International Finance FINA 5331 Lecture 6: Exchange rate regimes Read: Chapters 2 Aaron Smallwood Ph.D.

International Finance FINA 5331 Lecture 6: Exchange rate regimes Read: Chapters 2 Aaron Smallwood Ph.D.

Jan 05, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International FinanceFINA 5331

Lecture 6:

Exchange rate regimes

Read: Chapters 2Aaron Smallwood Ph.D.

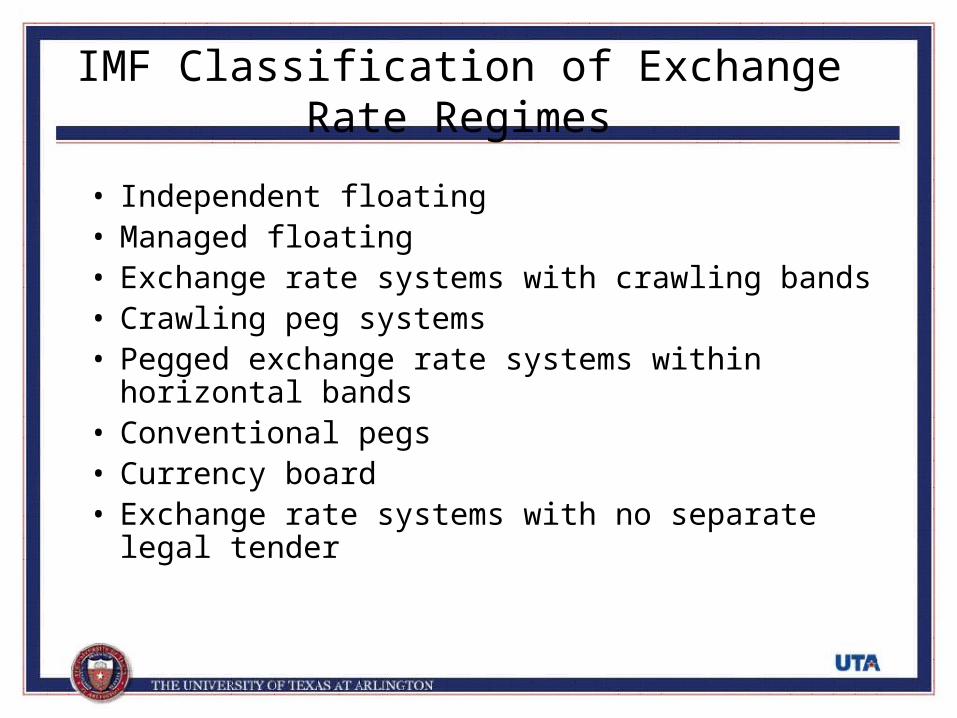

IMF Classification of Exchange Rate Regimes

• Independent floating• Managed floating• Exchange rate systems with crawling bands• Crawling peg systems• Pegged exchange rate systems within horizontal

bands• Conventional pegs• Currency board• Exchange rate systems with no separate legal tender

Independent Floating

• Exchange rate determined by market forces, with intervention aimed at minimizing volatility:

• Example: United States

Managed Floating

• There is no pre-announced path for the exchange rate, although intervention is common. Policy makers will try to influence the “level” of the exchange rate: example: India

Crawling Band

• The currency is maintained within bands around a central target for the domestic currency against another currency (or group of currencies). The bands themselves are periodically adjusted, sometimes in response to changes in economic indicators.

• Example: Costa Rica, Mexico in 1994.

Example: Belarus through Feb 2008

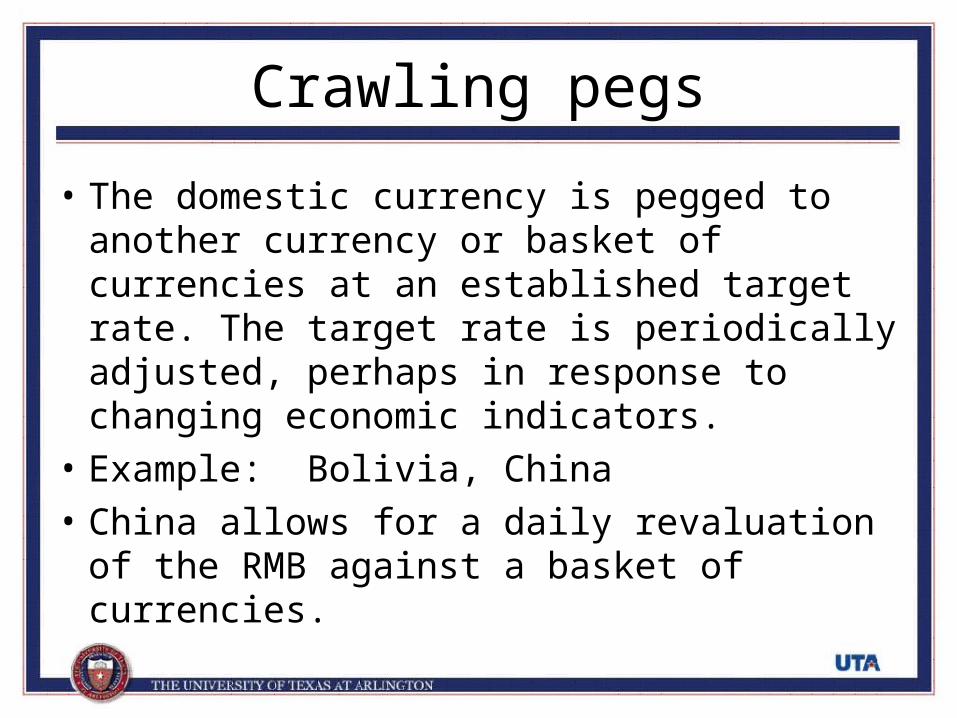

Crawling pegs

• The domestic currency is pegged to another currency or basket of currencies at an established target rate. The target rate is periodically adjusted, perhaps in response to changing economic indicators.

• Example: Bolivia, China

• China allows for a daily revaluation of the RMB against a basket of currencies.

Birr/$ between Apr 10 and Apr 11

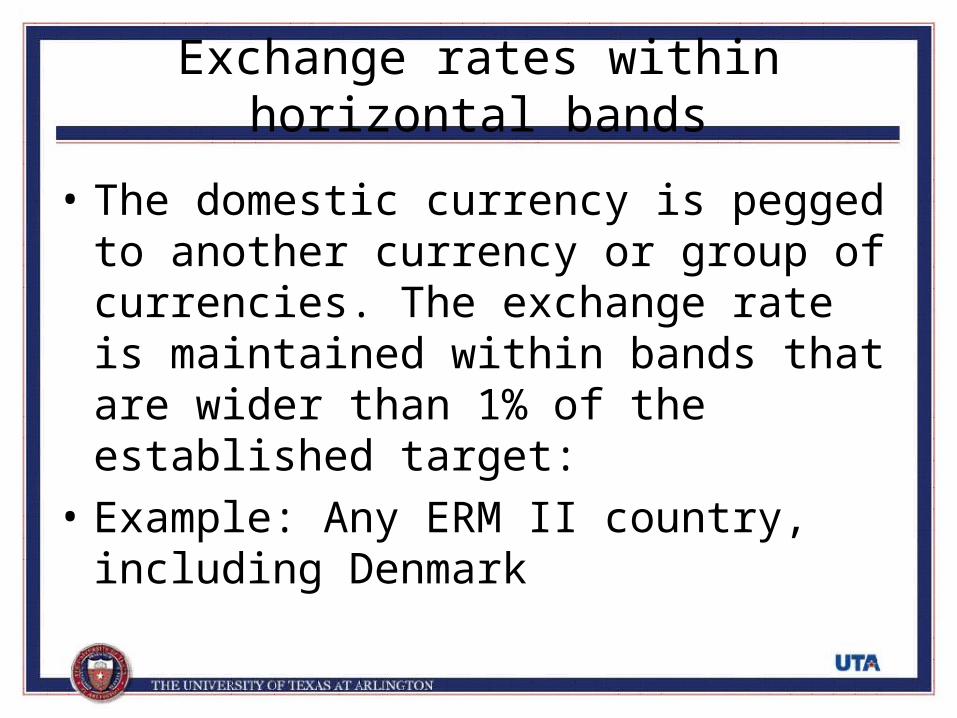

Exchange rates within horizontal bands

• The domestic currency is pegged to another currency or group of currencies. The exchange rate is maintained within bands that are wider than 1% of the established target:

• Example: Any ERM II country, including Denmark

Conventional pegs

• The country pegs its currency at a fixed rate to another currency (or group of currencies). The currency cannot fluctuate by more than 1% relative to the established target:

• Example: Saudi Arabia, formerly China

Currency boards

• Currency board countries are sometimes called “hard peggers”. Example: Hong Kong….

• The currency board is a separate government institution whose only responsibility is to buy and sell foreign currency at an established price. The country will typically maintain foreign currency reserves equivalent to 100% of the total amount of outstanding domestic money and credit.

Hong Kong

• Jim Rogers a famed currency trader has noted: “If I were the Hong Kong government, I would abolish the Hong Kong dollar. There's no reason for the Hong Kong dollar. It's a historical anomaly and I don't know why it exists anymore…. You have a gigantic neighbor who is becoming the most incredible economy in the world.”

No separate legal tender

• The country uses another country’s (or group of countries’) currency as its own:

• Example: Ecuador (US dollar)

Benefits of pegging your currency

• Exchange rates are stable– Could possibly benefit trade

• If pegged to a country with stable inflation, we may be able to import stable inflation.

• Likely provides an anchor for future inflation.

Drawbacks

• Loss of monetary policy independence

• Loss of the exchange rate as an automatic adjustment mechanism following economic shocks.

• Potential for major currency crises, especially if the trillema is violated.

Trillema

• The trillema, also known as the “impossible trinity” states that a country can ONLY have TWO of the following three:– Fixed exchange rate system– Free flow of capital– Independent monetary policy.

Integration in Europe

• Integration in Europe begins with the ECSC in 1951. With the Treaty of Rome, the ECSC becomes the EEC, which eventually becomes the EC and then the EU in 1994.– ESCS leads to EEC, which leads to EC, which leads to the EU.

• Monetary integration is formalized with the establishment of the EMS where exchange rates are fixed. The mechanism by which exchange rates are fixes is known as the exchange rate mechanism. The EMS leads to European Monetary Union. The 17 countries that use the euro are part of a currency union known as the EMU. Monetary policy for the entire EMU is overseen by the European Central Bank in Frankfurt.

The EU and the EMU.

• Today, there are 27 EU countries. The European Union is a political and economic union based on free trade. NOT ALL countries use the euro.

• There are several distinct groups

– EU Countries• EU countries who are not in the ERMII and have no

intention of adopting the euro

• EU Countries that will adopt

• ERM II countr(y)ies that have no stated intentions of adopting the euro

• ERM II countries that will adopt

• EMU Countries

Euro Area

• Austria Denmark• Belgium Latvia• Cyprus Lithuania• Estonia• Finland• France• Germany• Greece Bulgaria• Ireland Czech Republic• Italy Hungary• Luxembourg Poland• Malta Romania• Netherlands• Portugal Sweden• Slovenia UK• Spain• Slovakia

EU

EU countries that are not part of the ERMII

• EU countries that will eventually adopt (or plan to):

– Bulgaria– Czech Republic– Hungary – Poland– Romania

• EU countries (not part of ERMII) with no stated intention of adopting the euro

– Sweden– UK

ERM II Countries

• That will adopt:• Latvia• Lithuania

• The have no stated intentions of adopting• Denmark

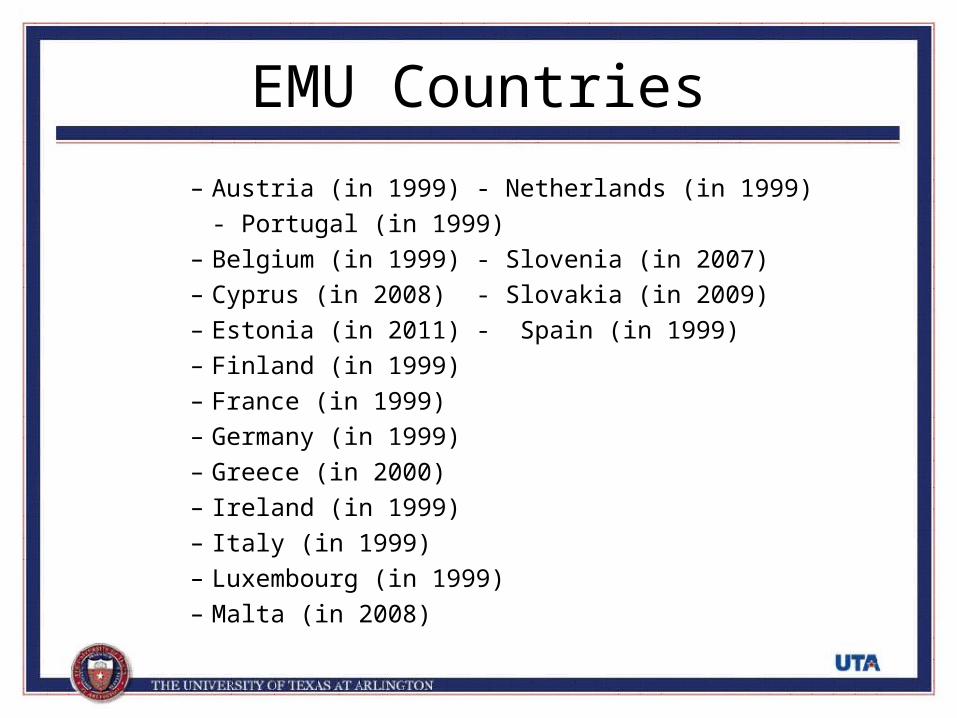

EMU Countries

– Austria (in 1999) - Netherlands (in 1999)

- Portugal (in 1999)– Belgium (in 1999) - Slovenia (in 2007)– Cyprus (in 2008) - Slovakia (in 2009)– Estonia (in 2011) - Spain (in 1999)– Finland (in 1999)– France (in 1999)– Germany (in 1999)– Greece (in 2000)– Ireland (in 1999)– Italy (in 1999)– Luxembourg (in 1999)– Malta (in 2008)

Is the EMU an OCA?

• OCA optimum currency area: The best geographic region where one currency is used within the region, and where outside the region, different currency(ies) are used.

• It is generally accepted that within an OCA:– Countries should be relatively buffered from

asymmetric shocks– Factors of production should be mobile

Related Documents