AUDIT AND ASSURANCE Introduction To Auditing

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

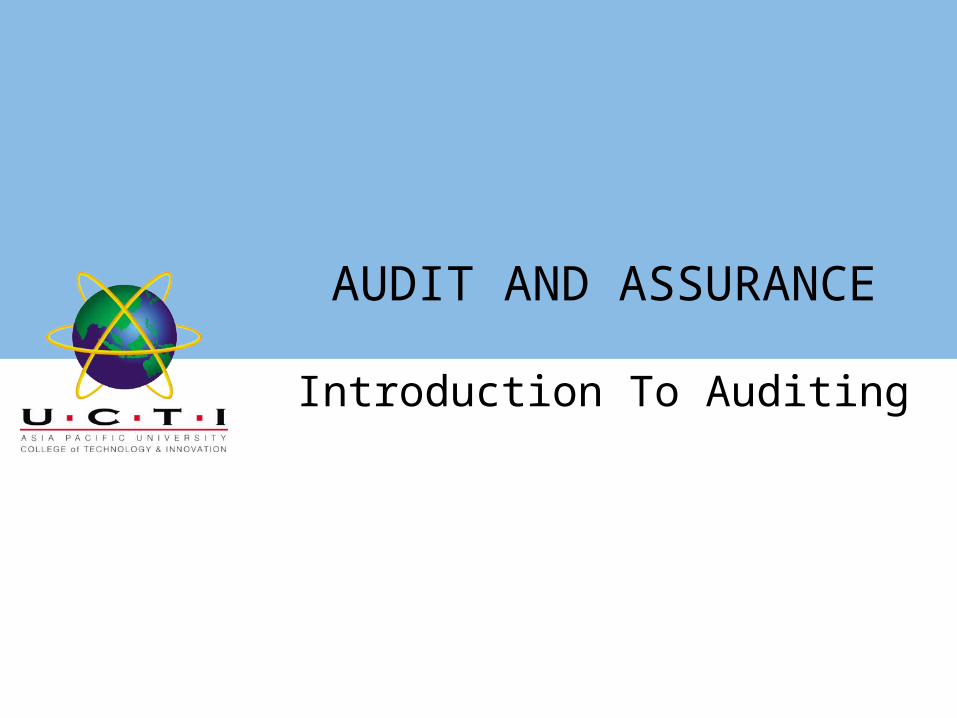

AUDIT AND ASSURANCE

Introduction To Auditing

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

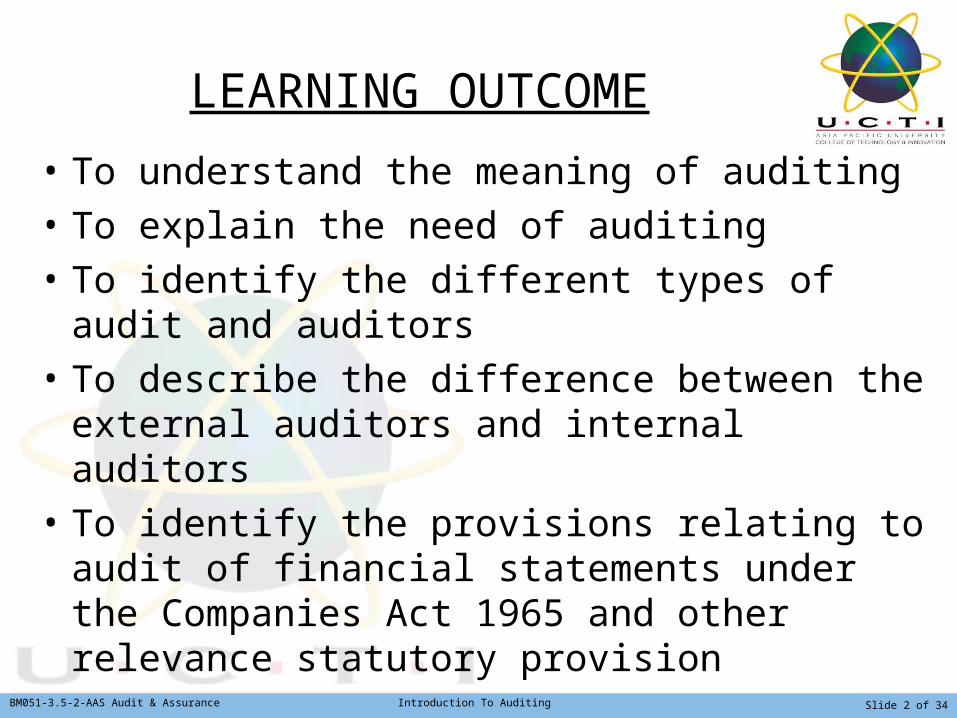

LEARNING OUTCOME• To understand the meaning of auditing• To explain the need of auditing• To identify the different types of audit and auditors

• To describe the difference between the external auditors and internal auditors

• To identify the provisions relating to audit of financial statements under the Companies Act 1965 and other relevance statutory provision

Slide 2 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

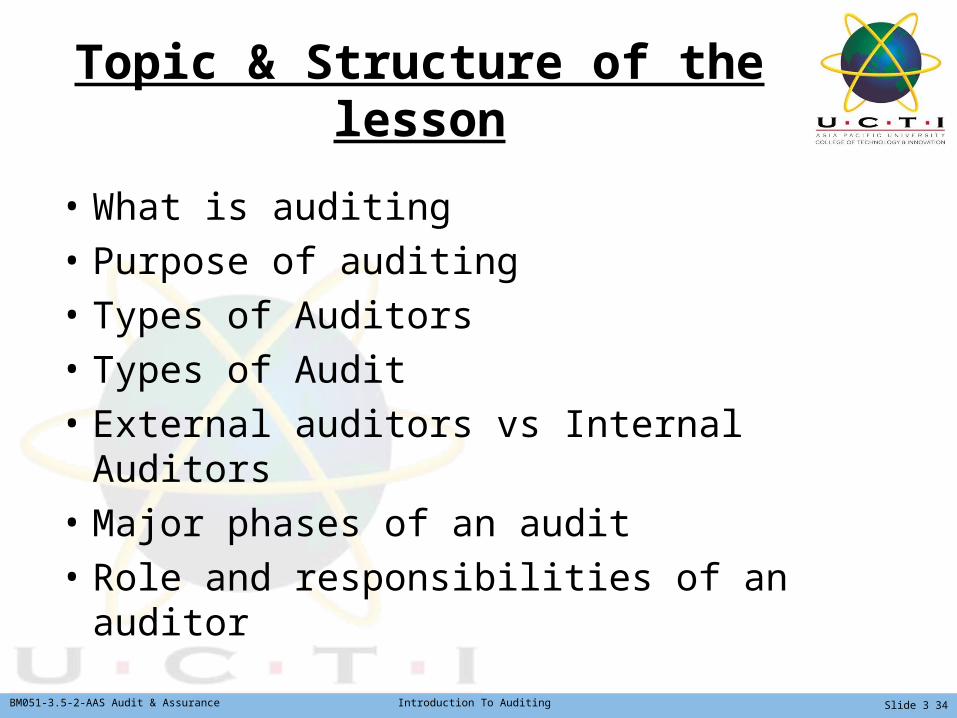

Topic & Structure of the lesson

• What is auditing• Purpose of auditing• Types of Auditors• Types of Audit• External auditors vs Internal Auditors

• Major phases of an audit• Role and responsibilities of an auditor

Slide 3 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Key Terms you must be able to use

• Accounting• Auditing• Compliance audit• Government audit• Financial statement audit• Internal auditors• Operational audit

Slide 4 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Introduction

• Auditing is The accumulation and evaluation of evidence

Against established criteriaDone by a competent and independent party

To express an opinion

Slide 5 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

The purpose of an audit

• To enable the auditor to express an opinion whether the financial statements present a true and fair view in accordance with the identified financial reporting framework

• This will enhance the credibility of financial statement

Slide 6 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Types of Auditors

• External auditors• Internal auditors• Governments auditors• Forensic auditors• Information System/Technology Auditors

Slide 7 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Types of audits

• Financial Statement auditCompulsory audit to be carried out annually

In compliance with the Financial Reporting Standards(FRS)

Companies ActInternational Standards on Auditing(ISA)

Slide 8 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Types of audits(con’t)

• Compliance AuditConformity in fulfilling official requirement

Specific procedures or rulesBy management or regulatory authority

E.g tax audit, internal audit

Slide 9 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Types of audits(con’t)

• Operational AuditEvaluating effectiveness and efficiency

Use of resourcesPerformance and improvemente.g computer usage, IT auditors

Slide 10 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Types of audits(con’t)

• Forensic auditPN4 Companies (PN means Practice Note)

Business fraud, Criminal investigation

e.g Due diligent audits, investigations

Slide 11 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

EXTERNAL AUDITORS VS INTERNAL AUDITORS

• Independent• Objective, Function, Scope• Methodology• Employment• Education background and Expertise

• Conflict of interest

Slide 12 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

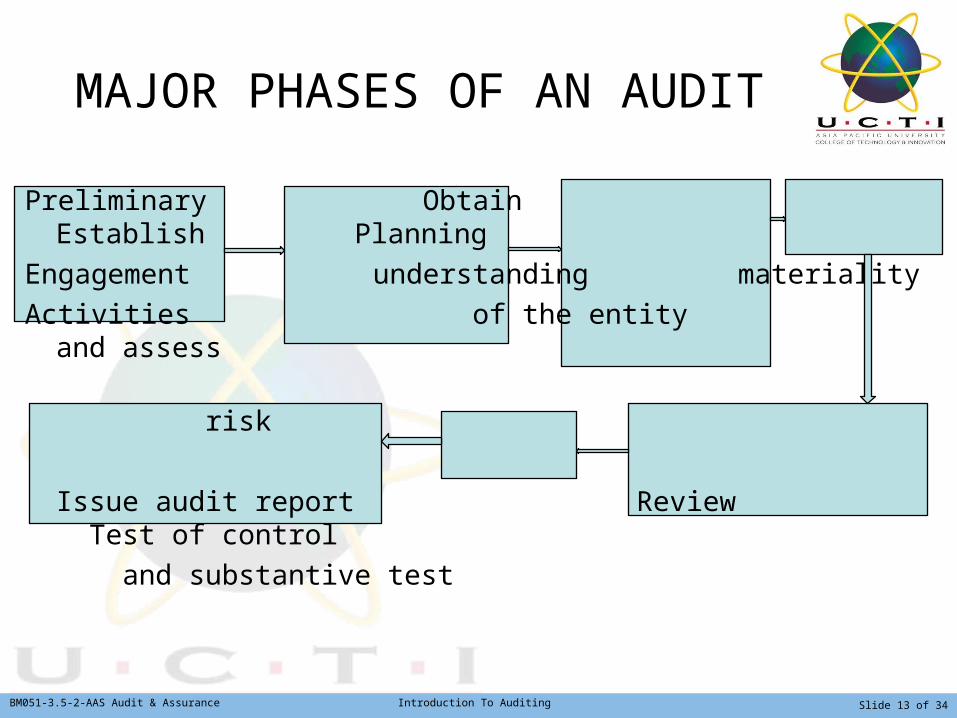

MAJOR PHASES OF AN AUDIT

Preliminary Obtain Establish Planning

Engagement understanding materialityActivities of the entity and assess

risk

Issue audit report Review Test of control and substantive test

Slide 13 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

ETHICS

• Code of conduct on moral duties and obligation

• How we should behave• MIA By-laws

Slide 14 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

INDEPENDENCE

• Auditor able to maintain an unbiased and objective attitude of mind and appearance

• Auditor must be independent and seen as independent

• 3 types of independence:Independence of mind/factIndependence in appearance

Slide 15 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

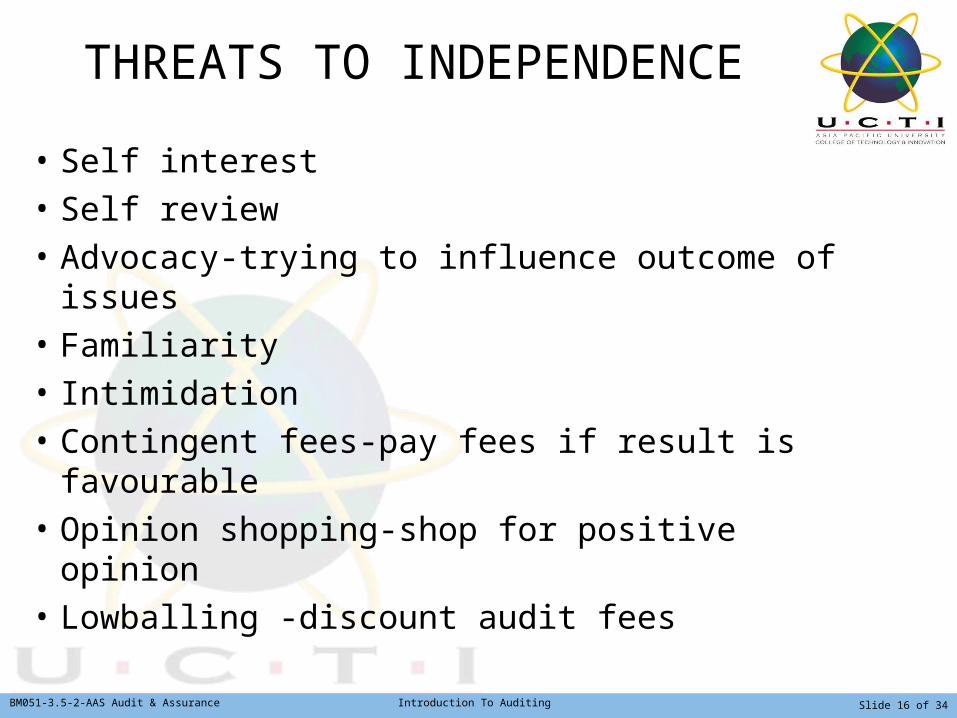

THREATS TO INDEPENDENCE• Self interest• Self review• Advocacy-trying to influence outcome of issues

• Familiarity• Intimidation• Contingent fees-pay fees if result is favourable

• Opinion shopping-shop for positive opinion

• Lowballing -discount audit fees

Slide 16 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

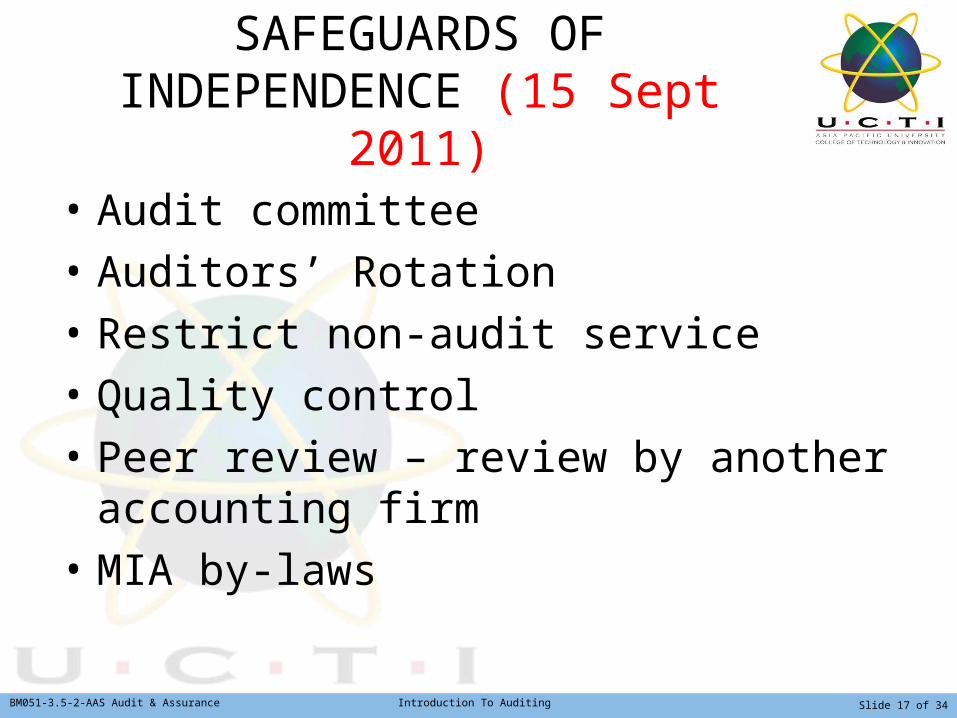

SAFEGUARDS OF INDEPENDENCE (15 Sept

2011)• Audit committee• Auditors’ Rotation• Restrict non-audit service• Quality control• Peer review – review by another accounting firm

• MIA by-laws

Slide 17 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

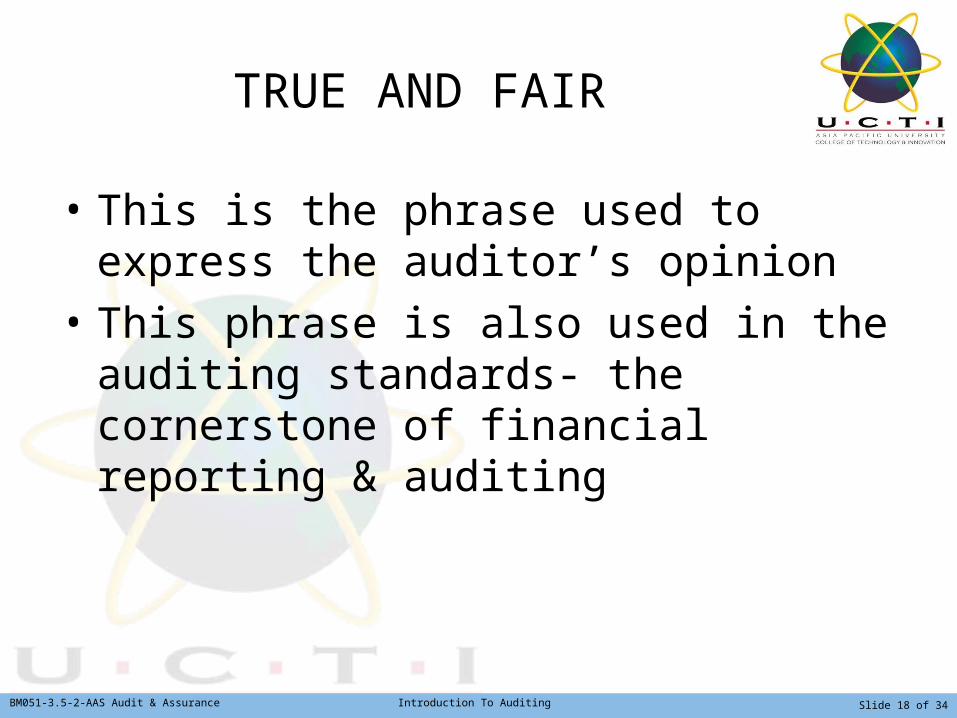

TRUE AND FAIR

• This is the phrase used to express the auditor’s opinion

• This phrase is also used in the auditing standards- the cornerstone of financial reporting & auditing

Slide 18 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

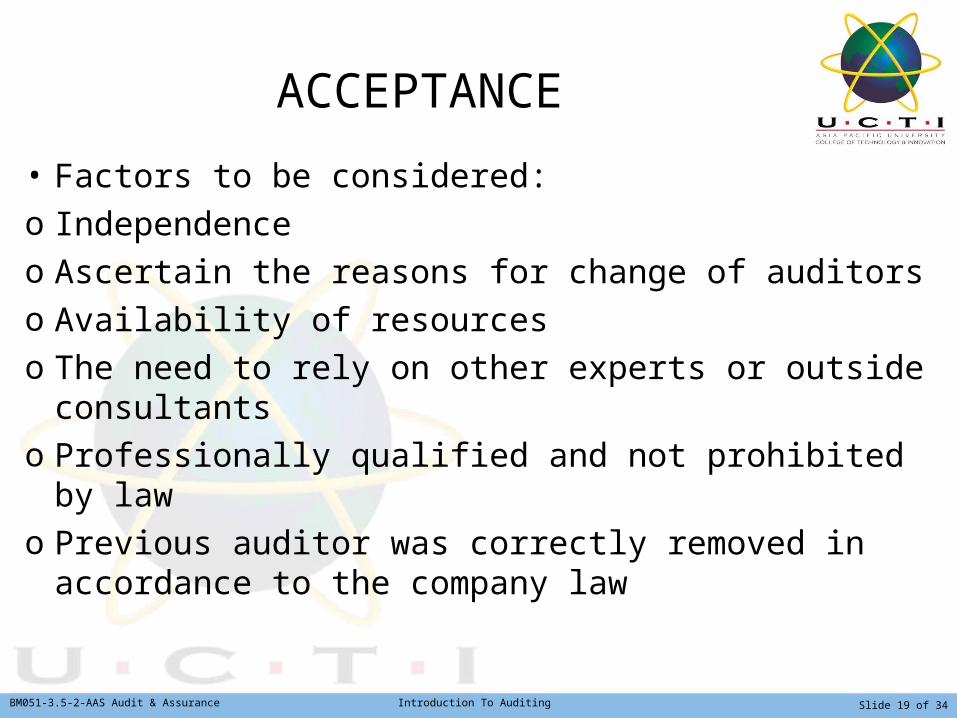

ACCEPTANCE• Factors to be considered:o Independenceo Ascertain the reasons for change of auditorso Availability of resourceso The need to rely on other experts or outside consultants

o Professionally qualified and not prohibited by law

o Previous auditor was correctly removed in accordance to the company law

Slide 19 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

FIRST APPOINTMENT

• Must be appointed by the directors within 3 months of the incorporation of the company

• Auditors to hold office until the first annual general meeting(AGM) of the company

Slide 20 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

SUBSEQUENT APPOINTMNET

• To be appointed by shareholders at each AGM (M’sian Co Act 1965 Section 172)

• Auditors to hold office from the date of appointment to the conclusion of next AGM

Slide 21 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

APPOINTMENT OF AUDITORS

• The auditors must hold the office as auditors of the company immediately before the meeting or notice of his/her nomination was properly given

Slide 22 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

SHAREHOLDERS’ RIGHT

•Shareholders are entitled in AGM to appoint an auditor other than existing auditor

Slide 23 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

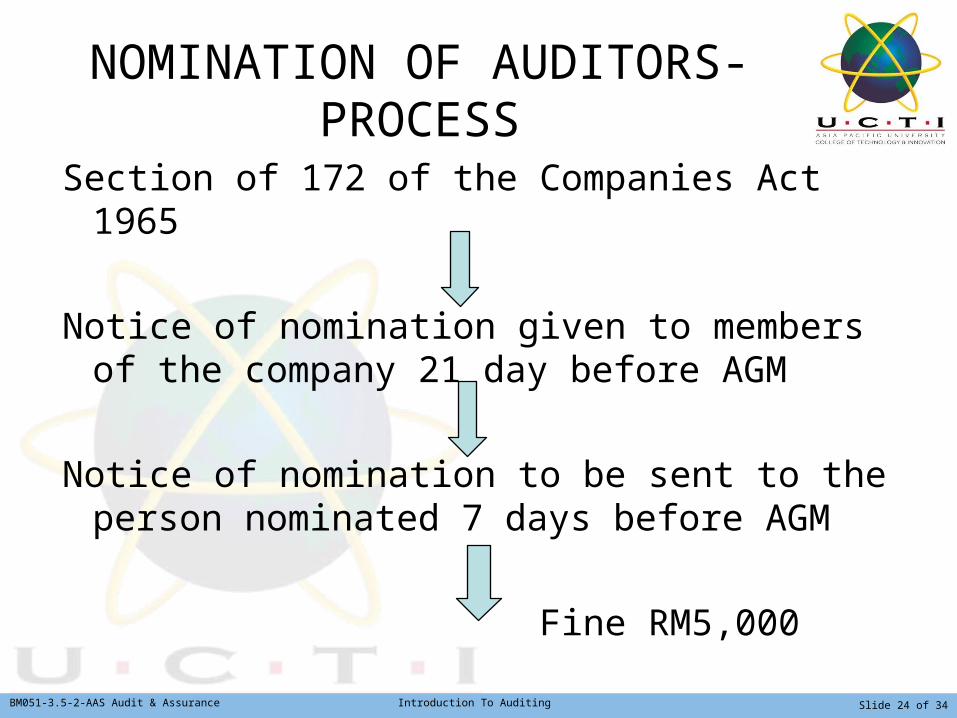

NOMINATION OF AUDITORS-PROCESS

Section of 172 of the Companies Act 1965

Notice of nomination given to members of the company 21 day before AGM

Notice of nomination to be sent to the person nominated 7 days before AGM

Fine RM5,000

Slide 24 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

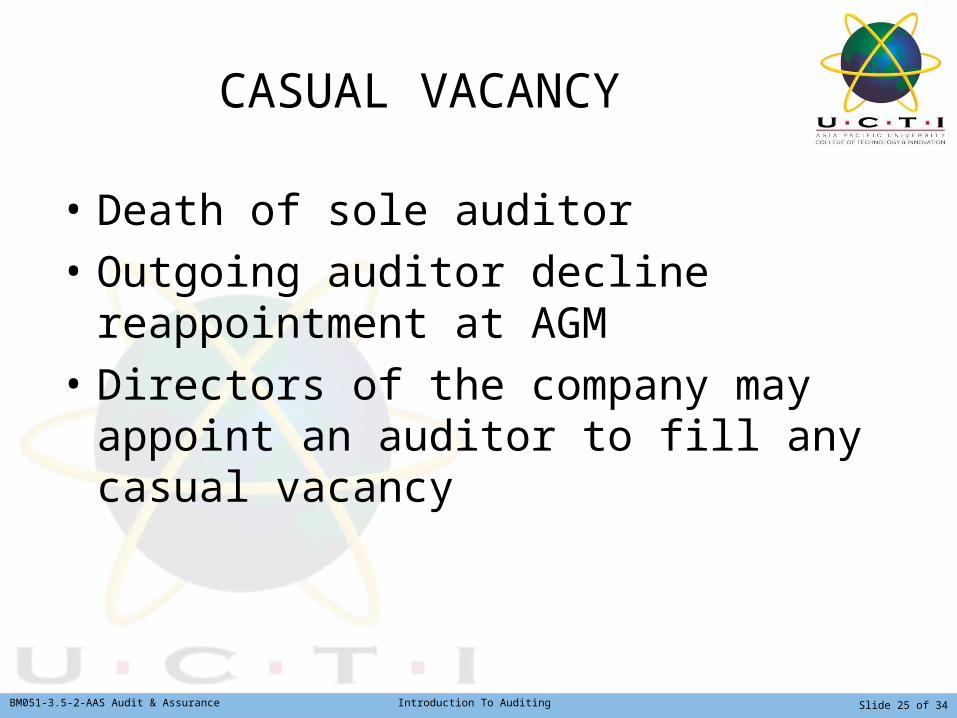

CASUAL VACANCY

• Death of sole auditor• Outgoing auditor decline reappointment at AGM

• Directors of the company may appoint an auditor to fill any casual vacancy

Slide 25 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

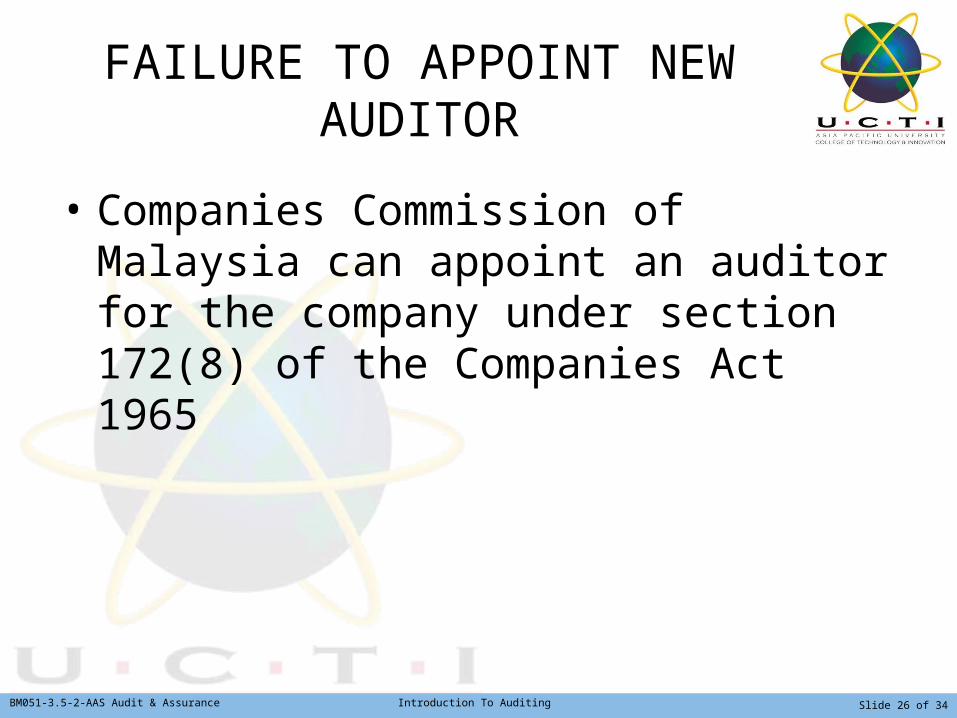

FAILURE TO APPOINT NEW AUDITOR

• Companies Commission of Malaysia can appoint an auditor for the company under section 172(8) of the Companies Act 1965

Slide 26 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

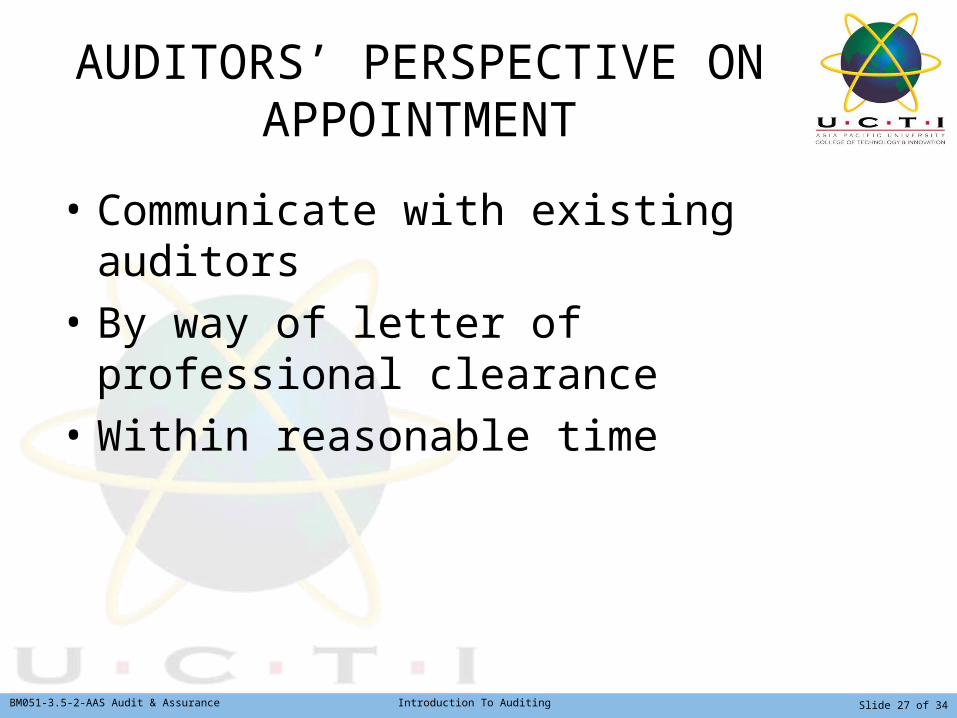

AUDITORS’ PERSPECTIVE ON APPOINTMENT

• Communicate with existing auditors

• By way of letter of professional clearance

• Within reasonable time

Slide 27 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

ENGAGEMENT LETTER

• Sent by auditor to client• Formalises the arrangement reached between the auditor and the client

• Serves as a contract, outlining the responsibility of both parties and preventing misunderstanding between the two parties

• ISA( I’ntl Std of Auditing) 210 ‘Term of Audit Engagements” provides guidance

Slide 28 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

DISQUALIFICATION OF AUDITORS – Sec. 9 Co. Act

1965• A person prohibited to act as auditor of co if:

Owe the company or its related corporations more than RM2,500

An officer of the companyA partner, employer or employee of an officer of the company

A partner, employee of an employee of an officer of the company

Slide 29 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

RESIGNATION OF AUDITORS

• Auditors will only resign from office : If he is not the sole auditor of the company

At a general meeting of the company• Written notice by the auditors• Directors must call a general meeting as soon as is practicable to appoint another auditor

• The auditor’s resignation will take effect once another auditor is appointed

Slide 30 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

REMOVAL OF AUDITORS

• By a resolution of the company at a AGM after a special notice is given

• Auditors may make representations within 7 days after receiving notice, in writing to the company dealing with the resolution for removal

• Lodge written notice of removal to registrar

• New auditors to be immediately appointed

Slide 31 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

ETHICAL CONSIDERATION• Too large/small for the client• Ethical impediment• Change in control or ownership of client company

• Fees/Unpaid fees• Non-audit work• Loss of confidence by the Board/Shareholders

• Dispute – accounting policies• Personality clash• Resources and competency

Slide 32 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Question & Answer

Slide 33 of 34

BM051-3.5-2-AAS Audit & Assurance Introduction To Auditing

Next Session (19 Sept 11)

Internal Control, Control Risks, Assessment and test of controls

Slide 34 of 34

Related Documents