November 5, 2013 Integrated Asset Management Solutions for Healthcare Organizations Sheila Noonan Senior Client Advisor J.P. Morgan Asset Management Karin Franceries Head of U.S. Strategy Group J.P. Morgan Asset Management FOR INSTITUTIONAL USE ONLY – NOT FOR PUBLIC DISTRIBUTION

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

November 5, 2013

Integrated Asset Management Solutions for

Healthcare Organizations

Sheila Noonan

Senior Client Advisor

J.P. Morgan Asset Management

Karin Franceries

Head of U.S. Strategy Group

J.P. Morgan Asset Management

FOR INSTITUTIONAL USE ONLY – NOT FOR PUBLIC DISTRIBUTION

Identify investment trends and challenges in healthcare

Explore the funded status of today’s plans

Discuss and explore an underfunded pension’s basic objective

Why should pension funds worry about interest rate risk today?

Key takeaways from our discussions with plans that are on a de-risking path

Learning Objectives

2 FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Healthcare organizations face a challenging environment in a

complex world

3

Greater focus on liabilities

DB funding status and

increased focus on DC

solutions

Increased complexity of

investment pools

Increased reliance on

investment income

Increased focus on tail /

event risk

Cost of capital and

maintaining financial

ratios

Pressure on

operating margins

Demand for greater

transparency from

rating agencies

Impact of Affordable Care

Act

Reduced

reimbursement rates

Increased regulations and

reporting requirements Increased competition

and M&A activity

Impact on profitability Impact on investment pools

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

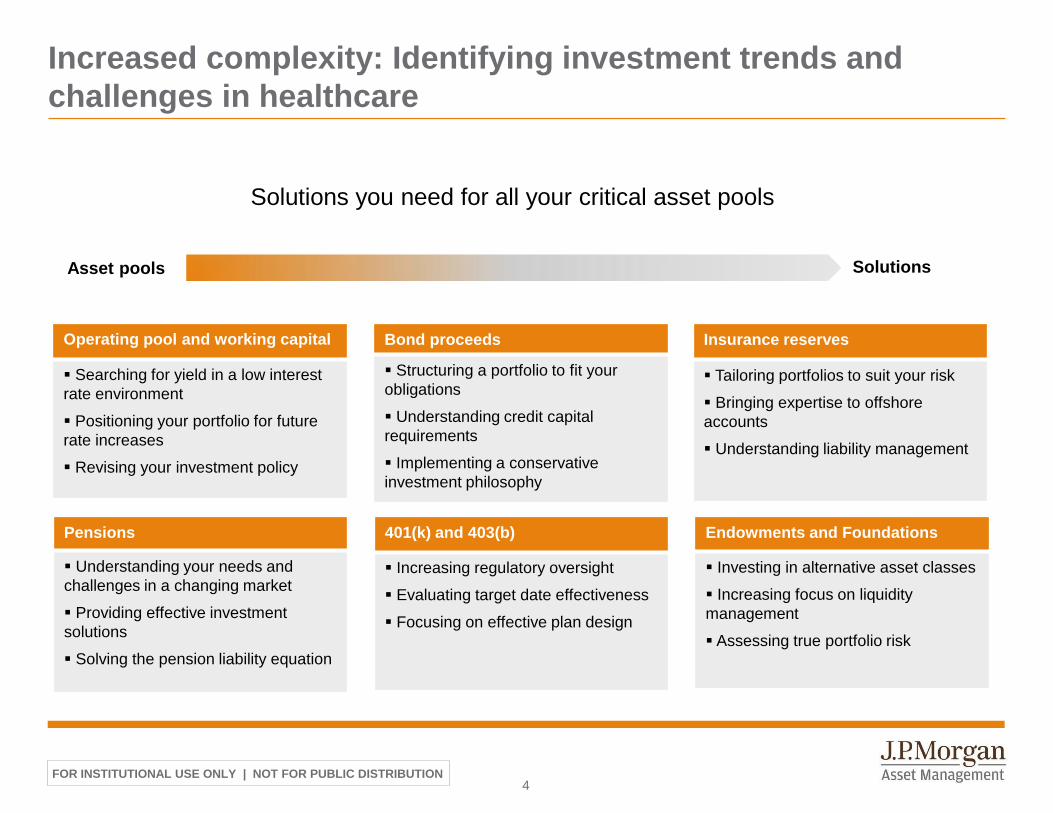

Increased complexity: Identifying investment trends and

challenges in healthcare

4

Solutions you need for all your critical asset pools

Operating pool and working capital

Searching for yield in a low interest

rate environment

Positioning your portfolio for future

rate increases

Revising your investment policy

Bond proceeds

Structuring a portfolio to fit your

obligations

Understanding credit capital

requirements

Implementing a conservative

investment philosophy

Insurance reserves

Tailoring portfolios to suit your risk

Bringing expertise to offshore

accounts

Understanding liability management

Endowments and Foundations

Investing in alternative asset classes

Increasing focus on liquidity

management

Assessing true portfolio risk

401(k) and 403(b)

Increasing regulatory oversight

Evaluating target date effectiveness

Focusing on effective plan design

Pensions

Understanding your needs and

challenges in a changing market

Providing effective investment

solutions

Solving the pension liability equation

Asset pools Solutions

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Pension

Promised benefits

Pension asset

allocation

Pension funded status

Contributions

Sponsor’s financial

statements

Sponsor’s health

Pension

Promised benefits

Pension asset

allocation

Pension funded status

Contributions

Sponsor’s financial

statements

Sponsor’s health

Pension

Promised benefits

Pension asset

allocation

Pension funded status

Contributions

Sponsor’s financial

statements

Sponsor’s health

Pension

Promised benefits

Pension asset

allocation

Pension funded status

Contributions

Sponsor’s financial

statements

Sponsor’s health

Pension

Promised benefits

Pension asset

allocation

Pension funded status

Contributions

Sponsor’s financial

statements

Sponsor’s health

Pension

Promised benefits

Pension asset

allocation

Pension funded status

Contributions

Sponsor’s financial

statements

Sponsor’s health

The Pension Merry-Go-Round:

Pensions and sponsors are intimately related

5

Source: JP Morgan Asset Management. For illustrative purposes only.

Rating agencies

FASB

HR & Unions

Creditors

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION 6

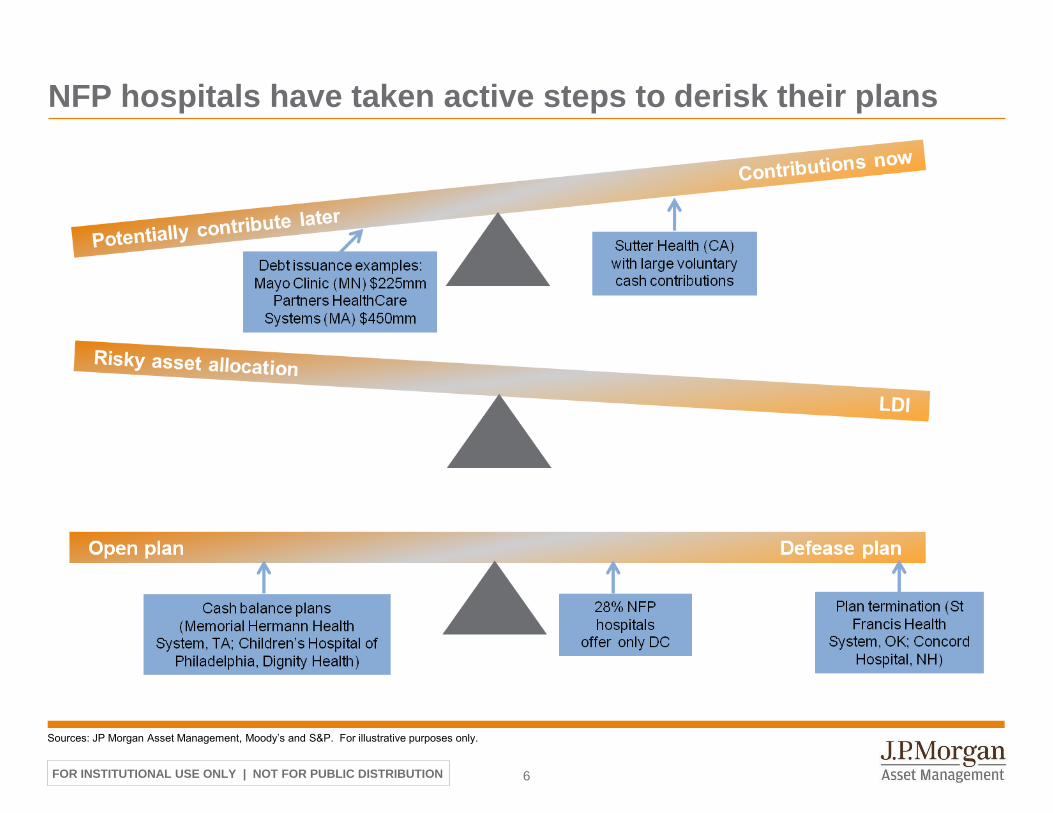

NFP hospitals have taken active steps to derisk their plans

Sources: JP Morgan Asset Management, Moody’s and S&P. For illustrative purposes only.

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

… And while the picture is rosier today than 9 months ago,

plans are on average underfunded

Deepa Patel. “Top seven not-for-profit hospital risk mitigation strategies for rising pension burdens” May 30, 2013. Standard & Poor’s. Liz Sweeney. “Low discount rates hurt pension funding in the U.S.

not-for-profit health care sector in 2012.” April 22, 2013. Among top 10 largest DB plans, median funded status fell to 78% in 2012 vs. 85% in 2011 (ABO, FASB, Moody’s)

72% of rated non-profit healthcare organizations offer DB pensions (Moody’s), with contributions dragging 15% of

hospital cash flows (2012 EBIDA ratio)

Median funded status has finally increased: at 82% in 3Q13, it is up from 69% in 2012, thanks to strong equity

performance and discount rate increase

Contribution pressure likely to have decreased thanks to MAP-21 and improved funded status

7

90%

81% 70% 72% 73% 69% 82%

2007 2008 2009 2010 2011 2012 Sept. '13 Est.

Fu

nd

ed

Sta

tus

(%

)

Year

80%

Not-For-Profit Hospitals / Health Systems Median Funded Status

Standard & Poor’s. “Low discount rates hurt pension funding in the U.S. not-for-profit health care sector in 2012.” April 22, 2013. Source: J.P. Morgan Asset Management,

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION 8

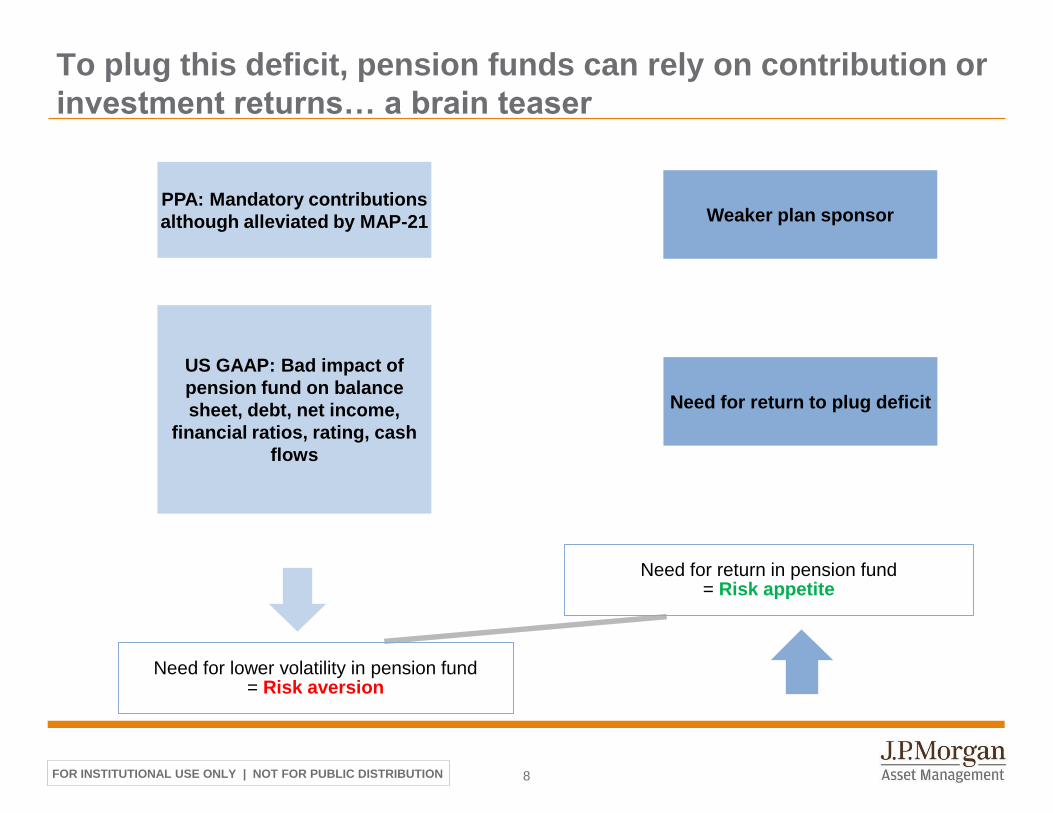

To plug this deficit, pension funds can rely on contribution or

investment returns… a brain teaser

PPA: Mandatory contributions

although alleviated by MAP-21

US GAAP: Bad impact of

pension fund on balance

sheet, debt, net income,

financial ratios, rating, cash

flows

Weaker plan sponsor

Need for return to plug deficit

Need for return in pension fund = Risk appetite

Need for lower volatility in pension fund = Risk aversion

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION 9

What is an underfunded pension’s basic objective?

ASSETS need to exceed LIABILITIES

LIABILITY values are driven by BONDS

ASSET GROWTH needs to exceed BOND RETURNS

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Based on the view, the story can be a little different...

But, the risk is in the eye of the beholder

10

0

20

40

60

80

100

120

140

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Rebased to 100 on 01/01/07 Pension Assets (S&P500)

-600

-400

-200

0

200

400

600

800

1000

1200

1400

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Rebased to 100 on 01/01/07 Pension Assets & Deficit (S&P500)

CFO (AL view):

Deficit vol. of 80% CIO (asset only) view:

Asset vol. of 14%

Source: JP Morgan Asset Management. For illustrative purposes only.

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

2012 deficits were still worse than in 2008 despite a TRILLION

dollars of contributions & investment returns over the last 4 years

11

Source: J.P.Morgan Asset Management Strategy Group, Bloomberg and Barclays, Barclays Live, chart data as of 12/31/2012. Funded status update as of 5/31/2013, excludes service cost,

contributions and benefit payments.

Russell 3000 combined deficit progression over the last 4 years, in dollars

188bn (+14%)

82bn

261bn

177bn (+12%)

84bn

216bn

79bn (+5%)

89bn

290bn

186bn (+11%)

90bn

383bn

Dec 2009:

$384bn deficit

80% funded

Dec 2012:

$554bn deficit

77% funded

Dec 2008:

$392bn deficit

78% funded

Dec 2011:

$461bn deficit

78% funded

Dec 2010:

$339bn deficit

82% funded

At $568 billion, the year-end 2012 deficit is greater than in January 2009, despite sizable contributions and

realized returns significantly exceeding expectations

Over the multi-year period, assets grew by $1 trillion dollars, yet this gain was essentially wiped out by

the simultaneous 260-bp decrease in discount rates

Funded status has in fact improved to 86% as of the end of May 2013

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION 12

The risks faced by the pension fund are ultimately borne by

the sponsor

The main risks faced by a typical pension plan are:

Pension Risks

Market risks Interest rate risk

Other investment risk

Both assets and liabilities are sensitive to the changes in long-

term interest rates (duration)

Plans are typically net-short duration (liabilities have much

longer duration than assets) so falling rates are bad for plans

funded status

The value of a pension fund’s investments will fluctuate with

the market and asset allocation decisions

Longevity risk If improvements in life expectancy outpace actuarial

assumptions, it will lead to higher draws on the pension

Sponsor risk Especially in periods of crisis when asset underperformance

might coincide with difficulties at plan sponsor level

Liquidity risk Benefit payments may be larger than contributions

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION 13

Why should pension funds worry about interest rate risk

today?

Short rates are at Zero, discount rates are NOT.

Discount rates are the sum of Treasury rates and credit spreads

– Pressure for Treasuries to remain flat (under Fed pressure)

– Credit spreads are higher than long term averages

Given that credit spreads and equities tend to be positively correlated:

- If equity markets perform well, credit spreads could tighten (and liability increase) => funded status ?

- If equity markets perform badly, credit spreads could widen (and liability decrease) => funded status ?

Given that pension funds are in deficits today, a tiny movement in rates can wipe out increase in growth assets:

The question is more: how to get duration from fixed income and return from growth assets ?

For a typical plan, the impact of a 10% increase in growth assets on the funded status is wiped out

by a 50bp decrease in discount rates

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

De-risking thoughts

We describe here key takeaways from our discussions with plans that are on a de-risking path

Dynamic de-risking alone does not necessarily reduce risk. It is crucial to distinguish the asset allocation decision

from the duration hedge decision

– The asset allocation decision drives expected contributions

We often recommend clients, who want to de-risk. To consider increasing their risky asset allocation

– The duration decision addresses downside contributions

We systematically recommend clients to consider increasing their duration hedge ratio

Systematic de-risking shortens the timeframe for pension funds

– An allocation solely focused on long term capital market assumptions is misaligned with the de-risking timeframe;

“cycle aware” changes can improve it

– The management of a de-risking plan needs to be quick and agile

The de-risking path is non-linear

– The tradeoff between risk and return changes with the funding status

– The de-risking decision may or may not be automated

– A significant surplus could change the risk/return tradeoffs for a sponsor who has the ability to use this surplus

14

Opinions, estimates, forecasts, projections and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to

change without notice. There can be no guarantee they will be met.

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Sample client pension exposure

15

Plan funded

status

Factors

driving asset

decision

Sponsor

circumstances

Plan liability

profile

Regulatory

and

accounting

framework

Capital

market

expectations

High contributions

Contributions/Assets: 16%

0% 5% 10% 15% 20% 25%

Contributions / Assets

Top quartile

Bottom quartile

Median

0% 5% 10% 15%

Benefit Payments/Assets

Above median drag on liquidity

Benefit Payments / Assets: 8%

Closed plan

Service cost/PBO: 0%

0.0% 2.0% 4.0% 6.0% 8.0%

Service cost / PBO

High return expectations

Expected return: 8%

4.0% 5.0% 6.0% 7.0% 8.0% 9.0%

Expected return

Cleveland Clinic 30% 50% 70% 90% 110%

Funding ratio

Underfunded

Funding Ratio: 69%

Source: Sample client, 2012 company reports/10-Ks; J.P. Morgan Asset Management. For illustrative purposes only. The bar charts represent the distributions of the Russell 3000 plans, based on

reported defined benefit assets. Minimums and maximums are represented by the 5th and 95th percentiles in each category. PBO/Market Cap is pre-tax. Liability proxied with Barclays Long

Corporate A or Higher Index.

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Discount rate

92% 4.1% 4.3% 4.6% 4.8% 5.1% 5.3% 5.6%

Gro

wth

Assets

Retu

rn

-20% 70% 72% 73% 75% 76% 78% 80%

-15% 73% 75% 76% 78% 79% 81% 83%

-10% 76% 77% 79% 81% 82% 84% 86%

-5% 79% 80% 82% 84% 85% 87% 90%

0% 81% 83% 85% 86% 88% 90% 93%

5% 84% 86% 87% 89% 91% 94% 96%

10% 87% 88% 90% 92% 94% 97% 99%

15% 89% 91% 93% 95% 97% 100% 102%

20% 92% 94% 96% 98% 100% 103% 106%

Looking towards 2013

Sensitivity analysis of the 12/31/2013 funding ratio, based on a range of discount rates and

return assumptions

Shaded areas correspond to less likely outcomes, as they would require a negative correlation between equities and spreads, which goes contrary to what we have seen historically. July 31, 2013

estimate is based solely on mark to market of assets and liabilities and does not account for contributions, service cost, or benefit payments; as of July 31, 2013. Estimated funding ratio as of 7/31/2013,

assuming 29% fixed income, 51% equities, and the remainder in alternatives. Liability proxied with Barclays Long Corporate A or Higher Index. Source: J.P.Morgan Asset Management Strategy Group.

To read the table: start from 86% (2013) funded status assuming discount rates stay flat at 4.8% and growth assets return 0%. To reach 90% by 2013 the fund would need discount rates to decrease by

25bp (move 1 column to the left) and growth assets to return 15% (move 3 rows below).

We estimate that you are 81% funded as of the end of July 2013

With this starting point, your plan would be 86% funded at year-end 2013, even if discount rates and growth

assets are flat in 2013

For example, to improve funded status to 90%, the plan would need growth assets to return 10%

For funded status to be 97%, need BOTH 10% increase in growth assets AND a discount rate increase

Positive correlation between equity returns and credit spread tightening makes this scenario less likely

16

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

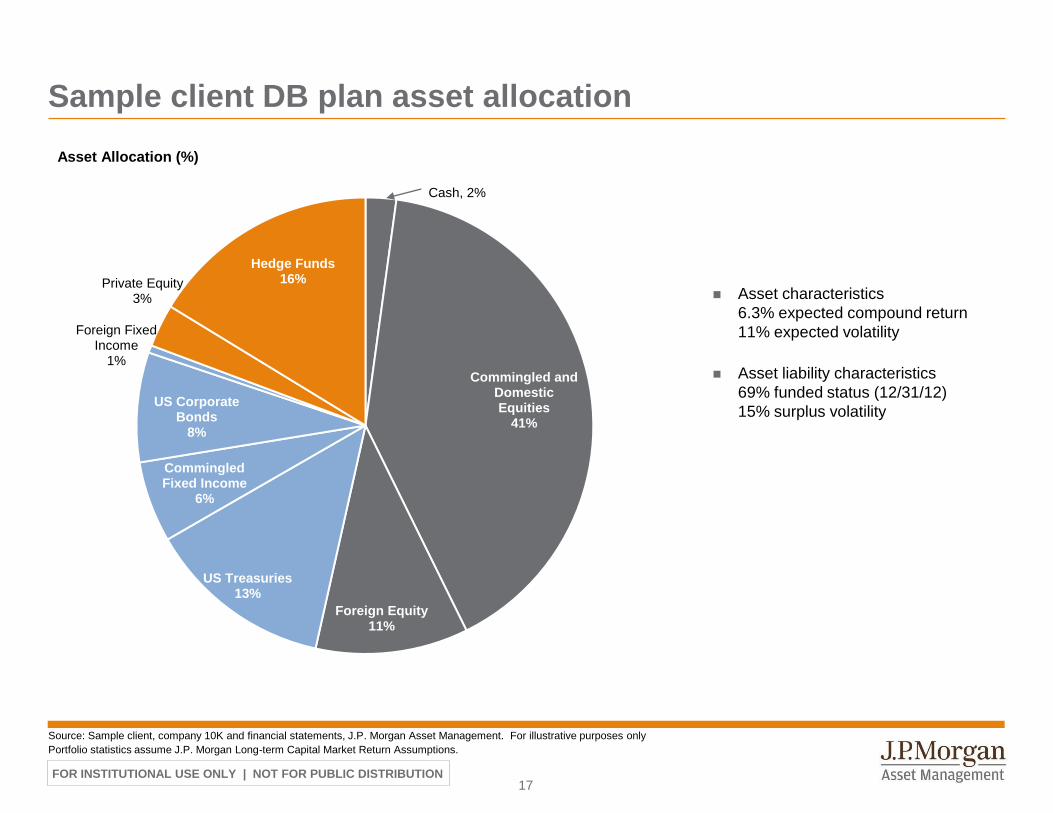

Sample client DB plan asset allocation

Cash, 2%

Commingled and Domestic Equities

41%

Foreign Equity 11%

US Treasuries 13%

Commingled Fixed Income

6%

US Corporate Bonds

8%

Foreign Fixed Income

1%

Private Equity 3%

Hedge Funds 16%

Asset characteristics

6.3% expected compound return

11% expected volatility

Asset liability characteristics

69% funded status (12/31/12)

15% surplus volatility

17

Source: Sample client, company 10K and financial statements, J.P. Morgan Asset Management. For illustrative purposes only

Portfolio statistics assume J.P. Morgan Long-term Capital Market Return Assumptions.

Asset Allocation (%)

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

14.3

11

1.5

15

0

5

10

15

20

25

30

Interest rate Equity Alternatives Diversification Total

Sta

nd

ard

de

via

tio

n o

ve

r 1

ye

ar

(%)

0.7

10

1.5 (0.9)

11

0

5

10

15

20

25

30

Fixed income Equity Alternatives Diversification Total

Sta

nd

ard

de

via

tio

n o

ve

r 1

ye

ar

(%)

Most of the asset risk comes from equities, but most funded

status risk comes from rate exposure, through liabilities

Sample client’s asset and liability risk decomposition analysis

Decomposition of the asset risk

Source: J.P. Morgan, based on J.P. Morgan Capital Market Assumptions, with observed 10-yr standard deviations and correlations

Asset classes used based on data provided by client X. For illustrative purposes only.

Decomposition of the deficit risk

(12)

18

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

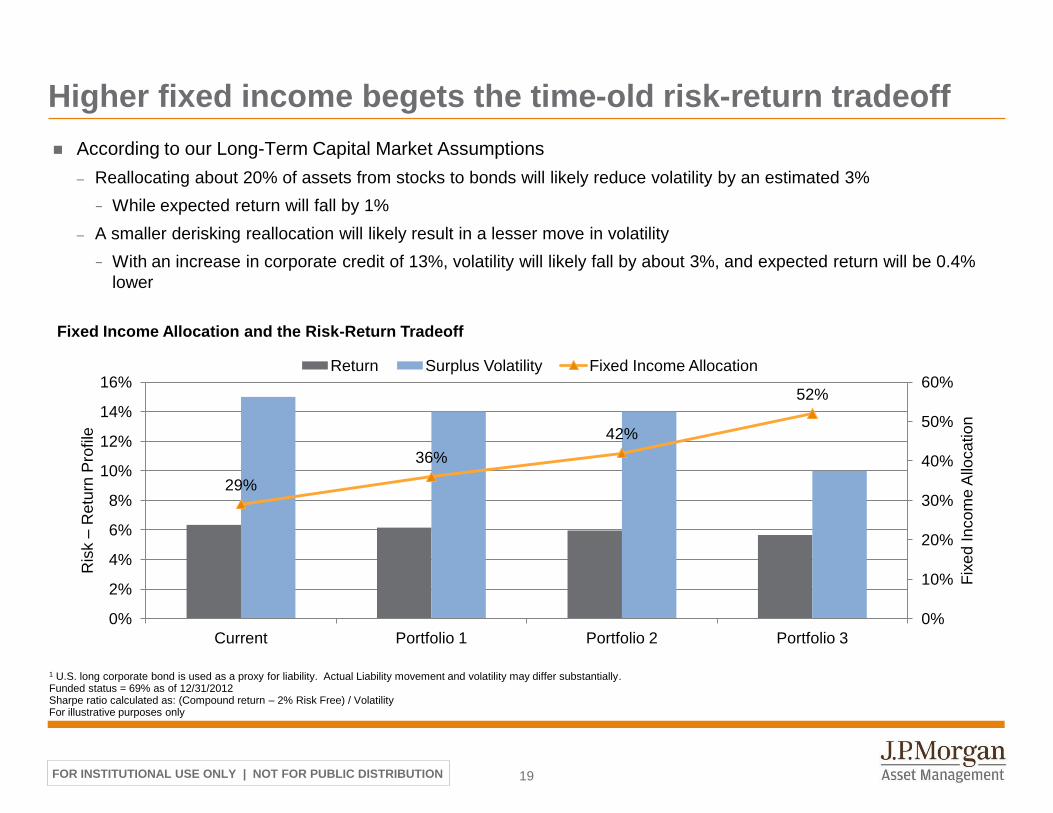

Higher fixed income begets the time-old risk-return tradeoff

19

1 U.S. long corporate bond is used as a proxy for liability. Actual Liability movement and volatility may differ substantially. Funded status = 69% as of 12/31/2012 Sharpe ratio calculated as: (Compound return – 2% Risk Free) / Volatility For illustrative purposes only

29%

36%

42%

52%

0%

10%

20%

30%

40%

50%

60%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Current Portfolio 1 Portfolio 2 Portfolio 3

Fix

ed

In

co

me

Allo

ca

tio

n

Ris

k –

Re

turn

Pro

file

Fixed Income Allocation and the Risk-Return Tradeoff

Return Surplus Volatility Fixed Income Allocation

According to our Long-Term Capital Market Assumptions

– Reallocating about 20% of assets from stocks to bonds will likely reduce volatility by an estimated 3%

− While expected return will fall by 1%

– A smaller derisking reallocation will likely result in a lesser move in volatility

− With an increase in corporate credit of 13%, volatility will likely fall by about 3%, and expected return will be 0.4%

lower

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

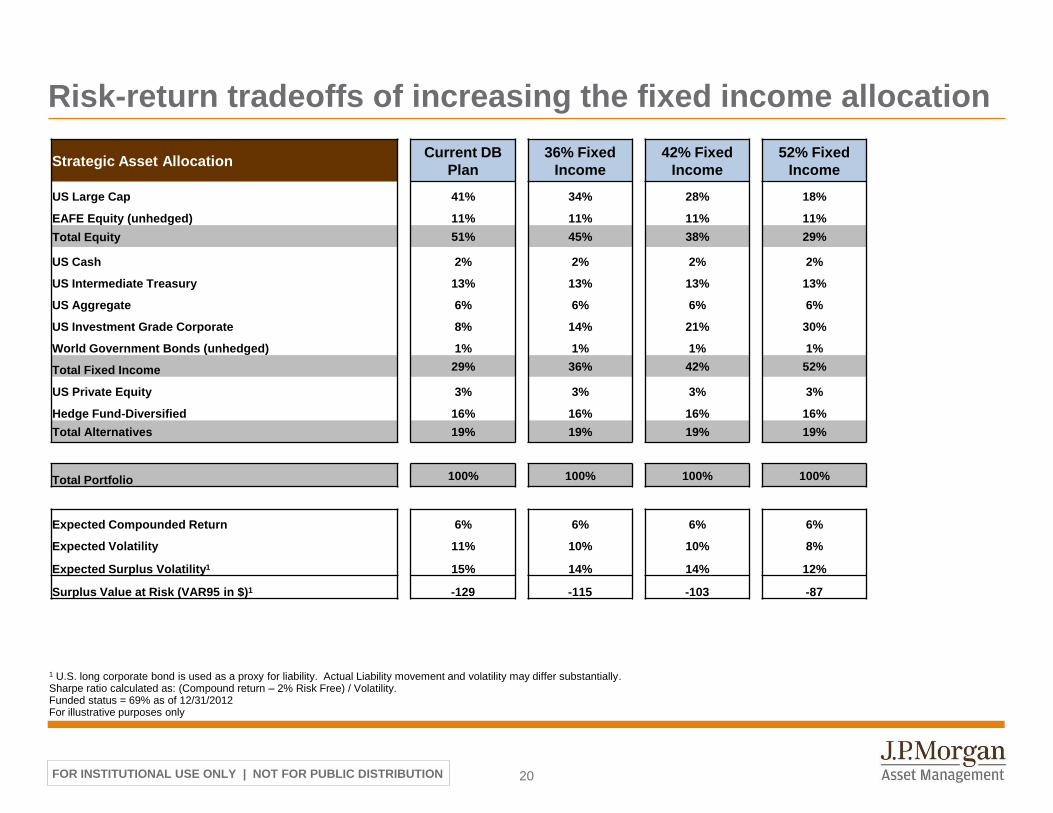

Risk-return tradeoffs of increasing the fixed income allocation

20

Strategic Asset Allocation Current DB

Plan

36% Fixed

Income

42% Fixed

Income

52% Fixed

Income

US Large Cap 41% 34% 28% 18%

EAFE Equity (unhedged) 11% 11% 11% 11%

Total Equity 51% 45% 38% 29%

US Cash 2% 2% 2% 2%

US Intermediate Treasury 13% 13% 13% 13%

US Aggregate 6% 6% 6% 6%

US Investment Grade Corporate 8% 14% 21% 30%

World Government Bonds (unhedged) 1% 1% 1% 1%

Total Fixed Income 29% 36% 42% 52%

US Private Equity 3% 3% 3% 3%

Hedge Fund-Diversified 16% 16% 16% 16%

Total Alternatives 19% 19% 19% 19%

Total Portfolio 100% 100% 100% 100%

Expected Compounded Return 6% 6% 6% 6%

Expected Volatility 11% 10% 10% 8%

Expected Surplus Volatility1 15% 14% 14% 12%

Surplus Value at Risk (VAR95 in $)1 -129 -115 -103 -87

1 U.S. long corporate bond is used as a proxy for liability. Actual Liability movement and volatility may differ substantially. Sharpe ratio calculated as: (Compound return – 2% Risk Free) / Volatility. Funded status = 69% as of 12/31/2012 For illustrative purposes only

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

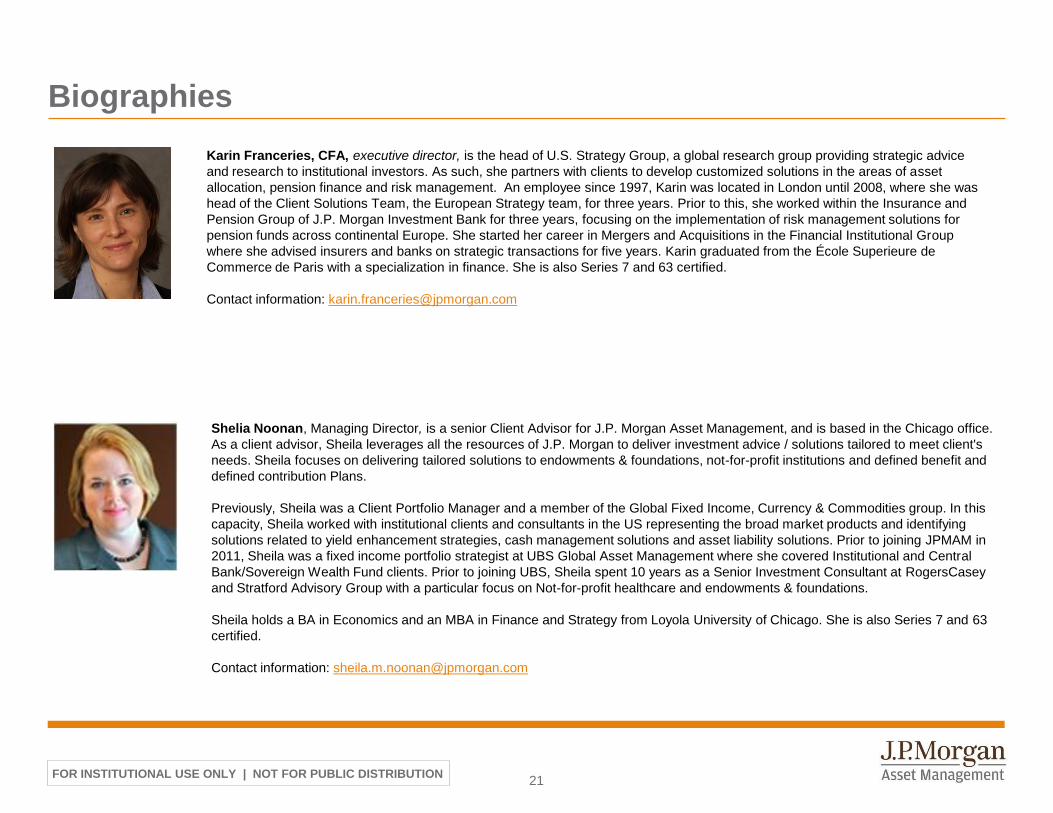

Biographies

21

Karin Franceries, CFA, executive director, is the head of U.S. Strategy Group, a global research group providing strategic advice

and research to institutional investors. As such, she partners with clients to develop customized solutions in the areas of asset

allocation, pension finance and risk management. An employee since 1997, Karin was located in London until 2008, where she was

head of the Client Solutions Team, the European Strategy team, for three years. Prior to this, she worked within the Insurance and

Pension Group of J.P. Morgan Investment Bank for three years, focusing on the implementation of risk management solutions for

pension funds across continental Europe. She started her career in Mergers and Acquisitions in the Financial Institutional Group

where she advised insurers and banks on strategic transactions for five years. Karin graduated from the École Superieure de

Commerce de Paris with a specialization in finance. She is also Series 7 and 63 certified.

Contact information: [email protected]

Shelia Noonan, Managing Director, is a senior Client Advisor for J.P. Morgan Asset Management, and is based in the Chicago office.

As a client advisor, Sheila leverages all the resources of J.P. Morgan to deliver investment advice / solutions tailored to meet client's

needs. Sheila focuses on delivering tailored solutions to endowments & foundations, not-for-profit institutions and defined benefit and

defined contribution Plans.

Previously, Sheila was a Client Portfolio Manager and a member of the Global Fixed Income, Currency & Commodities group. In this

capacity, Sheila worked with institutional clients and consultants in the US representing the broad market products and identifying

solutions related to yield enhancement strategies, cash management solutions and asset liability solutions. Prior to joining JPMAM in

2011, Sheila was a fixed income portfolio strategist at UBS Global Asset Management where she covered Institutional and Central

Bank/Sovereign Wealth Fund clients. Prior to joining UBS, Sheila spent 10 years as a Senior Investment Consultant at RogersCasey

and Stratford Advisory Group with a particular focus on Not-for-profit healthcare and endowments & foundations.

Sheila holds a BA in Economics and an MBA in Finance and Strategy from Loyola University of Chicago. She is also Series 7 and 63

certified.

Contact information: [email protected]

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION 22

J.P. Morgan Asset Management This document is intended solely to report on various investment views held by J.P. Morgan Asset Management. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. We believe the information provided here is reliable but should not be assumed to be accurate or complete. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. Indices do not include fees or operating expenses and are not available for actual investment. The information contained herein employs proprietary projections of expected returns as well as estimates of their future volatility. The relative relationships and forecasts contained herein are based upon proprietary research and are developed through analysis of historical data and capital markets theory. These estimates have certain inherent limitations, and unlike an actual performance record, they do not reflect actual trading, liquidity constraints, fees or other costs. References to future net returns are not promises or even estimates of actual returns a client portfolio may achieve. The forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. The value of investments and the income from them may fluctuate and your investment is not guaranteed. Past performance is no guarantee of future results. Please note current performance may be higher or lower than the performance data shown. Please note that investments in foreign markets are subject to special currency, political, and economic risks. Exchange rates may cause the value of underlying overseas investments to go down or up. Investments in emerging markets may be more volatile than other markets and the risk to your capital is therefore greater. Also, the economic and political situations may be more volatile than in established economies and these may adversely influence the value of investments made . All case studies are shown for illustrative purposes only and should not be relied upon as advice or interpreted as a recommendation. Results shown are not meant to be representative of actual investment results. Any securities mentioned throughout the presentation are shown for illustrative purposes only and should not be interpreted as recommendations to buy or sell. A full list of firm recommendations for the past year is available upon request. The value of investments and the income from them may fluctuate and your investment is not guaranteed. Past performance is no guarantee of future results. Please note current performance may be higher or lower than the performance data shown. Please note that investments in foreign markets are subject to special currency, political, and economic risks. Exchange rates may cause the value of underlying overseas investments to go down or up. Investments in emerging markets may be more volatile than other markets and the risk to your capital is therefore greater. Also, the economic and political situations may be more volatile than in established economies and these may adversely influence the value of investments made IRS Circular 230 Disclosure: JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or commendation by anyone unaffiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties. J.P. Morgan Asset Management is the marketing name for the asset management businesses of JPMorgan Chase & Co. Those businesses include, but are not limited to, J.P. Morgan Investment Management Inc., Security Capital Research & Management Incorporated and J.P. Morgan Alternative Asset Management, Inc. Copyright © 2013 JPMorgan Chase & Co. All rights reserved.

Related Documents