International Journal of Economics and Empirical Research http://www.tesdo.org/Publication.aspx - 465 - Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan Ahsen Mukhtar a , Muhammad Asif a , Ghamz-e-Ali Siyal a , Khalid Zaman a, a COMSATS Institute of Information and Technology, Abbottabad, Pakistan Highlights The nexus between institutions-macroeconomic is investigated. Cointegration and causality approaches are applied. Suitable policy recommendations are suggested. Abstract Purpose: On global perspective, it is observed that developing economies need a boost up to grow faster to overcome from poverty trap. This trap can be overcome by investment on large scales which results into augmenting productive capacity of an economy, increases the level of employment and promotes technical progress through embodiment of new techniques. However, institutional variables on the other hand play a vital role to attract investment. This study main objective was to analyze the role of relationship of foreign direct investment on macroeconomic and institutional variables. Methodology: This study used data from 1973-2010 and econometric tools such as unit root test, Johansen cointegration, Granger causality and Error correction model. Along with that this study used diagnostic tests to check the model authenticity. Findings: The study found that there exist a short run relationship among inflation (INF), Law and Order conditions (LWO) and Taxation (T) have a significant impact on foreign direct investment (FDI). Institutional variables like Political Instability, Law n Order & Corruption are major institutional hazards in diminishing foreign direct investment (FDI). For every economy it is necessary to have strong institutions which attract investments. Hence, institutional variables play a vital role to have sound economic indicators like inflation, taxation and interest rate. These robust economic indicators encourage foreign direct investment in the country. Recommendations: The paper presents new insights for policy makers to develop Pakistan’s economy. Keywords: Institutions, Macroeconomic, Pakistan JEL Classifications: E1 Corresponding Author: [email protected] Citation: Mukhtar, A., Asif, M., Siyal, G. and Zaman, K. (2014). Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan. International Journal of Economics and Empirical Research. 2(11), 465-479.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Journal of Economics and Empirical Research

http://www.tesdo.org/Publication.aspx

- 465 -

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in

Pakistan

Ahsen Mukhtar a , Muhammad Asif a, Ghamz-e-Ali Siyal a, Khalid Zaman a,

a COMSATS Institute of Information and Technology, Abbottabad, Pakistan

Highlights The nexus between institutions-macroeconomic is investigated. Cointegration and causality approaches are applied. Suitable policy recommendations are suggested. Abstract Purpose: On global perspective, it is observed that developing economies need a boost up to grow faster to overcome from poverty trap. This trap can be overcome by investment on large scales which results into augmenting productive capacity of an economy, increases the level of employment and promotes technical progress through embodiment of new techniques. However, institutional variables on the other hand play a vital role to attract investment. This study main objective was to analyze the role of relationship of foreign direct investment on macroeconomic and institutional variables. Methodology: This study used data from 1973-2010 and econometric tools such as unit root test, Johansen cointegration, Granger causality and Error correction model. Along with that this study used diagnostic tests to check the model authenticity. Findings: The study found that there exist a short run relationship among inflation (INF), Law and Order conditions (LWO) and Taxation (T) have a significant impact on foreign direct investment (FDI). Institutional variables like Political Instability, Law n Order & Corruption are major institutional hazards in diminishing foreign direct investment (FDI). For every economy it is necessary to have strong institutions which attract investments. Hence, institutional variables play a vital role to have sound economic indicators like inflation, taxation and interest rate. These robust economic indicators encourage foreign direct investment in the country. Recommendations: The paper presents new insights for policy makers to develop Pakistan’s economy. Keywords: Institutions, Macroeconomic, Pakistan JEL Classifications: E1

Corresponding Author: [email protected] Citation: Mukhtar, A., Asif, M., Siyal, G. and Zaman, K. (2014). Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan. International Journal of Economics and Empirical Research. 2(11), 465-479.

International Journal of Economics and Empirical Research. 2014, 2(11), 465-479.

- 466 -

I. Introduction Agosin and Ricardo, (2000) described investment plays a very important role in the economic growth of a country, as it raises the productive capacity of an economy, increases the level of employment and promotes technical progress through embodiment of new techniques. Similar study by Erdal and Masca, (2008) found that it also plays a crucial role in determining the long-run productive capacity of an economy, because investment creates new capital goods, so a higher rate of investment means that capital stock is growing rapidly. Investment could be broadly classified into two categories as: Domestic Investment Foreign Investment

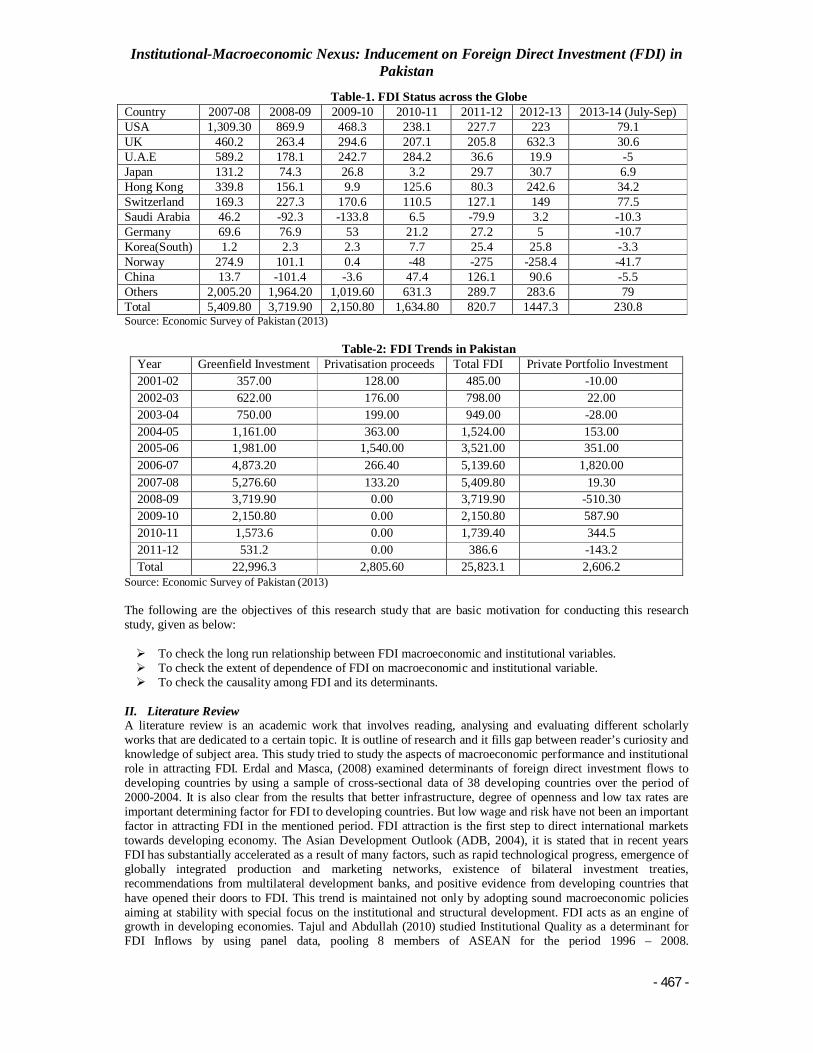

Foreign direct investment, in its classic definition, is defined as a company from one country making a physical investment into building a factory in another country. The direct investment in buildings, machinery and equipment is in contrast with making a portfolio investment, which is considered an indirect investment (Tajul and Abdullah, 2010). Foreign direct investment as an important factor in accelerating economic growth in developing countries has been proved completely (Sufian and Sidiropoulos, 2010). Foreign direct investment to the host country, which gives the ability to invest beyond the level of domestic savings to achieve Benefits of foreign direct investment are attracting capital, technology, knowledge, improving management capacity, increasing employment, improving competitiveness and increasing balance of payments (Javed et al. 2013). Foreign Direct Investment (FDI) has many positive as well negative effects, which include technology transfers, organizational and managerial skills transfers, labour training, employment generation, the introduction of new production processes, productivity gains, carbon dioxide emissions and social and cultural impacts (De Mello, 1999). In an open economy, investment is financed both by domestic savings and foreign capital inflows including FDI. Thus, FDI enables investment-receiving countries to achieve investment levels beyond their capacity to save and consequently stimulates their economic growth (Sahoo, 2006). Multinational Corporations (MNCs) have remained the major contributors in enhancing FDI. MNCs play vital role in the economic growth of developing countries, because these corporations use human and physical resources of such countries (Udomkerdmongkol and Morrissey, 2008). In the year 2000, the 100 largest MNCs made up 4.3% of the world’s Gross Domestic Product (GDP) by holding accumulated assets of US$ 6.3 trillion. In the same year, MNCs had combined foreign sales of US$ 2.4 trillion, hired 7.1 million employees for their foreign operations and also employed about 7 million people in their domestic operations (UNCTAD, 2002). FDI in Pakistan Pakistan is a developing country. It requires FDI to fill the saving-investment gap, export-import gap and to accelerate economic growth. The inflows of FDI remained less than 2% of GDP before the year 2003 but it increased sharply after the year 2003. It remained 3.7% of GDP in the year 2007 (World Bank, 2010). FDI has been rising significantly and it may have positive as well negative effects. So, there is an imperative need to investigate its impact on the economy of Pakistan (Azam et al. 2011). Foreign direct investment (FDI) is a pivotal component of capital flows and is considered to be one of the most important channel through which financial globalization benefits the economy (Aqeel and Nishat, 2005). Many studies find supportive evidence that FDI exerts positive effect on growth. To increase the level of FDI, liberalization of trade and investment regime by relaxing controls and offering special incentives to foreign investors, such as tax concessions, tariff reductions or exemptions and subsides for infrastructure is needed (Arslan and Qaisar, 2013). Such policies have been instrumental in accelerating FDI inflows to developing countries like Pakistan. The domestic policies opted by the host countries have an important influence on the decisions of foreign investment. To attract FDI, the recipient country should develop good and investor friendly policies and strong infrastructure and stable environment are the pre-requisite to restore the confidence of foreign investors (Azam et al. 2011). World Bank report on FDI (2010) in the last few years FDI is majorly directed from few countries. During the last few years apart from turbulent relations USA is the major contributor among other notables. Statistical overview of FDI country wise for last half five years is given in Table-1. FDI in Pakistan has been decreased in the last few years due to unstable environment. FDI inflows to Pakistan can be explained in terms of its size and percentage of gross domestic product (GDP). Due to inconsistent investment policies, the flow of FDI was insignificant until 1991; however, it steadily increased in the post-liberalisation period. Actual inflows of FDI to Pakistan have increased from $119.6 million in 1975-79 to $3299.8 million in 1995-99 and from $485 million in 2001-02 to $5,152.80 million in 2007 -08. Table 2 shows the trend of FDI in Pakistan during the last decade.

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan

- 467 -

Table-1. FDI Status across the Globe Country 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 (July-Sep) USA 1,309.30 869.9 468.3 238.1 227.7 223 79.1 UK 460.2 263.4 294.6 207.1 205.8 632.3 30.6 U.A.E 589.2 178.1 242.7 284.2 36.6 19.9 -5 Japan 131.2 74.3 26.8 3.2 29.7 30.7 6.9 Hong Kong 339.8 156.1 9.9 125.6 80.3 242.6 34.2 Switzerland 169.3 227.3 170.6 110.5 127.1 149 77.5 Saudi Arabia 46.2 -92.3 -133.8 6.5 -79.9 3.2 -10.3 Germany 69.6 76.9 53 21.2 27.2 5 -10.7 Korea(South) 1.2 2.3 2.3 7.7 25.4 25.8 -3.3 Norway 274.9 101.1 0.4 -48 -275 -258.4 -41.7 China 13.7 -101.4 -3.6 47.4 126.1 90.6 -5.5 Others 2,005.20 1,964.20 1,019.60 631.3 289.7 283.6 79 Total 5,409.80 3,719.90 2,150.80 1,634.80 820.7 1447.3 230.8 Source: Economic Survey of Pakistan (2013)

Table-2: FDI Trends in Pakistan

Source: Economic Survey of Pakistan (2013) The following are the objectives of this research study that are basic motivation for conducting this research study, given as below: To check the long run relationship between FDI macroeconomic and institutional variables. To check the extent of dependence of FDI on macroeconomic and institutional variable. To check the causality among FDI and its determinants.

II. Literature Review A literature review is an academic work that involves reading, analysing and evaluating different scholarly works that are dedicated to a certain topic. It is outline of research and it fills gap between reader’s curiosity and knowledge of subject area. This study tried to study the aspects of macroeconomic performance and institutional role in attracting FDI. Erdal and Masca, (2008) examined determinants of foreign direct investment flows to developing countries by using a sample of cross-sectional data of 38 developing countries over the period of 2000-2004. It is also clear from the results that better infrastructure, degree of openness and low tax rates are important determining factor for FDI to developing countries. But low wage and risk have not been an important factor in attracting FDI in the mentioned period. FDI attraction is the first step to direct international markets towards developing economy. The Asian Development Outlook (ADB, 2004), it is stated that in recent years FDI has substantially accelerated as a result of many factors, such as rapid technological progress, emergence of globally integrated production and marketing networks, existence of bilateral investment treaties, recommendations from multilateral development banks, and positive evidence from developing countries that have opened their doors to FDI. This trend is maintained not only by adopting sound macroeconomic policies aiming at stability with special focus on the institutional and structural development. FDI acts as an engine of growth in developing economies. Tajul and Abdullah (2010) studied Institutional Quality as a determinant for FDI Inflows by using panel data, pooling 8 members of ASEAN for the period 1996 – 2008.

Year Greenfield Investment Privatisation proceeds Total FDI Private Portfolio Investment 2001-02 357.00 128.00 485.00 -10.00 2002-03 622.00 176.00 798.00 22.00 2003-04 750.00 199.00 949.00 -28.00 2004-05 1,161.00 363.00 1,524.00 153.00 2005-06 1,981.00 1,540.00 3,521.00 351.00 2006-07 4,873.20 266.40 5,139.60 1,820.00 2007-08 5,276.60 133.20 5,409.80 19.30 2008-09 3,719.90 0.00 3,719.90 -510.30 2009-10 2,150.80 0.00 2,150.80 587.90 2010-11 1,573.6 0.00 1,739.40 344.5 2011-12 531.2 0.00 386.6 -143.2 Total 22,996.3 2,805.60 25,823.1 2,606.2

International Journal of Economics and Empirical Research. 2014, 2(11), 465-479.

- 468 -

The low impact of institutional quality does indeed suggest that ASEAN countries are yet to embark seriously on this issue and results could be different in the future. This is because, institutional quality could also serve as the cost of doing business and improvement would surely be able to reverse the inflows into ASEAN. These countries aiming at a high growth rate must introduce institutional reforms to support their healthy macroeconomic outlook. Sufian and Sidiropoulos, (2010) studied the determinants of foreign direct investment in MENA countries by employing a panel data methodology. The study concluded that, countries that are receiving fewer foreign investments could make themselves more attractive to potential foreign investors by making institutional adjustments. So, the policy makers in the MENA region should remove all barriers to trade, develop their financial systems, reduce the level of corruption, improve policy environment, and build appropriate institutions. Arshad and Shujaat, (2011) studied foreign direct investment and economic growth in Pakistan by using Granger causality and panel co-integration techniques over the period 1981-2008. FDI has a positive effect on output in the long run. Their results also supports the evidence of long-run causality running from GDP to FDI, while in the short run, the evidence of two-way causality between FDI and GDP is identified. Thus, policymakers should increasingly focus on attracting FDI in these sectors in order to attain short-term growth. Javed et al. (2013) studied determinants of foreign direct investment by using cointegration approach and error correction model (ECM) covering the time period 1973 to 2011. This study considered the Gross Domestic Product (GDP), consumer price index (CPI), political instability, exchange rate and population. All variables are found statistically significant and concluded that GDP in Pakistan is the most significant predictor of the FDI, followed by in order of importance the political instability, exchange rate and consumer price index. This study concluded that government should concentrate on the enhancement of growth rate and promote political stability in the country to bring the foreign investment inflow in the country. Salman, (2010) examined the determinants of foreign direct investment (FDI) in developing countries like Pakistan. He continued his research using the least square regression technique and data for the period 1980- 2005. Empirical finding discovered for all variants of growth and tariff related imports showed negative results for Pakistan. Sahoo, (2006) analysed the data for five South Asian countries and highlighted the importance of economic factors for FDI flows and used panel co integration technique to examine long run relationship between economic variables and FDI inflows and identified that market size; trade openness, infrastructure index and labour force growth rate were major determinants. Gropp and Kostial, (2000) used the panel data of nineteen OECD countries to find the relationship between FDI and tax revenue. They found a weak correlation between FDI and corporate income tax and found a strong positive impact of FDI inflows on the profit tax and total tax revenue. Arslan and Qaisar, (2013) utilised their energies on studying the Impact of Tariff structures on FDI in Pakistan by using Johansen Co-integration technique and Least Squares Regression Analysis covering the period 1973 – 2011. Their study concluded that lower tariff structures, higher GDP and higher inflation increase foreign direct investment whereas gross capital formation has no effect on the foreign direct investment. Aqeel and Nishat, (2005) examined the determinants of foreign direct investment (FDI) in Pakistan by using the cointegration and error-correction techniques over the period 1961 to 2003. Their study considers the tariff rate, exchange rate, tax rate, credit to private sector and index of general share price variables as they explain the inflow of foreign direct investment. Desai et al. (2004) also identified the role of taxes on FDI in host country. They found that high tax rate imposed on corporate sectors effect negatively to profit of firms through capital and labour market. Corporate tax depress capital labour ratio and decrease the profit margin. A high level of income tax helps in substitutions of capital with labour market. High income taxation rates appear to encourage firms to substitute labour for capital and to reduce levels of taxable income, whereas high rates of indirect taxation do not. Doğru, (2012) tried to establish the evidence from upper-middle income countries. The panel least square method is employed to estimate the relationship between FDI and its potential macroeconomic and instructional determinants. A sample of 54 developing countries for the period of 1995-2011. The panel regression results show that the size of economic activity (GDP growth rate and GDP per capita growth rate), population growth rate and school enrolment are the principle determinants of FDI inflows to host country, however economic stability, indicated by inflation rate, is not a major determinant of FDI. Among institutional variables country risk and global competitiveness are positively related to FDI as expected and have significant coefficients. Hyun, (2006) analysed the short run and long run relationship between institution quality and FDI inflows by analysing the data of 62 developing countries over the period of 1984 to 2003. The analysis shows that there is no short run causality between these two variables. It is also clear from the analysis that Institutional quality affects positively FDI in long run and short run. Anghel, (2005) examined Do Institutions Affect Foreign Direct Investment? The analysis found that countries whose governments are highly ranked according to various indices of the quality of institutions tend to do better in attracting foreign direct investment. In an empirical analysis of cross-sectional data, the study also found that different aspects of the quality of institutions from a country (corruption, protection of property rights, policies related to opening a

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan

- 469 -

business and maintaining it, etc.) are almost always significant, regardless of the other control variables that are used in the least-squares and instrumental variables estimation. Azam et al. (2011) studied institutions, macroeconomic policy and foreign direct investment in a panel data of seven South Asian countries over the period of 12 years since 1996-2007. The study found that a good institutional quality plays a key role in attractiveness of FDI inflows. A poor macroeconomic policy situation produces negative impact on FDI. This study suggests a rather unusual result that good institutional quality and macroeconomic policy generate negative impact in a combined form on FDI. International political dynamics should also be taken as stake holder in making the economic way forward. Internationalization and financial liberalizations makes arduous task to attract FDI. De Mello, (1999) studied foreign direct investment-led growth by using time series as well as panel data estimation. He included a sample of 15 developed and 17 developing countries for the period 1970-90. The study found strong relationship between FDI, capital accumulation, output and productivity growth. The time series estimations suggest that effect of FDI on growth or on capital accumulation and total factor productivity varies greatly across the countries. The panel data estimation indicates a positive impact of FDI on output growth for developed and developing countries. Harms and Ursprung, (2002) examined the relationship between average foreign direct investment per capita and indices of political rights, civil liberties, and repression. They found a negative and significant relationship between the dependent variable and all three indices. A related study, Jensen (2003) argues that a country which protects democratic rights receives more FDI compared to a non-democratic one. In other words, multinational firms prefer to invest in countries where democratic rights are protected. Johnson et al. (2000) measured the depth of the Asian crisis of 1997-1998 using currency depreciations and stock market declines across emerging market economies. They found that measures of law and order and the extent of protection of shareholders explain much more of the variation in exchange rates and stock market performance during the Asian crisis than do the macroeconomic variables. Countries with solid institutions, such as Singapore and Hong Kong experienced the mildest crises, while countries with weak institutions, such as Philippines and Russia, suffered the deepest. Udomkerdmongkol and Morrissey, (2008) investigated the effect of FDI on private investment controlling for political regime for developing countries classified into different regions. The study samples thirteen Latin American countries, eight Caribbean countries, eight Asian countries, ten European transition countries and five African countries. The study reveals that FDI tends to crowd out domestic private investment and this crowd out effect is greater in countries with high governance scores and lower in Latin America compared to Asia, Europe and Africa. Agosin and Ricardo, (2000) analysed the effect of lagged values of FDI inflows on investment rates in host countries to examine whether FDI crowds-in or crowds-out domestic investment over the 1970-95 periods. They conclude that FDI crowds-in domestic investment in Asian countries crowds-out in Latin American countries while in Africa their relationship is neutral (or one-to-one between FDI and total investment). Therefore, they conclude that effects of FDI have by no means always favourable and simplistic policies are unlikely to be optimal. Bosworth and Collins, (1999) examine the impact of capital inflows for recipient countries in panel set of 23 industrialized countries and 62 less developed countries. The study reveals that FDI complement (crowd in) domestic investment but when the model controlled for other variables such as the accelerator term in the developing countries, they found that FDI crowds out domestic investment. Grossman and Helpman, (1991) also point out that less-developed countries may specialize in low technological goods or natural resources in which spillovers and learning-by-doing opportunities are limited. So, the amount and the impact of FDI may not be effective. FDI to least developed countries has been concentrated in natural resource intensive sectors, particularly mining. FDI in mining has limited multiplier effects on output and employment. Apergis et al. (2006) to analyse the dynamic relationship between FDI inflows and domestic investment for a panel of thirty selected countries including Egypt, Tunisia, South Africa and Morocco among others. Their study used gross fixed capital formation as proxy for domestic investment. They find that the inflows of FDI crowds in domestic investment in a univariate model but in a multivariate model accounting for other variables FDI inflow crowds out domestic investment. Beven and Estrin, (2000) establish the determinants of FDI inflows to transition economies (Central and Eastern Europe) by taking determinant factors as country risk, labour cost, host market size and gravity factors from 1994 to1998. The study observes that country risks are influenced by private sector development, industrial development, the government balance, reserves and corruption. A dummy variable employed for capturing the key announcements of progress in EU accession seems to be directly influencing the FDI receipts. Kim and Seo, (2003) used the Vector Auto Regressive (VAR) model to find a relationship among domestic investment, FDI and economic growth in Korea. They found that FDI had a negative and insignificant impact on domestic investment, and domestic investment had a significant and negative impact on FDI. FDI could also generate imperfect competition in developing economies. Lipsey, (2000) found a negative and insignificant impact of FDI on domestic investment. Agosín and Mayer, (2000) found a strong crowding-in effect of FDI on domestic investment. They further explored the degree of impact in different regions and found that FDI had stronger crowding-in effect for Africa than for Asia and also had strong crowding-out effect for Latin America.

International Journal of Economics and Empirical Research. 2014, 2(11), 465-479.

- 470 -

Rehman, (2003) argued that credibility of trade liberalization policy of host country is more important for FDI inflows by analysing the data of 74 developing countries over the period of 1980-1998 and concluded creditability of trade policy concerned with export promotion efforts to attract FDI inflows in developing countries. Credibility of trade liberalization policy is important for FDI inflows relative to portfolio equity investment because FDI inflows are based on long term decision. Lack of creditability regarding polices in host country may generate risk for foreign investment. Wei, (2000a) examines the effects of taxation and corruption on FDI using bilateral FDI flow data from 12 source countries to 45 host countries. Using three different measures of corruption, he concluded that an increase in either the tax rate on multinational firms or the level of corruption in the host countries would reduce inward FDI. Wei, (2000b) also examines corruption’s effects on the composition of capital flows using bilateral capital flow data from 14 source countries to 53 host countries. His findings suggest that there is indeed a negative relationship between corruption and FDI and that the reduction in FDI caused by corruption is greater than the negative impact of corruption on other types of capital inflows. Akçay, (2001) uses cross-sectional data from 52 developing countries with two different indices of corruption to estimate the effects of the level of corruption on FDI inflows. He fails to `find evidence of a negative relationship between FDI and corruption. He concludes that the most significant determinants of FDI are market size, corporate tax rates, labour costs, and openness. Habib and Zurawicki, (2002) analysed the effects of corruption on bilateral FDI flows using a sample of seven source countries and 89 host countries. They found that foreign firms tend to avoid situations where corruption is visibly present because corruption is considered immoral and might be an important cause of inefficiency. Abed and Davoodi, (2000) examined the effects of levels of corruption on per capita FDI inflows to transition economies. They found that countries with a low level of corruption attract more per capita FDI. However, once they control for the structural reform factor, corruption becomes insignificant. They conclude that structural reform is more important than reducing the level of corruption in attracting FDI. Al-Sadig, (2009) used panel data to investigate the effect of corruption on aggregate FDI inflows into various host countries. Incorporating corruption in a gravity-type model of FDI determinants, it finds that there is a negative effect of corruption on aggregate FDI inflows, but, more strikingly, that this effect disappears if the quality of institutions is taken into account. Consequently, it concludes that the quality of country’s institutions is more important in attracting FDI inflows than low corruption. Kumar and Pradhan, (2002) analysed the relationship among FDI, growth and domestic investment for a sample of 107 less developed countries and used gross fixed capital formation as percentage of GDP as a proxy for domestic investment. Their study provides empirical evidence that FDI affects domestic investments in a dynamic manner with a negative initial effect and a subsequent positive effect for panel data as well as for most of countries individually. Though, the evidence is mixed as FDI appeared to crowd out domestic investment in general, some countries have had favourable effect of FDI on domestic investment suggesting a role for host country policies. Kinoshita and Campos, (2001), using a panel data framework, investigate the factors that account for the geographical patterns of FDI inflows among 25 transition economies. They classify determinants into three categories; locational factors, institutions and agglomeration economies. Using the fixed effects and GMM models, they find that the quality of institutions is the major determinant in the location of FDI. Specifically, they find that poor quality of bureaucracy and lack of rule of law are a deterrent to foreign investors because they increase the transaction cost which directly affects the profitability of investment projects. Asiedu, (2002) who uses panel data for 22 countries in Sub-Saharan Africa over the period 1984-2000, found that macroeconomic stability, efficient institutions; political stability and a good regulatory framework have a positive impact on FDI. More importantly, such a result would corroborate that Africa could simply attract more FDIs by promoting stronger institutions and others significant institutional reforms even if they are not naturally endowed. Mustafa and Valerica, (2011) studied The Relationship between Education and Foreign Direct Investment by using time-series data from 1980-1999, and applying GLS pooled cross-sectional time series fixed-effect for income group countries. Results indicate that rich countries with high human capital and poor countries with low human capital demonstrate an inverse correlation between FDI and human capital proxies. However, for middle-income and upper middle-income countries, human capital (especially tertiary education) has a positive relationship with FDI. Garibaldi et al (2002) also analysed the FDI and Portfolio investment flows to 26 transition economies in Eastern Europe including the former Soviet Union from 1990 to 1999. The regression estimation indicates that the FDI flows are well explained by standard economic fundamentals such as market size, fiscal deficit, inflation and exchange rate regime, risk analysis, economic reforms, trade openness, availability of natural resources, barriers to investments and bureaucracy. However, the portfolio flows are poorly explained by the fundamentals. Romita (2002) studied Determinants of Foreign Direct Investment by using panel data for 44 countries over the period 1983–90. The estimation results provide considerable support for the importance of both traditional and non-traditional factors in determining flows of foreign direct investment in a country.

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan

- 471 -

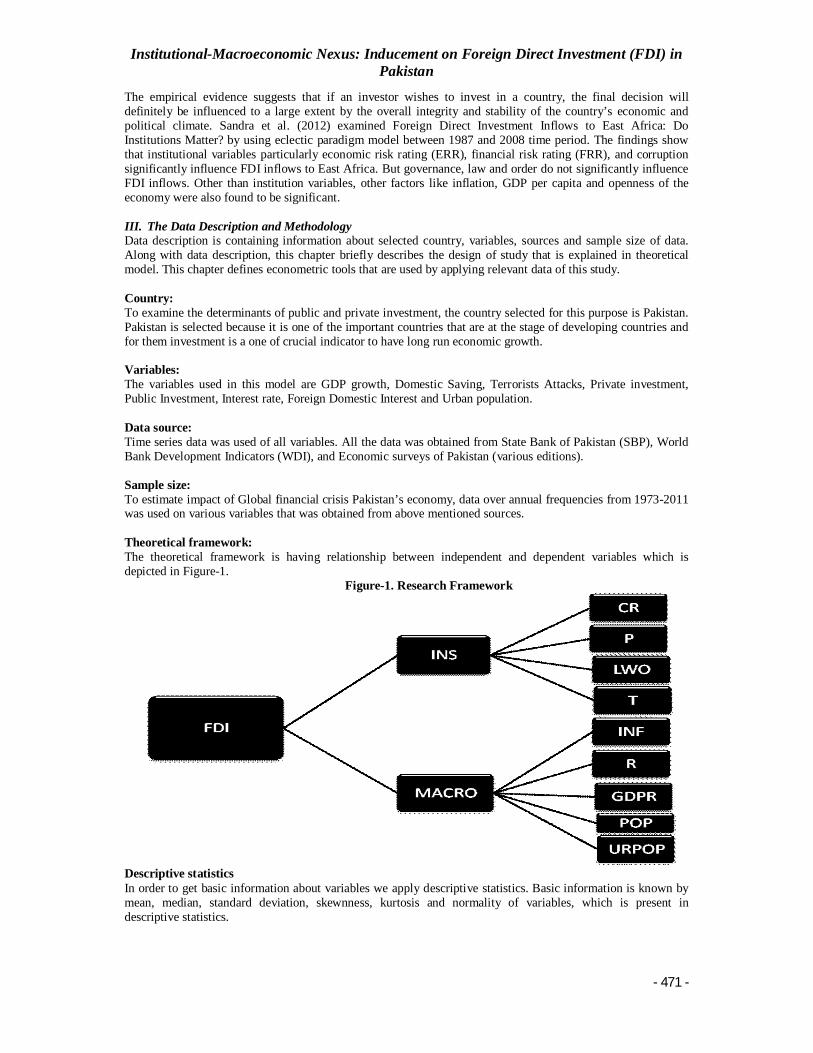

The empirical evidence suggests that if an investor wishes to invest in a country, the final decision will definitely be influenced to a large extent by the overall integrity and stability of the country’s economic and political climate. Sandra et al. (2012) examined Foreign Direct Investment Inflows to East Africa: Do Institutions Matter? by using eclectic paradigm model between 1987 and 2008 time period. The findings show that institutional variables particularly economic risk rating (ERR), financial risk rating (FRR), and corruption significantly influence FDI inflows to East Africa. But governance, law and order do not significantly influence FDI inflows. Other than institution variables, other factors like inflation, GDP per capita and openness of the economy were also found to be significant. III. The Data Description and Methodology Data description is containing information about selected country, variables, sources and sample size of data. Along with data description, this chapter briefly describes the design of study that is explained in theoretical model. This chapter defines econometric tools that are used by applying relevant data of this study. Country: To examine the determinants of public and private investment, the country selected for this purpose is Pakistan. Pakistan is selected because it is one of the important countries that are at the stage of developing countries and for them investment is a one of crucial indicator to have long run economic growth. Variables: The variables used in this model are GDP growth, Domestic Saving, Terrorists Attacks, Private investment, Public Investment, Interest rate, Foreign Domestic Interest and Urban population. Data source: Time series data was used of all variables. All the data was obtained from State Bank of Pakistan (SBP), World Bank Development Indicators (WDI), and Economic surveys of Pakistan (various editions). Sample size: To estimate impact of Global financial crisis Pakistan’s economy, data over annual frequencies from 1973-2011 was used on various variables that was obtained from above mentioned sources. Theoretical framework: The theoretical framework is having relationship between independent and dependent variables which is depicted in Figure-1.

Figure-1. Research Framework

Descriptive statistics In order to get basic information about variables we apply descriptive statistics. Basic information is known by mean, median, standard deviation, skewnness, kurtosis and normality of variables, which is present in descriptive statistics.

International Journal of Economics and Empirical Research. 2014, 2(11), 465-479.

- 472 -

Unit Root Tests: The time series data frequently shows the property of non-stationarity in levels and the resulted estimates usually give spurious results (Granger, 1981). Hence, the initial step in any time series empirical analysis is to check the presence of unit roots to remove the problem of inaccurate estimates. The next important step taken was to check the order of integration of each variable in a data series in the model to establish whether the data under hand suffers unit root and how many times it is needed to be differenced to gain stationarity (Yousaf et al 2008). We have chosen to apply the ADF unit root test in order to examine the integrating properties of the variables. Cointegration Test: The Johansen-Juselius (JJ) Method Johansen (1988, 1991, 1992) and Johansen-Juselius (1990, 1992) proposed a technique that helps in finding more than one co integration vectors if we have variables number more than two. Such technique is used because sometimes variables might form several equilibrium relationships in the model. So Johansen approach is used for multiple equations. A VAR representation of the N-dimensional data vector Xt by following Johansen (1988) and Johansen and Juselius (1990) can be specified as:

Xt = ПJ Xi-j + …+ П Ф Xi- Ф + δ +ei, i = 1, 2, …….T (1) Where e1,…..et are N-dimension variables, Xt is a vector which shows all endogenous variables in the model and δ shows a vector of constant. In this analysis there are two endogenous variables, Et and Rt. By using the information ∆=1-L, where L is the lag operator, the VAR system can be rewritten as Error Correction Model (ECM) as follows:

∆ Xt= ПJ Xi-j + Фj∆ Xi-j +…..Фk-j∆ Xi-k+1+ δ +ei (2) The central attention is on the parameter matrix П of the Johansen-Juselius method. The number of co integration vectors is the VAR system can be determined the rank γ of this matrix γ (П), where (0< γ<N). There are γ linear combinations of the variables in the system if the rank of this matrix is found to be γ. The matrix П can be replaced as П=αβ where β is the co integrating vector and α is the speed of adjustment vector. The maximum eign value test (λmax) and the trace test (λtrace) are employed to test for the value of γ on the basis of the number of significant eigen values of П. The above mentioned test statistics are distributed as X2 with the degrees of freedom (n-k) where γ is the value of rank and N represents the number of endogenous variables. If the values calculated are less than the critical values at the proper degrees of freedom and significance level then null hypothesis are accepted. Error Correction Model: If the time series are I(1), then one could run regressions in their first differences. But, by taking first differences, we lose the long run relationship that is store in the data. This implies that one needs to use variables in levels as well. Advantage of the Error Correction Model (ECM) incorporates variables both in their levels and first difference. By doing this, ECM captures the short-run disequilibrium situations as well as the long-run equilibrium adjustments between variables. ECM term having negative sign and value between “0 to 1” shows convergence of model towards long-run equilibrium and shows how much percentage adjustment takes place every year.

D(FDI) = αo+ α1D(GDPR)t-1+ α2D(INF)t-1 + α3D(CR)t-1 + α4D(R)t-1 + α5D(P)t-1 + α6D(LWO)t + α7(T)t-1 + α8(POP)t-1 + α9(URPOP)t-1 + ℮ (3) Where D stands for the first difference and t-1 indicates lag value. ℮ is the error correction term / adjustments coefficient. The coefficients α1 to α6 shows, short-run elasticities of the independent variables on Real GDP and α7 to α13 represents long-run elasticities that are having Log(-1). Multi-variate Granger Causality test: The standard Multi Granger causality test observes the casual relationships among more than two variables. It examines that whether current changes in variable y can be explained by past changes in other variables like u, v, and w along with the explanations provided by past changes in y itself. The variables are interchanged to see the causality in other directions. There are possible few relationship types: Unidirectional causality: x Granger causes u, v and w. Bidirectional causality: different variables causing in two directions. Independence: neither variable causes each other.

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan

- 473 -

The variables x, u, v, and w must be stationary for implication of standard Multi Granger Causality test. The standard Multi Granger causality regressions based on properly differenced stationary variables because most of the variables are non stationary in their levels forms. Hence this Multi-variate Wald Chi-stat value is used to reject the null hypothesis or accept it. One concludes that x Multi-variate Granger causes variables like y, u or v if null hypothesis is rejected. If value is insignificant then null hypothesis is accepted and if it is significant then null hypothesis is rejected. The mathematical equation for Granger causality will be considered with p and q lags as given below:

Yt. = α + φ1 Yt-1 + β1Xt-1 + β2Xt-2 + ℮t (4)

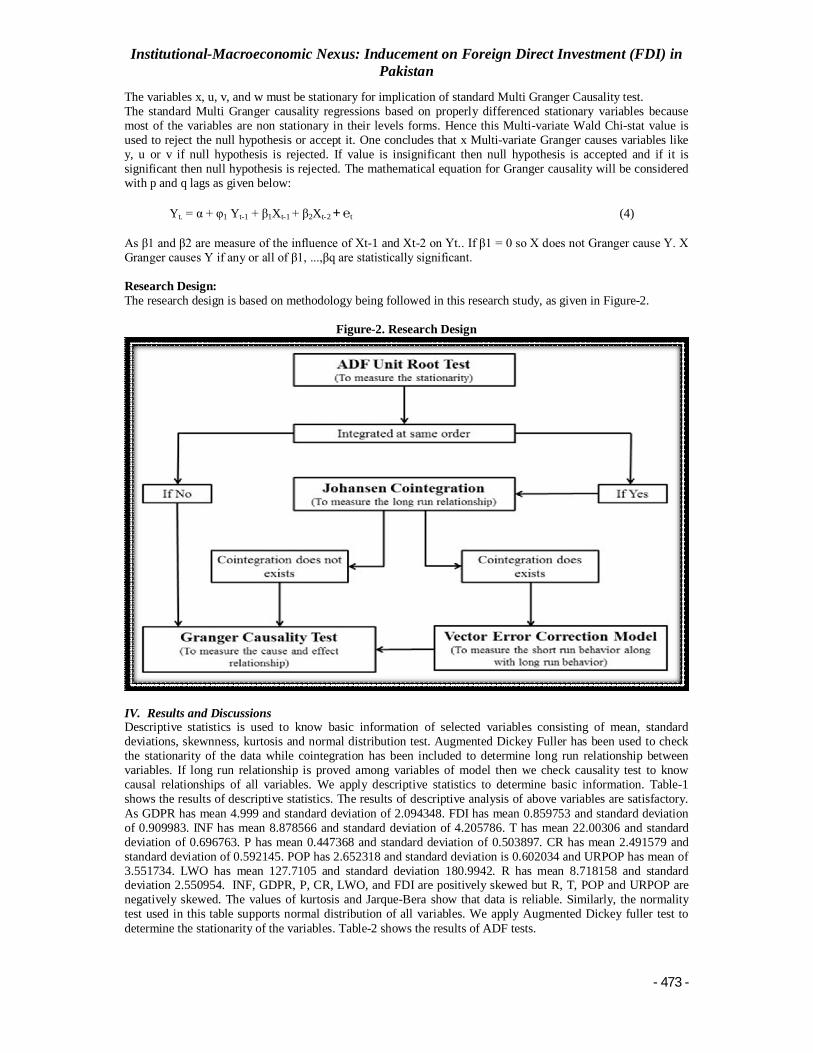

As β1 and β2 are measure of the influence of Xt-1 and Xt-2 on Yt.. If β1 = 0 so X does not Granger cause Y. X Granger causes Y if any or all of β1, ...,βq are statistically significant. Research Design: The research design is based on methodology being followed in this research study, as given in Figure-2.

Figure-2. Research Design

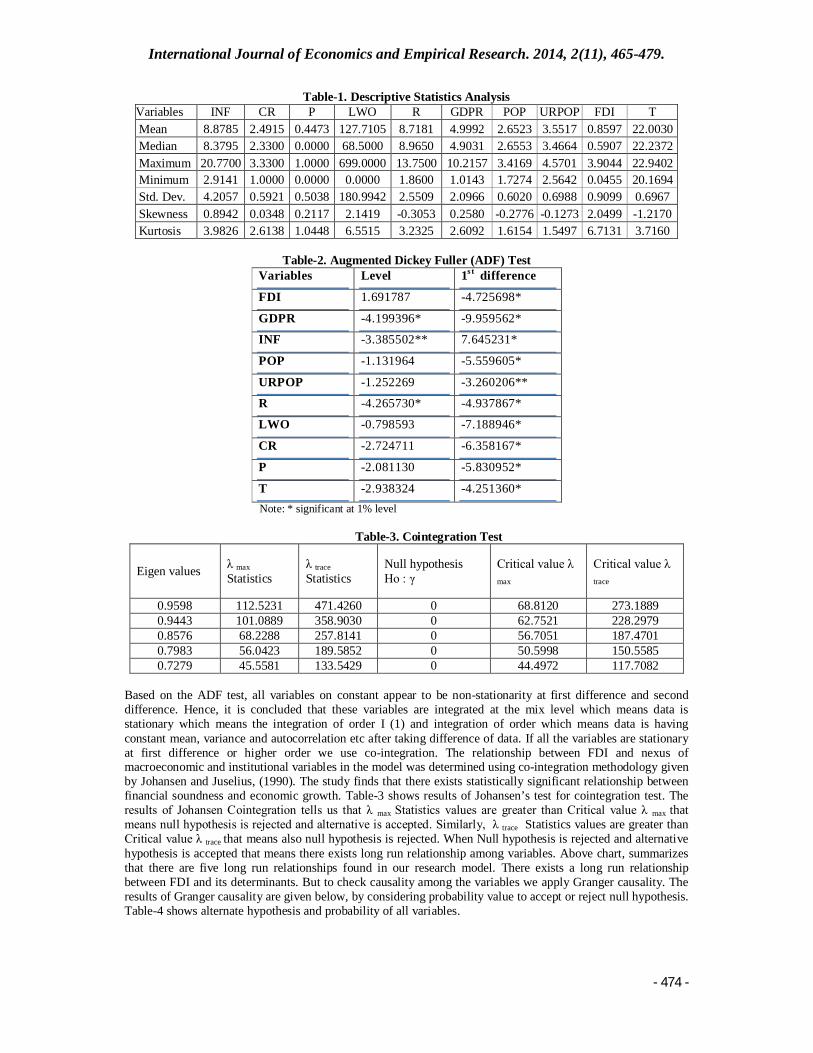

IV. Results and Discussions Descriptive statistics is used to know basic information of selected variables consisting of mean, standard deviations, skewnness, kurtosis and normal distribution test. Augmented Dickey Fuller has been used to check the stationarity of the data while cointegration has been included to determine long run relationship between variables. If long run relationship is proved among variables of model then we check causality test to know causal relationships of all variables. We apply descriptive statistics to determine basic information. Table-1 shows the results of descriptive statistics. The results of descriptive analysis of above variables are satisfactory. As GDPR has mean 4.999 and standard deviation of 2.094348. FDI has mean 0.859753 and standard deviation of 0.909983. INF has mean 8.878566 and standard deviation of 4.205786. T has mean 22.00306 and standard deviation of 0.696763. P has mean 0.447368 and standard deviation of 0.503897. CR has mean 2.491579 and standard deviation of 0.592145. POP has 2.652318 and standard deviation is 0.602034 and URPOP has mean of 3.551734. LWO has mean 127.7105 and standard deviation 180.9942. R has mean 8.718158 and standard deviation 2.550954. INF, GDPR, P, CR, LWO, and FDI are positively skewed but R, T, POP and URPOP are negatively skewed. The values of kurtosis and Jarque-Bera show that data is reliable. Similarly, the normality test used in this table supports normal distribution of all variables. We apply Augmented Dickey fuller test to determine the stationarity of the variables. Table-2 shows the results of ADF tests.

International Journal of Economics and Empirical Research. 2014, 2(11), 465-479.

- 474 -

Table-1. Descriptive Statistics Analysis Variables INF CR P LWO R GDPR POP URPOP FDI T Mean 8.8785 2.4915 0.4473 127.7105 8.7181 4.9992 2.6523 3.5517 0.8597 22.0030 Median 8.3795 2.3300 0.0000 68.5000 8.9650 4.9031 2.6553 3.4664 0.5907 22.2372 Maximum 20.7700 3.3300 1.0000 699.0000 13.7500 10.2157 3.4169 4.5701 3.9044 22.9402 Minimum 2.9141 1.0000 0.0000 0.0000 1.8600 1.0143 1.7274 2.5642 0.0455 20.1694 Std. Dev. 4.2057 0.5921 0.5038 180.9942 2.5509 2.0966 0.6020 0.6988 0.9099 0.6967 Skewness 0.8942 0.0348 0.2117 2.1419 -0.3053 0.2580 -0.2776 -0.1273 2.0499 -1.2170 Kurtosis 3.9826 2.6138 1.0448 6.5515 3.2325 2.6092 1.6154 1.5497 6.7131 3.7160

Table-2. Augmented Dickey Fuller (ADF) Test

Variables Level 1s t difference

FDI 1.691787 -4.725698*

GDPR -4.199396* -9.959562*

INF -3.385502** 7.645231*

POP -1.131964 -5.559605*

URPOP -1.252269 -3.260206**

R -4.265730* -4.937867*

LWO -0.798593 -7.188946*

CR -2.724711 -6.358167*

P -2.081130 -5.830952*

T -2.938324 -4.251360* Note: * significant at 1% level

Table-3. Cointegration Test

Eigen values λ max Statistics

λ trace Statistics

Null hypothesis Ho : γ

Critical value λ max

Critical value λ trace

0.9598 112.5231 471.4260 0 68.8120 273.1889 0.9443 101.0889 358.9030 0 62.7521 228.2979 0.8576 68.2288 257.8141 0 56.7051 187.4701 0.7983 56.0423 189.5852 0 50.5998 150.5585 0.7279 45.5581 133.5429 0 44.4972 117.7082

Based on the ADF test, all variables on constant appear to be non-stationarity at first difference and second difference. Hence, it is concluded that these variables are integrated at the mix level which means data is stationary which means the integration of order I (1) and integration of order which means data is having constant mean, variance and autocorrelation etc after taking difference of data. If all the variables are stationary at first difference or higher order we use co-integration. The relationship between FDI and nexus of macroeconomic and institutional variables in the model was determined using co-integration methodology given by Johansen and Juselius, (1990). The study finds that there exists statistically significant relationship between financial soundness and economic growth. Table-3 shows results of Johansen’s test for cointegration test. The results of Johansen Cointegration tells us that λ max Statistics values are greater than Critical value λ max that means null hypothesis is rejected and alternative is accepted. Similarly, λ trace Statistics values are greater than Critical value λ trace that means also null hypothesis is rejected. When Null hypothesis is rejected and alternative hypothesis is accepted that means there exists long run relationship among variables. Above chart, summarizes that there are five long run relationships found in our research model. There exists a long run relationship between FDI and its determinants. But to check causality among the variables we apply Granger causality. The results of Granger causality are given below, by considering probability value to accept or reject null hypothesis. Table-4 shows alternate hypothesis and probability of all variables.

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan

- 475 -

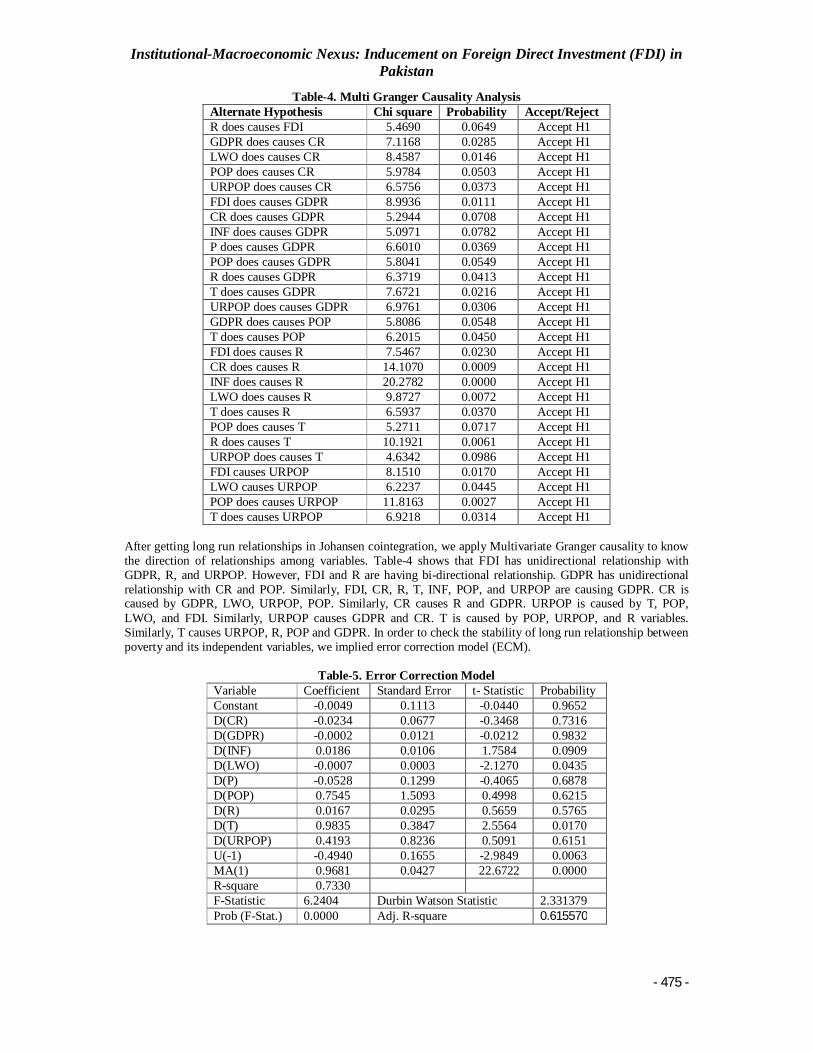

Table-4. Multi Granger Causality Analysis Alternate Hypothesis Chi square Probability Accept/Reject R does causes FDI 5.4690 0.0649 Accept H1 GDPR does causes CR 7.1168 0.0285 Accept H1 LWO does causes CR 8.4587 0.0146 Accept H1 POP does causes CR 5.9784 0.0503 Accept H1 URPOP does causes CR 6.5756 0.0373 Accept H1 FDI does causes GDPR 8.9936 0.0111 Accept H1 CR does causes GDPR 5.2944 0.0708 Accept H1 INF does causes GDPR 5.0971 0.0782 Accept H1 P does causes GDPR 6.6010 0.0369 Accept H1 POP does causes GDPR 5.8041 0.0549 Accept H1 R does causes GDPR 6.3719 0.0413 Accept H1 T does causes GDPR 7.6721 0.0216 Accept H1 URPOP does causes GDPR 6.9761 0.0306 Accept H1 GDPR does causes POP 5.8086 0.0548 Accept H1 T does causes POP 6.2015 0.0450 Accept H1 FDI does causes R 7.5467 0.0230 Accept H1 CR does causes R 14.1070 0.0009 Accept H1 INF does causes R 20.2782 0.0000 Accept H1 LWO does causes R 9.8727 0.0072 Accept H1 T does causes R 6.5937 0.0370 Accept H1 POP does causes T 5.2711 0.0717 Accept H1 R does causes T 10.1921 0.0061 Accept H1 URPOP does causes T 4.6342 0.0986 Accept H1 FDI causes URPOP 8.1510 0.0170 Accept H1 LWO causes URPOP 6.2237 0.0445 Accept H1 POP does causes URPOP 11.8163 0.0027 Accept H1 T does causes URPOP 6.9218 0.0314 Accept H1

After getting long run relationships in Johansen cointegration, we apply Multivariate Granger causality to know the direction of relationships among variables. Table-4 shows that FDI has unidirectional relationship with GDPR, R, and URPOP. However, FDI and R are having bi-directional relationship. GDPR has unidirectional relationship with CR and POP. Similarly, FDI, CR, R, T, INF, POP, and URPOP are causing GDPR. CR is caused by GDPR, LWO, URPOP, POP. Similarly, CR causes R and GDPR. URPOP is caused by T, POP, LWO, and FDI. Similarly, URPOP causes GDPR and CR. T is caused by POP, URPOP, and R variables. Similarly, T causes URPOP, R, POP and GDPR. In order to check the stability of long run relationship between poverty and its independent variables, we implied error correction model (ECM).

Table-5. Error Correction Model Variable Coefficient Standard Error t- Statistic Probability Constant -0.0049 0.1113 -0.0440 0.9652 D(CR) -0.0234 0.0677 -0.3468 0.7316 D(GDPR) -0.0002 0.0121 -0.0212 0.9832 D(INF) 0.0186 0.0106 1.7584 0.0909 D(LWO) -0.0007 0.0003 -2.1270 0.0435 D(P) -0.0528 0.1299 -0.4065 0.6878 D(POP) 0.7545 1.5093 0.4998 0.6215 D(R) 0.0167 0.0295 0.5659 0.5765 D(T) 0.9835 0.3847 2.5564 0.0170 D(URPOP) 0.4193 0.8236 0.5091 0.6151 U(-1) -0.4940 0.1655 -2.9849 0.0063 MA(1) 0.9681 0.0427 22.6722 0.0000 R-square 0.7330 F-Statistic 6.2404 Durbin Watson Statistic 2.331379 Prob (F-Stat.) 0.0000 Adj. R-square 0.615570

International Journal of Economics and Empirical Research. 2014, 2(11), 465-479.

- 476 -

In an error correction model, the short-run dynamics of the variables in the system are influenced by the deviation from equilibrium. Without a full dynamic specification of the model, it is impossible to find which of the possibilities will occur. Nevertheless, the short-run dynamics must be influenced by the deviation from the long-run relationship (Enders, 2010). The error correction term in ECM shows the speed of adjustment of variables in dynamic model over the period of time (see, Table-5). Now, we apply ECM test to know relationship on the basis of short run. In short run, INF, LWO, and T are having short run relationships as there p-values are significant that means there exist short run relationship among them. Similarly, Durbin Watson value is 2.331 that is acceptable and that respresents there is no multi-collinearity proble. Along with that R-square values show goodness of fit and its value is fine that shows goodness of our model (see Table-6). Table-6. Diagonestic Test

Diagonestic Test Ramsey RESET Test (Stability of model) 11.30362 (0.0023) Breusch-Pagan-Godfrey (Heteroskedasticity) 0.876771 (0.5571) Breusch-Godfrey ( Serial Correlation LM Test ) 8.473627 (0.2661) Wald Test (Multi collinearity test) 1.294274 (0.2893) F statistics without brackets and Probability values are given in brackets.

In order to check the validity of our research model, we apply following tests. Above tests like Ramsey RESET test check the stability of model, Breusch-Pagan-Godfrey checks the Heteroskedasticity, Breusch-Godfrey (Serial Correlation LM Test) checks the autocorrelation problems, Wald test checks Multi collinearity problem in our model. The results show that there is no above mentioned problem. Hence, our model is simply right and our results prove valid and correct. V. Conclusion and Recommendations The main objective of this study is to empirically analyze the relationship of foreign direct investment and variables (macro and institutional) in Pakistan, using Johansen co-integration analysis. In order to determine relationship between financial sector development and economic growth, we use a time series data from Economic surveys and World development indicators (WDI) database over a period of time i.e. 1973 to 2010. The research study concludes as per results after applying mentioned methodology of descriptive statistics, unit root test, cointegration test of Johasen Jesulius, Granger causality for checking causal relationship among variables i.e. direction of relationship and finally applied Error correction model. We find that inflation (INF), Law and Order conditions (LWO) and Taxation (T) have a significant impact on foreign direct investment (FDI) in short run. Foreign direct investment are largely depending upon inflation, Law and order conditions, and Taxation factors as measure of returns gets affected due to these factors. Political Instability, Law n Order & Corruption are major institutional hazards in diminishing foreign direct investment (FDI). If institutions are found engulfed in such problems of Political instability, Law and Order and corruption problems then institutions will be working on weak grounds. Causality analysis shows institutional impacts on economic determinants of foreign direct investment (FDI). Strong and proper working of institutions will increase efficacy of economic determinants that provide basis of foreign direct investment. Institutional stability is causing economic performance and thus inducing foreign direct investment (FDI). Our findings recommend that institutional variables should be controlled to have sound economic indicators like Inflation, Taxation and interest rate. These robust economic indicators will encourage foreign direct investment in the country. References Agosín, M. and Mayer, R. (2000). Foreign Investment in Developing Countries: Does it Crowd in Domestic

Investment? UNCTAD Discussion Paper 146, United Nations Publication, Geneva. Agrawal, P. (2000). Economic Impact of Foreign Direct Investment in South Asia. Working Paper, Indra

Gandhi Institute of Development Research, India. Al-Sadig, A. (2009). The Effects of Corruption on FDI Inflows. Cato Journal, 29(2), 44-50. Azam, M. and Khattak, N. R. (2009). Social and Political Factors Effects on Foreign Direct Investment in

Pakistan: 1971-2005. Gomal University Journal of Research, 25(1), 46-50. Anwar, S. and Nguyen, L. P. (2011). Foreign Direct Investment and Export Spillovers: Evidence from Vietnam.

International Business Review, 20, 177-193. Akmal, M. S. Ahmad, Q. M. Alam, S. and Butt, M. S. (2007). Long Run and Short-run Linkages between

Financial Development & Poverty Reduction in Pakistan. Journal of Social & Economic Policy, 1(4), 19-36.

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan

- 477 -

Ashfaque, H. K. (1997). Foreign Direct Investment in Pakistan: Policies and Trends. The Pakistan Development Review, 36(4), 959-985.

Atique, Z. Ahmad, M. H. and Azhar, U. (2004). The Impact of FDI on Economic Growth under Foreign Trade Regimes: A Case Study of Pakistan. The Pakistan Development Review, 43(2), 707-718.

Aqeel A. and Nishat, M. (2004). The Determinants of Foreign Direct Investment. The Pakistan Development Review, 43(4), 651-664.

Basu, P. and Guariglia, A. (2007). Foreign Direct Investment, Inequality, and Growth. Journal of Macroeconomics, 29 (4), 824-839.

Bevan, A. A. and Estrin, S. (2004). The Determinants of Foreign Direct Investment into European Transition Economies. Journal of Comparative Economics, 32(4), 775-787.

Blomstrom, M. and Persson, H. (1983). Foreign Investment and Spillover Efficiency in an Underdeveloped Economy: Evidence from the Mexican Manufacturing Industry. World Development, 11, 493-501.

Blonigen, B. A. (2005). A Review of the Empirical Literature on FDI Determinants. NBER Working Paper No. 11299, Atlantic Economic Journal.

Busse, M. and Hefeker, C. (2005). Political Risk, Institutions and Foreign Direct Investment. HWWA Discussion Paper No. 315.

Busse, M. and Groizard, J. L. (2008). Foreign Direct Investment, Regulation and Growth. Blackwell Publishing Ltd, 9600 Garsington Road, Oxford, OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA.

Caves, R. E. (1974). Multinational Firms, Competition, and Productivity in Host-Country Markets. Economica, 41, 176-193.

Chen, E. K. Y. (1983). Multinational Corporations and Technology Diffusion in Hong Kong Manufacturing. Applied Economics, 15, 309-321.

Dollar, D. and Kraay, A. (2002). Growth is Good for the Poor. Washington, D.C: World Bank, Workshop on Globalization and Poverty in Vietnam, Hanoi.

Dabla-Norris, E. Honda, J. Lahreche, A. and Verdier, G. (2010). FDI Flows to Low-Income Countries: Global Drivers and Growth Implications. IMF Working Paper No. 132

Dunning, J. H. (1996). Re-evaluating the Benefits of FDI. In: International Thomson Press on behalf of UNCTAD, Division on Transnational Corporations and Investment (ed.). International Thomson Business Press, London.

Driffield, N. (2001). Inward Investment and Host Country Market Structure: The Case of the UK. Review of Industrial Organization, 18, 363-378.

Egger, P. and Pfaffermayr, M. (2004). The Impact of Bilateral Investment Treaties on Foreign Direct Investment. Journal of Comparative Economics, 32(4), 788-804.

Figini, P. and Gorg, H. (2006). Does Foreign Direct Investment Affect Wage Inequality? An Empirical Investigation. Institute for the Study of Labor (IZA), Discussion Paper 2336. Bonn.

Fairchild, L. and Sosin, K. (1986). Evaluating Differences in Technological Activity between Transnational and Domestic Firms in Latin America. Journal of Development Studies, 22, 697-708.

Garibaldi, P. Mora, N. Sahay, R. Zettelmeyer, J. (1999). What Moves Capital to Transition Economies?” IMF Conference, Washington D.C

Gropp, R. and Kostial, K. (2000). The Disappearing Tax Base: Is Foreign Direct Investment Eroding Corporate Income Taxes? ECB Working Paper No.31. European Central Bank, Frankfurt.

Gopinath, M. and Echeverria, R. (2004). Does Economic Development Impact the Foreign Direct Investment-Trade Relationship? A Gravity-Model Approach. American Journal of Agriculture Economics, 86(3), 782-787.

Hanson, G. H. (2003). What has Happened to Wages in Mexico Since NAFTA? Implications for Hemispheric Free Trade. National Bureau of Economic Research, NBER Working Paper 9563. Cambridge, MA.

Hayami, Y. (2001). Development Economics: From the Poverty to the Wealth of Nations. Oxford University Press, Oxford.

Hashim, S. Munir, A. and Khan, A. (2009). Foreign Direct Investment in Telecommunication Sector of Pakistan: An Empirical Analysis. Journal of Managerial Sciences, 3(1), 111-123.

Hejazi, W. (2002). Foreign Direct Investment and Domestic Capital Formation. Industry Canada Working Paper No. 36, Industry Canada, Ottawa.

Hania, J. P. (1999). Determinanten van Buitenlandse Directe Investeringen in Centraal en Oost Europa: een Cross-Sectie Analyse”. De Nederlandse Bank, Afdeling Wetenschappelijk Onderzoek en Econometrie, Onderzoeksrapport No. 587

Kakwani, N. (2000). Growth and Poverty Reduction: An Empirical Analysis. Asian Development Review, 18(2), 256-275.

International Journal of Economics and Empirical Research. 2014, 2(11), 465-479.

- 478 -

Klein M. Aaron, C. Hadjmichael, B. (2001). Foreign Direct Investment and Poverty Reduction. New Horizons and Policy Challenges for Foreign Direct Investment in the 21st Century, Mexico.

Khan, M. A. (2007). Foreign Direct Investment and Economic Growth: The Role of Domestic Financial Sector. PIDE Working Papers 2007:18. Islamabad, Pakistan.

Kim, D. D. K. and Seo, J. S. (2003). Does FDI Inflow Crowd out Domestic Investment in Korea? Journal of Economic Studies, 30, 605-622.

Lipsey, R. E. (2000). Interpreting Developed Countries’ Foreign Direct Investment. NBER Working Paper No. 7810, National Bureau of Economic Research, Cambridge, MA.

Lipsey, R. E. and Sjoholm, F. (2004). Foreign Direct Investment, Education and Wages in Indonesian Manufacturing. Journal of Development Economics, 73(1), 415-422.

Lansbury, M. Pain, N. and Smidkova, K. (1996). Foreign Direct Investment in Central Europe since 1990: an Econometric Study”. National Institute of Economic and Social Research, Vol. 156

Mahmood, H. and Chaudhary, A. R. (2009). Application of Endogeous Growth Model to the Economy of Pakistan: A Cointegration Approach. Pakistan Journal of Commerce and Social Sciences, 2, 16-24.

Mughal, M. (2009). Boom or Bane-Role of FDI in the Economic Growth of Pakistan. MRPA Paper No. 16468, Munich Library, Germany.

Mudambi, R. (1999). Multinational Investment Attraction: Principle Agent Considerations. International Journal of Economics of Business, 6, 65-79.

Markusen, J. R. (2001). Contracts, Intellectual Property Rights and Multinational Investment in Developing Countries. Journal of International Economics, 53, 189-204.

Mah, J. S. (2002). The Impact of Globalization on Income Distribution: The Korean Experience. Applied Economics Letters, 9(15), 1007-1009.

Nunnenkamp, P. Schweickert, R. and Wiebelt, M. (2007). Distributional Effects of FDI: How the Interaction of FDI and Economic Policy Affects Poor Households in Bolivia. Development Policy Review, 25 (4), 429-450.

Nishat, M. and Anjum, A. (1998). The Empirical Determinants of Direct Foreign Investment in Pakistan. Saving and Development, XXII (4), 45-56.

Nishat, M. and Anjum, A. (2004). The Determinants of Foreign Direct Investment in Pakistan. The Pakistan Development Review, 43(2), 651-664.

Ozturk, I. and Kalyoncu, H. (2007). Foreign Direct Investment and Growth: An Empirical Investigation Based on Cross-Country Comparidson. Economia Internazionale, 60(1), 75-82.

Portes, R. and Rey, H. (2005). The Determinants of Cross-Border Equity Flows. Journal of International Economics, 65(2), 269-296.

Raff, H. and Srinivasan, K. (1998). Tax Incentives for Import Substituting Foreign Investment: Does Signaling Play a Role? Journal of Public Economics, 67, 167-193.

Razin, A. (2002). FDI Contribution to Capital Flows and Investment in Capacity.NBER Working Paper No. 9204, Cambridge, MA.

Stein E. and Daude C. (2001). Institutions, Integration and the Location of Foreign Direct Investment. Inter-American Development Bank, Washington, DC

Shabbir, Tayyab and M. Azhar (1992). The Effects of Foreign Private Investment on Economic Growth in Pakistan. Pakistan Development Review, 31(4), 831-841.

Shahbaz, M. Awan, R. U. and Ali, L. (2008). Bi-Directional Causality between FDI & Savings: A Case Study of Pakistan. International Research Journal of Finance and Economics, 17, 75-83.

Saeed, N. (2001). An Economic Analysis of Foreign Direct Investement and Its Impact on Trade and Growth in Pakistan. Unpublished PhD Dissertation submitted to Islamia University, Bhahawal Pure, Pakistan.

Shahbaz, M. Aamir, N. and Sabihuddin, M. B. (2007). Rural-Urban Income Inequality under Financial Development and Trade Openness in Pakistan: The Econometric Evidence. The Pakistan Development Review, 46(4), 657-672.

Shah, Z. and Masood, Q. A. (2003).The Determinants of Foreign Investment in Pakistan: An Empirical Investigation. The Pakistan Development Review, 42(4), 697-714.

Shah, Z. (2003). Fiscal Incentives, The cost of Capital and Foreign direct Investment in Pakistan. A Research paper submitted to Pakistan Institute of Development Economic (PIDE) to be presented in the Annual Conference, Islamabad, Pakistan.

Siddiqui R. and Kemal A. R. (2006). Poverty-Reducing or Poverty Inducing? A CGE-based Analysis of Foreign Capital Inflows in Pakistan. Pakistan Institute of Development Economics, Working Papers 2006:2, Islamabad, Pakistan.

Institutional-Macroeconomic Nexus: Inducement on Foreign Direct Investment (FDI) in Pakistan

- 479 -

Todaro, M. P. and Smith, S. C. (2003). Economic Development. 8th Edition, Pearson Education Limited, Essex, England.

Walsh, J. P. and Yu, J. (2010). Determinants of Foreign Direct Investment: a Sectoral and Institutional Approach. IMF Working Paper No. 187.

Wang, J. Y. and Blomstrom, M. (1992). Foreign Investment and Technology Transfer-A Simple Model. European Economic Review, 36, 137-155.

Whalley, J. and Xin, X. (2010). China’s FDI and non-FDI Economies and the Sustainability of Future High Chinese Growth. China Economic Review, 21, 123-135.

Yousaf, M. M. Hussain, Z. and Ahmad, N. (2008). Economic Evaluation of Foreign Direct Investment in Pakistan. Pakistan Development and Social Review, 46(1), 37-56.

Related Documents