Internal Internal Control and Control and Cash Cash PowerPoint Slides to accompany Fundamental Accounting Principles, 14ce Prepared by Joe Pidutti, Durham College CHAPTER 8 © 2013 McGraw-Hill Ryerson Limited.

Internal Control and Cash PowerPoint Slides to accompany Fundamental Accounting Principles, 14ce Prepared by Joe Pidutti, Durham College CHAPTER 8 © 2013.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Internal Internal Control and Control and

CashCash

PowerPoint Slides to accompanyFundamental Accounting Principles, 14ce

Prepared byJoe Pidutti, Durham College

CHAPTER

8

© 2013 McGraw-Hill Ryerson Limited.

1. Define, explain the purpose, and identify the principles of internal control. (LO1)

2. Define cash and explain how it is reported. (LO2)

3. Apply internal control to cash. (LO3)

4. Explain and record petty cash fund transactions. (LO4)

2 © 2013 McGraw-Hill Ryerson Limited.

Learning ObjectivesLearning Objectives

5. Explain and identify banking activities and the control features they provide. (LO5)

6. Prepare a bank reconciliation and journalize any resulting adjustment(s). (LO6)

7. Calculate the acid-test ratio and explain its use as an indicator of a company’s liquidity. (Appendix 8A) (LO7)

3 © 2013 McGraw-Hill Ryerson Limited.

Learning ObjectivesLearning Objectives

All policies and procedures used to :• Protect assets• Ensure reliable accounting• Promote efficient operations• Encourage adherence to company

policies

4 © 2013 McGraw-Hill Ryerson Limited.

Internal Control SystemInternal Control System

LO 1

5 © 2013 McGraw-Hill Ryerson Limited.

1. Ensure transactions and activities are authorized.

2. Maintain adequate records.

3. Insure assets and bond key employees.

4. Separate recordkeeping and custody of assets.

5. Establish a separation of duties.

Principles of Internal ControlPrinciples of Internal Control

LO 1

6 © 2013 McGraw-Hill Ryerson Limited.

6. Apply technological controls.

7. Perform internal and external audits.

Internal controls will vary based on the nature and size of the organization.

Principles of Internal ControlPrinciples of Internal Control

LO 1

Human Error• Negligence• Fatigue• Misjudgment• Confusion

Human Fraud

Intent to defeat internal controls for personal gain. Costs vs. Benefits The costs of internal control must not exceed their

benefits.

Limitations of Internal ControlLimitations of Internal Control

7 © 2013 McGraw-Hill Ryerson Limited. LO 1

• Is an important asset for every company.• Control of cash on hand and access to it is

critical.

Cash includes:• Currency • Coins• Deposits in bank accounts• Other items acceptable for deposit

8 © 2013 McGraw-Hill Ryerson Limited.

CashCash

LO 2

• Refers to how easily an asset can be converted into another asset or used in paying for services or obligations.

• Cash and similar assets are called liquid assets.

• Companies must own some liquid assets to pay their obligations.

9 © 2013 McGraw-Hill Ryerson Limited.

LiquidityLiquidity

LO 2

Guidelines:

1. Separate handling of cash from recordkeeping of cash.

2. Deposit cash receipts daily.

3. Make cash disbursements by cheque.

10 © 2013 McGraw-Hill Ryerson Limited.

Internal Control for CashInternal Control for Cash

LO 3

Internal control over cash receipts ensures that all cash received is properly recorded and deposited. These controls include:•The use of cash registers for over-the-counter cash sales.•The separation of recordkeeping and custody of cash.

11 © 2013 McGraw-Hill Ryerson Limited.

Control of Cash ReceiptsControl of Cash Receipts

LO 3

• All expenditures should be made by cheque. The only exception is for small payments from petty cash.

• Separate authorization, cheque signing, and recordkeeping duties.

• Apply a voucher system.

12 © 2013 McGraw-Hill Ryerson Limited.

Control of Cash DisbursementsControl of Cash Disbursements

LO 3

Mini-QuizMini-Quiz

An internal control system is all policies and procedures managers use to:

a)Protect assets.

b)Ensure reliable accounting.

c)Promote efficient operations.

d)Urge adherence to company policies.

e)All of the above.

13 © 2013 McGraw-Hill Ryerson Limited.

Mini-QuizMini-Quiz

An internal control system is all policies and procedures managers use to:

a)Protect assets.

b)Ensure reliable accounting.

c)Promote efficient operations.

d)Urge adherence to company policies.

e)All of the above.

14 © 2013 McGraw-Hill Ryerson Limited.

Good internal control procedures require cash disbursements be made by cheque.

The exception: Small payments required in most

companies for items such as postage, courier fees, repairs, and supplies.

15 © 2013 McGraw-Hill Ryerson Limited.

Petty Cash System of Internal Petty Cash System of Internal ControlControl

LO 4

Cashier’s Office Petty Cashier

GENERAL JOURNAL Page 4Date Description PR Debit Credit

May 1 Petty Cash 150

Cash 150

To establish a petty cash fund

Operating a Petty Cash FundOperating a Petty Cash Fund

Prepares cheque to

establish petty cash fund.

16 © 2013 McGraw-Hill Ryerson Limited. LO 4

The petty cashier makes payments from this fund for small disbursements.

… and ensures a petty cash receipt is signed by the person receiving the money to easily identify the expenses paid from petty cash.

17 © 2013 McGraw-Hill Ryerson Limited.

Operating a Petty Cash FundOperating a Petty Cash Fund

LO 4

GENERAL JOURNAL Page 4Date Description PR Debit Credit

May 15 Postage Expense 46

Courier Expense 80

Cash 126

A cheque is issued and the fund is replenished when the amount of cash on hand becomes low.

18 © 2013 McGraw-Hill Ryerson Limited.

Operating a Petty Cash FundOperating a Petty Cash Fund

A cash over and short account is used if needed.

LO 4

19 © 2013 McGraw-Hill Ryerson Limited.

Operating a Petty Cash FundOperating a Petty Cash Fund

LO 4

Cash required to replenish petty cash

= Fund size Cash remaining

-

Cash over/(short)=

Total of petty cash receipts

- Cash required to replenish petty cash

Basic Bank Services• Bank account• Bank deposits and cheques• Electronic funds transfer• Bank credit card transactions• Debit card transactions

20 © 2013 McGraw-Hill Ryerson Limited.

Banking Activities as ControlsBanking Activities as Controls

LO 5

• Many companies allow customers to use bank credit cards for their purchases.

• The risk of bad debts is transferred to the credit card company.

• The company collects cash from the sale quickly.

• The credit card companies charge a fee to the vendor.

21 © 2013 McGraw-Hill Ryerson Limited.

Credit Card TransactionsCredit Card Transactions

LO 5

TechCom has $100 of credit card sales with a 4% fee and cash is received immediately (assume cost of sales is $40).

GENERAL JOURNAL Page 8Description PR Debit Credit

Aug. 15 Cash 96.00

Credit Card Expense 4.00

Sales 100.00

To record credit card expense less 4% fee

15 Cost of Goods Sold 40.00 Merchandise Inventory 40.00

To record cost of sales

Date

22 © 2013 McGraw-Hill Ryerson Limited.

Illustration-Credit Card Illustration-Credit Card TransactionTransaction

LO 5

• Many companies allow customers to use debit cards for their purchases.

• The bank transfers funds from the customer’s account to the vendor’s bank account.

• The bank charges a fee to the vendor.• The entries are identical to a bank credit

card sale.

23 © 2013 McGraw-Hill Ryerson Limited.

Debit Card TransactionsDebit Card Transactions

LO 5

Bank reconciliations are:• Prepared periodically to explain the

difference between cash reported on the bank statement and the cash balance on company’s books.

• An important element of internal control.

Bank ReconciliationsBank Reconciliations

24 © 2013 McGraw-Hill Ryerson Limited. LO 6

The bank statement provides information

about everything that has gone

through the bank account for a given

period of time.

CM – Credit MemoDM – Debit MemoEC – Error CorrectionIN – Interest EarnedNSF – Non-sufficient FundsOD – OverdraftSC – Service Charge

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58 16 23.00 DM 150.00 2,126.58

17 122 70.00 485.00 2,541.58 18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58

29 128 135.00 2,041.58

31 IN 8.42 2,050.00

National BankHamilton, ON L8P 2X5

Bank Statement

Statement Date901 Main Street

Daily Balance

Hamilton, ON L8P 2J8

VideoBuster Company

723.00 1,163.42

Deposits and Credits

Cheques and Debits

Account Number

Total Cheques and Debits

Total Deposits and Credits

25 © 2013 McGraw-Hill Ryerson Limited. LO 6

Cheque # Amount119 55.00$

120 200.00 121 120.00

122 70.00 123 25.00 124 150.00 125 15.00

126 200.00

127 50.00

128 135.00

1,020.00$

(101)

Cash Disbursements Journal

The general ledger, cash receipts, and

cash disbursements journals provide

information about everything that has gone through our

accounting records for a given period of

time.

26 © 2013 McGraw-Hill Ryerson Limited. LO 6

*

Bank Reconciliation - Example

27 © 2013 McGraw-Hill Ryerson Limited.

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58

16 23.00 DM 150.00 2,126.58

17 122 70.00 485.00 2,541.58

18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58 29 128 135.00 2,041.58

31 IN 8.42 2,050.00

Total Deposits and Credits

901 Main Street

National BankHamilton, ON L8P 2X5

Account Number

Total Cheques and Debits

Bank Statement

Statement Date

Daily Balance

Hamilton, ON L8P 2J8

VideoBuster Company

723.00 1,163.42

Deposits and Credits

Cheques and Debits

Date Explanation PR Debit Credit Balance30-Sep Balance 1,609.58 31-Oct CR6 815.00 2,424.58 31-Oct CD4 1,020.00 1,404.58

Cash Account # 101

General Ledger Cash Account

Why are the balances different?

Some items are reflected on the bank statement but not in the accounting records and vice versa.

LO 6

Reconciling ItemsReconciling Items

Bank Statement• Outstanding

cheques.• Deposits in transit.• Bank errors.

General Ledger• Non-sufficient funds

cheque (NSF).• Bank service charges.• Interest earned on

bank account.• Collections made by

the bank.• Book errors.

28 © 2013 McGraw-Hill Ryerson Limited. LO 6

Let’s prepare the bank reconciliation for VideoBuster Company at the end of October 31, 2014.

29 © 2013 McGraw-Hill Ryerson Limited. LO 6

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58

16 23.00 DM 150.00 2,126.58

17 122 70.00 CM 485.00 2,541.58

18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58 29 128 135.00 2,041.58

31 IN 8.42 2,050.00

Daily Balance

1,163.42

Total Deposits and Credits

901 Main Street

Deposits and Credits

Cheques and Debits

National BankHamilton, ON L8P 2X5

Account Number

Total Cheques and Debits

Bank Statement

Statement DateHamilton, ON L8P 2J8

VideoBuster Company

723.00

DateDeposit Amount

Oct 3 $ 240.00

9 180.00

15 100.00 16 150.00 31 145.00

$ 815.00

(101)

Cash Receipts Journal

Cheque # Amount119 55.00$ 120 200.00

121 120.00

122 70.00

123 25.00 124 150.00 125 15.00 126 200.00

127 50.00 128 135.00

1,020.00$

(101)

Cash Disbursements Journal

These items appear on both the

Cash Receipts Journal and the bank statement;

therefore, none of these items is a reconciling item.

30 © 2013 McGraw-Hill Ryerson Limited.

LO 6

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58

16 23.00 DM 150.00 2,126.58

17 122 70.00 CM 485.00 2,541.58

18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58 29 128 135.00 2,041.58

31 IN 8.42 2,050.00

Hamilton, ON L8P 2J8

VideoBuster Company

723.00

National BankHamilton, ON L8P 2X5

Account Number

Total Cheques and Debits

Bank Statement

Statement Date

Daily Balance

1,163.42

Total Deposits and Credits

901 Main Street

Deposits and Credits

Cheques and Debits

DateDeposit Amount

Oct 3 $ 240.00

9 180.00

15 100.00 16 150.00 31 145.00

$ 815.00

(101)

Cash Receipts Journal

Cheque # Amount119 55.00$ 120 200.00

121 120.00

122 70.00

123 25.00 124 150.00 125 15.00 126 200.00

127 50.00 128 135.00

1,020.00$

(101)

Cash Disbursements Journal

These items appear on both

the Cash Disbursements

Journal AND the bank statement;

therefore, none of these items is a reconciling item.

31 © 2013 McGraw-Hill Ryerson Limited.

LO 6

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58

16 23.00 DM 150.00 2,126.58

17 122 70.00 CM 485.00 2,541.58

18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58 29 128 135.00 2,041.58

31 IN 8.42 2,050.00

Daily Balance

1,163.42

Total Deposits and Credits

901 Main Street

Deposits and Credits

Cheques and Debits

National BankHamilton, ON L8P 2X5

Account Number

Total Cheques and Debits

Bank Statement

Statement DateHamilton, ON L8P 2J8

VideoBuster Company

723.00

DateDeposit Amount

Oct 3 $ 240.00

9 180.00

15 100.00 16 150.00 31 145.00

$ 815.00

(101)

Cash Receipts Journal

Cheque # Amount119 55.00$ 120 200.00

121 120.00

122 70.00

123 25.00 124 150.00 125 15.00 126 200.00

127 50.00 128 135.00

1,020.00$

(101)

Cash Disbursements Journal

These items appear only in the Cash

Receipts Journal OR the Cash

Disbursements Journal OR the bank

statement; therefore, each of these items is a reconciling item.

32 © 2013 McGraw-Hill Ryerson Limited.

LO 6

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58

16 23.00 DM 150.00 2,126.58

17 122 70.00 CM 485.00 2,541.58

18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58 29 128 135.00 2,041.58

31 IN 8.42 2,050.00

Daily Balance

1,163.42

Total Deposits and Credits

901 Main Street

Deposits and Credits

Cheques and Debits

National BankHamilton, ON L8P 2X5

Account Number

Total Cheques and Debits

Bank Statement

Statement DateHamilton, ON L8P 2J8

VideoBuster Company

723.00

The items that show up only on the bank statement are reconciling items on the book side of the bank reconciliation.

33 © 2013 McGraw-Hill Ryerson Limited. LO 6

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58

16 23.00 DM 150.00 2,126.58

17 122 70.00 CM 485.00 2,541.58

18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58 29 128 135.00 2,041.58

31 IN 8.42 2,050.00

Daily Balance

1,163.42

Total Deposits and Credits

901 Main Street

Deposits and Credits

Cheques and Debits

National BankHamilton, ON L8P 2X5

Account Number

Total Cheques and Debits

Bank Statement

Statement DateHamilton, ON L8P 2J8

VideoBuster Company

723.00

Book Balance 1,404.58

Add:

Collection of $500 note less $15 collection fee 485.00 Interest earned 8.42 493.42

1,898.00 Less:

NSF cheque plus s/c 30.00 Cheque printing charge 23.00 53.00

1,845.00

Bank ReconciliationOctober 31, 2014

VIDEOBUSTER COMPANY

34 © 2013 McGraw-Hill Ryerson Limited. LO 6

31-Oct-14494 504 2

Previous Balance

Current Balance

1,609.58 2,050.00

DateNumber Amount Amount

Oct 1 1,609.58

3 119 55.00 240.00 1,794.58 9 123 25.00 180.00 1,949.58

15 127 50.00 100.00 1,999.58

16 23.00 DM 150.00 2,126.58

17 122 70.00 CM 485.00 2,541.58

18 120 200.00 2,341.58 19 125 15.00 2,326.58 20 20.00 NSF

10.00 DM 2,296.58

26 121 120.00 2,176.58 29 128 135.00 2,041.58

31 IN 8.42 2,050.00

Daily Balance

1,163.42

Total Deposits and Credits

901 Main Street

Deposits and Credits

Cheques and Debits

National BankHamilton, ON L8P 2X5

Account Number

Total Cheques and Debits

Bank Statement

Statement DateHamilton, ON L8P 2J8

VideoBuster Company

723.00

Book Balance 1,404.58

Add:

Collection of $500 note less $15 collection fee 485.00 Interest earned 8.42 493.42

1,898.00 Less:

NSF cheque plus s/c 30.00 Cheque printing charge 23.00 53.00

1,845.00

Bank ReconciliationOctober 31, 2014

VIDEOBUSTER COMPANY

35 © 2013 McGraw-Hill Ryerson Limited. LO 6

DateDeposit Amount

Oct 3 $ 240.00

9 180.00

15 100.00 16 150.00 31 145.00

$ 815.00

(101)

Cash Receipts Journal

Cheque # Amount119 55.00$ 120 200.00

121 120.00

122 70.00

123 25.00 124 150.00 125 15.00 126 200.00

127 50.00 128 135.00

1,020.00$

(101)

Cash Disbursements Journal

The items that show up only on the Cash Receipts or Cash Disbursements Journal are reconciling items on the bank side of the bank reconciliation.

36 © 2013 McGraw-Hill Ryerson Limited.

LO 6

DateDeposit Amount

Oct 3 $ 240.00

9 180.00

15 100.00 16 150.00 31 145.00

$ 815.00

(101)

Cash Receipts Journal

Cheque # Amount119 55.00$ 120 200.00

121 120.00

122 70.00

123 25.00 124 150.00 125 15.00 126 200.00

127 50.00 128 135.00

1,020.00$

(101)

Cash Disbursements Journal

Bank Balance 2,050.00$

Add:

Deposit in transit 145.00 2,195.00

Less: Outstanding cheques

No. 124 150.00$ No. 126 200.00 350.00

1,845.00$

VIDEOBUSTER COMPANY

Bank ReconciliationOctober 31, 2014

37 © 2013 McGraw-Hill Ryerson Limited.

LO 6

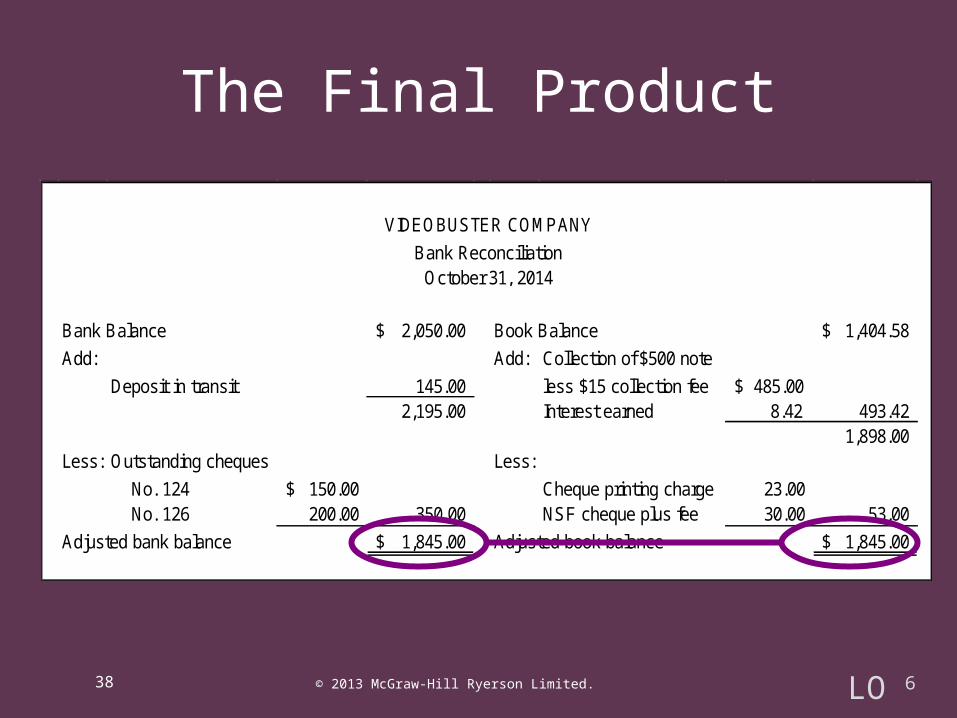

The Final Product

38 © 2013 McGraw-Hill Ryerson Limited.

Bank Balance 2,050.00$ Book Balance 1,404.58$

Add: Add: Collection of $500 note

Deposit in transit 145.00 less $15 collection fee $ 485.00 2,195.00 Interest earned 8.42 493.42

1,898.00 Less: Outstanding cheques Less:

No. 124 150.00$ Cheque printing charge 23.00 No. 126 200.00 350.00 NSF cheque plus fee 30.00 53.00

Adjusted bank balance 1,845.00$ Adjusted book balance 1,845.00$

VIDEOBUSTER COMPANY

Bank ReconciliationOctober 31, 2014

LO 6

Recording Adjusting Entries Recording Adjusting Entries from the Bank Reconciliationfrom the Bank Reconciliation

39 © 2013 McGraw-Hill Ryerson Limited.

GENERAL JOURNAL Page 8Description PR Debit Credit

Oct. 31 Cash 485.00 Collection expense 15.00

Notes Receivable 500.00

To record collection by bank

Oct. 31 Cash 8.42 Interest earned 8.42

To record collection by bank

Date2014

LO 6

GENERAL JOURNAL Page 8Description PR Debit Credit

Oct. 31 Accounts Receivable - Heflin 30.00

Cash 30.00

To record NSF cheque plus s/c

Oct. 31 Office supplies expense 23.00 Cash 23.00

To record cheque printing charge

2014

Date

Recording Adjusting Entries Recording Adjusting Entries from the Bank Reconciliationfrom the Bank Reconciliation

40 © 2013 McGraw-Hill Ryerson Limited. LO 6

Recording Adjusting Entries from Recording Adjusting Entries from Bank ReconciliationBank Reconciliation

After posting the reconciling entries the cash account looks like this . . .

41 © 2013 McGraw-Hill Ryerson Limited.

GENERAL LEDGER

Account: Cash Acct. No. 101 Balance

Date Item PR Debit Credit DR (CR)

2014

Oct. 31 Balance 1,404.58

31 Adjusting entry G8 485.00 1,889.58

31 Adjusting entry G8 8.42 1,898.00 31 Adjusting entry G8 30.00 1,868.00 31 Adjusting entry G8 23.00 1,845.00

Adjusted balance on October 31LO 6

ReviewReview

Discuss the purpose of a bank reconciliation.A bank reconciliation is a procedure designed to explain the differences between the balance in a firm's bank account and the balance on the period's bank statement. The reconciliation procedure examines the differences based on the information available to each party and adjusts for the differences. It also serves as a format for the discovery and correction of recording errors.

42 © 2013 McGraw-Hill Ryerson Limited.

ReviewReview

Identify the principles of internal control. Principles of internal control include the following: • establishing responsibilities• maintaining adequate records• insuring assets and bonding key employees• separating recordkeeping from custody of assets• dividing responsibilities for related transactions• applying technological controls• performing regular independent reviews

43 © 2013 McGraw-Hill Ryerson Limited.

Acid-Test Ratio• A measure of a company’s liquidity.• Similar to current ratio but excludes less

liquid assets.• Ratio will vary from industry to industry.

44 © 2013 McGraw-Hill Ryerson Limited.

Using the Information-Appendix 8AUsing the Information-Appendix 8A

LO 7

Acid-Test Ratio =

45 © 2013 McGraw-Hill Ryerson Limited.

Quick assets*

Current liabilities

* cash, short-term investments, and receivables

LO 7

Using the Information-Appendix 8AUsing the Information-Appendix 8A

End of Chapter End of Chapter

46 © 2013 McGraw-Hill Ryerson Limited.

Related Documents