INTERNAL AUDIT REPORT of D AI I\T HA T MUAil C I P AL I TY Reg. Office: Dainhat, Purba Bardhaman, West Bengal. FINANCIAL YEAR: 2015 - 16 Audit Period: From 0110412015 to 3110312016 B KAR & ASSOCIATES Chartered Accountants e-mail : bkarassociates@gmail. com bkurur * o. i ut. r @reai ffr"ui l- r o* Mobile: +91 9432 44 15 44 I +918100 82 92 99 Ree. Off.: PO- Ram chandrapur, Howrah, Bagnan- 711303 Docs. Hub: Holding No. 132,WardNo. 11, Madhyamgram CTC Bus Stand, Kolkata -700129.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTERNAL AUDIT REPORT

of

D AI I\T HA T MUAil C I P AL I TY

Reg. Office: Dainhat, Purba Bardhaman, West Bengal.

FINANCIAL YEAR: 2015 - 16

Audit Period: From 0110412015 to 3110312016

B KAR & ASSOCIATESChartered Accountants

e-mail : bkarassociates@gmail. combkurur * o. i ut. r @reai ffr"ui l- r o*

Mobile: +91 9432 44 15 44 I +918100 82 92 99

Ree. Off.: PO- Ram chandrapur, Howrah, Bagnan- 711303

Docs. Hub: Holding No. 132,WardNo. 11, MadhyamgramCTC Bus Stand, Kolkata -700129.

ts KAR &ASSCC]IATESChartered Accountants

ToThe ChairmanDainhat Municipality,Dainhat Purba Bardhaman,West Bengal.

Ref: Yo u r Appointment Letter vide M emo No.-438lD M/co NT. Dared-23/og lzo1g.

Sir,

In terms of your above appointment letter vide Memo No.- 438/DM/CONT. Dated-23l09l20t9. related to Internal Audit of Dainhat Municipality, we have visited the followingdepartment of your ULB from time to time during course of our Audit works to verifl7 the variousrecords and vouch transactions thereto:

1) Accounts Section2) PWD Section3) Establishment Section4) Relief Section5) Death & Birth Section6) Licence Section7) Tax Section8) Received Section9) Cash Section10) General Section11) Conservancy Section12) Health Section

After verifying the records as maintained by above department of your ULB we notedsome discrepancies/ findings and observations and on the basis we have prepared statement onthe department wise findings and submitted the same for the clarifications/replies against ouraudit queries from your end.

We have considered your clarifications/replies against our Audit queries while preparingyour this Audit Report for Dainhat Municipality for the year 2015-16.

We hereby submit the detailed Internal Audit Report for your kind perusal and on wardnecessary Action from your end.

Thanking you,

Yours faithfully,

l4

For -B

KAR a ASSOCTATES --

|Charlerod Accounlantg ;

+91 9432 44 t5 [email protected]

'abi*-i,IEMBERSI.IIP NO

PO. - Ramchandra pur, Dist. _ Howrah, Bagnan _ 711303

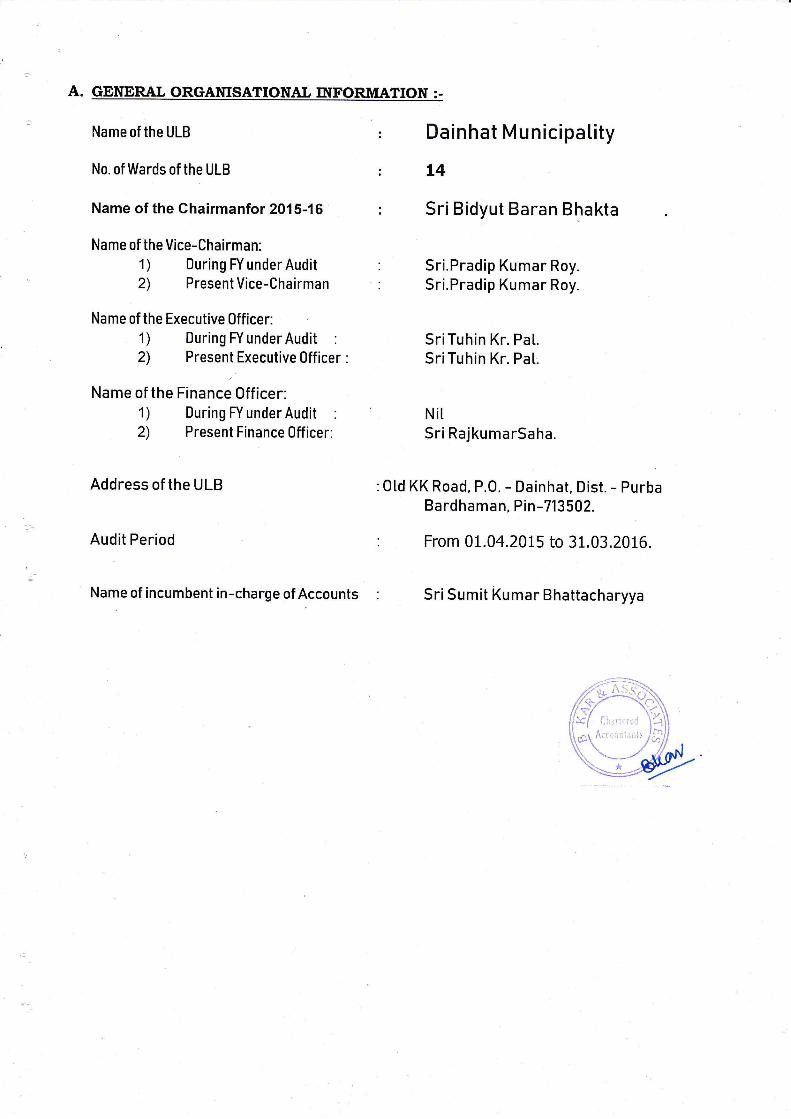

A. GENERAL 9RGANISATIONAL INFORMATION :.

Name of the ULB

No. of Wards of the ULB

Name of the Chairmanfor 2015-16

Name of the Vice-Chairman:1) During FY under Audit2) Present Vice-Chairman

Name of the Executive 0fficer:1) During FY under Audit :

2) Present Executive 0fficer :

Name of the Finance Officer:

2) Present Finance Officer:

Address ofthe ULB

Audit Period

Name of incumbent in-charge of Accounts

Dainhat Municipatity

L4

Sri Bidyut Baran Bhakta

Sri.Pradip Kumar Roy.Sri.Pradip Kumar Roy.

SriTuhin Kr. Pat.SriTuhin Kr. Pat.

NitSri RajkumarSaha.

Otd KK Road, P.O. - Dainhat, Dist. - PurbaBardhaman, Pin-713502.

From 01.04.2015 to 31.03.2016.

Sri Sumit Kumar Bhattacharyya

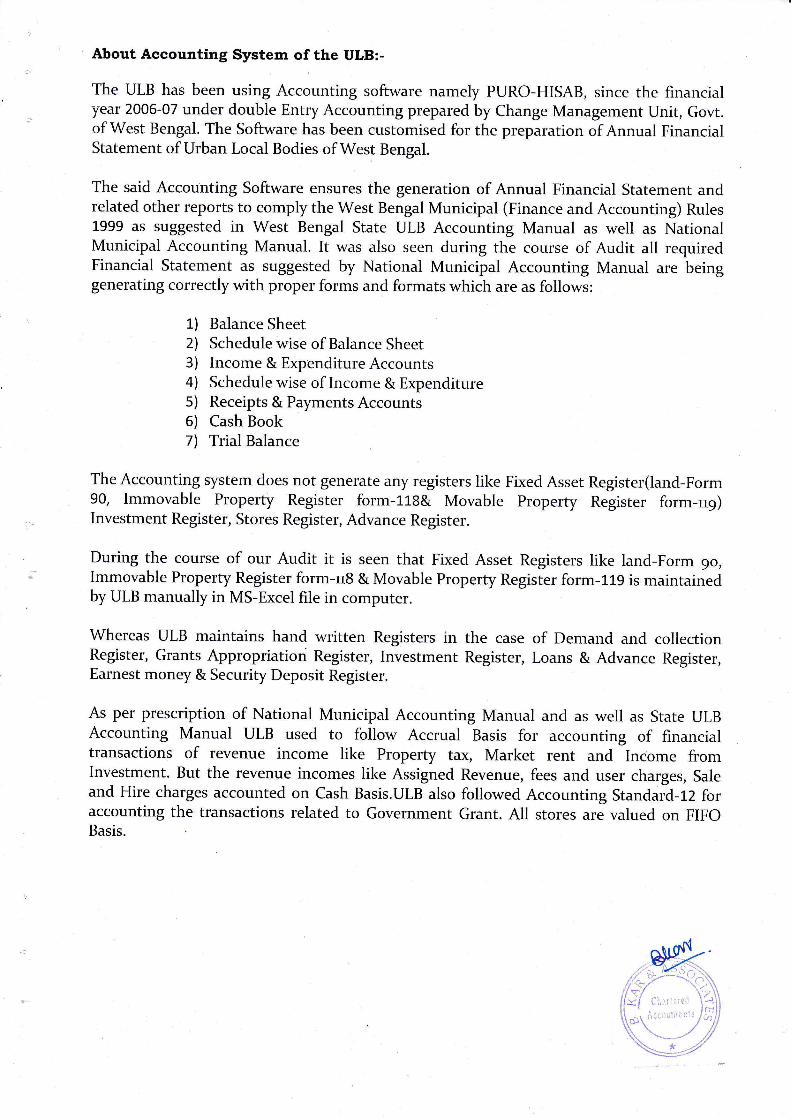

About Accounting System of the ULB:-

The ULB has been using Accounting software namely PURO-HISAB, since the financialyear 2006-07 under double Entry Accounting prepared by Change Management Unit, GoW.of West Bengal. The Software has been customised for the preparation of Annual FinancialStatement of Urban Local Bodies of West Bengal.

The said Accounting Software ensures the generation of Annual Financial Statement andrelated other reports to comply the West Bengal Municipal (Finance and Accounting) Rules1999 as suggested in West Bengal State ULB Accounting Manual as well as NationalMunicipal Accounting Manual. It was also seen during the course of Audit all requiredFinancial Statement as suggested by National Municipal Accounting Manual are beinggenerating correctly with proper forms and formats which are as follows:

1) Balance Sheet2) Schedule wise of Balance Sheet3) Income & Expenditure Accounts4\ Schedule wise of Income & Expenditure5) Receipts & Payments Accounts6) Cash Book7) Trial Balance

The Accounting system does not generate any registers like Fixed Asset Register(land-Form90, Immovable Property Register form-11-8& Movable Property Register form-ug)Investment Register, Stores Register, Advance Register.

During the course of our Audit it is seen that Fixed Asset Registers like tand-Form 90,Immovable Property Register form-rrS & Movable Property Register form-i.19 is maintainedby ULB manually in MS-Excel file in computer.

Whereas ULB maintains hand written Registers in the case of Demand and collectionRegister, Grants Appropriation Register, Investment Register, Loans & Advance Register,Earnest money & Security Deposit Register.

As per prescription of National Municipal Accounting Manual and as well as State ULBAccounting Manual ULB used to follow Accrual Basis for accounting of financialtransactions of revenue income like Property tax, Market rent and Income fromInvestment. But the revenue incomes like Assigned Revenue, fees and user charges, Saleand Hire charges accounted on Cash Basis.ULB also followed Accounting Standard-tz foraccounting the transactions related to Government Grant. All stores are valued on FIFOBasis.

B. PENDING POSITION Or POSITION OF PREVIOUS AUDIT COMPLIANCE:-

Bl: AUDIT 0 F EXAMI N ER O F LOCAL ACCOUNTS- TRANSACTI O N AU Dlt

a) Financial year up to which Transaction Audit has been completed by Examiner ofLocal Accounts: 201 5-1 6.

b) Audit Period up to which Broad Sheet Reply to the lnspection Report ofExaminers of Local Accounts: 2015-16.

B2: lnternal Audit:

lnternal Audit for the period 2011+-15 has been completed by ULB in the month of August2018.

Point-wise Auditor's Obsenration/ queries and ULB Replies and Auditor,sSuggestion:-

Cl: Audit 0bservation on Cash Management:

a) Own source Revenue of the ULB:

As explained by the ULB during course of our audit all cash receipts from the variousdepartments like property tax, trade license etc. are collected by cashier and are entered in theaccounting software. The entire cash deposited to Bank Account of Municipal fund own source atthe end of every day. No amount cash collected from various departments of the ULB is retained inthe Municipality. The head-wise revenue income is entered in the accounting software at timereceipt of all collections. Contra vouchers are made to Bank Account of Municipal fund own source(SBI A/c No. 11891643558) after deposit of the amount to the bank and sum total of entirecollections from own source income is checked from the daily receipt summery generated from theaccounting software by cash section at the end of everyday to ensure correctness between cashcollected from own source and deposited to own source bank (total of daily receipt summery = totalof contra voucher of deposit daily collection in to bank = total Amount deposited at the end of thed"v)'

b) Fund Management of Grant Fund Accounts:Generally own source revenues are not sufficient for running an ULB.The creation of urban

Development infrastructure (land, shelter and civic services) would require dispensing a largeamount of resources by the Urban Local Ggvernments. With the rising levels of urbanization andgrowth of urban population, the pressure on development of cities is increasing in India, aselsewhere in the World. Major sources finance comes from Central Government as well as StateGovernment in the form of Government Grant. Like other ULBs in West BengalDainhatMunicipality also receives grant from Central Government as well as State Government.Government Funds are sent to Treasury Account L/F account & Various Scheduled Bank Accountsof Dainhat Municipality.

As explained to us during the course our audit for the management of fund related togovernment grant on receipt of any Government order showing received of fund or on receipt ofany cheque from any government agenry like SUDA an accounting entry is made creditingrespective grant account and debiting respective treasury and bank account by accountsdepartment of the ULB in the shape of Receipt / Journal voucher in the Accounting software.

As explained to us during the course of audit, when expenditure (Revenuei Capital)ott of grant fund, after necessary approval from BOC the bill is sent to treasury in form ofadvice along with a cheque as signed by Chairman and E.O of the ULB for clearance. The

t

oflicer checks the authenticity of the bill and accordingly passes the bill and resend the bitl to ULBand cheque after passing the same. The cheque is then handed over to party on receipt of moneyreceipt.

Detailed balance of Gash, Bank and treasury balance as on 31.03.2016 as per following table:

sL.No.

NAME OF BANK ACCOUNT NO. PURPOSEBALANCEAS ON

3L.O3.2016

1 SBl,0ainhat Branch 1 1891643558 ()wn Sources 4,17,195.052 SBl, Katwa Branch 34346434738 Treasury retated a/c 39,277.00

3 SBl,0ainhat Branch 11891643s47 Govt. Grant 36,78,605.494 SBl,0ainhat Branch 30659287809 Securrity [leposit A/c 43,229.OO

5 SBl, Dainhat Branch 32379784939 BSUP 664.006 lBDl, Katwa Br. 20310{000334 SBM 11,22,979.OO

8 SBl, []ainhat Branch 32112204706 HUP 19,79,057.00

I UBl. Kawa Branch 208010474047 14th FC 49,85,455.0010 SBl, t]ainhat Branch 1 {89{644{65 BZSS 11,013.74

11 SBl,0ainhat Branch 31440617283 BEUP 2,19,779.00

12 SBl,0ainhat Branch 11891646264 KUSP 421.48

13 SBl, []ainhat Branch 1 1 891646785 IHSDP 23,519.8414 SBl. []ainhat Branch 31715622668 IGNWPS 18,41,422.0015 SBl, []ainhat Branch 31715623468 IGNOPS 36,375.00

16 SBl, []ainhat Branch 11891546253 HHW 4,80,734.0014 SBl, [lainhat Branch 3171561 1996 IENOAPS 5,40,391.0019 SBI, []ainhat Branch 1 1 891644585 PENSIONA/C 7,43,891.4420 SBl, Dainhat Branch 33723216914 SALARYFUND A/C 4,69,642.0021 SBl. []ainhat Branch 3{768332841 Mt]M 44,95,437.4622 SBI,0ainhat Branch 3527524226 MPLad (Ritabrata) 5,00,662.0023 SBl, I]ainhat Branch 32112207093 ILCS 8,026.0024 SBl, []ainhat Branch 3372329694s NFBS 2,707.0025 SBl.0ainhat Branch 317159000000 WATER SUPPLYA/C 20,692.0026 SBl. []ainhat Branch I 18916000000 HERITAGE 31,457.5827 SBl, []ainhat Branch 31440616369 MPLA0 (SunitMondaU 3,86,280.0028 SBI, t]ainhat Branch 32379784316 sEcc-l1 86,632.0029 SBl.0ainhat Branch 315930146526 REVLOVING FUND 1,181.0030 SBI,0ainhat Branch 31768575374 NCLP 2,88,314.00

31 SBl, [Iainhat Branch 30703232135 SJSRY 4,00,996.0032 HDFC, Katwa Br. 5010014784s350 PMAY 3,04,28,939.0033 HI]FC, Katwa Br. 50100131500632 GeneraI Purpose 23,832.4036 UBl, Kawa Branch 2080{0288736 12TH FC 1,52,453.0037 Katwa Treasury 8448 LFA/c 1,19,61,449.00

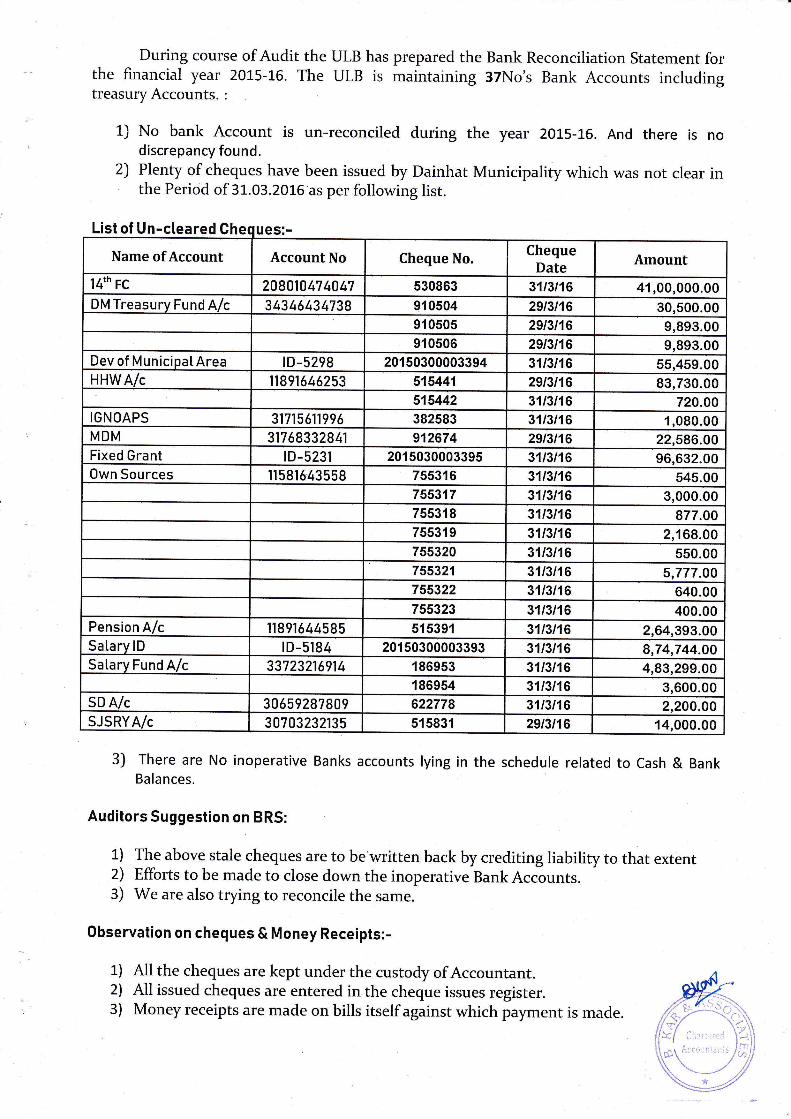

During course of Audit the ULB has prepared the Bank Reconciliation Statement forthe financial year 2015-16. The ULB is maintaining 37No's Bank Accounts includingtreasury Accounts. :

1) No bank Account is un-reconciled during the year 2015-16. And there is nodiscrepancy found.

2) Plenty of cheques have been issued by Dainhat Municipality which was not clear inthe Period of gt.Og.ZO1G as per following list.

List of Un-cleared Ch

3) There are No inoperative Banks accounts lying in the schedule related to Cash & BankBalances.

Auditors Suggestion on BRS:

1) The above stale cheques are to be written back by crediting liability to that extent2) Efforts to be made to close down the inoperative BankAccounts.3) We are also tryrng to reconcile the same.

0bservation on cheques & Money Receipts:-

1) All the cheques are kept under the custody of Accountant.2) Atl issued cheques are entered in the cheque issues register.3) Money receipts are made on bills itself against which payment is made.

Name of Account Account No Cheque No.Cheque

Date Amount

14th Fc 208010474947 530863 31t3t16 41,00,000.00DM Treasurv Fund A/c 34346434738 910504 29t3t16 30,500.00

910505 2913r16 9,893.009{0506 29t3t16 9,893.00

Dev of MunicipaI Area lD-5298 20150300003394 31t3t16 55,459.00HHWA/c 118916462s3 515441 29t3t16 83,730.00

515442 31t3t16 720.0OIGNOAPS 3171561'.t996 382583 3113t16 1,080.00MDM 31768332841 912674 29t3t16 22,586.00Fixed Grant lD-5231 2015030003395 3113t16 96,632.00Own Sources 1r581643558 755316 31131'.t6 545.00

755317 31t3t16 3,000.00755318 31t3t16 877.00755319 31t3t16 2,169.00755320 31t3t16 550.00755321 31t3t16 5,777.00755322 31t3t16 640.00755323 31t3t16 400.00

Pension A/c 1r891644585 515391 31t3t16 2,64,393.00Satary lD lD-5184 20150300003393 31t3t16 8,74,744.OOSalarv Fund A/c 33723216914 186953 31tst16 4,83,299.00

186954 31t3t16 3,600.00SD A/c 30659287809 622778 31/3/16 2,200.00SJSRYA/c 30703232135 515831 2913t16 14,000.00

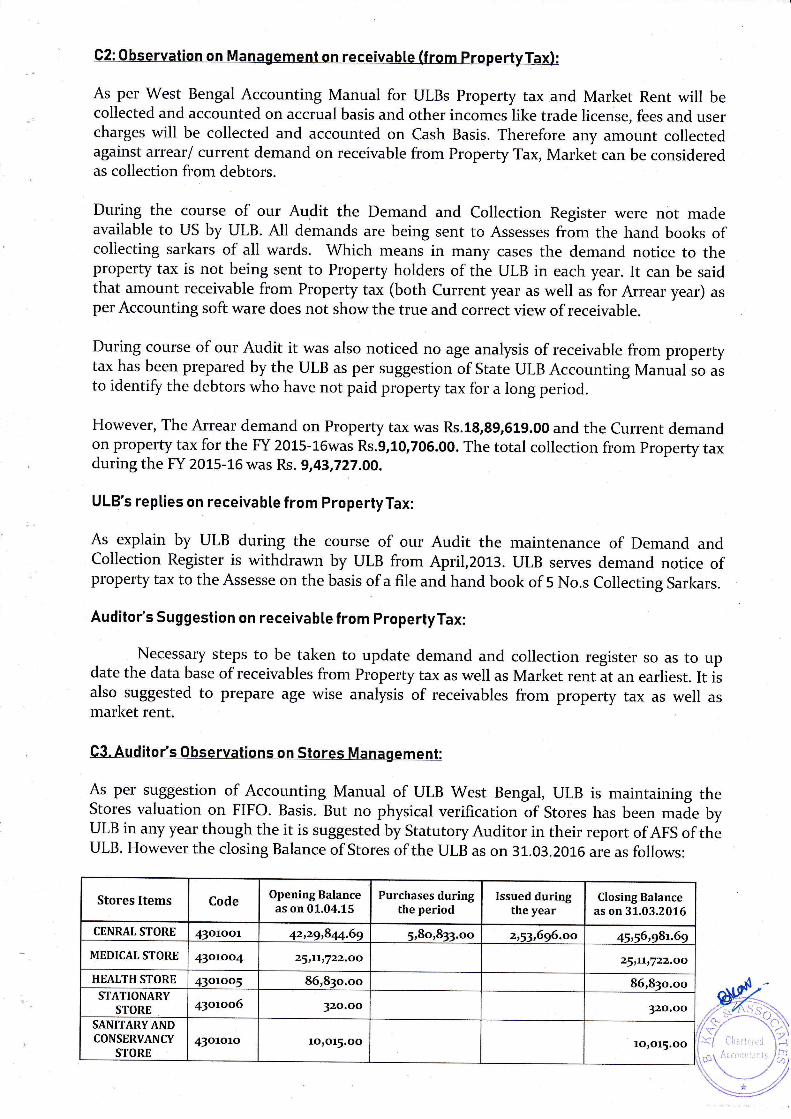

C2:0bseryation on Management on receivable (from PropertyTax):

As per West Bengal Accounting Manual forcollected and accounted on accrual basis andcharges will be collected and accounted onagainst arrear/ current demand on receivableas collection from debtors.

ULBs Property tax and Market Rent will beother incomes like trade license, fees and userCash Basis. Therefore any amount collectedfrom Property Tax, Market can be considered

During the course of our Audit the Demand and Collection Register were not madeavailable to US by ULB. All demands are being sent to Assesses from the hand books ofcollecting sarkars of all wards. Which means in many cases the demand notice to theproperty tax is not being sent to Property holders of the ULB in each year. It can be saidthat amount receivable from Property tax (both Current year as well as for Arrear year) asper Accounting soft ware does not show the true and correct view of receivable.

During course of our Audit it was also noticed no age analysis of receivable from propertytax has been prepared by the ULB as per suggestion of State ULB Accounting Manual ro "tto identiflr the debtors who have not paid property tax for a long period.

However, The Arrear demand on Property tax was Rs.18,89,519.00 and the Current demandon property tax for the FY 2015-15was Rs.9,10,705.00. The total collection from Property taxduring the FY 2015-16 was Rs. g,4g,7T7.AO.

ULB's replies on receivable from PropertyTax:

As explain by ULB during the course of our Audit the maintenance of Demand andCollection Register is withdrawn by ULB from April,2013. ULB serves demand notice ofproperty tax to the Assesse on the basis of a file and hand book of 5 No.s Collecting Sarkars.

Auditorrs Suggestion on receivable from PropertyTax:

Necessary steps to be taken to update demand and collection register so as to update the data base of receivables from Property tax as well as Market rent at an earliest. It iialso suggested to Prepare age wise analysis of receivables from property tax as well asmarket rent.

C3. Audito/s 0hservations on Stores Management:

As per suggestion of Accounting Manual of ULB West Bengal, ULB is maintaining theStores valuation on FIFO. Basis. But no physical verification of Stores has been made byULB in any year though the it is suggested by Statutory Auditor in their report of AFS of thlULB. However the closing Balance of Stores of the ULB as on 31.03.2016 are as follows:

Opening Balanceas on 01.04.15

Closing Balanceas on 31.03.2016

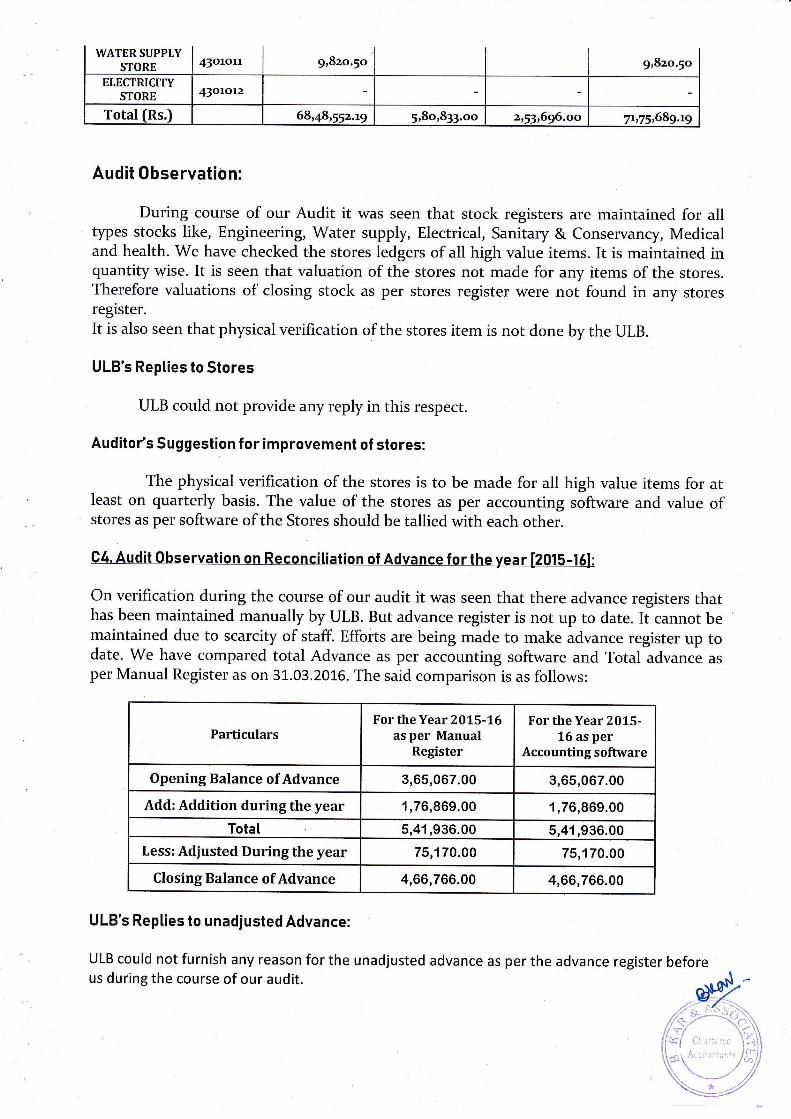

WATERSUPPLYSTORE 4Solorr 9,82o.50 9,82o.5o

ELECTRICITYSTORE 43otorz

Total [Rs.) 68r48,552.r9 5,8o,833.oo 2,53,696.oo V175,689.rg

Audit 0bservation:

During course of our Audit it was seen that stock registers are maintained for alltypes stocks like, Engineering, Water supply, Electrical, Sanitary & Conservdncf, Medicaland health. We have checked the stores ledgers of all high value items. It is maintained inquantity wise. It is seen that valuation of the stores not made for any items of the stores.Therefore valuations of closing stock as per stores register were not found in any storesregister.It is also seen that physical verification of the stores item is not done by the ULB.

ULB's Replies to Stores

ULB could not provide any reply in this respect.

Auditor's Suggestion for improvement of stores:

The physical verification of the stores is to be made for all high value items for atleast on quarterly basis. The value of the stores as per accounting software and value ofstores as per software of the Stores should be tallied with each other.

On verification during the course of our audit it was seen that there advance registers thathas been maintained manually by ULB. But advance register is not up to date. It cannot bemaintained due to scarcity of staff. Efforts are being made to make advance register up todate. We have compared total Advance as per accounting software and Total advance asper Manual Register as on 31.03.2016. The said comparison is as follows:

ParticularsFor the Year 2015-16

asper ManualRegister

For the Year 2015-16 as per

Accounting software

Opening Balance of Advance 3,65,067.00 3,65,067.00

Add: Addition duringthe year 1,76,869.00 1,76,869.00

Total 5,41,936.00 5,41,936.00

Less: Adjusted During the year 75,170.00 75,170.00

Closing Balance of Advance 4,66,766.00 4,66,766.00

ULB's Repties to unadjusted Advance:

ULB could notfurnish any reason forthe unadjusted advance as perthe advance register beforeus during the course of our audit.

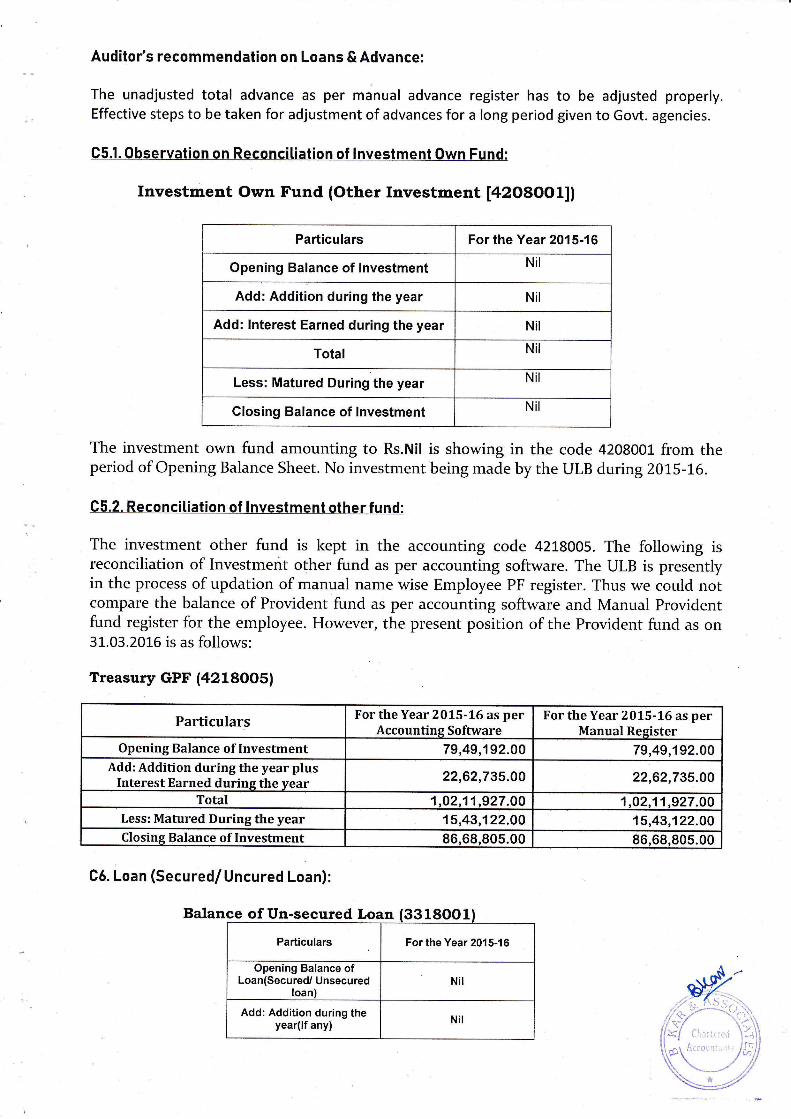

Audito/s recommendation on Loans &Advance:

The unadjusted total advance as per manual advance register has to be adjusted properly.Effective steps to be taken for adjustment of advances for a long period given to Govt. agencies.

CS.l.0bservation on Reconciliation of lnvestment Own Fund:

Investment Own F.und (Other Investment [42O8OOUI

Particulars For the Year 2015-f6

Opening Balance of lnvestment Nit

Add: Addition during the year Nit

Add: lnterest Earned during the year Nit

Total Nit

Less: Matured During the year Nit

Closing Balance of lnvestment Nit

The investment own fund amounting to Rs.Nil is showing in the code 4208001 from theperiod of Opening Balance Sheet. No investment being made by the ULB during20ti-16.

Q5.2. Reconciliation of !nvestment otherfund:

The investment other fund is kept in the accounting code 4218005. The following isreconciliation of Investment other fund as per accounting software. The ULB is presentlyin the process of updation of manual name wise Employee PF register. Thus we could notcompare the balance of Provident fund as per accounting software and Manual Providentfund register for the employee. However, the present position of the Provident fund as on3L.03.2016 is as follows:

Treasury GPF (4218OOS}

C6. Loan (Secured/Uncured Loan):

Balance of Un d Loan 331

Particulars For the Year 2015-16 as perAccountinq Software

For the Year 2015-16 as perManual Resister

Opening Balance of Investment 79,49,192.00 79,49,192.00Add: Addition during the year plus

Interest Earned during the vear 22,62,735.OO 22,62,735.O0

Total 1,O2.11.927.00 1.O2.11.927.00Less: Matured During the year 15,43,122.00 15,43,122.00Closine Balance of Investment 86.68.805.00 86.68.805.00

-secured Loan I3318OO1

Particulars For the Year 2015-16

Opening Balance ofLoan(Secured/ Unsecured

loan)Nil

Add: Addition during theyear(lf any) Nit

Add: lnterest onl-oan(Secured/ Unsecured

loan)Nit

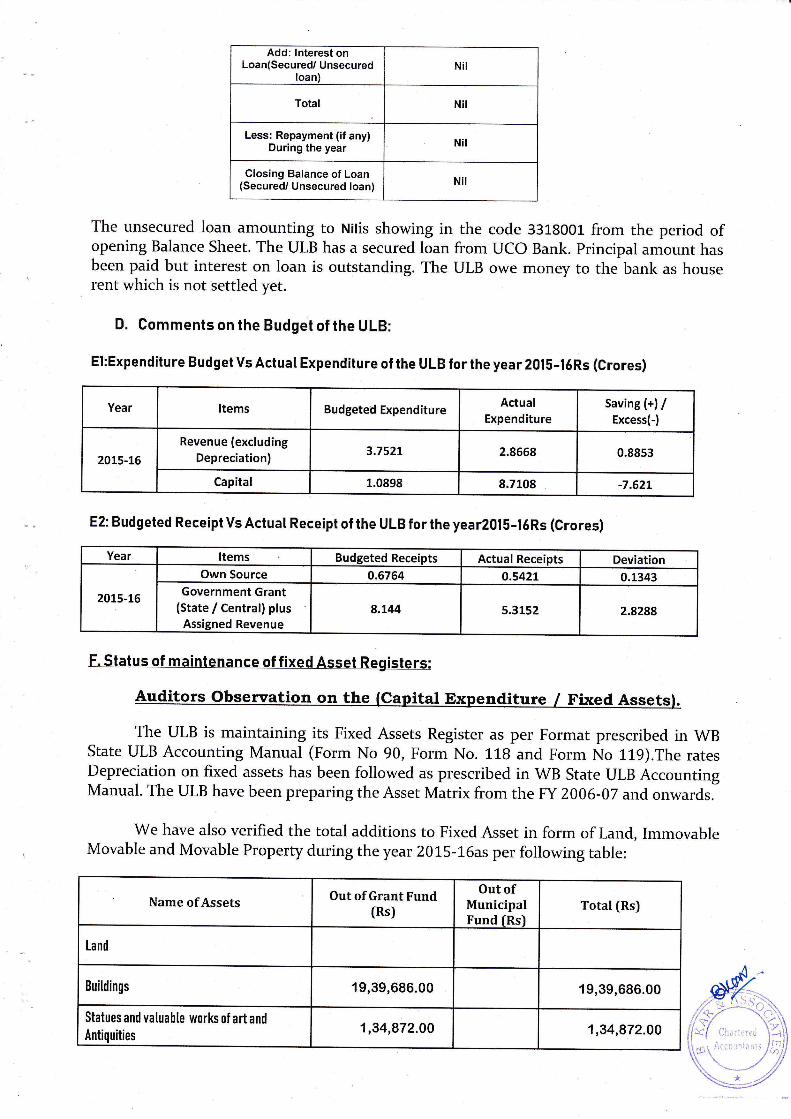

Total Nit

Less: Repayment (if any)During the year Nil

Closing Balance of Loan(Secured/ Unsecured loan) Nit

The unsecured loan amounting to Nilis showing in the code 33i.8001 from the period ofopening Balance Sheet. The ULB has a secured loan from UCO Bank. Principal amount hasbeen paid but interest on loan is outstanding. The ULB owe money to the bank as houserent which is not settled yet.

D. Comments on the Budget of the ULB:

El:Expenditure BudgetVsActual Expenditure of the ULB forthe year2015-l5Rs (Crores)

Year Items Budgeted ExpenditureActual

ExpenditureSaving (+)/

Excess(-)

20L5-L6

Revenue (excludingDepreciation) 3.1521 2.8668 0.8853

Capital 1.0898 8.7108 -7.621

E2: Budgeted Receipt Vs Actual Receipt of the ULB for the year20l5-15Rs (Crores)

F. Status of maintenance of fixed Asset Registers:

The ULB is maintaining its Fixed Assets Register as per Format prescribed in WBState ULB Accounting Manual (Form No 90, Form No. 118 and Form No 119).The ratesDepreciation on fixed assets has been followed as prescribed in WB State ULB AccountingManual. The ULB have been preparing the Asset Matrix from the FY 2006-07 and,onwards.

We have also verified the total additions to Fixed Asset in form of Land, ImmovableMovable and Movable Property during the year 2015-16as per following table:

Name of Assets Out ofGrant Fund(Rs)

Out ofMunicipalFund fRs)

Total (Rs)

Land

Buitdings 19,39,686.00 19,39,696.00

Statues and valuahle works of art and

Antiquities1,34,872.00 1,34,872.00

Year Items Budgeted Receipts Actual Receipts Deviation

2015-16

Own Source 0.6764 o.s42L 0.1343Government Grant

(State / Central) plusAssisned Revenue

8.l44 5.3152 2.8288

fl.,m,CrlAri' '"''''" JE,\:\"7

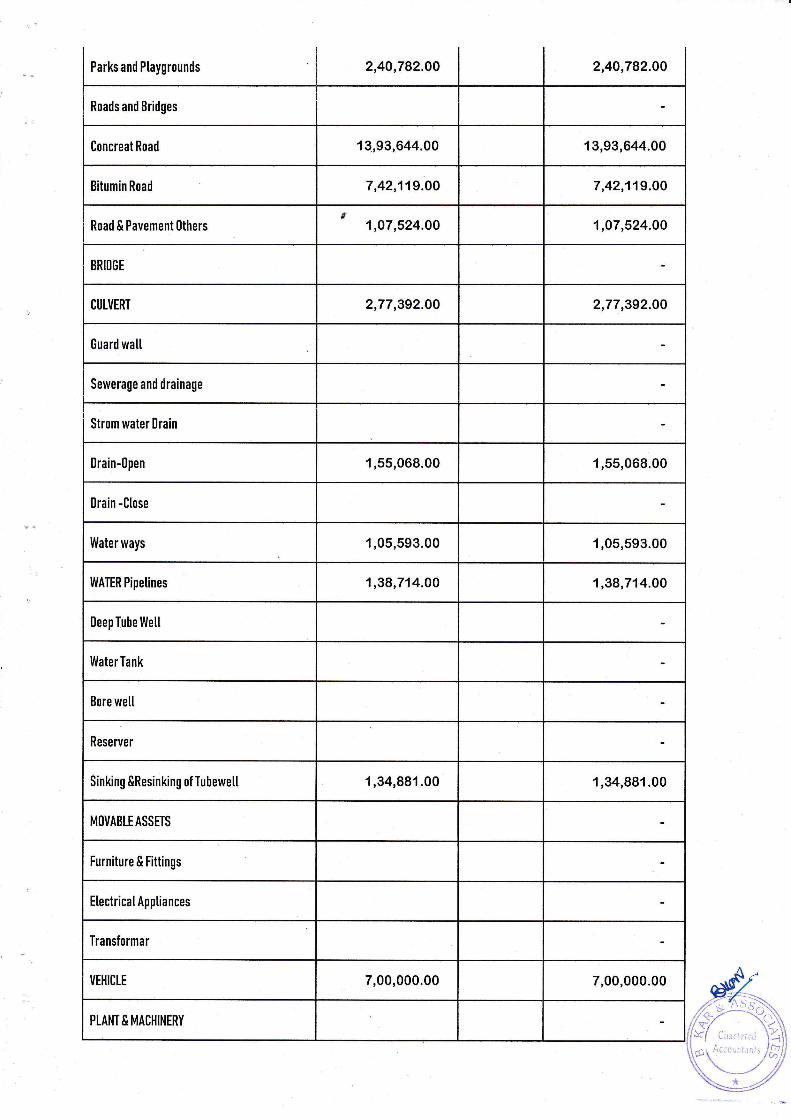

Parks and Ptaygrounds 2,4O,782.OO 2,4O,782.OO

13,93,644.00

7,42,119,OO 7,42,119.00

Road & Pavement (lthers 1,O7,524.OO 1,O7,524.00

2,77,392.AO 2,77,392.A0

1,05,593.00

1,38,714.00

1,34,881.00

7,00,000.00

r}3l{sAct:ollt,:nis,fil

0ffice & 0ther E0 41,160.00 41,160.00

0ther Assets 2,852.50 2,852.50

Total 61,14,287.50 61,14,287.50

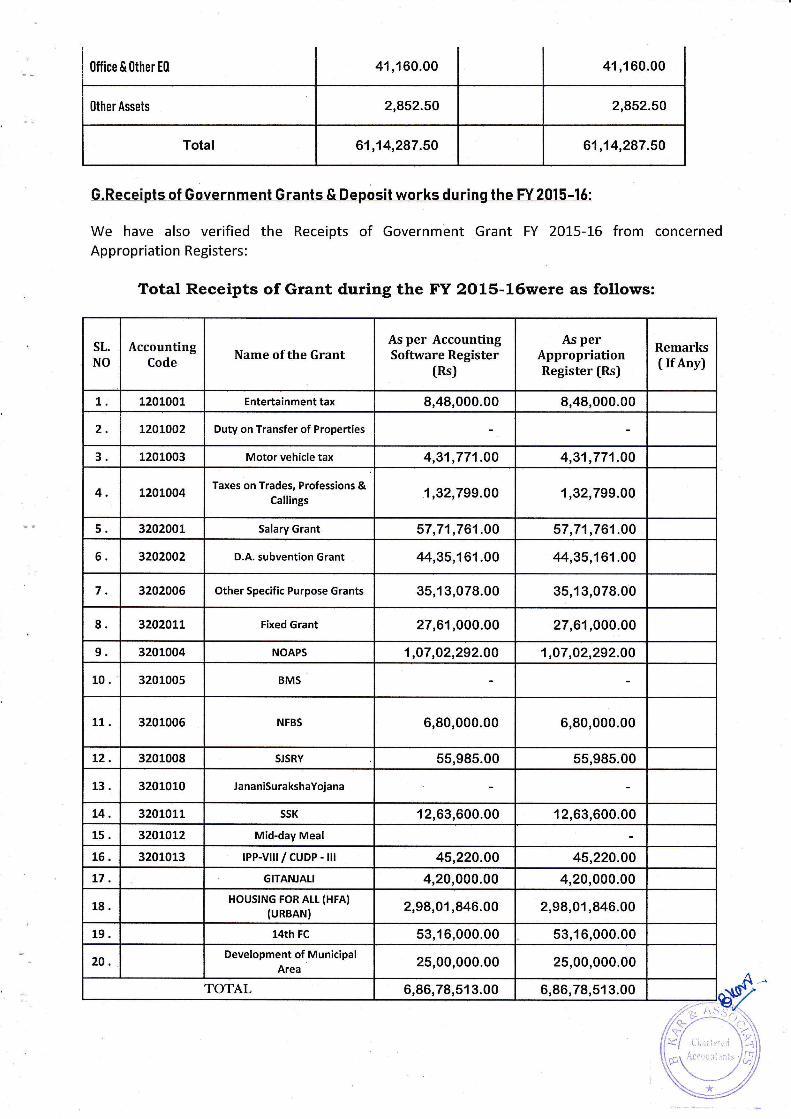

G.Receipts of Government Grants & Deposit works during the FY2015-15:

We have also verified the Receipts of Government Grant FY 2015-16 from concernedAppropriation Registers:

Total Receipts of Grant during the FY 2015-16were as follows:

Name of the GrantAs per AccountingSoftware Register

(Rs)

As perAppropriationRegister (Rs)

Duty on Transfer of Properties

4,3',1,771.OO 4,31,771.O0

1,32,799.00 1,32,799.00

57,71,761.OO 57,71,761.00

44,35,161.00 44,35,161.00

35,13,078.00

27,61,000.00 27,61,000.00

1,07,02,292.00 1,O7,02,292.00

12,63,600.00

2,98,01,846.00 2,98,01,846.00

53,16,000.00 53,16,000.00

6,86,78,513.00 6,86,78,513.00

,4'y&f:\17 \(**/ ., '',.,.,,f!61 Ac",,i::ri.,nl,,fff

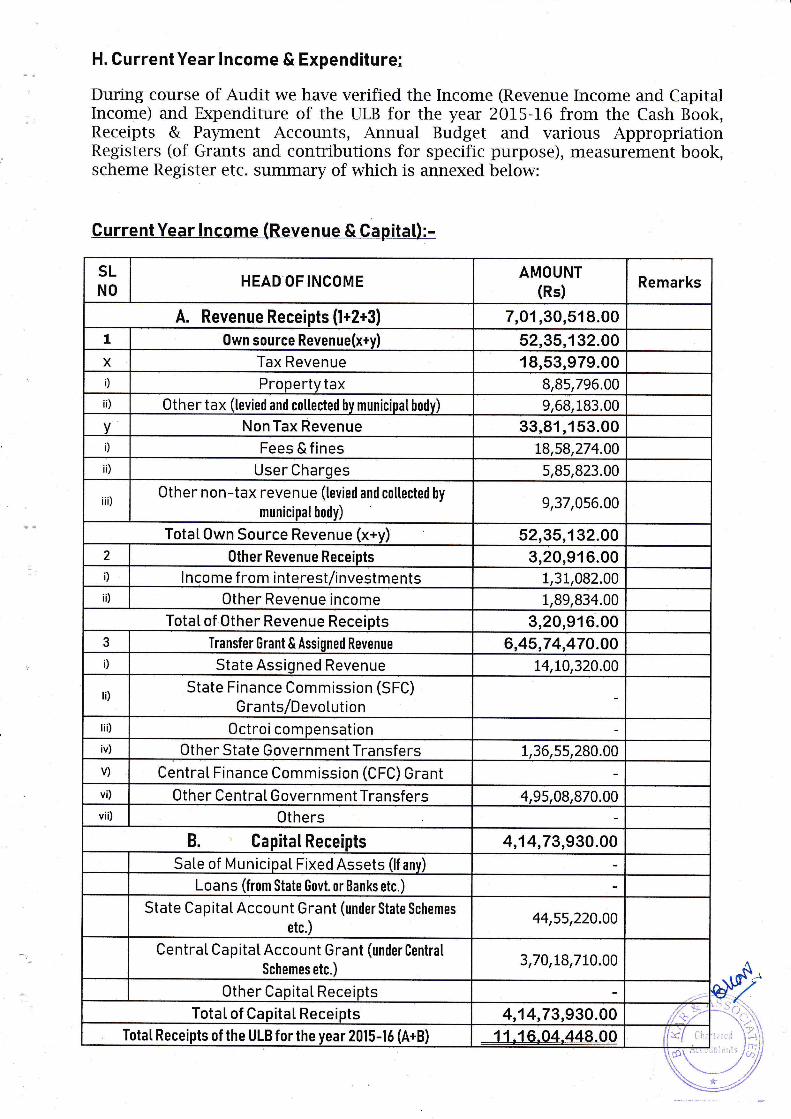

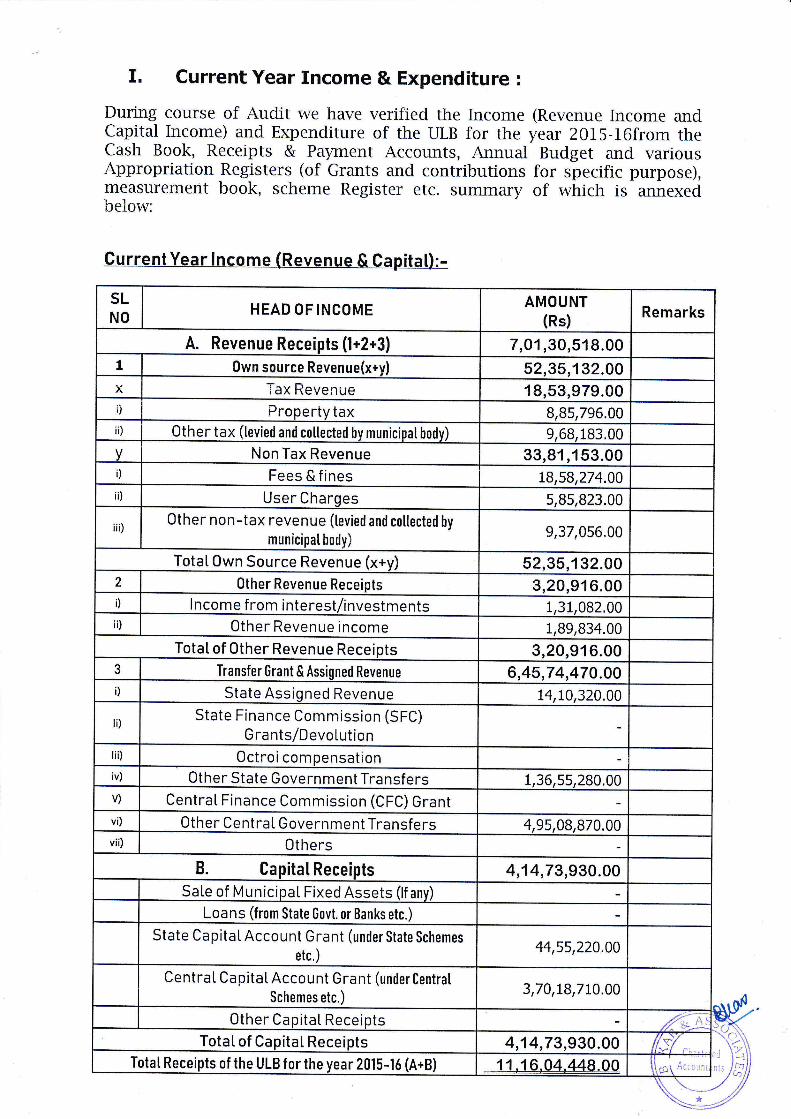

H. CurrentYear lncome & Expenditure;

During course of Audit we have verified the Income (Revenue Income and CapitalIncome) and Expenditure of the ULB for the year 2015-16 from the Cash Book,Receipts & Payment Accounts, Annual Budget and various AppropriationRegisters (of Grants and contributions for specific purpose), measurement book,scheme Register etc. summary of which is annexed below:

CurrentYear lncome (Revenue & Capital):-

SLNO

HEAD OFINCOMEAMOUNT

(Rs) Remarks

*r-{r.\,

'i"r"A

A. Revenue Receipts (l+2+3) 7,01,30,518.00I Own source Revenue(x+y) 52,35,132.00x Tax Revenue 18,53,979.00i) Propertv tax 8,85,796.00ii) 0ther tax (tevied and collected by munieipat hody) 9.68.183.00

V NonTax Revenue 33,81,153.00i) Fees & f ines L8,58,274.00ii) User Charqes 5,85,823.00

iiD0ther non-tax revenue (tevied and cotlected hy

municipalbody)9,37,056.00

Totat Own Source Revenue (x+y) 52,35,132.002 0ther Revenue Receiots 3,20,916.00i) I ncome from interest/investments 1,31.082.00ii) 0ther Revenue income 1,89,834.00

Totat of 0ther Revenue Receipts 3,20,916.003 Transfer Grant & Assiuned Revenue 6,45,74,470.00D State Assiqned Revenue 14,10,320.00

ri)State Finance Commission (SFC)

Grants/Devo[utionri i) 0ctroi compensationiv) 0ther State Government Transfers 1,36,55,280.00v) CentraI Finance Commission (CFC) Grantvi) 0ther CentraI Government Transfers 4,95,08,870.00vii) 0thers

B. Gapital Receipts 4,14,73,930.00Sate of MunicipaI Fixed Assets (lf any)

Loans (from State Govt. or Banks etc.)

State Ca pita L Accou nt G ra nt (under State Schemes

etc.)44,55,220.0O

CentraI Capitat Account Grant (under Gentral

Schemes etc.)3,70,18,710.00

0ther Capital. Receipts ,-j-r:

Totat of Capitat Receipts 4,14,73,930.00 r{s7"TotaI Receipts of the ULB f or the year 2015-16 (A+B) 11,16,04,449.00 :(/ Ch

t*Jtx ,,,/

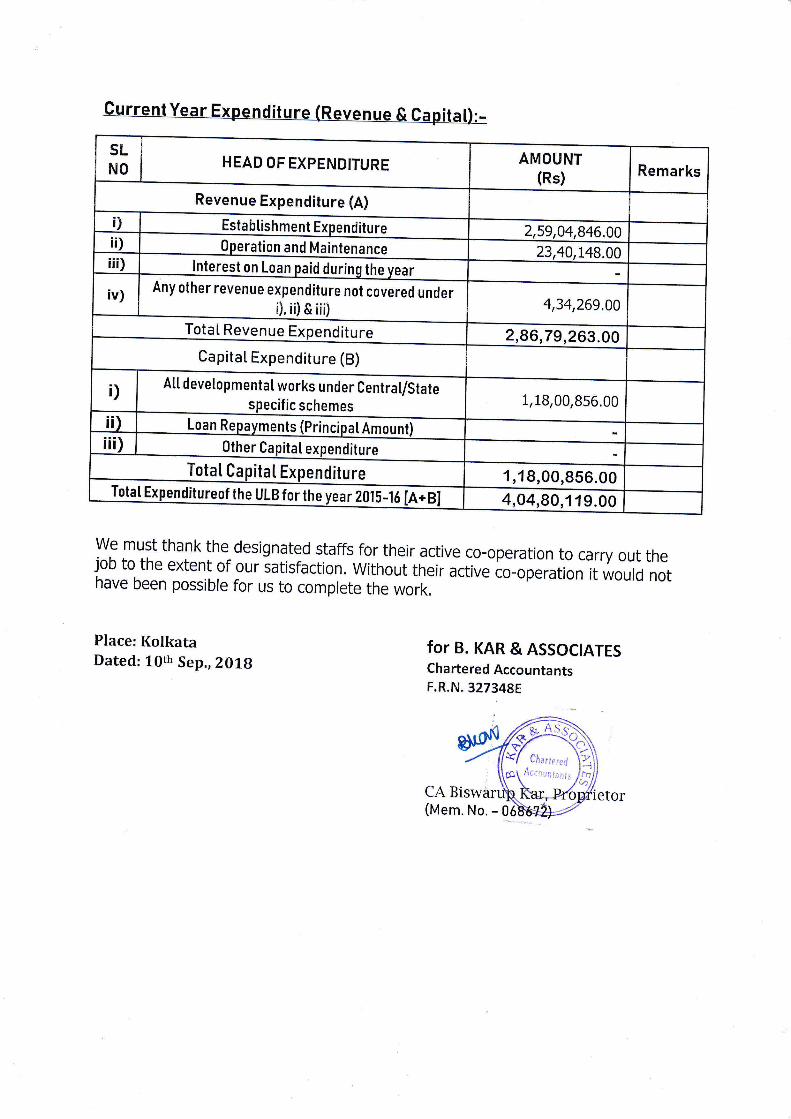

SLNO

HEAD OF EXPENDITUREAMOUNT

(Rs) Remarks

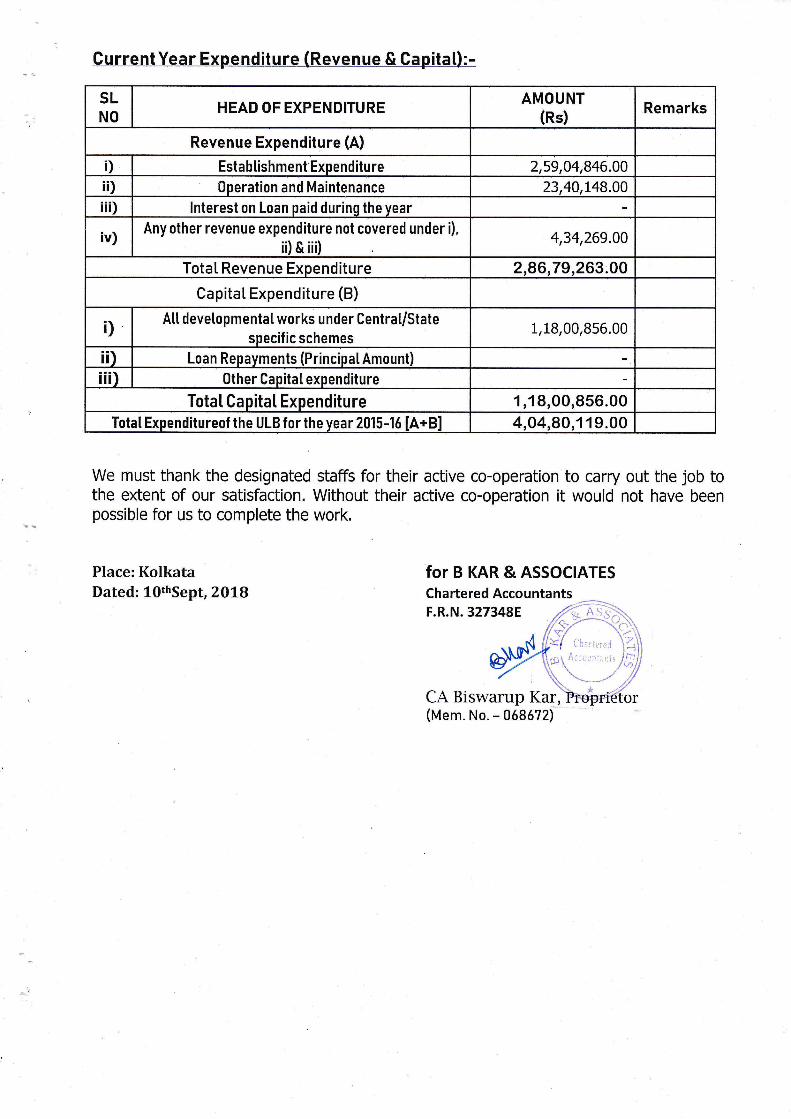

Revenue Expenditure (A)

i) Establishment Exoenditure 2.59.04.846.00ii) 0neration and Maintenance 23.40.L48.00iii) lnterest on Loan oaid durino the vear

iv) Any other revenue expenditure not covered under i),

ii) & iii)4,34,269.00

TotaI Reven ue Expenditure 2.86.79.263.00

Capitat Expenditure (B)

i) At[ devetopmentaI works under Centrat/Statespecific schemes

1,18,00,856.00

ii) Loan Repavments (Principal Amount)

i ii) Other Capitat expenditure

Total CapitaI Expenditure 1,18,00,856.00Total Expenditureof the ULB for the year 2015-16 [A+BI 4.04.80.119.00

Current Yea"r Expenditure (Reve n ue & Cap ita!):-

We must thank the designated staffs for their active co-operation to carry out the job tothe extent of our satisfaction. Without their active co-operation it would not have beenpossible for us to comptete the work.

Place: KolkataDated: 10tt Sept, ?OLB

CA Biswarup Kar,(Mem. No. - 068672)

forBKAR&ASSOCIATESChartered Accountantsp*s

F/ rlh-.i,,,..,1 \l(tYz

ts KAR &ASSOC]IATESChartered Accountants

ToThe ChairrnanDainhat Municipality

5ub: lnternat Audit Report for the FY2015-16of Dainhat Municipatity

Ref:YourAppointnnent Lettervide Merno [vo.43glDMlc0NT. Dated-23.0g.20.lg.

Sir,

In terms of your above appointment letter vide Memo No. 43BlDMlcoNT.Dated- 23.08.2018, related Internal Audit of Dainhat Municipality, we have visitedthe following department of your ULB from time to time during course to verifu thevarious records and vouch transactions thereto:

1) Accounts Sectlon2) PWD Section3) Establishment Section4) Relief Section

5) Death & Birth Section6) Licence Section

7) Tax Section

B) Received Section

9) Cash Section

10) General Section1 1) Conservancy Section12) Health Section

After verifuing the records as maintained by above department of your ULBwe noted some discrepancies/ findings and observations and on the basis we haveprepared statement on the department wise findings and submitted the same for theclarificationslreplies against our audit queries from your end.

We have considered your clarifications/replies against our Audit queries whilepreparing your this Audit Report for Dainhat Municipality for the year 2015-16.

We hereby submit the detailed Internal Audit Report for your kind perusal andon ward necessary Action from your end.

+91 9432 44 t5 [email protected]

Thanking you,

Yours faithftrlly, ::-1-:1r*p. r3i &.AssoctATE s,,n ;1, .

Chartorcd Accountantr - , -i lF.RN 3?rrorEolqgi

, i

flE#0F#s,fltJt*f i,..

--'i-'::::-'--

;;; il

PO. - Ramchandra Pur, Dist. - Howrah, Bagnan - 711303

I" Current Year Income & Expenditure :

During course of Audit we have verified the IncomeCapital Income) and Expenditure of the ULB for theCash Book, Receipts & Payment Accounts, AnnualAppropriation Registers (of Grants and contributionsmeasurement book, scheme Register etc. summarybelow:

Current Year lncome (Revenue & Capital):-

(Revenue Income andyear 2015-16from the

Budget and variousfor specific purpose),of which is annexed

SLNO

HEAD OF INCOMEAMOUNT

(Rs) Remarks

\o;\\a_'

'i \1ntc /f4

" /'''-/ /t,//

2?

A. Revenue Receipts (l+2+3) 7,01,30,519.001 0wn source Revenue(x+y) 52,35,132.00x Tax Revenue 18,53,979.00i) Fropertv tax 8,85,796.00ii) 0ther tax (levied and collected bv municinatbodv) 9,68,183,00V Non Tax Revenue 33,81,153.00i) Fees & fines 18,58,274.00ii) User Charqes 5,85,923.00

iii)0ther non-tax revenue (tevied and collected hy

municipalhody)9,37,056.00

Totat Own Source Revenue (x+y) 52,35,132.002 0ther Revenue Receipts 3,20,916.000 I ncome from interest/investments 1,31,082.00ii) 0ther Revenue income 1,89,834.00

TotaI of 0ther Revenue Receipts 3,20,916.003 Transfer Grant & Assiuned Revenue 6,45,74,470.00D State Assiqned Revenue 14,10,320.00

ti)State Finance Commission (SFC)

G rants/Devotutionrii) 0ctroi compensationiv) 0ther State Government Transfers 1,36,55,290.00v) CentraI Finance Commission (CFC) Grantvi) 0ther CentraI Government Transfers 4,95,08,870.00vii) 0thers

B. Capitat Receipts 4,14,73,930.00SaLe of Municipat Fixed Assets (lf anv)

Loans (from State Govt. or Banks etc.)

State Capitat Account Grant (under State Schemes

etc.)44,55,220.00

CentraI CapitatAccount Grant (under Central

Schemes etc.)3,70,18,710.00

Other Capitat Receipts KATotat of Ca pitat Receipts 4,14,73,930.00

T rtal Receipts of the t!LB for the year 2015-16 (A+B) 11 .16,04.448.00 ;ffi;lS;-

SLNO

I.{EAD OF EXPENDITURE AMOUNT(Rs) Remarks

Revenue Expenditure (A)

.)

=ll2,59,A4,846.00

UPeration and Maintenannp 23,40,148.00iii) lnterest on Loan naid durinn thp va:r

iv) Any other revenue expenditure not covered underr), ii) & iii) 4,34,269.00

TotaI Revenue Expenditure 2,96,79,263.00Capitat Expenditure (B)

i) Au 0ever0pmentaI works under Centrat/Statespecific schemes 1,18,00,856.00

0ther CaoitaI exnpnditrrrp

TotaI CapitaI Expenditure 1,19,00,956.00I urar Expenotrureor the ULB for the year 2015_16 [A+B] 4,O4,90,119.00

we must thank the designated staffs for their active co-operation to carry out thejob to the extent of our satisfaction. without their active co-operation it would nothave been possible for us to complete the work.

Place: KolkataDated:10th Sep., ZOLB

for B. KAR & ASSOCTATESChartered AccountantsF"R.N.327348E

CA Bis(Mem. No.

Related Documents