INTERIM REPORT 1 JANUARY – 30 JUNE 2006 our position INTERIM REPORT FOR CONCORDIA MARITIME AB (PUBL) 1 JANUARY – 30 JUNE 2006 n Profit after tax SEK 18.7 (27.9) million, including a profit of SEK 0.0 (51.5) million on the sale of ships and exchange rate differences of SEK 4.4 (-46.2) million n Profit per share after tax: SEK 0.39 (0.58) n Net sales: SEK 153.3 (185.3) million n Forecast for 2006: SEK 75 million before tax corresponding to SEK 1.58 per share, i.e. unchanged n The P-MAX vessels Stena Primorsk and Stena Performance delivered during second quarter n New 2-year time charter contracts for the chartered V-MAX tankers signed with Lukoil

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

ou r p o si t ionI N T E R I M R E P O R T F O R C O N C O R D I A M A R I T I M E A B ( P U B L )

1 JANUARY – 30 JUNE 20 0 6

n Profit after tax SEK 18.7 (27.9) million, including a profit of SEK 0.0 (51.5) million on the sale of ships and exchange rate differences of SEK 4.4 (-46.2) million

n Profit per share after tax: SEK 0.39 (0.58)

n Net sales: SEK 153.3 (185.3) million

n Forecast for 2006: SEK 75 million before tax corresponding to SEK 1.58 per share, i.e. unchanged

n The P-MAX vessels Stena Primorsk and Stena Performance delivered during second quarter

n New 2-year time charter contracts for the chartered V-MAX tankers signed with Lukoil

CONCORDIA MARIT IME INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

Concordia Maritime is an international tanker shipping company listed on the O List on the Stockholm Stock Exchange. In 2003, six vessels, which will be built in accordance with the max concept, were ordered. In 2006 two additional p-max tankers were ordered. These vessels, p-max, are product tankers of about 65,200 dwt. The max concept means that the vessels are designed for maximum loading capacity in shallow waters. In addition to having mandatory double hulls, they have been designed according to a new concept for safer oil transportation with double main engines in two completely separate engine rooms, double rudders and steering gear, two propellers and double control systems. In 2004, two Panamax tankers of about 75,000 dwt, in which the company has a 50 per cent share, were ordered. The final vessels vill be delivered 2009. Concordia Maritime also has two v l ccs, each 313,000 dwt, on time charter for five years. These vessels, v-max, which were taken into service in 2001, were originally built for Concordia and are the first vessels built in accordance with the max concept.

Innovation and Performance Our mission is to generate a profit by providing our customers with safe, cost-efficient tanker transportation based on innovation and performance.

CONCORDIA MARIT IMEINTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

Product tankersDuring the year, Stena Paris and Stena Provence, have been employed by the French oil and energy company TOTAL. Both vessels are signed to TOTAL on 5-year time charters.

In mid-May, Concordia Maritime took delivery of the third p-max tanker, Stena Primorsk. The vessel is on a 10-year time charter to the Russian logistics company Progetra. Read more about Stena Primorsk and her naming ceremony in Stockholm on page 16.

The fourth p-max tanker, Stena Performance, was deliv-ered at the end of June and has been chartered for five years to the US oil company Amerada Hess Corporation.

The product tanker segment also includes the two ice-strengthened Panamax tankers, which have been ordered in a joint venture with Neste Shipping. These vessels have been chartered to Neste Oil for ten years

The newbuilding projects are proceeding according to plan. Delivery of the first Panamax tanker, Stena Poseidon, is planned for the last quarter of 2006.

Large tankers/VLCC

Since november 2004 Concordia Maritime has time-char-tered from Arlington Tankers LTD the two v-max vlccs Stena Vision and Stena Victory. The charters expire at the end of 2009 after which the company has options on three 1-year extensions. These two vessels have been on charter to the US oil company Sunoco since 2001.

During the second quarter, two-year time charter contracts and one-year option were signed for the two v-max tankers with Litasco, a subsidiary of the Russian oil company Lukoil. The vessels will enter the new charters when their current charters with Sunoco expires at the end of 2007. This means that Concordia Maritime has secured employment for the two v-max tankers until the end of 2009 when the time charters with Arlington Tankers LTD expires.

In conjunction with the scheduled dry-docking of Stena Vision, the tanker’s reduction gear was found to be damaged. Repairs, including the manufacture of new parts, will take several months, and during this period, Stena Vision will not be sailing for Sunoco. During the second quarter, the vessel was unemployed for 28 days, 13 of which were covered by insurance. At present, the vessel is employed as a floating oil storage facility in the Arabian Gulf while awaiting the deliv-ery of necessary engine parts. The result of the segment has been affected negative by approximately msek -10 in regards to loss of hire, deductibles and reparation costs.

The sister vessel Stena Victory was also dry-docked ac-cording to plan during the period.

As a result of the sale in 2004 of the v-max tankers to Arlington Tankers, Concordia Maritime has an undertak-ing relating to the daily operation of these vessels. The provisions made for this undertaking did not cover the actual costs and affected the result with approximately sek -2 million.

Summary of business activities

CONCORDIA MARIT IME INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

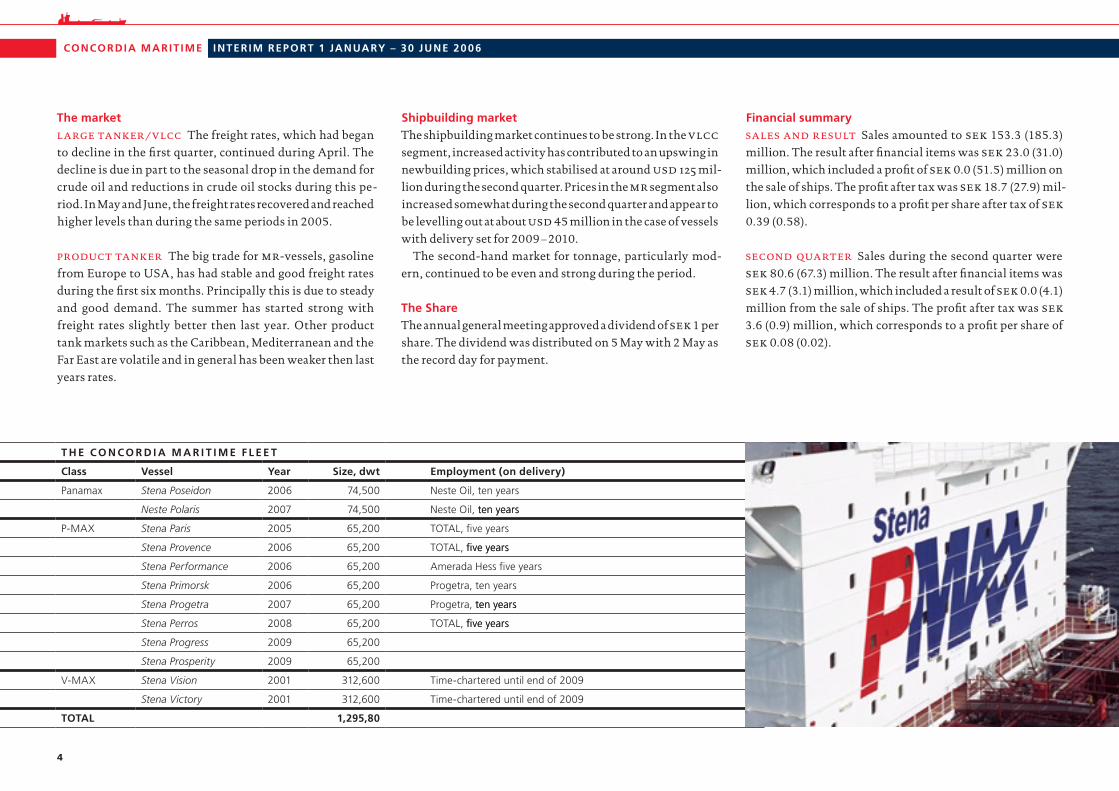

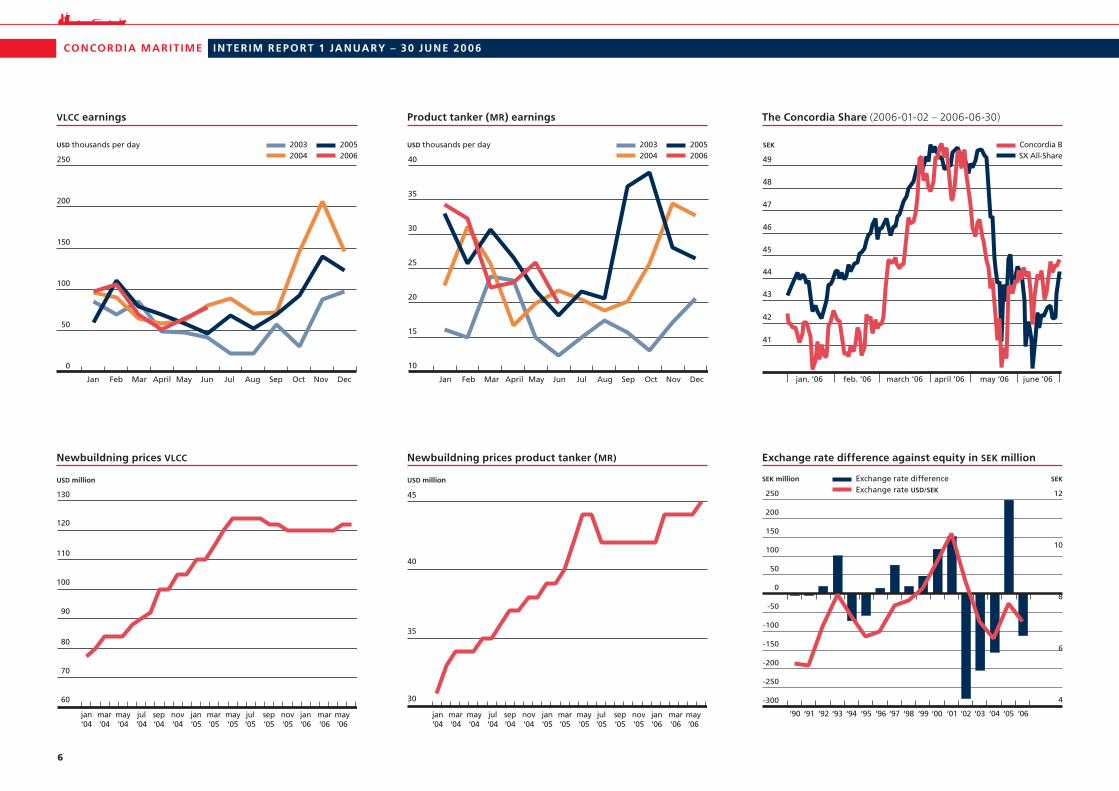

The marketL a rg e ta n k e r / V L C C The freight rates, which had began to decline in the first quarter, continued during April. The decline is due in part to the seasonal drop in the demand for crude oil and reductions in crude oil stocks during this pe-riod. In May and June, the freight rates recovered and reached higher levels than during the same periods in 2005.

P rod u C t ta n k e r The big trade for mr-vessels, gasoline from Europe to USA, has had stable and good freight rates during the first six months. Principally this is due to steady and good demand. The summer has started strong with freight rates slightly better then last year. Other product tank markets such as the Caribbean, Mediterranean and the Far East are volatile and in general has been weaker then last years rates.

Shipbuilding marketThe shipbuilding market continues to be strong. In the vlcc segment, increased activity has contributed to an upswing in newbuilding prices, which stabilised at around usd 125 mil-lion during the second quarter. Prices in the mr segment also increased somewhat during the second quarter and appear to be levelling out at about usd 45 million in the case of vessels with delivery set for 2009 – 2010.

The second-hand market for tonnage, particularly mod-ern, continued to be even and strong during the period.

The Share The annual general meeting approved a dividend of sek 1 per share. The dividend was distributed on 5 May with 2 May as the record day for payment.

Financial summaryS a L e S a n d r e S u Lt Sales amounted to sek 153.3 (185.3) million. The result after financial items was sek 23.0 (31.0) million, which included a profit of sek 0.0 (51.5) million on the sale of ships. The profit after tax was sek 18.7 (27.9) mil-lion, which corresponds to a profit per share after tax of sek 0.39 (0.58).

S e C o n d qua r t e r Sales during the second quarter were sek 80.6 (67.3) million. The result after financial items was sek 4.7 (3.1) million, which included a result of sek 0.0 (4.1)

million from the sale of ships. The profit after tax was sek 3.6 (0.9) million, which corresponds to a profit per share of sek 0.08 (0.02).

T H E C O N C O R D I A M A R I T I M E F L E E T

Class Vessel Year Size, dwt Employment (on delivery)

Panamax Stena Poseidon 2006 74,500 Neste Oil, ten years

Neste Polaris 2007 74,500 Neste Oil, ten yearsten years

P-MAX Stena Paris 2005 65,200 TOTAL, five years

Stena Provence 2006 65,200 TOTAL, five yearsfive years

Stena Performance 2006 65,200 Amerada Hess five years

Stena Primorsk 2006 65,200 Progetra, ten years

Stena Progetra 2007 65,200 Progetra, ten yearsten years

Stena Perros 2008 65,200 TOTAL, five yearsfive years

Stena Progress 2009 65,200

Stena Prosperity 2009 65,200

V-MAX Stena Vision 2001 312,600 Time-chartered until end of 2009

Stena Victory 2001 312,600 Time-chartered until end of 2009

TOTAL 1,295,80

CONCORDIA MARIT IMEINTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

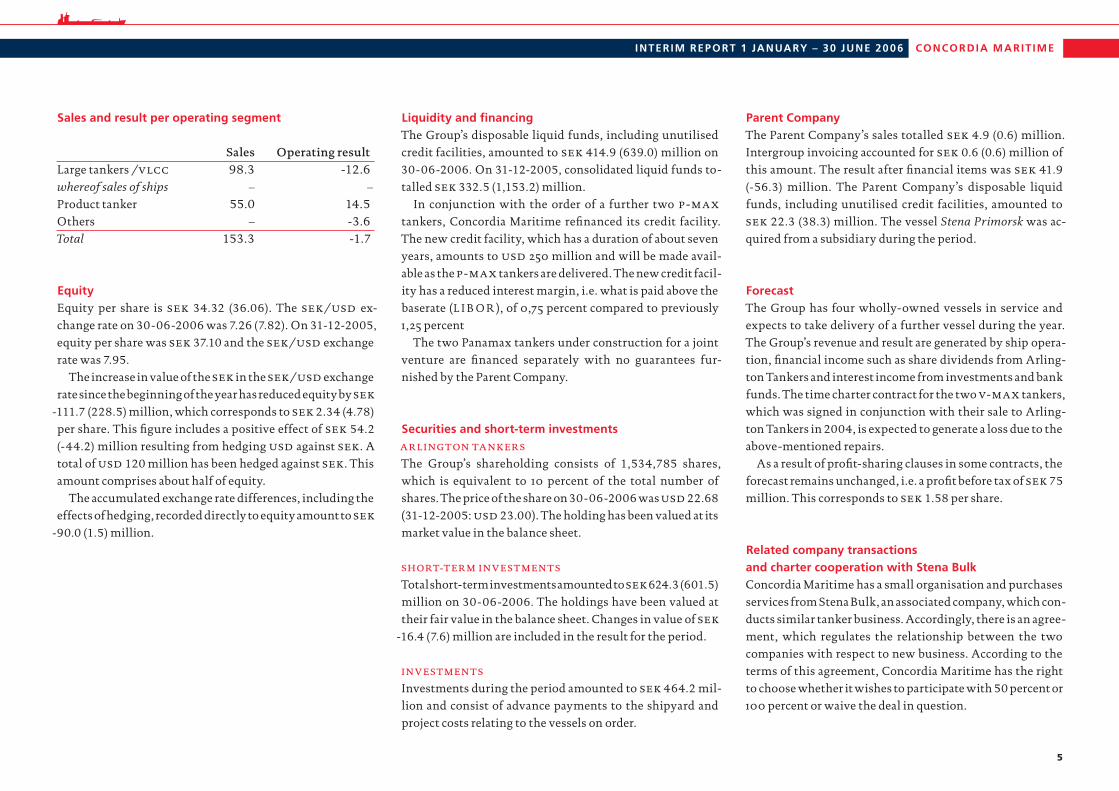

Sales and result per operating segment

Sales OperatingresultLarge tankers /vlcc 98.3 -12.6whereof sales of ships – –Product tanker 55.0 14.5 Others – -3.6Total 153.3 -1.7

EquityEquity per share is sek 34.32 (36.06). The sek/usd ex-change rate on 30-06-2006 was 7.26 (7.82). On 31-12-2005,

equity per share was sek 37.10 and the sek/usd exchange rate was 7.95.

The increase in value of the sek in the sek/usd exchange rate since the beginning of the year has reduced equity by sek

-111.7 (228.5) million, which corresponds to sek 2.34 (4.78) per share. This figure includes a positive effect of sek 54.2

(-44.2) million resulting from hedging usd against sek . A total of usd 120 million has been hedged against sek . This amount comprises about half of equity.

The accumulated exchange rate differences, including the effects of hedging, recorded directly to equity amount to sek

-90.0 (1.5) million.

Liquidity and financingThe Group’s disposable liquid funds, including unutilised credit facilities, amounted to sek 414.9 (639.0) million on 30-06-2006. On 31-12-2005, consolidated liquid funds to-talled sek 332.5 (1,153.2) million.

In conjunction with the order of a further two p-max tankers, Concordia Maritime refinanced its credit facility. The new credit facility, which has a duration of about seven years, amounts to usd 250 million and will be made avail-able as the p-max tankers are delivered. The new credit facil-ity has a reduced interest margin, i.e. what is paid above the baserate (L I B O R ), of 0,75 percent compared to previously 1,25 percent

The two Panamax tankers under construction for a joint venture are financed separately with no guarantees fur-nished by the Parent Company.

Securities and short-term investmentsa r L i ng t on ta n k e r S

The Group’s shareholding consists of 1,534,785 shares, which is equivalent to 10 percent of the total number of shares. The price of the share on 30-06-2006 was usd 22.68

(31-12-2005: usd 23.00). The holding has been valued at its market value in the balance sheet.

S hort-t e r m i n V e S t m e n t S

Total short-term investments amounted to sek 624.3 (601.5)

million on 30-06-2006. The holdings have been valued at their fair value in the balance sheet. Changes in value of sek

-16.4 (7.6) million are included in the result for the period.

i n V e S t m e n t S

Investments during the period amounted to sek 464.2 mil-lion and consist of advance payments to the shipyard and project costs relating to the vessels on order.

Parent CompanyThe Parent Company’s sales totalled sek 4.9 (0.6) million. Intergroup invoicing accounted for sek 0.6 (0.6) million of this amount. The result after financial items was sek 41.9

(-56.3) million. The Parent Company’s disposable liquid funds, including unutilised credit facilities, amounted to sek 22.3 (38.3) million. The vessel Stena Primorsk was ac-quired from a subsidiary during the period.

ForecastThe Group has four wholly-owned vessels in service and expects to take delivery of a further vessel during the year. The Group’s revenue and result are generated by ship opera-tion, financial income such as share dividends from Arling-ton Tankers and interest income from investments and bank funds. The time charter contract for the two v-max tankers, which was signed in conjunction with their sale to Arling-ton Tankers in 2004, is expected to generate a loss due to the above-mentioned repairs.

As a result of profit-sharing clauses in some contracts, the forecast remains unchanged, i.e. a profit before tax of sek 75

million. This corresponds to sek 1.58 per share.

Related company transactions and charter cooperation with Stena BulkConcordia Maritime has a small organisation and purchases services from Stena Bulk, an associated company, which con-ducts similar tanker business. Accordingly, there is an agree-ment, which regulates the relationship between the two companies with respect to new business. According to the terms of this agreement, Concordia Maritime has the right to choose whether it wishes to participate with 50 percent or 100 percent or waive the deal in question.

CONCORDIA MARIT IME INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

0

50

100

150

200

250

Jan Feb Mar April May Jun Jul Aug Sep Oct Nov Dec

2003USD thousands per day2004

20052006

VLCC earnings

Jan Feb Mar April May Jun Jul Aug Sep Oct Nov Dec

USD thousands per day 20032004

20052006

10

15

20

25

30

35

40

Product tanker (MR) earnings

SEK

jan. ’06 feb. ’06 march ’06 april ’06 may ’06 june ’06

49

48

47

46

45

44

43

42

41

Concordia BSX All-Share

The Concordia Share (2006-01-02 – 2006-06-30)

jan‘04

mar‘04

may‘04

jul‘04

sep‘04

nov‘04

jan‘05

mar‘05

may‘05

jul‘05

sep‘05

nov‘05

jan‘06

mar‘06

may‘06

USD million

60

70

80

100

110

130

90

120

Newbuildning prices VLCC

jan‘04

mar‘04

may‘04

jul‘04

sep‘04

nov‘04

jan‘05

mar‘05

may‘05

jul‘05

sep‘05

nov‘05

jan‘06

mar‘06

may‘06

USD million

30

35

45

40

Newbuildning prices product tanker (MR)

SEK million SEK

-300

-250

-200

-150

-100

-50

0

50

100

150

200

250

‘90 ‘91 ‘92 ‘93 ‘94 ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06

4

6

8

10

12

Exchange rate differenceExchange rate USD/SEK

Exchange rate difference against equity in SEK million

CONCORDIA MARIT IMEINTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

Concordia purchases services on a regular basis from Stena Bulk or other companies in the Stena Sphere in the follow-ing areas:

n �essel charter. Payment is based on a commission of�essel charter. Payment is based on a commission of 1.25 percent on freight rates

n Commission on the purchase and sale of vessels.Commission on the purchase and sale of vessels. Payment is based on a commission of 1percent on purchases and sales

n Operation and manning of the Group’s vessels, so-calledOperation and manning of the Group’s vessels, so-called ship management. Payment is based on a fixed price per year and vessel

n Purchases of bunker oil. Payment is based on a fixedPurchases of bunker oil. Payment is based on a fixed commission per ton purchased

n Administration, marketing, insurance, technical fol-Administration, marketing, insurance, technical fol-low-up and development of Concordia’s fleet. Payment is based on a fixed price per month and vessel. In the case of technical consulting services for newbuilding projects, an hourly rate is charged on current account, which is then charged to the project

n Office rent and office services for Concordia’s personnel.Office rent and office services for Concordia’s personnel. A fixed price per year is charged

All related company transactions take place on commercial terms and at market-related prices.

Reports and informationThe interim report for the first nine months will be published on 19 October and and the result for the full year on 15 Febru-ary, 2007. Historical and current reports, together with news and comments on the Company and the tanker markets, can be found on our web site www.concordia-maritime.se.

Gothenburg, 10 August, 2006

c o n c o r d i a m a r i t i m e a b (publ)

Hans NorénPresident

CONCORDIA MARIT IME INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

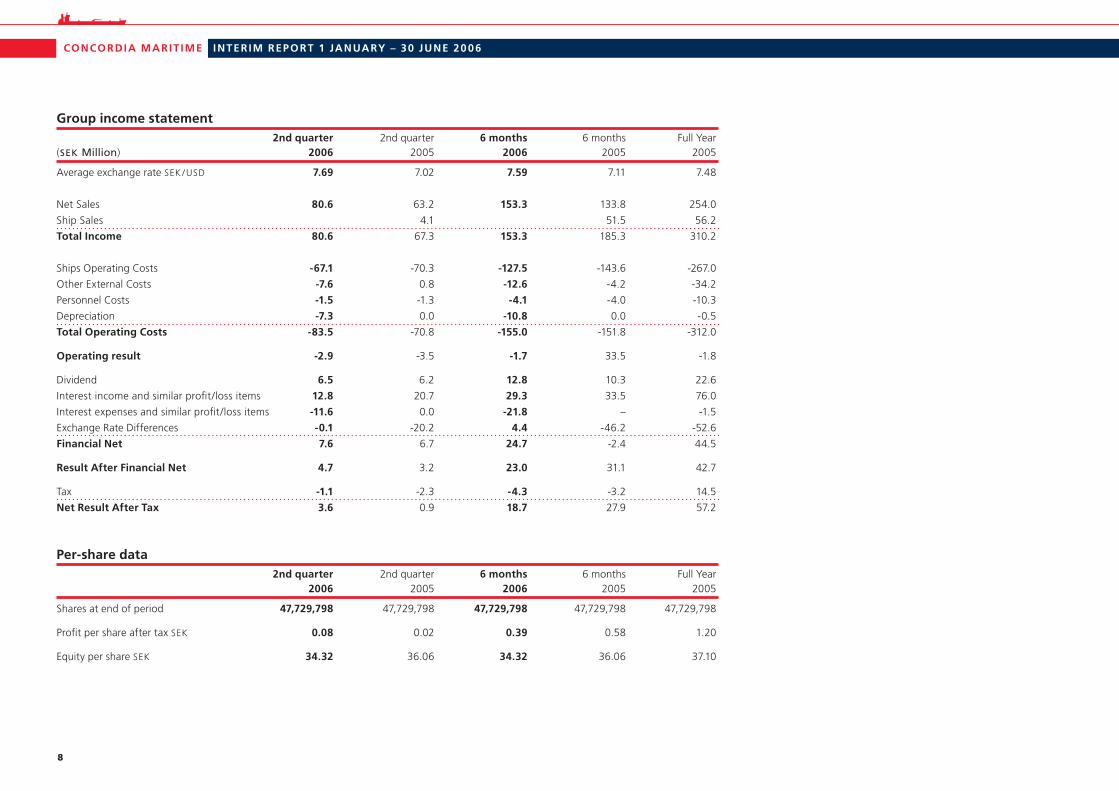

Group income statement 2nd quarter 2nd quarter 6 months 6 months Full Year(SEK Million) 2006 2005 2006 2005 2005

Average exchange rate SEK / USD 7.69 7.02 7.59 7.11 7.48

Net Sales 80.6 63.2 153.3 133.8 254.0

Ship Sales 4.1 51.5 56.2

Total Income 80.6 67.3 153.3 185.3 310.2

Ships Operating Costs -67.1 -70.3 -127.5 -143.6 -267.0

Other External Costs -7.6 0.8 -12.6 -4.2 -34.2

Personnel Costs -1.5 -1.3 -4.1 -4.0 -10.3

Depreciation -7.3 0.0 -10.8 0.0 -0.5

Total Operating Costs -83.5 -70.8 -155.0 -151.8 -312.0

Operating result -2.9 -3.5 -1.7 33.5 -1.8

Dividend 6.5 6.2 12.8 10.3 22.6

Interest income and similar profit/loss items 12.8 20.7 29.3 33.5 76.0

Interest expenses and similar profit/loss items -11.6 0.0 -21.8 – -1.5

Exchange Rate Differences -0.1 -20.2 4.4 -46.2 -52.6

Financial Net 7.6 6.7 24.7 -2.4 44.5

Result After Financial Net 4.7 3.2 23.0 31.1 42.7

Tax -1.1 -2.3 -4.3 -3.2 14.5

Net Result After Tax 3.6 0.9 18.7 27.9 57.2

Per-share data 2nd quarter 2nd quarter 6 months 6 months Full Year 2006 2005 2006 2005 2005

Shares at end of period 47,729,798 47,729,798 47,729,798 47,729,798 47,729,798

Profit per share after tax SEK 0.08 0.02 0.39 0.58 1.20

Equity per share SEK 34.32 36.06 34.32 36.06 37.10

CONCORDIA MARIT IMEINTERIM REPORT 1 JANUARY – 30 JUNE 20 06

�

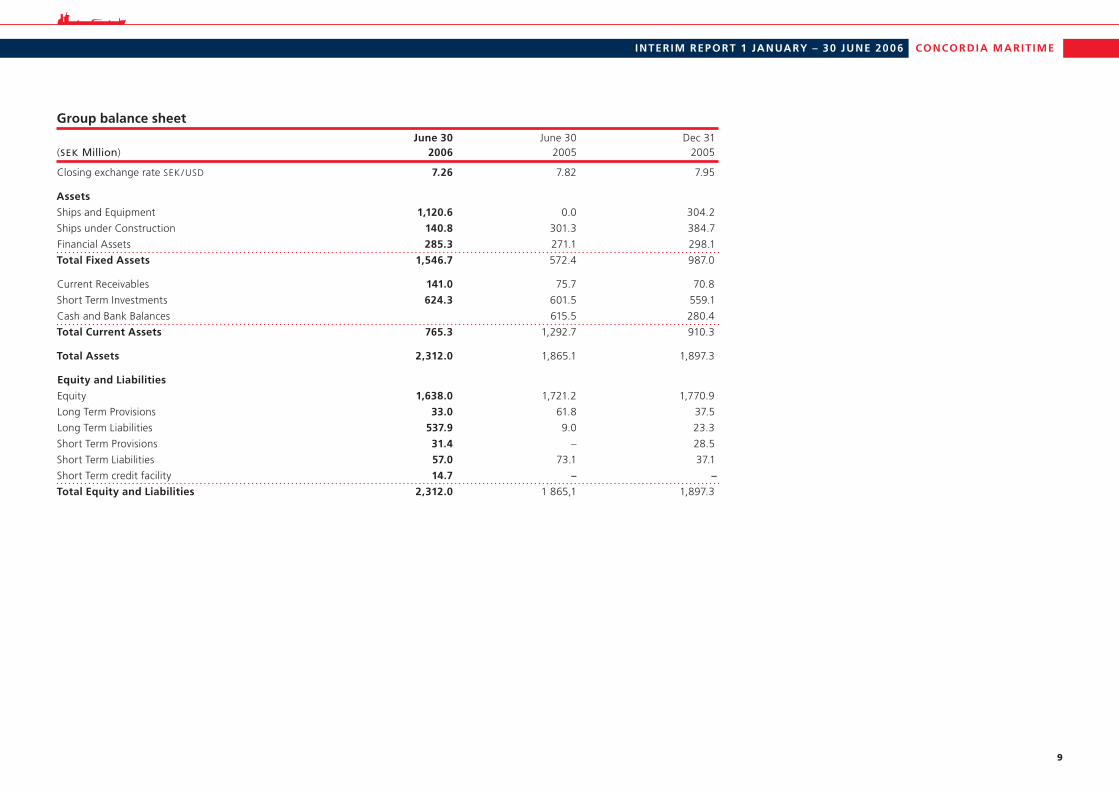

Group balance sheet June 30 June 30 Dec 31(SEK Million) 2006 2005 2005

Closing exchange rate SEK / USD 7.26 7.82 7.95

Assets

Ships and Equipment 1,120.6 0.0 304.2

Ships under Construction 140.8 301.3 384.7

Financial Assets 285.3 271.1 298.1

Total Fixed Assets 1,546.7 572.4 987.0

Current Receivables 141.0 75.7 70.8

Short Term Investments 624.3 601.5 559.1

Cash and Bank Balances 615.5 280.4

Total Current Assets 765.3 1,292.7 910.3

Total Assets 2,312.0 1,865.1 1,897.3

Equity and Liabilities

Equity 1,638.0 1,721.2 1,770.9

Long Term Provisions 33.0 61.8 37.5

Long Term Liabilities 537.9 9.0 23.3

Short Term Provisions 31.4 – 28.5

Short Term Liabilities 57.0 73.1 37.1

Short Term credit facility 14.7 – –

Total Equity and Liabilities 2,312.0 1 865,1 1,897.3

CONCORDIA MARIT IME INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

10

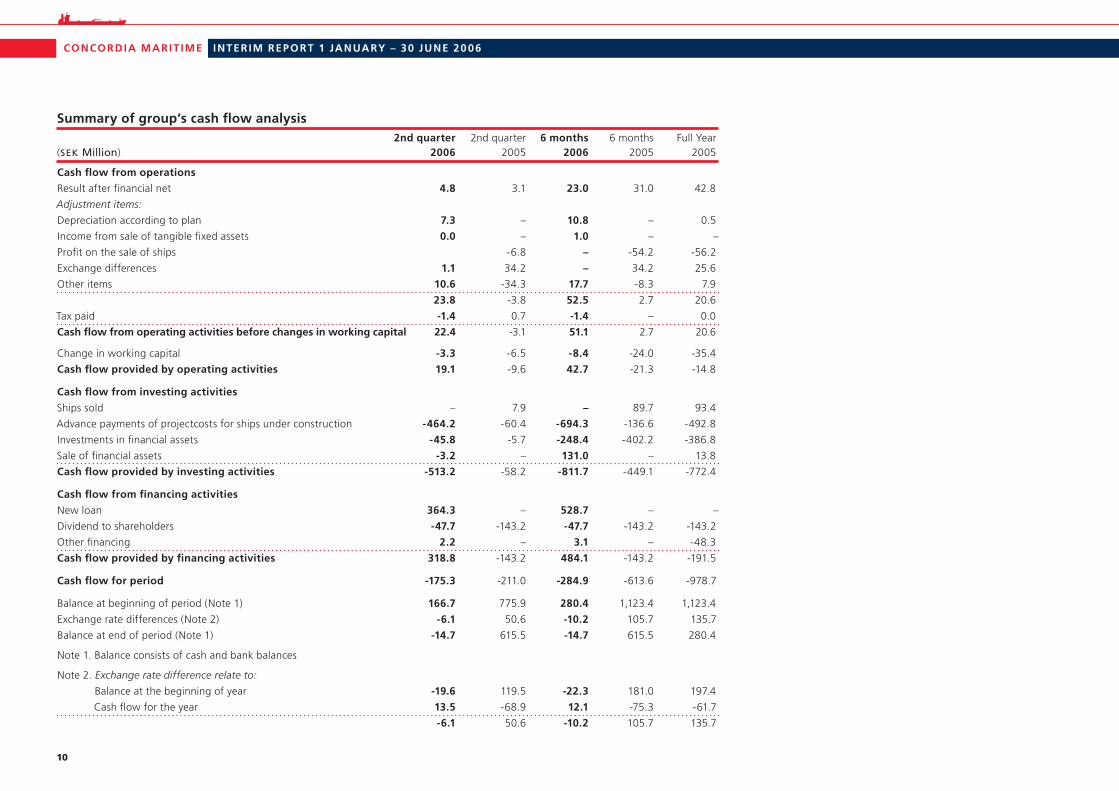

Summary of group’s cash flow analysis 2nd quarter 2nd quarter 6 months 6 months Full Year(SEK Million) 2006 2005 2006 2005 2005

Cash flow from operations

Result after financial net 4.8 3.1 23.0 31.0 42.8

Adjustment items:

Depreciation according to plan 7.3 – 10.8 – 0.5

Income from sale of tangible fixed assets 0.0 – 1.0 – –

Profit on the sale of ships -6.8 – -54.2 -56.2

Exchange differences 1.1 34.2 – 34.2 25.6

Other items 10.6 -34.3 17.7 -8.3 7.9

23.8 -3.8 52.5 2.7 20.6

Tax paid -1.4 0.7 -1.4 – 0.0

Cash flow from operating activities before changes in working capital 22.4 -3.1 51.1 2.7 20.6

Change in working capital -3.3 -6.5 -8.4 -24.0 -35.4

Cash flow provided by operating activities 19.1 -9.6 42.7 -21.3 -14.8

Cash flow from investing activities

Ships sold – 7.9 – 89.7 93.4

Advance payments of projectcosts for ships under construction -464.2 -60.4 -694.3 -136.6 -492.8

Investments in financial assets -45.8 -5.7 -248.4 -402.2 -386.8

Sale of financial assets -3.2 – 131.0 – 13.8

Cash flow provided by investing activities -513.2 -58.2 -811.7 -449.1 -772.4

Cash flow from financing activities

New loan 364.3 – 528.7 – –

Dividend to shareholders -47.7 -143.2 -47.7 -143.2 -143.2

Other financing 2.2 – 3.1 – -48.3

Cash flow provided by financing activities 318.8 -143.2 484.1 -143.2 -191.5

Cash flow for period -175.3 -211.0 -284.9 -613.6 -978.7

Balance at beginning of period (Note 1) 166.7 775.9 280.4 1,123.4 1,123.4

Exchange rate differences (Note 2) -6.1 50.6 -10.2 105.7 135.7

Balance at end of period (Note 1) -14.7 615.5 -14.7 615.5 280.4

Note 1. Balance consists of cash and bank balances

Note 2. Exchange rate difference relate to:

Balance at the beginning of year -19.6 119.5 -22.3 181.0 197.4

Cash flow for the year 13.5 -68.9 12.1 -75.3 -61.7

-6.1 50.6 -10.2 105.7 135.7

CONCORDIA MARIT IMEINTERIM REPORT 1 JANUARY – 30 JUNE 20 06

11

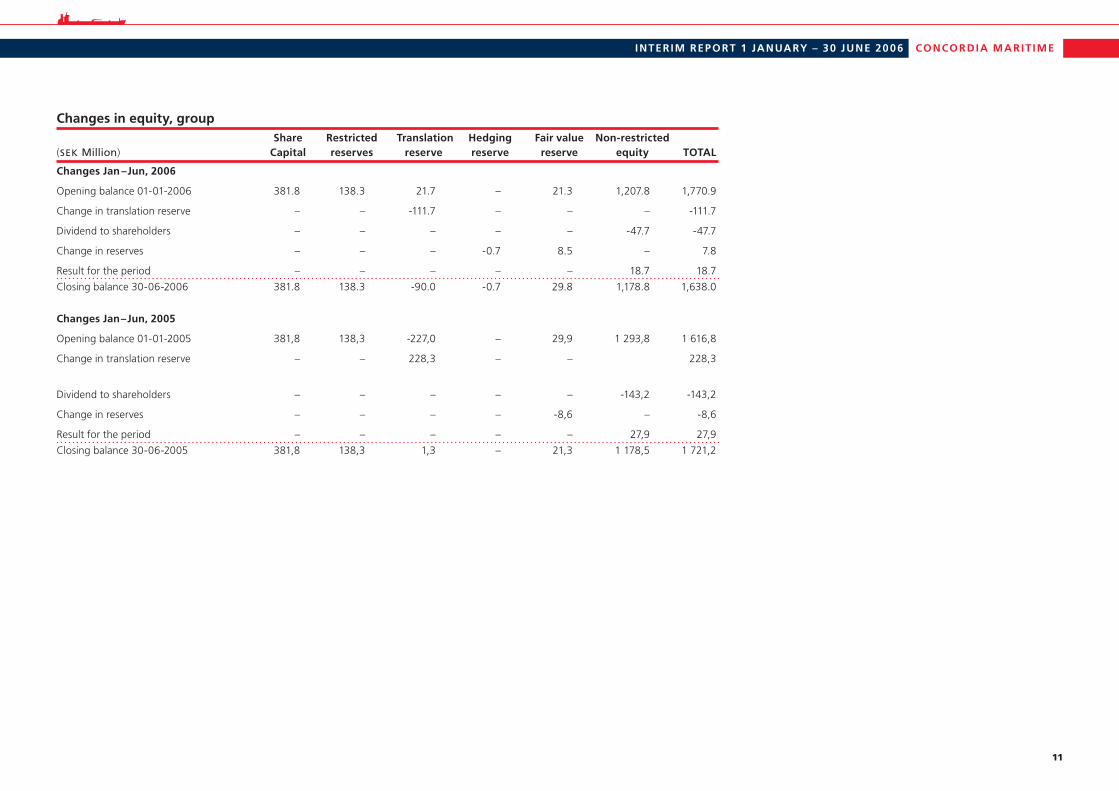

Changes in equity, group Share Restricted Translation Hedging Fair value Non-restricted(SEK Million) Capital reserves reserve reserve reserve equity TOTAL

Changes Jan –Jun, 2006

Opening balance 01-01-2006 381.8 138.3 21.7 – 21.3 1,207.8 1,770.9

Change in translation reserve – – -111.7 – – – -111.7

Dividend to shareholders – – – – – -47.7 -47.7

Change in reserves – – – -0.7 8.5 – 7.8

Result for the period – – – – – 18.7 18.7

Closing balance 30-06-2006 381.8 138.3 -90.0 -0.7 29.8 1,178.8 1,638.0

Changes Jan–Jun, 2005

Opening balance 01-01-2005 381,8 138,3 -227,0 – 29,9 1 293,8 1 616,8

Change in translation reserve – – 228,3 – – 228,3

Dividend to shareholders – – – – – -143,2 -143,2

Change in reserves – – – – -8,6 – -8,6

Result for the period – – – – – 27,9 27,9

Closing balance 30-06-2005 381,8 138,3 1,3 – 21,3 1 178,5 1 721,2

CONCORDIA MARIT IME INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

1�

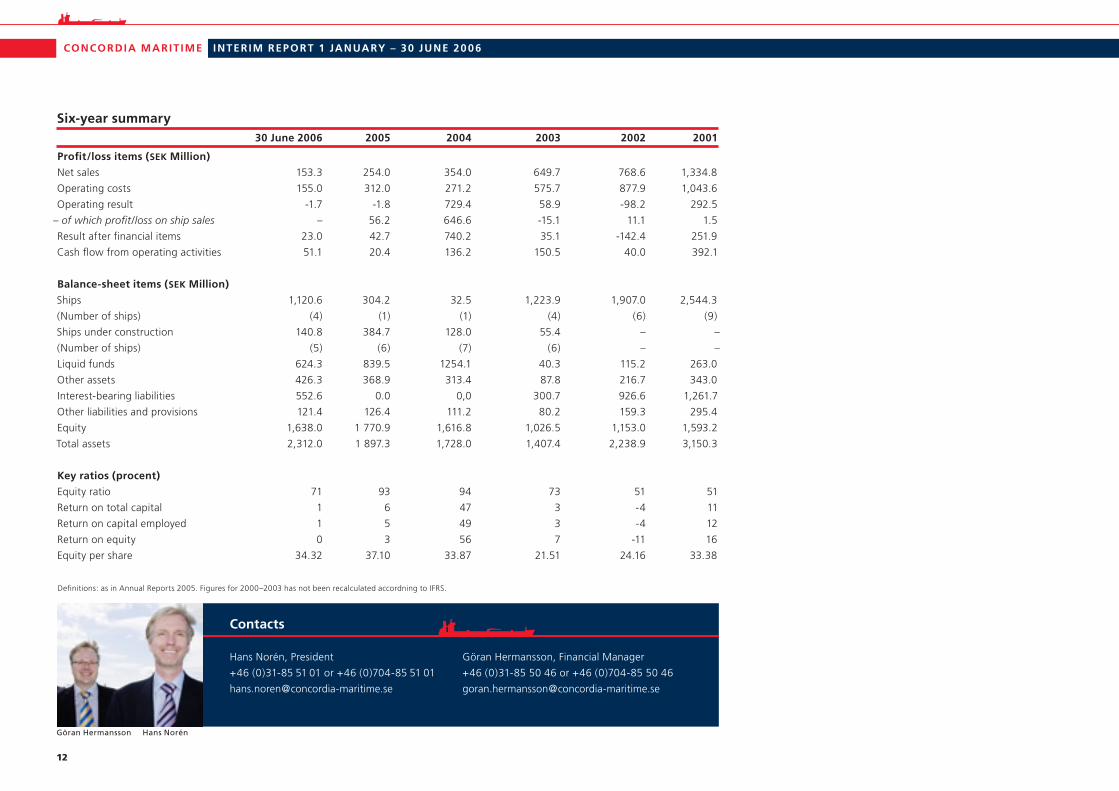

Six-year summary 30 June 2006 2005 2004 2003 2002 2001

Profit/loss items (SEK Million)

Net sales 153.3 254.0 354.0 649.7 768.6 1,334.8

Operating costs 155.0 312.0 271.2 575.7 877.9 1,043.6

Operating result -1.7 -1.8 729.4 58.9 -98.2 292.5

– of which profit/loss on ship sales – 56.2 646.6 -15.1 11.1 1.5

Result after financial items 23.0 42.7 740.2 35.1 -142.4 251.9

Cash flow from operating activities 51.1 20.4 136.2 150.5 40.0 392.1

Balance-sheet items (SEK Million)

Ships 1,120.6 304.2 32.5 1,223.9 1,907.0 2,544.3

(Number of ships) (4) (1) (1) (4) (6) (9)

Ships under construction 140.8 384.7 128.0 55.4 – –

(Number of ships) (5) (6) (7) (6) – –

Liquid funds 624.3 839.5 1254.1 40.3 115.2 263.0

Other assets 426.3 368.9 313.4 87.8 216.7 343.0

Interest-bearing liabilities 552.6 0.0 0,0 300.7 926.6 1,261.7

Other liabilities and provisions 121.4 126.4 111.2 80.2 159.3 295.4

Equity 1,638.0 1 770.9 1,616.8 1,026.5 1,153.0 1,593.2

Total assets 2,312.0 1 897.3 1,728.0 1,407.4 2,238.9 3,150.3

Key ratios (procent)

Equity ratio 71 93 94 73 51 51

Return on total capital 1 6 47 3 -4 11

Return on capital employed 1 5 49 3 -4 12

Return on equity 0 3 56 7 -11 16

Equity per share 34.32 37.10 33.87 21.51 24.16 33.38

Definitions: as in Annual Reports 2005. Figures for 2000–2003 has not been recalculated accordning to IFRS.

Göran Hermansson Hans Norén

Contacts

Hans Norén, President Göran Hermansson, Financial Manager

+46 (0)31-85 51 01 or +46 (0)704-85 51 01 +46 (0)31-85 50 46 or +46 (0)704-85 50 46

CONCORDIA MARIT IME INTERIM REPORT 1 JANUARY – 30 JUNE 20 06

SE-405 19 Gothenburg

Phone +46 31 85 50 00

Fax +46 31 12 06 51

www.concordia-maritime.se

Proactive safety The Stena P-MAX has several features for minimizing the risk of casualties, mishaps

or incidents. Double hull, optimal corrosion control, two engine rooms with full fire and water integrity,

redundant and separate systems for propulsion are vital safeguards for proactive safety. Add manoeuvrability

and an integrated bridge layout to facilitate safe navigation in narrow waters. Sum up with a dedicated and

well-trained crew and you have the Stena P-MAX – probably the safest MR tanker ever.

ww

w.v

icto

ria

gb

g.s

e

Ph

oto

: C

on

ny

Wic

kb

erg

/Ka

tja

An

de

rsso

n

Illu

stra

tio

ns:

Da

n H

am

be

Related Documents