of $350,000. Using the accounting equation, determine the following amounts:

a. Owner’s equity, as of December 31, 2009.b. Owner’s equity, as of December 31, 2010, assuming that

assets increased by $130,000 and liabilities decreased by $25,000 during 2010.

Letter a first – remember the accounting equation(A=L+E)

Example Exercise 1-2 Page 9

15

a. Assets = Liabilities + Owner’s Equity $800,000 = $350,000 + Owner’s Equity

Owner’s Equity = $450,000

Example Exercise 1-2 (continued)

16

Same equation A=L+E but the assets increased by 130K and liabilities decreased by $25K but both sides have to balance.

Example Exercise 1-2 (continued)

b. First, determine the change in Owner’s Equity during 2010 as follows:

Assets = Liabilities + Owner’s Equity $130,000 = –$25,000 + Owner’s Equity

Owner’s Equity = $155,000

Next, add the change in Owner’s Equity on December 31, 2009 (remember the 2009 balance was $450K) to arrive at Owner’s Equity on December 31, 2010, as shown below:

$605,000 = $450,000 + $155,000 For fun let’s put this into the accounting equation to check it.

17

A = L + E (or OE)

• Balances: Assets were $800K and they increased by $130K to become $930KLiabilities were $350K and they decreased by $25K to become $325K

So if A = L + E$930K = 325K + 605K – does it work?

Describe and illustrate how business transactions can be recorded in terms of the resulting change in the elements of the accounting equation. P 10

Make sure you go through the examples on pages 11 – 14 slowly.

Objective 4

19

A business transaction is an economic event or condition that directly changes an entity’s financial condition or its results of operations.

Business Transaction

20

Transactions

Salvo Delivery Service is owned and operated by Joel Salvo. The following selected transactions were completed by Salvo Delivery Service during February:

From the listed transactions numbered 1 through 5 indicate the effect of each transaction on the accounting equation elements (Assets, Liabilities, Owner’s Equity, Drawing, Revenue, and Expense) by listing the numbers identifying the transactions, (1) through (5). Also, indicate the specific item within the accounting equation element that is affected. To illustrate, the answer to (1) is shown.

First, let’s back up and talk about 3 more elements

Example Exercise 1-3 p 15

21

Owner’s Equity

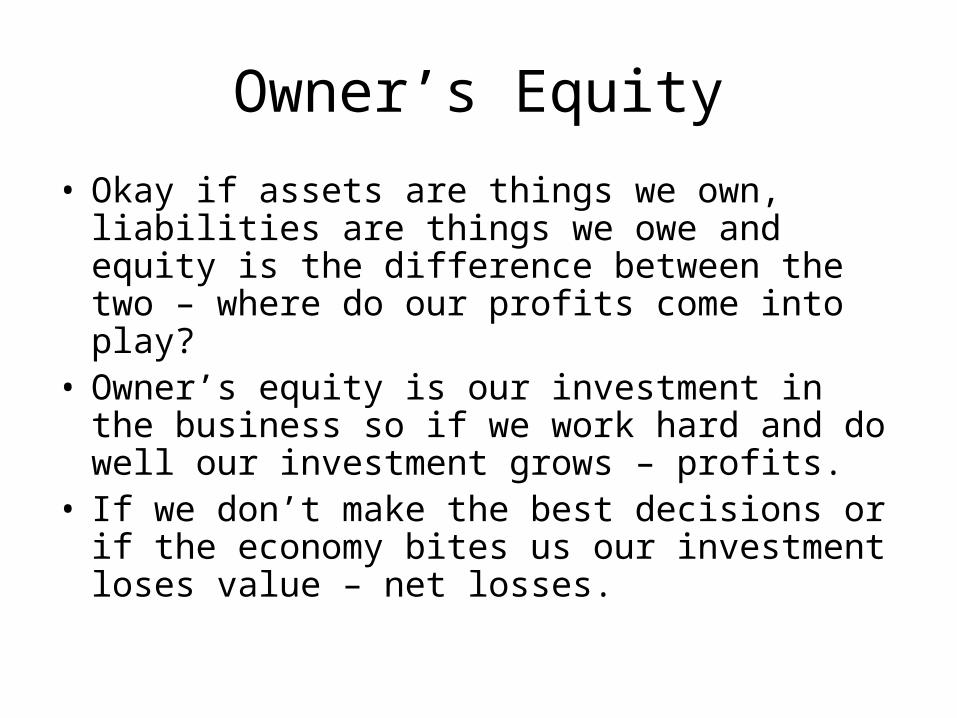

• Okay if assets are things we own, liabilities are things we owe and equity is the difference between the two – where do our profits come into play?

• Owner’s equity is our investment in the business so if we work hard and do well our investment grows – profits.

• If we don’t make the best decisions or if the economy bites us our investment loses value – net losses.

Owner’s Equity Con’t.

• So net profits will increase our equity or worth in the business.

• Net losses will reduce our worth.• How does that play out?• We figure our net profits or losses by taking our

revenues and subtracting our expenses (or cost of doing business).

• If revenues are higher we have a profit.• If expenses are higher then a loss.

So back to the example exercise to see this play out a little.

1. Received cash from owner as additional investment, $35,000.

(1) Asset (Cash) increases by $35,000; Owner’s Equity (Joel Salvo, Capital) increases by $35,000.

A=L + OE so… +35K to A = L (same) + add 35K to OE

2. Paid creditors on account, $1800.

(2) Asset (Cash) decreases by $1,800; Liability (Accounts Payable) decreases by $1,800.

Drop A and L by $1800, both sides still balance

24

3. Billed customers for delivery services on account (means they owe us for this), $11,250.

(3) Asset (Accounts Receivable) increases by $11,250; Revenue (Delivery Service Fees) increases by $11,250.

4. Received cash from customers on account, $6,740.

(4) Asset (Cash) increases by $6,740; Asset (Accounts Receivable) decreases by $6,740.

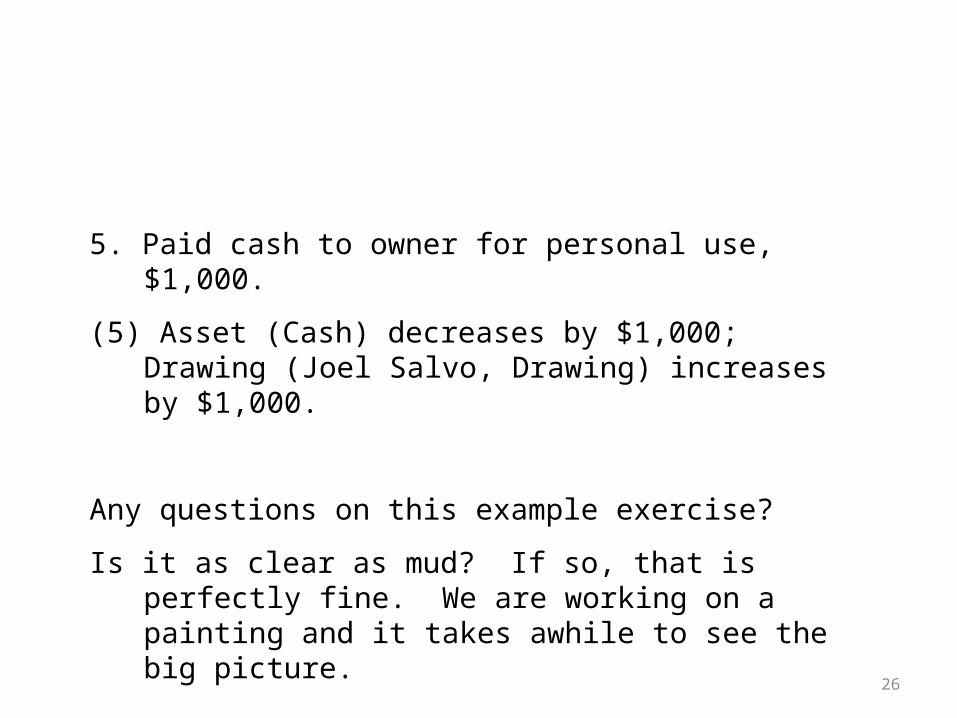

5. Paid cash to owner for personal use, $1,000.

(5) Asset (Cash) decreases by $1,000; Drawing (Joel Salvo, Drawing) increases by $1,000.

Any questions on this example exercise?

Is it as clear as mud? If so, that is perfectly fine. We are working on a painting and it takes awhile to see the big picture.

26

Describe the financial statements of a proprietorship and explain how they interrelate. P 15

Objective 5

27

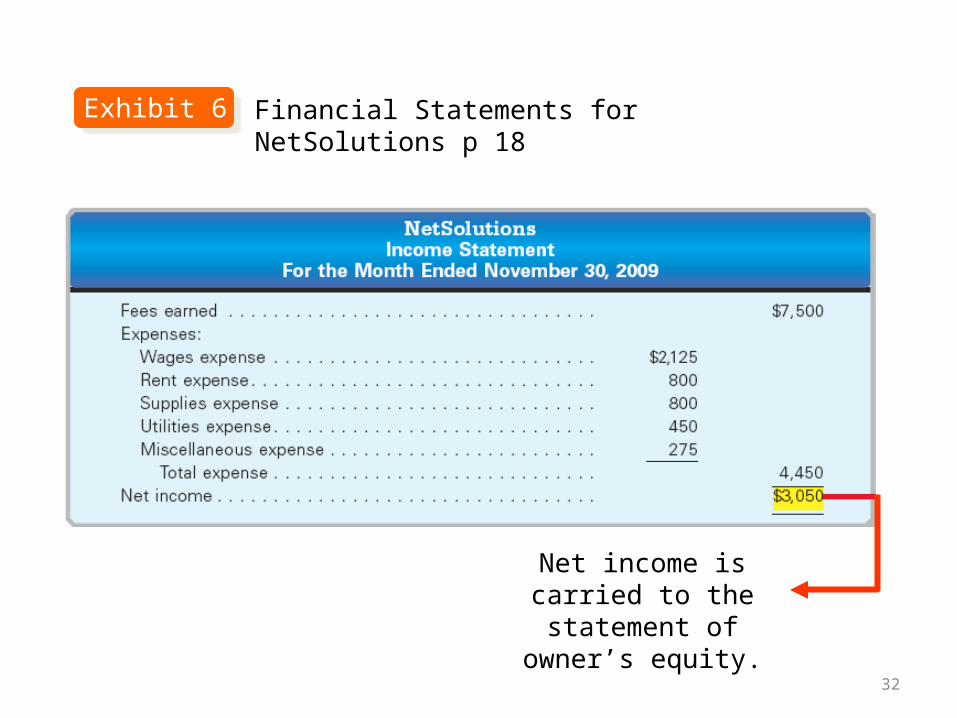

After transactions have been recorded and summarized, reports are prepared for users. The accounting reports providing this information are called financial statements.

Financial Statements

28

The income statement reports the revenues and expenses for a period of time, based on the matching concept (another concept to add to our list from page 8).

Income Statement p 16

29

The matching concept is applied by matching the expenses with the revenue generated during a period by those expenses.

Matching Concept

30

The excess of revenue over the expenses is called net income or net profit. If the expenses exceed the revenue, the excess is a net loss.

31

Net income is carried to the statement of owner’s

equity.

Financial Statements for NetSolutions p 18Exhibit 6

32

Income Statement

The assets and liabilities of Chickadee Travel Service at April 30, 2010, the end of the current year, and its revenue and expenses for the year are listed below. The capital of the owner, Adam Cellini, was $80,000 at May 1, 2009, the beginning of the current year.

Accounts payable $ 12,200 Miscellaneous expense $ 12,950Accounts receivable 31,350 Office expense 63,000Cash 53,050 Supplies 3,350Fees earned 263,200 Wages expense 131,700Land 80,000

Prepare an income statement for the current year ended April 30, 2010. (we won’t need everything they just gave us)

Example Exercise 1-4 p 16

33

CHICKADEE TRAVEL SERVICEINCOME STATEMENT

For the Year Ended April 30, 2010

Fees earned $263,200Expenses:

Wages expense $131,700Office expense 63,000Miscellaneous expense 12,950 Total expenses 207,650

Net income $ 55,550

Example Exercise 1-4 (continued)

34

The statement of owner’s equity reports the changes in the owner’s equity for a period of time.

Statement of Owner’s Equity

35

From the income statement

To the balance sheet

Exhibit 6 Financial Statements for NetSolutions p 18

36

Statement of Owner’s Equity

Using the data for Chickadee Travel Service shown in Example Exercise 1-4, prepare a statement of owner’s equity for the current year ended April 30, 2010. Adam Cellini invested an additional $50,000 in the business during the year and withdrew cash of $30,000 for personal use.

Example Exercise 1-5 p 17

CHICKADEE TRAVEL SERVICEINCOME STATEMENT

For the Year Ended April 30, 2010

Fees earned $263,200Expenses:

Wages expense $131,700Office expense 63,000Miscellaneous expense 12,950 Total expenses 207,650

Net income $ 55,55037

CHICKADEE TRAVEL SERVICESTATEMENT OF OWNER’S EQUITYFor the Year Ended April 30, 2010

Example Exercise 1-5 continued

Adam Cellini, capital, May 1, 2009 $ 80,000 Additional investment by owner during year $ 50,000Net income for the year 55,550

$105,550Less withdrawals 30,000 Increase in owner’s equity 75,550Adam Cellini, capital, April 30, 2010 $155,550

38

A balance sheet is a list of the assets, liabilities, and owner’s equity as of a specific date.Note: this is the accounting equation in a financial statement.

Balance Sheet

39

This amount is compared to the net cash flow on the statement of cash flows.

From the statement of owner’s equity

Exhibit 6 Financial Statements for NetSolutions p 18

40

Balance Sheet

Using the data for Chickadee Travel Service shown in Example Exercises 1-4 and 1-5, prepare the balance sheet as of April 30, 2010.

Example Exercise 1-6 p19

Accounts payable $ 12,200 Miscellaneous expense(IS)$12,950Accounts receivable 31,350 Office expense (IS) 63,000Cash 53,050 Supplies 3,350Fees earned (IS) 263,200 Wages expense (IS) 131,700Land 80,000

CHICKADEE TRAVEL SERVICESTATEMENT OF OWNER’S EQUITYFor the Year Ended April 30, 2010

Adam Cellini, capital, May 1, 2009 $ 80,000 Additional investment by owner during year $ 50,000Net income for the year 55,550

$105,550Less withdrawals 30,000 Increase in owner’s equity 75,550Adam Cellini, capital, April 30, 2010 $155,550

41

Example Exercise 1-6 (continued)

CHICKADEE TRAVEL SERVICEBALANCE SHEET

April 30, 2010

Cash $ 53,050 Accounts payable $ 12,200Accounts receivable 31,350Supplies 3,350 Owner’s EquityLand 80,000 Adam Cellini, capital 155,550Total assets $167,750 Total liab. & owner’s eq. $167,750

Assets Liabilities

42

A statement of cash flows is a summary of the cash receipts and payments for a specific period of time. It consists of three sections: (1) operating activities, (2) investing activities, and (3) financing activities.

**We get to this in AC116.

Statement of Cash Flows

43

This amount should match Cash on the balance sheet.

Financial Statements for NetSolutions (continued)Exhibit 6

44

Questions?Always read the Financial Analysis and Interpretation at the

end of the chapter (page 21 in chapter 1).

Your textbook exercises for this unit (due on Tuesday by 11:59 PM Eastern Time) are:

Exercise 1-7 page 31 (Example Exercise 1-2)Exercise 1-8 page 31 (use transactions on pages 11-14)

Exercise 1-12 page 32 (Example Exercise 1-3)Exercise 1-22 page 35 (Example Exercises 1-4 & 1-6)

Problem 1-3A page 37 (Problem 1-3B, solution in Doc Sharing)NOTE!!! The cash flow on Problem 1-3A is required.

Use the templates available in Doc Sharing to complete your textbook exercises. There is a set for each set of textbook exercises due this

term.45

Related Documents