International Management and Executive Search Consultants allocate “Stormy Weathers” in the European Wind Power sector – how to keep the pace? Dr. Jörg Fabri allocate International, Managing Partner Presentation at EcoSummit Düsseldorf, 15. November 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

International Management and Executive Search Consultants

allocate

“Stormy Weathers” in the European Wind Power sector – how to keep the pace?

Dr. Jörg Fabri allocate International, Managing Partner

Presentation at EcoSummit Düsseldorf, 15. November 2012

2 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Investment “hot spot”: more than $ 200 billion investment annually in Renewable Energy

Comments New investments in Renewable Energy by sector Q1 2004 to Q2 2012 in bn. $

Source: allocate, Bloomberg

Is the Renewables sector prepared for further growth if subsidization is decreasing?

• Global new investments in renewable energies is app. $ 200 billion annually

• Since peak in 2011 decreasing volumes • Share of wind investments is 33% • VC/PE share stable at low level $ 8 bn. • New class of investors entering rene-

wables markets: low interest levels for low risk assets directs attention to renewables with infrastructure characteristics

New investments in Renewable Energy

Initial growth to a large extend driven by subsidization and legal framework

3 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Capacity figures wind Europe in MW

Success story: wind power is becoming a significant pillar in the European power production

Source: EWEA, allocate

Breakdown European generation capacity mix (in %,2000 vs. 2011)

Annual on and offshore wind installations in MW, Europe, 2001 to 2011

Significant pillar in Europe - Germany alone plans to add 25-40 GW until 2030

Cumulative 94 GW

Absolute MW

2

10

2000 2011

other

PV

Wind

Large hydro

Fuel oil

Gas

Nuclear

Coal

However, recently significant challenges occurred to proceed with the projected pace in developing the wind power sector

4 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Investment needs Wind parks and grid connections

Status 4/2012

1 17.09.12 Studie "Daten zur Umwelt 2012” 2 Source: CO2 Newsletter, Umweltbundesamt, allocate

• Installation of 25 GW until 2030 planned

• More than 120 billion € total investment (based on 4,5 mn. €/MW)

• Planned/ approved offshore volume 50GW

• Central pillar of German power generation:

- 25 GW produce 17% of today‘s electricity demand (50 GW accounts for 33%)

- Key challenge: integration with the grid and transport to main consuming areas

Very ambitious plans but problems increase with the implementation….

Huge growth ambitions: Germany has planned to install 25 GW until 2030 offshore Wind parks German North Sea (German economic zone only, AWZ)

5 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Bandwidths in wind investments

Investors’ perspective: not all wind is the same – onshore and offshore wind investments with different risk-reward profiles

Attraction of different investors: infrastructure funds focusing on the low risk profile of Onshore Wind – PE investors on high IRR of Offshore Wind (if the risk can be managed)

KPI onshore

EPC Cost € ‚000/MW ~1400 ~30001

offshore

Capacity Utilization 20-35% 30-45%

Investment Cost €/kWh ~80 – 46 € c ~114 – 76 € c

Operating Cost 1.5 – 1.8€c/kWh 2.2 – 2.8€c/kWh

Debt Service Cover Ratio @ P90 1.25 1.3 – 1.5

Proj. Financial Leverage 70 – 75 % 55 – 65 %

Equity IRR @ P50 9 – 12 % 14 – 18%

1 Site dependent

6 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Investment uncertainties

Investors are becoming increasingly reluctant towards wind power investments

Technical

Subsidies

Grid connection

Operational

Obvious high first mover risks in deep water offshore wind, grid uncertainties and reduced subsidization currently reduce investors’ appetite

Risks Description

Source: allocate

• Near shore/ 40+km offshore experiences uncovers a magnitude of unexpected problems (foundations, ship & employee bottlenecks,…)

• Deep water pioneer project BARD with big financial problems

• Feed in tariffs guaranteed for 10 year, planning cycles are 25 years • Decreasing willingness to grant new subsidies, trend to reductions & caps • Government tries to avoid another „solar bubble“ due to over subsidization

• Sales risks, TenneT with problems to connect the wind parks to the grid • Planned state guarantees still have to pass the parliament • New annual grid plan will coordinate grid and generation build up

• Limited experience in „true“ operational costs esp. maintenance. (manufactures often guarantee for 20 years only)

7 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

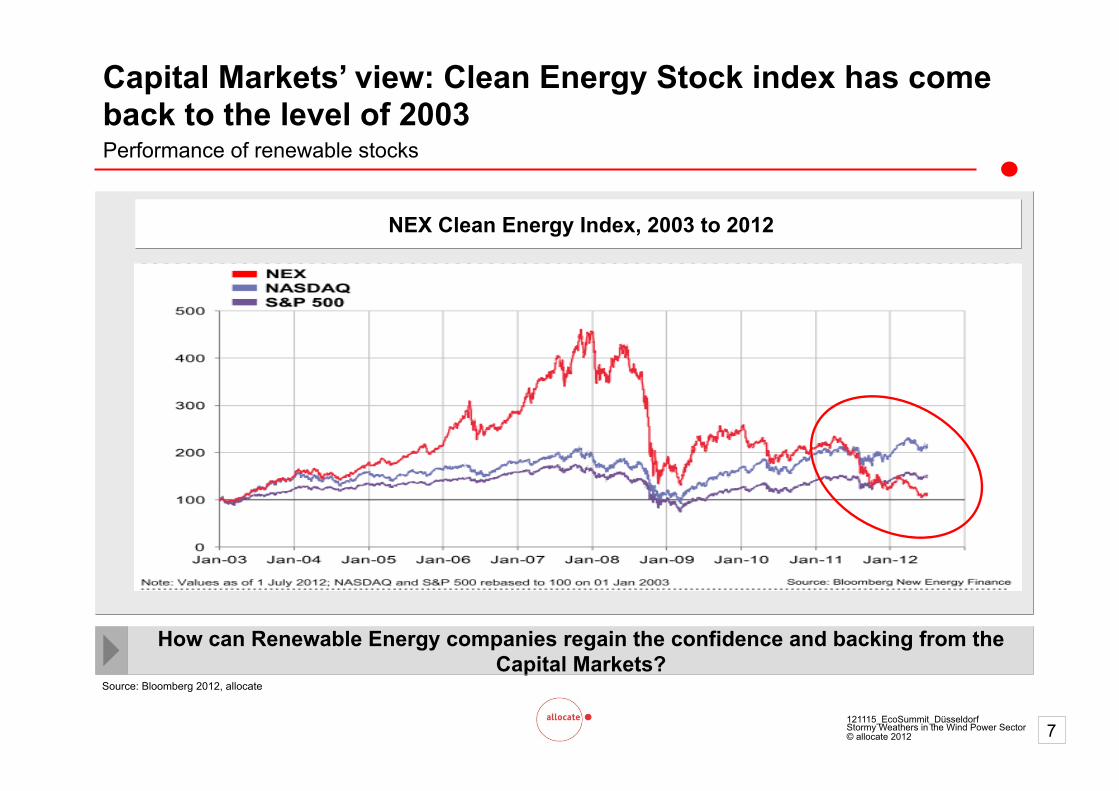

NEX Clean Energy Index, 2003 to 2012

Source: Bloomberg 2012, allocate

How can Renewable Energy companies regain the confidence and backing from the Capital Markets?

Capital Markets’ view: Clean Energy Stock index has come back to the level of 2003 Performance of renewable stocks

8 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Overview of investment per MW over exposure1)

Costs of offshore wind parks increase significantly with distance to coast & water depth…but do the profits as well?

8

Source: Company web pages; allocate research Remark: other parameters such as turbine capacity not considered in this analysis 1) Exposure = distance to coast [km] + water depth [m]

Cost per MW installed [EUR m]

Exposure1)

1,5 1,8 1,9

3,3 3,5

2,2 2,7

3,7 3,6

4,2

3,5 3,5

0

1

2

3

4

5

6

10 20 30 40 50 60 70 80 90 100 110 120 130

Lill- grund

Thanet Belwind

Alpha Ventus

Global Tech 1

Horns Rev2

Nysted

Egmond am Zee „Official“

figures

Will this be sufficient?

Borkum West II

London Array Thornton

Banks Ph. 2+3

BARD Offshore 1

EUR 250m for 60 MW

With more distance to coast the operational (wind) hours increase – thus the higher investment might pay back by higher energy output per installed MW (but risks increase)

9 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Changing rules of the game

Decreasing subsidies and entering new life cycle phases change success factors in the wind industry significantly . . .

Operational Excellence - Go to Market Strategy - Cash optimization are becoming key to stay in the game and to proceed with the growth

Comments Life cycle wind industry by segment –illustrative -

Introduction Growth Maturity Saturation

Euro

Sales Profit

Time

Offshore

Onshore

• Readiness and willingness of governments to subsidize renewables decreases (esp. in Germany)

• New success factor need to be mastered due to the progress in life cycle - Onshore entering maturity phase - Offshore leaving pioneer phase

• Financial crisis has dramatically increased the equity required in the industry

New strategies and operational concepts required to stay competitive Innovation Production Operational

Excellence Sales

Life cycle phase

Critical success factors

10 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Implications for manufacturers suppliers and operating/service companies

…with significant implications for the industry

Main implications

Industry Concentration/ Consolidation i.e. reduction of the number of competitors

Adaptation of Business Systems required

Operational Excellence becomes “key ” to sustainable profitability

The wind power industry has to adopt consequently to the new conditions to maintain the attractiveness for required investments

11 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Market concentration by selected industries – Herfindahl index , 2011

Industry structure: Herfindahl index indicates that significant industry consolidation might be required to secure profitability

Remark: maximum Herfindahl-Index is 10.000

266

358

737

Solar Modules

Airlines

Wind Turbine

Degree of industry concentration not concentrated moderate high

1600

Scenarios indicate that top 3 wind players have to double its market shares to reach moderate industry concentration / competitive rivalry

Scenario assumption: Top 3 players double their market shares

12 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Example: Owner-/ Operator stage of value chain

Business systems: industry players need to redefine their role in the wind power value chain

Different business models are applicable – which require a match with their specific key success factors

Service businesses

Development and Planning

Identification &

Feasibility Study

Owner- & Operatorship Building

very high very high high moderate

Existing strategy

type

Integrator e.g. RWE

Extended Operator e.g. DONG

Operator e.g. EnBW

Pure owner e.g. Insurances

Lever

Developer e.g. PNE

Owner- & Operatorship

Hardware e.g. turbines Other e.g. finance Services

13 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Example with selected offshore KPIs

Operational Excellence: future “key ” to sustainable profitability in wind power

Huge deviation of manageable OPEX – Operational Excellence with huge impact on profitability

1 includes contingencies Source: KPMG , allocate international

3,8 3,3 Mio € / MW CAPEX1 3,5

max min

Target Project

Average

3,6

36,7 20,1 € / MWh OPEX 35,0

25,5

52 41 in % Wind yield 49%

44

Projects Offshore

Limited bandwidth

Mana-geable

Site depen-dent

14 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Example: Maintenance strategy wind parks

Operational Excellence: Minimizing total operating cost in wind power operations by a tailored maintenance strategy

Optional maintenance strategies Downtime by reason / components

Source: IWES, DEWI, allocate

Total operating and maintenance cost Cost of repairs

• State based strategy • Time/periodic based

strategy • Event/crash based strategy • Mix

Strategy 1 Strategy 2

15 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Activities

allocate International supports clean energy companies across the whole set of their key challenges

Investment planning

CF1 CF2 CFn

1+r + + + …

1+r2 1+rn NPV =

Structures and processses

Financing

Business planning

‘13 ‘08 ‘09 ‘10 ‘11 ‘12

equity Total value

Portfolio development

/

+

x

x

x

-

Real value added ratio

Turnover

Real value added

Total waste

PHEK PCB ECU

plant

PHEK PCB ECU

plant

Fixed costs PHEK fix PCB ECU

Cost of inspections

Variable waste +

Cost of rework

Cost of shipping

errors

Cost per inspection employee

# of inspections

Average cost per shipping error

# of shipping errors

Cost per direct employee per hr

Time for reworking PCB ECU

Operational Excellence

Combining and implementing different key success factors in Wind Power

Success in Clean Energy businesses

16 121115_EcoSummit_Düsseldorf Stormy Weathers in the Wind Power Sector © allocate 2012

Anton J. Setter Partner Management Consulting allocate International GmbH Plange Mühle 3 (Medienhafen) D-40221 Düsseldorf Tel.: + 49 211 137 233 21 Fax.: +49 211 137 220 87 Mobil: +49 177 8387611 E-Mail: [email protected] www.allocate.de

Dr. Jörg Fabri Managing Partner Management Consulting allocate International GmbH Plange Mühle 3 (Medienhafen) D-40221 Düsseldorf Tel.: + 49 211 137 233 21 Fax.: +49 211 137 220 87 Mobil: +49 177 340 5095 E-Mail: [email protected] www.allocate.de

Arnd Fabri Managing Partner Executive Search allocate International GmbH Plange Mühle 3 (Medienhafen) D-40221 Düsseldorf Tel.: + 49 211 137 220 88 Fax.: +49 211 137 220 87 Mobil: +49 179 204 3328 E-Mail: [email protected] www.allocate.de

Thank you for your attention – we would be pleased to discuss with you! Contact details for further discussions

Related Documents