International Equity Markets Prof. Ian GIDDY Stern School of Business New York University

International Equity Markets Prof. Ian GIDDY Stern School of Business New York University.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

InternationalEquity Markets

Prof. Ian GIDDYStern School of Business

New York University

Copyright ©2003 Ian H. Giddy Equity markets 2

Emerging Market Financing

Emerging markets

Equity

Debt

Copyright ©2003 Ian H. Giddy Equity markets 3

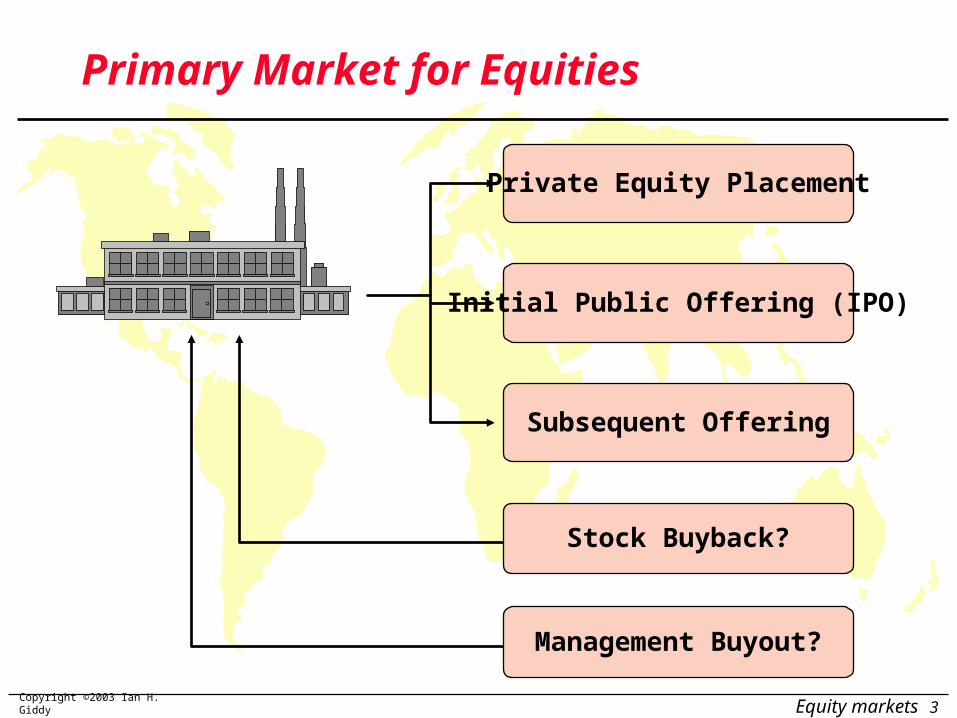

Primary Market for Equities

Initial Public Offering (IPO)

Subsequent Offering

Private Equity Placement

Stock Buyback?

Management Buyout?

Copyright ©2003 Ian H. Giddy Equity markets 4

Investment Banking Arrangements

Underwritten vs. “Best Efforts”Underwritten: firm commitment on

proceeds to the issuing firmBest Efforts: no firm commitment

Negotiated vs. Competitive BidNegotiated: issuing firm negotiates terms

with investment bankerCompetitive bid: issuer structures the

offering and secures bids

Copyright ©2003 Ian H. Giddy Equity markets 5

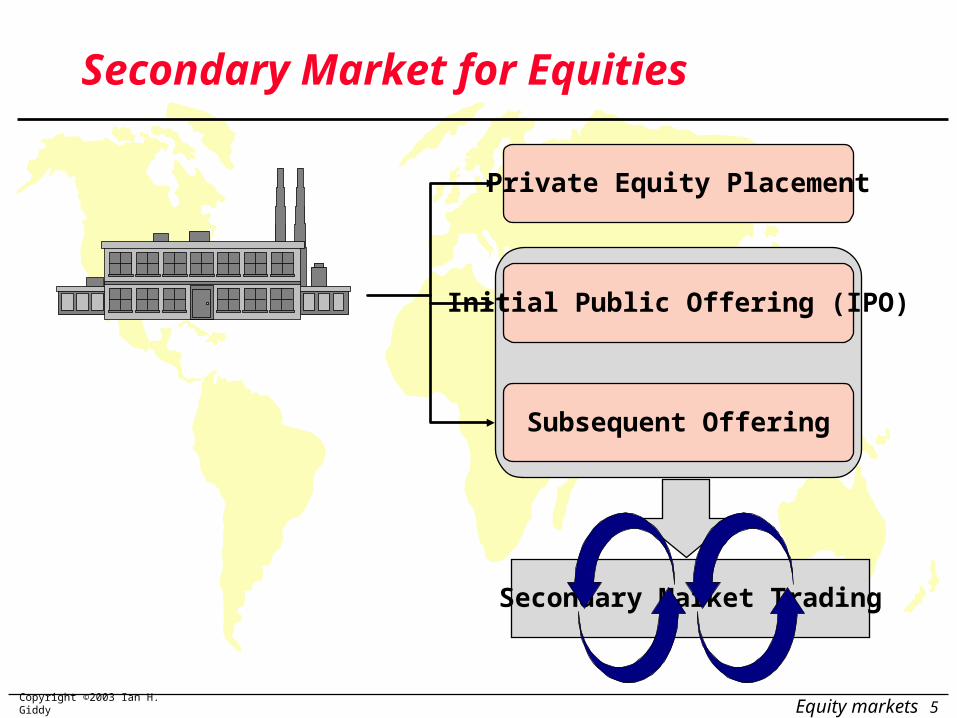

Secondary Market Trading

Secondary Market for Equities

Initial Public Offering (IPO)

Subsequent Offering

Private Equity Placement

Copyright ©2003 Ian H. Giddy Equity markets 6

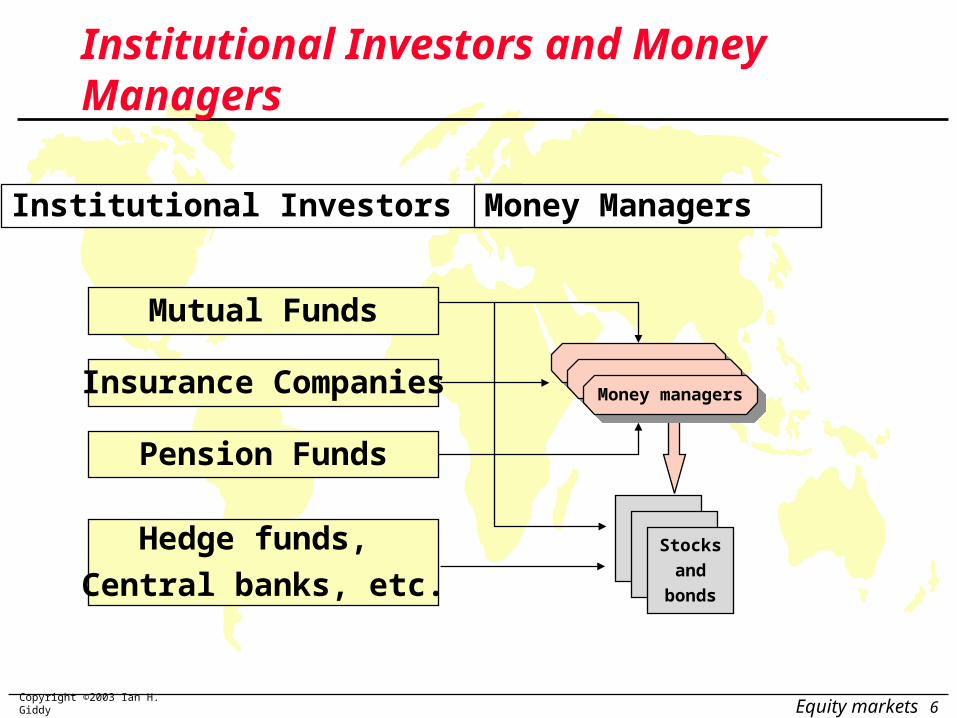

Institutional Investors and Money Managers

Institutional Investors Money Managers

Mutual Funds

Insurance Companies

Pension Funds

Hedge funds,

Central banks, etc.

Stocks

and

bonds

Money managersMoney managers

Copyright ©2003 Ian H. Giddy Equity markets 7

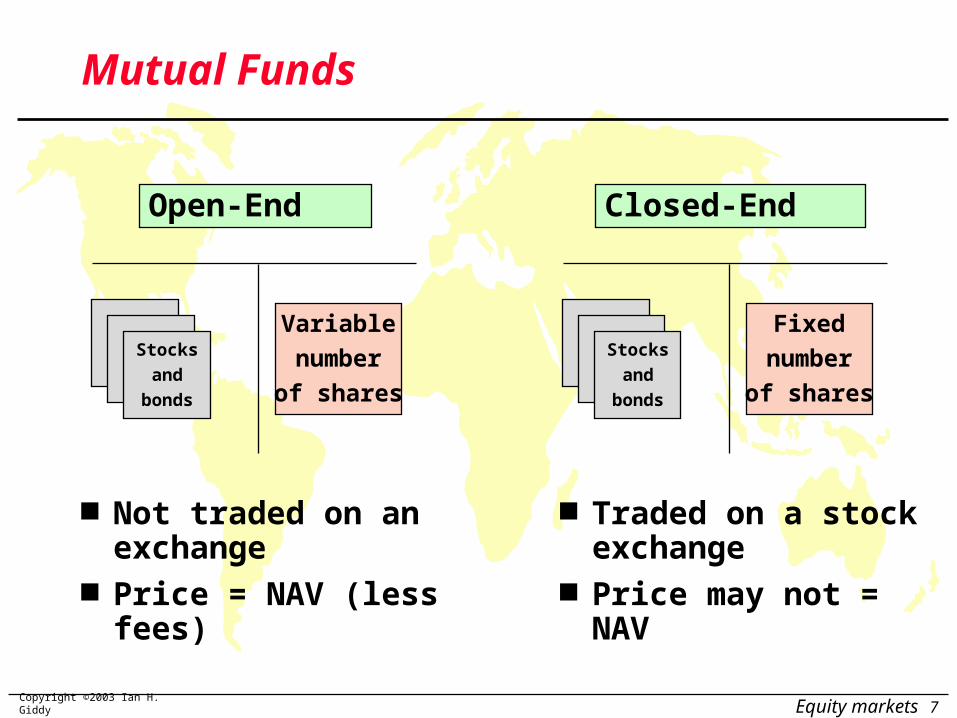

Mutual Funds

Open-End Closed-End

Stocks

and

bonds

Variable

number

of shares

Not traded on an exchange

Price = NAV (less fees)

Stocks

and

bonds

Fixed

number

of shares

Traded on a stock exchange

Price may not = NAV

Copyright ©2003 Ian H. Giddy Equity markets 9

Raising Capital for Emerging Market Companies

Debt

Equity

Copyright ©2003 Ian H. Giddy Equity markets 10

Raising Capital for Emerging Market Companies

Debt

Equity

Domestic market

Foreign market

Euromarket

Copyright ©2003 Ian H. Giddy Equity markets 11

Raising Capital for Emerging Market Companies

Debt

Equity

Domestic market

Foreign market

Euromarket

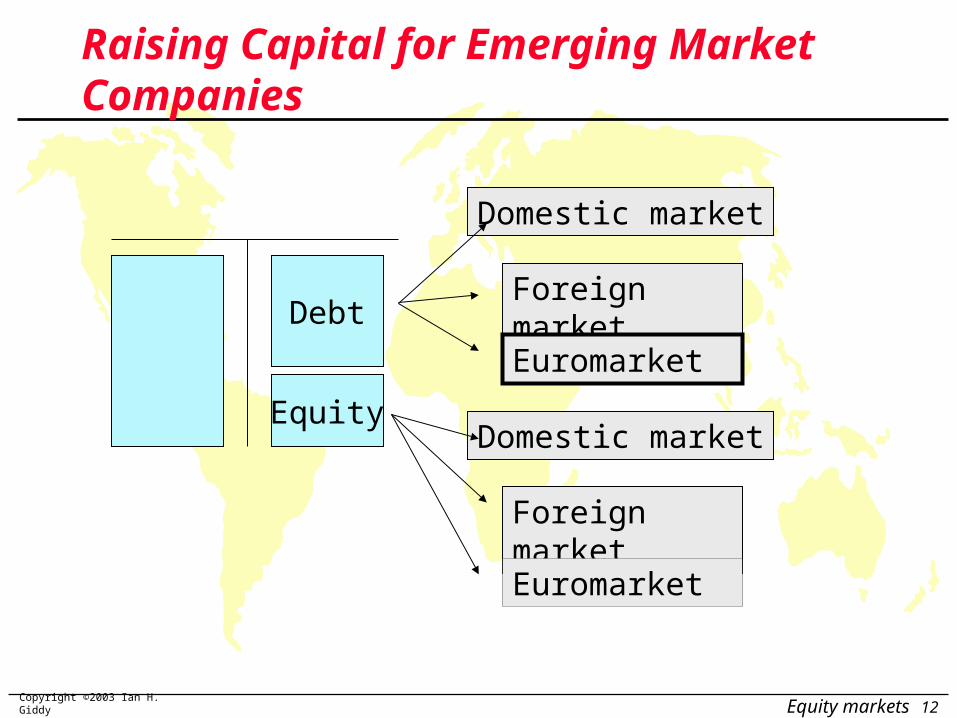

Copyright ©2003 Ian H. Giddy Equity markets 12

Raising Capital for Emerging Market Companies

Debt

Equity

Domestic market

Foreign market

Euromarket

Domestic market

Foreign market

Euromarket

Copyright ©2003 Ian H. Giddy Equity markets 13

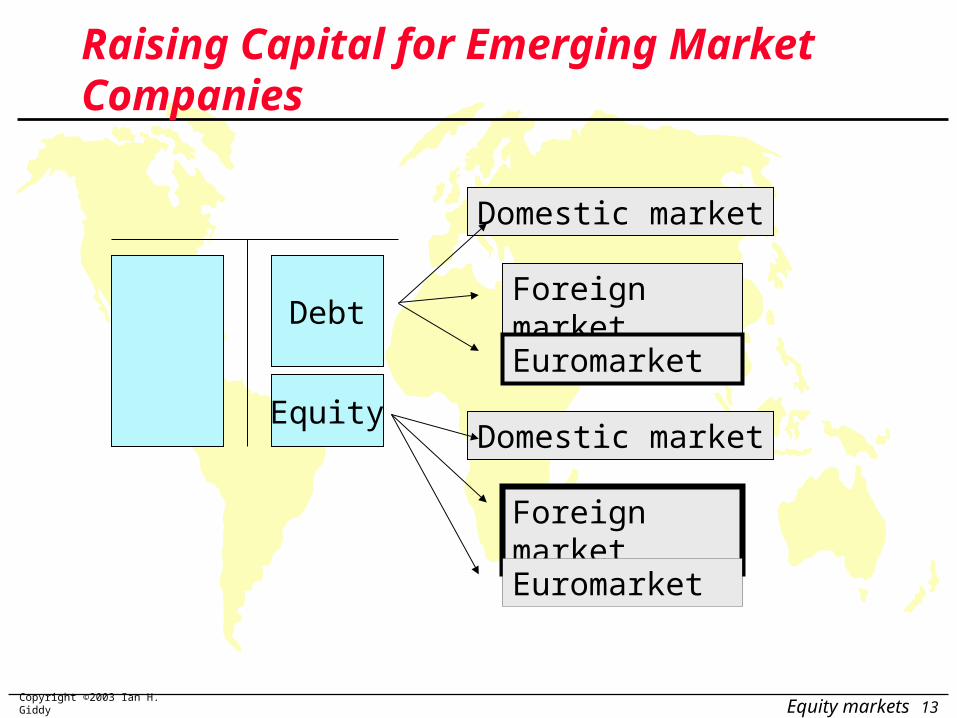

Raising Capital for Emerging Market Companies

Debt

Equity

Domestic market

Foreign market

Euromarket

Domestic market

Foreign market

Euromarket

Copyright ©2003 Ian H. Giddy Equity markets 14

Raising Capital for Emerging Market Companies

Debt

Equity

Domestic market

Foreign market

Euromarket

Domestic market

Foreign market

Euromarket

Copyright ©2003 Ian H. Giddy Equity markets 15

Debt

EquityDomestic marketForeign market

Can globally mobile investors capture value & control?

yesno(Russia) (S Africa)

Copyright ©2003 Ian H. Giddy Equity markets 17

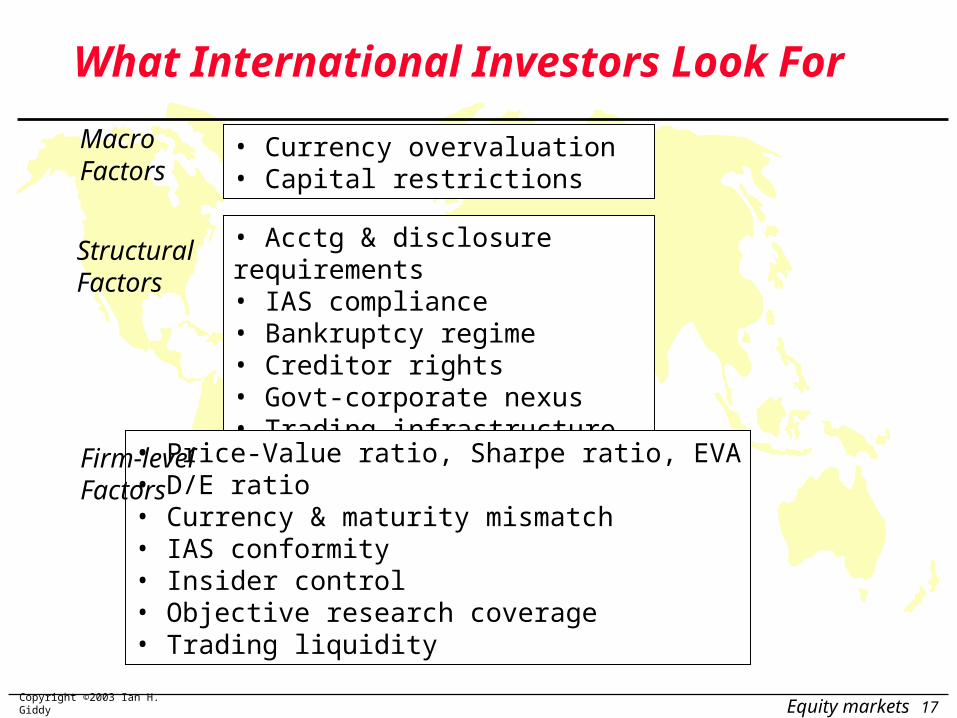

MacroFactors

• Currency overvaluation• Capital restrictions

StructuralFactors

• Acctg & disclosure requirements• IAS compliance• Bankruptcy regime• Creditor rights• Govt-corporate nexus• Trading infrastructure

• Price-Value ratio, Sharpe ratio, EVA• D/E ratio• Currency & maturity mismatch• IAS conformity• Insider control• Objective research coverage• Trading liquidity

Firm-levelFactors

What International Investors Look For

Prof. Ian GiddyNew York University

Investment Bankingand Underwriting

Copyright ©2003 Ian H. Giddy Equity markets 21

Underwriting Sequence

Engagement: Mandate signed by issuer engaging lead manager

Due Diligence: Conducted by Lead manager

Documentation: Loan agreement, Prospectus

Signing: Underwriting agreement signed and issue priced

Closing: Settlement of the offering

EngagementEngagement

Due Diligence and

Documentation

Due Diligence and

Documentation

Signing and PricingSigning and Pricing

ClosingClosing

“Beauty Contest”“Beauty Contest”

Copyright ©2003 Ian H. Giddy Equity markets 25

Distribution

Lead ManagerBook-Runner

“International Coordinator

Joint Co-Lead

ManagerJoint Co-Lead

ManagerJoint Co-Lead

Managers

Lead

ManagerLead

ManagerLead

Managers

ManagerManagerManagers Selling Agent

Co-Lead Manager

Question 1:Which banks were involved with the DT IPO, and what were their roles?

Copyright ©2003 Ian H. Giddy Equity markets 35

Pricing

Debt Instruments Bonds priced according

to yield over benchmark (spread)

Yield too low – issue does not sell

Yield too high – too much given away

Generally syndicate holds price for a day; in a successful issue yields gradually tighten

Equity Mature issue: based on

current market price and market conditions, small premium for dilution; comparables

IPO: comparables and discounted cash flow analysis

Question 2:What price should DT

shares have, based on:(a)Book value(b)P/E ratio(c)Future cash flows

Copyright ©2003 Ian H. Giddy Equity markets 36

Deutsche Telekom: Group work 11:20-12:20

Question 1:Which banks were involved with the DT IPO, and what were their roles? Question 2:

What price should DT shares have, based on:

(a) Book value(b) P/E ratio(c) Future cash flows

Prof. Ian GiddyNew York University

Raising and PricingEquity

Copyright ©2003 Ian H. Giddy Equity markets 39

Raising Equity: The Investment Banker’s Job

Market conditions Corporate needs Valuation Information Distribution

Telekom

Telekom

Copyright ©2003 Ian H. Giddy Equity markets 40

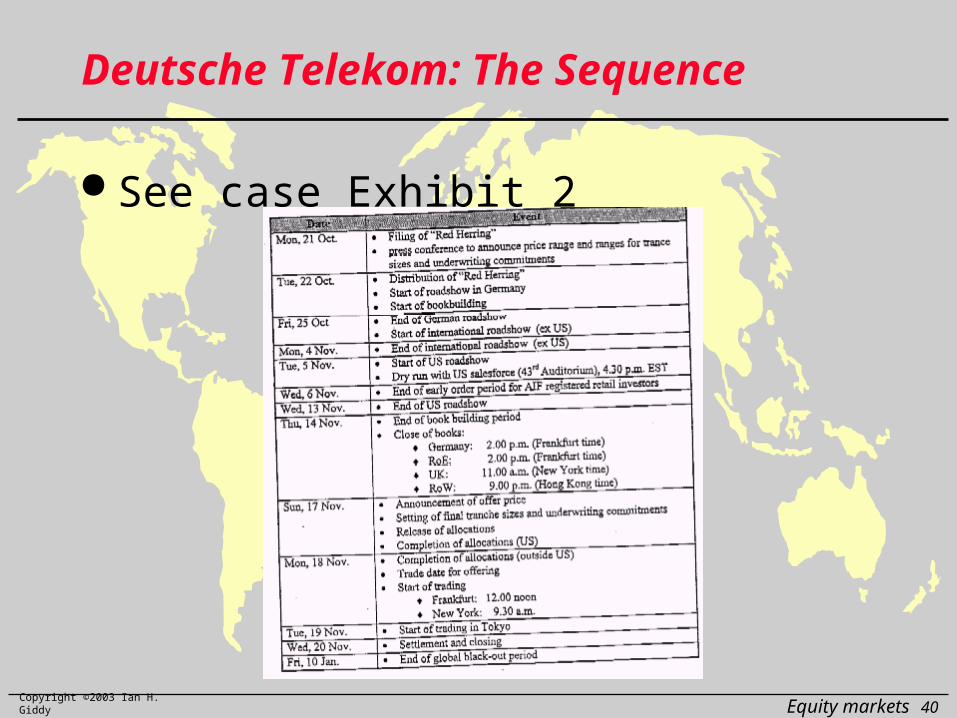

Deutsche Telekom: The Sequence

See case Exhibit 2

Copyright ©2003 Ian H. Giddy Equity markets 41

What’s a Company Worthto Investors?

Required Returns Types of Models

Balance sheet modelsDividend discount & corporate cash flow

modelsPrice/Earnings ratiosOption models

Estimating Growth Rates

Telekom

Telekom

Copyright ©2003 Ian H. Giddy Equity markets 42

Equity Valuation: From the Balance Sheet

Value of Assets Book Liquidation Replacement

Value of Liabilities

Book Market

Value of Equity

Copyright ©2003 Ian H. Giddy Equity markets 43

Deutsche Telekom: Book Value

See case Exhibit 3

Copyright ©2003 Ian H. Giddy Equity markets 44

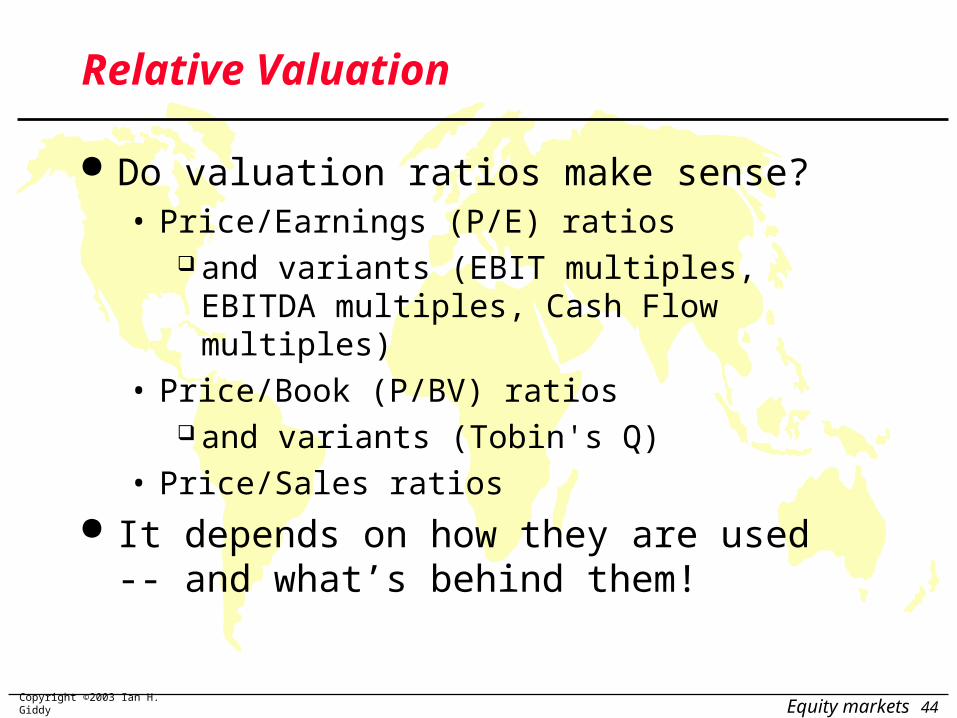

Relative Valuation

Do valuation ratios make sense?• Price/Earnings (P/E) ratios

and variants (EBIT multiples, EBITDA multiples, Cash Flow multiples)

• Price/Book (P/BV) ratios and variants (Tobin's Q)

• Price/Sales ratios

It depends on how they are used -- and what’s behind them!

Copyright ©2003 Ian H. Giddy Equity markets 45

Deutsche Telekom:Ratios and Comparables

See case page 9

Copyright ©2003 Ian H. Giddy Equity markets 46

Discounted Cashflow Valuation: Basis for Approach

where n = Life of the asset CFt = Cashflow in period t r = Discount rate reflecting the

riskiness of the estimated cashflows

Value = CFt

(1+ r)tt =1

t = n

Copyright ©2003 Ian H. Giddy Equity markets 47

Deutsche Telekom: Earnings

See case page 8

Copyright ©2003 Ian H. Giddy Equity markets 48

Valuing a Firm with DCF: An Illustration

Historical financial results

Adjust for nonrecurring aspects

Gauge future growth

Adjust for noncash items

Projected sales and operating profits

Projected free cash flows to the firm (FCFF)

Year 1 FCFF

Year 2 FCFF

Year 3 FCFF

Year 4 FCFF

Terminal year FCFF

Stable growth model or P/E comparable

Present value of free cash flows

+ cash, securities & excess assets

- Market value of debt

Value of shareholders equity

…

Discount to present using weighted average cost of capital (WACC)

Copyright ©2003 Ian H. Giddy Equity markets 49

Telkom South Africa

1. Why did South Africa follow its initial 30% privatization of Telkom with an initial public offering? What are the advantages and disadvantages of a public listing for a company?

2. What is an ADR? Why did Telkom use the ADR technique in conjunction with its Johannesburg IPO?

3. What does a company have to do to ensure a successful IPO? What makes shares attractive to investors?

4. Was the Telkom IPO priced correctly? How would you value a company in order to judge the price for an IPO?

Copyright ©2003 Ian H. Giddy Equity markets 50

Related Documents