Accounting cycle’s 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting cycle’s

1

Accounting cycle’s

Introduction

Purpose of Accounting

Accounting plays an important role in our economic system. The primary purpose of accounting is to provide information to the management for efficient operation of the enterprise. It is concerned with the preparation of reports, analysis and interpretations of the recorded data. Accounting is said to be the “LANGUAGE of Business”.

Accounting is a systematic process of identifying, recording, measuring, classifying, verifying, summarizing, interpreting and the value and nature of a firm’s assets, liabilities and owner’s equity. It provides useful information to the interested parties such as owners, managers, creditors and investors in decision making and controls the business affairs.

Accounting concerned primarily with:

1) Methods for recording transactions.2) Keeping financial records.3) Performing internal audits.4) Reporting and analyzing financial information to the management.5) Advising on taxation matters.

Today the accounting achieved a great importance and the whole development of commerce is depending upon it.

2

Accounting cycle’s

History of Accounting

Accounting is as old as business itself however the history of accounting cannot be exactly located. But the present accounting system was developed in 16th century, with the increase in needs and with the passage of time the exchange of commodities increased and goods becoming sold on credit then there is felt the need of maintenance of records of business transactions.

Lacus Pacioli (1445-1515) an Italian mathematician is pioneer of accounting. He is the founder of modern accounting system of bookkeeping. He wrote a comprehensive book titled “De Computiset Scripturis” published in Venice in 1494, and defined the principles of double entry system of bookkeeping on which the modern accounting system in based.

3

Accounting cycle’s

Definition of Accounting

1.The art of recording, classifying and reporting the financial data of an organization.

2.The art of collecting, processing, analyzing. Interpreting and projecting of financial information.

3. The principles or practice of systematically recording, presenting and interpreting financial accounts.

4. The systematic recording, reporting, and analysis of financial transactions of a business.

5. Accounting has also been said to provide the “Eye and Ears for management” all accounting is management accounting.

4

Accounting cycle’s

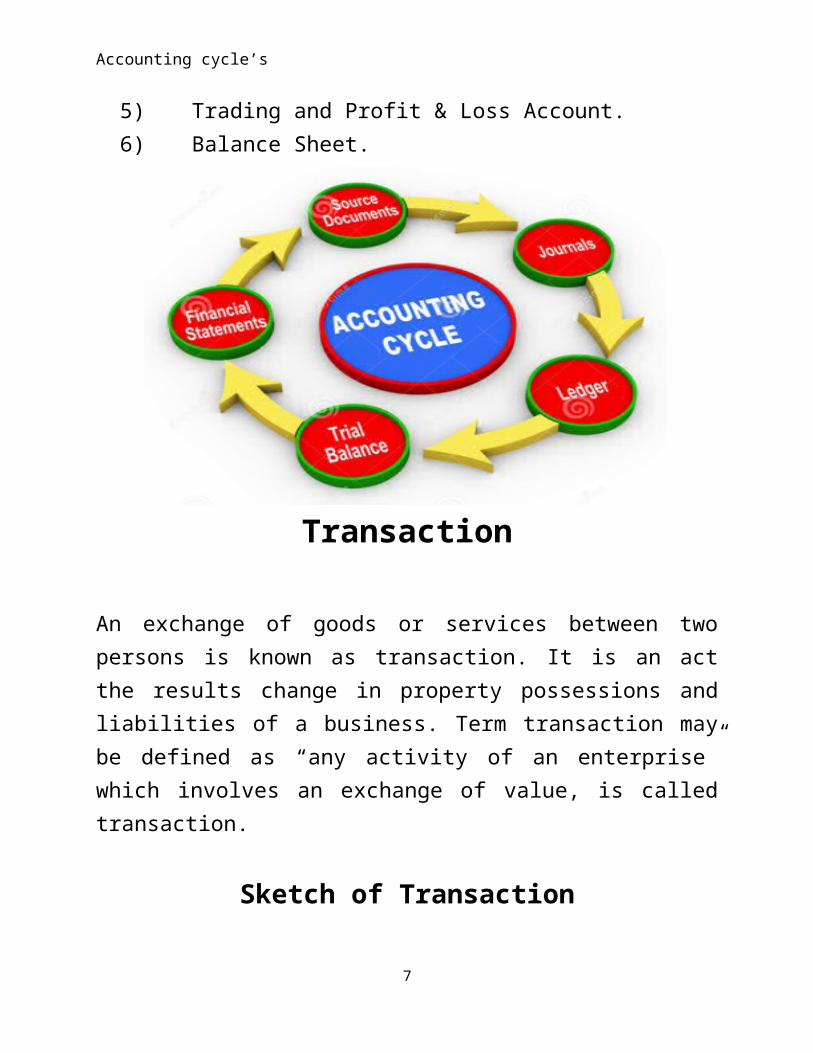

The Accounting Cycle

It is a complete sequence of accounting procedure, which is necessary to be repeated in the same order during the accounting period. It starts with the recording of transactions in the journal and ends with the preparation of balance sheet. In practical life there is a process of accounting record from a “Transaction to the Balance Sheet”.

Accounting Cycle includes the following important stages of accounting:

1) Transaction.2) Journal.3) Ledger.4) Trial Balance.5) Trading and Profit & Loss Account.6) Balance Sheet.

5

Accounting cycle’s

Transaction

An exchange of goods or services between two persons is known as transaction. It is an act the results change in property possessions and liabilities of a business. Term transaction may be defined as “any activity of an enterprise” which involves an exchange of value, is called transaction.

Sketch of Transaction

6

Accounting cycle’s

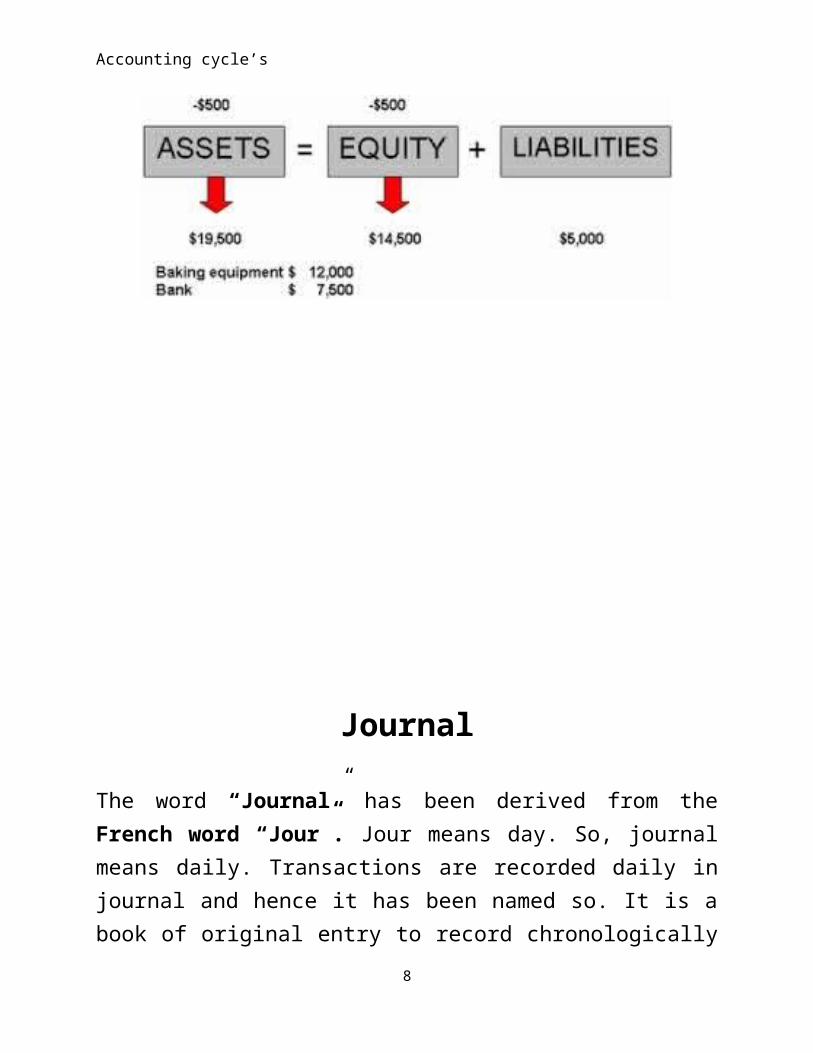

Journal

The word “Journal” has been derived from the French word “Jour”. Jour means day. So, journal means daily. Transactions are recorded daily in journal and hence it has been named so. It is a book of original entry to record chronologically (i.e. in order of date) and in detail the various transactions of a trader. It is also known Day Book because it contains the accounts of every day’s transactions. It is basically a descriptive, chorological record of day-to-day business transactions, like a diary.

Definition:1) Accounting journal where financial transactions are initially.2) An accounting record where all business transactions are originally

entered.3) Journal is a book of original entry where entries are usually

recorded in chronological order, and using the double-entry method of bookkeeping.

Sketch of Journal

7

Accounting cycle’s

Ledger

Ledger is called the king of all the books of accounts because all entries from the books of original entry must be posted to the various accounts record while ledger contains a classified record of all transactions.When all the transactions of a given period have been journalized, the next thing is to classify them according to the accounts affected. All similar transactions must be together. For instance, all transactions related to cash must be put in one place. Similarly, all transactions with a customer or a supplier must be assembled at one place. This gives a “T” shape to each individual ledger account. A “T” account showing debits on the left and credits on the right. The book in which this classification is done is called the ledger.

Definition:1) Ledger is a book of final entry where transactions are listed in

separate accounts.2) A book in which the monetary transactions of a business are posted

in the form of debits and credits.3) A book to which the record of accounts is transferred as final entry

from original posting.

Sketch of Ledger

8

Accounting cycle’s

Trial Balance

The trial balance is prepared in each financial period as a summary of the closing of the previous ledger. The total of the debit side should always be equal to the total of the credit side, which proves the arithmetic accuracy of the ledger entry. Its main and primary purpose is to check mathematical\arithmetic accuracy of accounting. Trial balance is nothing but the debit balance must be equal to credit balance.

Definition:1) The act of totaling debit balances and credit balances confirm that

total debits equal total credits.2) A trial balance is a list of all the accounts for a period, to test that

the debits agree with the credits.3) A trial balance is a list of ledger account balances prepared on a

particular date.

Sketch of Trial Balance

9

Accounting cycle’s

Trading and Profit & Loss Account

The trading and profit & loss account is one account. But it is usually divided into two sections. The first is called “trading Account” and the second section the “Profit and Loss Account.

Definition of Trading Account:

1) The main objective of preparing the trading account is to ascertain the gross profit or gross loss of accounting usually a year.

Sketch of Trading Account

10

Accounting cycle’s

Definition of Profit and Loss Account:

1) The profit and loss account can be defined as “a report that summaries the revenues and expenses of an accounting period to reflect the change in various critical areas of firm’s operation”.

Sketch of Profit and Loss Account

11

Accounting cycle’s

Balance Sheet

The balance sheet is the list of assets and claims of business prepared at some specific point of time. It shows financial position of the business sheet. A balance sheet shows the assets and liabilities grouped, properly classified and arrange in a specific manner. It normally prepared at the close of each financial year.

Sketch of Balance Sheet

12

Accounting cycle’s

References

13

Accounting cycle’s

Books:

1. Principle of Accounting

2. Financial Accounting

Websites:

1. http://www.accountingverse.com/accounting-basic/accounting-cycle.html

2. http://www.kashoo.com/accounting.../what-are-the-different-

14

Related Documents