Interim Financial Report | Q3 FY 2020-21 1 Interim Financial Statements As of 13 th April 2021 (31 st Chaitra 2077)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Interim Financial Report | Q3 FY 2020-21 1

Interim Financial Statements As of 13th April 2021 (31st Chaitra 2077)

Interim Financial Report | Q3 FY 2020-21 2

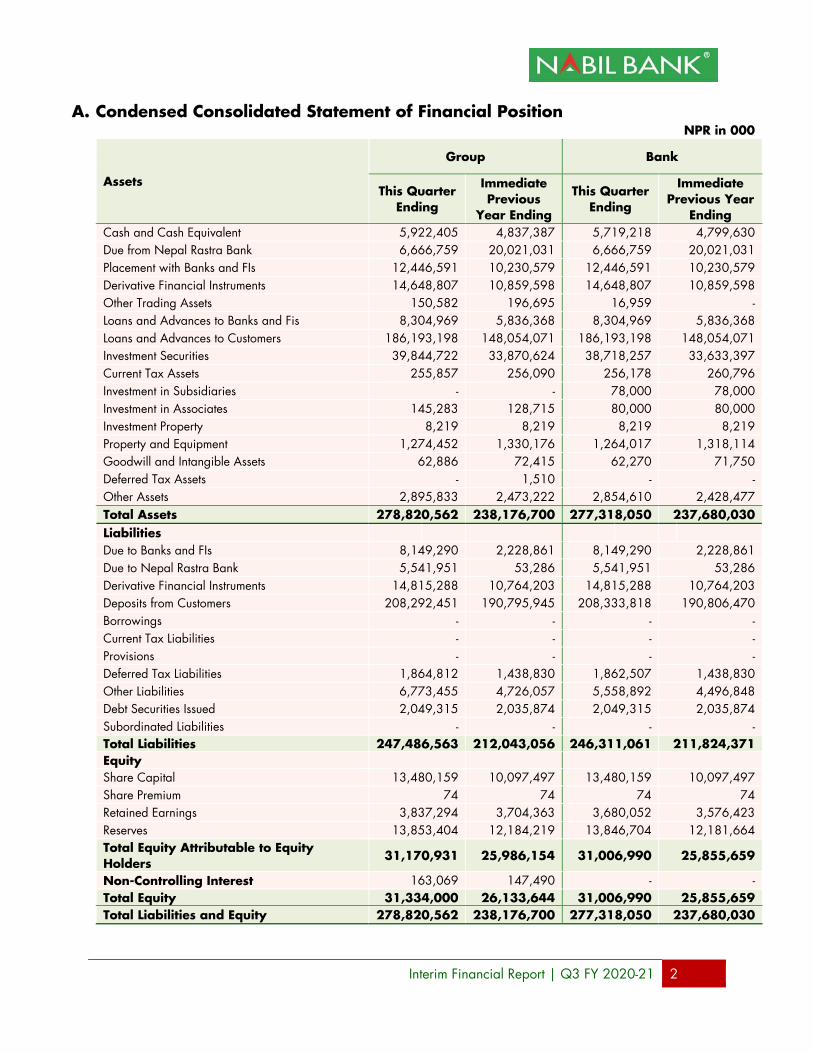

A. Condensed Consolidated Statement of Financial Position NPR in 000

Assets

Group Bank

This Quarter Ending

Immediate Previous

Year Ending

This Quarter Ending

Immediate Previous Year

Ending Cash and Cash Equivalent 5,922,405 4,837,387 5,719,218 4,799,630 Due from Nepal Rastra Bank 6,666,759 20,021,031 6,666,759 20,021,031 Placement with Banks and FIs 12,446,591 10,230,579 12,446,591 10,230,579 Derivative Financial Instruments 14,648,807 10,859,598 14,648,807 10,859,598 Other Trading Assets 150,582 196,695 16,959 - Loans and Advances to Banks and Fis 8,304,969 5,836,368 8,304,969 5,836,368 Loans and Advances to Customers 186,193,198 148,054,071 186,193,198 148,054,071 Investment Securities 39,844,722 33,870,624 38,718,257 33,633,397 Current Tax Assets 255,857 256,090 256,178 260,796 Investment in Subsidiaries - - 78,000 78,000 Investment in Associates 145,283 128,715 80,000 80,000 Investment Property 8,219 8,219 8,219 8,219 Property and Equipment 1,274,452 1,330,176 1,264,017 1,318,114 Goodwill and Intangible Assets 62,886 72,415 62,270 71,750 Deferred Tax Assets - 1,510 - - Other Assets 2,895,833 2,473,222 2,854,610 2,428,477 Total Assets 278,820,562 238,176,700 277,318,050 237,680,030 Liabilities Due to Banks and FIs 8,149,290 2,228,861 8,149,290 2,228,861 Due to Nepal Rastra Bank 5,541,951 53,286 5,541,951 53,286 Derivative Financial Instruments 14,815,288 10,764,203 14,815,288 10,764,203 Deposits from Customers 208,292,451 190,795,945 208,333,818 190,806,470 Borrowings - - - - Current Tax Liabilities - - - - Provisions - - - - Deferred Tax Liabilities 1,864,812 1,438,830 1,862,507 1,438,830 Other Liabilities 6,773,455 4,726,057 5,558,892 4,496,848 Debt Securities Issued 2,049,315 2,035,874 2,049,315 2,035,874 Subordinated Liabilities - - - - Total Liabilities 247,486,563 212,043,056 246,311,061 211,824,371 Equity

Share Capital 13,480,159 10,097,497 13,480,159 10,097,497 Share Premium 74 74 74 74 Retained Earnings 3,837,294 3,704,363 3,680,052 3,576,423 Reserves 13,853,404 12,184,219 13,846,704 12,181,664 Total Equity Attributable to Equity Holders

31,170,931 25,986,154 31,006,990 25,855,659

Non-Controlling Interest 163,069 147,490 - - Total Equity 31,334,000 26,133,644 31,006,990 25,855,659 Total Liabilities and Equity 278,820,562 238,176,700 277,318,050 237,680,030

Interim Financial Report | Q3 FY 2020-21 3

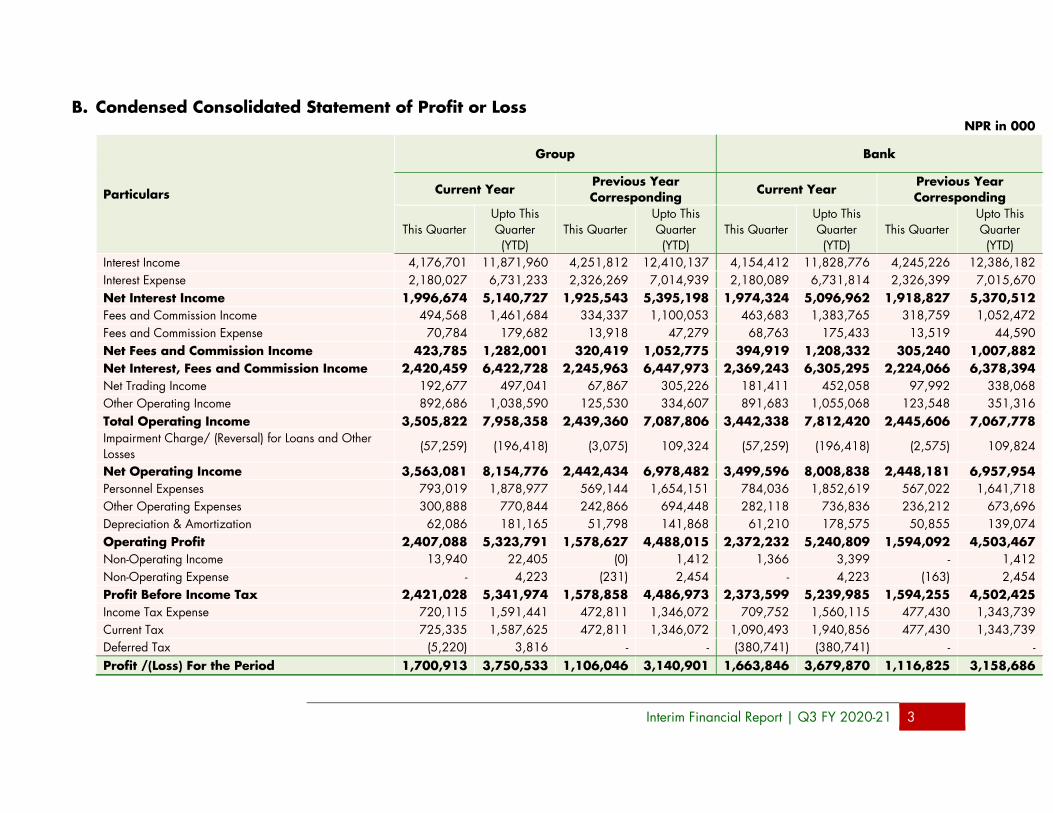

B. Condensed Consolidated Statement of Profit or Loss NPR in 000

Particulars

Group Bank

Current Year Previous Year Corresponding

Current Year Previous Year Corresponding

This Quarter Upto This Quarter (YTD)

This Quarter Upto This Quarter (YTD)

This Quarter Upto This Quarter (YTD)

This Quarter Upto This Quarter (YTD)

Interest Income 4,176,701 11,871,960 4,251,812 12,410,137 4,154,412 11,828,776 4,245,226 12,386,182 Interest Expense 2,180,027 6,731,233 2,326,269 7,014,939 2,180,089 6,731,814 2,326,399 7,015,670 Net Interest Income 1,996,674 5,140,727 1,925,543 5,395,198 1,974,324 5,096,962 1,918,827 5,370,512 Fees and Commission Income 494,568 1,461,684 334,337 1,100,053 463,683 1,383,765 318,759 1,052,472 Fees and Commission Expense 70,784 179,682 13,918 47,279 68,763 175,433 13,519 44,590 Net Fees and Commission Income 423,785 1,282,001 320,419 1,052,775 394,919 1,208,332 305,240 1,007,882 Net Interest, Fees and Commission Income 2,420,459 6,422,728 2,245,963 6,447,973 2,369,243 6,305,295 2,224,066 6,378,394 Net Trading Income 192,677 497,041 67,867 305,226 181,411 452,058 97,992 338,068 Other Operating Income 892,686 1,038,590 125,530 334,607 891,683 1,055,068 123,548 351,316 Total Operating Income 3,505,822 7,958,358 2,439,360 7,087,806 3,442,338 7,812,420 2,445,606 7,067,778 Impairment Charge/ (Reversal) for Loans and Other Losses

(57,259) (196,418) (3,075) 109,324 (57,259) (196,418) (2,575) 109,824

Net Operating Income 3,563,081 8,154,776 2,442,434 6,978,482 3,499,596 8,008,838 2,448,181 6,957,954 Personnel Expenses 793,019 1,878,977 569,144 1,654,151 784,036 1,852,619 567,022 1,641,718 Other Operating Expenses 300,888 770,844 242,866 694,448 282,118 736,836 236,212 673,696 Depreciation & Amortization 62,086 181,165 51,798 141,868 61,210 178,575 50,855 139,074 Operating Profit 2,407,088 5,323,791 1,578,627 4,488,015 2,372,232 5,240,809 1,594,092 4,503,467 Non-Operating Income 13,940 22,405 (0) 1,412 1,366 3,399 - 1,412 Non-Operating Expense - 4,223 (231) 2,454 - 4,223 (163) 2,454 Profit Before Income Tax 2,421,028 5,341,974 1,578,858 4,486,973 2,373,599 5,239,985 1,594,255 4,502,425 Income Tax Expense 720,115 1,591,441 472,811 1,346,072 709,752 1,560,115 477,430 1,343,739 Current Tax 725,335 1,587,625 472,811 1,346,072 1,090,493 1,940,856 477,430 1,343,739 Deferred Tax (5,220) 3,816 - - (380,741) (380,741) - - Profit /(Loss) For the Period 1,700,913 3,750,533 1,106,046 3,140,901 1,663,846 3,679,870 1,116,825 3,158,686

Interim Financial Report | Q3 FY 2020-21 4

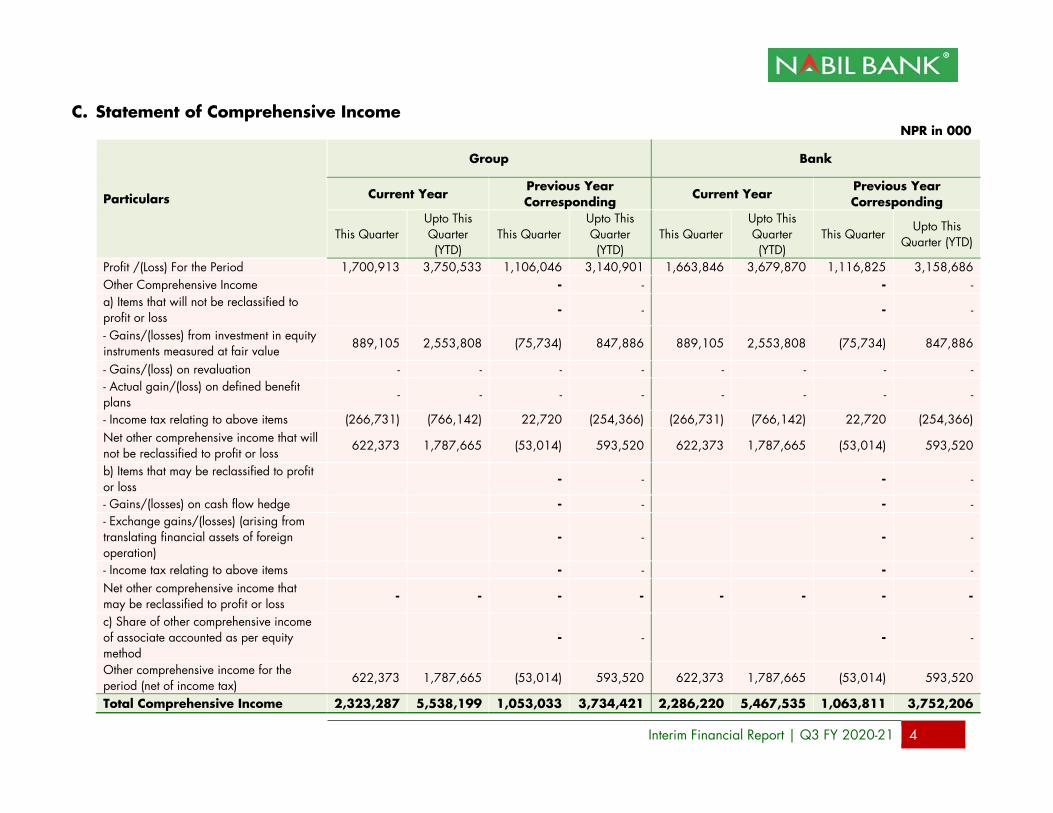

C. Statement of Comprehensive Income NPR in 000

Particulars

Group Bank

Current Year Previous Year Corresponding

Current Year Previous Year Corresponding

This Quarter Upto This Quarter (YTD)

This Quarter Upto This Quarter (YTD)

This Quarter Upto This Quarter (YTD)

This Quarter Upto This

Quarter (YTD)

Profit /(Loss) For the Period 1,700,913 3,750,533 1,106,046 3,140,901 1,663,846 3,679,870 1,116,825 3,158,686 Other Comprehensive Income

- - - -

a) Items that will not be reclassified to profit or loss - -

- -

- Gains/(losses) from investment in equity instruments measured at fair value

889,105 2,553,808 (75,734) 847,886 889,105 2,553,808 (75,734) 847,886

- Gains/(loss) on revaluation - - - - - - - - - Actual gain/(loss) on defined benefit plans

- - - - - - - -

- Income tax relating to above items (266,731) (766,142) 22,720 (254,366) (266,731) (766,142) 22,720 (254,366) Net other comprehensive income that will not be reclassified to profit or loss

622,373 1,787,665 (53,014) 593,520 622,373 1,787,665 (53,014) 593,520

b) Items that may be reclassified to profit or loss - -

- -

- Gains/(losses) on cash flow hedge - -

- - - Exchange gains/(losses) (arising from translating financial assets of foreign operation)

- - - -

- Income tax relating to above items - -

- - Net other comprehensive income that may be reclassified to profit or loss - - - - - - - -

c) Share of other comprehensive income of associate accounted as per equity method

- - - -

Other comprehensive income for the period (net of income tax)

622,373 1,787,665 (53,014) 593,520 622,373 1,787,665 (53,014) 593,520

Total Comprehensive Income 2,323,287 5,538,199 1,053,033 3,734,421 2,286,220 5,467,535 1,063,811 3,752,206

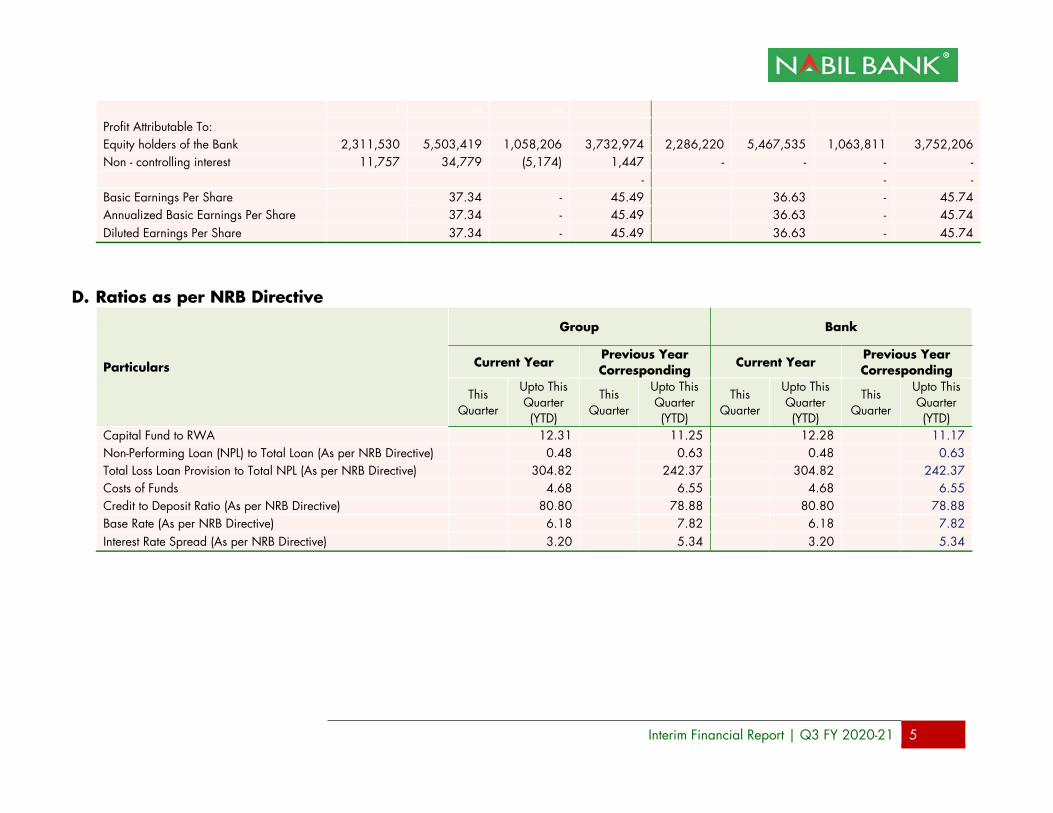

Interim Financial Report | Q3 FY 2020-21 5

- - - - - - - -

Profit Attributable To:

Equity holders of the Bank 2,311,530 5,503,419 1,058,206 3,732,974 2,286,220 5,467,535 1,063,811 3,752,206 Non - controlling interest 11,757 34,779 (5,174) 1,447 - - - -

-

- -

Basic Earnings Per Share

37.34 - 45.49

36.63 - 45.74 Annualized Basic Earnings Per Share

37.34 - 45.49

36.63 - 45.74

Diluted Earnings Per Share

37.34 - 45.49

36.63 - 45.74

D. Ratios as per NRB Directive

Particulars

Group Bank

Current Year Previous Year Corresponding

Current Year Previous Year Corresponding

This Quarter

Upto This Quarter (YTD)

This Quarter

Upto This Quarter (YTD)

This Quarter

Upto This Quarter (YTD)

This Quarter

Upto This Quarter (YTD)

Capital Fund to RWA

12.31

11.25

12.28

11.17 Non-Performing Loan (NPL) to Total Loan (As per NRB Directive)

0.48

0.63

0.48

0.63

Total Loss Loan Provision to Total NPL (As per NRB Directive)

304.82

242.37

304.82

242.37 Costs of Funds

4.68

6.55

4.68

6.55

Credit to Deposit Ratio (As per NRB Directive)

80.80

78.88

80.80

78.88 Base Rate (As per NRB Directive)

6.18

7.82

6.18

7.82

Interest Rate Spread (As per NRB Directive)

3.20

5.34

3.20

5.34

Interim Financial Report | Q3 FY 2020-21 6

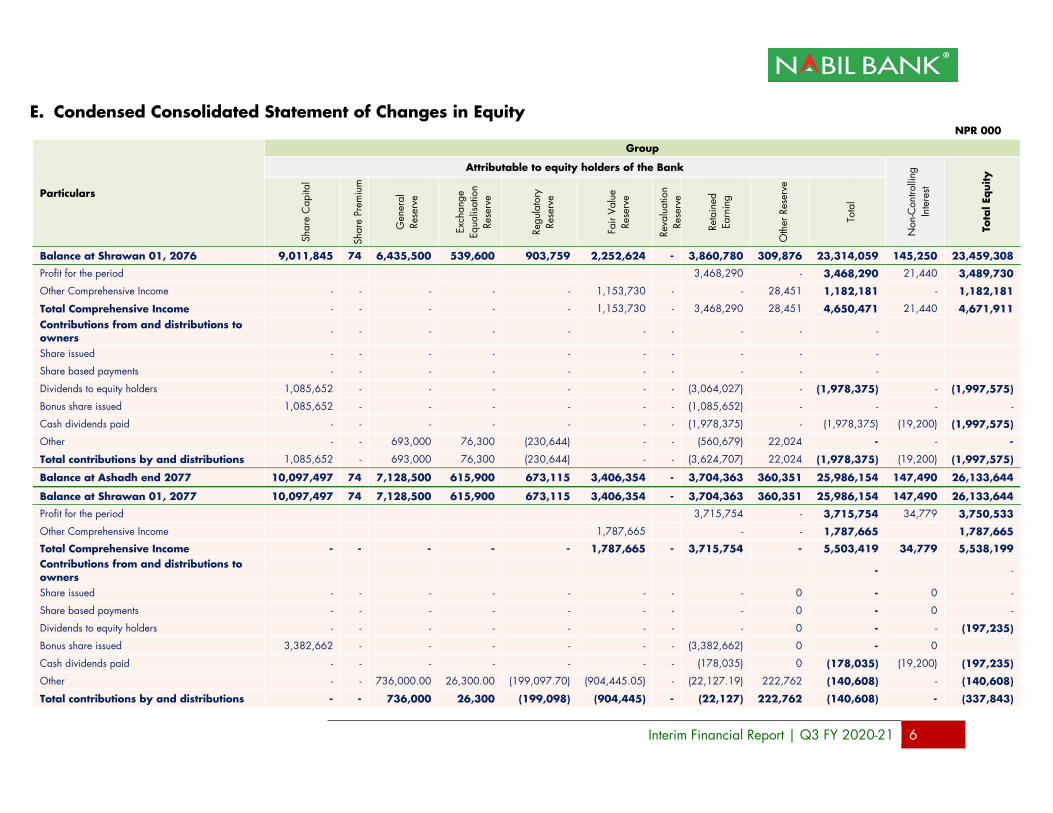

E. Condensed Consolidated Statement of Changes in Equity NPR 000

Particulars

Group

Attributable to equity holders of the Bank

Non

-Con

trolli

ng

Inte

rest

Tota

l Equity

Shar

e C

apita

l

Shar

e Pr

emiu

m

Gen

eral

Re

serv

e

Exch

ange

Eq

ualis

atio

n Re

serv

e

Regu

lato

ry

Rese

rve

Fair

Valu

e Re

serv

e

Reva

luat

ion

Rese

rve

Reta

ined

Ea

rnin

g

Oth

er R

eser

ve

Tota

l

Balance at Shrawan 01, 2076 9,011,845 74 6,435,500 539,600 903,759 2,252,624 - 3,860,780 309,876 23,314,059 145,250 23,459,308

Profit for the period

3,468,290 - 3,468,290 21,440 3,489,730

Other Comprehensive Income - - - - - 1,153,730 - - 28,451 1,182,181 - 1,182,181

Total Comprehensive Income - - - - - 1,153,730 - 3,468,290 28,451 4,650,471 21,440 4,671,911 Contributions from and distributions to owners

- - - - - - - - - -

Share issued - - - - - - - - - -

Share based payments - - - - - - - - - -

Dividends to equity holders 1,085,652 - - - - - - (3,064,027) - (1,978,375) - (1,997,575)

Bonus share issued 1,085,652 - - - - - - (1,085,652) - - - -

Cash dividends paid - - - - - - - (1,978,375) - (1,978,375) (19,200) (1,997,575)

Other - - 693,000 76,300 (230,644) - - (560,679) 22,024 - - -

Total contributions by and distributions 1,085,652 - 693,000 76,300 (230,644) - - (3,624,707) 22,024 (1,978,375) (19,200) (1,997,575)

Balance at Ashadh end 2077 10,097,497 74 7,128,500 615,900 673,115 3,406,354 - 3,704,363 360,351 25,986,154 147,490 26,133,644

Balance at Shrawan 01, 2077 10,097,497 74 7,128,500 615,900 673,115 3,406,354 - 3,704,363 360,351 25,986,154 147,490 26,133,644

Profit for the period

3,715,754 - 3,715,754 34,779 3,750,533

Other Comprehensive Income

1,787,665

- - 1,787,665 1,787,665

Total Comprehensive Income - - - - - 1,787,665 - 3,715,754 - 5,503,419 34,779 5,538,199 Contributions from and distributions to owners -

-

Share issued - - - - - - - - 0 - 0 -

Share based payments - - - - - - - - 0 - 0 -

Dividends to equity holders - - - - - - - - 0 - - (197,235)

Bonus share issued 3,382,662 - - - - - - (3,382,662) 0 - 0

Cash dividends paid - - - - - - - (178,035) 0 (178,035) (19,200) (197,235)

Other - - 736,000.00 26,300.00 (199,097.70) (904,445.05) - (22,127.19) 222,762 (140,608) - (140,608)

Total contributions by and distributions - - 736,000 26,300 (199,098) (904,445) - (22,127) 222,762 (140,608) - (337,843)

Interim Financial Report | Q3 FY 2020-21 7

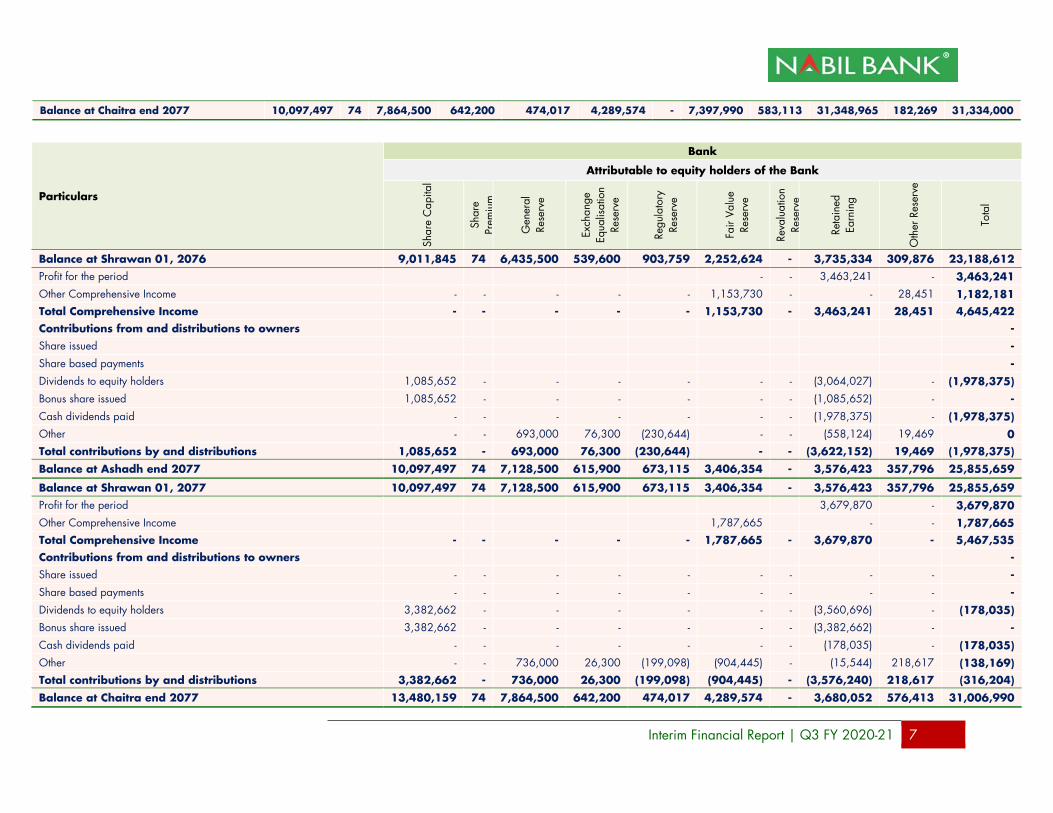

Balance at Chaitra end 2077 10,097,497 74 7,864,500 642,200 474,017 4,289,574 - 7,397,990 583,113 31,348,965 182,269 31,334,000

Particulars

Bank

Attributable to equity holders of the Bank

Shar

e C

apita

l

Shar

e Pr

emiu

m

Gen

eral

Re

serv

e

Exch

ange

Eq

ualis

atio

n Re

serv

e

Regu

lato

ry

Rese

rve

Fair

Valu

e Re

serv

e

Reva

luat

ion

Rese

rve

Reta

ined

Ea

rnin

g

Oth

er R

eser

ve

Tota

l

Balance at Shrawan 01, 2076 9,011,845 74 6,435,500 539,600 903,759 2,252,624 - 3,735,334 309,876 23,188,612 Profit for the period

- - 3,463,241 - 3,463,241

Other Comprehensive Income - - - - - 1,153,730 - - 28,451 1,182,181 Total Comprehensive Income - - - - - 1,153,730 - 3,463,241 28,451 4,645,422 Contributions from and distributions to owners - Share issued

- Share based payments

- Dividends to equity holders 1,085,652 - - - - - - (3,064,027) - (1,978,375)

Bonus share issued 1,085,652 - - - - - - (1,085,652) - -

Cash dividends paid - - - - - - - (1,978,375) - (1,978,375) Other - - 693,000 76,300 (230,644) - - (558,124) 19,469 0 Total contributions by and distributions 1,085,652 - 693,000 76,300 (230,644) - - (3,622,152) 19,469 (1,978,375)

Balance at Ashadh end 2077 10,097,497 74 7,128,500 615,900 673,115 3,406,354 - 3,576,423 357,796 25,855,659

Balance at Shrawan 01, 2077 10,097,497 74 7,128,500 615,900 673,115 3,406,354 - 3,576,423 357,796 25,855,659 Profit for the period

3,679,870 - 3,679,870

Other Comprehensive Income

1,787,665

- - 1,787,665 Total Comprehensive Income - - - - - 1,787,665 - 3,679,870 - 5,467,535 Contributions from and distributions to owners - Share issued - - - - - - - - - -

Share based payments - - - - - - - - - -

Dividends to equity holders 3,382,662 - - - - - - (3,560,696) - (178,035) Bonus share issued 3,382,662 - - - - - - (3,382,662) - - Cash dividends paid - - - - - - - (178,035) - (178,035) Other - - 736,000 26,300 (199,098) (904,445) - (15,544) 218,617 (138,169) Total contributions by and distributions 3,382,662 - 736,000 26,300 (199,098) (904,445) - (3,576,240) 218,617 (316,204)

Balance at Chaitra end 2077 13,480,159 74 7,864,500 642,200 474,017 4,289,574 - 3,680,052 576,413 31,006,990

Interim Financial Report | Q3 FY 2020-21 8

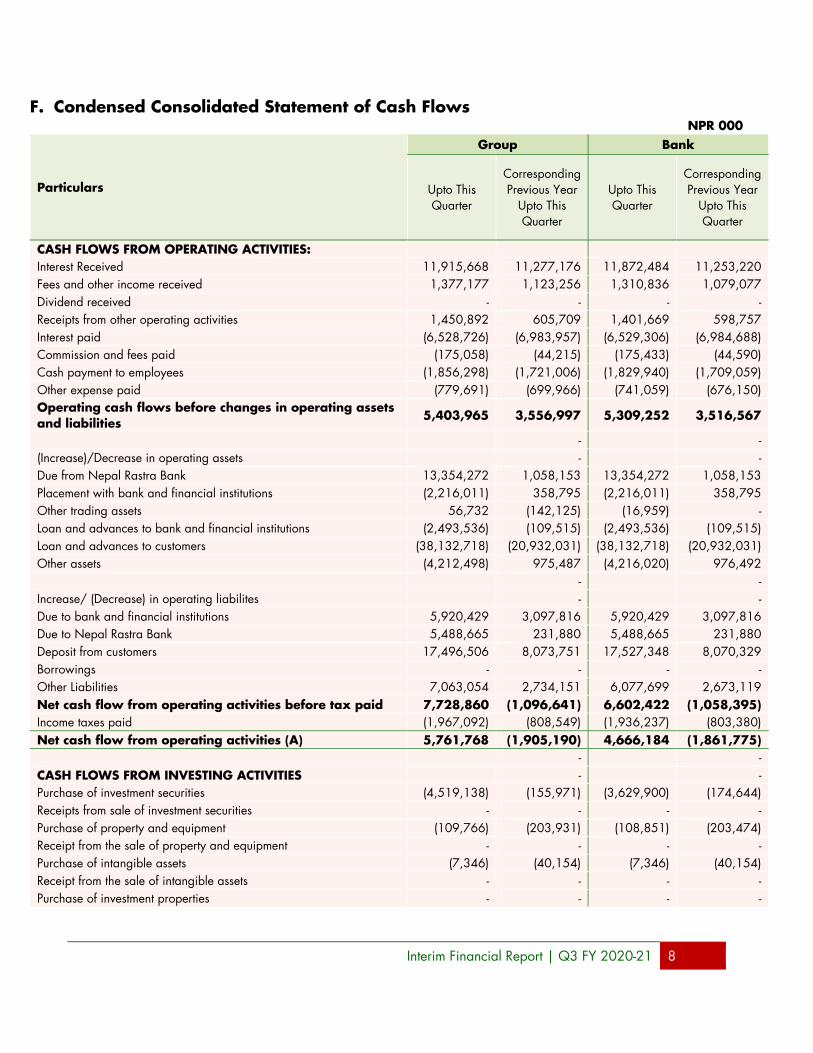

F. Condensed Consolidated Statement of Cash Flows NPR 000

Particulars

Group Bank

Upto This Quarter

Corresponding Previous Year

Upto This Quarter

Upto This Quarter

Corresponding Previous Year

Upto This Quarter

CASH FLOWS FROM OPERATING ACTIVITIES: Interest Received 11,915,668 11,277,176 11,872,484 11,253,220 Fees and other income received 1,377,177 1,123,256 1,310,836 1,079,077 Dividend received - - - - Receipts from other operating activities 1,450,892 605,709 1,401,669 598,757 Interest paid (6,528,726) (6,983,957) (6,529,306) (6,984,688) Commission and fees paid (175,058) (44,215) (175,433) (44,590) Cash payment to employees (1,856,298) (1,721,006) (1,829,940) (1,709,059) Other expense paid (779,691) (699,966) (741,059) (676,150) Operating cash flows before changes in operating assets and liabilities

5,403,965 3,556,997 5,309,252 3,516,567

-

-

(Increase)/Decrease in operating assets

-

- Due from Nepal Rastra Bank 13,354,272 1,058,153 13,354,272 1,058,153 Placement with bank and financial institutions (2,216,011) 358,795 (2,216,011) 358,795 Other trading assets 56,732 (142,125) (16,959) - Loan and advances to bank and financial institutions (2,493,536) (109,515) (2,493,536) (109,515) Loan and advances to customers (38,132,718) (20,932,031) (38,132,718) (20,932,031) Other assets (4,212,498) 975,487 (4,216,020) 976,492

-

-

Increase/ (Decrease) in operating liabilites

-

- Due to bank and financial institutions 5,920,429 3,097,816 5,920,429 3,097,816 Due to Nepal Rastra Bank 5,488,665 231,880 5,488,665 231,880 Deposit from customers 17,496,506 8,073,751 17,527,348 8,070,329 Borrowings - - - - Other Liabilities 7,063,054 2,734,151 6,077,699 2,673,119 Net cash flow from operating activities before tax paid 7,728,860 (1,096,641) 6,602,422 (1,058,395) Income taxes paid (1,967,092) (808,549) (1,936,237) (803,380) Net cash flow from operating activities (A) 5,761,768 (1,905,190) 4,666,184 (1,861,775)

-

-

CASH FLOWS FROM INVESTING ACTIVITIES -

-

Purchase of investment securities (4,519,138) (155,971) (3,629,900) (174,644) Receipts from sale of investment securities - - - - Purchase of property and equipment (109,766) (203,931) (108,851) (203,474) Receipt from the sale of property and equipment - - - - Purchase of intangible assets (7,346) (40,154) (7,346) (40,154) Receipt from the sale of intangible assets - - - - Purchase of investment properties - - - -

Interim Financial Report | Q3 FY 2020-21 9

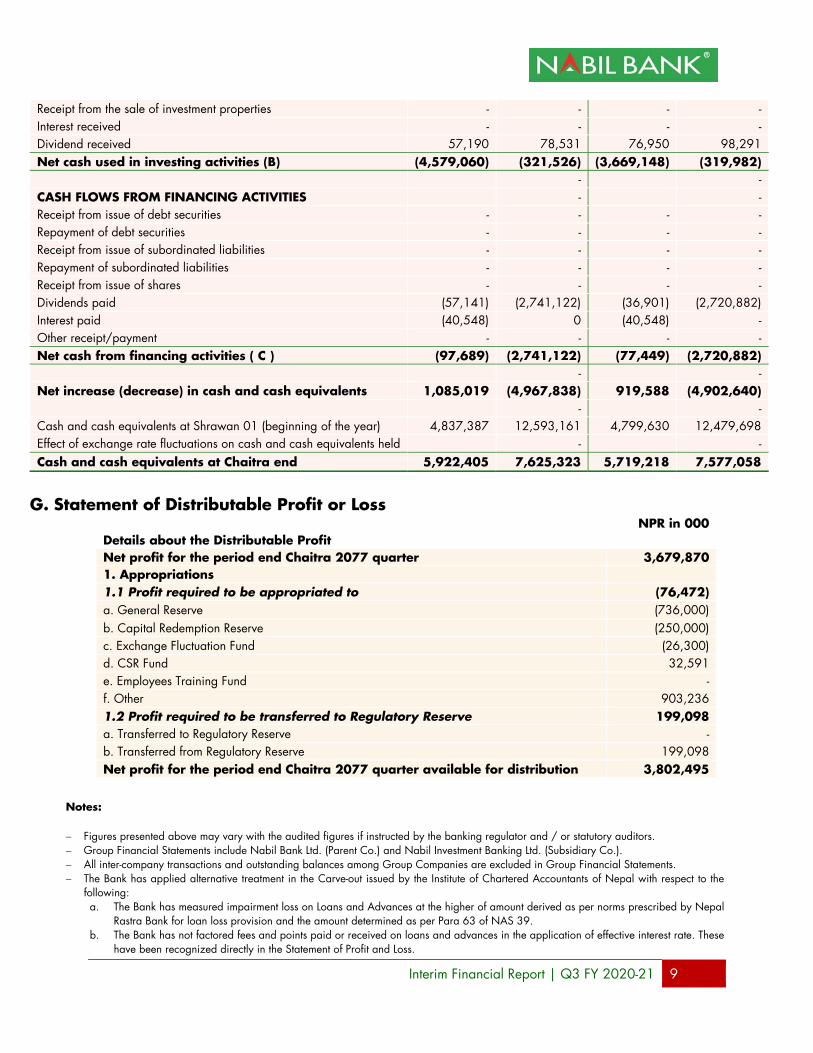

Receipt from the sale of investment properties - - - - Interest received - - - - Dividend received 57,190 78,531 76,950 98,291 Net cash used in investing activities (B) (4,579,060) (321,526) (3,669,148) (319,982)

-

-

CASH FLOWS FROM FINANCING ACTIVITIES -

-

Receipt from issue of debt securities - - - - Repayment of debt securities - - - - Receipt from issue of subordinated liabilities - - - - Repayment of subordinated liabilities - - - - Receipt from issue of shares - - - - Dividends paid (57,141) (2,741,122) (36,901) (2,720,882) Interest paid (40,548) 0 (40,548) - Other receipt/payment - - - - Net cash from financing activities ( C ) (97,689) (2,741,122) (77,449) (2,720,882)

-

-

Net increase (decrease) in cash and cash equivalents 1,085,019 (4,967,838) 919,588 (4,902,640)

-

-

Cash and cash equivalents at Shrawan 01 (beginning of the year) 4,837,387 12,593,161 4,799,630 12,479,698 Effect of exchange rate fluctuations on cash and cash equivalents held

-

-

Cash and cash equivalents at Chaitra end 5,922,405 7,625,323 5,719,218 7,577,058

G. Statement of Distributable Profit or Loss

NPR in 000 Details about the Distributable Profit Net profit for the period end Chaitra 2077 quarter 3,679,870 1. Appropriations 1.1 Profit required to be appropriated to (76,472) a. General Reserve

(736,000)

b. Capital Redemption Reserve (250,000) c. Exchange Fluctuation Fund (26,300) d. CSR Fund 32,591 e. Employees Training Fund - f. Other 903,236 1.2 Profit required to be transferred to Regulatory Reserve 199,098 a. Transferred to Regulatory Reserve - b. Transferred from Regulatory Reserve 199,098 Net profit for the period end Chaitra 2077 quarter available for distribution 3,802,495

Notes:

Figures presented above may vary with the audited figures if instructed by the banking regulator and / or statutory auditors. Group Financial Statements include Nabil Bank Ltd. (Parent Co.) and Nabil Investment Banking Ltd. (Subsidiary Co.). All inter-company transactions and outstanding balances among Group Companies are excluded in Group Financial Statements. The Bank has applied alternative treatment in the Carve-out issued by the Institute of Chartered Accountants of Nepal with respect to the

following: a. The Bank has measured impairment loss on Loans and Advances at the higher of amount derived as per norms prescribed by Nepal

Rastra Bank for loan loss provision and the amount determined as per Para 63 of NAS 39. b. The Bank has not factored fees and points paid or received on loans and advances in the application of effective interest rate. These

have been recognized directly in the Statement of Profit and Loss.

Interim Financial Report | Q3 FY 2020-21 10

Loans and Investments are presented net of impairment charges and includes interest accruals and staff loans. Likewise, deposits include accrued interest payables.

Personnel Expenses includes provision for staff bonus which has been calculated in line with the provisions in Bonus Act.

Figures are regrouped /rearranged/restated wherever necessary for consistent presentation and comparison.

Interim Financial Report | Q3 FY 2020-21 11

H. Notes to the Interim Financial Statements 1. Basis of preparation

The consolidated financial statements of the Group have been prepared in accordance with Nepal Financial Reporting Standards 2013 (NFRS) developed by the Accounting Standards Board along with the carve outs, Nepal (ASBN) and pronounced for application by the Institute of Chartered Accountants of Nepal (ICAN) on September 13, 2013 along with the carve outs opted for by the Institute in NFRS implementation.

2. Statement of Compliance with NFRSs These financial statements comply with the requirements of the Nepal Financial Reporting Standards 2013 (NFRS), Companies Act, 2006 and amendments thereto and also provide appropriate disclosures required under regulations of the Securities Exchange Board of Nepal (SEBON).

Carve-outs in NFRS

The ICAN, on recommendation from ASBN, has issued following carve-outs in the implementation of NFRS at licensed banks and financial institutions and has also prescribed alternative treatments explained below:

a) NAS 39 – “Financial Instruments: Recognition and Measurements”

Carve out from the requirement to determine impairment loss on financial assets – loans and advances by adopting the ‘Incurred Loss Model’ as specified in para 63 of NAS 39 unless the reporting entity is a bank or a financial institution registered as per Bank and Financial Institutions Act 2073. Such entities shall measure impairment loss on loans and advances at the higher of: - amount derived as per norms prescribed by Nepal Rastra Bank for loan loss provisioning; and

- amount determined as per para 63 of NAS 39 adopting Incurred Loss Model The Group has adopted this mandatory treatment. As a result of this treatment, the Group has recognized impairment loss on loans and advances at the higher of the amount derived as per prudential norms specified in NRB directive no. 2/75 and the amount derived from incurred loss model as specified in para 63 of NAS 39. The Group has recognized impairment loss on other financial assets measured at amortized cost in accordance with para 63 of NAS 39.

b) NAS 39 – “Financial Instruments: Recognition and Measurements”

Carve out from the requirement to incorporate all fees and points paid or received under contractual terms of a financial instrument in the calculation of ‘Effective Interest Rate’ for the

Interim Financial Report | Q3 FY 2020-21 12

financial instrument as specified in para 9 of NAS 39 unless it is immaterial or impracticable to determine such fees and points reliably. The Group has adopted this alternative treatment. As a result of this alternative treatment, the Group has excluded the full amount of upfront loan management fees or commission received on loans and advances in the calculation of effective interest rate for the loan. The upfront fees and commission are recognized as income in the same period the loan is approved. The Group has assessed that this election is justifiable in line with the principal of cost and benefit of adopting certain provisions in NFRS.

c) NAS 39 – “Financial Instruments: Recognition and Measurements”

Carve out from the requirement to recognize interest income on a financial asset or a group of similar financial assets, which has been written down as a result of an impairment loss, by applying the rate of interest used to discount the asset’s future cash flows for the purpose of measuring its impairment loss as specified in para AG 93 of NAS 39. As a result of this alternative treatment, interest income on such impaired financial asset are allowed to be calculated by applying the original effective interest rate to the gross carrying amount of a financial asset unless the financial asset is written off either partially or fully. The Group has adopted this alternative treatment. As a result of this alternative treatment, the Group has recognized interest income on impaired financial asset by applying the original effective interest rate to the gross carrying amount of a financial asset unless the financial asset is a credit impaired financial asset. The Group has adopted this alternative treatment considering the practical difficulty in the application of para AG 93 of NAS 39.

3. Use of estimates, assumptions and judgments

Preparation of financial statements in conformity with NFRS required the Group’s management to make critical judgments, estimates and assumptions such that could potentially have a material impact on the reported financial figures. These affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. On an ongoing basis the management reviews these estimates and underlying assumptions to ensure that they continue to be relevant and reasonable. Revisions to accounting estimates are recognized prospectively. The most significant areas of assumptions and estimation applied in the application of accounting policies that have the most significant effect on the amounts recognized in the financial statements are listed hereinafter and their description follows: - Fair value of financial instruments - Classification of financial assets and financial liabilities - Impairment losses on financial assets

Interim Financial Report | Q3 FY 2020-21 13

- Impairment losses on non-financial assets - Useful economic life of property and equipment - Taxation and deferred tax - Defined benefit obligations - Provisions for liabilities, commitments and contingencies

4. Changes in accounting policies The Group has consistently applied the accounting policies for all periods reported in the financial statements. There were no changes in accounting policy in the reporting period.

5. Significant accounting policies The Group has applied the accounting policies set out below consistently to all periods presented in the accompanying financial statements unless specifically stated otherwise. i. Basis of measurement Financial Statements of the Group have been prepared on historical cost convention, except for the following: - Other Trading Assets (investment in mutual funds) and Investment Securities (investment in equity instruments) are measured at fair value under NFRS 9 ‘Financial Instrument’. - Investment Property (land and building acquired as non-banking assets) are measured at fair value under NAS 40 ‘Investment Property’. - Liabilities for employee defined benefit obligations and liabilities for long service leave are measured at fair value under NAS 19 ‘Employee Benefits’.

ii. Basis of consolidation The Group’s financial statements comprise consolidation of the financial statements of the Bank and those of the following entities:

a. The Subsidiary, in accordance with NFRS 10 – “Consolidated Financial Statements” inclusive of the alternative treatment prescribed on carve-out in NFRS; and

b. The proportionate share of the profit or loss and net assets of the Associate Company in accordance with NAS – 28 “Investments in Associates and Joint Ventures” inclusive of the alternative treatment prescribed on carve-out in NFRS.

iii. Investment in subsidiary The Group has recognized Nabil Investment Banking Ltd. as a Subsidiary company in which the Bank held 52% controlling interest at the report date. There has been no change in the Bank’s holding in the Subsidiary for the reporting period and the previous comparative period.

Interim Financial Report | Q3 FY 2020-21 14

iv. Investment in Associate The Group has recognized NADEP Laghubitta Bittiya Sanstha Ltd. as an Associate company in which the Bank held 25% equity interest at the report date. There has been no change in the Bank’s holding in the Associate for the reporting period and the previous comparative period.

v. Cash and cash equivalents Cash and cash equivalent comprise of the total amount of cash-in-hand, balances with other bank and financial institutions, money at call and short notice, and highly liquid financial assets with original maturities of three months or less from the acquisition date that are subject to an insignificant risk of changes in their fair value, and are used by the licensed institution in the management of its short term commitments. Restricted deposits are not included in cash and cash equivalents. These are measured at amortized cost and presented as a line item on the face of consolidated Statement of Financial Position (SoFP). vi. Financial assets and financial liabilities Financial assets refer to assets that arise from contractual agreements on future cash flows or from owning equity instruments of another entity. Since financial assets derive their value from a contractual claim, these are nonphysical in form and are usually regarded as being more liquid than other tangible assets. Common examples of financial assets are cash, cash equivalents, bank balances, placements, investments in debt and equity instruments, derivative assets and loans and advances. Financial liabilities are obligations that arise from contractual agreements and that require settlement by way of delivering cash or another financial asset. Settlement could also require exchanging other financial assets or financial liabilities under potentially unfavorable conditions. Settlement may also be made by issuing own equity instruments. Common examples of financial liabilities are due to banks, derivative liabilities, deposit accounts, money market borrowings and debt capital instruments. The contractual agreements, generally referred to as financial instruments, are characterized by the existence of counterparties and the contract terms give rise to a financial asset to one counterparty and a corresponding financial liability or equity instrument to the other counterparty. The Group has applied NFRS 9 – “Financial Instruments” in the classification and measurement of its financial instruments. Para 5.2.2 of NFRS 9 prescribes the application of impairment requirements in paragraphs 58-65 and AG84-AG93 of NAS 39 to financial assets measured at amortized cost. Accordingly, the Group has applied para 63 of IAS 39 and measured impairment loss on financial assets measured at amortized cost following the incurred loss model. vii. Trading Assets Trading assets are those assets that are acquired principally for the purpose of selling in the near term, or held as part of a portfolio that is managed together for short-term profit. It includes non-derivative financial assets such as government bonds, NRB bonds, domestic corporate bonds, treasury bills, equities, etc. held primarily for trading purpose. If a trading asset is a debt instrument, it is subject to

Interim Financial Report | Q3 FY 2020-21 15

the same accounting policy applied to financial assets measured at amortized cost. If a trading asset is an equity instrument, it is subject to the same accounting policy applied to financial assets measured at FVTPL. viii. Derivative assets and derivative liabilities Derivative assets and derivative liabilities (derivatives) create rights and obligations that have the effect of transferring between the parties to the instrument one or more of the financial risks inherent in an underlying primary financial instrument. However, they generally do not result in a transfer of the underlying primary financial instrument on inception of the contract, nor does such a transfer necessarily take place on maturity of the contract.

The value of a derivative changes with the change in value of the underlying. Examples of derivative are forward, futures, options or swap contracts. The underlying could be specified interest rate, security price, commodity price, exchange rate, price index, etc.

Derivative financial instruments meet the definition of a financial instrument and are accounted for as derivative financial asset or derivative financial liability measured at FVTPL and corresponding fair value changes are recognized in profit or loss. The Group has not designated derivative as a hedging instrument in an eligible hedging relationship under NFRS 9 – “Financial Instrument” and has not applied hedge accounting, ix. Property and Equipment Property and equipment are tangible items that are held for and used in the provision of services, for rental to others, or for administrative purposes, and are expected to be used for more than one year period. The Group applies NAS 16 – “Property, Plant and Equipment” in the accounting of property and equipment. Property and equipment are recognized if it is probable that future economic benefits associated with the asset will flow to the Group and the cost of the asset can be reliably measured. An item of property and equipment that qualifies for recognition as an asset is initially measured at cost. Cost includes expenditure that is directly attributable to the acquisition of the asset and eligible subsequent expenditure. Subsequent expenditure is capitalized only when it is probable that the future economic benefits of the expenditure will flow to the Group. Ongoing repairs and maintenance are expensed off as incurred. The Group applies the cost model to all property and equipment and records these at cost of purchase together with any incidental expenses thereon, less accumulated depreciation and any accumulated impairment losses. Cost also includes the cost of replacing part of the equipment when the recognition criteria are met.

Interim Financial Report | Q3 FY 2020-21 16

The carrying amount of an item of property and equipment is derecognized upon disposal or when no future economic benefits are expected from its use. Any gain or loss arising on de-recognition of an asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is recognized in profit or loss in the year the asset is derecognized

x. Goodwill and intangible assets Goodwill that arises on the acquisition of Subsidiaries is initially measured at cost, being the excess of the aggregate of the consideration transferred and the amount recognized for non-controlling interests, and any previous interest held, over the net identifiable assets acquired and liabilities assumed. Subsequent to initial recognition, goodwill is measured at cost less accumulated impairment losses. For the purpose of impairment testing, goodwill acquired in a business combination is, from the acquisition date, allocated to each of the Group’s cash-generating units that are expected to benefit from the combination, irrespective of whether other assets or liabilities of the acquiree are assigned to those units. At the reporting date, the Group does not have intangible asset in the form of goodwill, arising on business combination. Intangible assets are identifiable non-monetary asset without physical substance, which are held for and used in the provision of services, for rental to others or for administrative purposes. The Group applies NAS 38 – “Intangible Assets” in accounting for its intangible assets. The Group recognizes an intangible asset when: - The cost of the asset can be measured reliably; - There is control over the asset as a result of past events (for example, purchase or self-creation); and - Future economic benefits (inflows of cash or other assets) are expected from the asset. Intangibles can be acquired by separate purchase; as part of a business combination; by a government grant; by exchange of assets; or by self-creation (internal generation). An intangible asset appearing in the Group’s books is computer software. xi. Investment Property Investment properties are land or building or both other than those classified as property and equipment under NAS 16 – “Property, Plant and Equipment”; and assets classified as non-current assets held for sale under NFRS 5 – “Non-Current Assets Held for Sale & Discontinued Operations”. The Group has recognized as investment property all land or land and building acquired by the Bank

Interim Financial Report | Q3 FY 2020-21 17

as non-banking assets in course of recovery of loans and advances to borrowers that have turned into chronic defaulters. Non-banking assets (only land and building) are initially recognized at cost. Subsequent to initial recognition the Group has chosen to apply the cost model allowed by NAS 40 – “Investment Property” and since it is not intended for owner-occupied use, a depreciation charge is not raised. xii. Income Tax Tax expense is the aggregate amount included in the determination of profit or loss for the period in respect of current and deferred taxes. The Group applies NAS 12 – “Income Taxes” for the accounting of Income Tax. Income tax expense is recognized in profit or loss, except to the extent it relates to items recognized directly in equity or directly in other comprehensive income. Tax expense relating to items recognized directly in other comprehensive income is recognized in the Statement of Other Comprehensive Income. xiii. Deposits, debt securities and subordinated liabilities

1. Deposits from customers and BFIs The Group presents deposit accounts held by customers and those held by BFIs in the Bank under respective line items in the face of the consolidated statement of financial position. These are classified as financial liabilities measured at amortized cost.

2. Debt securities issued

The Group presents debenture issued by the Bank under this line item. These are classified as financial liabilities measured at amortized cost.

3. Subordinated liabilities

These comprise of liabilities subordinated, at the event of winding up, to the claims of depositors, debt securities issued and other creditors. Items eligible for presentation under this line item include redeemable preference share, subordinated notes issued, borrowings etc. These are subject to the same accounting policies applied to financial liabilities measured at amortized cost. The Group does not have any subordinated liabilities at the reporting date.

xiv. Provisions The Group applies NAS 37 – “Provisions, Contingent Liabilities & Contingent Assets” in the accounting of provisions. xv. Revenue Recognition Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Group and the revenue can be measured reliably. The Group applies NAS 18 – “Revenue” in the accounting of revenue, unless otherwise stated.

Interim Financial Report | Q3 FY 2020-21 18

1. Interest income Interest income are recognized in profit or loss using the effective interest rate (EIR) method for all financial assets measured at amortized cost. Interest income is earned on bank balances, investments in money market and capital market instruments, loans and advances, etc.

2. Fees and commission income

The Group earns fee and commission income on providing a diverse range of services to its customers. Such income earned on services including account maintenance, remittance transactions, agency commissions, e-commerce transactions, letter of credits, bank guarantees, loan management, etc. are recognized as the related services are performed. Fee and commission earned for the provision of services over a period of time are accrued over that period.

3. Dividend income

Dividend income is recognized when the right to receive income is established, which is the ex-dividend date for quoted equity instruments and unit investments. In line with the requirements of the Income Tax Act 2002, dividends received from domestic companies are recognized as final withholding income, while those received in respect of unit investments in mutual funds and equity interest in foreign companies are recognized in gross amounts and respective withholding taxes are recognized as tax receivables.

4. Net trading income

Trading income comprises of gains or losses relating to financial assets and liabilities held in the Group’s trading books. The Group presents all accrued interest, dividend, unrealized fair value changes and disposal gains or losses in respect of trading assets and liabilities under this head. The Group also presents foreign exchange trading gains or losses arising on foreign exchange buy and sell transactions under trading income.

5. Other Operating Income

The Group presents income other than those presented under interest income, fees and commission income and trading income under this heading. Income recognized here includes items such as foreign exchange revaluation gain or loss; dividend on equity investments that are measured at FVTOCI; dividend from subsidiary and associates; gain or loss on disposal of property and equipment; gain and loss on disposal of investment property; and gain or loss on disposal of investment securities except for equity investments measured at FVTOCI.

Interim Financial Report | Q3 FY 2020-21 19

6. Foreign exchange revaluation gain / (loss)

Gains and losses arising from day-to-day revaluations of foreign currency denominated assets and liabilities, exclusively due to the effect of changes in foreign currency exchange rates, are recognized in profit or loss in the period in which they arise.

7. Gain / (loss) on disposal of property and equipment

Gain or loss on the disposal of property and equipment is determined on the difference between the asset’s carrying amount on disposal date and the disposal proceeds, net of any incremental disposal costs. This is recognized as an item of Other Operating Income in the year in which significant risks and rewards incidental to the asset’s ownership is transferred to the buyer.

xvi. Interest Expense Interest expense is recognized in profit or loss using the effective interest rate (EIR) method for all financial liabilities measured at amortized cost. Interest expense is borne on inter-bank borrowings, deposit from customers, debenture issued, refinance borrowing, etc. xvii. Employee Benefits Employee benefits are all forms of consideration given by an entity in exchange for service rendered by employees. The Group’s remuneration package includes both short term and long term benefits and comprise of items such as salary, allowances, paid leave, accumulated leave, gratuity, provident fund and annual statutory bonus. The Group applies NAS 19 – “Employee Benefits” in accounting of all employee benefits and recognizes the followings in its financial statements: - A liability when an employee has provided service in exchange for employee benefits to be paid in the future; and - An expense when the Group consumes the economic benefit arising from service provided by an employee in exchange for employee benefits. xviii. Leases The Group determines whether an arrangement is a lease (or it contains a lease) based on the substance of the arrangement. It requires that under a leasing agreement the lessor must convey to the lessee, in return for a payment or series of payments, the right to use an asset for an agreed period of time. The Bank has applied NAS 17 – “Leases” in the accounting for leases. The lease payments under the operating lease are recognized as an expense on a straight line basis over the lease term. In accordance with the standard, spreading the total lease payments under the operating Lease on straight line basis over the lease term is applied even if the payments are not made on such basis.

Interim Financial Report | Q3 FY 2020-21 20

xix. Foreign currency transaction, translation and balances All foreign currency transactions are translated into the functional currency, which is Nepalese Rupees, using the spot exchange rates prevailing at respective transaction dates. All foreign exchange gains and losses resulting from the settlement of such transactions are recognized in profit or loss. All monetary assets and liabilities denominated in foreign currencies are translated into the functional currency by applying the year end exchange rates, and the resulting foreign exchange gains and losses are recognized in profit or loss. All non-monetary assets and liabilities held at historical cost are translated at historical exchange rates (rate prevailing at transaction date), and those held at fair value are translated at year-end exchange rate. The resulting exchange gains and losses are recognized in profit or loss OR in other comprehensive income. When gain or loss on a non-monetary item is recognized in other comprehensive income, any exchange component of that gain or loss is also recognized in other comprehensive income. Similarly, when gain or loss on a non-monetary item is recognized in profit or loss, any exchange component of that gain or loss is also recognized in profit or loss. xx. Financial guarantee and loan commitment Financial guarantees are contracts that require the Group to make specified payments to reimburse the holder for a loss that it incurs because a specified debtor fails to make payment when it is due in accordance with the terms of a debt instrument. Loan commitments are firm commitments to provide credit under pre-specified terms and conditions. Liabilities arising from financial guarantees or commitments to provide a loan at a below-market interest rate are initially measured at fair value and the initial fair value is amortized over the life of the guarantee or the commitment. The liability is subsequently carried at the higher of this amortized amount and the present value of any expected payment to settle the liability when a payment under the contract has become probable. xxi. Share Capital and Reserves Ordinary shares in the Bank are recognized at the amount paid per ordinary share. Nabil Bank Ltd.’s shares are listed at Nepal Stock Exchange Ltd. The holders of ordinary shares are entitled to one vote per share at general meetings of the bank and are entitled to receive the annual dividend payments. The Bank does not have any other form of share capital (preference shares, convertible instruments, share based payments, etc.) apart from the ordinary shares. There are a number of statutory and non- statutory reserve headings maintained by the Group in order to comply with regulatory framework and other operational requirements. The various reserve headings are explained hereinafter:

1. General reserve

Interim Financial Report | Q3 FY 2020-21 21

This is a statutory reserve and is a compliance requirement of NRB directive no. 4/75 and stipulations of BAFIA. The Bank is required to appropriate a minimum 20% of current year’s net profit into this heading each year until it becomes double of paid up capital and then after a minimum 10% of profit each year. This reserve is not available for distribution to shareholders in any form and requires specific approval of the central bank for any transfers from this heading. The Bank has consistently appropriated the required amount from each year’s profit into this heading. There is no such statutory requirement for the Subsidiary.

2. Exchange equalization reserve

This is a statutory reserve and is a compliance requirement of NRB directive no. 4/75 and stipulations of BAFIA. The Bank is required to appropriate 25% of current year’s total revaluation gain (except gain from revaluation of Indian Currency) into this heading. The Bank has consistently appropriated the required amount from each year’s profit into this heading. There is no such statutory requirement for the Subsidiary.

3. Fair value reserve

This is a non-statutory reserve and is a requirement in the application of accounting policy for financial assets. NFRS 9 requires that cumulative net change in the fair value of financial assets measured at FVTOCI is recognized under fair value reserve heading until the fair valued asset is de-recognized. Any realized fair value changes upon disposal of the re-valued asset is reclassified from this reserve heading to retained earnings. The Group has complied with this accounting policy application.

4. Asset revaluation reserve

This is a non-statutory reserve and is a requirement in the application of accounting policy for non-financial assets such as property, equipment, investment property and intangible assets that are measured following a re-valuation model. Revaluation reserves often serve as a cushion against unexpected losses but may not be fully available to absorb unexpected losses due to the subsequent deterioration in market values and tax consequences of revaluation. The Group does not have any amount to present under asset revaluation reserve.

5. Capital reserve

This is a non-statutory reserve and represents the amount of all capital nature reserves such as the amounts arising from share forfeiture, capital grants and capital reserve arising out of business combinations. Funds in this reserve are not available for distribution of cash dividend but can be capitalized by issuing bonus shares upon obtaining prior approval from the central bank. The Group does not have any amount to present under asset revaluation reserve.

Interim Financial Report | Q3 FY 2020-21 22

6. Special reserve

This is a statutory reserve and is a compliance requirement of NRB circular 12/072/73. The Bank is required to appropriate an amount equivalent to 100% of capitalized portion of interest income on borrowing accounts where credit facility was rescheduled or restructured, following the after effects of the great earthquake that struck the nation in April 2015. Fund in this account can be reclassified to retained earnings upon full and final repayment of the credit facility. There is no such statutory requirement for the Subsidiary. 7. Capital redemption reserve

This is a non-statutory reserve created for making payment towards redeemable non-convertible preference shares. The Group does not have any amount to present under asset revaluation reserve.

8. Dividend equalization fund

This is a non-statutory reserve created for supporting the dividend payout policy by appropriating amounts from current year’s profit to fund for future period’s payout. Fund in this heading is available for distribution to shareholders upon approval of the board of directors and endorsement of the share holders’ general meeting. The Group does not have any amount to present under asset revaluation reserve.

9. Capital adjustment / equalization fund

This is a non-statutory reserve created by appropriating amounts from current year’s profit and by crediting amounts for calls is advance towards raising capital. The Group does not have any amount to present under asset revaluation reserve.

10. Corporate social responsibility fund

This is a statutory reserve and is a compliance requirement of NRB circular 11/073/74. The Bank is required to appropriate an amount equivalent to 1% of net profit into this fund annually. The fund is created towards funding the Bank’s corporate social responsibility expenditure during the subsequent year. There is no such statutory requirement for the Subsidiary.

11. Investment adjustment reserve

This is a statutory reserve heading and is a compliance requirement of NRB directive no. 4/075 and 8/075. The Bank is required to maintain balance in this reserve heading which is calculated at fixed percentages of the cost of equity investments that are not held for trading. Changes in this reserve requirement are reclassified to retained earnings. The Bank has consistently appropriated the required amount from each year’s profit into this heading. There is no such statutory requirement for the Subsidiary.

Interim Financial Report | Q3 FY 2020-21 23

12. Actuarial gain / loss reserve

This is a non-statutory reserve and is a requirement in the application of accounting policy for employee benefits. NAS 19 requires that actuarial gain or loss resultant of the change in actuarial assumptions used to value defined benefit obligations be presented under this reserve heading. Any change in this reserve heading is recognized through other comprehensive income and is not an appropriation of net profit. The Group has complied with this accounting policy application.

13. Regulatory reserve

This is a statutory reserve and is a requirement in the application of accounting policy as prescribed in NRB directive no. 4/075. In the transition to NFRS from previous GAAP the Bank is required to reclassify all amounts that are resultant of re-measurement adjustments and that are recognized in retained earnings into this reserve heading. The amount reclassified to this reserve includes re-measurement adjustments such as interest income recognized against interest receivables, difference in loan loss provision as per NRB directive and impairment on loan and advance as per NFRS, amount equals to deferred tax assets, actual loss recognized in other comprehensive income, amount of goodwill recognized under NFRS, etc. Balance in this reserve is not regarded as free for distribution of dividend. The Bank has complied with this regulatory requirement. There is no such statutory requirement for the Subsidiary.

14. Other reserve fund

Contingent reserve This is a non-statutory reserve and is created by the Bank towards meeting operational requirements. A fixed amount is annually appropriated from net profit into this fund. Balance in this fund is utilized towards providing financial support to employees for treatment of severe cases of life threatening ailments that are not adequately covered under medical insurance policy. Amount paid to staff from this fund is re-classified to retained earnings and is recognized as personnel expense in profit or loss. No such reserve is maintained by the Subsidiary. Debenture Redemption Reserve This is a statutory reserve and is a compliance requirement of NRB directive no.16/075. The Bank is required to maintain a redemption reserve in respect of borrowing raised through debenture issuance. As per the terms of NRB approval relating to the Bank’s debenture issuance, the Bank is annually required to transfer 20% of the debenture’s face value to redemption reserve, starting from the 6th year of the issue. The Subsidiary has not raised any borrowing through debenture issuance.

Interim Financial Report | Q3 FY 2020-21 24

Employees training and capacity development fund

This is a statutory reserve and is a compliance requirement of NRB circular 6/075. The Bank is required to incur expenses towards employee training and development for an amount that is equivalent to at least 3% of the preceding year’s total personnel expenses. Any shortfall amount in meeting this mandatory expense requirement in the current year will have to be transferred to this reserve fund through appropriation of net profit and the amount shall accumulate in the fund available for related expenses in the subsequent year. Balance in this fund is directly reclassified to retained earnings in the subsequent year to the extent of expenses made for employees training related activities.

xxii. Earnings per Share The Group calculates basic and diluted Earnings per Share (EPS) data for its ordinary shares as required under Nepal Accounting Standards – NAS 33 on “Earnings per Share”. Basic EPS is calculated by dividing the profit or loss that is attributable to ordinary shareholders of the Bank by the weighted average number of ordinary shares outstanding during the reported period. Diluted EPS is calculated by adjusting the profit or loss that is attributable to the ordinary shareholders of the Bank and the weighted average number of ordinary shares outstanding adjusted for the effects of all dilutive potential ordinary shares, such as share options granted to employees and hybrid capital instruments. The Group does not hold any dilutive potential ordinary shares, and as such the Basic EPS is also the Diluted EPS of the Group. xxiii. Segment Reporting The Group has disclosed information on operating segments to enable users of financial statements to evaluate the nature and financial effects of the Group’s business activities and that of the economic environment in which the Group operates. xxiv. Statement of Cash Flows The Group has reported its cash flow statement applying the ‘Direct Method’ in accordance with NAS 07 – “Statement of Cash Flows”. Application of the direct method in presenting cash flow statement discloses major classes of gross cash receipts and gross cash payments, thereby provides information which may be useful in estimating future cash flows of an entity.

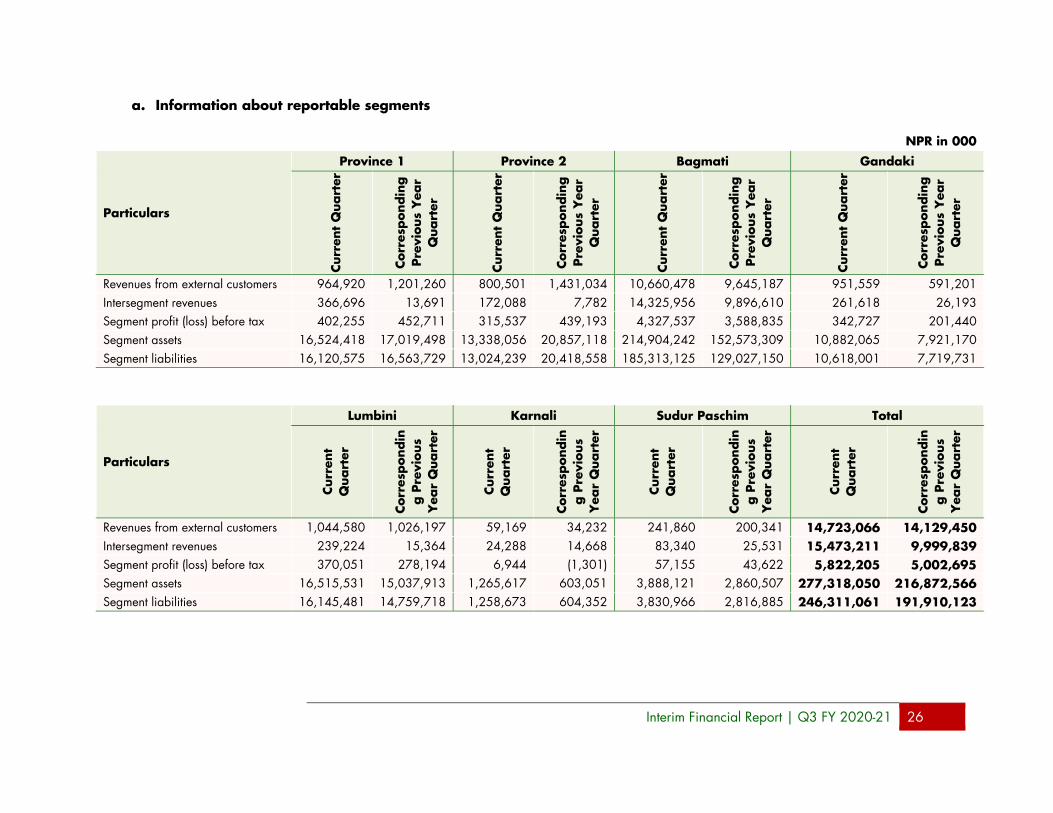

6. Segmental Information The Bank has adopted “Management Approach” for identifying the operating segments i.e. seven segments based on the geographic locations of its offices in the 7 provinces of the country. Interest earnings and foreign exchange gains/losses generated while conducting businesses under different segments are reported under the respective segment. Shareholder's Equity in Segment Liabilities and Tax Expense in Segment profit/ (loss) are not allocated to the individual segments. For segmentation purpose, all business transactions of offices and business units located in a particular province are

Interim Financial Report | Q3 FY 2020-21 25

grouped together. All transactions between the units are conducted on arm's length basis, with intra unit revenue and cost being nullified at the bank level.

Interim Financial Report | Q3 FY 2020-21 26

a. Information about reportable segments NPR in 000

Particulars

Province 1 Province 2 Bagmati Gandaki

Curr

ent

Quart

er

Corr

espondin

g

Pre

vious

Yea

r Q

uart

er

Curr

ent

Quart

er

Corr

espondin

g

Pre

vious

Yea

r Q

uart

er

Curr

ent

Quart

er

Corr

espondin

g

Pre

vious

Yea

r Q

uart

er

Curr

ent

Quart

er

Corr

espondin

g

Pre

vious

Yea

r Q

uart

er

Revenues from external customers 964,920 1,201,260 800,501 1,431,034 10,660,478 9,645,187 951,559 591,201 Intersegment revenues 366,696 13,691 172,088 7,782 14,325,956 9,896,610 261,618 26,193 Segment profit (loss) before tax 402,255 452,711 315,537 439,193 4,327,537 3,588,835 342,727 201,440 Segment assets 16,524,418 17,019,498 13,338,056 20,857,118 214,904,242 152,573,309 10,882,065 7,921,170 Segment liabilities 16,120,575 16,563,729 13,024,239 20,418,558 185,313,125 129,027,150 10,618,001 7,719,731

Particulars

Lumbini Karnali Sudur Paschim Total

Curr

ent

Quart

er

Corr

espondin

g P

revi

ous

Yea

r Q

uart

er

Curr

ent

Quart

er

Corr

espondin

g P

revi

ous

Yea

r Q

uart

er

Curr

ent

Quart

er

Corr

espondin

g P

revi

ous

Yea

r Q

uart

er

Curr

ent

Quart

er

Corr

espondin

g P

revi

ous

Yea

r Q

uart

er

Revenues from external customers 1,044,580 1,026,197 59,169 34,232 241,860 200,341 14,723,066 14,129,450 Intersegment revenues 239,224 15,364 24,288 14,668 83,340 25,531 15,473,211 9,999,839 Segment profit (loss) before tax 370,051 278,194 6,944 (1,301) 57,155 43,622 5,822,205 5,002,695 Segment assets 16,515,531 15,037,913 1,265,617 603,051 3,888,121 2,860,507 277,318,050 216,872,566 Segment liabilities 16,145,481 14,759,718 1,258,673 604,352 3,830,966 2,816,885 246,311,061 191,910,123

Interim Financial Report | Q3 FY 2020-21 27

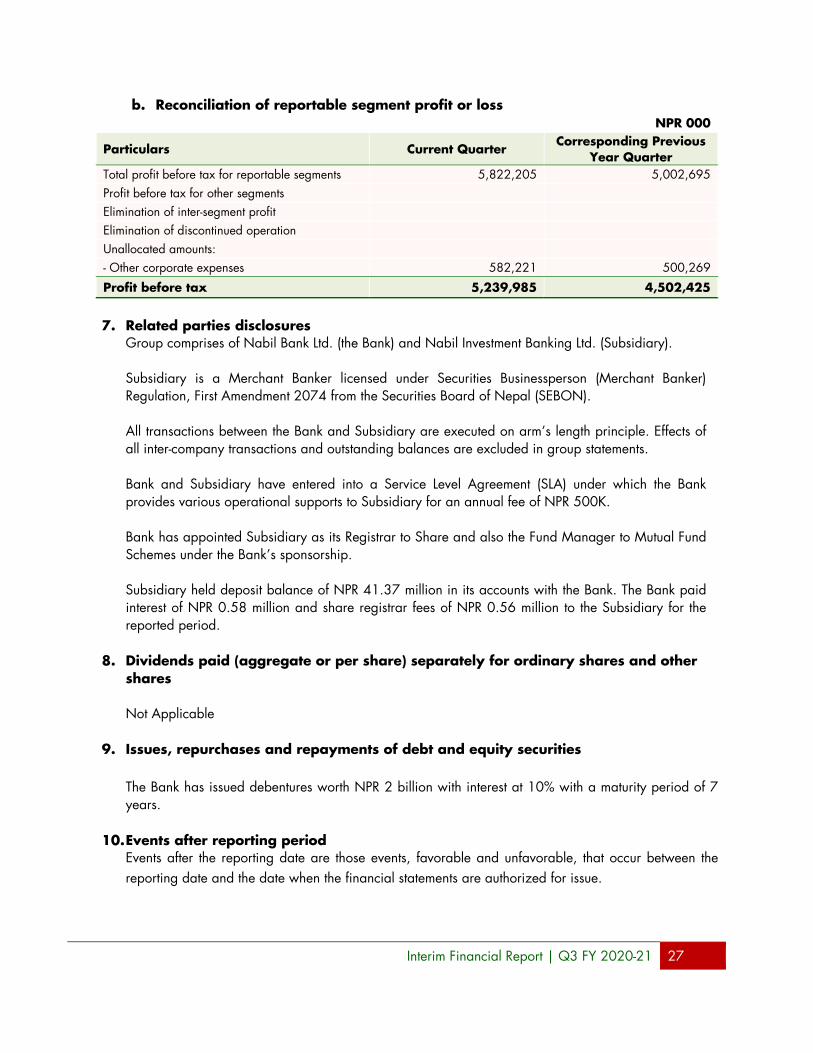

b. Reconciliation of reportable segment profit or loss NPR 000

Particulars Current Quarter Corresponding Previous

Year Quarter Total profit before tax for reportable segments 5,822,205 5,002,695 Profit before tax for other segments

Elimination of inter-segment profit

Elimination of discontinued operation

Unallocated amounts:

- Other corporate expenses 582,221 500,269

Profit before tax 5,239,985 4,502,425

7. Related parties disclosures

Group comprises of Nabil Bank Ltd. (the Bank) and Nabil Investment Banking Ltd. (Subsidiary). Subsidiary is a Merchant Banker licensed under Securities Businessperson (Merchant Banker) Regulation, First Amendment 2074 from the Securities Board of Nepal (SEBON). All transactions between the Bank and Subsidiary are executed on arm’s length principle. Effects of all inter-company transactions and outstanding balances are excluded in group statements. Bank and Subsidiary have entered into a Service Level Agreement (SLA) under which the Bank provides various operational supports to Subsidiary for an annual fee of NPR 500K. Bank has appointed Subsidiary as its Registrar to Share and also the Fund Manager to Mutual Fund Schemes under the Bank’s sponsorship. Subsidiary held deposit balance of NPR 41.37 million in its accounts with the Bank. The Bank paid interest of NPR 0.58 million and share registrar fees of NPR 0.56 million to the Subsidiary for the reported period.

8. Dividends paid (aggregate or per share) separately for ordinary shares and other shares Not Applicable

9. Issues, repurchases and repayments of debt and equity securities

The Bank has issued debentures worth NPR 2 billion with interest at 10% with a maturity period of 7 years.

10. Events after reporting period

Events after the reporting date are those events, favorable and unfavorable, that occur between the reporting date and the date when the financial statements are authorized for issue.

Interim Financial Report | Q3 FY 2020-21 28

There are no material events after reporting period affecting financial status of the bank as on Chaitra end 2077.

11. Effect of changes in the composition of the entity during the interim period including merger and acquisition

There are no merger and acquisition affecting changes in the composition of the entity during the interim period as on Chaitra end 2077.

I. Management Analysis Management is adamant on portfolio diversification, sustainable growth of high quality assets,

achieving effective recovery, effective resource management and enhancing management and workplace efficiency.

The Bank is persistently working on upgrading IT infrastructure, automating work processes, embracing digitization, enhancing transaction security and improving internal control systems and risk management practices.

There are no such incidents during the period which might have negative impact on the reserve, profit or cash flow position of the Bank.

J. Details Related to Legal Proceedings

Except in the regular course of business, there are no law-suits of material nature filed by or filed against the Bank/promoters/directors on account of violation of prevailing laws or commission of criminal offences or financial crime.

K. Analysis of Bank's shares transactions The market price of the Bank’s share is fully dependent on market movements and the Bank does not

comment on its share transactions. The Bank has complied with the prevailing disclosure norms and regulatory directives issued by

Securities Board of Nepal (SEBON) and Nepal Rastra Bank (NRB). Details of share transactions during the quarter:

Ordinary Shares

Maximum Price NPR 1,435 Minimum Price NPR 1,065 Closing Price NPR 1,380 Total Units Traded 8,641,643

Total Days Traded 59

L. Problems and Challenges Internal: - Challenge of normal operation of the organisation in light of the current pandemic whilst ensuring the safety and security of the human resource pool.

- Challenge of coming up with new products/services which can be provided in the new normal and exploring alternate channels of delivery.

Interim Financial Report | Q3 FY 2020-21 29

External: - The hit taken by the global economy is bound to impact the bank as well. - Managing the impact on revenue generation while honouring our commitments in this pandemic scenario. - Managing the impact of fluctuating interest rates. - Possible impact of frugal spending by all stakeholders of the economy. Bank's strategy to mitigate problems and challenges: - Focused approach in operation with minimum possible resources without compromising on the quality of service delivery while striving for organic growth.

- Prudent management of assets and liabilities. - Effective management of cost through improved productivity and efficiency. - Exploration of alternate business avenues and channels for maintaining the contribution from non-interest income.

- Embracing digitization for remarkable improvement in product offerings and service delivery. - Enhancing skill sets of staff for upgrading our service standard.

M. Corporate Governance The Bank has a separate Governance Unit in place for continuous monitoring of governance issues within the Bank. The Board of Directors, Audit Committee and Senior Management are committed to upholding good corporate governance practices in the Bank. The Bank’s organization structure, internal control system and management practices are designed keeping best corporate governance practices in mind.

N. Declaration by Chairman/ CEO about the truthfulness of financials/ information I, CEO of the Bank, take responsibility on the truthfulness of the information and particulars disclosed in this report to the best of my knowledge. Further, I declare that the particulars mentioned in this report, to the best of my knowledge, are true, fair and complete at the time of publication of this report and have not knowingly concealed any material particulars and information for investors to take informed decisions.

Related Documents