Intraday Return Predictability, Informed Limit Orders, and Algorithmic Trading DARYA YUFEROVA * July 19, 2018 ABSTRACT I study the effect of algorithmic trading on the strategic choice of informed traders for market versus limit orders. I proxy for this choice by means of intraday return predictability from market and limit orders around the NYSE Hybrid Market introduction. My findings show that the increase in algorithmic trading by 16% leads to an increase in informed trading through both market and limit orders at the inner levels of the limit order book by 3.5% and 6.2%, respectively. The change in the informativeness of different order types depends on the change in the competition among algorithmic traders. JEL classification: G12, G14. Keywords: Price Discovery, Limit Order Book, Liquidity Provision, Algorithmic Trading. * Norwegian School of Economics (NHH); email address: [email protected]. I am grateful to Dion Bongaerts, Mathijs Cosemans, Sarah Draus, Thierry Foucault, Wenqian Huang, Lingtian Kong, Albert Menkveld, Marco Pagano, Christine Parlour, Loriana Pelizzon, Dominik R¨ osch, Stephen Rush, Asani Sarkar, Elvira Sojli, Mark Van Achter, Mathijs van Dijk, Wolf Wagner, Jun Uno, Marius Zoican, participants of the FMA Europe 2018, the SGF conference 2018, the NFN 2016 Young Scholars Finance Workshop, the FMA 2015 Doctoral Consortium, the PhD course on “Market Liquidity” in Brussels, and seminar participants at Gothenburg University, Goethe University, Norwegian School of Economics, Norwegian Business School, Paris Dauphine University, Erasmus University, NYU Stern, and the Tinbergen Insitute for helpful comments. I gratefully acknowledge financial support from the Vereniging Trustfonds Erasmus Universiteit Rotterdam. I am also grateful to NYU Stern and Rotterdam School of Management, Erasmus University, where some work on this paper was carried out. This work was carried out on the National e-infrastructure with the support of the SURF Foundation. I thank OneMarket Data for the use of their OneTick software.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Intraday Return Predictability, Informed Limit Orders,

and Algorithmic Trading

DARYA YUFEROVA∗

July 19, 2018

ABSTRACT

I study the effect of algorithmic trading on the strategic choice of informed traders for marketversus limit orders. I proxy for this choice by means of intraday return predictability frommarket and limit orders around the NYSE Hybrid Market introduction. My findings showthat the increase in algorithmic trading by 16% leads to an increase in informed tradingthrough both market and limit orders at the inner levels of the limit order book by 3.5%and 6.2%, respectively. The change in the informativeness of different order types dependson the change in the competition among algorithmic traders.

JEL classification: G12, G14.

Keywords: Price Discovery, Limit Order Book, Liquidity Provision, Algorithmic Trading.

∗Norwegian School of Economics (NHH); email address: [email protected]. I am grateful to DionBongaerts, Mathijs Cosemans, Sarah Draus, Thierry Foucault, Wenqian Huang, Lingtian Kong, AlbertMenkveld, Marco Pagano, Christine Parlour, Loriana Pelizzon, Dominik Rosch, Stephen Rush, Asani Sarkar,Elvira Sojli, Mark Van Achter, Mathijs van Dijk, Wolf Wagner, Jun Uno, Marius Zoican, participants of theFMA Europe 2018, the SGF conference 2018, the NFN 2016 Young Scholars Finance Workshop, the FMA2015 Doctoral Consortium, the PhD course on “Market Liquidity” in Brussels, and seminar participantsat Gothenburg University, Goethe University, Norwegian School of Economics, Norwegian Business School,Paris Dauphine University, Erasmus University, NYU Stern, and the Tinbergen Insitute for helpful comments.I gratefully acknowledge financial support from the Vereniging Trustfonds Erasmus Universiteit Rotterdam.I am also grateful to NYU Stern and Rotterdam School of Management, Erasmus University, where somework on this paper was carried out. This work was carried out on the National e-infrastructure with thesupport of the SURF Foundation. I thank OneMarket Data for the use of their OneTick software.

The limit order book is the dominant market design in equity exchanges around the

world.1 The prevalence of limit order book markets calls for a detailed understanding of

how such markets function. In particular, understanding the price discovery process on

these markets required a detailed study of the trader’s choice between submissions of market

and limit orders. The conventional wisdom in the microstructure literature used to be that

informed traders use only market orders, while uninformed traders use both market and

limit orders (see Glosten and Milgrom (1985); Kyle (1985); Glosten (1994); Seppi (1997)).

Only recent studies explicitly consider the choice of informed traders for market or limit

orders.2 Informed traders can submit a market order and experience immediate execution

at the expense of the bid-ask spread (consume liquidity). Alternatively, informed traders

can submit a limit order and thus bear the risk of non-execution, as well as the risk of

being picked off, but earn the bid-ask spread (provide liquidity). In sum, understanding

how informed trading takes place and how this process was altered by recent technological

advances are important questions to explore in modern market microstructure. In this paper,

I investigate how the increase in algorithmic trading affects the relative informativeness of

different order types.

The informational advantage of algorithmic traders (and especially their subset, high-

frequency traders) is based on superior technologies for information collection and processing,

1According to Swan and Westerholm (2006), 48% of the largest equity markets are organized as purelimit order book markets (e.g., the Australian Stock Exchange, Toronto Stock Exchange, and Tokyo StockExchange), 39% are organized as limit order books with designated market makers (e.g., the New York StockExchange (NYSE) and Borsa Italiana), and the remaining 12% are organized as hybrid dealer markets (e.g.,NASDAQ and the Sao Paulo Stock Exchange) as of the beginning of 2000.

2For theoretical studies on the choice of uninformed traders between market and limit orders, see Co-hen, Maier, Schwartz, and Whitcomb (1981), Chakravarty and Holden (1995), Handa and Schwartz (1996),Parlour (1998), Foucault (1999), Foucault, Kadan, and Kandel (2005), Goettler, Parlour, and Rajan (2005),and Rosu (2009); for theoretical studies on the choice of informed traders between market and limit orders,see Kaniel and Liu (2006), Goettler, Parlour, and Rajan (2009), and Rosu (2016); for empirical stud-ies on the choice between market and limit orders on equity markets, see Bae, Jang, and Park (2003),Anand, Chakravarty, and Martell (2005), Bloomfield, O’Hara, and Saar (2005), and Baruch, Panayides,and Venkataraman (2014); for empirical studies on the choice between market and limit orders on foreignexchange markets, see Menkhoff, Osler, and Schmeling (2010), Kozhan and Salmon (2012), and Kozhan,Moore, and Payne (2014).

1

and also on the ability to continuously monitor and respond to market conditions. Previ-

ous research has focused mainly on informed algorithmic trading via market orders. Only

Brogaard, Hendershott, and Riordan (2017) examine informed trading via both market and

limit orders by a subset of algorithmic traders (high-frequency traders). They document that

high-frequency traders contribute to price discovery mainly through limit orders. However,

they do not establish the causal effect of high-frequency trading on the relative informative-

ness of different order types, which is crucial given the increasing trend of high-frequency

traders’ participation in modern markets.

In order to establish causal effects of algorithmic traders on the relative informativeness of

order types, I follow the approach of Hendershott, Jones, and Menkveld (2011) and use NYSE

Hybrid Market introduction as an instrumental variable to help determine the causal effects

of algorithmic trading activity on the choice made by informed traders. The introduction

of the NYSE Hybrid Market was a permanent technological change in market design that

resulted in increased automation and speed of trading (Hendershott and Moulton (2011)).

The rollout of stocks to the NYSE Hybrid Market was implemented in a staggered way

from October 2006 through January 2007, which allows for a causal effect identification. I

proxy for algorithmic trading activity by means of the ratio of best bid-offer quote updates

relative to the daily trading volume following Hendershott, Jones, and Menkveld (2011) and

Boehmer, Fong, and Wu (2015), and I proxy for the relative informativeness of different

order types by means of intraday return predictability using tick-by-tick consolidated trade

and quote data and data on the first 10 best levels of the NYSE limit order book from the

Thomson Reuters Tick History (TRTH) database.

Naturally, orders submitted by informed traders contain information about future price

movements. If an informed trader actively uses market orders, an imbalance between buyer-

and seller-initiated volume may be informative about future price movements. If an informed

trader actively uses limit orders, the limit order book may contain information that is not

yet incorporated into the price. Therefore, strategies employed by informed traders may

2

induce intraday return predictability from market and limit order flows alike.

I develop two alternative hypotheses of the effects of algorithmic trading on informed

traders’ choices: the competition hypothesis and the efficient technology hypothesis. Com-

petition between algorithmic traders for (trading on) the same information makes market

orders more attractive to them because they guarantee immediate execution (the compe-

tition hypothesis). The technological advantage of algorithmic traders makes limit orders

more attractive to them because they are able to reduce pick-off risks better than the other

market participants (the efficient technology hypothesis).

The results show that the increase in algorithmic trading activity leads to increases in

the relative informativeness of market order imbalance and depth imbalance at the inner

levels of the limit order book by 3.5% and 6.2% relative to the sample average, respectively.

The relative importance of the depth imbalances at the deeper levels of the limit order book

decreases. The latter is in line with the anecdotal evidence that algorithmic traders tend

to acquire short-lived information, and thus operate mainly at the inner levels of the limit

order book.

Furthermore, I show that the relative importance of market order imbalance increases

significantly only for small and mid-cap stocks by 3.4% and 5.2% relative to the sample

average, while the relative importance of the limit orders at the inner levels of the limit order

book increases significantly only for mid-cap and large stocks by 5.6% and 15.9% relative

to sample average, respectively. The former findings are consistent with the competition

hypothesis, while the latter findings are consistent with the efficient technology hypotheses.

One potential explanation for such phenomena is that large stocks are likely to be more

saturated with algorithmic traders, and thus less likely to exhibit new algorithmic traders

entering the market than smaller stocks are.3 Therefore, the competition hypothesis is more

3Hagstromer and Norden (2013), Brogaard, Hendershott, and Riordan (2014), ESMA (2014), andAvramovic, Lin, and Krishnan (2017) document that algorithmic traders (especially high-frequency traders)are more present in large stocks than in small stocks. In addition, Baron, Brogaard, Hagstromer, and Kir-ilenko (2017) show that there are strong entry barriers in high-frequency traders’ business, and therefore,

3

profound in smaller stocks, while the efficient technology hypothesis is more profound in

large stocks. Put differently, the overall effect of algorithmic traders on the choice of the

order types used for informed trading depends on the change in the amount of competition

between them.

My main contribution to the literature is twofold. First, I contribute to the literature on

intraday return predictability by documenting that the main source of the intraday return

predictability is private information embedded in limit orders for a wide cross-section of

stocks. Among other papers studying intraday return predictability from limit order book

are Kavajecz and Odders-White (2001); Bae, Jang, and Park (2003); Anand, Chakravarty,

and Martell (2005); Harris and Panchapagesan (2005); Kaniel and Liu (2006); Cao, Hansch,

and Wang (2009); Baruch, Panayides, and Venkataraman (2014); Cenesizoglu, Dionne, and

Zhou (2014); and Putnins and Michayluk (2015). However, these papers focus only on the

limited amount of stocks (mainly the largest and most actively traded stocks).

Second, my paper contributes to the ongoing debate on the effect of algorithmic traders

(especially high-frequency traders) on market quality. Among other papers taking part in

this debate are McInish and Upson (2012); Hagstromer and Norden (2013); Hirschey (2013);

Brogaard, Hendershott, and Riordan (2014); Biais, Foucault, and Moinas (2015); Jovanovic

and Menkveld (2015); Foucault, Hombert, and Rosu (2016); and Foucault, Kozhan, and

Tham (2017). Biais and Foucault (2014), O’Hara (2015), and Menkveld (2016) provide a

comprehensive review of papers on high-frequency trading activity and market quality. While

Brogaard, Hendershott, and Riordan (2017) show that high-frequency traders actively use

limit orders for informed trading, my paper is the first one to establish a causal relation

between algorithmic trading and the informativeness of different order types.4 My evidence

the degree of competition largely remains constant for top 25 Swedish stocks.4My paper is closely related to Hendershott, Jones, and Menkveld (2011), who also look at the causal

effect of algorithmic trading on price changes related and unrelated to trading. They come to the conclusionthat large stocks exhibit an increase in price discovery not related to trading activity. However, theydocument a confounded effect of inventory costs and information incorporated in the quotes, and additionallyfocus only on the best bid-offer level, thus not taking into account information embedded in deeper levels of

4

shows that an increased degree of algorithmic trading activity leads to an increased usage of

both informed market and informed limit orders at the inner levels of the limit order book

accompanied by a decreased usage of informed limit orders at the deeper levels of the limit

order book. The ultimate effect of algorithmic trading activity on the way price discovery

takes place depends on the competition among them.

The paper is structured as follows. Section I develops the hypotheses. Section II discusses

the data and methodology used in the paper. Section III provides the main empirical results.

Section IV contains additional analysis. Section V concludes.

I. Hypotheses

In this section, I develop the hypotheses for the effects of algorithmic trading on the

choice between limit and market orders by informed traders. Under the traditional view

(see, e.g., Glosten and Milgrom (1985); Kyle (1985); Glosten (1994); and Seppi (1997)), only

market orders are used for informed trading, which may be an inadequate approximation of

reality. Later studies build upon this initial work and allow both informed and uninformed

traders to choose between the order types (Kaniel and Liu (2006); Goettler, Parlour, and

Rajan (2009); Rosu (2016)).

Based on theoretical predictions from Goettler, Parlour, and Rajan (2009), an informed

trader who receives good news about a stock has three different options to exploit this

information. First, the trader can submit a buy market order and consume liquidity. Second,

the trader can submit a limit buy order at the inner levels of the bid side of the limit order

book (this limits execution probability, but saves transaction costs). Third, the trader can

also submit a limit sell order at the outer levels of the ask side of the limit order book, in

combination with one of the two other order options, to lock in the benefit from the price

difference. The opposite is true for the bad-news scenario.

the limit order book.

5

During the past decade, a new group of market participants — algorithmic traders — has

emerged and evolved into a dominant player responsible for the majority of trading volume.

Algorithmic trading “is thought to be responsible for as much as 73% of trading volume in

the United States in 2009” (Hendershott, Jones, and Menkveld (2011), p. 1). Therefore, it

is natural to ask what role algorithmic traders are playing in the price discovery process and

to what extent their presence affects the informed trader’s choice between market and limit

orders.

Possessing private information is equivalent to having the capacity to absorb and analyze

publicly available information (including information from the past order flow) faster than

other market participants (Foucault, Hombert, and Rosu (2016); Foucault, Kozhan, and

Tham (2017); Menkveld and Zoican (2017)). Efficient information-processing technology is

a distinct feature of algorithmic traders, hence they are more likely to be informed than

other market participants. However, ex ante, it is not clear whether algorithmic traders

would prefer to use market or limit orders to profit from their informational advantage.

On the one hand, competition among informed traders will lead to a faster price discov-

ery and a shorter lifespan for the information obtained by the informed trader. Algorithmic

traders compete for the same information by processing the same news releases or by ana-

lyzing past order flow patterns as fast as possible. In a competitive market, a trader must

be the first in line to trade on information in order to profit from it. Given that only mar-

ket orders can guarantee immediate execution, algorithmic traders may be inclined to use

market orders for informed trading.

On the other hand, limit orders are attractive for traders who can accurately predict

execution probabilities, continuously monitor the market, and quickly adapt to market con-

ditions. Algorithmic traders possess all of these characteristics. Thus, they may be inclined

to use limit orders for informed trading.

Therefore, I formulate two alternative hypotheses for the effect of increase in algorithmic

trading on the informed traders’ choice between market and limit orders.

6

HYPOTHESIS 1: With the increase in algorithmic trading activity, the proportion of price

discovery that occurs via market orders increases. (The competition hypothesis)

HYPOTHESIS 2: With the increase in algorithmic trading activity, the proportion of price

discovery that occurs via limit orders increases. (The efficient technology hypothesis)

II. Data and method

In this section, I describe my data and variables (see Section II.A) as well as methodology

to identify the causal effects of algorithmic trading on the choice of order types used for

informed trading (see Section II.B).

A. Data and variables

I obtain the data for the period from June 2006 till May 2007. I obtain intraday data on

trades and best bid-offer quotes as well as the 10 best levels of the limit order book for the

U.S. market from the TRTH database. The TRTH database is provided by the Securities

Industry Research Centre of Asia-Pacific (SIRCA). The limit order book data provided

by TRTH does not include order-level information (e.g., it contains no order submission,

revision, or cancellation details), only the 10 best price levels and the depth on bid and ask

sides of the book that are visible to the public. The data for limit order book comes from

the NYSE. The data for trades and best bid-offer quotes comes from the consolidated tape.

In other words, the best bid-offer reported in the data is the best bid-offer for any exchange

in the U.S.

TRTH data are organized by Reuters Instrumental Codes (RICs), which are identical to

TICKERs provided by the Center for Research in Security Prices (CRSP). Merging data

from CRSP and TRTH allows me to identify common shares that indicate the NYSE as

their primary exchange and to use company-specific information (e.g., market capitalization

7

and turnover). This study is limited to NYSE-listed stocks only due to the limit order book

data availability. I require all stocks to be present in CRSP database for the whole sample

period. I discard stocks with an average monthly price bigger than $1,000 and smaller than

$5. I winsorize all the variables at the 95% level (2.5% at the each tail of the distribution).

For the purpose of further analysis, I aggregate intraday data from TRTH in the follow-

ing way. I compute one-minute mid-quote returns and market order imbalances, and take

snapshots of the limit order book at the end of each one-minute interval. I filter the intraday

data following Rosch, Subrahmanyam, and Van Dijk (2016). First, I discard trades, quotes,

and limit order book data that are not part of the continuous trading session. Continuous

trading session hours for NYSE are 9:30-16:00 ET and they remain unchanged during the

sample period. Second, I discard block trades (i.e., trades with a trade size greater than

10,000 shares) because these trades are likely to receive special treatment. Third, I discard

data entries that are likely to be faulty. Faulty entries include entries with negative or zero

prices or quotes; entries with a negative bid-ask spread; entries with a proportional bid-ask

spread bigger than 25%; and entries that have a trade price, bid price, or ask price that

deviates from the 10 surrounding ticks by more than 10%. In addition, I require that at

least five levels of the limit order book are available in the end of each one-minute interval.

For a stock-day to enter my sample, at least 100 valid one-minute intervals with at least one

trade are required. If there are less than 200 days in my sample period for a particular stock,

I exclude this stock from the analysis. Overall, I am left with 944 common NYSE-listed

stocks.

A.1. Proxy for algorithmic trading

My data does not allow me to identify algorithmic traders directly. However, anecdotal

evidence suggests that algorithmic traders tend to send multiple messages per each individual

transaction. Therefore, I consider the following two proxies for algorithmic trading activity in

8

the spirit of Hendershott, Jones, and Menkveld (2011) and Boehmer, Fong, and Wu (2015):

QTE/DV OL, a daily number of best bid-offer quote updates relative to daily trading volume

(in $10,000) and QTE/TRD, a daily number of best bid-offer quote updates relative to the

daily number of transactions. I use theQTE/DV OL in a baseline analysis, whileQTE/TRD

is used for robustness check.

A.2. Proxy for order-type informativeness

I use intraday predictive regressions to proxy for the informational content of different

order types. I construct intraday data on returns, market order imbalances (MOIB)5, and

limit order book imbalances at a one-minute frequency. For all the variables, I discard

overnight observations. I use these variables to predict returns one minute ahead.

I follow Chordia, Roll, and Subrahmanyam (2008) and compute one-minute log returns

(Ret) based on the prevailing mid-quotes (the average of the bid and ask prices) at the end of

the one-minute interval, rather than the transaction prices or mid-quotes matched with the

last transaction price. In this way, I avoid the bid-ask bounce and ensure that the returns

for every stock are indeed computed over a one-minute interval. I implicitly assume that

there are no stale best bid-offer quotes in the sample, and thus I consider a quote to be valid

until a new quote arrives or until a new trading day starts.

To calculate a one-minute MOIB, I match trades with quotes and sign trades using the

Lee and Ready (1991) algorithm. TRTH data are stamped to the millisecond, therefore the

Lee and Ready (1991) algorithm is quite accurate. In particular, a trade is considered to be

buyer initiated (seller initiated) if it is closer to the ask price (bid price) of the prevailing

quote. For each one-minute interval, I aggregate the trading volume in USD for buyer- and

seller-initiated trades separately at the stock level. Thereafter, I subtract seller-initiated

dollar volume from buyer-initiated dollar volume to obtain MOIB and normalize it by the

5Market order imbalance is based on both market and marketable limit orders.

9

total trading volume. For stock i on date d at one-minute interval t,

MOIBi,d,t =Buyer initiated volumei,d,t − Seller inititated volumei,d,tBuyer initiated volumei,d,t + Seller inititated volumei,d,t

(1)

There are multiple ways to describe the limit order book. Most of the papers that study

intraday return predictability either focus on different levels of the limit order book or on the

corresponding ratios of these levels between the ask and bid sides of the limit order book.

For instance, Wuyts (2008), Cao, Hansch, and Wang (2009), and Cenesizoglu, Dionne, and

Zhou (2014) use slopes and depth at different levels of the limit order book to summarize

its shape. However, due to variation in the shape of the limit order book as well as in the

number of available levels of the limit order book, I believe that definition of inner, middle,

and outer levels by means of a relative threshold is more suitable than definition by means

of the number of levels in the limit order book (e.g., levels from 1 to 3 are inner levels, levels

from 4 to 6 are middle levels, and levels from 7 to 10 are outer levels).

Examples of a relative approach to limit order book description are Cao, Hansch, and

Wang (2009), who also use volume-weighted average price for different order sizes to describe

the limit order book, and Kavajecz and Odders-White (2004), who use a so-called “near-

depth” measure, which is a proportion of the depth close to the best bid-offer level relative

to the cumulative depth within a certain price range.

For the purpose of testing the private information hypothesis, I focus on the ratios of

depth concentrated at inner, middle, and outer levels of the limit order book between the

ask and bid sides. I use a modification of the “near-depth” measure introduced by Kavajecz

and Odders-White (2004). First, I compute a snapshot of the ask and bid sides of the limit

order book at the end of each one-minute interval. Then, I define the inner levels as price

levels between the mid-quote and one-third of the minimum across bid and ask sides of the

total distance between the 10th available limit price and the mid-quote. Outer levels are

defined as price levels above two-thirds of the minimum across bid and ask sides of the total

10

distance between the 10th available limit price and the mid-quote. I refer to the remaining

levels as middle levels of the limit order book. For stock i on date d at one-minute interval

t,

Heighti,d,t = min[(PAsk,10i,d,t −MidQuotei,d,t), (MidQuotei,d,t − PBid,10

i,d,t )] (2)

Inneri,d,t =

∑10k=1Depth

Bid,ki,d,t ∗ 1(|PBid,k

i,d,t −MidQuotei,d,t| <= 13Heighti,d,t)−∑10

k=1DepthBid,ki,d,t ∗ 1(|PBid,k

i,d,t −MidQuotei,d,t| <= 13Heighti,d,t)+

−DepthAsk,ki,d,t ∗ 1(|PAsk,k

i,d,t −MidQuotei,d,t| <= 13Heighti,d,t)

+DepthAsk,ki,d,t ∗ 1(|PAsk,k

i,d,t −MidQuotei,d,t| <= 13Heighti,d,t)

(3)

Middlei,d,t =

∑10k=1Depth

Bid,ki,d,t ∗ 1(1

3Heighti,d,t < |PBid,k

i,d,t −MidQuotei,d,t| <= 23Heighti,d,t)−∑10

k=1DepthBid,ki,d,t ∗ 1(1

3Heighti,d,t < |PBid,k

i,d,t −MidQuotei,d,t| <= 23Heighti,d,t)+

−DepthAsk,ki,d,t ∗ 1(1

3Heighti,d,t) < |PAsk,k

i,d,t −MidQuotei,d,t| <= 23Heighti,d,t)

+DepthAsk,ki,d,t ∗ 1(1

3Heighti,d,t) < |PAsk,k

i,d,t −MidQuotei,d,t| <= 23Heighti,d,t)

(4)

Outeri,d,t =

∑10k=1Depth

Bid,ki,d,t ∗ 1(|PBid,k

i,d,t −MidQuotei,d,t| > 23Heighti,d,t)−∑10

k=1DepthBid,ki,d,t ∗ 1(|PBid,k

i,d,t −MidQuotei,d,t| > 23Heighti,d,t)+

−DepthAsk,ki,d,t ∗ 1(|PAsk,k

i,d,t −MidQuotei,d,t| > 23Heighti,d,t)

+DepthAsk,ki,d,t ∗ 1(|PAsk,k

i,d,t −MidQuotei,d,t| > 23Heighti,d,t)

(5)

My relative approach allows me to define in a unified fashion the levels that are close to

the best bid-offer level, as well as the levels that are far away from the best bid-offer level

across stocks and through time.

In order to estimate order-type informativeness, I run stock-day predictive regressions

at a one-minute frequency using one-minute mid-quote returns as the dependent variable.

As explanatory variables, I use lagged returns, lagged market order imbalance (MOIB),

and lagged depth imbalances at the inner, middle, and outer levels of the limit order book.

Controlling for lagged returns allows me to differentiate between temporary effect (inventory

11

management) and permanent effect (private information). The regression equation for each

stock i on day d is given by:

Reti,d,t = α + β1Reti,d,t−1 + β2MOIBi,d,t−1+

+ β3Inneri,d,t−1 + β4Middlei,d,t−1 + β5Outeri,d,t−1 + εt(6)

For each stock-day I proxy for order-type informativeness by contribution of the each

variable to the R2 of the predictive regressions averaged across all possible orderings of the

variables as in Lindeman, Merenda, and Gold (1980).

B. Instrumental variable approach

The main contribution of this study is the identification of causal effects of algorithmic

trading on the relative informativeness of different order types. Identifying the causal effects

of the algorithmic trading activity is not a trivial task, as the degree of algorithmic trading

activity in each stock on each day is an endogenous choice made by the algorithmic trader.

Therefore, I adopt an instrumental variable approach following Hendershott, Jones, and

Menkveld (2011) to identify the causal effects of the algorithmic trading on the choice of

order types used for informed trading.

I focus on the period surrounding the introduction of the NYSE Hybrid Market – an

exogenous change in market design that led to increased speed and automation of the NYSE

– from June 2006 till May 2007 (following Hendershott and Moulton (2011)).6 Among

other changes, after the NYSE Hybrid Market’s introduction, orders were allowed to “walk”

through the limit order book automatically; before this technological change, market orders

were executed automatically at the best bid-offer level only. I obtain data on the NYSE

Hybrid Market’s rollout, which was when the actual increase in the degree of automated

6I prefer the introduction of the NYSE Hybrid Market to the Autoquote introduction used in Hender-shott, Jones, and Menkveld (2011) because the effects of Autoquote’s introduction are likely to be con-taminated by the recent effects of making the NYSE limit order book publicly available as of January 24,2002.

12

execution and speed took place, from Terrence Hendershott’s website. This rollout was

implemented in a staggered way from October 2006 through January 2007 (see Figure 1),

which allows for a causal effect identification.

INSERT FIGURE 1 HERE

I follow Hendershott, Jones, and Menkveld (2011) and estimate the following IV panel

regression with stock and day fixed effects (implicit difference-in-difference approach) and

with standard errors clustered by stock:

Yi,d = αi + γd + β1ATi,d + β2MCAPi,m−1 + β3(1/PRCi,m−1)+

+ β4Turnoveri,m−1 + β5PQSPRi,m−1 + β6Rangei,m−1 + εi,d

(7)

where Yi,d is the contribution of each variable to the R2 of predictive regressions (see equation

(6)) averaged across all possible orderings of the variables as in Lindeman, Merenda, and

Gold (1980) for stock i on day d, and αi and γd are stock and day fixed effects, respectively.

ATi,d is a proxy for algorithmic trading activity for stock i on day d (the daily number of

quotes relative to daily trading volume in USD 10,000, QTE/DV OL). In addition, I control

for the daily log of market capitalization in billions (MCAPi,m−1), inverse of price (1/Pi,m−1),

annualized turnover (Turnoveri,m−1), closing quoted spread (PQSPRi,m−1), and the square

root of high minus low range (Rangei,m−1) averaged over the previous month, m− 1. As a

set of instruments, I use all explanatory variables with ATi,d replaced by Hybridi,d, a dummy

variable that equals one if the stock i on day d is rolled out to the NYSE Hybrid Market

and 0 otherwise.

III. Empirical results

In this section, I discuss my empirical results. First, I provide summary statistics for

the algorithmic trading activity in my sample (see Section III.A). Second, I document the

13

informativeness of different order types (see Section III.B). Finally, I analyze the effect of

algorithmic trading on the informativeness of different order types (see Section III.C).

A. Algorithmic trading activity

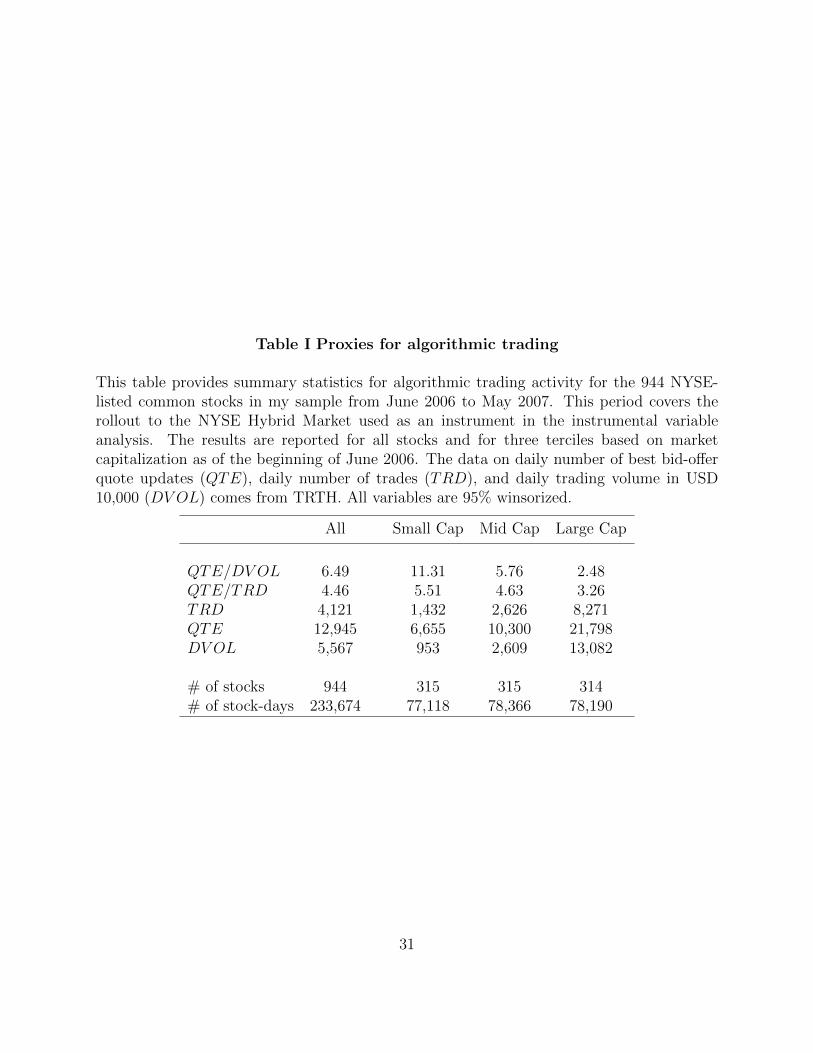

I present the average proxies for algorithmic trading activity (averaged across stock-days)

in Table I for the whole sample of 944 stocks and for different market capitalization terciles

(based on market capitalization in the beginning of June 2006). I show that amounts of best

bid-offer quote updates, trades, and trading volume increase monotonically from small-cap

stocks to large-cap stocks from 6,655 to 21,798 quote updates, from 1,432 to 8,271 trades,

and from USD 9,530,000 to USD 130,820,000, respectively. On average, in my sample,

for each USD 10,000 of daily trading volume, I observe 6.49 best bid-offer quote updates,

and for each trade, I observe 4.46 best bid-offer quote updates. For instance, Hendershott,

Jones, and Menkveld (2011) document 5.42 electronic messages for each USD 10,000 of

daily trading volume for the largest stocks quantile, while the corresponding statistic of the

largest tercile in my data is 2.48. I note that my measure is different from the one used

in Hendershott, Jones, and Menkveld (2011) as I do not have access to the whole order

history (i.e., submission, modification, and cancellation) and I use only updates at the best

bid-offer level. In other words, the number of electronic messages for each USD 10,000 must

be by definition higher than number of the best bid-offer quote updates. I also note that the

changes in the algorithmic trading measure from large-cap stocks to small-cap stocks are in

line with those documented by Hendershott, Jones, and Menkveld (2011).

INSERT TABLE I HERE

B. The informativeness of different order types

Table II presents the estimation results of the predictive stock-day regressions of one-

minute mid-quote returns on one-minute lagged mid-quote returns, one-minute lagged mar-

14

ket order imbalances, and one-minute lagged depth imbalances at the inner, middle, and

outer levels of the limit order book (see equation (6)) for the whole sample and market capi-

talization terciles. Controlling for lagged returns allows me to separate inventory effects from

the effects of private information, as information should result in a permanent price change. I

discuss the whole sample results only as the results for different market capitalization terciles

are in line with the results of the whole sample.

INSERT TABLE II HERE

Panel A of Table II reports average coefficients together with the proportion of the regres-

sions that have significant individual t-statistics. MOIB is positively related to future stock

returns (in line with, e.g., Chordia, Roll, and Subrahmanyam (2005, 2008)). In particular,

the MOIB coefficient is 0.596 and is positive and significant in 27.3% of the stock-day regres-

sions.7 Depth imbalances at the inner and middle levels of the limit order book are positively

and significantly related to the future price movements in 46.5% and 12.7%, respectively,

while depth imbalances at the outer levels of the limit order book have, on average, negative

effects; however, the proportion of positive and negative significant stock days is almost the

same. The latter could be due to the fact that outer levels are used for informed trading if

and only if an informed trader receives a relatively strong signal, which is unlikely to happen

regularly on the market.

In order to measure the relative importance of different order types, I look at the R2

decomposition of the predictive regressions averaged across all possible orderings of the

variables as in Lindeman, Merenda, and Gold (1980). Panel B of Table II shows that the

average adjusted R2 of the predictive regressions is equal to 2.5% for the whole sample.

MOIB contributes 19.4% to the R2 (0.49% in absolute terms), while limit order book

imbalances, LOIB, jointly account for 57.6% of the R2 (1.44% in absolute terms). The

7As a comparison, Rosch, Subrahmanyam, and Van Dijk (2016) document that coefficient of MOIBis positive and significant in 30.07% of the predictive regressions using only lagged dollar market orderimbalance as predictive variable over the period between 1996 and 2010 for NYSE common stocks.

15

largest predictive power comes from depth imbalances at the inner levels of the limit order

book (30.9% in relative terms). As a comparison, Chordia, Roll, and Subrahmanyam (2008)

document an adjusted R2 of 0.51% for predictive regressions using only lagged dollar market

order imbalance as predictive variable for the 1993-2002 period.

My results are consistent with Cao, Hansch, and Wang (2009), who document an increase

in adjusted R2 after inclusion of additional levels of the limit order book with a monotonic

decrease of the added value for each additional level. My results are, however, at odds with

Cont, Kukanov, and Stoikov (2014), who argue that only imbalances at the BBO level drive

intraday return predictability.

All in all, this suggests that private information is the main source of the intraday return

predictability: roughly 20% of this predictability is attributable to the informed market

orders, and roughly 60% is attributable to the informed limit orders. The remaining 20%

stem from inventory-management concerns (lagged returns).

C. The effect of algorithmic trading on order-type informativeness

In this section, I discuss the casual effect of algorithmic trading on the relative informa-

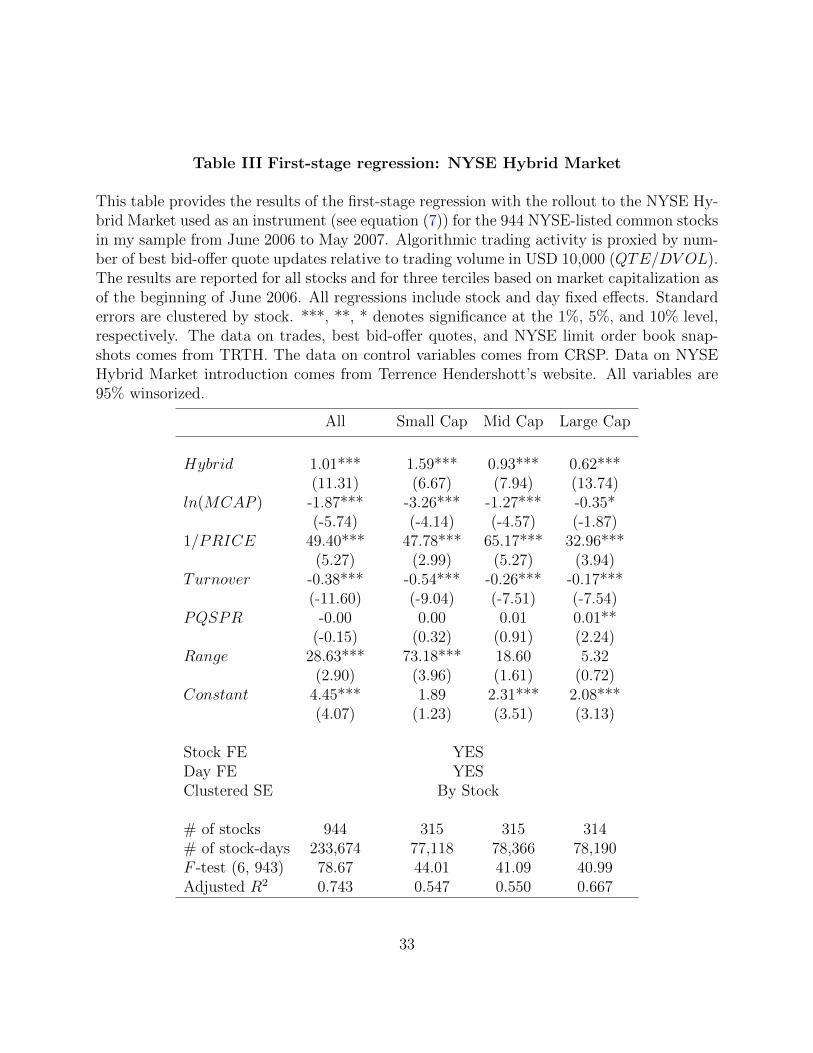

tiveness of different order types. Table III reports the results of the first-stage instrumental

variable regression (see equation (7)), with the NYSE Hybrid Market’s introduction as an

instrument for algorithmic trading activity.

INSERT TABLE III HERE

I document that algorithmic trading activity, as proxied by the number of best bid-

offer quote updates relative to daily trading volume in USD 10,000 (QTE/DV OL) increases

significantly for the whole sample as well as for different market capitalization terciles. In

particular, algorithmic trading increases by 1.01 best bid-offer quote update per USD 10,000

trading volume or 16% relative to its average value for the whole sample period.

16

Interestingly, I observe a monotonic decrease in the changes of algorithmic trading due

to the NYSE Hybrid Market’s introduction, moving from small to large stocks. However,

the relative effect exhibits the opposite pattern: from a 14% increase for small stocks to a

25% increase for large stocks.

INSERT TABLE IV HERE

The results for the second-stage regression for the whole sample are presented in Table

IV. In particular, I estimate the effect of algorithmic trading on the R2 decomposition from

predictive regressions (see equation (6)).8 Algorithmic trading increases price informative-

ness as manifested by an increase of adjusted R2 by 0.31% – or, in relative terms, by 12.4%

(0.31%/2.5%). Algorithmic trading activity increases the relative importance of both mar-

ket orders and limit orders at the inner levels of the limit order book by 0.68% and 1.92%,

or by 3.51% and by 6.21%, relative to the sample mean, respectively. This implies that

on average, adjusted R2 attributable to market order imbalances increases from 0.49% to

0.56% and adjusted R2 attributable to the depth imbalances at the inner levels of the limit

order book increases from 0.77% to 0.92%. Depth imbalances at the middle and outer levels

of the limit order book decrease their relative importance. This finding is in line with the

fact that algorithmic trading operates with short-lived information extracted from the order

flow, and thus traders will not be inclined to use the middle and outer levels of the limit

order book in their trading strategies due to the long elapsed time between order submission

and execution. Overall, there is a shift of relative importance to both market orders and

limit orders at the inner levels of the limit order book, which is consistent with both the

competition and efficient technology hypotheses.

Among others, Hagstromer and Norden (2013) and Brogaard, Hendershott, and Riordan

(2014) provide empirical evidence that algorithmic traders (especially high-frequency traders)

8I use the relative decomposition of the R2 rather than the absolute one because I want to isolate thechange of different order types’ relative informativeness from the general effect of the changes in R2 due tothe increase in algorithmic trading activity.

17

are more present in large stocks than in small stocks. Therefore, the effects of increase in

algorithmic trading activity might be different for stocks with different market capitalization.

INSERT TABLE V HERE

Table V presents the second-stage results for different market capitalization terciles. In

line with the competition hypothesis, I document that the relative importance of market

order imbalances increases significantly for small and medium-size stocks by 0.64% and

0.96%, or by 3.35% and 5.22%, relative to sample average, respectively, but not for the large

stocks. A possible explanation for medium-size stocks having a larger increase in importance

of market orders for the price discovery process than small stocks is that small stocks have

the largest spread, which makes it more costly to use market orders in the first place. At

the same time, the relative importance of inner levels increases significantly with algorithmic

trading for medium and large stocks by 1.86% and 4.29%, or by 5.63% and 15.89%, relative to

sample average, respectively, but not for the small stocks. Put differently, the competition

hypothesis manifests itself more in small stocks, while the efficient technology hypothesis

manifests itself more in large stocks. This is consistent with strong entry barriers within

high-frequency traders’ business (see Baron, Brogaard, Hagstromer, and Kirilenko (2017)),

which lead to a larger increase in competition between high-frequency traders in stocks with

ex-ante low presence of high-frequency traders.

To sum up, I contribute to the debate on whether algorithmic traders adversely select

other market participants. I provide evidence that the increased participation of algorithmic

traders has caused an increase in the relative importance of the price discovery process for

both market orders and limit orders concentrated at the inner levels of the limit order book.

Moreover, in large stocks, which were likely to have a lot of algorithmic trading activity

before the introduction of the NYSE Hybrid Market, prices become more informative purely

via limit orders. This suggests that, in the absence of new algorithmic traders entering the

18

market, any increase in algorithmic trading activity will lead to an increase of the informed

liquidity provision.

IV. Additional analysis

In this section, I provide additional results to support the baseline analysis discussed in

the Section III.C. I show that my results are robust to using another proxy of algorithmic

trading activity (Section IV.A) and also conduct a placebo test (Section IV.B). I provide

additional support to the competition versus efficient technology hypotheses by looking at

the NYSE Hybrid Market’s rollout sequence (Section IV.C). In Section IV.D, I confirm that

algorithmic traders are focused on short-lived information.

A. Another proxy for algorithmic trading

In this section, instead of using QTE/DV OL, the daily number of best bid-offer quote

updates relative to daily trading volume (in $10,000), as a proxy of algorithmic trading, I use

QTE/TRD, the daily number of best bid-offer quote updates relative to the daily number

of transactions. I note that this proxy of algorithmic trading activity is inferior to the one

used in the baseline analysis because it does not take into account the size of each individual

transaction.

INSERT TABLE VI HERE

The results for the second-stage of the instrumental variable regression (see equation (7))

for the whole sample are presented in Table VI. Overall, the results are consistent with my

findings in the baseline analysis. However, the shift in the relative importance of different

order types for the price discovery process is more profound. Algorithmic trading activity

increases the relative importance of both market orders and limit orders at the inner levels

19

of the limit order book by 2.36% and 6.70%, respectively (as opposed to the baseline case:

0.68% and 1.98%, respectively). Depth imbalances at the middle and outer levels of the limit

order book decrease their importance for the price discovery process.

B. Placebo test

In order to ensure that my results are indeed driven by the NYSE Hybrid Market’s

rollout, which resulted in increased algorithmic trading activity, I perform a placebo test. In

particular, for each stock, I randomly pick an NYSE Hybrid Market rollout date from a pool

of all rollout dates observed in my sample, excluding the actual rollout date for this stock.

Afterwards, I re-estimate second-stage of the instrumental variable regression (see equation

(7)) with randomly assigned rollout dates. I repeat this exercise 1,000 times and report the

average coefficient in front of algorithmic trading from the second-stage regression and also

the proportion of cases in which this variable was statistically significant at the 10%, 5%,and

1% levels.

INSERT TABLE VII HERE

The results for the placebo test are presented in Table VII. Remarkably, the proportion

of cases with a statistically significant effect of algorithmic trading is always well below the

significance level. To sum up, I confirm that my results indeed have a causal interpretation

rather than the common-trends explanation.

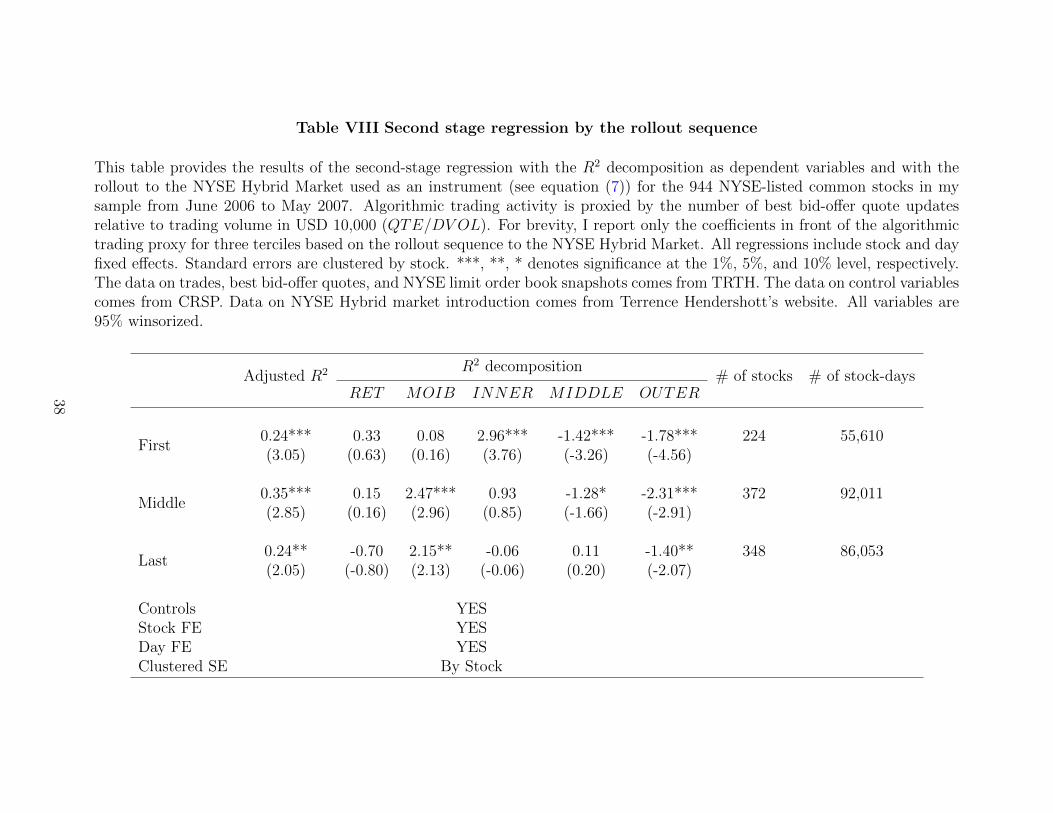

C. Rollout sequence

New algorithmic traders would require some time in order to set up their systems for

algorithmic trading (e.g., colocate their servers and develop software). I expect that such

traders will not appear in the stocks that were rolled out to the NYSE Hybrid Market

first, but rather in the stocks that were rolled out later. New algorithmic traders are likely

20

to rely more heavily on using market orders in their trading strategies because it requires

less experience and less expensive connections to exchange than engaging in market-making

business (i.e., an active usage of limit orders) – for example, Brogaard, Hagstromer, Norden,

and Riordan (2015) document that mainly high-frequency market makers undertake the

colocation upgrade offered by NASDAQ OMX Stockholm voluntarily. Besides that, entry of

the new algorithmic traders to the market increases competition for the same information,

which in turn leads to increased attractiveness of market orders for informed trading (the

competition hypothesis).

INSERT TABLE VIII HERE

The results for the second-stage of the instrumental variable regression (see equation (7))

split by the rollout sequence to the NYSE Hybrid Market are presented in Table VIII. I show

that stocks that were rolled out first experience an increase in the relative importance of the

depth imbalances at the inner levels of the limit order book, but not stocks that were rolled

out later, while the opposite is true for market order imbalances. All in all, my findings are

consistent with the fact that new algorithmic traders are likely to rely on trading strategies

involving market orders and with the fact that increased competition among algorithmic

traders leads to increased relative informativeness of market orders.

D. Lifespan of information

Anecdotal evidence suggests that algorithmic traders rely on short-lived information.

Therefore, I expect that the effects of algorithmic trading on the relative importance of

different order types deteriorates with an increase in the predictive horizon (i.e., the lifespan

of the information).

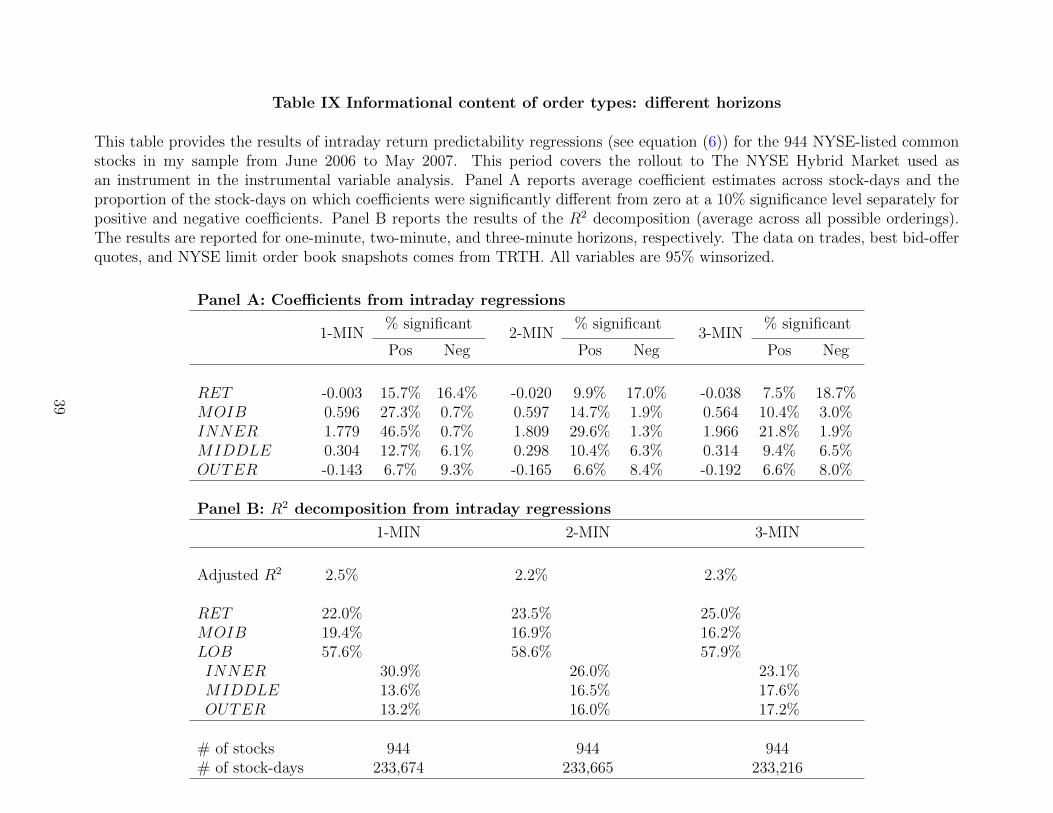

INSERT TABLE IX HERE

21

I start by providing summary statistics for the relative importance of different order

types for the price discovery process for different predictive horizons: one minute (baseline

analysis), two minutes, and three minutes (see Table IX). Panel A of Table IX presents

the average coefficients of the predictive regressions (see equation (6)) together with the

proportion of stock-days when they were significantly different from zero. Interestingly, I

observe that inventory effects become stronger when I increase the predictive horizon from

one minute to three minutes. In particular, the size of the coefficient in front of lagged

returns increases monotonically, as does the proportion of stock-days when this coefficient is

negative and significant.

Panel B of Table IX presents R2 decomposition averaged across all possible orderings of

the variables as in Lindeman, Merenda, and Gold (1980). I confirm that the importance of

inventory effects increases while moving from a one-minute horizon to a three-minute horizon:

from 22% to 25% of the overall predictive power. If information has a longer lifespan, an

informed trader does not mind waiting longer (conditional on getting a better price), and

therefore an informed trader is likely to submit limit orders deep in the limit order book if

her information lives long enough. In line with this consideration, the importance of market

order imbalances and depth imbalances at the inner levels of the limit order book decreases

from 19.4% to 16.2% and from 30.9% to 23.1%, respectively, while increasing the predictive

horizon. At the same time, the importance of depth imbalances at the middle and outer

levels of the limit order book increases from 13.6% to 17.6% and from 13.2% to 17.2%,

respectively, while increasing the predictive horizon.

INSERT TABLE X HERE

Table X presents the results of the second-stage regressions for the different predictive

horizons. I observe that algorithmic traders become more concerned about their inventory

with an increase in the horizon: the relative importance of the lagged returns in predicting

future price movements increases significantly by 1.43% and 1.14% for the two-minute and

22

three-minute horizons, respectively. The importance of market order imbalances either does

not change or decreases with increase in algorithmic trading activity for the two-minute

and three-minutes horizons, respectively. The importance of depth imbalances at the inner

levels of the limit order book increases with an increase in algorithmic trading activity by

0.59% and 0.66% for the two-minute and three-minute horizons, respectively. However, this

increase is almost three times smaller than the increase observed for the one-minute horizon

(1.92%). If algorithmic traders also collect long-lived information, one can expect that the

relative informativeness of the depth imbalances at the middle and outer levels of the limit

order book will increase with the increasing horizon. However, the relative informativeness

of depth imbalances at the middle and outer levels of the limit order book decreases as well,

suggesting that algorithmic traders are not acquiring long-lived information.

Overall, my findings suggest that market orders and orders at the inner levels of the limit

order book are used for short-lived information, while orders deep in the limit order book are

used for long-lived information. Besides that, algorithmic traders are focused on short-lived

information only.

V. Conclusion

The recent public debates regarding algorithmic traders (and high-frequency traders)

adversely selecting retail investors highlighted the importance of understanding how informed

trading is taking place and how it was affected by the emergence of algorithmic trading.

Motivated by this, I investigate the intraday return predictability from informed market

limit orders around introduction to the NYSE Hybrid Market – a change in market design

that I use as an instrumental variable for algorithmic trading activity.

To the best of my knowledge, I am the first to establish a causal relation between al-

gorithmic trading activity and the relative informativeness of different order types. In line

with the previous literature, I confirm that both limit and market orders are actively used for

23

informed trading. I show that an increase in algorithmic trading activity leads to a shift of

relative informativeness from the limit orders deep in the limit order book to the limit orders

at the inner levels of the limit order book and market orders. The net effect of algorithmic

trading depends on the change in competition between them.

One important implication of my analysis concerns measures of asymmetric information

and/or informed trading (e.g., the PIN measure by Easley, Kiefer, and O’Hara (1996) and

the adverse selection component of bid-ask spread by Glosten and Harris (1988) and Huang

and Stoll (1997)), which have been used widely in studies on market microstructure, asset

pricing, and corporate finance.9 These measures are exclusively based on market orders, and

thus neglect the lion’s share of informed trading on the equity markets – informed trading

via limit orders.

In conclusion, in the market where new algorithmic traders are not likely to enter, any

increase of algorithmic trading should lead to more informed liquidity provision, keeping

constant informed liquidity demand. This fact should not be neglected while analyzing the

adverse selection effects on financial markets as well as regulatory actions targeted at the

important subset of algorithmic traders known as high-frequency traders.

9E.g., Easley, Hvidkjaer, and O’Hara (2002), Vega (2006), Chen, Goldstein, and Jiang (2006), Korajczykand Sadka (2008), Bharath, Pasquariello, and Wu (2008), and Easley, de Prado, and O’Hara (2012).

24

References

Anand, A., S. Chakravarty, and T. Martell (2005). Empirical evidence on the evolution

of liquidity: Choice of market versus limit orders by informed and uninformed traders.

Journal of Financial Markets 8 (3), 288–308.

Avramovic, A., V. Lin, and M. Krishnan (2017). Market structure: We are all high frequency

traders now. Credit Suisse: Trading Strategy Report .

Bae, K.-H., H. Jang, and K. S. Park (2003). Traders choice between limit and market orders:

evidence from nyse stocks. Journal of Financial Markets 6 (4), 517–538.

Baron, M., J. Brogaard, B. Hagstromer, and A. Kirilenko (2017). Risk and return in high-

frequency trading. Forthcoming .

Baruch, S., M. Panayides, and K. Venkataraman (2014). Informed trading before corporate

events: Theory and evidence. Working paper .

Bharath, S. T., P. Pasquariello, and G. Wu (2008). Does asymmetric information drive

capital structure decisions? Review of Financial Studies 22 (8), 3211–3243.

Biais, B. and T. Foucault (2014). HFT and market quality. Bankers, Markets and In-

vestors 128, 5–19.

Biais, B., T. Foucault, and S. Moinas (2015). Equilibrium fast trading. Journal of Financial

Economics 116 (2), 292–313.

Bloomfield, R., M. O’Hara, and G. Saar (2005). The make or take decision in an electronic

market: Evidence on the evolution of liquidity. Journal of Financial Economics 75 (1),

165–199.

Boehmer, E., K. Y. Fong, and J. J. Wu (2015). International evidence on algorithmic trading.

Working paper .

25

Brogaard, J., B. Hagstromer, L. L. Norden, and R. Riordan (2015). Trading fast and slow:

Colocation and market quality. Review of Financial Studies 28 (12), 3407–3443.

Brogaard, J., T. Hendershott, and R. Riordan (2014). High-frequency trading and price

discovery. Review of Financial Studies 27 (8), 2267–2306.

Brogaard, J., T. Hendershott, and R. Riordan (2017). Price discovery without trading:

Evidence from limit orders. Working paper .

Cao, C., O. Hansch, and X. Wang (2009). The information content of an open limit-order

book. Journal of Futures Markets 29 (1), 16–41.

Cenesizoglu, T., G. Dionne, and X. Zhou (2014). Effects of the limit order book on price

dynamics. Working paper .

Chakravarty, S. and C. W. Holden (1995). An integrated model of market and limit orders.

Journal of Financial Intermediation 4 (3), 213–241.

Chen, Q., I. Goldstein, and W. Jiang (2006). Price informativeness and investment sensitivity

to stock price. Review of Financial Studies 20 (3), 619–650.

Chordia, T., R. Roll, and A. Subrahmanyam (2005). Evidence on the speed of convergence

to market efficiency. Journal of Financial Economics 76 (2), 271–292.

Chordia, T., R. Roll, and A. Subrahmanyam (2008). Liquidity and market efficiency. Journal

of Financial Economics 87 (2), 249–268.

Cohen, K. J., S. F. Maier, R. A. Schwartz, and D. K. Whitcomb (1981). Transaction

costs, order placement strategy, and existence of the bid-ask spread. Journal of Political

Economy 89 (2), 287–305.

Cont, R., A. Kukanov, and S. Stoikov (2014). The price impact of order book events. Journal

of Financial Econometrics 12 (1), 47–88.

26

Easley, D., M. M. L. de Prado, and M. O’Hara (2012). Flow toxicity and liquidity in a

high-frequency world. Review of Financial Studies 25 (5), 1457–1493.

Easley, D., S. Hvidkjaer, and M. O’Hara (2002). Is information risk a determinant of asset

returns? Journal of Finance 57 (5), 2185–2221.

Easley, D., N. M. Kiefer, and M. O’Hara (1996). Cream-skimming or profit-sharing? the

curious role of purchased order flow. Journal of Finance 51 (3), 811–833.

ESMA (2014). Economic Report: High frequency trading activity in EU equity markets.

Foucault, T. (1999). Order flow composition and trading costs in a dynamic limit order

market1. Journal of Financial Markets 2 (2), 99–134.

Foucault, T., J. Hombert, and I. Rosu (2016). News trading and speed. Journal of Fi-

nance 71 (1), 335–382.

Foucault, T., O. Kadan, and E. Kandel (2005). Limit order book as a market for liquidity.

Review of Financial Studies 18 (4), 1171–1217.

Foucault, T., R. Kozhan, and W. W. Tham (2017). Toxic arbitrage. Review of Financial

Studies 30 (4), 1053–1094.

Glosten, L. R. (1994). Is the electronic open limit order book inevitable? Journal of

Finance 49 (4), 1127–1161.

Glosten, L. R. and L. E. Harris (1988). Estimating the components of the bid/ask spread.

Journal of financial Economics 21 (1), 123–142.

Glosten, L. R. and P. R. Milgrom (1985). Bid, ask and transaction prices in a specialist

market with heterogeneously informed traders. Journal of Financial Economics 14 (1),

71–100.

27

Goettler, R. L., C. A. Parlour, and U. Rajan (2005). Equilibrium in a dynamic limit order

market. Journal of Finance 60 (5), 2149–2192.

Goettler, R. L., C. A. Parlour, and U. Rajan (2009). Informed traders and limit order

markets. Journal of Financial Economics 93 (1), 67–87.

Hagstromer, B. and L. Norden (2013). The diversity of high-frequency traders. Journal of

Financial Markets 16 (4), 741–770.

Handa, P. and R. A. Schwartz (1996). Limit order trading. Journal of Finance 51 (5),

1835–1861.

Harris, L. E. and V. Panchapagesan (2005). The information content of the limit order book:

evidence from NYSE specialist trading decisions. Journal of Financial Markets 8 (1), 25–

67.

Hendershott, T., C. M. Jones, and A. J. Menkveld (2011). Does algorithmic trading improve

liquidity? Journal of Finance 66 (1), 1–33.

Hendershott, T. and P. C. Moulton (2011). Automation, speed, and stock market quality:

The NYSE’s hybrid. Journal of Financial Markets 14 (4), 568–604.

Hirschey, N. (2013). Do high-frequency traders anticipate buying and selling pressure? Work-

ing paper .

Huang, R. D. and H. R. Stoll (1997). The components of the bid-ask spread: A general

approach. Review of Financial Studies 10 (4), 995–1034.

Jovanovic, B. and A. J. Menkveld (2015). Middlemen in limit-order markets. Working paper .

Kaniel, R. and H. Liu (2006). So what orders do informed traders use? Journal of Busi-

ness 79 (4), 1867–1913.

28

Kavajecz, K. A. and E. R. Odders-White (2001). An examination of changes in specialists

posted price schedules. Review of Financial Studies 14 (3), 681–704.

Kavajecz, K. A. and E. R. Odders-White (2004). Technical analysis and liquidity provision.

Review of Financial Studies 17 (4), 1043–1071.

Korajczyk, R. A. and R. Sadka (2008). Pricing the commonality across alternative measures

of liquidity. Journal of Financial Economics 87 (1), 45–72.

Kozhan, R., M. Moore, and R. Payne (2014). Market order flows, limit order flows and

exchange rate dynamics. Working paper .

Kozhan, R. and M. Salmon (2012). The information content of a limit order book: The case

of an FX market. Journal of Financial Markets 15 (1), 1–28.

Kyle, A. S. (1985). Continuous auctions and insider trading. Econometrica 53 (6), 1315–1335.

Lee, C. and M. J. Ready (1991). Inferring trade direction from intraday data. Journal of

Finance 46 (2), 733–746.

Lindeman, R. H., P. F. Merenda, and R. Z. Gold (1980). Introduction to bivariate and

multivariate analysis. Scott, Foresman, Glenview.

McInish, T. H. and J. Upson (2012). Strategic liquidity supply in a market with fast and

slow traders. Working paper .

Menkhoff, L., C. L. Osler, and M. Schmeling (2010). Limit-order submission strategies under

asymmetric information. Journal of Banking and Finance 34 (11), 2665–2677.

Menkveld, A. J. (2016). The economics of high-frequency trading: Taking stock. Annual

Review of Financial Economics (8).

29

Menkveld, A. J. and M. A. Zoican (2017). Need for speed? Exchange latency and liquidity.

The Review of Financial Studies 30 (4), 1188–1228.

O’Hara, M. (2015). High frequency market microstructure. Journal of Financial Eco-

nomics 116 (2), 257–270.

Parlour, C. A. (1998). Price dynamics in limit order markets. Review of Financial Stud-

ies 11 (4), 789–816.

Putnins, T. J. and D. Michayluk (2015). Liquidity provision in limit order book markets.

Working paper .

Rosch, D. M., A. Subrahmanyam, and M. A. Van Dijk (2016). The dynamics of market

efficiency. Review of Financial Studies 30 (4), 1151–1187.

Rosu, I. (2009). A dynamic model of the limit order book. Review of Financial Stud-

ies 22 (11), 4601–4641.

Rosu, I. (2016). Liquidity and information in order driven markets. Working paper .

Seppi, D. J. (1997). Liquidity provision with limit orders and a strategic specialist. Review

of Financial Studies 10 (1), 103–150.

Swan, P. and P. J. Westerholm (2006). Market architecture and global exchange efficiency:

One design need not fit all stock sizes. Working paper .

Vega, C. (2006). Stock price reaction to public and private information. Journal of Financial

Economics 82 (1), 103–133.

Wuyts, G. (2008). The impact of liquidity shocks through the limit order book. Working

paper .

30

Table I Proxies for algorithmic trading

This table provides summary statistics for algorithmic trading activity for the 944 NYSE-listed common stocks in my sample from June 2006 to May 2007. This period covers therollout to the NYSE Hybrid Market used as an instrument in the instrumental variableanalysis. The results are reported for all stocks and for three terciles based on marketcapitalization as of the beginning of June 2006. The data on daily number of best bid-offerquote updates (QTE), daily number of trades (TRD), and daily trading volume in USD10,000 (DV OL) comes from TRTH. All variables are 95% winsorized.

All Small Cap Mid Cap Large Cap

QTE/DV OL 6.49 11.31 5.76 2.48QTE/TRD 4.46 5.51 4.63 3.26TRD 4,121 1,432 2,626 8,271QTE 12,945 6,655 10,300 21,798DV OL 5,567 953 2,609 13,082

# of stocks 944 315 315 314# of stock-days 233,674 77,118 78,366 78,190

31

Table II Informational content of order types

This table provides the results of intraday return predictability regressions (see equation (6)) for the 944 NYSE-listed commonstocks in my sample from June 2006 to May 2007. This period covers the rollout to NYSE Hybrid Market used as an instrumentin the instrumental variable analysis. Panel A reports average coefficient estimates across stock-days and proportion of thestock-days on which coefficients were significantly different from zero at a 10% significance level separately for positive andnegative coefficients. Panel B reports the results of the R2 decomposition (average across all possible orderings). The resultsare reported for all stocks and for three terciles based on market capitalization as of the beginning of June 2006. The data ontrades, best bid-offer quotes, and NYSE limit order book snapshots comes from TRTH. All variables are 95% winsorized.

Panel A: Coefficients from intraday regressions

All% significant

Small Cap% significant

Mid Cap% significant

Large Cap% significant

Pos Neg Pos Neg Pos Neg Pos Neg

RET -0.003 15.7% 16.4% -0.016 12.2% 19.0% 0.004 17.6% 15.4% 0.004 17.2% 14.8%MOIB 0.596 27.3% 0.7% 0.752 27.6% 0.7% 0.531 27.1% 0.7% 0.507 27.3% 0.7%INNER 1.779 46.5% 0.7% 2.631 48.6% 0.6% 1.718 51.5% 0.6% 1.000 39.3% 0.9%MIDDLE 0.304 12.7% 6.1% 0.428 13.0% 5.3% 0.275 13.0% 6.3% 0.210 12.2% 6.7%OUTER -0.143 6.7% 9.3% -0.170 6.4% 8.5% -0.169 6.5% 9.8% -0.091 7.0% 9.4%

Panel B: R2 decomposition from intraday regressions

All Small Cap Mid Cap Large Cap

Adjusted R2 2.5% 2.8% 2.7% 2.0%

RET 22.0% 21.3% 21.6% 23.1%MOIB 19.4% 19.1% 18.4% 20.5%LOB 57.6% 58.6% 59.0% 55.2%INNER 30.9% 32.5% 33.0% 27.0%MIDDLE 13.6% 13.3% 13.1% 14.3%OUTER 13.2% 12.8% 12.8% 13.9%

# of stocks 944 315 315 314# of stock-days 233,674 77,118 78,366 78,190

32

Table III First-stage regression: NYSE Hybrid Market

This table provides the results of the first-stage regression with the rollout to the NYSE Hy-brid Market used as an instrument (see equation (7)) for the 944 NYSE-listed common stocksin my sample from June 2006 to May 2007. Algorithmic trading activity is proxied by num-ber of best bid-offer quote updates relative to trading volume in USD 10,000 (QTE/DV OL).The results are reported for all stocks and for three terciles based on market capitalization asof the beginning of June 2006. All regressions include stock and day fixed effects. Standarderrors are clustered by stock. ***, **, * denotes significance at the 1%, 5%, and 10% level,respectively. The data on trades, best bid-offer quotes, and NYSE limit order book snap-shots comes from TRTH. The data on control variables comes from CRSP. Data on NYSEHybrid Market introduction comes from Terrence Hendershott’s website. All variables are95% winsorized.

All Small Cap Mid Cap Large Cap

Hybrid 1.01*** 1.59*** 0.93*** 0.62***(11.31) (6.67) (7.94) (13.74)

ln(MCAP ) -1.87*** -3.26*** -1.27*** -0.35*(-5.74) (-4.14) (-4.57) (-1.87)

1/PRICE 49.40*** 47.78*** 65.17*** 32.96***(5.27) (2.99) (5.27) (3.94)

Turnover -0.38*** -0.54*** -0.26*** -0.17***(-11.60) (-9.04) (-7.51) (-7.54)

PQSPR -0.00 0.00 0.01 0.01**(-0.15) (0.32) (0.91) (2.24)

Range 28.63*** 73.18*** 18.60 5.32(2.90) (3.96) (1.61) (0.72)

Constant 4.45*** 1.89 2.31*** 2.08***(4.07) (1.23) (3.51) (3.13)

Stock FE YESDay FE YESClustered SE By Stock

# of stocks 944 315 315 314# of stock-days 233,674 77,118 78,366 78,190F -test (6, 943) 78.67 44.01 41.09 40.99Adjusted R2 0.743 0.547 0.550 0.667

33

Table IV Second-stage regression

This table provides the results of the second-stage regression with the R2 decomposition asdependent variables and with the rollout to the NYSE Hybrid Market used as an instrument(see equation (7)) for the 944 NYSE-listed common stocks in my sample from June 2006 toMay 2007. Algorithmic trading activity is proxied by number of best bid-offer quote updatesrelative to trading volume in USD 10,000 (QTE/DV OL). All regressions include stock andday fixed effects. Standard errors are clustered by stock. ***, **, * denotes significanceat the 1%, 5%, and 10% level, respectively. The data on trades, best bid-offer quotes, andNYSE limit order book snapshots comes from TRTH. The data on control variables comesfrom CRSP. Data on NYSE Hybrid Market introduction comes from Terrence Hendershott’swebsite. All variables are 95% winsorized.

Adjusted R2 R2 decomposition

RET MOIB INNER MIDDLE OUTER

QTEDV OL

0.31*** 0.32 0.68*** 1.92*** -1.10*** -1.71***(6.64) (1.06) (2.58) (4.88) (-4.77) (-6.96)

ln(MCAP ) 0.41** 3.16*** -2.20** 2.88** -1.32* -2.44***(2.02) (3.34) (-2.45) (2.05) (-1.70) (-2.71)

1/PRICE -9.37* 10.07 -25.07 -87.73** 48.74** 49.97**(-1.90) (0.39) (-1.11) (-2.46) (2.40) (2.03)

Turnover 0.12*** 0.22 0.42*** 0.63*** -0.47*** -0.76***(4.98) (1.50) (3.31) (3.11) (-4.08) (-6.31)

PQSPR -0.00 0.03 0.01 -0.01 -0.02 0.00(-0.61) (1.30) (0.59) (-0.50) (-1.61) (0.12)

Range -28.03*** 6.31 -43.90 -157.45*** 71.76*** 110.16***(-5.52) (0.22) (-1.61) (-3.88) (3.33) (4.45)

Constant 1.35** 12.62*** 25.28*** 23.72*** 16.60*** 20.92***(2.13) (4.31) (9.24) (5.42) (6.88) (7.29)

Stock FE YESDay FE YESClustered SE By Stock

# of stocks 944# of stock-days 233,674

34

Table V Second stage regression by market capitalization

This table provides the results of the second-stage regression with the R2 decomposition as dependent variables and with therollout to the NYSE Hybrid Market used as an instrument (see equation (7)) for the 944 NYSE-listed common stocks in mysample from June 2006 to May 2007. Algorithmic trading activity is proxied by the number of best bid-offer quote updatesrelative to trading volume in USD 10,000 (QTE/DV OL). For brevity, I report only the coefficients in front of the algorithmictrading proxy for three terciles based on market capitalization as of the beginning of June 2006. All regressions include stockand day fixed effects. Standard errors are clustered by stock. ***, **, * denotes significance at the 1%, 5%, and 10% level,respectively. The data on trades, best bid-offer quotes, and NYSE limit order book snapshots comes from TRTH. The data oncontrol variables comes from CRSP. Data on NYSE Hybrid Market introduction comes from Terrence Hendershott’s website.All variables are 95% winsorized.

Adjusted R2 R2 decomposition# of stocks # of stock-days

RET MOIB INNER MIDDLE OUTER

Small Cap0.15*** 0.37 0.64** 0.63 -0.70*** -0.88*** 315 77,118(3.15) (1.08) (2.08) (1.51) (-2.89) (-3.38)

Mid Cap0.33*** -0.29 0.96** 1.86** -1.37*** -1.04*** 315 78,366(3.99) (-0.49) (2.04) (2.43) (-3.15) (-2.85)

Large cap0.56*** 0.60 0.94 4.29*** -1.42** -4.24*** 314 78,190(4.92) (0.78) (1.27) (4.80) (-2.27) (-7.01)

Controls YESStock FE YESDay FE YESClustered SE By Stock

35

Table VI Second stage regression: another proxy for algorithmic trading activity

This table provides the results of the second-stage regression with the R2 decomposition asdependent variables and with the rollout to the NYSE Hybrid Market used as an instrument(see equation (7)) for the 944 NYSE-listed common stocks in my sample from June 2006to May 2007. Algorithmic trading activity is proxied by the number of best bid-offer quoteupdates relative to number of transactions (QTE/TRD). All regressions include stock andday fixed effects. Standard errors are clustered by stock. ***, **, * denotes significanceat the 1%, 5%, and 10% level, respectively. The data on trades, best bid-offer quotes, andNYSE limit order book snapshots comes from TRTH. The data on control variables comesfrom CRSP. Data on NYSE Hybrid Market introduction comes from Terrence Hendershott’swebsite. All variables are 95% winsorized.

Adjusted R2 R2 decomposition

RET MOIB INNER MIDDLE OUTER

QTETRD

1.09*** 1.11 2.36** 6.70*** -3.84*** -5.95***(5.66) (1.06) (2.48) (4.53) (-4.32) (-5.86)

ln(MCAP ) -0.26 2.48*** -3.67*** -1.26 1.05 1.24(-0.93) (3.15) (-4.70) (-0.77) (1.05) (1.13)

1/PRICE 6.60 26.19 9.40 9.98 -7.25 -36.77(1.14) (1.23) (0.48) (0.28) (-0.35) (-1.49)

Turnover 0.17*** 0.28 0.53*** 0.95*** -0.65*** -1.04***(4.96) (1.45) (3.15) (3.46) (-4.04) (-5.72)

PQSPR -0.01** 0.02 -0.00 -0.06* 0.00 0.04*(-2.17) (0.90) (-0.24) (-1.80) (0.06) (1.87)

Range -20.05*** 14.36 -26.67 -108.62** 43.78* 66.81**(-3.48) (0.54) (-0.97) (-2.51) (1.92) (2.23)

Constant 0.22 11.48*** 22.84*** 16.81*** 20.56*** 27.05***(0.22) (3.11) (6.58) (2.70) (5.35) (6.29)

Stock FE YESDay FE YESClustered SE By Stock

# of stocks 944# of stocks 233,674674

36

Table VII Second stage regression: Placebo test

This table provides the results of the second-stage regression with the R2 decomposition asdependent variables for 1,000 repetitions of the random assignment of rollout to the NYSEHybrid Market used as an instrument (see equation (7)) for the 944 NYSE-listed commonstocks in our sample from June 2006 to May 2007. In particular, this table reports theaverage coefficient in front of the proxy for algorithmic trading activity, and the proportionof significant cases at the 1%, 5%, and 10% levels. Algorithmic trading activity is proxiedby the number of best bid-offer quote updates relative to trading volume in USD 10,000(QTE/DV OL). All regressions include stock and day fixed effects. Standard errors areclustered by stock. The data on trades, best bid-offer quotes, and NYSE limit order booksnapshots comes from TRTH. The data on control variables comes from CRSP. Data onNYSE Hybrid Market introduction comes from Terrence Hendershott’s website. All variablesare 95% winsorized.

Adjusted R2 R2 decomposition

RET MOIB INNER MIDDLE OUTER

QTEDV OL

0.43 -1.23 -1.13 3.58 -1.94 0.67

1% 0.2% 0.0% 0.0% 0.0% 0.1% 0.3%5% 1.2% 0.4% 0.1% 0.4% 0.8% 1.9%10% 3.2% 2.3% 0.5% 2.3% 1.9% 5.9%

Controls YESStock FE YESDay FE YESClustered SE By Stock

# of stocks 944Observations 233,674

37

Table VIII Second stage regression by the rollout sequence

This table provides the results of the second-stage regression with the R2 decomposition as dependent variables and with therollout to the NYSE Hybrid Market used as an instrument (see equation (7)) for the 944 NYSE-listed common stocks in mysample from June 2006 to May 2007. Algorithmic trading activity is proxied by the number of best bid-offer quote updatesrelative to trading volume in USD 10,000 (QTE/DV OL). For brevity, I report only the coefficients in front of the algorithmictrading proxy for three terciles based on the rollout sequence to the NYSE Hybrid Market. All regressions include stock and dayfixed effects. Standard errors are clustered by stock. ***, **, * denotes significance at the 1%, 5%, and 10% level, respectively.The data on trades, best bid-offer quotes, and NYSE limit order book snapshots comes from TRTH. The data on control variablescomes from CRSP. Data on NYSE Hybrid market introduction comes from Terrence Hendershott’s website. All variables are95% winsorized.

Adjusted R2 R2 decomposition# of stocks # of stock-days