International Tax Structuring

International Tax Structuring. Tax Structuring Tax Structuring is defined as a form into which business or financial activities may be organized to minimize.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Tax Structuring

Tax Structuring• Tax Structuring is defined as a form into which business or financial

activities may be organized to minimize taxation.

• An important part of tax structuring is deciding how to set up a business before commencing operations. A business may run as a sole proprietorship, general partnership, limited partnership, corporation or limited company.

• International tax structuring means different things to different people—depending upon their responsibilities within a company; but if its done correctly it can relieve (sometimes) onerous financial burdens that can inhibit a company’s development.

• An integrated international tax program which takes careful account of all of a company’s tax exposures can free up precious capital that can be redirected to the firm’s long-term benefit.

• Tax Residency

• Permanent Establishment

• Transfer Pricing

• Substance

• Due Diligence

• Anti Avoidance/Abuse/Tax Risk Management

• Treaty Shopping/WHT issues

Issues Underlying Tax Structuring

Cross border transaction imperatives

Cross Border Transactions

Cross Border Transactions

Legal & regulatory framework

Identifying and delivering synergies

Tax regimes & treaties

Business Dynamics

Business Environment

Cultural Issues

Accounting treatment

Cross border transactions

Cross border transactions

Exit considerations

Cash repatriation

Debt Structuring

Income flows and their taxability

Entry Strategy

Financing options

1

2

3

4

5

6

Key tax and financial considerations

• What should you acquire (assets or shares)?

• How should you acquire it (holding company issues)?

• How will you pay for it (tax efficient funding)?

• How will you use profits (maximizing dividend flows)?

• What if things don’t work out (tax efficient exit)?

The Five Questions of Tax Structuring

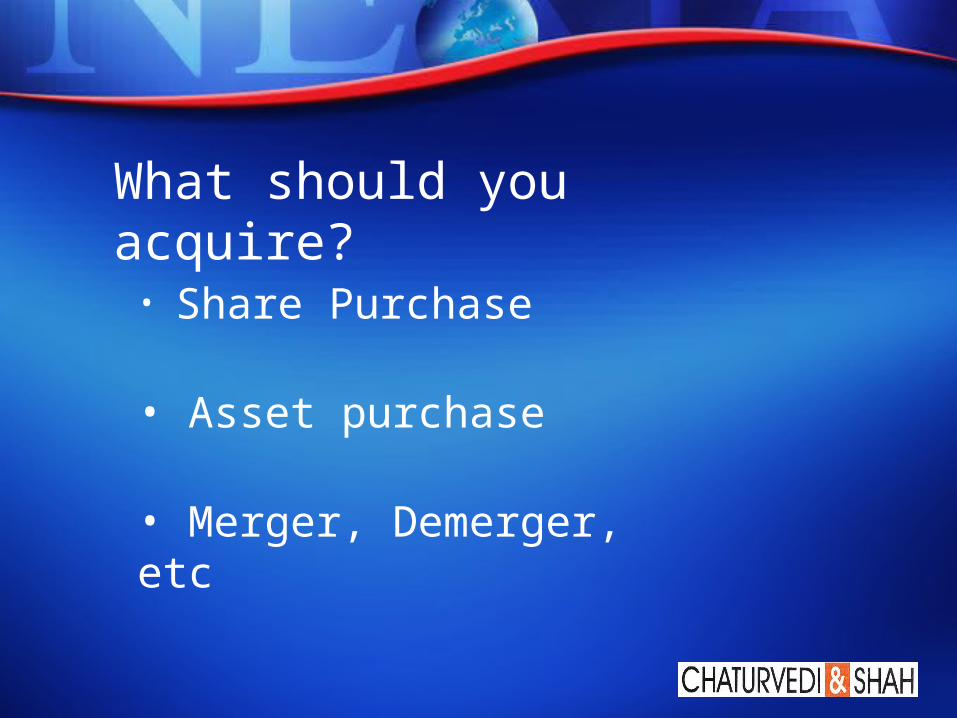

What should you acquire?

• Share Purchase

• Asset purchase

• Merger, Demerger, etc

Asset PurchaseTarget Structure Acquisition Structure

Parent Company

Holding Company

Target Company

Parent Company

Holding Company

Target Company

Acquirer

Acquisition Co.

Share Purchase

• Acquirer sets up Acquisition Company in Target Country• Acquisition Company purchases Assets/Business of Target Company for

cash consideration

How should you acquire it ?...

SPV Options• Company• Branch / Liaison office• Trust• LLPs

Applicable Tax Laws• Host Country• Target Country• SPV Jurisdiction• Tax Treaties

Need for an Overseas Holding Company (OHC)

• Taxation of foreign dividends in India

• Retention of profits in offshore jurisdiction

• Deferment of tax

• Greater flexibility for inter-company transfer of funds and for setting up operations in other overseas jurisdictions

• Future restructuring easy

• Better tax regime within European Union

Investors Considerations when choosing OHC• Receive dividends and capital gains tax free - Corporate Tax (Participation) Exemption

• Tax efficient repatriation of profits - Reduced Witholding of Profits

• Controlled Foreign Company (CFC) legislation

• Finance companies mechanism

• Flexible reorganizations

• Reliable tax authorities - Rulings

• Non tax driven considerations, e.g. IPO, exchange control regulations, protection IPR

How should you acquire it ?Considerations

• Capital Gains• Local taxes and underlying credit of foreign taxes• Withholding Taxes – Interest, Dividends and Royalties• Controlled Foreign Corporation Rules• Thin Capitalization Norms

- Debt Vs Equity• Ability to push up / down debt cost• Valuation of intangibles• Accounting (Consolidation)• Stamp Duties

Direct Tax• Tax Incentives• Utilisation of B/f tax losses• Group Relief• Revenue - Operating arrangements – Revenue vs Capital • Expenses

- Interest - Double dip• Treaty Shopping

Indirect taxes• Stamp Duty

Integration• Indirect Taxes

- Tax arbitrage from VAT via export and import• Transfer Pricing

How will you minimize tax incidence on Profits ?

Income stream and their taxability

Income streams Principles for evaluation

Dividends

Capital Gains

Interest

Other royalty / brand fees /technical Services / management services

• Interest, TS and royalty can flow independent of ownership pattern

• TS and royalty would typically flow to an operating entity, which possess technical capabilities

• Principal drivers are tax costs associated with dividend flows and gains on disposal of shares

• Brand fee would flow to the IPR company

Key elements – arm’s length principle, documentation, overall tax costs and foreign tax

credits

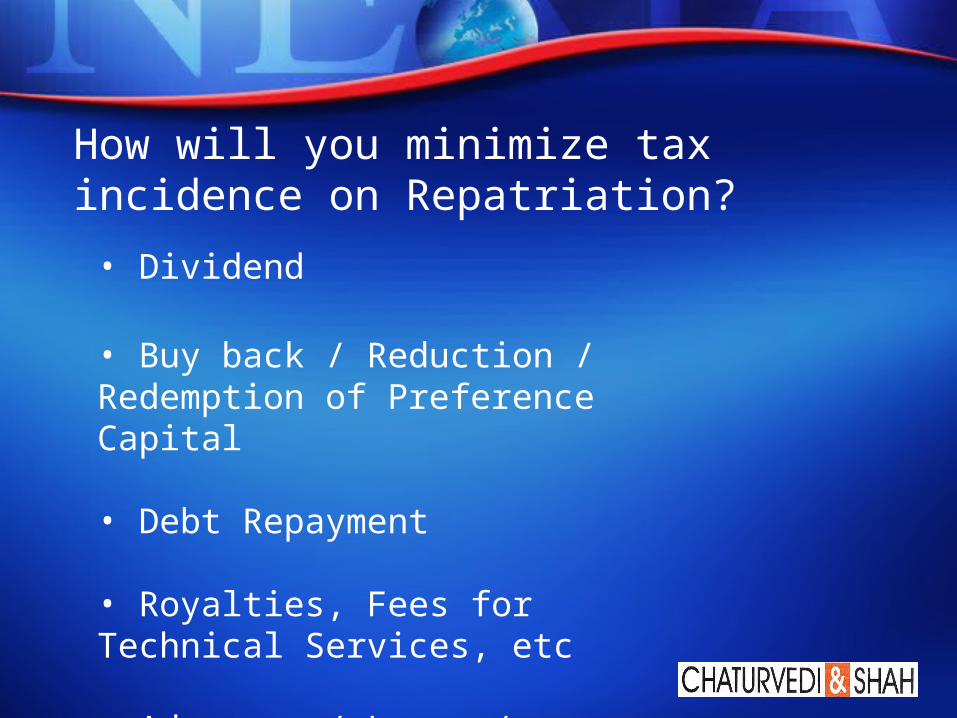

How will you minimize tax incidence on Repatriation?

• Dividend

• Buy back / Reduction / Redemption of Preference Capital

• Debt Repayment

• Royalties, Fees for Technical Services, etc

• Advances / Loans / Investments

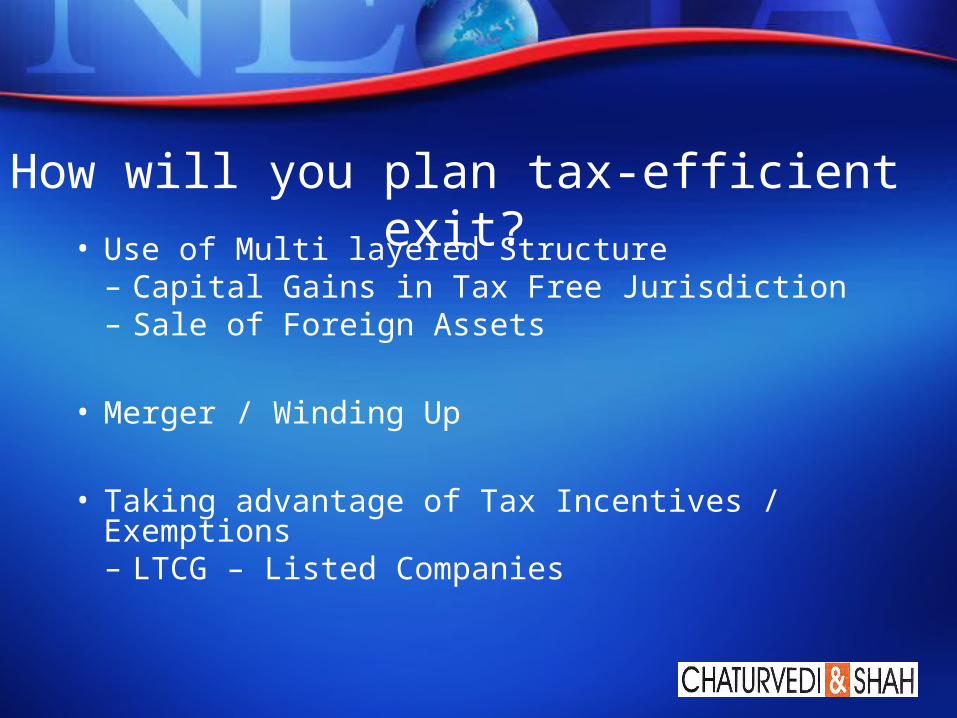

How will you plan tax-efficient exit?

• Use of Multi layered Structure– Capital Gains in Tax Free Jurisdiction– Sale of Foreign Assets

• Merger / Winding Up

• Taking advantage of Tax Incentives / Exemptions– LTCG – Listed Companies

Transfer of intermediary foreign company’s shares - Vodafone Case

Mechanics

• CCo1 sold its stake in CCo2 to Acquirer

UK CoUK

Acquirer NCo

I Co

CCo1

CCo2

Ne

the

rla

nd

sC

ay

ma

n I

sla

nd

Ind

ia

Issue

• Revenue Authorities contend that this transfer is taxable in India since the “controlling interest” in Indian Asset is transferred

Mauritius Co

Ma

uri

tiu

s

Through downstream

subsidiaries

Debatable issues after Vodafone Case

• What is the subject matter of transaction ?

• Is transfer of interest in subsidiary merely a mode of transfer of interest in the downstream company ?

• Does consideration paid or payable represents the value of assets of intermediary or of the downstream company ?

• What is the effect of declarations made by the parties to the transaction to their respective shareholders and / or to their regulatory authorities ?

THANK YOU

Related Documents