Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Dear Reader

Until fairly recently, mostintergovernmental attention wmfacused on federal grants. Now,the federalism debati is shiftingto the revenue side of the equa-tion,

Changes in federal tax pelicyforeshadowed this shifi. The Eco-nomic Recovery Tax Act of 1981may ba viewed as the beginningof a new chapter in faderal.state.lacal relations. The most signif-icant change in inter-governmental te~s in the 1981legislation was the AcceleratedCost Recovery Systam deprecia-tion methad. Because many statasused the federal cade h determinedepreciation, the new ACSSmeant the loss of millions of dol-lars from state treasuries. Notsu~risingly, many statee decou.pled from the federal depreciationsystem ti avoid this loss and,more fundamentally, state leadershad god reaaon w Iaek at themerits of close conformity to fed-eral tax rules.

The federal government alsoraised certain excise taxes. In1982, for the first time in 20years, the federal cigarette excisetax and the federal excise tax rateon gasoline were at least doubled.

2 With the long federal status quo,

many sta~s had come to view ex-cise taxes as “their” revenuesources and would increase theeetaxes to make up for small short-falls in their budgets. It should benoted that this federal action didnot result in states avoiding thesetaxes. In fact, several states, in.eluding my own, have raised their@bacco or gasoline taxes, or both,since Congress imposed thesehigher rates in 1982,

Other legislation under currentconsideration would raise the ex-cise tax on alcoholic beveragesand would make part of the tem-parary cigarette tax increasepermanent, Another threat tostute-lacal uae of selective taxescomes from the Adviaery Councilon Social Sacurity which wants beamark revenues from excisetaxes to cover the anticipatedMedicare deficit. The debate overcurbing industrial revenue bon&is the latest example of the im-portance of tax policy to stabsand localities.

At the Commimion’s Springmeeting, these and other proposedfederal tax changes were mea-sured for their intergovernmentaleffecb. ACIR came out strongly infavor of protecting the basic ten-ets of fiscal federalism and theabilities of states and localities braise revenues h finance the lev-els of services they find desirable.

This issue of Inter.governmental Perspective dealswith tax intemelationahips. Thefirst article discusses the potentialimpact on stabs and localities ofproposed changes in federal taxplicy. me second highlightwhat local govemmenta are doing

b make ends meet in the 1980s.The third compares our system offiscal federalism tIJWest Ger-many’s, Unlike West Germanywhere the national governmentraises and redistributes revenues,several levels of taxing authoritycompete for resources within theframework of American federal-ism. The challenge of the remain-der of this decade may well bereconciling the many conflictinginterests that can ariae when fed-eral, stak, and local governmentsvie for the same tax dollars.

David E. NethingMajority kader

North Dakota Stati Senate

ln~mental spring 1984, Vol. 10, No. 2

staffExecutive Director:S. Kenneth Il,,w:,rd

Assistant Directors:.J(,h,, Shan,,(]r,I)uvid K W;,lk<r

Editor:Stvph:~nie J, fi?cker

Contributors:K>,rc.r,I<enk<.rI)<,r,,thy r)ickt:rs<,!,(y.thit, (.;c>l<!ll~t,J,!rry F,,nst’!,m;lnI)c,phne Keny{,n[>,,tKoch[<,”,? Mc[)owcllMt,rk Mc.r)chik

8 Juggling Intergovernmental Revenue Cf>ncernsA(; llt Sc:rlior Analyst Robc,rt Kleine ex:{mirles the int(:rg{]tt.rnmcntaldimcr~si[>rls of”pr(]pc).c.d ch;lr]~t;s in I’t.rlc,r:ll t:,x pt)licy. I [is ;Irticlc, ist)iised or> th(, recent w~,rk of the (~orr>rnissic)”’s T:,x;tti<)n ;,”d FinanceSc,ctit)n.

18 Local Finance A Rootstraps operationCity and county efforts to diversify their revenue systc?ms haveundergone several r:~ther dr:lmatic ch:{nges in rcccnt years. ACIRInfi)rn];ition Off[cer Steph:illit. Ftcckcr provides :sn overview of sonle ofthest: ch:]n~es.

25 Similarities and Differences: Federalism in West Germany andthe United St;itesK(’,,nc:th Ht)wKrd, A(!IRs Exc:cutive [)ir(.c(or, c{,mp:,res a“d c{]”trastsfederalism in tht? LJnitcd States and West (lcrm:iny,

32 A Fiscal NoteComparative L:ix burdc>ns among m:ijc)r LJ.S. cities ar<: presented byMichiiel [,awson, an A(; IR An:~lyst.

34 The+ Chairm:ln’s ViewA(;llt Ch:,irnliirl R,)hert 13. Ili,wkirls Rivf!s his vit.ws on the cht~]lgingst.rv ice delivery p>ltterns ;Ippc:: iring ;It [dl levels of govc:rr]n)e”t.

35 ACIR News

A(;IR Adopts Inter#overnment:il Ttix Policy, Tt]kes St:lnd onMunicip:]l AntitrustSenior An:ilyst Bearr) l,e:,ves (~<>mmissio”

Regional Councils Changing,Survey Finda

Results of a 1983 survey of substateregional councils have recently beenm:ide avaikible by the National Asso-ciation of Regi,>nal Councils (SpecialReport No. 91, January 1984, NARC,1700 K Street, N. W., Washington, DC20006). The two principal findings arethat (1) regional council activities andfunding sources have diversifiedWeatly, and (2) federal funding h:isreceded substantially—from 76% ofthe typical council budget in 1977 (asreported by the Census of Govern-ments) to 48<2 in 19S3 Another sig-nificant fact that enlerged is that overhalf (56[1 I of these regional organiza-tions have some in-house computercapability—a completely new de-velopment for many,

Over the past decade, land-useplanning and environmental pro-tection concerns have remained onthe agendas of most regional organi-zations. During the same period, :ic-tivities in tbe fields of economic de-velopment, transportation, housing,human services, management and as-sistance, and computer services havebecome much more frequently in-cluded on these agendas. Each of theactivities mentioned above was re-ported in the work programs of wellover half of the 335 substate regionalcouncils responding to NARC’S 1963survey.

Revenue diversification by regi<>walcouncils has taken several forms,States, local government, and “other>’sources of funding all support largerproportions <>fregional budgets, nowthat federal funds have been cutback. State funding in 1983 accountedfor 17 percent of regional councilbudgets, compared to 10 percent in1977, while the local share of thesebudgets rose from 12 tc] 19 percent. Inboth cases, contract services became amuch more prominent part of thisfunding, in comparison to grants forgeneral support of the regional orga-nizations, Funds from other sourceshave risen from 2 to 16 percent. Theyare provided hy “other” service con-tracts (6%), regional taxes (39), foun.dation grants (1<%),and miscellaneous

4 sources (60/:).

In-nmenblw

The new rtdes of service contractsmay be the most significant feature ofthis fiscal reali~ment. Combiningthe state, local government, and otherservice contracts, 23 percent of re-gional cc>uncil budgets now come fromsuch c<,ntracts—a tig”re roughlyequivalent to the 28 percent reducti(]nin the federally-s{lpplied portion ofthe budget. Most regi<>nal c(>uncilbudgets are not only substantiallysmaller, but the flexibility to spend inaccordance with the council’s own re-@onal priorities has also been re-duced. In fact, the new service con-tracts often provide a council withless flexibility than the federal wantsthey replaced, and they are less sup-portive of br[)adly-conceived platlningactivities.

Intergovernmental RegulatoryRelief Act Introduced

On March 8, 1984, Senator I)avidDurenberger (MN), Chairman of theSenate Intergovernmental RelationsSubconlm ittee, introd”ced the Inter.governmental Regulatory Relief Actof 1984. The bill will relieve state andlocal gove:rnmerlts frotn costs theymay incur when conlplying with fed-eral reg”lationg

. by reimbursing state and localgovernments for direct costs theyincur in complying with new reg-ulations,

. by requiring a rflduction in ex-isting costs eitb~:r by reim-bursement, by reducing the reg-ulatory require n]ents themselves,or by a combination of the two.

If such relief is not provided for, thebill prohibits any federal agency orcourtfr<pm en forcingthe unre-imbursed re~lat<)n.

The bill also requires the Presidentto prepare anannua] report esti-mating totid costs irtcurrc;d by state:ind local governmetlts in complyingwith federal regulations.

Senator Durenberger said that thebasic premise behind the bill is that ifCongress passes legislation to pursuea national purpose, the federal gov.ernment, not the states or cities,should pay the costs of achieving it:

It’s time to put an end to our “n.savory practice of shifting cost onto

state and local governments. If wewant the cr[,dit f<,r s<,lving socialproblems, wc (Congress) must stateour objectives clearly and voteopenly to spend scarce Federal dol-lars to pay for the solution.In its rt?cently published study on

reKulat,jry federalism, the AdvisoryCommission on IntergovernmentalRelatio,~s (ACIR) has identified m{,rethan 35 majorfederal regulatorystiatutes employing interg[]vernment>slreg”latio”s that place significant f~s-cal burdens on state and local gov-ernments.

Over the years, Congress haspassed Legislation to achieve a wh(deo,nge <Ifs<]cial and econo~]ic gcyals. Inimplementing these programs. a si~nificant share of the cost has beenshifted onto .t>~te :ind local govern-ments. This cost shifting ,)ccursthrough various forms of federal r“letiand regulations and their interpreta-tionby the courts. For example:

Direct orders, which mandatestate and local actions underthreat of civil c>rcrimi”al penal-ties,, such as the Equal Employ-ment Opportunity Act of 1972;Crosscutting, or generally appli-cable requirements imposed onmany or all assistance programsmantst[> furthera wide range ofsocial and economic policies.These requirements, includingbans on discrimination on the~~<>t]nds(>fr:~ce, S(?Xand handi-capped; environtnent impactsttiteme]]t procedures; and l.)avis -B;icon Act prev:liling wage rules,must be adhered to by recipientsof fc:deral assistance or the aidcan be suspended. In a recentOb’tB inventory, :36 across-the-board requirements dealing withvarious socioeconomic issues, aswell as 2:3 administrative and fis-c:d p(dicy requirements, wereidentified;Crossover sanctions, in whichthe failure to comply with the rc.quirements ofone program mayresult in the reduction c]r elimina-tion of aid funds provided underothc:r specified programa, asexemplified by the requirementthat states having speed limits inexcc,ssof 55 MPH “c>t receive fed.

eral funds for highway construc-tion or under the National HealthPlanning Act; and,

. Partial preemptions, which es-tablish a national federal stan-dard, but authorize states to im-plement the program if theyadopt standards at least as strin.gent as the federal ones, as pro-vided by the environmental pro-tection and OSHA laws. In eitherinstance, states bear much of thecost of implementing the federalor greater standard.

Senator Durenberger stated thatthe Intergovernmental RegulatoryRelief Act of 1984 is based on thetindings and recommendation of theACIR.

Furthermore, Senator Durenbergerstated his intention to introduce twoadditional bills aimed at federalismreform. One will address the technicalquestions of writing and managingfederal regulations directed at stateand local governments. The other willgo to more fundamental questions ofstate-federal relations in the areas offederal preemption of state laws anddirect federal orders that come in theform of both legislation and court de-cisions.

The Subcommittee plans to holdhearing this spring on the inter-governmental Regulatory Relief Actof 1984.

The Supreme Courl So Far. . .

Although a few cases of extremeintergovernmental significance re-mainto be decided—thus preventinga final assessment of the 1983-84 Su-preme Court Term+nce again, as inprevious years, the Burger Court hasexhihited no clear voting hlocs norany consistent view ofjudical federal.ism. Hence, the states prevailed inimportant grant law, EleventhAmendment, and antitrust cases, butcame out badly on the losing side ofthe judicial ledger in the alwaystension-filled realm of preemption.

At issue in the major Want lawcase of the Term, Norfolk Redeuelop-

mentand Housing Authority u. Che8-apeake and Potomac Telephone Co. ofVirginia, was tbe Uniform MlocationAssistance and Real Property Acquisi-tions Act of 1970. The Act applies tomost diaplacement8 caused by gov.ernment programn using federalfunds other than General @venueSharing. The case in question arosewhen Chesapeake and Potomac Tele-phone requeeted relocation a~sistanceafter it waa required to move Borne ofits tranBmiaaion facilities from a pub-lic right-of-way as part of a Norfolkurban renewal project, Althoughbusinesses as well as people may beconsidered “displacedpersons” for thepurposes of the Act, public utilitiesare a unique category of bu0ine8s,presenting government with specialproblems. For example, a long-establiahed principle of common lawholds “that a utility forced to relocatefrom a public right-of-way must do soat its own expense. ” Thus, amici join.ing the Norfolk Authority asked theCourt ti decide that “[a]bsent a clearcongressional statement that publicutilities should be compensated underthe statute, the courts should be re-luctant to interpret the law in such away as to obviate decades of Statecommon law. .“TheCourta greedand state and local governmentschalkeduD their tirst major victory ofthe Term.’

The states achieved another impor-tantwin when, earlyin 1984, an~r-rowly divided Court greatly expandedthe Eleventh Amendment, the con-stitutional provision which givesstates immunity from being sued infederal court without their consent. Inthe now familiar case of PennhurstState School and Hospital u. Hal-derman (the case yielded an impor-tant grant law decision in 19814eeIntergovernrnental Perspective,Fall 1981) a 5-4 majority ruled thatfederal judges cannot order “state of-ficials to conform their conduct tostate law.’’ The decision is perhapsthe most far-reaching to date in aseries of Burger Couti actions de-signed ticurbth epowerofthe fed-eraljudiciaw—most notably, in therealm of habeas corpus petitions. Thenewest Pennhurst decision may pre-vent federal judges from questioning

state officials on their Wlicies con-ceming state in8titution0, such a~priuons and mental facilities, gov-ernedby stata laws.

Stati interests were also victoriousthis Term in the still evolving and asyet legally murky area of official lia-bility under the federal antitrustlawn, In Hoover u. Ronwin, the Courtheld that state bar officials cannot besued under the antitrust laws bypeo-ple denied admis6ion to a stab’s bar.Arguing that Arizona bar officials, byallowing only a set number h passthe bar exam rather than all thosenurpasninga net standard, knwinsued the bar and itsofflcials chargingareatriction of competition. By a 4-3plurality, the Court ruled that barexamineru are an arm of the stab 8u-preme court and thus are covered bythe ~tati’s broad immunity from theantitrust laws. Lackinga majority,the precedential value of the decisionmaybe limited. However, it shouldserve 8B unimportant guidepost inthe continued development of theCourt’s thinking in this area.

The states found themselves in aless auspicious legal milieu whenquestions of federal preemption wereat issue. Thus, in Secretary of Inte -rioru. California—a caee pitting Rea-gan Administration interests againstthose of the state+a badly dividedCourt ruled that states may not ob-struct federal offshore lease sales onthe basis that such transactions areinconsistent with state coastal pro-tection plans

States suffered another preemptionsetback when the Court, in a one-eentence order, affirmed an appealscourt ruling on a Connecticut ban ofdouble trailer trucks. At issue was aprovision of the federal SurfaceTransptiation Assistance Act(STAA) disallowing states from pro.hibiting such vehicles. Connecticutargued that the law violated itsrights under the equal protectioncomponent of the Fifth Amendment’sDue Process Clause and the TenthAmendment. The High Court, how-ever, chose to give itablessing to thelower court’s assertion that “ln gen-eral, the power of Congres~ to pre-empt state legislation affecting inter-state commerce is sweeping. [Ilt is 5

6

likely that the Connecticut statute,even in the absence of any con.gressional preemption, might have anunconstitutional impact on interstatecommerce. ”

Far less controversial—though aloss nonetheless for one state—wisthe Court’s unanimous decision inAloha Airlines u. Director of Taxationof ffawaii. In that case, the Courtruled that Hawaii’s tax on the a“n”alWoss income of airlines operatingwithin that state is preempted by theAirport Development AccelerationAct of 1973. Section 1513(a) of thatAct expressly prohibits states fromtaxing “directly or indirectly” grossreceipti derived from air transDol’ta-tion. -

Despiti the foregoing losse~, thestates were judicially blest in onepreemption holding, In Silkwaod u.Kerr.McGee the Court was asked todecide whether federal law preemptsstate laws under which employees canobtain punitive damage awards fromtheir employers if the companies al-low their employees to become radio-actively contaminated. Fifteen st;itesjoined the Silkwood estate; the Rea-gan Administration supported theposition of Kerr-McGee. In contrast tothe California case, Administrati,)npolicy was rebuffed and the stateposition vindicated when a narrowlydivided Court found “ample evidence”for ruling that state negligence lawmay permit awarding punitive dam-ages.

Finally, of interest to city govern-ments attempting to deal with urbanand minority unemployment by usingset-asides, was the Court’s ruling inUnited Building and ConstructionTrade Council u. Mayor and Councilof the City of Camden. At issue was aCamden ordinance requiring that atleast 40% of the employees of con-tractors and suhcontractora workingon city construction projects be res-idents of Camden. The Building andTrade Council sought to have the lawdeclared unconstitutional asavio-lation of the Privileges and Immu-nities Clause, That constitutionalprovision seeks tn ensure that citizensfrom one state who visit a secondstate are treated in the same manneras the citizens of the second state.

The city ar~ed that municipal ordi-nances, unlike state laws, are notsubject tn the strictures of the Clause,Although the Court did not declarethe ordinance unconstitutional, it didreject Camden’s contention, remand-ing the case to the New Jersey Su-preme Court for determination of con-stitutionality. The result may thus beviewed as a mixed blessing, the cityhas been lefi open to constitutionalattack, but the state has been givenfinal legal say.

1984 State Tax Changes

This year, states with tax changescan be divided into two categories:those statea that are still dealingwith recession-induced problems (par-titularly the western and southernenergy producing states), and thosestates that are experiencing the wind-fall from a healthy economic recove~(primarily the Great Lakesmanufacturing-based stiates).

The states that still are coping withrevenue shortfalls have been raisingtaxes. So far, three states have in-creased sales tax rates. These includeLouisiana from 3C%to 4%; Oklahomafrom2% to3%; and Tennessee from4.57. to 5.570. Three other westernstates extended last year’s sales taxincreases that were slated for expira.tion this July. Utah maintained the4.625CZ rate forthreem(~re years,while Idaho permanently adopted a4% sales tax rate rather than allowthe current 4.fJ%,tax to decrease to3% as was scheduled; and Arizonamaintained the 5% rate rather thanallow the rate to revert to 4Yo,

Other significant tax increases in-clude:. Arizona raised tbe cigarette tax

rate from 13pto 15@per pack andhiked excise taxes for spirits, wine,and beeq

. Louisiana increased the cigarettetax rate from llc to lG@per pack,changed the motor fuel tax from 84to 16q per gallon, instituted anew5% tax for on-premise con~”mptionof alcoholic beverages, and raisedinsurance premium, severance, andhazardous waste taxes. A con.stitutional amendmc:nt will be re-

ferred tothevoters to increase theco~rah income tax base. This taxpackage, including the propsedamendment, totaled over $7OO mil-lion.

. Okfahoma raised the gasoline taxfrom 6.6g to 9C per gallon, hiked al-cohol excise taxes by 257,, and re.pealed the sales tax exemption forher and cigarette

. South Dakota will maintain the13$ per gallon motor fuel tax whichwas enacted as a temWrary meaa-ure in 1981;

. Tennessee increased the corporatefranchise tax and insurance pre-m]um tax;

o Utah raised the franchise and netincome tax and severance tax on oil,gas, and hydrocarbons, and hikedthemotor fuels tax from lle pergallonta 14apergal10n;

. Washington instituted a $30 permonth commuter tax targeted atOregon residents;

. Vermont temporarily increased thepersonal income tax from 26% ta26.5% of federal tax liability andplaced a 20<%surcharge on cor-porate incomq

. Connecticut raised the motir fueltax fr0m14epergal10nt0 15c pergallon and provided for an annualone cent increase for each year until1991 when it will reach 23g per gal-lon;

. Alabama increased the motor fuelstax 2C per gallon and the cigarettitax from 16gapackto 16.5@a pack;and

. West Virginia taxpayers will voteon a November legislative refer.endure to amend the constitutionand raise the sales tax from 570 to6%.Major tax increa~en are now pend-

ing in the Alabama, Connecticut,Mississippi, and South Carolina Iegis.latures.

ConverseIv. tax talk in the GreatLakes area ~enkrs around tax de-

creases. At this time, Wisconsin hastaken action to lift the 10% surtax onpersonal and corporate income taxes,and Minnesota decided to remove its10% surtax-both retroactive toJanuary 1984. A personal income taxdecrease is imminent in Michigan.Reductions in income taxes also ap-pear likely in Delaware and Pennsyl-vania.

Other tax decreases include:. Georgia exempted prescription

drugs from the sales tax begin-ningin fiscal year 1986, becomingthe 44th state to do so (5 states donot have sales taxes);

. Nebraska reduced the personalincome tax from 2090 to 1970 offederal tax liability, auto-matically triggering a reductionin the corporate income tax be-cause the corporate rate is com-puted as a set percentage of theindividual rate;

. South Dakota and Washingtonlowered severance taxe% -

. Tennessee will phase-out thesales tax on food purchases overthree years beginning in 1985;

. Colorado will allow the 3.57.Balest= rate to decrease to 3% asscheduled;

. Hawaii will provide a $1 creditfor each exemption on the per-sonal income tax as mandated bythe constitutional budget surplusprovision; and

. Rhode Island decreased tbe per-sonal income tax from 26% of fed-eral tax liability to 24.99..

House, Senste ConsiderMunicipal Antitrust Msbility

When the Congress adopted theSherman Antitrust Act of 1690 it in-tended to circumscribe potentiallyanticompetitive activities of privatetrusts and catiels, not the public sec-tor. In the 1943 Parker ruling, tbeSupreme Court affirmed that stateswere free of antitrust scrutiny. It wasassumed that local governments weresimilarly immune.

But in its 1978 plurality decision inLafayette, the Court brought localgovernment activities under the reachof this body of law. In the most pub-

licized case in this regard—Boulder(1962)—the Court ended any auto-matic immunity enjoyed by localitiesby ruling that home rule by itselfdoes not constitute a sufficient grantof authority for local govenmentstoact anticompetitively.

hal governments are now beingsued with increasing frequency for li-censing, franchising, zoning, andreg-ulatory decisions that by definitiondisplace or restrain competition.These cases are resulting in largecosts even when local governmentswin. A case recently lost by a localgovernment will cost it $28.5 millionunless the decision is overturned.Concerned with the growing cosh tolocal governments, botb in terms offinances and their ability to govern,committees in both houses of Con-gress held hearingson this issuewithin tbe last few m{,nths.

The Subcommittee on Monopoliesand Commercial Law of the HouseCommittee on the Judiciary heldhearing on March 29 on three billsintroduced by members tlfthat Sub-committee aimed at providing reliefto local governments. Presided overby Rep. Peter Rodino, chair of theCommittee, and the bills’ author~Representatives Edwards, Fish, andHyde, respectively—the witnessesprovided strong testimony, thoughfew surprises. The testimony of stateand local oficials representing tbeNational Association of AttorneysGeneral (NAAG), the NationalLeague of Cities (NLC), the NationalAssociation of Counties (NACO), theNational Institute of Municipal LawOfficers (NIMLO), and the NationalConference of State Legislatures(NCSL) closely followed the pOsitiOnof their associations, further under-scoring the sharp differences c}nthisissue between the state and local lev-els (see Intergovernmental Per-spective, Fall 1983).

Most important, perhaps, was theopening statement by Rep. Rodino inwhich he asserted several limits orLegislative approaches to this pr<>b-Iem. In setting the context for thishearing, be questioned whether theSupreme Court’s ruling in Boulder“ tndyrepresents abold new de-parture, or merely a clarification of

developments long in the mak-ing. .“ Further, Rodino stressedthat any legislative solution wouldface the problem of offering

some measure of protection tolocal units without running afoul ofthe Tenth Amendment and its ad-monition to the federal branches ofgovernment t.a avoid interferingunnecessarily into the relationshipbetween the Sta@s and their politi-cal subdivisions.

Congressman Radino also noted thatState immunity is not absolute, thusa state cannot exempt “. privateconduct which is violative of the anti-trust laws simply by authorizing it.”

The hearing before the Senate Ju-diciary Committee on April 24 en-ableda number of Senators, the Ad-ministration and others to clearlyskate their positions. Senator Thur-mond, Chairman of the Committeeand author of the bill on which thishearing focused, began by statingthat “. a legislative response toBoulder is necessary.” His emphasison rapid congressional action to pro-tect local units stands in sharp con-trastto a statement he made nearlytwoyears ago that congressional ac-tion would await state and localagreement on the appropriate solu-tion.

Mayor Joseph Riley of Charleston,South Carolina, a member of ACIR,testified on behalf of the NLC andunderscored the threat to localfinances and governance capabilitiesposed hy their exposure to numerousand costly antitrust suits. The mayorcaused a stir by noting a pendingantitrust suit against a village ofabout 600 people in Colorado forroughly $850 million—more than$140,000 per village resident. Heextrapolated that a comparable suitagainst the U.S. as a whole wouldseek in excess of $35 trillion! To re-medy this situation Mayor Rileyurged that Congress amend the anti-trust laws to provide a broad immu-nity for localities similar to that en-joyed by the states.

JugglingIntergovernmental

RevenueConcerns

by Robert J. Kleine

Government watchers have documentedthe rise, distribution, and decline of fed-eral intergovernmental aid. Washington’sregulation of state and local activities hasalso been examined. The judiciary’s rolelikewise has been scrutinized and its im-pact on the federal system substantiated.I.ittle noted, however, are the complexwebs of tax interrelationships and howthe search for revenues to finance thethree levels of government leads to com-

8 petition for tax dollars.

GOVERNMENT RECEIPTS, BY LEVEL OFGOVERNMENT

SELECTED YEARS, 1954-1983(Percent Distribution)

Federalt State Local1954 70.9”/. 14 .90/. 14.1 ”/01959 69.4 15,6 15.01964 66.0 17.4 16,61969 66,4 18.5 15,21974 63,2 20,9 15.91979 64.5 21.6 13.91980 64.5 21.7 13.71981 65.5 20.9 13.41982 83.5 22.2 14,41983 (est.) 61.7 23.1 15.2

‘Includessocial insurancecontributions,Note:Percentagesmay not equal 100 becau$e of rounding.Source: ACIR,Significant Features of Fiscal Federalism, 1982-83

Edition, M.137, JanuaW 19&, Table 22.

I.—______ —J

ACIR’S Tax Policy

At its March meeting in Phoenix, Arizona, theJdvisory Commission on Intergovernmental Rela-ions adopted the following recommendations re-:arding federal revenue actions to reduce themdget deficit.

~1) FISCAL DISCIPLINE—The Commission de-sires to make clear that its recommendationsconcerning the intergovernmental implicationsof any action to strengthen the federal revenuesystem are coupled with two additional rec-ommendations for building greater fiscal dis-cipline into the federal budget process:● that the deficit be steadily reduced and that

until the budget is balanced revenues gen-erated by any additional taxation be appliedonly to reducing the deficit; and

● that to move toward budgetary balance asquickly as possible, Congress give attentionto the widest array of approaches availableto achieve balance-including expenditurecuts, a separate capital budget, a line-itemveto, and a constitutional mechanism to en-sure balanced budgets,

2) PRIOR CONSULTATION—The Commissionrecognizes that the federal tax system could berestructured in ways that would affect stateand local funding. The Commission recom-mends, therefore, that national policymakersconsult extensively with stak and local electedofficials before charting any major new coursefor federal revenue policy.

In particular, broad federal income tax re-form which reduces or eliminates a wide rangeof tax benefits may substantially restrict twoprovisions of the present income tax that pro-vide fiscal assistance to state and localgovernment~eductibility of state and localtaxes and the tax exemption of interest onstate and local bonds. Therefore, such federaltax reform and revenue raising efforts shouldinclude explicit consideration of potentialharm to state and local ability to raise rev-enues and to borrow funds.

3) NO INCREASE IN FEDERAL SELEC-TIVE EXCISE TAXES-The ACIR has con-cluded that the benefits the national govern-ment would derive from increasing selectiveexcise taxes would be more than offset by the

negative effects such actions would have onstate and local revenue-raising ability. TheCommission recommends that Congress resistpressure to increase federal reliance on selec-tive excise taxes.

(4) OPPOSITION TO FEDERAL VAT—TheCommission concluded that a major intrusioninto the consumption tax field by the federalgovernment would restrict the ability of stateand local governments to increase their salestaxes, would provide a powerful new engine forfederal spending, and would reinforce the cen-tralization and fiscal dominance of thenational government at the expense of stateand local governments. The Commission there-fore recommends that the federal governmentrefrain from enacting a major consumption taxas an additional revenue source or as a re-placement for other federal taxes.

(5) RETAIN INDEXATION—The “Commissionreaffirms its support for indexing the federalpersonal income tax. If and when Congressraises income taxes, the tax increase should bethe consequence of direct legislative action andnot the result of inflation-induced bracketcreep.

(6) NO VOLUME CAPS ON TAX-EXEMPTBONDS-The Commission concludes thatstate and local interests in issuing tax-exemptbonds for private forms of economic develop-ment must be balanced against federal aver-sion to financing private projects that arewidely viewed as not deserving federal as-sistance. The Commission opposes the im-position of new federal volume caps. It recom-mends, however, that Congress build on thereforms enacted in TEFRA by: (1) eliminatingtax-exempt financing for projects that do notmerit federal assistance or that do not con-tribute to economic development; (2) elimi-nating certain opportunities for “double-dipping” in which private businesses benefitfrom federal tax benefits in addition to tax-exempt financing and (3) limiting the totalamount of “small issue” IDB’s allowed any oneuser. The Commission noted, bowever, thatthese restrictions should not apply to residen-tial housing bonds and economic developmentbonds for distressed communities.

‘r:d)h!2.1‘rhc, vev<xIIuc! loss \v:Is :i [ll:ij(,r cO1lcc:rn to st;st(: :III(i

l<)c:Il oflici:ils, h~]t II()[ the IIrlly c<)llcerr]. ‘rh(, illzlt.tcr]t iorlto Lht, irltcrcovt,r rlrll<,llt:ll irlLr)tic;lti<)ns ()( t.h(, 1981 lc~is-

T(! 1>/<2Status of Accelerated Cost Recovery System

forState Corporation tncome Taxes at End of 1983

.-ACRS

AllowedAlabamaAlaska (t)AtizonaColoradoDelawareHawaiiIdahoIllinoisIndianaIowaKansasLouisianaMa~landMassachusettsMichigan (2)MississippiMissouriMontanaNebraskaNew HampshireNew MexicoNodh CarolinaOklahomaRhode IslandUtahVarmontWisconsin (3)District ofColumbia

Parf ofACRS Allowed

ArkansasConnecticutFloridaKentucky (4)Maine (4)Minnesota (4)North Dakota (5)Ohio (4)Pennsylvania (4)South CarolinaTennesseeVirginiaWest Virginia

ACRSNot AllowetCaliforniaGeorgiaNew Jereey(4)New YorkOregon

(1) Depreciation for oil snd gas producers and pipeknes is com-puted on the basis o! section i 67 of the Internal RevenueCode as that section read on June 30, 19S1.

(2) No corporation income tax. ACRS allowed for personal in-come tax. Depreciation not relevant for single business tax.

(3) ACFiS not available for public utilities nor for propetiy locatedoutside the state.

(4) ACRS allowed in tull for individuals.(5) Individuals filing the shoti term are allowed ACRS in full.

Source: Federation of Tsx Administrators, Tax AdministrationNews, Vol. 48, No. 2, Februaw 1984.

THE CURRENT PROBLEM:CONFLICTING ALTERNATIVES

Impose Surtax on Individual and Corporate IncomeTaxes. A I () pIrCt>rIl sllrt:ix wc)[lld r;lis,. :Ih<)!It $4 I hil-Ii,,ll :Illrlll:lllv :Ind w(l(,ld h:lv<, rl,t]ghly the. S:,II>C. irT>p,!ct011 ,St,l[(, :Irld Ioc:l I g<)v<>rrlnl(,”ts :,5 rc.p<.;tI (II itld(.x:iti, )rl.I li~}) fc:dc,r:ll irlc<),llc. t:lx<s wIl(lld, :1s (Iisvl]sscd :Ih(lvt,11:1,( s(IrII( positiv< i[]t.c,rgo\6>r11r))c,[1t:11 (,fJ’(,cts II(II wI)tlldprol):lhly stifY(,n r(.sist:irlcc to r:lisir>g st:tt,, iitld I(Ic:IIt ;Ixc,s c,\tLII r!lOrc: t h;tirl w(IcIld r(p(,;ilitlg irld(, x:lt i<)t>.

Th( lrl:c,jor pr[]hltr,l wittl th( surt; lx, IS with rcsp(,:Il [,Sir]dt,x;ltilll]. is th:it it d[,[,s rl<)tfli!&Xt<) ;iddr<,ss thl, l,c<l-rl[jrl]ic :IrI[i t.:ix-<.>(ll]it.,vwc; tkrl(>sst, s [II th<, li~dc,r:~l irlv(Br]lt>t:lx. III t:lct, it t,x;ir(.rh:!t.c>s t tlt,s,. w<.:ik,l<>ss<.s.

Table 3

Major Revenue Proposals For Reducing The Federal BudgetDeficit4 Comparative Analysis

KEY POLICY CONSIDERATIONS

EFFECTSAT FEOERALLEVEL EFFECTSAT STATE-LOCALLEVEL

Political Administrative Emnomic TU Equity fiscal

Tax andOescriptiOn

INCREASETAX RATES

i, Repeal individualincome tax indexing

2. Add 10!1,SUlt8X toindividual & corporateincome tax

BROADENBASE OFINOIVIOUAL INCOME TAX

1. Close major taxloopholes (no fax ratereduction)’

2. Switch to motif iedflat rate income tax

3. Switch to a comprehensive, flat rateIncome tw

ENACTNEW CONSUMPTION-NPE TM

1. Add a broad-basedenergy Im

2. Add a Value-AddedTM (consumption-type)to current law’

3. Switch to a per-sonal expenditure tax

Effect on Effect on Effect on Effect onEase01 Politiml Ease of

ThreatensCapi&l Effect on Effect on

lmplemen-Ettect on EHecton Value of S-L Effect on S-L Sales

Account- Taxpayer Formation Work Economic Progres. Horizontal Tax Oeduc- Tax-Exempt Taxtation’ abiliv’ Compliance Incentives? Incentives? Distortions? sivity? Equity? titilify? Bond Slalus? Position?

fair to very no change no change slightly slightly slightly slightly enhancesgood poor weakens worse reduces worse value

fair to good no change slightly slightly slightly no change slightly enhancesgood weakens weakens worse worse value

fair to fair slightly no malor no ma]or slightly no majorgood improves change change Improves change

fair to good considerably slightly consider- consider- slightlypoor improves weakens ably ably reduces

improves improves

Vely good greatly slightly greatly greatly greatlypoor improves Improves improves Improves reduces

fair to good nO change no change no changegood

poor poor ROchange’ slightly no changeto Improves

good’

vefy good greatly greatly consider-poor Improves improves ably

Improves

Sou!ce ACIRs!ati, April 16, 1984.

‘On a sale of f to 4, very poor= t, poor =2, fair =3, and good =4.“Fair to good” and “fair to poor”’ OCCUPYintermediate positions. Seealso Note 5.

‘Refer to Table 1 for a complete listing of selected tax loopholes. Fromthat selecbon, the Iaroest revenue sources would be: eliminating the ex-clusion for private-pu;pose tu-exempt bonds, repealing deductibidy ofconsumer interest payments, taxing 50% of Social Security benefits, re-pealing the state and Iota sales t% deduction, and tming someemployer-paid health ben8fltS.

‘Complete etiminafion of the sales and personal property deduction cou-pled with a major reduction in the value of the real prope~ and per-sonal income tax deductions.

no major slightlychange reduces

no major slightlychange reduces

greatly slightlyimproves reduces

slightlyimproves

constder-ablv

greatlylnlproves

no malorchange

no majorchange

consider-ably

tmproves

ma]orweakening

majorweakening’

completeehmination

no change

no change

completeelimination

enhancesvalue

enhancesvalue

malorweakenifig

malorweakening

completeelimination

no change

no change

completeelimination

“Assumes that virtually all of additional revenue obtained from the tax willbe used for deficit reduction and not as a supplement for the eliminationof any existing federal tax.

‘Poor” accountability if the tax is hidden; “good” political accountabilitytf the total tax is staied separately at the retail level

‘Ease of tm compliance will be unchanged for individual taxpayers. al-though business taxpayers may tind tax administration more complex,depending on its exact form,

‘The seriousness of the threat is determined largely by the height andvisi~lity of the tax, A VAT with a relatively Mgh rate. say 8?, that isstatti separately at the retail level would be highly restrictive. Con-versely, a VAT with a relatively low rate, my 3% that is hidden in theretail price would be far less restrictive.

no

no

no

no

no

no

possibly’

no

Individual Income Tax Returns, Statistics of Income, 1981, Tables 1.1and 2.1.

“Tax Reform Act of 1903, Report of the Committee on I~ays andM...., U.S House of Represenlatlves o“ H.R. 4170, Vol 1, 1983, p375

Table 4

A Comparative Description Of The Major Revenue

EsIimate of Total

Tax Change

INCREASE TAX RATES

1, Repeal individual incometax indexing

Additional FY 85 toRevenue W 89for FY 85 Revenuein billions” Etilmate(SOurca) in bilfions Tsx Rate Tax 8ase

$17 (CBO, $185 NIA A@usting the individual income tsx toFY 86) changes with Censumer Price Index is

scheduled to begin January 1985, U~Erindexafion, inceme tax brackets, standarddeduction, and personal exemptions will beadjusted 10 annual inflationary economicchanges.

W9 (CEO) $230-245 1o% Existing individual and wrporate tsx baaesurcharge would be used with a 10% surcharge placed

on tax habilify.

2. Add surtsx to individual& cur~rate imme tax

BROADEN BASE OF $25 (ACIR $170-210INDIVIDUAL INCOME TAX based

1. Close major taxestimatesfrom CBO &

Impholes (No chan9e in@ OMB)rates)

2, Switfi to mtified flat $45 (ACIR $225-250rate tss estimates

assuming a15“A Sll~=)

No change

14”A up to

$40,000

26% $40,ml565,00030% over$85,000(for jointreturns)

22%

Under the Tsx Equity and FiscalResponsibility Act of 1982, numerous minortw changes were made to raise Largeamounts of revenue. The revenue e<lmaieeassumes closing the follwing cornmenlydiscussed tax preferences (Ieopholes); tax50”A of social security and railroadretirement bene6ts over a spacifdthreshold: tax unemployment wmpenaafion& workmen’s cmnpenaation benefti fimitmoflgags interest deductions to onlyprima~ residences; repesl charitablecentributiens for nen-itemizeffi; etiminate thetax-exempt status for newly issued pfivate-purpose state-local bonds; and repaal state& l-l ssles tsx tiucfions.

Under the current Bradley-Gephardtproposal, there would be a ba~ tex rate of14°A and two sutiax rates of 12% and 16“/0depetitng on inceme level. The persenaleXEmPfiOnwould rise to $1,~ for eachtsspayer and the standard deduction weuldbe 53,W for single taxpayers and $6,000for mar~d tsxpayers. This measure wouldgreatly broaden the income tsx base, butretains the popular daductiins for interestpsid on home n’mngagas, charitablecontributions, Iargs medical expnses, andstate and l-l inceme and real propertytaxes. These deductions, however, spplyOn~ to inCOMe tsxsd at the 14% rate.

A flat rata tw would provide one tax rate forall taxpayers and eliminate all faxpreferences. To match current individualincome t* receipts of abut $300 Wlllion,CBO Assumptions are based en a 19°A fssrate and raising the persenal exemption to

3. Switch to a .$45 (CBO) $225-$250ydrhe=naive, flat rate

Proposals For Reducing The Federal Deficit

Estimate of TotalAdditional FY 85 toRevenue FY 89for Ff S5 Revenuein billions’ Eafimate

Tax Change (Source) in billions Tas Rate Tas saw

$1,500 from $1,000 and the zero bracketamount to $3,00Q for single tax filers and to56,000 from $3,400 for joint returns.Assuming a 15°/0 incmaae (Qr $45 MlIii) inrevenue was desired, a 22% tax rate wouldbe required.

ENACT NEWCONSUMPTION TYPETAX

1. Add a broad-baaedenergy tas

2. Add a Value-Added tas(consumption wp)

3. Switch to a personalexpenditure tas

$11(CBO)

$54 (ACIR)

$43-61(Brwkinga)

$s3 5“/0 A broad-based enemv consumDfion tas

$310-340 3“A

$215-305 Similar tocurrentincome tassystem

would tas &meefic k- inrpoffed’ energy,including petroleum, natural gas, cual,hydroelectric & nutiar per. The CBOrevenue e~lmate is baaad on the value ofenergy produced, but ahamafiveapproaches could include faxing the unitsproduced (such aa fona or *efa) or theamount of heat content pmdd by eachenergy source measured by Brffiah ThermalUnits (BTus).

A value-added fax ia a fax on the vafue thata stage of production adds to a product.This addad valua is the sales pf~ of thepfoducta acid, nrinue the wmfraee ptice ofthe inputs or raw materials used inproducfii. The fax ia WIad at each stageof producfien end during resale. Aresumption-type VAT would show theamount of VAT to be paid by the mnaumerseperate fmm the selling price of theproduct. This fax WOUH share certaincharacfe~lce with a atate sales tas. A VATcan be daviaad to exclude from taxationbusiness capital formation expenditures.

A personal ex~iture taxis similar to anin~me fas, but rather than tasing in-eamings, it would fas i~iiduals’ spandiW& exempt from tasafion savings &investment. The tas rates, ~raonalexemption, & zero bracket amount can beformulated to be progressive. The majorsource of additional tax revenue would bederived from eliminating moaf faspreferenu?s now in the faderal tas cnde.

.Frsvenueestimatesfmm the ti~~onal @u@ Offica and the* of Managementati eudget were reads in F~maty 19rr4.

~urce: ACIR staff (March 20, IW).

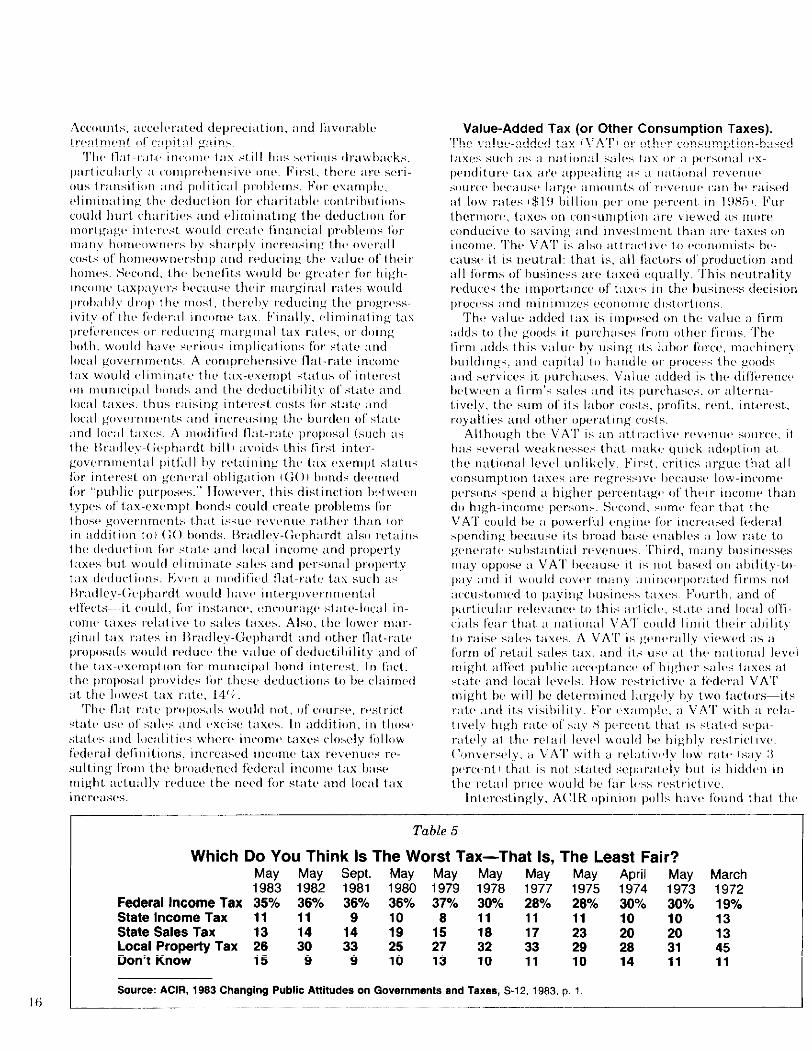

Table 5

Which Do You Think Is The Worst Tax—That Is, The Least Fair?May May Sept. May May May May’ May APril May1983 1982 1981 1980 1979 1978 1977 1975 1974 1973

Federal Income Tax 35% 36% 36% 36% 37% 30% 28% 28% 30% 30%State Income Tax 11 11 10 11 11

1: 19 1:10

State Salea Tax 13 :; :: 20Local Property Tax 26 ~ 33 25 27 ;; ~ 29 2S 31Don’t Know 15 9 9 10 13 10 11 10 14 11

March197219%13134511

1Ii L- ....,Source: ACIR, 1983 Changing Public Anitudes on Governments and Taxes, S.12, 1983, p. 1.

Description of Michigan VAT

The only state that levies a value-added tax(VAT) is Michigan. The Michigan VAT took effecton January 1, 1976, and replaced seven otherbusiness taxes, including the corporate income tax,the corporate franchise tax, and personal propertytaxes on inventories. Because the VAT is the onlymajor business tax in Michigan, other than thelocal property tax, it is known as the Single Busi-ness Tax.

The Michigan VAT is of the modified, con.sumption type and is calculated using the additivemethod. The taxpayer begins with federal taxableincome and adds to it the other components ofvalue-added: compensation, interest paid, depre-ciation, royalties paid, and dividends paid. A fulldeduction is allowed for capital investment eachyear. There is a $40,000 small business deduction(which is phased out as profits increase), a creditfor firms with gross receipts of $3,000,000 or lessand low profits, a deduction for firms with corn.pensation costs in excess of 63 percent of the taxbase, and a limit on the tax base of 50 percent ofgross receipts for all firms. The original legislationincluded a number of special transition dedt~ctionsthat have been largely phased out. The tax is col-lected in four quarterly payments and an annualsettlement. The rate is 2.35 percent, which has notchanged since the tax was enacted.

The yield of the tax in its first full year, FY1977, was $803.5 million, The yield in FY 1983was $999.7 million and the estimate for FY 1984is $1.135 billion.

,..

Rokc,rt ,J. Kleinc, is o Sc?nic)r A nal,y,st iaA [.?IR’s TILxatioa ancj Jf’in,ance, S’(,(tion. other

m.c,nz h(,r.s of th(, Sc>cti(>a c:r)rtlri[)[Ltia~, to tkc,r<,~]ort on [i)h ich this arti(lr r~)a..sha.s(~d incl{i(l(,.tJah a Shnn non, J)a.[]h n<, K(,rz,voa, S[isarz nah(;[L/kirLs, E?nn)<,litL<, Rocha, Kart,n B[,I1 k(,r aa<iMark M<,nch ik.

17

Local Finance:A Bootstraps

Operationby Stephanie Becker

Over the past decade, three major joltshave altered the landscape of local gov-ernment finance. First, local financialemergencies-particularly in New Yorkand Cleveland—stunned the municipalcommunity in the mid 1970s. Secondly,beginning in 1978, the taxpayers’ revoltdrove home the message of the public’saversion to property taxes and of a wide-spread desire for slower governmentgrowth. Third was the decline in federalaid, first in relative terms in the late 1970sand then in absolute terms in the early

18 1980s.

This article will explore the effect of these three joltson local efforts to diversify their revenue systems. Rev-enue diversification began in earnest afier World War Ifwhen local governments sought to reduce reliance onthe property tax while increasing revenues throughlocal sales or income taxes. This type of revenue diver-sification continues to the present day, but local salesand income taxes have been joined by an array of non-tax and other tax sources. Further, the revenue diver-sification movement has taken a new twist: revenuesare increasingly viewed by local oficials as not merelysources to be tapped, but something government leaderscan help create.

REVENUE DIVERSIFICATIONTaxation is frequently likened to plucking a goose; in

both, the object is to gain the most feathers with theleast squawking. For most years in our nation’s history,the favored local “feather” was the property tax whichin 1932, provided about two-thirds of the funds for alllocal governments combined. By the beginning of thisdecade, that proportion had fallen to about one-quarter,Increasing federal and state aid undoubtedly was aprimary factor behind the declining role of propertytaxes. Other influences, however, were important. Col-lectively they can be termed revenue diversification or“anything but property taxes. ”

Not all local governments have traversed the diver-sification path at the same speed. As Chart 1 indicates,

chart 7Properly Taxee Ae a Parceb

of Own SourceRevenuePercent of* SWrce

“~mge$00

00

‘eo b **

.70

m

*

m--9

“\30

‘\

at I

.’:~Ymt94252576267 727762_ ACIRstuff~

Table 2

Reliance On Local Sales Taxes ByIndividual Large Cities

General Sales and Gross ReceiptsTaxes as Percent of All Taxes for:Fiscal Year Frscal Year

City and State 1971-72 198?-S2Buffalo, NY 7.2Chicago, IL 14.1 16.7Dallas, TX 19.6 27.3Denver, CO 41.0 47.5El Paso, TX 222 24.8Fort Worth, TX 23.6 29.6Houston, TX 25.0 29.9

Kansas City, MO 5.6 16.4

Long Beach, CA 22.5 22.3Los Angeles, CA 19.5 23.9

Nashville-Davidson, TN 22.4 31.0

New Orleans, LA 41.2 48.5New York, NY 13.5 17.6Oakland, CA 22.1 20.8

Oklahoma City, OK 37.6 68.5Omaha, NE 26.6 42.3Phoenix, AZ 39.0 41.5

St. Louis, MO 11.7 18.5San Antonio, TX 26.5 45.6San Diego, CA 29.1 40.3

San Francisco, CA 13.3 11,8

San Jose, CA 23.5 30.6Seattle, WA 14.4 14.4Tulsa, OK 55,1 80.5

Note: Large cities” are those with at least 300,0W residents in both1979 and 1980 enumerations. Washington, DC., is excludedas outside a state-local system, The large cities hsted indi.vidually are those that levied a general sales or gross receiptstm in at least one of the two fiscal years: 1971.72 and1980-81,

Source: ACIR stall compilation based on U.S. Bureau of the Cen-sus, City Government Finances in 1971-72 (GF72, No. 4,Table 7) and City Government Finances in 1981.82(GF82, No. 4, Table 7).

‘Buffalo rescinded its sales tsx

Table 3

Reliance On Local Income Or WageTaxes By Individual Large Cities

Income Taxaaaa Percant of All Taxr?a for

Fiscal Year Fiscal YaarCity and Stata 1971-72 1981-82Baltimore, MD 14.2 21.6Cincinnati, OH 57.7 72,7Cleveland, OH 47.8 72.2Columbus, OH 78.2 63.7Detroit, Ml 35.1 47.9Kansas City, MO 37.0 32,7Louisville, KY 55.6 64.5New York, NY 21.0 27.1Philadelphia, PA 62.5 66,4Pittsburgh, PA 16.8 24.4St. Louis, MO 29.4 31.4Toledo, OH 74.9 76.8

Note: Large cities are those with at least 300,000 residents i“ hth1970 and 1980 enumeration. Washington, DC., is excludedas outside a state-local system. The large cities listed indi-vidually are those that levied an income tax in at least one ofthe two tiscal years 1971-72 and 1981.82.

Source: ACIFI staff compilation based on U.S. Bureau of the Cen-sus, City Government Financas in 1971-72 (GF72, No, 4,Table 7) and City Government Finances in 1981 .a2(GF82, No. 4, Table 7).

Table 4

Local Government Current Charges Per Dollar of Local Taxes,

Fiscal Years 1972-1982

Stateand RegionU.S. Average

New EnglandConnecticutMaineMassachusettsNew HampshireRhode IslandVermont

MideaatDelawareDist. of ColumbiaMarylat ,dNew JerseyNew YorkPennsylvania

Great LakesIllinoisIndianaMichiganOhioWisconsin

PlainsIowaKansasMinnesotaMissouriNebraskaNorth DakotaSouth Dakota

SoutheastAlabamaArkansas

1972.22

.07

.08

.11

.09

.06

.06

.49

.17

.17

.12

.17

.20

.15

.25

.27

.23

.15

.24

.22

.24

.25

.22

.18

.13

.67

.56

1982.34

0.110.160.190.110.070.09

0.600.100.260.160.200.24

0,220.500.350.270.50

0.400.350.590.350.410.280.19

0.850.78

FloridaGeorgiaKentuckyLouisianaMississippiNorth CarolinaSouth CarolinaTennesseeVirginiaWest Virginia

SouthwestArizonaNew MexicoOklahomaTexas

Rocky MountainColoradoIdahoMontanaUtahWyoming

Far WastCaliforniaNevadaOregonWashington

AlaskaHawaii

.50

.66

.40

.27

.70

.36

.49

.42

.21

.37

.20

.65

.41

.33

.22,37.15.23.43

,18.44.21.41.70.10

0.570.750.400.431.120.510.660.470.220.54

0.370.550.440,38

0.270,670,190.300.33

0.430.960,290.600.590.12

Source: ACIR stall computations based on U.S. GeneralAccounting ~ce, ,lncludng User Charges in the GeneralRevenue Sharing Formulas Could Broaden the Measure ofRevenue Efforl, PAO-82 .23, September 2, 19S2, Table12, pp. 50-51; and U.S. Oepaflment of Commerce, aureauof the Census, Governmental Finances in 19al-19S2.

“Ibid., P, 12 21

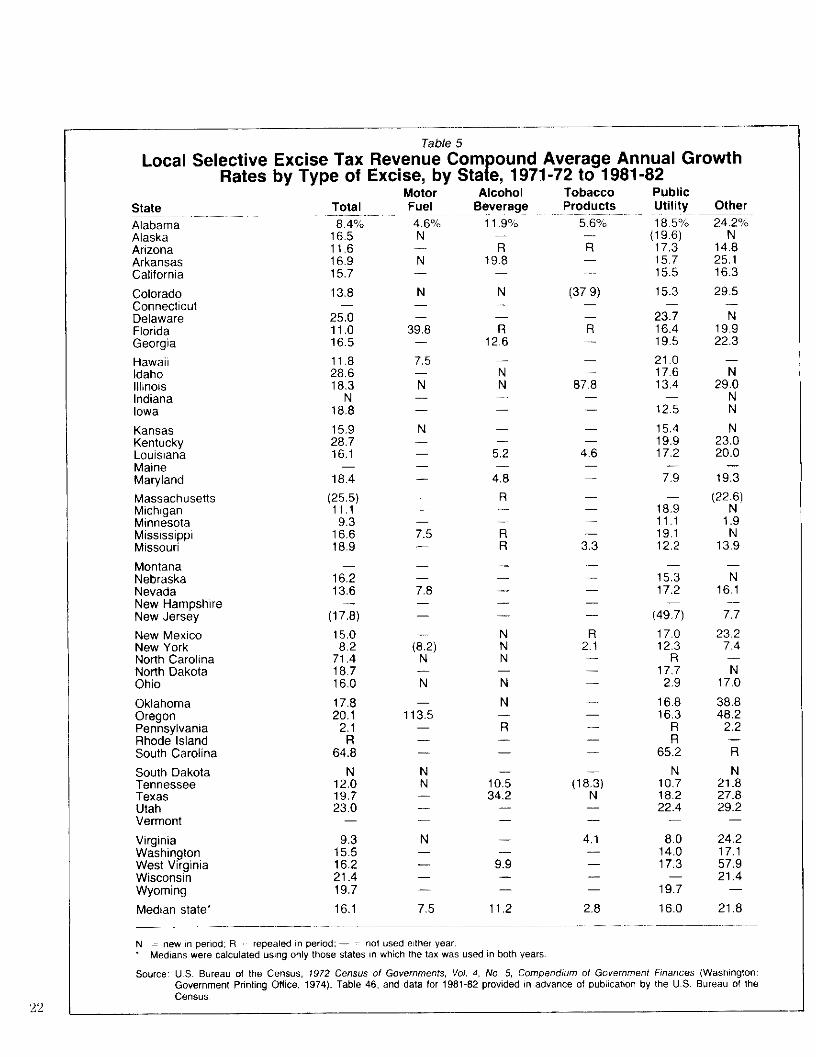

Table 5 I

Local Selective Excise Tax Revenue Corn ound Average Annual GrowthrRates by Type of Excise, by Sta e, 1971-72 to 1981-82

Motor Alcohol Tobacco PublicProducts Utility

5.6% 18.5%(j;::)

15.715.5

Other

24.2%N

14.825,116.3

29.5

State

AlabamaAlaskaArizonaArkansasCalifornia

ColoradoConnecticutDelawareFloridaGeorgia

HawaiiIdahoIllinoisIndianaIowa

KansasKentuckyLouisianaMaineMaryland

Total

8.4”/.16.511.616.915.7

Fuel

4.6”/0N

Beverage

11 .9°in

x19.8

—

—.R

(379)

E—

—

87~8

4,6

3;

2;

—

—

—N

13.8 N N—

15.3

23.716.419.5

21.017.6134

12.5

15.419.917.2

7<

18,911119112,2

15<17.2

N19.922.3

25.011.016.5

11.828.618.3

N18.8

15,928.716.1

— —39.8 R

12,6

7.5

29!NN

N23.020.0

19;

(22;)

1.9N

13.9

N

N —

5.2

—18.4

(;;:;)

9.316.618.9

16;13.6

4.8

RMassachusettsMichiganMinnesotaMississippiMissouri

75—

—RR

MontanaNebraskaNevadaNew HampshireNew Jersey

—————

NNN

zN

K—

N16.1

—7,8

(17.8) (49.7)

17.012,3

R17.7

2.9

16.816.3

R

651

N10,718.222.4

7,7

23.27.4

—

15,08.2

71.418.716.0

New MexicoNew YorkNotth CarolinaNorih DakotaOhio

N17.0

38.848.2

2.2

OklahomaOregonPennsylvaniaRhode IslandSouth Carolina

17.820.1

2.1

64!

—13,5

——R

21!27.829.2

South DakotaTennesseeTexasUtah

N12.019.723.0

NN 10.5

34.2(18:)

4,1———

2.8,,,,,,,.

Vermont

VirginiaWashingtonWest VirginiaWisconsinWyoming

9.315.516.221.419.7

N—

8.014.017.3

24,217.157.921.4

9.9—

——

19.7

16.0Median state” 16.1 75 112 21.8—

N new ,. period; R repealed in period: — not used e,ther year,, Mefians were calculated using only those states in which the tax was used in both years

Source: u.S. Bureau of the Census, 1972 Census of Governments, VOJ 4, No 5, Compendium o! Government FI”.”c.s (Washington:Government Printing OMCe, 1974), Table 46: and data for 1981-82 provided I. advance of publication by the U.S. Bureau of theCensus

—,2 ‘2

Table 6

Composition of State Aid(~;~7Bitlions)

1957 1962 1972 1977 1981 1982Education 570/0 ($4.2) 59”/0 ($6.5) 620/o ($1 1.9) 580/. ($21 .2) 61 O/. ($37.0) 630/. ($57,2) 630/. ($60.7)Public Welfare 150/. ($1.1 ) 160/0 ($1 .8) 150/0 ($ 2.9) 190/o ($ 7,0) 140/0 ($ 8.7) 120/0 ($1 1.0) 12”A($1 2.0)General Aid 9% ($0.7) 80/0 ($0.8) 80/0 ($ 1.6) 100A ($ 3.8) 10% ($ 6.4) 11 O/. ($ 9.6) 10°/.($lO.O)Highwaya 150/. ($1.1) 12“/0 ($1 .3) 10% ($ 1.9)Other

7“/0 ($ 2.6) 60/. ($ 3.6)5“/. ($0.3)

5% ($ 4.7) 5“/. ($ 5.0)4% ($0.5) 5% ($ 0.9) 60/0 ($ 2.2) 90/. ($ 5.4) 100/. ($ 8.7) 90/0($ 9.2)

Sources: The States and Intergovernmental Aids (1977], ACIB Report A-59, p, 10, State Payments to Local Governments, v. 6, No. 3, ofthe Census 01 Governments, U.S. Csnsus, p. 14; State Government Wnances in 1981 and 1982, U.S. Census, p 10, adjusted forstate lntergove,nment expenditure to federal governrne.t.

“The Entrepreneur in Local Government, cd. by Barbara H Moore,Internat,vnal City Management Assoclat, on, Wash, r%gtan, D.C., 1983,p, 7. 2:1

fi]ll.y providing t.mplt]yl]lent ii[ld tilx dt]ll[irs.

“lb!d, p, 61.l“Tercy Clark and Lorna Ferg,, sIJn. City Money, Colc)mb,~~U,,,vc!rsi(y

j .4 Press, New York. 1983, p. 6

L& ‘l’he most importantingredient in the localgovernment survival mix maywell turn out to be the decidedlyentrepreneurial approach beingtaken bv more and more localleaders:

YY

THE EFFECTS OF HISTORYAND CULTURAL VALUES

Similarities andDifferences:

Federalism inWest Germanyand the United

Statesby S. Kenneth Howard

Startled, stimulated, reassured and re-signed are all emotional reactions this au-thor felt during two days of intensiveroundtable discussions and many infor-mal conversations that were held betweensmall C~erman and American delegationsassembled to discuss the workings of theirrespective federalisms. This paper cap.~ultls the m{)~t striking similarities and

differences that emerged during a bi-lateral symposium. These gleaningsseemed to arise under three general head-ings: the effects of history and culturalvalues; the powers and roles of the states;and the impact of parties and tht: media.The first three sections that follow willtake each of these categories in turn. Be-cause these three sections tend to high-light differences, a fourth and final sec-tion will focus specifically on similarities. ‘2,’,

German and AmericanFederalism

Under the aegis of the Konrad Adenauer Foun-dation and the Council for International UrbanLiaison and with financial support from the Oer-man Marshall Fund, delegations from the UnitedStates and the Republic of West Germany met inBuehlerhoehe, West Germany, last September todiscuss the problems their respective nations facein making a federal system work. The Americandelegation included four past or present membersof the U.S. Advisory Commission on Inter-governmental Relations (ACIR): Governor ScottMatheson of Utah, Mayor Tom Bradley of bsAngeles, Ambassador Richard S, Williamson, andCongressman Robert S. Walker of Pennsylvania.Other members of tbe delegation were formerMinnesota Governor and U.S. Senator WendellAnderson; Scott County (Iowa ) Supervisor MaggieTinsman who is also Chairperson of the IowaACIR Lou Winnick of the Ford Foundation; andJohn Herbers of the New York Times. The Ger-man participants included Dr. Wolfgang Zeidler,President of tbe Federal Constitutional Cou@Minister of State Friedrich Vogel; Chief MayorManfred Rommel of Stuttgart; Dr. Franz RudolfKlein, President of the Federal Fiscal Court; Dr.Wilhelm Kewenig, a sta~ senator from Berlim Di-rector Hans Ruhe of the Federal Ministery ofFinance; Dr. Thomas Loffelbolz, Editor in Chief ofthe Stuttgart.erZeitun& and Stuttgati CityManager, Dr. Wolfgang Schuster. Tbe symposiumwas coordinated and directed by Professor HorstZimmerman of Marburg University and Dr. S.Kenneth Howard, Executive Director of ACIR.

.THE POWERS AND ROLES OF THE STATES

:! AflIclt?7;3 1,2)3

Excerpts From “Notes OnWest Germany”

by Anthony Downs

POPULATION

The Federal Republic of Germany (West Germany)had a 1981 population of 61,.4 million persons inan area of 96,000 square miles—about the size ofOregon or Wyoming (each of which contains fewerthan 2,7 million people), So West Germany has27.3Ch of the total population of the continentalU.S. in 3.2% of its total area. West Germany’spopulation was 50.2 million in 1950, rose to 61.8million in 1974, and has declined since then, Itsgrowth after 1945 included over 14 million refu-gees. That inflow was cut off by construction of theBerlin wall in 1961. East Germany’s 1981 popu-lation was 16.8 million in an area about the size ofOhio, which had 10.8 million people in 1980.

West Germany is now experiencing a notable mi-gration of households from north to south quitesimilar to our movement from the Northeast andMidwest to the South and West-though relativelysmaller. It is occurring for similar reasons, too: thesouth has a more attractive climate and geog-raphy, many older persons are retiring there, thefastest-growth industries are located there, andthe older, more obsolete heavy industries are inthe north in the Ruhr area. Hence housing pricesare higher in the southern states than in thenorth, and vacancies are rising in the indus-trialized Ruhr,

INCOME AND POVERTY

Why has Germany been more successful in almosteliminating poverty among its citizens than theU. S.? This was the most intriguing question raisedby my visit, especially since the U.S. is perhaps abit wealthier. My discussions with West Germaneconomists and others indicate that these WestGerman traits lacking in the U.S. help explainthis result:

. The West German government inherited atradition of paternalistic care for tbe workingclass by the government that started with Bis-marck. There was no such tradition in theU.S. until the New Deal of the 1930s, andeven than it was not universally accepted asdesirable or necessary.

. By the end of World War II, nearly all WestGerman citizens, from the very richest to thevery poorest, had personally experienced thehardships of extreme deprivation and loss,

.

.

both economic and personal. Everyone saw thedesirability of creating a social welfare systemthat would help those injured by forces beyondtheir control to survive at a decent minimumstandard of living,

Until recently, the West German populationconsisted almost entirely of persons of Germanethnicity who spoke German. This homo-geneity prevented any large groups from be-ing considered socially or otherwise inferior bythe majority, and therefore discriminatedagainst in any way. That has clearly not beenthe case in the U.S. We have a long history ofethnic discrimination, and many social aidprograms predominantly serving blacks orother minority groups have been limited inresources for that reason,

West German Dublic education is far moreequal in quality all across the country thanU.S. public education. All schools are financedby the state and national governments, notlocal governments; hence they receive aboutthe same funding per student regardless ofwhere they are located. Also, teachers arecivil servants who cannot refuse assignmentto specific jobs; so tbe quality of teaching ismuch more even geographically. Finally, tbevast majority of students come fromethnically-similar homes with parents highlyrespectful of the value of education.

This drastic reduction of poverty through oper-ation of a welfare state has some costs, too, thoughit is hard to prove exactly how large they are. Taxreceipts as a fraction of gross domestic product in1980 were lower in the U.S. than in West Ger-many but higher in France and Sweden than inWest Germany, Fringe benefits now compriseabout 70% of total wage costs per worker, and it isdifficult to fire workers once they have been hired,Firms are reluctant to hire additional workers,preferring instead h substitute capital for labor,Moreover, small businesses have more difficultygetting started than in the U.S. All these factorsmay be related to the much slower growth of em-ployment in West Germany than in the U. S., andthe supposedly larger extent there of the so-called“underground economy” that does not pay taxes.There is now pressure to shift to a 35-hour weekto spread the work around. But doing so withoutreducing worker incomes would increase laborcosts and thus reduce the competitiveness of WestGerman products in world markets.

Anthony Downs is a Senior Fellow with the BrookingsInstitution in Washin&<jn, D.C.

LL The German penchant forregulation and legalization givessustenance to the statelegislatures.

97

m<)st nl>lj<]r An]eri call p~)litic~ll campaigns. In tht:United States, the Irec. marktt ,~perates among both theprint :ind th~, elc:ctronic n>edia. In [>c:rm any, the: c,lcc-tr(]nic media, both radio and tt:levisi(~tl, are publiclyc]wn~:d and <]peratcd. The print media is not so c~)r]-strtli ncd.

Under legislation supported by both parties, the)I):iti[>nal k,c)vc.rnm[;llt alloctltes r:ldio :ind Lelevisi(]n timeto th{: partit:s it) c~cc<)rd:il)ce with the proportion c)f’v(>tcseach receivc,d in the I;ist r(:lt.v:~nt elect ic)r). The ~irtiesill turn detcrl~]inc, ht]w thiit Lirr]c will 1><,used. Ir!(li -vidual candidatt<s sittl ply ca~lll<)t “k)uy” time,, This ar-rtingcrnt, rlt c,nharlct, s ptlrty disciplil]e further and rt;-duces the te,]dency ft)r stlcccssful candid:lcy to he ,,functi(]ll of one’s ability to fi~ise morley by whateverIIlea[ls. These arfi~ngen]cnts also Lend t{] [Ilitlinlize the:~dv:int~lg~:s ot” rurlninK :1 nc~~atit,e ctlnlpaigll a~,iir]st {lnirldividu>ll [jpp<]nent..

T(] assllre s{)ll]e objectivity it] IIews c{)vtr;ige, ir]di-\,idu:ll r(,portt.rs art, giv(, n II lot <If irldc,pc,l]dt:nct, irl the(;t,rnl:lll t:lc,ctror)ic nledi:i, witkl the c,xpect:ili<)n thatthey will USC,this irldepc,r)dc.rlct? in :Lprofessi{)tlally res-ponsible rnarlnt:r. StLch repc)rt<,rs {IIS(Jel~joy muchgreater j[d~ terlure than thc:ir Arrlerican <,quiv:ilt, nts.(~cirman parties urldt,rstalld w(?I I that whoever is i,! con-trol todtiy n]:xy be out of power t,<)nl<)rrow. Fears sc!emalnl(jst non-(? xistc,nt i!] (ic:i-rl]:l!l,y that tht, g<)vernrtlentwill >{busc its c(lnl.rol <If the t:lt:ctr[~l>ic rrl<!di:i for c:im-p:iign purpos<s :Irld stll-I>r[)llloti(]rl.

TENDENCIES AND SIMILARITIES

t)rspitt, tht sh:irp dif’lerer]cts irl tbc,ir pt)litic:il piirtypractices atld tht,ir mt:diil sc ttings, the (+erInan aJ1dAmerican systenls st?elxl to bt, n]c)ving down some sirrli-Iar paths, s(]mc, of which m{ly he nlorc partdlelirl~ thiinct]nverginK, but at least they i~r<, not diverging.

111both nations, present, intercsl in g<,vernmcnttd de-cc,ntr:lliz:itillll may rc.fl<,ct curr~nt c,corlc)mic c[]nditi<lnsm{)r(, th:it~ ch:irlk,[,!s in ullderlyirl&, poll tictd v:il[It.H, th]ttl

nutic~rls art> ct)nlirlg t~ut of dc~,p t,cononlic” r~.cc,ssic)ns.When fiscal resources :,,<, SC:I,C<X, all sorts of idc.as ~r(:treconsidered, inclllding gre:itt~r governnlt+nt:ll d~!-ct:ntrt]liz:itiorl. tltjwt,ver, the, b:isic social forces whichetlco[lr:i~ed nl<)re :Irld more: centr;~lization in tht: firstplace h:i~,(, not re:ill.y ab:ited [t rt?nla ins to bt? s(!t:nwhctbt?r tht, decentralization r]lovemc,nt in eitht:r coun-try can sustain itsc 1f after C.c{)n{)mlicrc+covery.

tt(~h;il:lrlvirlg c:ithcr fcd+,r:lli:,txl prc)h:lhly rllc:atls lll(Iv-I]lL, n]or(, r<:s<)urct?s [In d p<)w(:rs t{)w:+rd I<IcL$Igc)v<srrl-ments. The, c,xtc,nl. to which SILCh shifts take, pl:ice incithc, r country depends prim:lrily UP(>II the actions [dstate ~,overnnlents, Ii[)w the states choose to trc~at tbc:irlocal g(]verrllxlents on :1 v:lriety t]f m:itters will kcc,nl.y:iffc.ct how much dec(?[ltr:lliztl(ion tictutd Iy occurs.Withir~ the st:ltc, g{,vt:rn,,lt;nts, the state legisl:lturcsseenl rllost importaljt, particularly in th(: <,xtcnt t<)which th(,.y w:l~lt t.{)continue heavy-handed reg(llati~)n[If ]ocill k,t)v~>rnlnt,tlls, ~,sp(,ci:il Iy in (ierlT1til).y. H (.,w tb{:st;ltc. lt,~islat{lrc,s rc:sp(lnd t<) tht, lt, adc~rsbip OSthc~ir re-

:10 specti VC,~,uvt:rn(>rs LIn d to the c(~rlcerns of their It)ct{i

goverrl!]lt>nts is LIII [Irlsf,ttle:d b(kt cb;~llt:nginK iss”t. inboth [Iations.

Both rt)cirltries :ire rt:corlsideril)K how they distribute,the variotls g[~vernr]lc,rlt:il Ihncti(]rls ~~mong the differt,l)tgovcrnmc~r,t.. III the, [Inite,i St.itcs, this process hasc<,mc: to bc. known as “sorting out.’” It was givel~ a sharpforw,ird thrust by I’resident Rc,{ig:,n’s N(w Fcdcralisnlproposals. The Gcrm~in c{)ncerri is n)t~re subdued at thistinle, but serious qucstic]ns iii-e bc, ing raised about tht+,j<)int sti~te-f<:der>d fclnctic)ns :ind wbetb{~r <II’not theyshould bt, rt,zirr:irlg<:d irl sik,ll]flc:i]lt w:iys. .SorIIc. chtingt, sn]ay be accc)rnpl isbed statutorily, hilt (}thcrs would rc>-quire c(!r]stitt]tion:il amer]dmc,rlt.s. Th<! c(>nlplc>xity andpcjlitic:ll difficulty of this ~jnd(+rttikinK art, r~~co~nizcd in

NOTES . . .

URBAN PLANNING, AFFAIRS,AND POLICIES

. A rather authoritarian planning tradition inWest @rmany influences the layout and op-eration of urban areas, as well as many otheraspects of life. For example, housing construc-tion quality standards are even higher andcostlier than in the U.S. Retail stores are notopen evenings or on Sundays because of oppo-sition from unions and owners. Televisionprogramming is heavily itiuenced by gov-ernments. There are two national channelsand one regional one, and they operate formany fewer hours than in the US.

. In West German urban areas, central-cityboundaries have been extended out to en-compass most surrounding built-up areas.State legislatures did this in the past decadewithout major opposition from the suburbs.This extension permits more coordinated con-trol of land-use developments in fringe areas,and helps reduce the relative fiscal burdens ofcentral-city governments.

. Because central cities influence land-use regulation of surrounding areas, they haveslowed development of outlying shoppingcenters. This plus their excellent public tran-sit systems have kept downtown retail dis-tricts the main centers for retail shopping ineach metropolitan area. Most big cities haveextensive pedestrian malls in the hearts oftheir downtiwns, under which run urbansubway systems. Outside downtowns, thereare serious parking shortages, and cars arejammed onto parkways and along curbseverywhere.

–Anthony Downs

66 The American concernwith altering current fiscalinterrelationships seems drivenby necessity; the Germaninterest seems more motivatedby ideological considerations.Nonetheless, the issue is commonto both and changes seem in the

S. Kenneth H(jwarli is A CIR’s Executi[]eDirector.

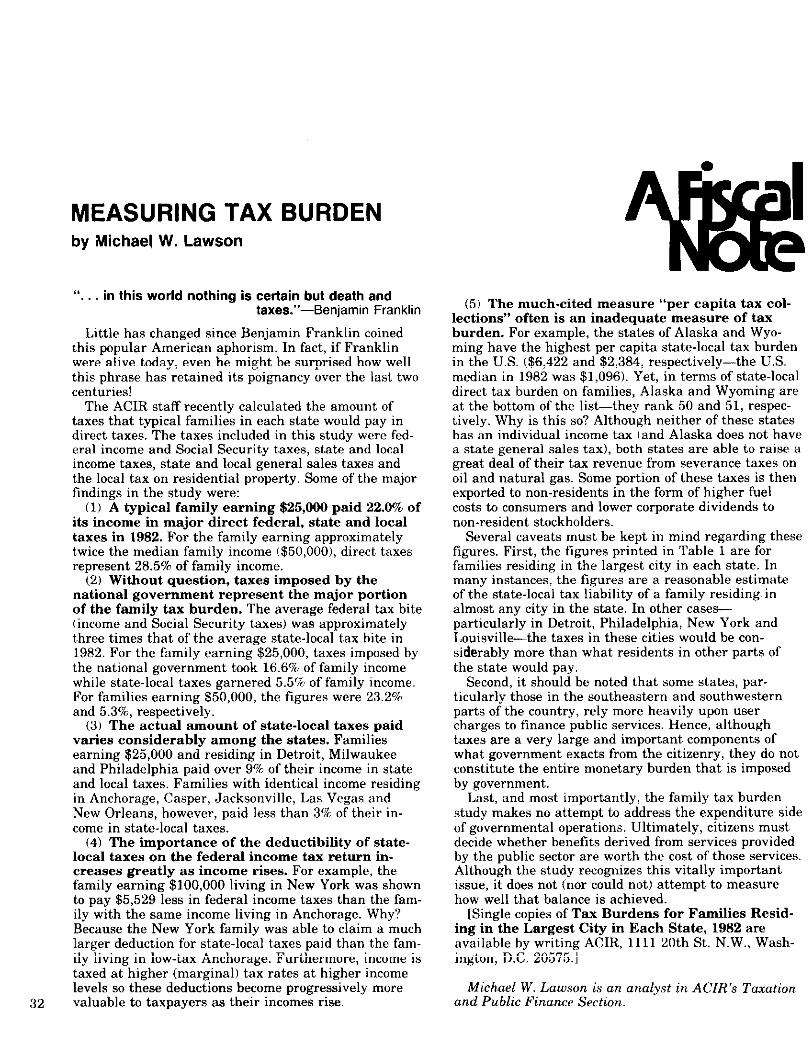

MEASURING TAX BURDENby Michael W. Lawson

,,. . . in this world nothing is certain but death andtsxes.’’—Benjamin Franklin

Little has changed since Benjamin Franklin coinedthis popular American aphorism. In fact, if Franklinwere alive today, even he might be surprised how wellthis phrase has retained its poignancy over the last twocenturies!

The ACIR staff recently calculated the amount oftaxes that typical families in f>ach state would pay indirect taxes. The taxes included in this study were fed-eral income and Social Security taxes, state and localincome taxes, state and local general sales taxes andthe local tax on residential praperty. Some of the majorfindings in the study were:

(1) Atypical family earning $25,000 paid 22. O%,ofits income in major direct federal, state and localtaxes in 1982. Forthefamily earning approximatelytwice the median family income ($50,000 ), direct taxesrepresent 28.57. of family income.

(2) Without question, taxes imposed by thenational government represent the major portionof the fcmily tax burden. The average federal tax bite(income and Social Security taxes) was approximatelythree times that of the average state-local tax bite in1982. For the family earning $25,000, taxes imposed bythe national government tools 16.6% of family incomewhile state-local taxes garnerf>d 5.570 of family income.For families earning $50,000, the figures were 23.2%and 5.3%, respectively.

(3) The actual amount of state-local taxes paidvaries considerably among the states. Familiesearning $25,000 and residing in Detroit, Milwaukeeand Philadelphia paid over 9%, of their income in stateand local taxes, Families with identical income residingin Anchorage, Casper, Jacksonville, Las Vegas :~ndNew Orleans, however, paid less than 3’% of their in-come in state-local taxes.

(4) The importance of the deductibility of state-Iocal taxes on the federal income tax return in-creases greatly as income rises. For example, thefamily earning $100,000 living in New York was shownto pay $5,529 less in federal income taxes than the fam-ily with the same income living in Anchorage. Whyt~Because the New York family was able to claim a muchlarger deduction for state-local taxes paid than the fam-ily living in low-tax Anchorage. Furthermore, income istaxed at higher (marginal) tax rates at higher incomelevels so these deductions became progressively more

32 valuable to taxpayers as their incomes rise.

(5) The much-cited measure “per capita tax col-lections” often is an inadequate measure of taxburden. For example, the states of Alaska and Wyo-ming have the highest per capita state-local tax burdenin the U.S. ($6,422 and $2,384, respectively—the U.S.median in 1982 was $1,096). Yet, in terms of state-localdirect tax burden on families, Alaska and Wyoming areat the bottom of the liskthey rank 50 and 51, respec-tively. Why is this so’? Although neither of these stateshas an individual income t:~x (and Alaska does not havea state general sales tax), both states are able to raise agreat deal of their tax revenue from severance taxes onoil and natural gas. Some portion of these taxes is thenexported to non-residents in the form of higher fuelcosts b consumers and lower carporate dividends tonon-resident stockholders.

Several caveats must be kept in mind regarding thesefigures. First, the figures printed in Table 1 are forfamilies residing in the largest city in each state. Inmany instances, the figures are a reasonable estimateof the state-local tax liability of a family residing. inalmost any city in the state. In other cases-particularly in Detroit, Philadelphia, New York andLouisville-the taxes in these cities would he con-siderably more than what residents in other parts ofthe state would pay.

Second, it should be noted that some states, par-ticularly those in the southeastern and southwesternparts of the country, rely more heavily upon usercharges to finance public s{)rvices. Hence, althoughtaxes are a very large and important components ofwhat government exacts from the citizenry, they do notconstitute the entire monetary burden that is imposedby government.

Last, and most importantly, the family tax burdenstudy makes no attempt to address the expenditure sideof governmental operations. Ultimately, citizens mustdecide whether benefits derived from services providedby the public sector are worth the cost of those services.Although the study recognizes this vitally importantissue, it does not (nor could not) attempt to measurehow well that balance is achieved.

[Single copies of Tax Burdens for Families Resid-ing in the Largest City in Each State, 1982 areavailable by writing ACIR, 1111 20th St. N. W., Wash-ington, DC. 20575. ]

Michael W. Lawson is an arlalyst in ACIR’S Tmationand Public Finance Section.

Table 1

A Comparison of Direct Tax Burdens for a Married Couple with Two Dependenta, Locatedin the Lsraest Citv in Each State. for Selacted Federal and StateLocal Taxea. 1982.~––. –,

As a Percentage of Income

City and Stateby Re ion

iU.S. edianNew England

Bridgepofl, CTPottland, MEBoston, MAManchester, NHProvidence, RIBurlington, ~

MideastWlmington, DEDist. of ColumbiaBaltimore, MDNewark, NJNew York, NYPhiladelphia, PA

Great LakesChicago, ILIndianapolis, INDetroit, MlCleveland, OHMilwaukee. WI

PlainaDes Moines, 1AWchita, KSMinneapolis, MNSt. Louis, MOOmaha, NEFargo, NDSioux Falls, SD

SoutheastBirmingham, ALtinle Rock, ARJacksonville, FLAtlanta, GALouisville, KYNew Orleans, LAJackson, MSCharlotle, NCColumbia, SCMemphis, TNNorfolk, VACharleston, WV

SouthwastPhoenix, AZAlbuquerque, NMOklahoma City, OKHouston, TX

Rocky MountainDenver, COBoise, IDBillings, MTSalt Lake City, UTCasper, WY

FarWeatLos Angeles, CALas Vegas, NVPotiland, ORSeattle, WAAnchorage, AKHonolulu. HI

Income Level: $25,000 - Income Level: $50,000Total for Total Total Total for Total TotalSelectad Fedaral Sta;~x~~cal Selectad Faderal State-Local

Taxaa Taxes’ Taxaa Taxee”22.O1”A

Taxes16,56”A 5.45”/0 28.46% 23.21”/- 5.25°h

22.3222.7524.2S21.3323.4322.96

21.7723.7223.9622.7624.4625.10

22.8621,5626.1723,0625.41

23.5820.9622.7S21.5622.1820,4721.86

21.9121.3819.7122.0223,0719,5620.4022,1421.24211222.3421.06

21.4420.4120.4121.26

21.3022.6121.3323.1219.50

22.0119,5724.4420.9619,5424.03

16.4716.3415.9016.7316.1216.29

16.6016,0315.9616.3415.6515,66

16.2916.6415.3716.2515.59

16.0716.8216.3416.6416,4716.9516.60

16,5616.7317.1716.5616,2517,2217.0016,5116,7816.7816,4716,62

16.6916.9517.0016.73

16.7316.3416.7316.2017.26

16.5617,2215,6516.S217.2615.96

5.66 27.62 23.716.41 29.72 22.358.38 29.73 22.434,60 26.96 24.147.31 29.71 22.356,66 29.46 22.46

5.177.707.976.428.619.42

29.3630.2930.0426.1931.4630.47

22.6222.0022.1923.4021.3021.68

6.56 28.45 23.254.92 27.89 23.60

10.80 31.30 21.416.81 29.27 22.709.82 30.97 21.61

7.504.146.444.915.723.525.26

5.354.652.545.466.822.373.405,634.464.355.874.24

4.753.463.414.53

4.576.464.606.922.24

5.452.358.584.142.288.04

29.6127.9931.0026.2728.8327.2527.49

28.3328.6626,4829.1329.4326.9427.6529.3028.9027.4128.9228,15

22.5023.4821.6123.3222.9723.9323.79

23,3223.0924.4522.7822.5824.1823.7522.7022.9323.8722.9323.40

26.48 23.2127,58 23.7528.16 23.4027.52 23.79

26.0829.5628.2229.3026.19

29.2426.2230.5627.0426.0930.39

23.4422.5023,3622.6224.61

22.7424.8121.8424.1024.8921.96

3.917.387.302.827.366.96

6.748.497.854.76

10.178.59

5.204.309.886.579.36

7.114.519.394,945.863.323.70

5.015.592.026.356.852.753.906.605.973.545.984.75

5.253.634.753.73

4.647.054.866681.58

6.501,618.722.931.408.43

.The reason that federal lax liaMtiUesare not the sama for all states is b,cause stale and local lwes have been deducted from taxable incomein the federal income 18xtalc.ladona. Taxes included are federal income and Social Security taxes, S!ate.local income and general sales taxesand the local properly tax

Source: ACIR 33

vi

34

Dear Reader

A revolution in the provision ofpublic goods and services is takingplace throughout the United States,Governments contracting with privateorganizations, cooperative agreementsamong jurisdictions and provision ofmunicipal services by neighborhoodgroups are all variations on a singletheme New ways of producing publicgoods and services are here to stay.

A decade ago conventional wisdomheld that the best way to provide p“b-Iic services was through existing pub-lic agencies. The last ten years, how-ever, have seen cutbacks in publicfunding (encouraging an intensifiedsearch for efficiency) as well as agrowing body of successful experiencewith innovative means of providinggovernment services.