International Adjustment and the Great Recession Dr. Catherine L. Mann Professor, Brandeis International Business School Visiting Scholar, Federal Reserve Bank of Boston Senior Fellow, Peterson Institute for International Economics CLMann @Brandeis.edu Northeastern University, January 26, 2010

International Adjustment and the Great Recession Dr. Catherine L. Mann Professor, Brandeis International Business School Visiting Scholar, Federal Reserve.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Adjustmentand the

Great Recession

Dr. Catherine L. Mann

Professor, Brandeis International Business School Visiting Scholar, Federal Reserve Bank of Boston

Senior Fellow, Peterson Institute for International Economics

CLMann @Brandeis.edu

Northeastern University, January 26, 2010

2

Outline

Why an international lens?

Domestic vs. International adjustment in Great Recession

Adjustment in trade patterns and products

Adjustment in asset ownership and instruments

Observations for policymakers

3

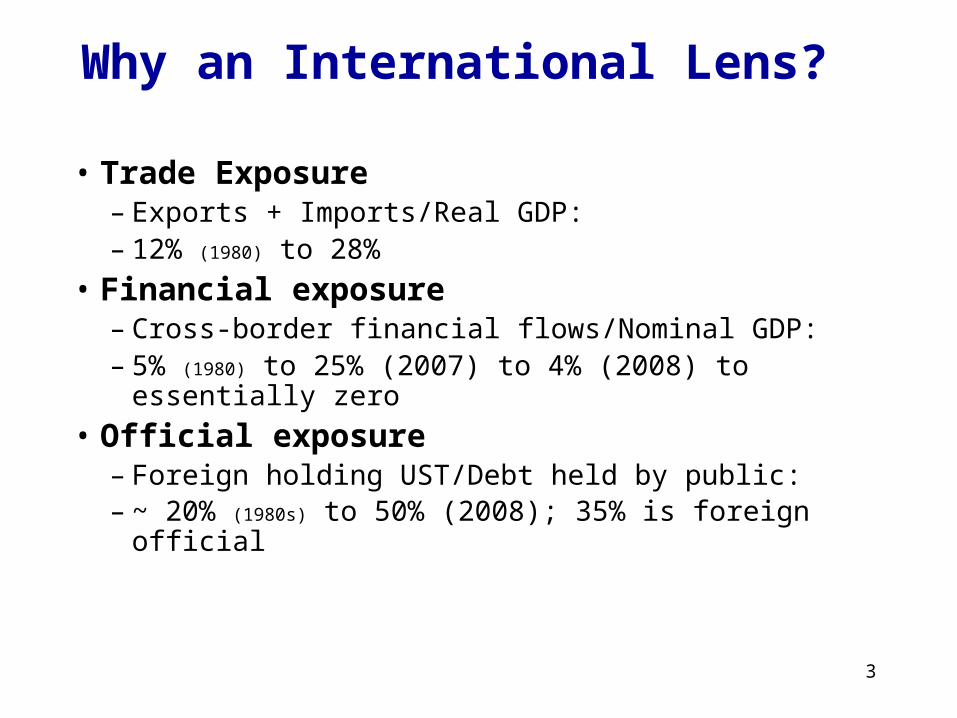

Why an International Lens?

• Trade Exposure– Exports + Imports/Real GDP: – 12% (1980) to 28%

• Financial exposure– Cross-border financial flows/Nominal GDP:– 5% (1980) to 25% (2007) to 4% (2008) to essentially zero

• Official exposure– Foreign holding UST/Debt held by public:– ~ 20% (1980s) to 50% (2008); 35% is foreign official

4

Overall Adjustment: Domestic vs. International

Recessions Compared

This recession: Significant external sector support of GDPInto recession: + X and –M kept GDP growth + in 2007/early 2008, In recession: significant NX offset contracting PCE and drop in I

BEA, NIPA table 1.1.2

5

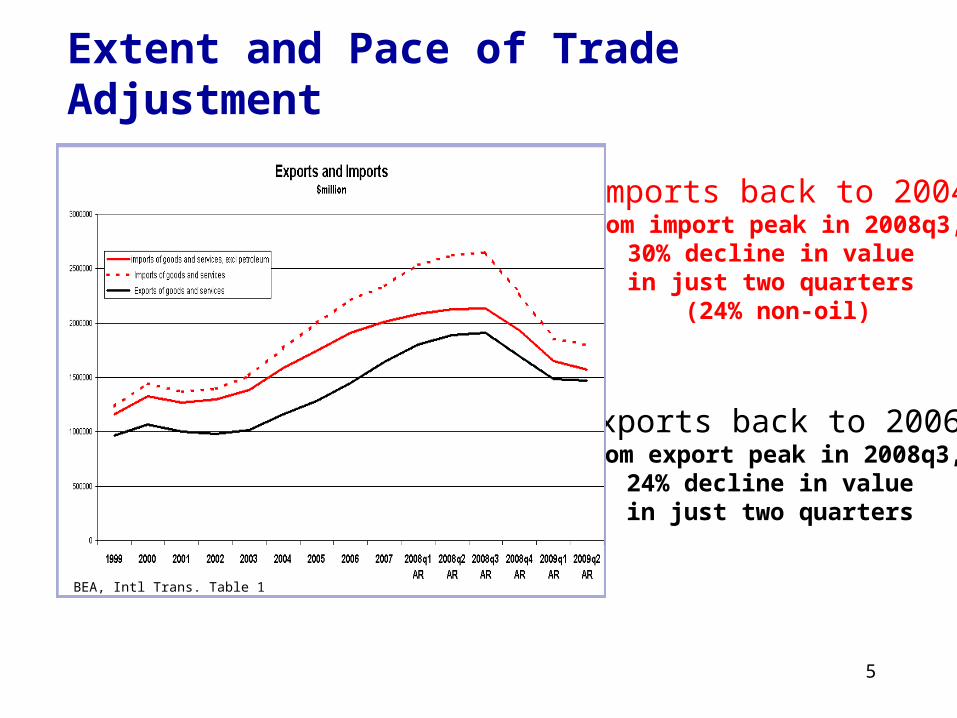

Imports back to 2004From import peak in 2008q3,

30% decline in value in just two quarters

(24% non-oil)

Exports back to 2006From export peak in 2008q3,

24% decline in value in just two quarters

Extent and Pace of Trade Adjustment

BEA, Intl Trans. Table 1

6

Pattern of Adjustment: Import by Product

Auto and durables led contraction, but consumer imports now stableInvestment goods contraction dominates import decline

BEA, Intl Trans. Table 2a and Table 1

7

Pattern of Adjustment: Imports

Asia:37% of trade

27% of adjustmentless than expected

Asia ‘protected’ from downturn

8

Pattern of Adjustment: Exports

Investment goods decline catastrophic, and still worseningAuto supply chain stabilized

BEA, Intl Trans. Table 2a and Table 1

9

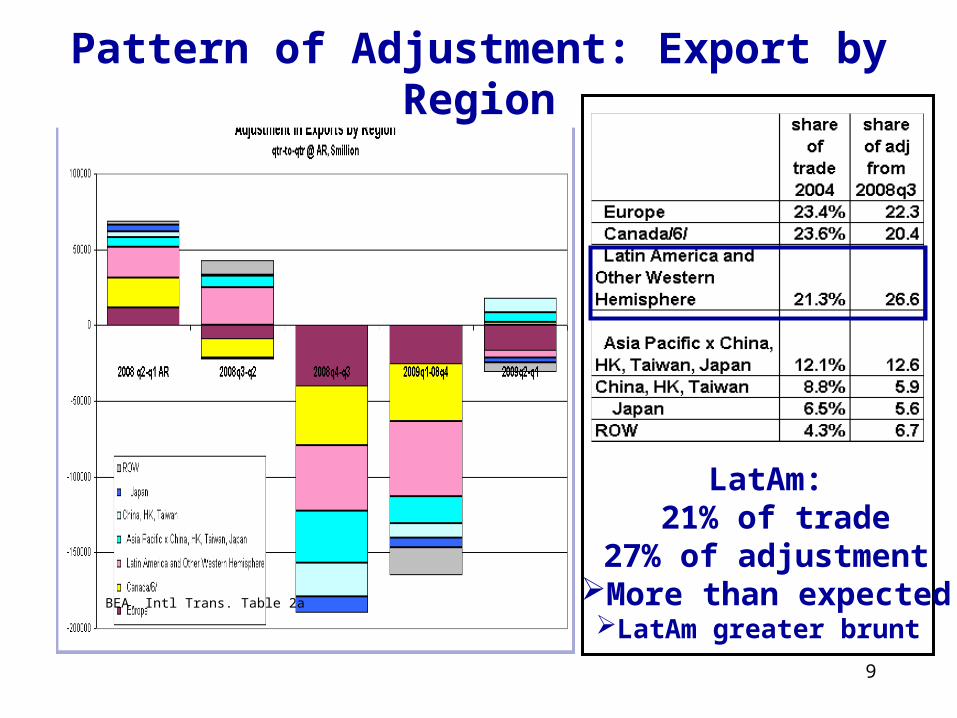

Pattern of Adjustment: Export by Region

BEA, Intl Trans. Table 2a

LatAm: 21% of trade

27% of adjustmentMore than expectedLatAm greater brunt

10

Extent and Pace of Financial AdjustmentUnprecedented

Almost never before (ex.1990q1) have foreign investors, net, left the U.S.Very infrequently have US investors, net, come ‘home’

(87q1, 88q1,99q1,01q3,02q3,05q4 and never for more than 1 qtr)

BEA, Intl Trans. Table 1

11

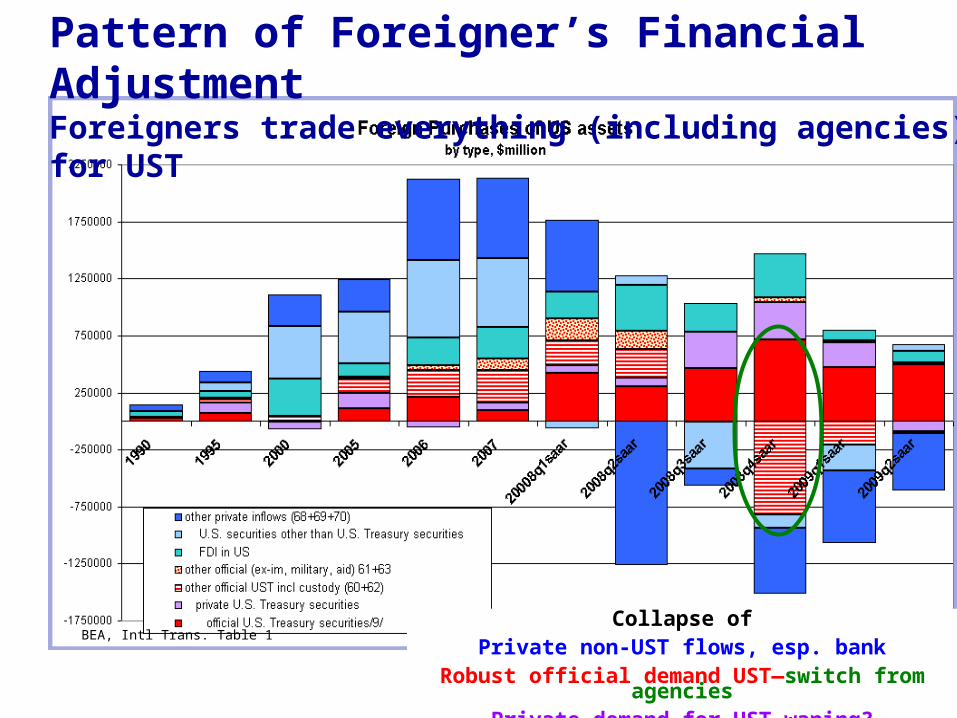

Pattern of Foreigner’s Financial AdjustmentForeigners trade everything (including agencies) for UST

BEA, Intl Trans. Table 1 Collapse of

Private non-UST flows, esp. bankRobust official demand UST—switch from agencies

Private demand for UST waning?

12

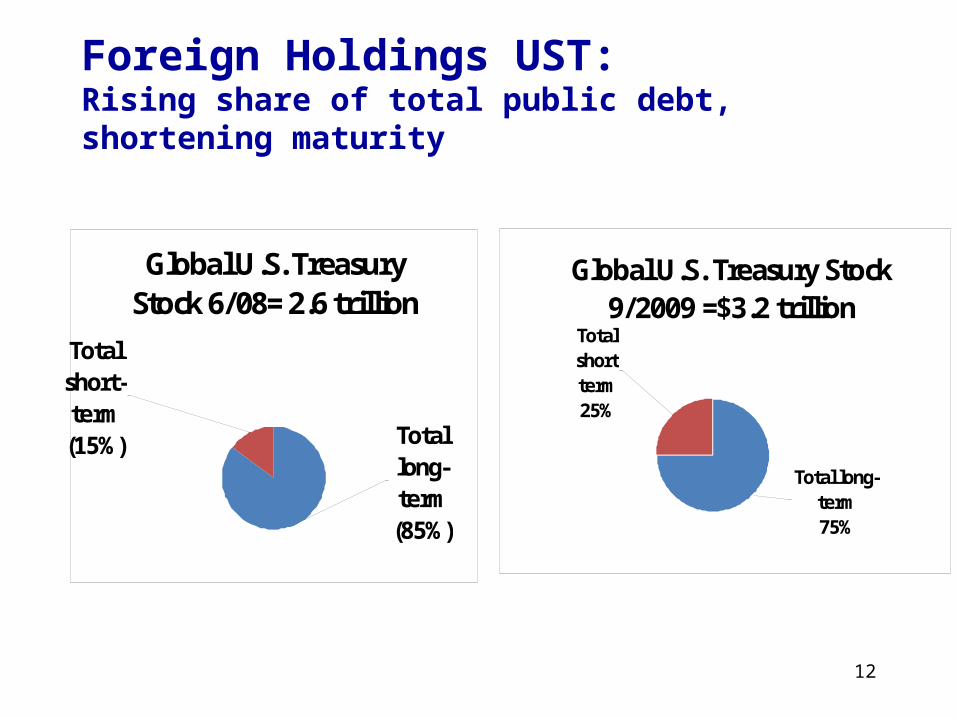

Foreign Holdings UST: Rising share of total public debt, shortening maturity

Global U.S. Treasury Stock 6/08= 2.6 trillion

Total long-term (85%)

Total short-term (15%)

Global U.S. Treasury Stock 9/2009 =$3.2 trillion

Total short term 25%

Total long-term 75%

13

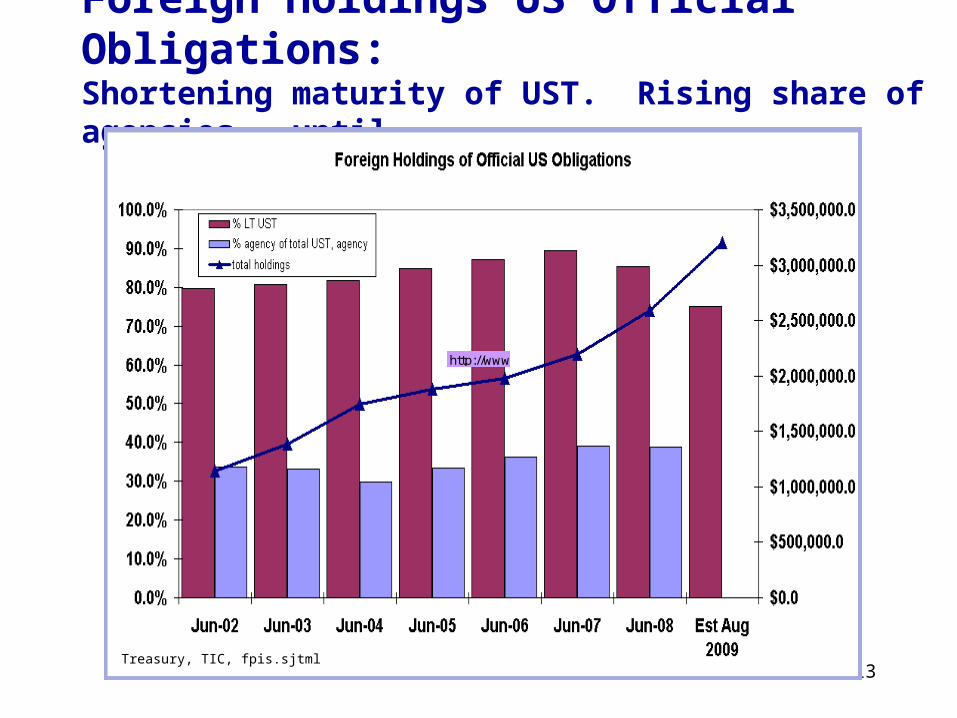

Foreign Holdings US Official Obligations: Shortening maturity of UST. Rising share of agencies.. until…

http://www.ustreas.gov/tic/fpis.shtml

Treasury, TIC, fpis.sjtml

14BEA, Intl Trans, table 5.

Foreign Official Purchases of Official US Assets: All Asia. Shortening maturity? What to buy without agencies?

15

China and Japan: Key holdersNot only UST but even more of Agency securities

Treasury, TIC, fpis.sjtml

16

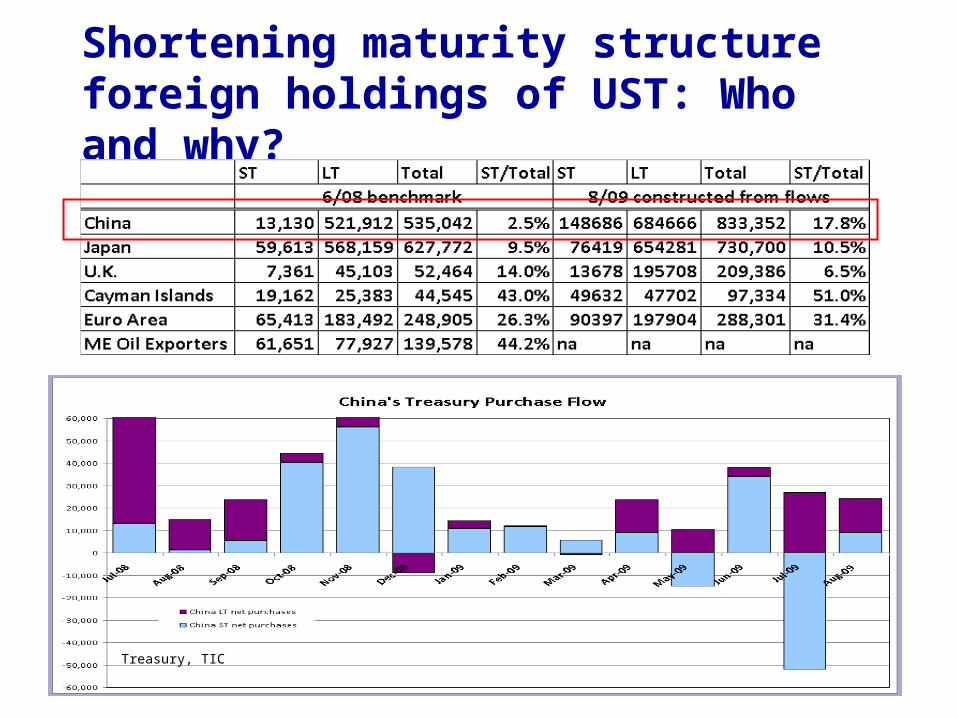

Shortening maturity structure foreign holdings of UST: Who and why?

Treasury, TIC

17

Summary: Trade Story

• Consumer-led recession

– but biggest import adjustment is via investment goods.

• Reviving consumer demand

– implies imports and return to a widening trade deficit,

sustainability issues

• Adjustment is less via Asia imports than expected,

more via LatAm exports than expected

– In large part due to differences in exchange rate adjustment

18

Summary: Finance Story

• Unprecedented adjustment in international capital

flows. – What explains the shortening maturity?

– And what will replace agency securities?

• Rising concentration of holdings of UST in Asia– A counterpart of exchange rate story and trade story

19

Policy Observations• Policies to support consumers or business?

– Why not buy business CDOs instead of MBS?– Purchasing mortgages is particularly blunt approach

– Reviving implies widening trade deficit, sustainability issues • Policies for attracting capital flows?

– Is shortening maturity evidence of concern over inflation?

– What if foreign participation in US Treasury auctions lags?

• Potential complications – rising trade deficit at the same time as desire of foreigners to

buy US bonds lags

– higher interest rates, depreciating dollar.

Related Documents