COVER INSPIRE INNOVATE INTEGRATE “Creating breakthroughs to close the growth gap and deliver new sources of value.” DR. HITENDRA PATEL Joint Message of the Chairman and President | Page 06 CHI at 30: An Enduring Belief in Cebu | Page 22 How we create value | Page 32 “While cities are the nexus of many of our most dramatic challenges, they also represent the opportunity to resolve them with cross-cutting policies, programs and urban design.” PETER CALTHORPE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COVER

CE

BU

HO

LDIN

GS

, INC

. 2018 IN

TEGR

ATED

REPO

RT

INSPIREINNOVATEINTEGRATE

“Creating breakthroughs to close the growthgap and deliver new sources of value.”DR. HITENDRA PATEL

Joint Message of the Chairman and President| Page 06

CHI at 30: An Enduring Belief in Cebu | Page 22

How we create value | Page 32

“While cities are the nexus of many of our most dramatic challenges, they also represent the opportunity to resolve them with cross-cutting policies, programs and urban design.”

PETER CALTHORPE

Now a benchmark for excellence in property development and good corporate governance in the region, our Company has grown mixed-use estates that

have driven business growth in the Visayas region over the past three decades.

20F Ayala Center Cebu Tower, Bohol St., Cebu Business Park, Cebu City, Cebu 6000

Tel: (63 32) 888 3700www.cebuholdings.com

ANICETO V. BISNAR, JR.PRESIDENT

CK M Y RED 80K 40K K C 80C 40CM CY K C40M K M Y 80Y 40Y PaperM Y BLUE 80MGREEN CK M Y RED 80K 40K K C 80C 40CM CY K C40M K M Y 80Y 40Y PaperM Y BLUE 80MGREEN CK M Y RED 80K 40K K C 80C 40CM CY K C40M K M Y 80Y 40Y PaperM Y BLUE 80MGREEN CK M Y RED 80K 40K K C 80C 40CM Y GREEN

PETER CALTHORPECo-founder, Congress for New Urbanism

Sustainable development is an idea just a little older than Cebu Holdings, Inc. (CHI).

In 1987, the World Commission on Environment and Development called for “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” Among the insights in the Brundtland Report, named after the Norwegian prime minister who led the body, was that more people would live in cities than in rural areas in the 21st century. It envisioned a world where public policy and the choices of corporations and institutions would provide social and economic advantages without harming the environment that supported both.

CHI began in 1988, with an innovative deal that eventually transformed a former golf course into Cebu’s first integrated and master-planned estate. The success of its Cebu Business Park and the Cebu I.T. Park that soon followed draws from the sustainable development ideals that surrounded CHI’s birth.

About six years after the Brundtland Report, American architect and urban planner Peter Calthorpe co-founded the Congress for New Urbanism. Three tenets anchor his advocacy for sustainable design: that buildings and spaces must fill individual needs, that design must enable diversity, and that it must conserve natural landscapes by nurturing “an ethic of reuse and repair.”

Our cities play a powerful role in addressing the challenges of mass urbanization and climate change. “While cities are the nexus of many of our most dramatic challenges, they also represent the opportunity to resolve them with cross-cutting policies, programs and urban design,” Calthorpe wrote in nextcity.org.

Well-planned, mixed-use estates connected to transportation and jobs use less energy and water, release less carbon, and create stronger communities. That’s a vision CHI embraces.

In its first 30 years, Cebu Holdings has helped transform Cebu into a vibrant and productive community, by building integrated estates where more than 94,000 individuals now create work that shows the best of what Filipinos can do. Using everything it has learned from its flagship estates and the evolving ideas of sustainable development and design, CHI is now building new estates like Gatewalk Central in Mandaue City and Seagrove in Lapu-Lapu City.

Inspired ideas and innovative systems bring to life communities that are pedestrian-friendly, inclusive, and consistently built on a human scale. This is both our hope and our promise: diverse and interconnected economic centers that give the present generation the space to pursue its dreams, while protecting the ability of future generations to do the same.

INSPIREINNOVATEINTEGRATE

2018 INTEGRATED REPORT 3

ABOUT THIS REPORT

KEY FEATURES AND SCOPE

» 12th combined report and 2nd Integrated report covering our performance on the financial, corporate governance, economic, social, and environment aspects

» Contribution to the UN SDGs and Four Focus Areas of parent company (Ayala Land, Inc.)

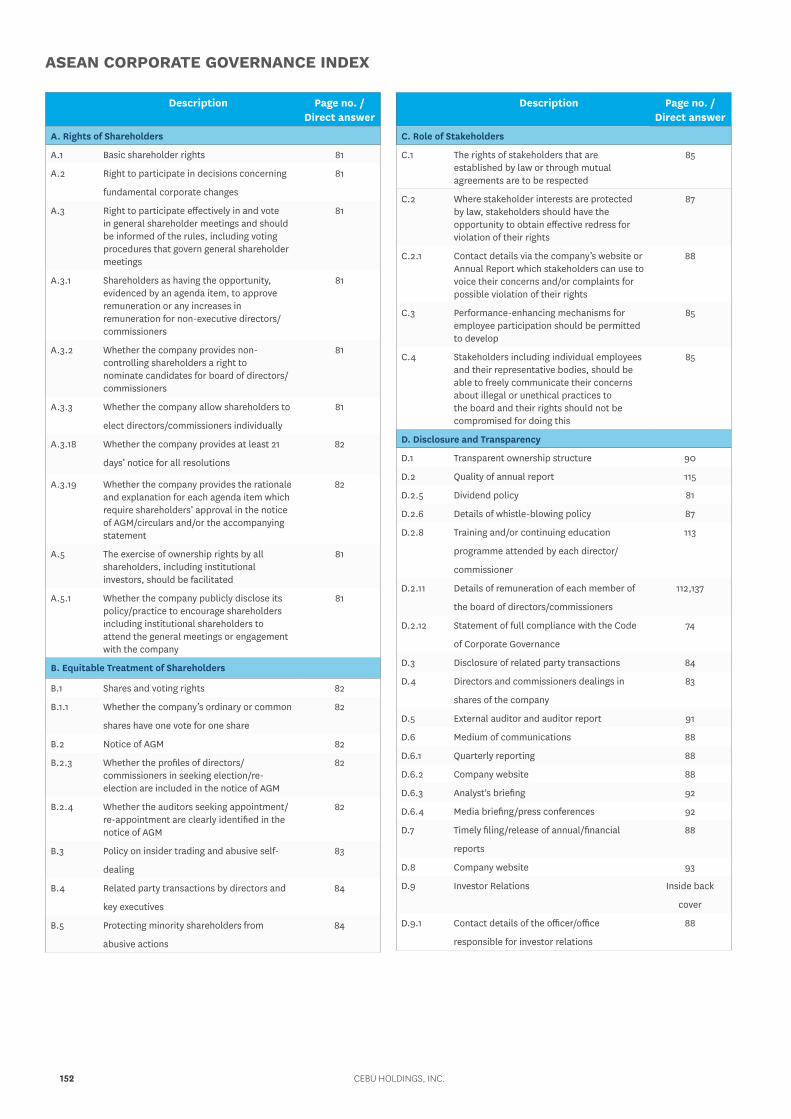

» This report is prepared in accordance with GRI Standards: Core Option and ASEAN Corporate Governance Scorecard (ACGS) – see pages 152 to 153 for the ACGS Index.

» Presents consolidated data from fiscal year January 1 to December 31, 2018 coming from our internal business units and those of our general contractors for property management (Ayala Property Management Corporation) and construction (Makati Development Corporation)

» Discusses the merger of CHI with major subsidiary, Cebu Property Ventures and Development Corporation

» Where possible, this report provides three years of historical information so that there is sufficient basis for comparison.

Inspire. Innovate. Integrate. details how Cebu Holdings, Inc. (CHI) continued to integrate sustainability principles into the

company’s core strategies and operations in 2018.

Building on the lessons learned from our first integrated report, this report continues to use the <IR> Framework to finetune the way we develop and deliver our products and services.

By continuing to subscribe to the <IR> Framework and GRI Standards, we monitor and manage all the topics that are material to the economic, social, and environmental aspects of our operations.

In celebration of CHI’s 30th anniversary, we take this opportunity to reassess our achievements over the past three decades toward sustainable development and responsible growth.

ADDITIONAL REFERENCE

The company’s operational and financial performance filed with the Securities and Exchange Commission (SEC) is reflected in the Information Statement sent to stockholders and is available at our corporate website, via www.cebuholdings.com.

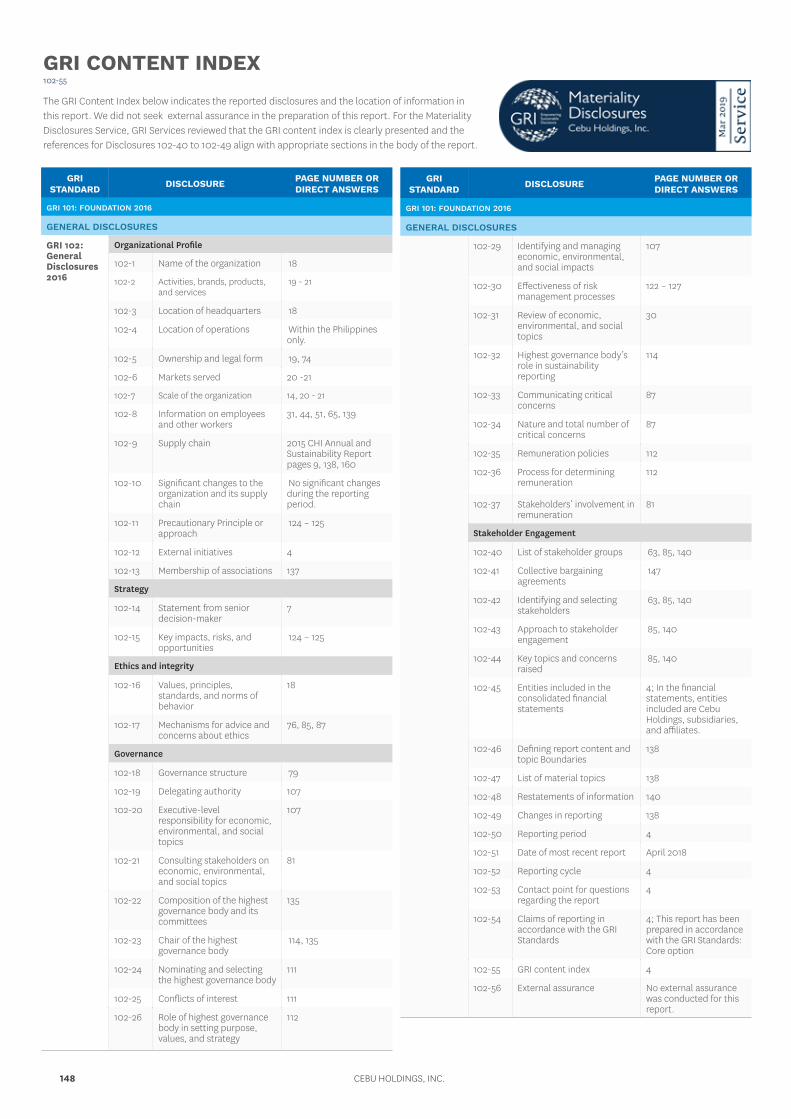

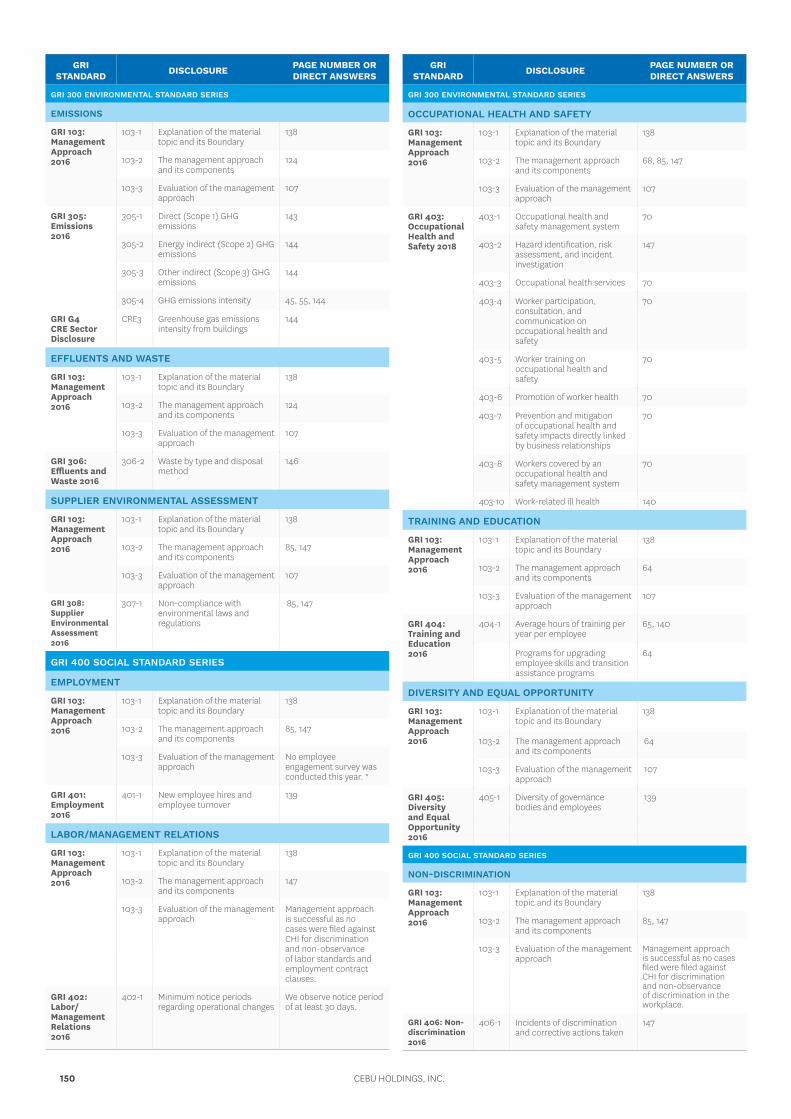

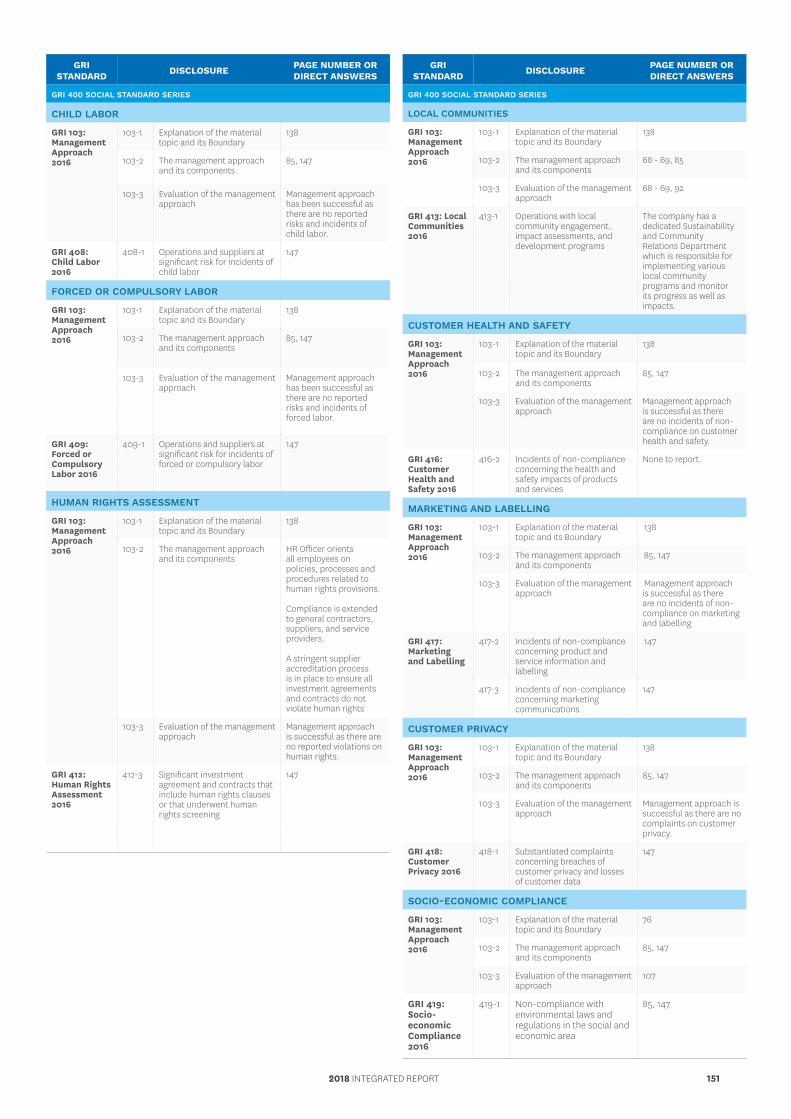

As in our past five reports, this report has successfully completed the GRI Materiality Disclosures Service which verifies that GRI 102: General Standard Disclosures 2016 102-40 to 102-49 were correctly located in both the GRI Content Index (see pages 148 to 151) and in the pages of this report.

FEEDBACK Feedback and comments about our report can be emailed to [email protected].

102-54, 102-45

CEBU HOLDINGS, INC.4

1

4

2

5

3

6

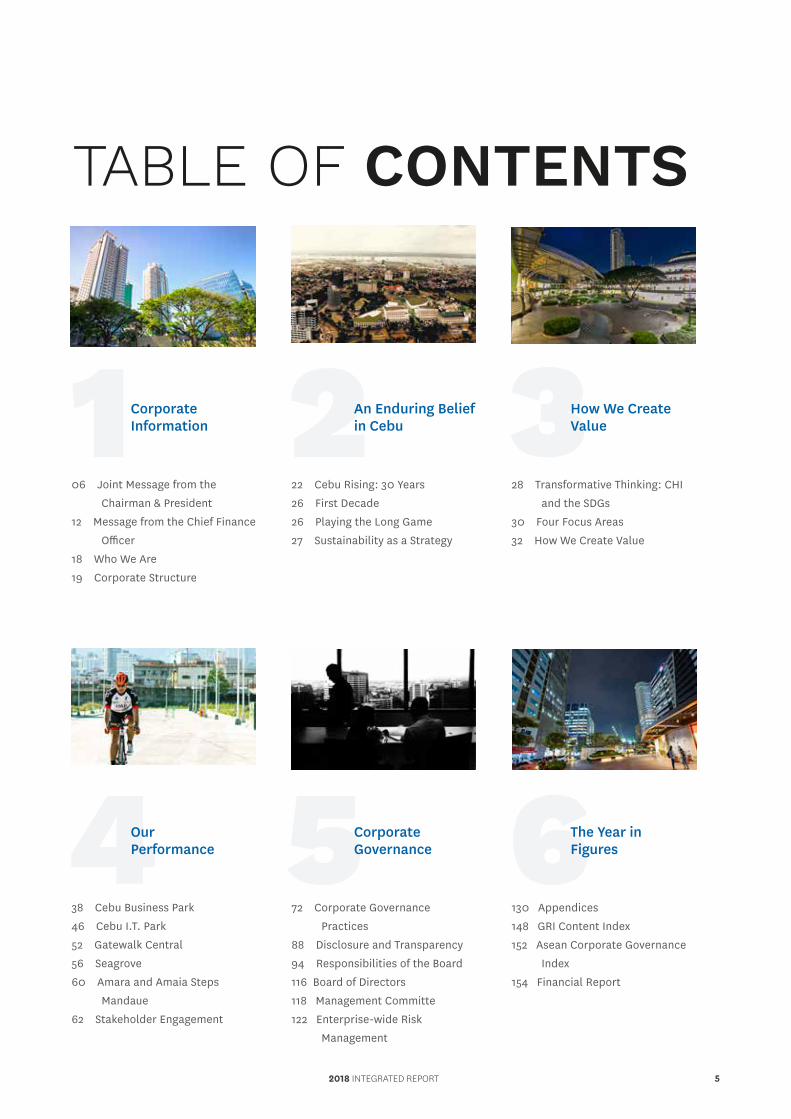

TABLE OF CONTENTS

CorporateInformation

OurPerformance

An Enduring Belief in Cebu

How We Create Value

CorporateGovernance

The Year in Figures

06 Joint Message from the

Chairman & President

12 Message from the Chief Finance

Officer

18 Who We Are

19 Corporate Structure

38 Cebu Business Park

46 Cebu I.T. Park

52 Gatewalk Central

56 Seagrove

60 Amara and Amaia Steps

Mandaue

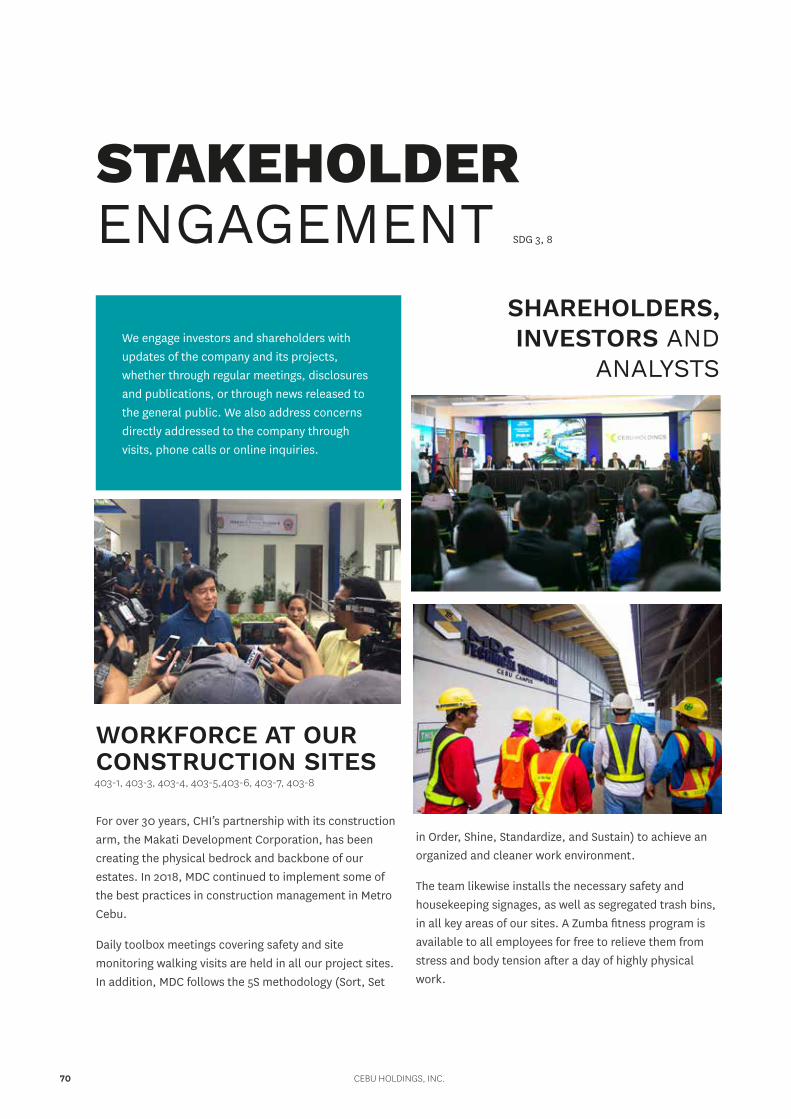

62 Stakeholder Engagement

22 Cebu Rising: 30 Years

26 First Decade

26 Playing the Long Game

27 Sustainability as a Strategy

72 Corporate Governance

Practices

88 Disclosure and Transparency

94 Responsibilities of the Board

116 Board of Directors

118 Management Committe

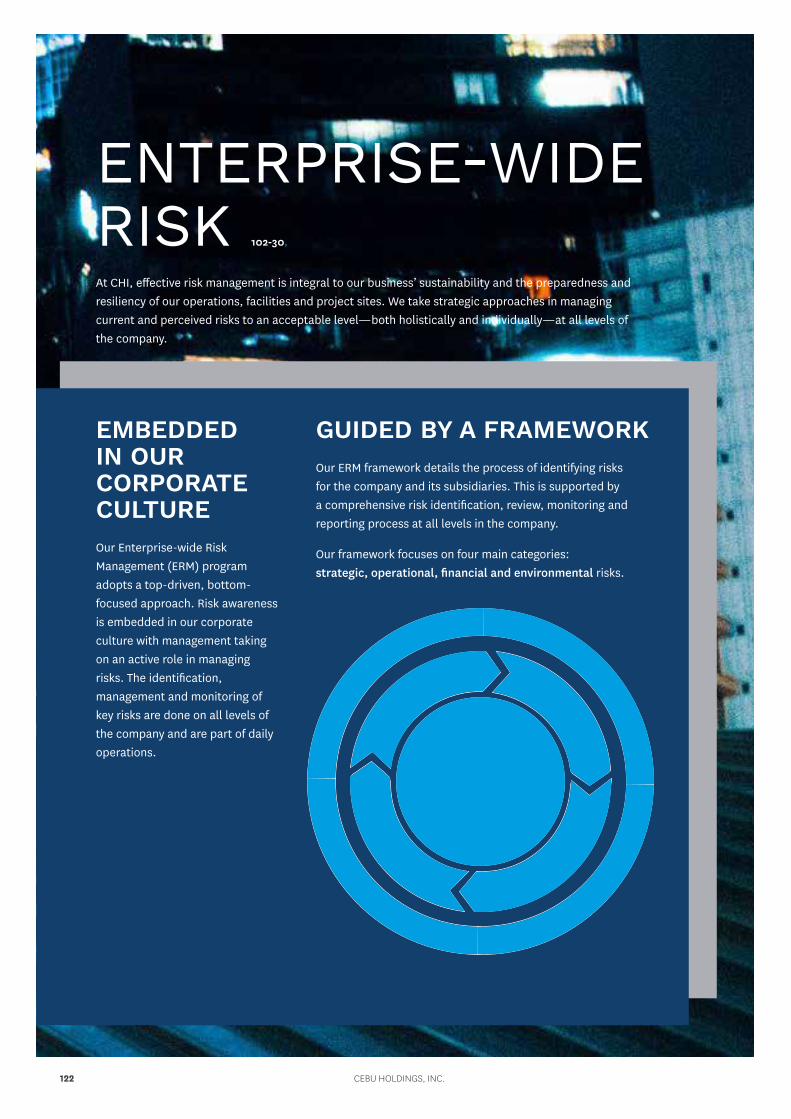

122 Enterprise-wide Risk

Management

28 Transformative Thinking: CHI

and the SDGs

30 Four Focus Areas

32 How We Create Value

130 Appendices

148 GRI Content Index

152 Asean Corporate Governance

Index

154 Financial Report

2018 INTEGRATED REPORT 5

Cebu Holdings’ vision has always

been about enriching the lives of the

communities we serve. In the years

to come, we will continue to improve

corporate and shareholder value by

remaining true to this vision and by

providing opportunities for sustainable

growth and development.

JOINT MESSAGE FROM THE CHAIRMAN & PRESIDENT 102-14

HIGHLIGHTS

167

257,219

94,000+

HECTARES

SQUARE METERS

JOBS

Master-planned developments

Generated at Cebu Business Park and Cebu I.T. Park

Gross Leasable Area in operation

Cebu Holdings, Inc. (CHI) marks its 30th year in business as one of the country’s premier property developers and a leading advocate of sustainable land development.

Now a benchmark for excellence in property development and good corporate governance in the region, our Company has grown mixed-use estates that have driven business growth in the Visayas region over the past three decades. We have also delivered concrete sustainability solutions at scale, proving that a profitable business can grow parallel with social and environmental values.

Our unwavering vision to bring inclusive economic growth has enriched our sense of community and our pride of place, while contributing to Cebu’s unprecedented development over the years.

30TH YEAR MILESTONESWe are pleased to celebrate our 30th founding anniversary as a record year. Revenues significantly grew by 20 percent to P3.7 billion versus 2017’s P3.1 billion. Net income is at a record high at ₱857.1 million, 14 percent higher than the previous year’s P753.4 million.

Since breaking ground in Cebu Business Park in February 1990, we have progressively expanded our initial 50-hectare asset base to a total of 167.2 hectares as of end 2018. More importantly, we have now transformed and enriched 155.9 hectares of this total landbank into thriving estates, commercial districts, retail destinations, and residential communities.

2018 INTEGRATED REPORT 7

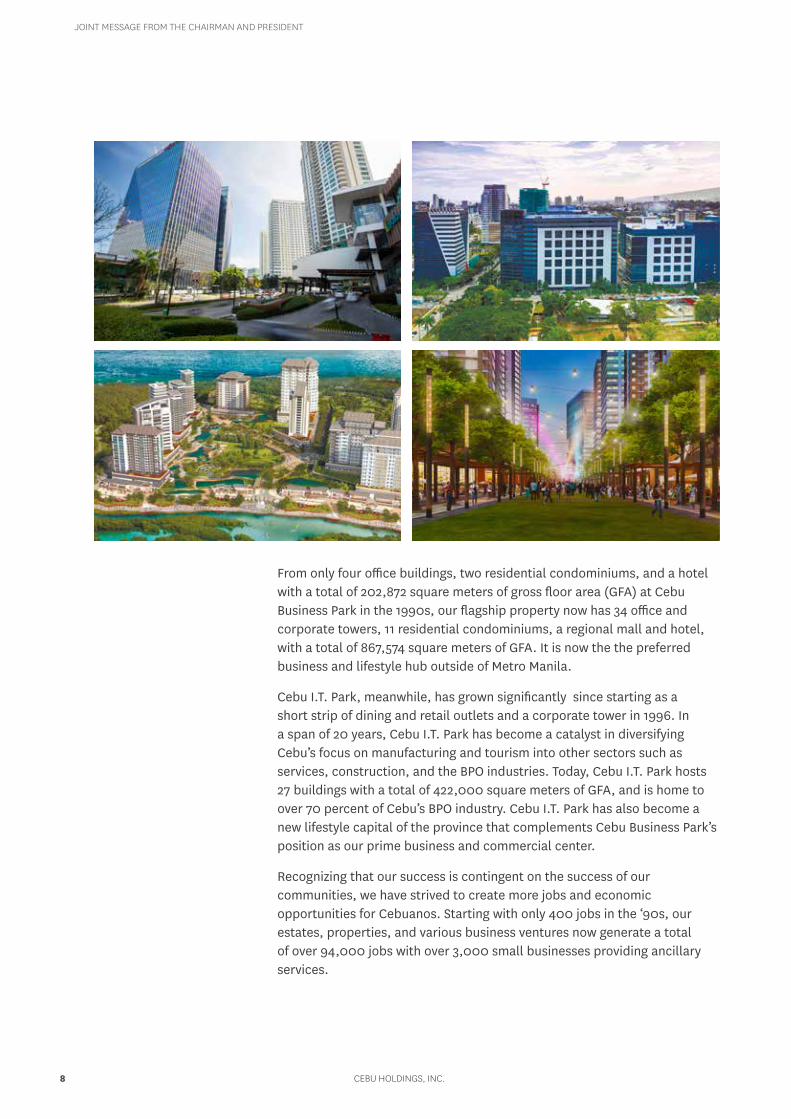

From only four office buildings, two residential condominiums, and a hotel with a total of 202,872 square meters of gross floor area (GFA) at Cebu Business Park in the 1990s, our flagship property now has 34 office and corporate towers, 11 residential condominiums, a regional mall and hotel, with a total of 867,574 square meters of GFA. It is now the the preferred business and lifestyle hub outside of Metro Manila.

Cebu I.T. Park, meanwhile, has grown significantly since starting as a short strip of dining and retail outlets and a corporate tower in 1996. In a span of 20 years, Cebu I.T. Park has become a catalyst in diversifying Cebu’s focus on manufacturing and tourism into other sectors such as services, construction, and the BPO industries. Today, Cebu I.T. Park hosts 27 buildings with a total of 422,000 square meters of GFA, and is home to over 70 percent of Cebu’s BPO industry. Cebu I.T. Park has also become a new lifestyle capital of the province that complements Cebu Business Park’s position as our prime business and commercial center.

Recognizing that our success is contingent on the success of our communities, we have strived to create more jobs and economic opportunities for Cebuanos. Starting with only 400 jobs in the ‘90s, our estates, properties, and various business ventures now generate a total of over 94,000 jobs with over 3,000 small businesses providing ancillary services.

CEBU HOLDINGS, INC.8

JOINT MESSAGE FROM THE CHAIRMAN AND PRESIDENT

Now a benchmark for excellence

in property development and good

corporate governance in the region, our

Company has grown mixed-use estates

that have driven business growth in

the Visayas region over the past three

decades.

Boosted by this surge in economic activity and driven by a more

cohesive strategy and tighter organizational structure, we are

proud to report that our Company continues to be at a strong

position at the end of 2018.

As we created more platforms for larger economic opportunities, we likewise intensified our conservation and preservation efforts as part of our continuing sustainability initiatives. We increased our efficiency in the use of our resources as well as managed waste and emissions of our operations. We improved pedestrian mobility and transit connectivity within our estates, by enhancing the public transport network, making our streets more walkable, and opening two new access roads at Cebu I.T. Park. We continue to champion environmental initiatives such as Assisted Natural Regeneration of identified carbon forest sinks, waterway and coastal clean-ups, and native-tree growing.

EXECUTING KEY STRATEGIC PRIORITIES IN 2018Our Company has managed to steer through 30 years of a constantly changing business environment to become one of Cebu’s strongest and most dynamic companies. This held especially true in the past year, as we maximized resources and seized opportunities brought by the country’s continued steady rise as one of Asia’s best-performing markets.

The Philippine economy continued to sustain high growth rates, driven by a rise in our exports and strong domestic consumption and public-sector spending based on reviews by the Oxford Business Group and other economic think tanks.

Boosted by this surge in economic activity and driven by a more cohesive strategy and tighter organizational structure, we are proud to report that our Company continues to be at a strong position at the end of 2018. Total assests grew by 28 percent to P26.3 billion, and stockholder’s equity grew by 15 percent versus last year’s.

We continue to enhance our existing estates while developing new growth centers in Cebu. In August 2018, Seda Ayala Center Cebu in Cebu Business Park opened with 301 rooms. We also broke ground for The Flats at both Cebu Business Park and Cebu I.T. Park last December 2018. Once completed, these innovative shared living spaces will offer a total of 852 rooms.

CEBU HOLDINGS, INC.10

JOINT MESSAGE FROM THE CHAIRMAN AND PRESIDENT

ANICETO V. BISNAR, JR. PRESIDENT

ANNA MA. MARGARITA B. DY CHAIRMAN

Central Bloc, the 2.2-hectare mixed development at Cebu I.T. Park retail will open in 2019. Upon completion, this development will have a regional mall, two office towers and a Seda hotel.

ACCELERATING DEVELOPMENTWe are optimistic to be celebrating our 30th anniversary at a time when the future of retail and tourism in Cebu is at its brightest. Demand for tourism infrastructure and retail spaces in and around Cebu City continues to grow, and CHI is well-prepared to capture a significant share of these opportunities.

Already, we have made proactive strides toward expanding into new markets and replicating our success in Cebu Business Park and Cebu I.T. Park into other key cities in Metro Cebu, such as Mandaue and Lapu-Lapu.

Construction for our two new estates in key cities in Metro Cebu remains on track. Land development is already complete and mall construction is ongoing at Gatewalk Central in Mandaue City, while land development at Seagrove in Lapu-Lapu City is also underway.

With the expected opening of various developments including Central Bloc in Cebu I.T. Park in 2019, Seagrove in 2020, and Gatewalk Central in 2021, we

will reach a total of 304,222 square meters retail GLA, 219,119 square meters office GLA, three hotels with 716 rooms and two dormitories with 852 rooms in the next five years – making us the largest full-line property developer in the Visayas.

INTENSIFYING SUSTAINABLE CHANGE Throughout the last 30 years, Cebu Holdings has become an intrinsic part of Cebuano society. We have hosted communal programs and activities that are now integral to the lives of Cebuanos. Our communities have celebrated their own personal milestones in our malls. We have partnered with various barangays to accelerate job creation. Ultimately, we have strived to build enduring Cebuano institutions that serve society at large and not only our immediate corporate goals.

Cebu Holdings’ vision has always been about enriching the lives of the communities we serve. In the years to come, we will continue to improve corporate and shareholder value by remaining true to this vision and by providing opportunities for sustainable growth and development.

We thank all our customers, partners, employees, and the entire province of Cebu for 30 years of growth and innovation. Here’s to another 30 years of unity and heightened collaboration.

2018 INTEGRATED REPORT 11

With our business drivers in place, we reached

major financial milestones as we marked our

30th year in 2018. Net income after tax was at

an all-time high as we hit P857.1 million, up by

14 percent from the previous year.

After three decades of operation, Cebu Holdings, Inc. (CHI) has established its position as the leading full-line real estate developer in Cebu with a wide range of

product offerings, strategically positioned to take advantage of opportunities in the market.

With our business drivers in place, we reached major financial milestones as we marked our 30th year in 2018. Net income after tax was at an all-time high as we hit P857.1 million, up by 14 percent from the previous year. Revenue registered 20 percent growth to P3.7 billion versus the previous year’s P3.1 billion.

PROGRESS MADE ACROSS ALL BUSINESS LINESThe strong performance of our business lines – particularly commercial leasing and residential sales – bolstered growth in our revenues. This reflected a solid year of gains and progress, as we increased our operating earnings by 16 percent, while continuing to fine-tune our operational focus.

Leasing income composed majority of our earnings at 59 percent or P2.2 billion. Our mall business continued to be the major contributor of our leasing revenue, which also continued to show steady growth, reflecting the upbeat trend in retail, which was boosted by the continued upswing of tourist arrivals and spending. Various studies, including Colliers’ recent economic outlook survey for Cebu, show this trend continuing well into the next few years.

Meanwhile, office leasing also remains strong with full lease-out of the four eBloc towers, Ayala Center Cebu Tower, and new- comer Tech Tower. Total gross leasable office space reached 128,119 square meters, making CHI dominate the Cebu market at 14 percent market share.

HIGHLIGHTS

3.7B

857M

26.3B

324M

REVENUE

NET INCOME

TOTAL ASSETS

DIVIDEND AMOUNT

3.1B2.7B3.7B

753M680M827M

20.6B19.6B19.7B

288M230M230M

201720162015

201720162015

201720162015

201720162015

MESSAGE FROM THE CHIEF FINANCE OFFICER

2018 INTEGRATED REPORT 13

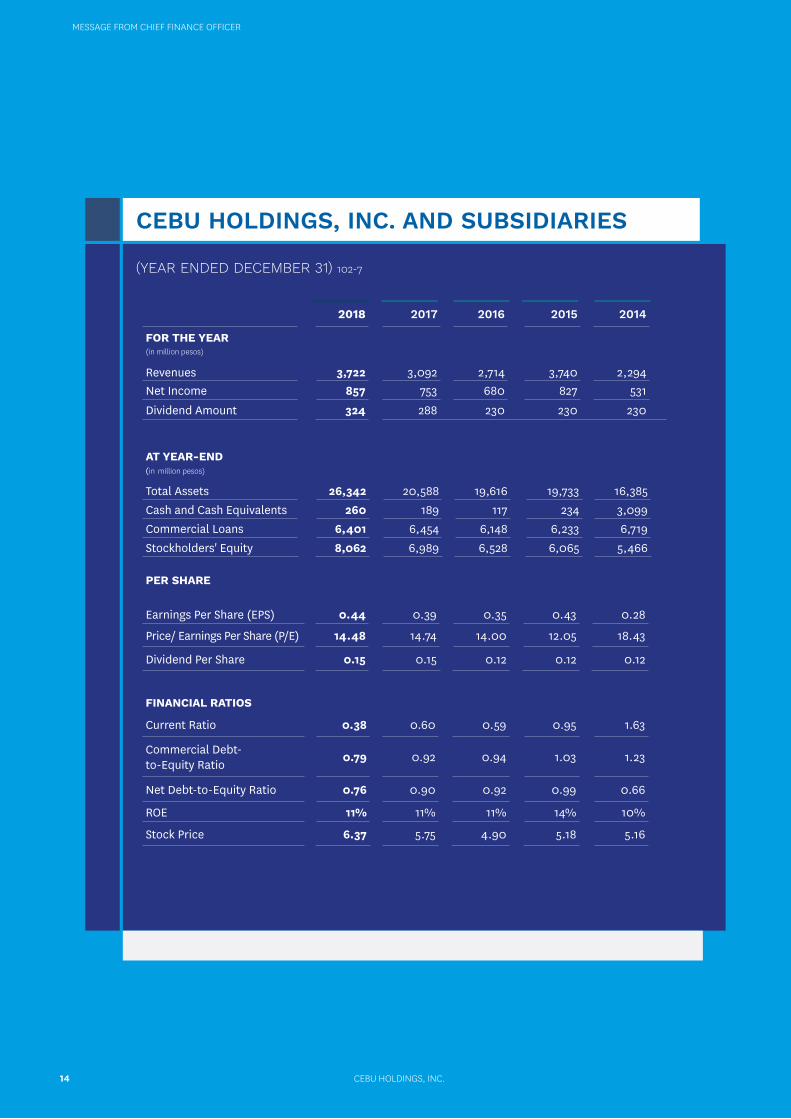

CEBU HOLDINGS, INC. AND SUBSIDIARIES

FINANCIAL RATIOS

Current Ratio 0.38 0.60 0.59 0.95 1.63

Commercial Debt-to-Equity Ratio 0.79 0.92 0.94 1.03 1.23

Net Debt-to-Equity Ratio 0.76 0.90 0.92 0.99 0.66

ROE 11% 11% 11% 14% 10%

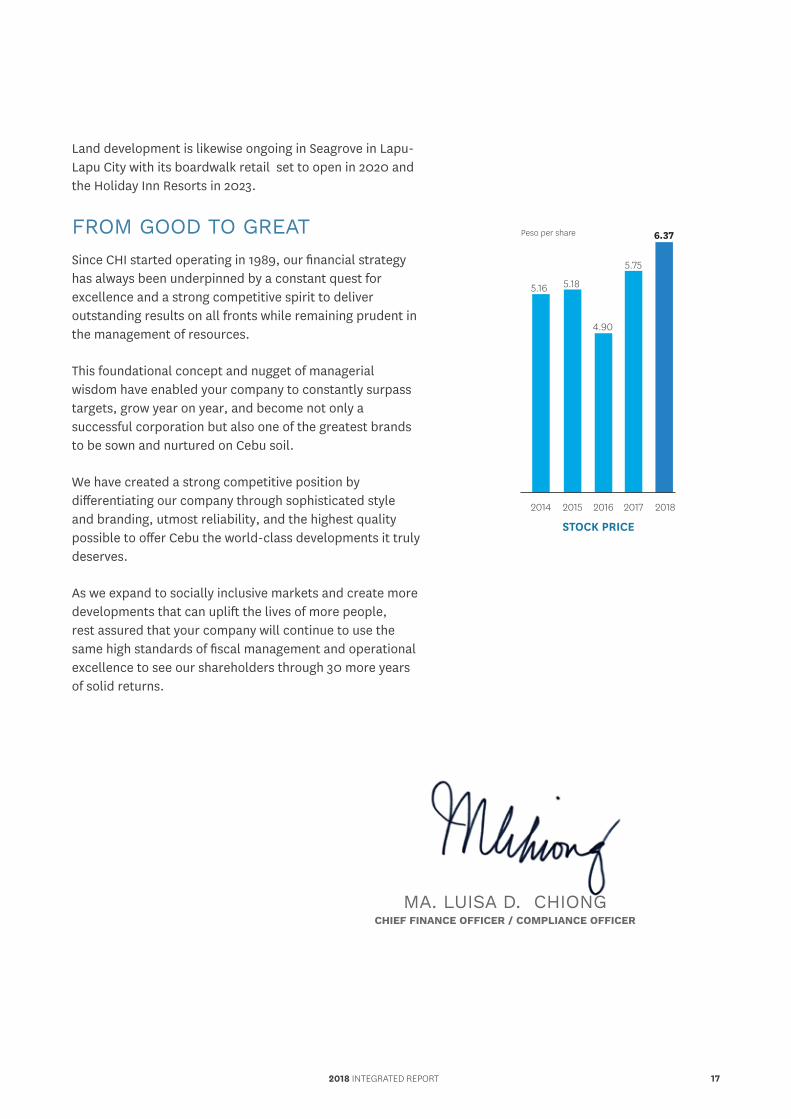

Stock Price 6.37 5.75 4.90 5.18 5.16

2018 2017 2016 2015 2014

FOR THE YEAR(in million pesos)

Revenues 3,722 3,092 2,714 3,740 2,294Net Income 857 753 680 827 531Dividend Amount 324 288 230 230 230

PER SHARE

Earnings Per Share (EPS) 0.44 0.39 0.35 0.43 0.28

Price/ Earnings Per Share (P/E) 14.48 14.74 14.00 12.05 18.43

Dividend Per Share 0.15 0.15 0.12 0.12 0.12

AT YEAR-END(in million pesos)

Total Assets 26,342 20,588 19,616 19,733 16,385Cash and Cash Equivalents 260 189 117 234 3,099Commercial Loans 6,401 6,454 6,148 6,233 6,719Stockholders' Equity 8,062 6,989 6,528 6,065 5,466

(YEAR ENDED DECEMBER 31) 102-7

CEBU HOLDINGS, INC.14

MESSAGE FROM CHIEF FINANCE OFFICER

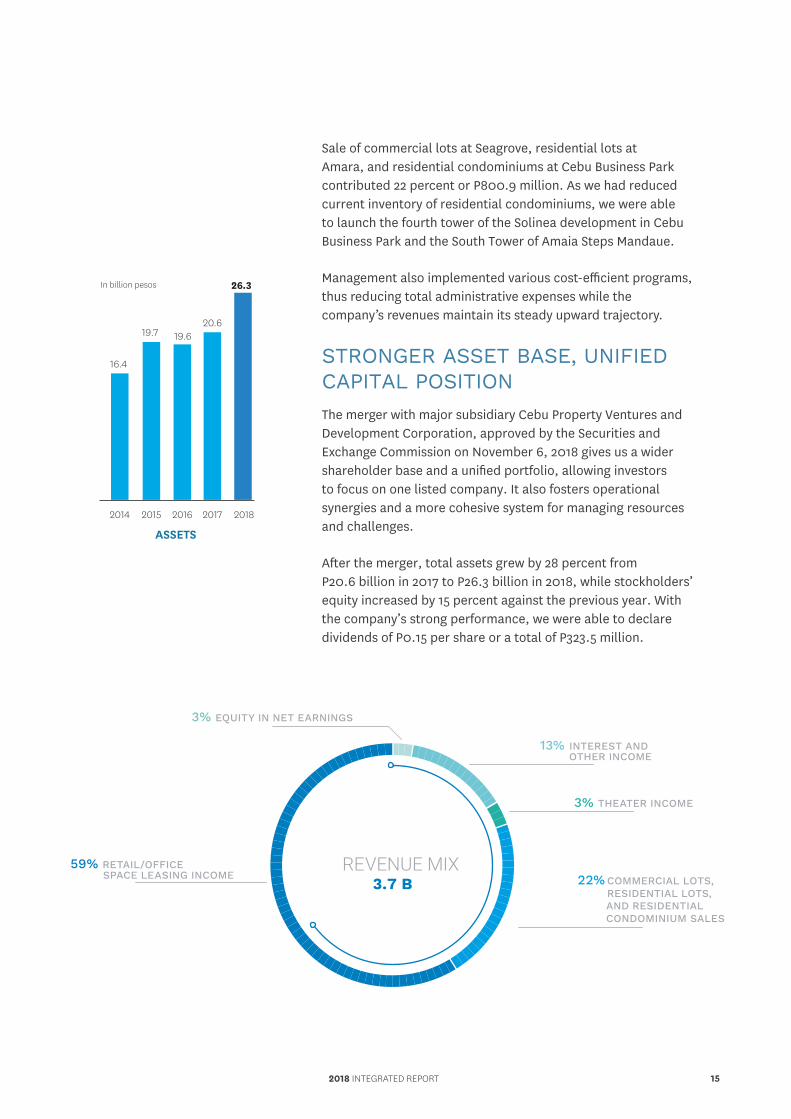

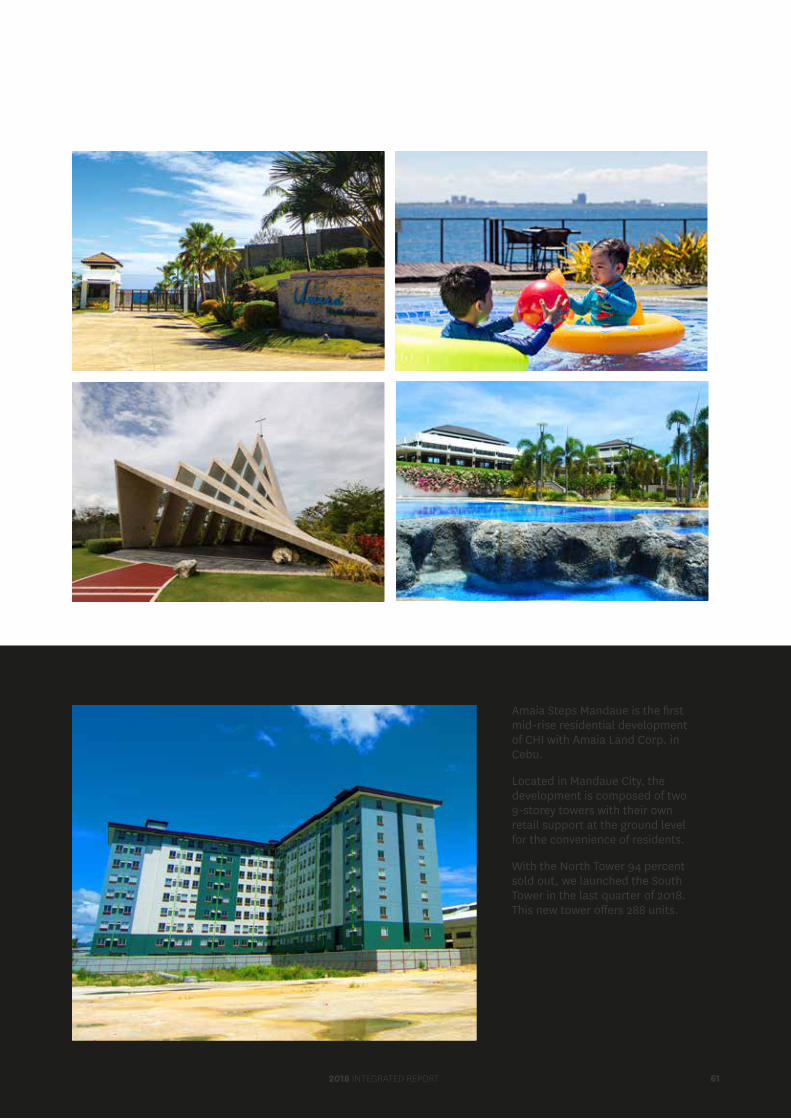

Sale of commercial lots at Seagrove, residential lots at Amara, and residential condominiums at Cebu Business Park contributed 22 percent or P800.9 million. As we had reduced current inventory of residential condominiums, we were able to launch the fourth tower of the Solinea development in Cebu Business Park and the South Tower of Amaia Steps Mandaue.

Management also implemented various cost-efficient programs, thus reducing total administrative expenses while the company’s revenues maintain its steady upward trajectory.

STRONGER ASSET BASE, UNIFIED CAPITAL POSITIONThe merger with major subsidiary Cebu Property Ventures and Development Corporation, approved by the Securities and Exchange Commission on November 6, 2018 gives us a wider shareholder base and a unified portfolio, allowing investors to focus on one listed company. It also fosters operational synergies and a more cohesive system for managing resources and challenges.

After the merger, total assets grew by 28 percent from P20.6 billion in 2017 to P26.3 billion in 2018, while stockholders’ equity increased by 15 percent against the previous year. With the company’s strong performance, we were able to declare dividends of P0.15 per share or a total of P323.5 million.

ASSETS

20182017201620152014

26.3

16.4

19.7 19.620.6

In billion pesos

3% EQUITY IN NET EARNINGS

13% INTEREST AND OTHER INCOME

3% THEATER INCOME

22% COMMERCIAL LOTS, RESIDENTIAL LOTS,

AND RESIDENTIAL CONDOMINIUM SALES

59% RETAIL/OFFICE SPACE LEASING INCOME

REVENUE MIX3.7 B

2018 INTEGRATED REPORT 15

STOCKHOLDERS’ EQUITY

20182017201620152014

8.0

5.5

6.16.5

7.0In billion pesos

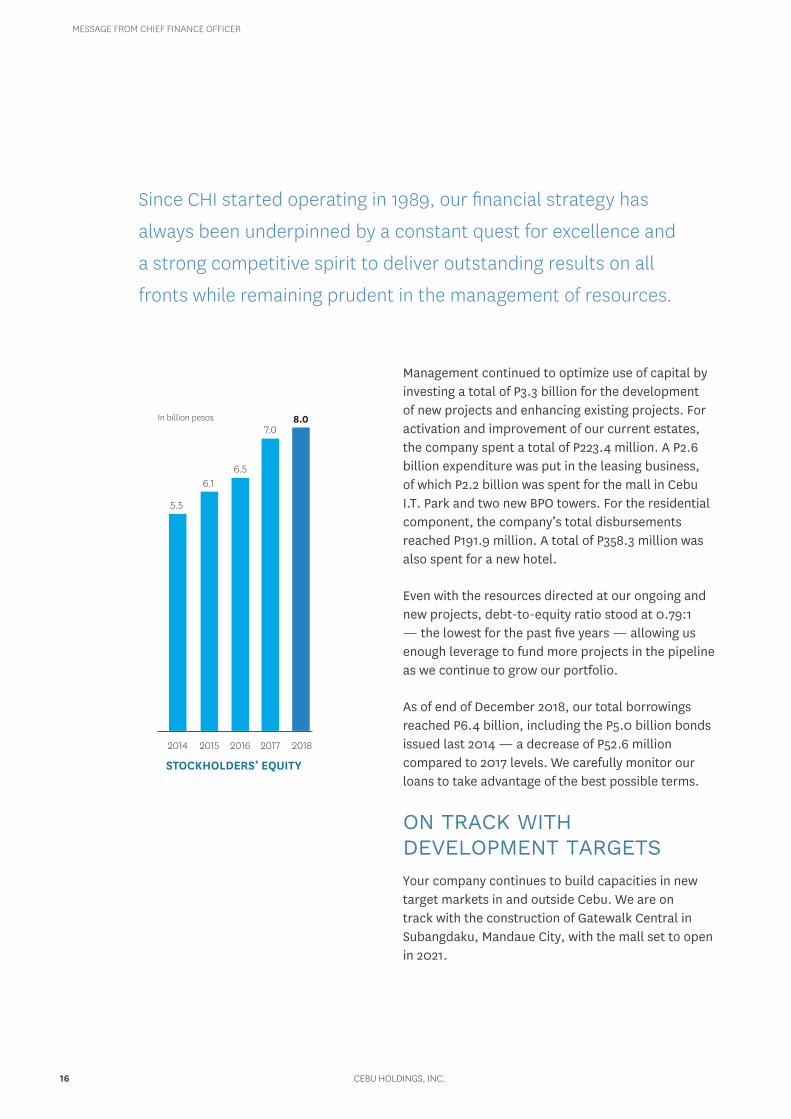

Management continued to optimize use of capital by investing a total of P3.3 billion for the development of new projects and enhancing existing projects. For activation and improvement of our current estates, the company spent a total of P223.4 million. A P2.6 billion expenditure was put in the leasing business, of which P2.2 billion was spent for the mall in Cebu I.T. Park and two new BPO towers. For the residential component, the company’s total disbursements reached P191.9 million. A total of P358.3 million was also spent for a new hotel.

Even with the resources directed at our ongoing and new projects, debt-to-equity ratio stood at 0.79:1 — the lowest for the past five years — allowing us enough leverage to fund more projects in the pipeline as we continue to grow our portfolio.

As of end of December 2018, our total borrowings reached P6.4 billion, including the P5.0 billion bonds issued last 2014 — a decrease of P52.6 million compared to 2017 levels. We carefully monitor our loans to take advantage of the best possible terms.

ON TRACK WITH DEVELOPMENT TARGETSYour company continues to build capacities in new target markets in and outside Cebu. We are on track with the construction of Gatewalk Central in Subangdaku, Mandaue City, with the mall set to open in 2021.

Since CHI started operating in 1989, our financial strategy has

always been underpinned by a constant quest for excellence and

a strong competitive spirit to deliver outstanding results on all

fronts while remaining prudent in the management of resources.

CEBU HOLDINGS, INC.16

MESSAGE FROM CHIEF FINANCE OFFICER

Land development is likewise ongoing in Seagrove in Lapu-Lapu City with its boardwalk retail set to open in 2020 and the Holiday Inn Resorts in 2023.

FROM GOOD TO GREATSince CHI started operating in 1989, our financial strategy has always been underpinned by a constant quest for excellence and a strong competitive spirit to deliver outstanding results on all fronts while remaining prudent in the management of resources.

This foundational concept and nugget of managerial wisdom have enabled your company to constantly surpass targets, grow year on year, and become not only a successful corporation but also one of the greatest brands to be sown and nurtured on Cebu soil.

We have created a strong competitive position by differentiating our company through sophisticated style and branding, utmost reliability, and the highest quality possible to offer Cebu the world-class developments it truly deserves.

As we expand to socially inclusive markets and create more developments that can uplift the lives of more people, rest assured that your company will continue to use the same high standards of fiscal management and operational excellence to see our shareholders through 30 more years of solid returns.

MA. LUISA D. CHIONG CHIEF FINANCE OFFICER / COMPLIANCE OFFICER

STOCK PRICE

20182017201620152014

6.37

4.90

5.75

5.185.16

Peso per share

2018 INTEGRATED REPORT 17

WHAT WE AIM FOR 102-16

We shall be the premier real estate company in the region, creating and enhancing integrated, masterplanned, and sustainable mixed-use developments through a customer-focused and empowered team of professionals.

We ensure the trust and confidence of our stakeholders with sustainable growth while improving the quality of life of the communities we serve with passion and integrity.

Cebu Holdings, Inc. (CHI) is a listed company with the Philippine Stock Exchange (PSE) since 1994. CHI is compliant with all the rules and regulations of the PSE and the Securities and Exchange Commission (SEC), and applicable rules and regulations relating to the development of the Philippine capital market.

CHI is a leading full-line property developer with headquarters at Ayala Center Cebu Tower, Cebu Business Park, Cebu City.

Since its establishment in 1989, the company has played a key role in creating major growth areas in the province through socially inclusive and environmentally responsible business strategies.

CHI is engaged in real estate development, including sale of residential and office units, sports club shares, and lease of commercial spaces.

For 30 years, our business has allowed us to transform 155.9 hectares of land into integrated, masterplanned and mixed-use eco-zones and business parks; launch 5,318 residential lots and condo units; and lease 129,100 square meters of retail and 128,119 square meters of office spaces.

A more comprehensive discussion of our corporate governance practices, including our ownership structure, are found on pages 71 to 121 of this report.

WHO WE ARE 102-1, 102-2, 102-3, 102-6, 102-7

» Focus on Customer

» Bias for Results

» Entrepreneurial Drive

» Teamwork

» Concern for People

» Empowerment of People

» Pursuit of Excellence

» Love of God

» Responsibility to the Community

» Enhancement of Quality of Life

WHAT INSPIRES US 102-16

CEBU HOLDINGS, INC.18

CORPORATE STRUCTURE

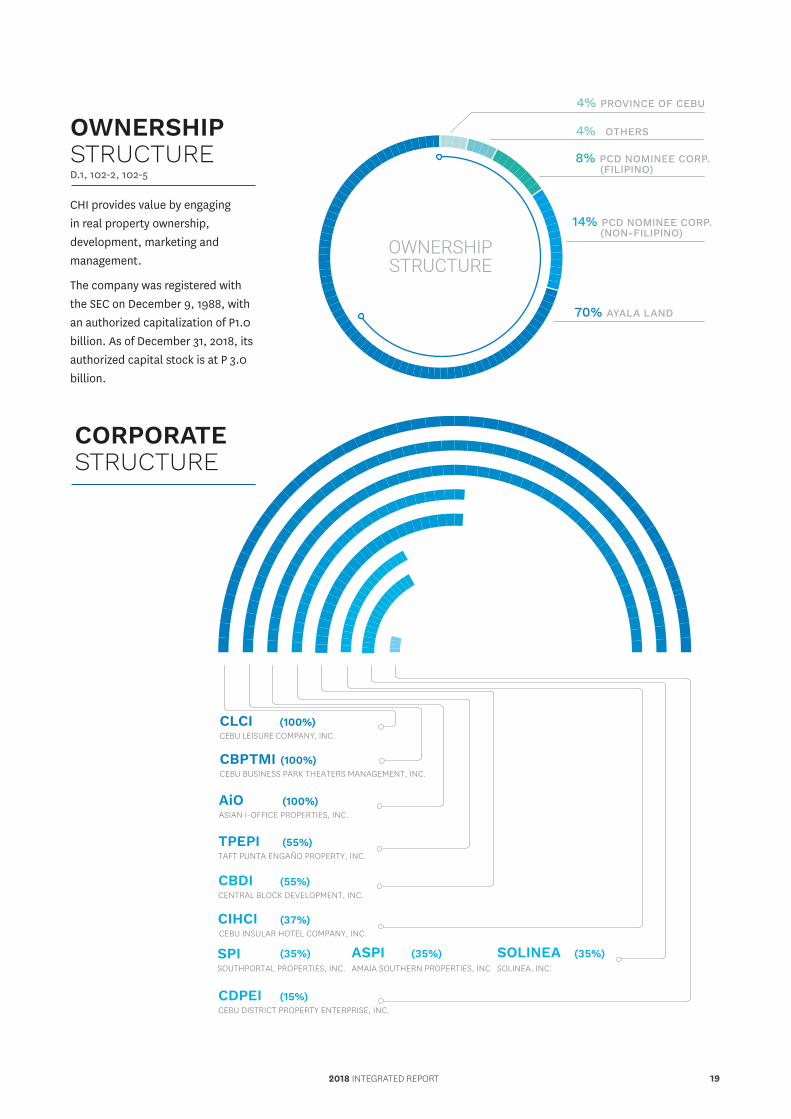

4% PROVINCE OF CEBU

4%

OTHERS

8%

PCD NOMINEE CORP. (FILIPINO)

14%

PCD NOMINEE CORP. (NON-FILIPINO)

70%

AYALA LAND

OWNERSHIPSTRUCTURE

OWNERSHIP STRUCTURED.1, 102-2, 102-5 CHI provides value by engaging in real property ownership, development, marketing and management.

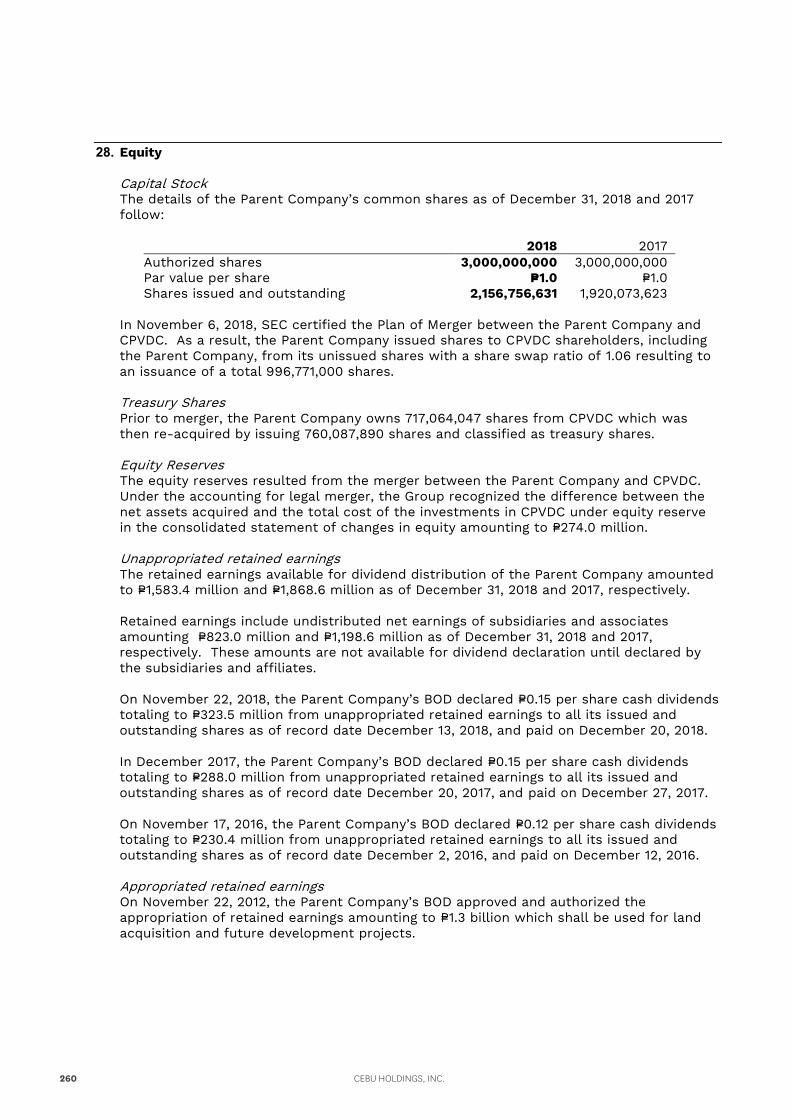

The company was registered with the SEC on December 9, 1988, with an authorized capitalization of P1.0 billion. As of December 31, 2018, its authorized capital stock is at P 3.0 billion.

CLCI (100%)CEBU LEISURE COMPANY, INC.

CBPTMI (100%)CEBU BUSINESS PARK THEATERS MANAGEMENT, INC.

MANAGEMENT COMPANY, INC.

AiO (100%)ASIAN i-OFFICE PROPERTIES, INC.

TPEPI (55%)TAFT PUNTA ENGAÑO PROPERTY, INC.

CIHCI (37%)CEBU INSULAR HOTEL COMPANY, INC.

ASPI (35%)AMAIA SOUTHERN PROPERTIES, INC

SOLINEA (35%)SOLINEA, INC.

SPI (35%)SOUTHPORTAL PROPERTIES, INC.

CBDI (55%)CENTRAL BLOCK DEVELOPMENT, INC.

CDPEI (15%)CEBU DISTRICT PROPERTY ENTERPRISE, INC.

2018 INTEGRATED REPORT 19

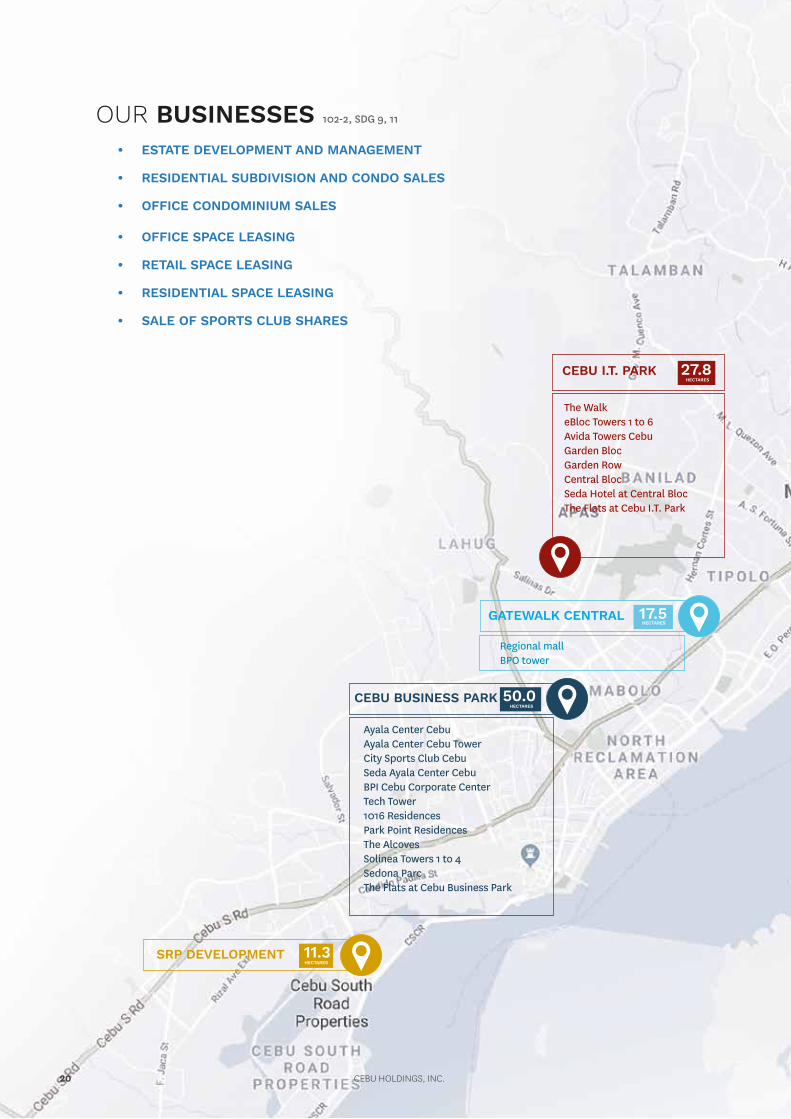

• ESTATE DEVELOPMENT AND MANAGEMENT

• RESIDENTIAL SUBDIVISION AND CONDO SALES

• OFFICE CONDOMINIUM SALES

• OFFICE SPACE LEASING

• RETAIL SPACE LEASING

• RESIDENTIAL SPACE LEASING

• SALE OF SPORTS CLUB SHARES

OUR BUSINESSES 102-2, SDG 9, 11

CEBU BUSINESS PARK

CEBU I.T. PARK

Ayala Center CebuAyala Center Cebu TowerCity Sports Club CebuSeda Ayala Center CebuBPI Cebu Corporate CenterTech Tower1016 ResidencesPark Point ResidencesThe AlcovesSolinea Towers 1 to 4Sedona ParcThe Flats at Cebu Business Park

The WalkeBloc Towers 1 to 6Avida Towers Cebu Garden BlocGarden RowCentral BlocSeda Hotel at Central BlocThe Flats at Cebu I.T. Park

50.0

27.8

HECTARES

HECTARES

SRP DEVELOPMENT 11.3HECTARES

GATEWALK CENTRAL 17.5HECTARES

Regional mallBPO tower

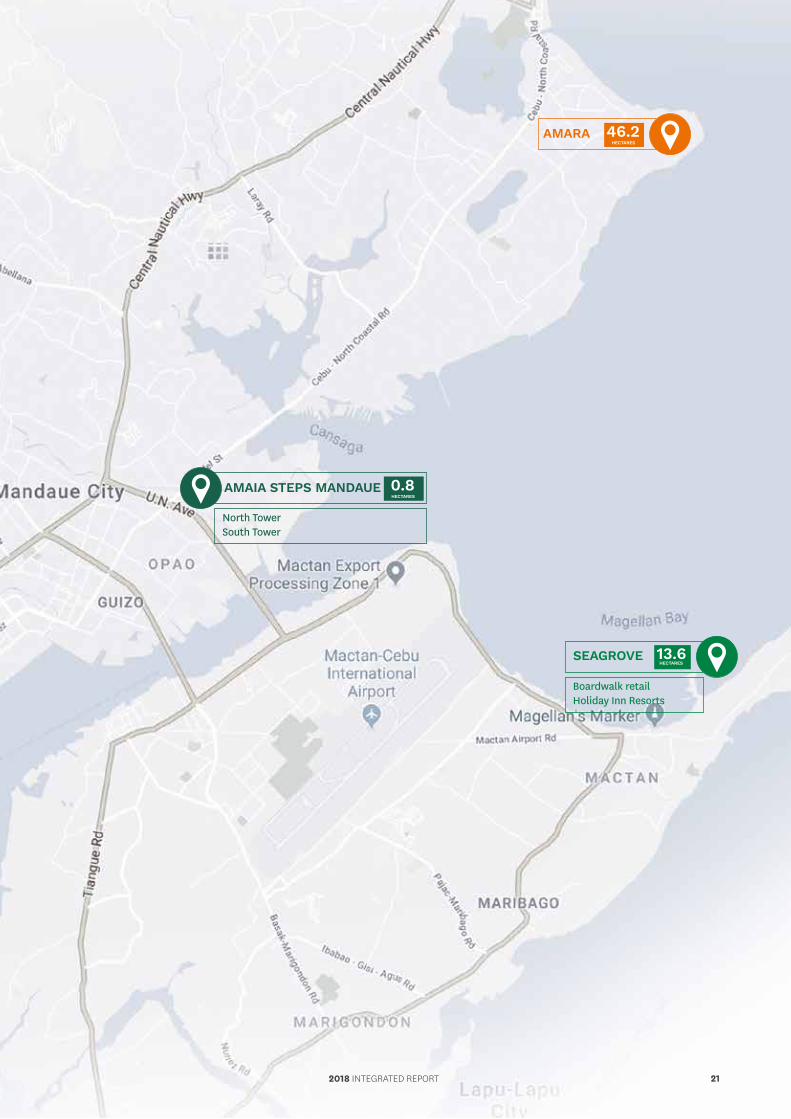

CEBU HOLDINGS, INC.20

SEAGROVE

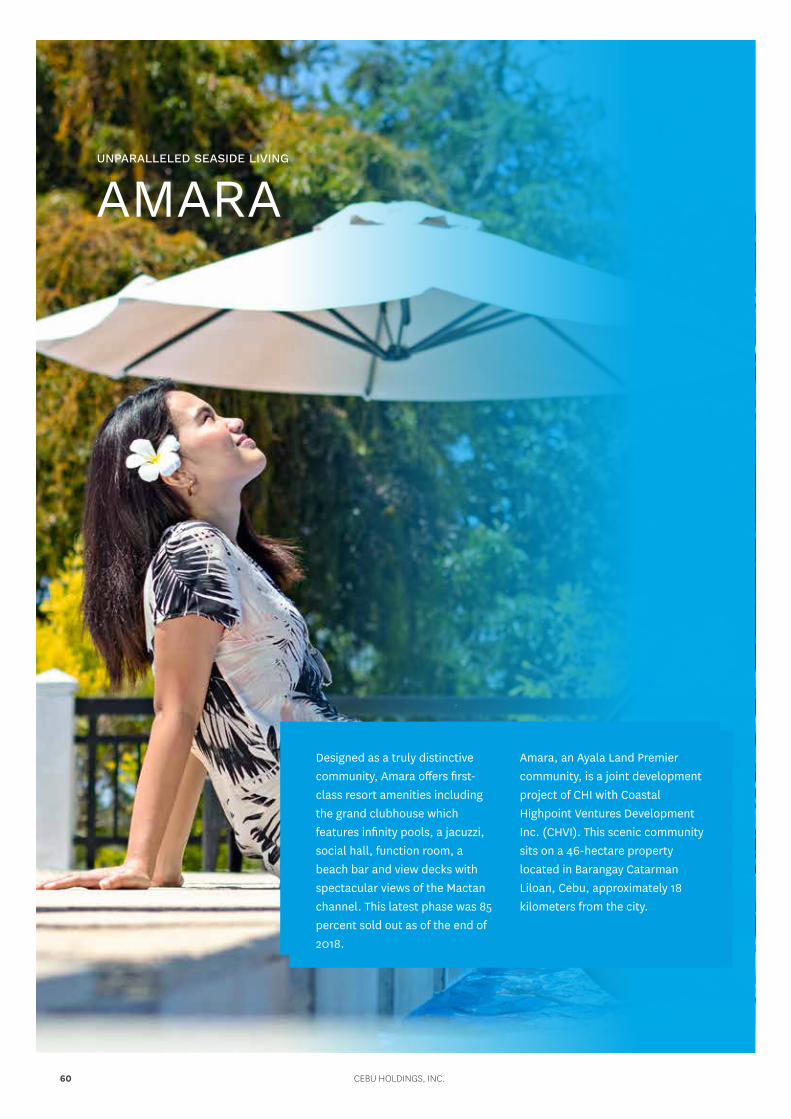

AMARA

AMAIA STEPS MANDAUE

13.6

46.2

0.8

HECTARES

HECTARES

HECTARES

Boardwalk retailHoliday Inn Resorts

North TowerSouth Tower

2018 INTEGRATED REPORT 21

1990 19921991 19941993 1995 1996 19981997 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20102009 2011 2012 2013 20162014 2015 2017 2018

342

80,512

447

80,512 71980,512

1,212

80,512786

80,512

450

80,512

527

80,512 70280,512672

91,519

512

91,519

538

91,519

642

91,519691

91,519

1,037

91,519

1,282

95,237

1,288127,901

1,633

144,752

2,170

193,528

2,294

209,752

3,740

209,752

241,173

3,092

241,173

3,722

257,219

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1000

500

0

250,000

225,000

200,000

150,000

125,000

100,000

75,000

50,000

25,000

0

10,0009,0008,0007,0006,0005,0004,0003,0002,0001,000

0

1,500

107,084

REVENUE

FDI

GLA

GRDPRATE (%)

109876543210

Ayala Center Cebu opens.

CHI lists in the Manila and Makati Stock Exchanges.

CHI acquires 76.26 percent of Cebu Property Venturesand Development Corp. (CPVDC).CHI begins development of the

Cebu Business Park.

CHI breaks ground on Ayala Life-FGU and Park Tower One.

CPVDC breaks ground on the Cebu Civic and TradeCenter, on the old Lahug airport site.

CHI and Ayala Land, Inc. launch City Sports Club Cebu

The reenergized cinema and Food Choices in Ayala CenterCebu open.

The company breaks ground on 1016 Residences, Sedona Parc, and the second Ayala Center Cebu expansion.

The company launches Gatewalk Central in Mandaue City,in collaboration with AboitizLand and Ayala Land.

CHI breaks ground on eBloc Tower 3, and Solinea Towers1 and 2.

Tech Tower and BPI Cebu Corporate Center, both in CebuBusiness Park, are completed.

CHI launches Seagrove in Lapu-Lapu City, in partnershipwith Taft Properties.

The company breaks ground on The Flats in Cebu BusinessPark and Cebu I.T. Park, as well as launches Amaia Steps MandaueSouth Tower.

Seda Ayala Center Cebu opens.

CHI merges with subsidiary, CPVDC.

-0.50.2

1.4

4

5.4

492

8.2

8.2

2.1

3.5

8.5

4.3 4.5 4.6

7.2

6

5

8.6

12.5

6.8

9.49.4

8.8 8.8

4.8

5.1

936 563 530 544 288 1,238

1,591 1,478 1,5172,287

1,247 1,487760

1,769 3.3

0.8

180

80,512

1988 1989

Cebu City Marriott Hotel opens.

Construction of Park Tower Two in the Cebu Business Park begins.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

155,7521,500

155,752 1,433

1,222688

1,854 2,921 2,916

1,544

1,9631,298 1,852

3,2153,737

5,739 5,639

8,279

10,057

Ayala Center Cebu opens its new wing.

Groundbreaking ceremonies take place for Ayala CenterCebu Tower and BPI Cebu Corporate Center.

CHI is recognized among the top 50 listed companiesbased on the Asean Corporate Governance Scorecard.

Cebu Business Park is declared as an I.T. Park and special economic zone.

CHI launches eBloc Tower 2, the first two Avida Towers, 1016 Residences, and Sedona Parc.

Cebu I.T. Park (formerly Asiatown I.T. Park) is declaredas a special economic zone.

Cebu Civic and Trade Center is repositioned as Asiatown I.T. Park. The Village opens.

The first four eOffice modules in Cebu I.T. Park are completed.

Two projects break ground: the expansion of AyalaCenter Cebu and Amara clubhouse.

CHI opens The Terraces in Ayala Center Cebu andThe Walk in Cebu I.T. Park.

Ayala Center Cebu's expansion building opens.In Cebu I.T. Park, work begins on the first eBloc office building.

Cebu Holdings, Inc. registers with the Securities and ExchangeCommission on Dec. 9, with an authorized capitalization of P1 billion.

19881994

1996

1999

1990

1995

1997

20002002

2004

2007

2011

2008

2010

2012

2013

2015

2017

2018

2005

2001

GROSS LEASABLE AREA

GROSS REGIONAL DOMESTIC PRODUCT FOREIGN DIRECT INVESTMENT

2,714

REVENUE(in millions)

ofyears

CREATING LANDMARKS SETTING STANDARDS BUILDING RELATIONSHIPS

SDG 8, 9, 10, 11, 12, 13, 14, 15, 17

1990 19921991 19941993 1995 1996 19981997 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20102009 2011 2012 2013 20162014 2015 2017 2018

342

80,512

447

80,512 71980,512

1,212

80,512786

80,512

450

80,512

527

80,512 70280,512672

91,519

512

91,519

538

91,519

642

91,519691

91,519

1,037

91,519

1,282

95,237

1,288127,901

1,633

144,752

2,170

193,528

2,294

209,752

3,740

209,752

241,173

3,092

241,173

3,722

257,219

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1000

500

0

250,000

225,000

200,000

150,000

125,000

100,000

75,000

50,000

25,000

0

10,0009,0008,0007,0006,0005,0004,0003,0002,0001,000

0

1,500

107,084

REVENUE

FDI

GLA

GRDPRATE (%)

109876543210

Ayala Center Cebu opens.

CHI lists in the Manila and Makati Stock Exchanges.

CHI acquires 76.26 percent of Cebu Property Venturesand Development Corp. (CPVDC).CHI begins development of the

Cebu Business Park.

CHI breaks ground on Ayala Life-FGU and Park Tower One.

CPVDC breaks ground on the Cebu Civic and TradeCenter, on the old Lahug airport site.

CHI and Ayala Land, Inc. launch City Sports Club Cebu

The reenergized cinema and Food Choices in Ayala CenterCebu open.

The company breaks ground on 1016 Residences, Sedona Parc, and the second Ayala Center Cebu expansion.

The company launches Gatewalk Central in Mandaue City,in collaboration with AboitizLand and Ayala Land.

CHI breaks ground on eBloc Tower 3, and Solinea Towers1 and 2.

Tech Tower and BPI Cebu Corporate Center, both in CebuBusiness Park, are completed.

CHI launches Seagrove in Lapu-Lapu City, in partnershipwith Taft Properties.

The company breaks ground on The Flats in Cebu BusinessPark and Cebu I.T. Park, as well as launches Amaia Steps MandaueSouth Tower.

Seda Ayala Center Cebu opens.

CHI merges with subsidiary, CPVDC.

-0.50.2

1.4

4

5.4

492

8.2

8.2

2.1

3.5

8.5

4.3 4.5 4.6

7.2

6

5

8.6

12.5

6.8

9.49.4

8.8 8.8

4.8

5.1

936 563 530 544 288 1,238

1,591 1,478 1,5172,287

1,247 1,487760

1,769 3.3

0.8

180

80,512

1988 1989

Cebu City Marriott Hotel opens.

Construction of Park Tower Two in the Cebu Business Park begins.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

155,7521,500

155,752 1,433

1,222688

1,854 2,921 2,916

1,544

1,9631,298 1,852

3,2153,737

5,739 5,639

8,279

10,057

Ayala Center Cebu opens its new wing.

Groundbreaking ceremonies take place for Ayala CenterCebu Tower and BPI Cebu Corporate Center.

CHI is recognized among the top 50 listed companiesbased on the Asean Corporate Governance Scorecard.

Cebu Business Park is declared as an I.T. Park and special economic zone.

CHI launches eBloc Tower 2, the first two Avida Towers, 1016 Residences, and Sedona Parc.

Cebu I.T. Park (formerly Asiatown I.T. Park) is declaredas a special economic zone.

Cebu Civic and Trade Center is repositioned as Asiatown I.T. Park. The Village opens.

The first four eOffice modules in Cebu I.T. Park are completed.

Two projects break ground: the expansion of AyalaCenter Cebu and Amara clubhouse.

CHI opens The Terraces in Ayala Center Cebu andThe Walk in Cebu I.T. Park.

Ayala Center Cebu's expansion building opens.In Cebu I.T. Park, work begins on the first eBloc office building.

Cebu Holdings, Inc. registers with the Securities and ExchangeCommission on Dec. 9, with an authorized capitalization of P1 billion.

19881994

1996

1999

1990

1995

1997

20002002

2004

2007

2011

2008

2010

2012

2013

2015

2017

2018

2005

2001

GROSS LEASABLE AREA

GROSS REGIONAL DOMESTIC PRODUCT FOREIGN DIRECT INVESTMENT

2,714

REVENUE(in millions)

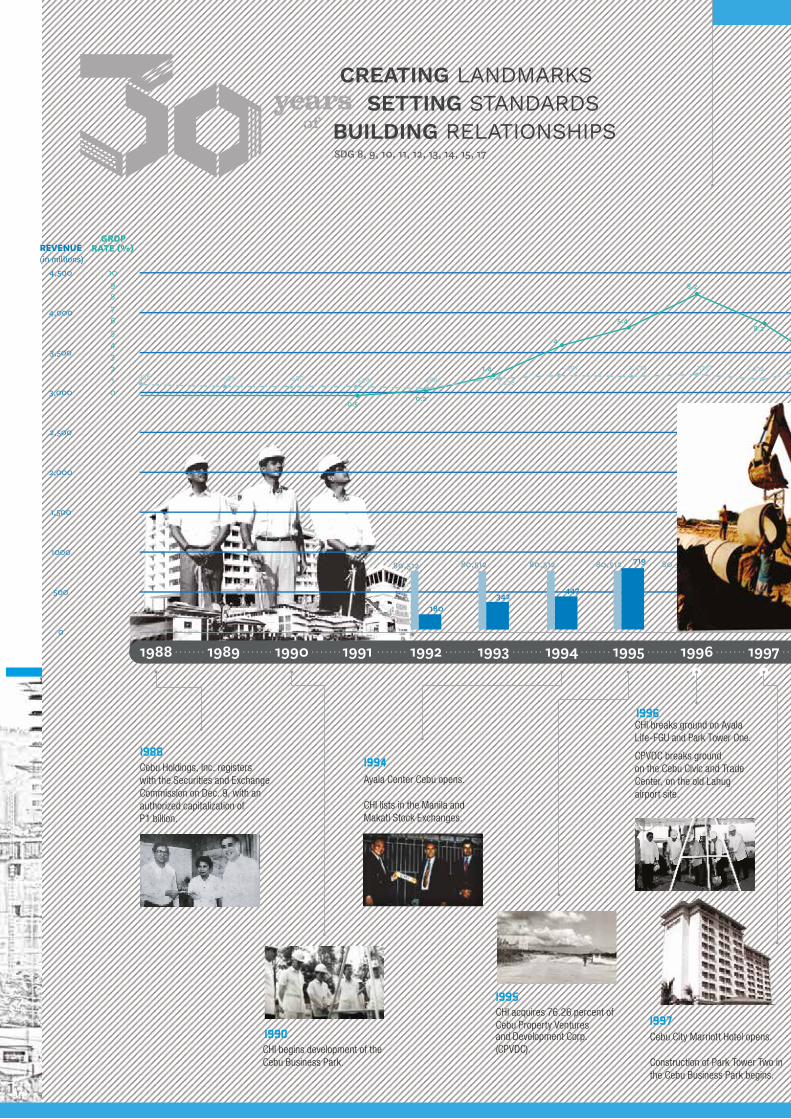

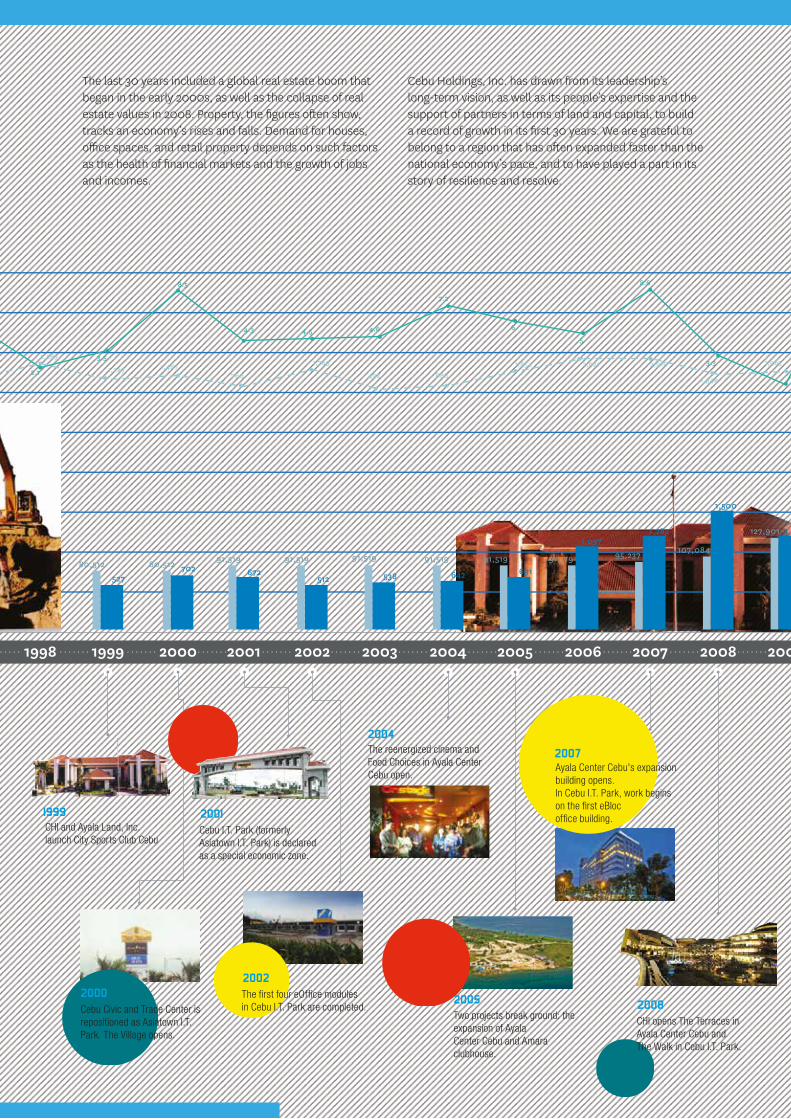

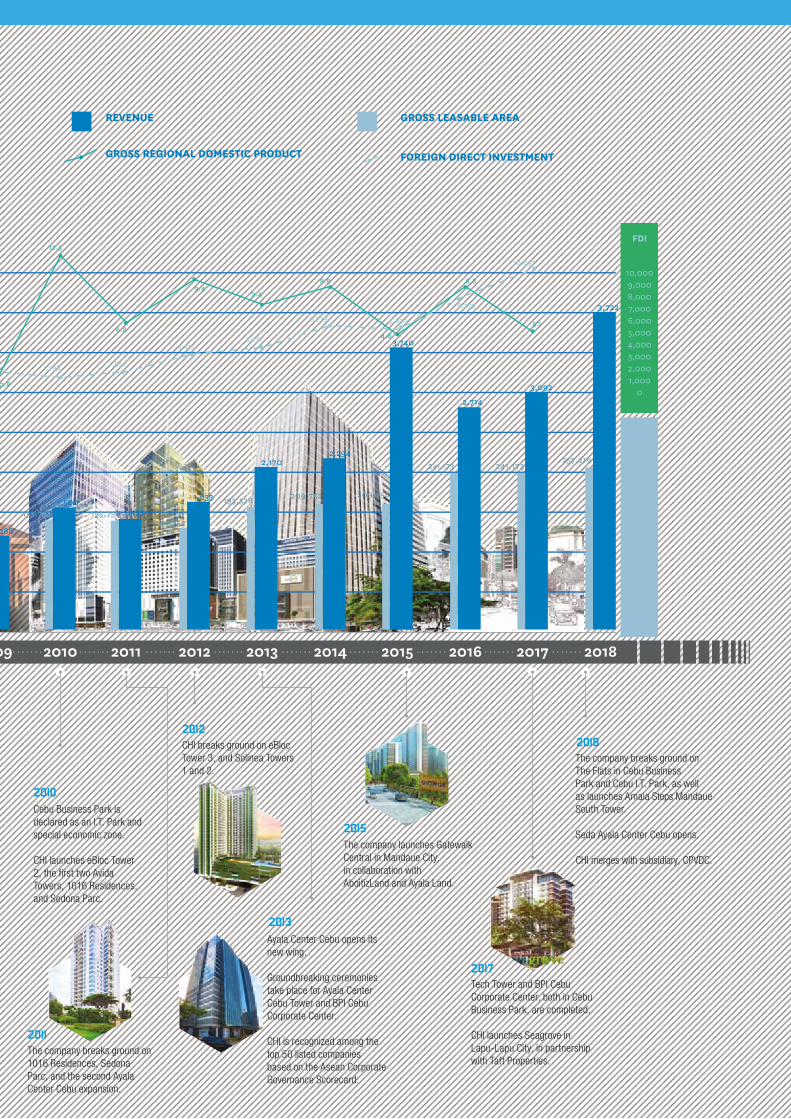

The last 30 years included a global real estate boom that began in the early 2000s, as well as the collapse of real estate values in 2008. Property, the figures often show, tracks an economy’s rises and falls. Demand for houses, office spaces, and retail property depends on such factors as the health of financial markets and the growth of jobs and incomes.

Cebu Holdings, Inc. has drawn from its leadership’s long-term vision, as well as its people’s expertise and the support of partners in terms of land and capital, to build a record of growth in its first 30 years. We are grateful to belong to a region that has often expanded faster than the national economy’s pace, and to have played a part in its story of resilience and resolve.

1990 19921991 19941993 1995 1996 19981997 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20102009 2011 2012 2013 20162014 2015 2017 2018

342

80,512

447

80,512 71980,512

1,212

80,512786

80,512

450

80,512

527

80,512 70280,512672

91,519

512

91,519

538

91,519

642

91,519691

91,519

1,037

91,519

1,282

95,237

1,288127,901

1,633

144,752

2,170

193,528

2,294

209,752

3,740

209,752

241,173

3,092

241,173

3,722

257,219

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1000

500

0

250,000

225,000

200,000

150,000

125,000

100,000

75,000

50,000

25,000

0

10,0009,0008,0007,0006,0005,0004,0003,0002,0001,000

0

1,500

107,084

REVENUE

FDI

GLA

GRDPRATE (%)

109876543210

Ayala Center Cebu opens.

CHI lists in the Manila and Makati Stock Exchanges.

CHI acquires 76.26 percent of Cebu Property Venturesand Development Corp. (CPVDC).CHI begins development of the

Cebu Business Park.

CHI breaks ground on Ayala Life-FGU and Park Tower One.

CPVDC breaks ground on the Cebu Civic and TradeCenter, on the old Lahug airport site.

CHI and Ayala Land, Inc. launch City Sports Club Cebu

The reenergized cinema and Food Choices in Ayala CenterCebu open.

The company breaks ground on 1016 Residences, Sedona Parc, and the second Ayala Center Cebu expansion.

The company launches Gatewalk Central in Mandaue City,in collaboration with AboitizLand and Ayala Land.

CHI breaks ground on eBloc Tower 3, and Solinea Towers1 and 2.

Tech Tower and BPI Cebu Corporate Center, both in CebuBusiness Park, are completed.

CHI launches Seagrove in Lapu-Lapu City, in partnershipwith Taft Properties.

The company breaks ground on The Flats in Cebu BusinessPark and Cebu I.T. Park, as well as launches Amaia Steps MandaueSouth Tower.

Seda Ayala Center Cebu opens.

CHI merges with subsidiary, CPVDC.

-0.50.2

1.4

4

5.4

492

8.2

8.2

2.1

3.5

8.5

4.3 4.5 4.6

7.2

6

5

8.6

12.5

6.8

9.49.4

8.8 8.8

4.8

5.1

936 563 530 544 288 1,238

1,591 1,478 1,5172,287

1,247 1,487760

1,769 3.3

0.8

180

80,512

1988 1989

Cebu City Marriott Hotel opens.

Construction of Park Tower Two in the Cebu Business Park begins.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

155,7521,500

155,752 1,433

1,222688

1,854 2,921 2,916

1,544

1,9631,298 1,852

3,2153,737

5,739 5,639

8,279

10,057

Ayala Center Cebu opens its new wing.

Groundbreaking ceremonies take place for Ayala CenterCebu Tower and BPI Cebu Corporate Center.

CHI is recognized among the top 50 listed companiesbased on the Asean Corporate Governance Scorecard.

Cebu Business Park is declared as an I.T. Park and special economic zone.

CHI launches eBloc Tower 2, the first two Avida Towers, 1016 Residences, and Sedona Parc.

Cebu I.T. Park (formerly Asiatown I.T. Park) is declaredas a special economic zone.

Cebu Civic and Trade Center is repositioned as Asiatown I.T. Park. The Village opens.

The first four eOffice modules in Cebu I.T. Park are completed.

Two projects break ground: the expansion of AyalaCenter Cebu and Amara clubhouse.

CHI opens The Terraces in Ayala Center Cebu andThe Walk in Cebu I.T. Park.

Ayala Center Cebu's expansion building opens.In Cebu I.T. Park, work begins on the first eBloc office building.

Cebu Holdings, Inc. registers with the Securities and ExchangeCommission on Dec. 9, with an authorized capitalization of P1 billion.

19881994

1996

1999

1990

1995

1997

20002002

2004

2007

2011

2008

2010

2012

2013

2015

2017

2018

2005

2001

GROSS LEASABLE AREA

GROSS REGIONAL DOMESTIC PRODUCT FOREIGN DIRECT INVESTMENT

2,714

REVENUE(in millions)

Enduring

in

AnBelief

CebuFor 30 years now, Cebu Holdings, Inc. (CHI) has done its part in changing Cebu, building spaces for shelter and entrepreneurial ambitions, creating a sense of community. We look back at how

CHI has helped transform—and been transformed by—Cebu.

Like all new ventures, it faced the twin possibilities of risk and reward. Yet at its birth in 1988, Cebu Holdings, Inc. (CHI) had the distinct advantage of having a parent corporation with more than a century and a half of experience in the business of property.

What else worked in its favor: local leaders, particularly in Cebu Province, with an ambitious vision for the province and the political capital and business savvy to pursue it. In 1988, the Province under Gov. Emilio Mario Osmeña offered for lease 44.6 hectares that were then being used as a golf course. Ayala Corporation made the winning bid of P550.7 million, on which CHI would build the first master-planned and integrated estate in Cebu.

Within its first decade, CHI built Ayala Center Cebu, Cebu Holdings Center, and the Park Tower condominiums in the Cebu Business Park. It also launched the 24-hectare Cebu Civic and Trade Center in what used to be the Lahug

airport, after acquiring a 76-percent stake in Cebu Property Ventures and Development Corp. (CPVDC), a joint venture between Ayala Land and Cebu Province.

Despite difficulties, those early years after Martial Law were a season of opportunities. Policy reforms were designed to spur Filipinos to look outward, at a global economy that was growing more connected. Exports surged as a result of investments in manufacturing, and Cebu attracted foreign assistance for its infrastructure needs. Property development projects in Metro Cebu rose sharply from 59 projects in 1988 to 1992, according to the Housing and Land Use Regulatory Board, to 158 projects in the next five years.

Central Visayas’ economy grew faster than the national economy from 1994 to 1998. Those who believed, as CHI did, in the potential of Cebu enjoyed the satisfaction of being proven right.

CHI began its second decade like most companies, keeping a watchful eye on a financial contagion that would eventually grip all of Asia.

During the financial crisis of 1997 to 1998, developers had to figure out how to survive high interest rates, a rapidly devaluing peso, and a consumer base that had suddenly grown timid.

Government’s economic managers emphasized the need for investments to help the country break its boom-and-bust cycles, but to bring investors in, such challenges as the high cost of power and aging or inadequate ports, telecommunications lines, and infrastructure had to be fixed.

But it was also during downturns “that we were able to spot the best opportunities and develop these as new sources of growth,” said Ayala Land President and Chief Operating Officer Fernando Zobel de Ayala. Recurring income from Ayala Center Cebu enabled CHI to ride out a lean period and prepare for the tide to turn.

Despite a rough start, CHI’s second decade turned out to be one of expansion. In 2001, the landmark declaration of the Cebu I.T. Park as a special economic zone sparked a new engine of growth for the region. Opening the City Sports Club

Cebu and embarking on the first expansion of Ayala Center Cebu demonstrated CHI’s commitment to keep the Cebu Business Park vital. In 2005, the company launched Amara, its high-end residential development in Liloan.

Meanwhile, CPVDC began developing its eBloc office spaces in the Cebu I.T. Park, as part of initiatives to create an environment where business process management and IT-enabled services could grow. Emerging changes in Cebu’s skyline mirrored its community’s evolving needs. And CHI evolved along with it.

FIRST DECADE

PLAYING THE LONG GAME

About 60 percent of the new office spaces that will be made available from 2018 to 2020 will be in the Cebu Park District, which comprises Cebu Business Park and Cebu I.T. Park.

As CHI marks its third decade, it finds itself in a buoyant environment. In 2017, investors poured some US$164 million in the Philippines’ real estate sector, the highest level in more than a decade. A fortunate combination of rising demand and low interest rates, plus robust remittances from Filipinos working abroad, is at play. That the Philippines has become among Asia’s fastest growing economies in recent years also forms part of the story.

Cebu has much to be upbeat about. The completion of a new international terminal in Mactan in 2018 opens more opportunities in tourism and leisure. The opening of a third bridge between Cebu mainland and Mactan Island in 2021 bodes well for a community that faces the challenges that rapid urbanization brings.

Even as it continues to enhance its flagship estates in Cebu City, CHI has elected to venture to other points of Metro Cebu. It is on

track to open in 2021 its 17.5-hectare Gatewalk estate in Mandaue City, under a joint venture with parent company, Ayala Land and AboitizLand. In Lapu-Lapu City’s resort community of Punta Engaño, it is working with Taft Property Venture Development Corp. on its 13.6-hectare Seagrove estate.

For more than a decade now, CHI has gauged its progress not solely in financial terms, but also in its social and ecological impacts. Its investments in waste management and wastewater treatment technology gained recognition from the United Nations Development Program, which acknowledged its contributions to transformational business.

In 1994, at the opening of Ayala Center Cebu, Don Jaime Zobel de Ayala said, “We believed then, as we believe now, that Cebu will emerge as the next growth center; that the Philippines will not only be known because of Makati, but will also be known because of Cebu.” That belief in Cebu endures. It is what feeds CHI’s every effort to build estates that are safe, inclusive, resilient, and sustainable: to reinvent Cebu’s landscape and enrich its community’s life.

SUSTAINABILITY AS STRATEGY

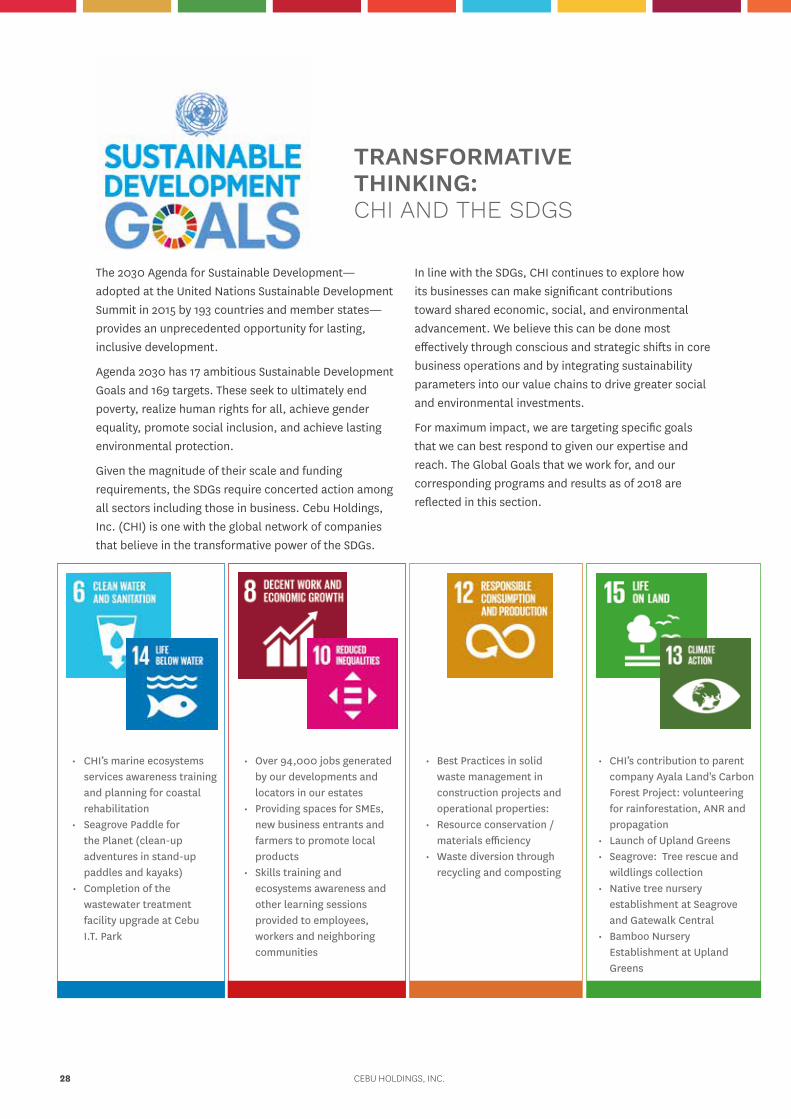

The 2030 Agenda for Sustainable Development—adopted at the United Nations Sustainable Development Summit in 2015 by 193 countries and member states—provides an unprecedented opportunity for lasting, inclusive development.

Agenda 2030 has 17 ambitious Sustainable Development Goals and 169 targets. These seek to ultimately end poverty, realize human rights for all, achieve gender equality, promote social inclusion, and achieve lasting environmental protection.

Given the magnitude of their scale and funding requirements, the SDGs require concerted action among all sectors including those in business. Cebu Holdings, Inc. (CHI) is one with the global network of companies that believe in the transformative power of the SDGs.

In line with the SDGs, CHI continues to explore how its businesses can make significant contributions toward shared economic, social, and environmental advancement. We believe this can be done most effectively through conscious and strategic shifts in core business operations and by integrating sustainability parameters into our value chains to drive greater social and environmental investments.

For maximum impact, we are targeting specific goals that we can best respond to given our expertise and reach. The Global Goals that we work for, and our corresponding programs and results as of 2018 are reflected in this section.

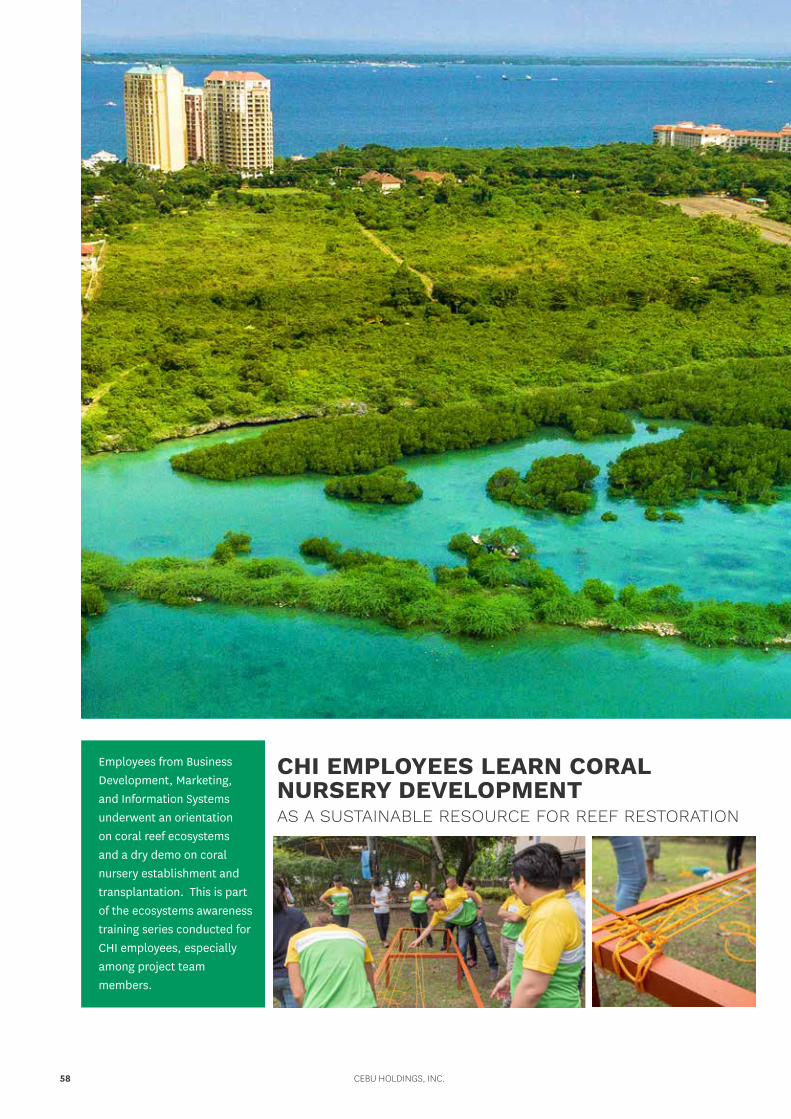

• CHI’s marine ecosystems services awareness training and planning for coastal rehabilitation

• Seagrove Paddle for the Planet (clean-up adventures in stand-up paddles and kayaks)

• Completion of the wastewater treatment facility upgrade at Cebu I.T. Park

• Best Practices in solid waste management in construction projects and operational properties:

• Resource conservation / materials efficiency

• Waste diversion through recycling and composting

• Over 94,000 jobs generated by our developments and locators in our estates

• Providing spaces for SMEs, new business entrants and farmers to promote local products

• Skills training and ecosystems awareness and other learning sessions provided to employees, workers and neighboring communities

• CHI’s contribution to parent company Ayala Land's Carbon Forest Project: volunteering for rainforestation, ANR and propagation

• Launch of Upland Greens • Seagrove: Tree rescue and

wildlings collection• Native tree nursery

establishment at Seagrove and Gatewalk Central

• Bamboo Nursery Establishment at Upland Greens

TRANSFORMATIVE THINKING: CHI AND THE SDGS

CEBU HOLDINGS, INC.28

Engagement with civil society organizations, national government agencies, LGUs and neighboring communities through:

• Promotion of farm-to-market products through spaces provided to farmers

• Support to SMEs and promotion of local products:

• Health awareness• Educational support • Ecosystems services awareness • Completion of police community precincts

within the two estates

• Community partnership for Livelihood through Ayala Center Cebu’s Solid Waste Management Program: Waste collection and segregation done by community partner, Barangay Luz

• P 32.9 million in community Investments in the areas of education, environment, livelihood, health and wellness, arts and culture, promotion of local products

• Support to schools and health organizations via provision of mall spaces for promotional activities, exhibitions and competitions

• Occupational health and safety• CHI PLUS /Health and Wellness programs for all employees

• Women in board and senior leadership• Lactation breaks• Ratio of male and female employees

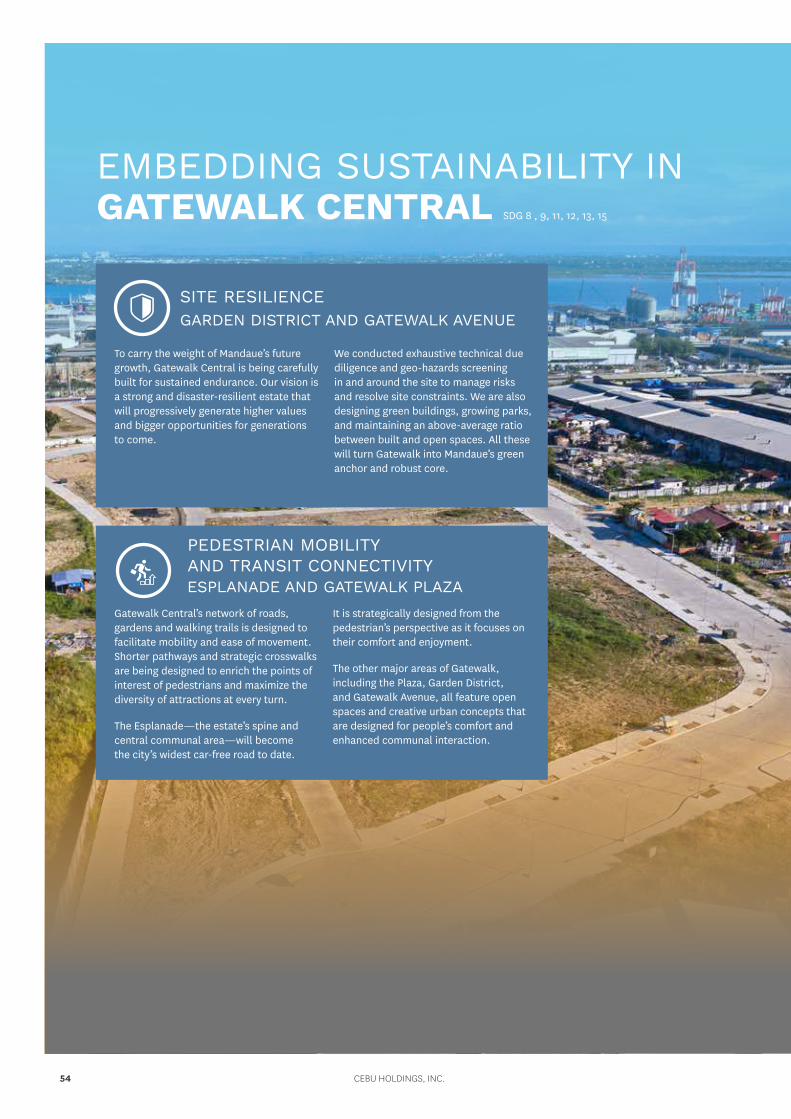

CHI focuses on providing master-planned, integrated, mixed-use developments that are resilient, accessible, pedestrian-friendly, eco-efficient, and inclusive. Through strengthened partnerships with local communities for projects concerning the environment, livelihood, and disaster preparedness, as well as continued stakeholder engagements for market shaping, our company creates a sustainable and inclusive setting for the growth of local economies.

In the past recent years, CHI has made several enhancements in their infrastructures to provide better services for their customers and pedestrians. These improvements were done through the increase on the availability of mass transport systems, construction of additional access roads, and provision of more

pedestrian and PWD-friendly facilities.

2018 INTEGRATED REPORT 29

FOUR FOCUS AREAS 102-31, SDG 8, 9, 11

PEDESTRIAN MOBILITY AND TRANSIT CONNECTIVITY

SITE RESILIENCE

We continue to enhance our estates through improving our estate wide-disaster readiness program, using native plants and trees species for landscaping, and providing space for refuge and rainwater absorption.

We put first the comfort and safety of our pedestrians in our site design and master planning. For estates and buildings under construction, we ensure that transit connectivity is not compromised for the convenience of our pedestrians.

COMPLEX DRILLS, AND 2 PARK-WIDE DRILLS

GREEN AND OPEN SPACE

NUMBER OF TREES

NATIVE PLANT SPECIES

TREE NURSERY

SPACE USED AS EVACUATION AREA

64,980 m2

4,391

72

4,392 m2

52 EMERGENCY BRIGADE DRILL

120,505 m2

OPERATIONAL BUILDINGS

CONSTRUCTION PROJECTS/ OPERATIONAL PROPERTIES

Maintaining dynamic, efficient, and accessible built environment for our locators, merchants, shoppers, clients, workforce, and other stakeholders

Addressing a growing demand for residential, office, and commercial spaces to support Cebu’s economic growth expressed in:

Gross Floor Area (GFA) Gross Leasable Area (GLA) Common Areas Constructed Floor Area

PERFORMANCE METRICS

BIKE RACKS

STREET SIGNAGES

SPACE FOR PUV

STREETLIGHTS

MARKEDCROSSWALKS

27

Enhanced

4,210 m2

Enhanced

58

PEDESTRIANPRIORITY SIGNS

TRAFFIC CALMING DEVICES

PWD RAMPS

COVEREDWALKWAYS

BUS STOPS

35

55

86

6,852

5

CEBU HOLDINGS, INC.30

GREEN AND OPEN SPACESCreating a healthy balance of leasable spaces, common areas and greeneries to deliver higher value to our locators and customers.

EFFICIENT RESOURCE USE AND WASTE MANAGEMENTWe implement resource efficiency programs through regular monitoring of our capitals, tracking of GHG emissions and enforcing better waste management measures.

TOTAL ENERGY CONSUMPTION55% INCREASE VS 2017

TOTAL WATER CONSUMPTION39% INCREASE VS 2017

WASTE COLLECTED IN COMMON AREAS19% DECREASE VS 2017

89,531.3 GJ

361,686.8 m3

4,785.2 tonnes

INVESTED ON LED RETROFITS201-2

P 3.92 M

LOCAL ECONOMIC DEVELOPMENT

Local economy continues to be vibrant brought about by the generation of direct and indirect employment and increase in the number of homegrown businesses in our estates.

WORKFORCE

DISTRIBUTION63,752 BPO/IT/TELCO

1,294 RESIDENTIAL

10,695TRADITIONAL

OFFICE /BANKS

9,047RETAIL

507HOTEL/LEISURE

8,813CONSTRUCTION

94,108

WORKFORCE

Investing in our people by providing development programs in a work environment that is creative, healthy, and safe which makes our people more productive. High-performing employees bring more success to our business.

2018 INTEGRATED REPORT 31

OUR CAPITALS

BUSINESS ACTIVITIES

Acquire Land

Turn to high-value estates

Build and Lease out retail and office spaces & Sell residential units

HOW WE CREATE VA

LUE

THE VALUE WE CREATEFOR OUR STAKEHOLDERS

INTELLECTUALOur knowledge base and our brand

HUMANOur employees, their skills,

and competencies

FINANCIALThe funds that we use to build and provide services

SOCIAL AND RELATIONSHIPOur relationships with societyand our stakeholders

MANUFACTUREDOur man-made assets

NATURALThe environmental resources

that we use and which all other capitals draw from

High value business, commercial, residential, and recreational spaces

Economic growth and beneficial partnerships

Business opportunities and financial growth

INVESTORSEMPLOYEES

SUPPLIERS

COMMUNITIES

CUSTOMERS,TENANTSAND BUILDING OCCUPANTS

Sustained financial growthDecent jobs,

benefits

MARKET OUTLOOK

AND TRENDS

RISK AND OPPORTUNITIES

Strengthen our leasing asset base through partnership and acquisition

Land acquisition and building of new estates

• Partnership• Co-development

Reach diverse markets through• Equity holdings• New products

OUR STRATEGIES

CEBU HOLDINGS, INC.32

OUR CAPITALS

BUSINESS ACTIVITIES

Acquire Land

Turn to high-value estates

Build and Lease out retail and office spaces & Sell residential units

HOW

WE CREATE VALU

ETHE VALUE WE CREATEFOR OUR STAKEHOLDERS

INTELLECTUALOur knowledge base and our brand

HUMANOur employees, their skills,

and competencies

FINANCIALThe funds that we use to build and provide services

SOCIAL AND RELATIONSHIPOur relationships with societyand our stakeholders

MANUFACTUREDOur man-made assets

NATURALThe environmental resources

that we use and which all other capitals draw from

High value business, commercial, residential, and recreational spaces

Economic growth and beneficial partnerships

Business opportunities and financial growth

INVESTORSEMPLOYEES

SUPPLIERS

COMMUNITIES

CUSTOMERS,TENANTSAND BUILDING OCCUPANTS

Sustained financial growthDecent jobs,

benefits

MARKET OUTLOOK

AND TRENDS

RISK AND OPPORTUNITIES

Strengthen our leasing asset base through partnership and acquisition

Land acquisition and building of new estates

• Partnership• Co-development

Reach diverse markets through• Equity holdings• New products

OUR STRATEGIES

332018 INTEGRATED REPORT

OUR CAPITALS

OUR BUSINESS ACTIVITIES

CHI’s operations and business activities follow an expanding cycle of land acquisition, collaboration, development and transformation, and innovation. We acquire land, nurture partnerships, develop and transform land into high-value estates, build and lease out retail and office spaces, sell commercial and residential lots, and begin the cycle anew by expanding our land holdings to enrich more areas. The cycle expands through disruptions and innovations that lead to the discovery of fresh business models and new income streams.

MARKET OUTLOOKOver the past five years, Cebu Business Park and Cebu I.T. Park charted continuously increasing occupancy trends. Even at a 30 percent premium versus other locations, average vacancy rates in CBP and CITP are only at around 1.7 percent. This vacancy rate is also significantly lower than the 11 percent vacancy rate in other developments in Cebu. All these point to the continued high demand for the kind of office and retail spaces that CHI creates and provides.

The GDP per capita of Central Visayas has grown from P69,218 in 2009 to P134,288 in 2017 according to the PSA. In addition, various economic outlook researches predict Cebu’s outsourcing workforce rising by 5 percent to 10 percent yearly over the next three years. The growing middle class, as well as the

growing count of the young professional demographic ages 25-35, also point to heightened economic activity in Metro Cebu over the next years. These all create positive market outlook scenarios not only for CBP and CITP but more so for CHI’s upcoming estates in Mandaue and Lapu-Lapu.

The continued improvement and expansion of the Mactan Cebu International Airport, the growing number of direct international flights to Cebu and the lower travel costs, the complementary improvement of Metro Cebu’s road network, and the booming medical tourism industry all point to a steady increase in tourist arrivals and ease of traffic movement in Metro Cebu and the entire province.

CHI utilized the following capitals during our 2018 operations:

NATURAL

INTELLECTUAL

HUMAN

MANUFACTURED

FINANCIAL

SOCIAL AND RELATIONSHIP

167 HECTARES OF LAND

89,531 GJ TOTAL ENERGY CONSUMED

361,687 m³ TOTAL WATER CONSUMED

14,986 EMPLOYEES & OUTSOURCED PERSONNEL

155.9 HECTARES OF DEVELOPED ESTATES

P12M SPENT ON TECHNICAL CONSULTANTS & OTHER PROFESSIONALS

P60.2B CAPITAL EXPENDITURE FOR CHI AND ALI PROJECTS IN CEBU

17 LGUS & 2 CIVIL SOCIETY ORGS ENGAGED

CEBU HOLDINGS, INC.34

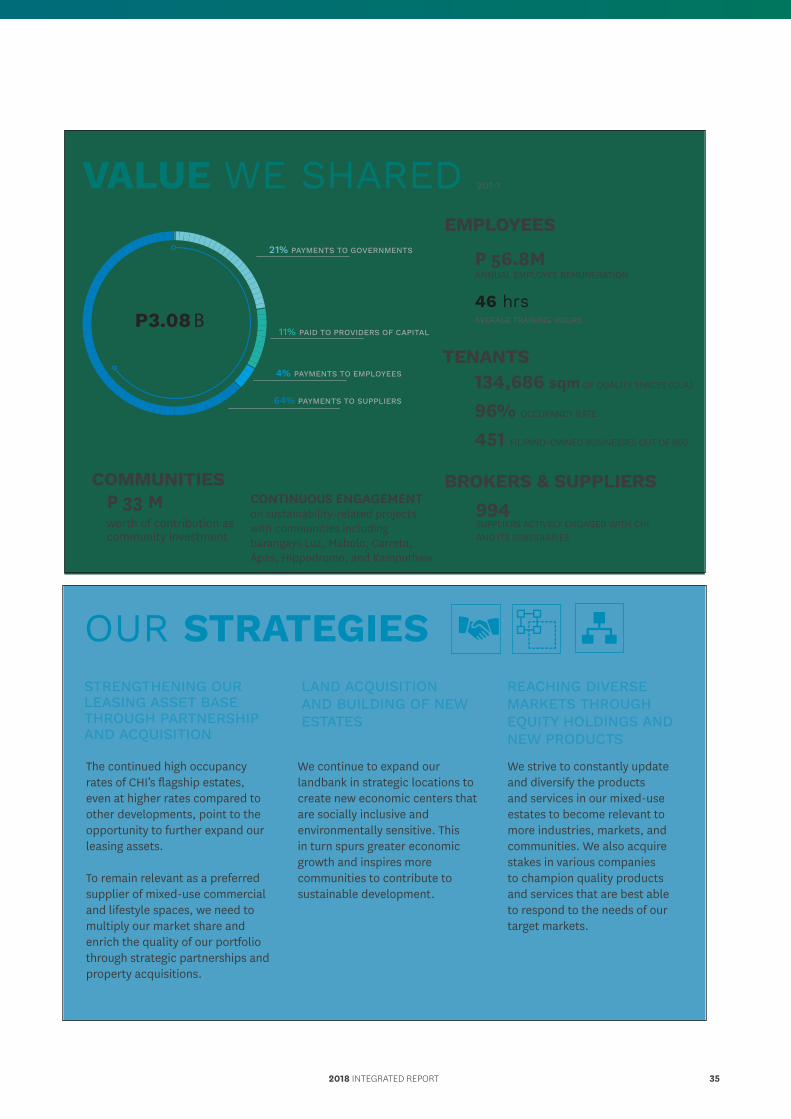

VALUE WE SHARED 201-1

EMPLOYEES

TENANTS

BROKERS & SUPPLIERSCOMMUNITIESP 33 Mworth of contribution as community investment

994SUPPLIERS ACTIVELY ENGAGED WITH CHI AND ITS SUBSIDIARIES

CONTINUOUS ENGAGEMENT on sustainability-related projects with communities including barangays Luz, Mabolo, Carreta, Apas, Hippodromo, and Kamputhaw

134,686 sqm OF QUALITY SPACES (GLA)

96% OCCUPANCY RATE

451 FILIPINO-OWNED BUSINESSES OUT OF 650

OUR STRATEGIES

The continued high occupancy rates of CHI’s flagship estates, even at higher rates compared to other developments, point to the opportunity to further expand our leasing assets.

To remain relevant as a preferred supplier of mixed-use commercial and lifestyle spaces, we need tomultiply our market share and enrich the quality of our portfolio through strategic partnerships and property acquisitions.

We continue to expand our landbank in strategic locations to create new economic centers thatare socially inclusive and environmentally sensitive. This in turn spurs greater economic growth and inspires more communities to contribute to sustainable development.

We strive to constantly update and diversify the products and services in our mixed-use estates to become relevant to more industries, markets, and communities. We also acquire stakes in various companies to champion quality products and services that are best able to respond to the needs of our target markets.

STRENGTHENING OUR LEASING ASSET BASE THROUGH PARTNERSHIP AND ACQUISITION

LAND ACQUISITION AND BUILDING OF NEW ESTATES

REACHING DIVERSE MARKETS THROUGH EQUITY HOLDINGS AND NEW PRODUCTS

46 hrsAVERAGE TRAINING HOURS

ANNUAL EMPLOYEE REMUNERATIONP 56.8M

4% PAYMENTS TO EMPLOYEES

11% PAID TO PROVIDERS OF CAPITAL

21% PAYMENTS TO GOVERNMENTS

64%

PAYMENTS TO SUPPLIERS

P3.08 B

2018 INTEGRATED REPORT 35

Rethinking urban sprawl anddesigning sustainable spacesPeter Calthorpe

Cebu Business Park | Page 40

Ayala Center Cebu | Page 44

Cebu I.T. Park | Page 48

OURPERFORMANCE

CEBU HOLDINGS, INC.36

Gatewalk Central | Page 56

Seagrove | Page 60

Amara and Amaia Steps Mandaue | Page 64

2018 INTEGRATED REPORT 37

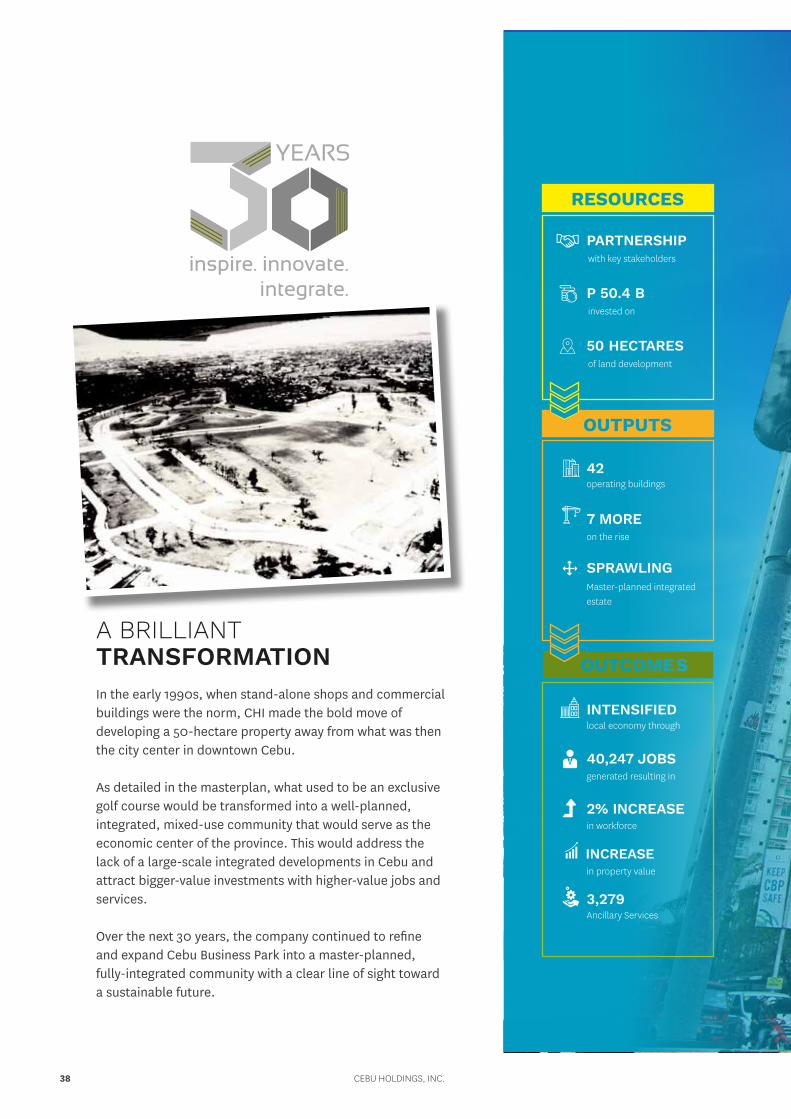

A BRILLIANT TRANSFORMATION In the early 1990s, when stand-alone shops and commercial buildings were the norm, CHI made the bold move of developing a 50-hectare property away from what was then the city center in downtown Cebu. As detailed in the masterplan, what used to be an exclusive golf course would be transformed into a well-planned, integrated, mixed-use community that would serve as the economic center of the province. This would address the lack of a large-scale integrated developments in Cebu and attract bigger-value investments with higher-value jobs and services.

Over the next 30 years, the company continued to refine and expand Cebu Business Park into a master-planned, fully-integrated community with a clear line of sight toward a sustainable future.

40,247 JOBSgenerated resulting in

INCREASEin property value

2% INCREASE in workforce

INTENSIFIEDlocal economy through

3,279Ancillary Services

invested on

P 50.4 B

with key stakeholders

PARTNERSHIP

of land development

50 HECTARES

42

7 MORE

SPRAWLING

operating buildings

on the rise

Master-planned integrated estate

CEBU HOLDINGS, INC.38

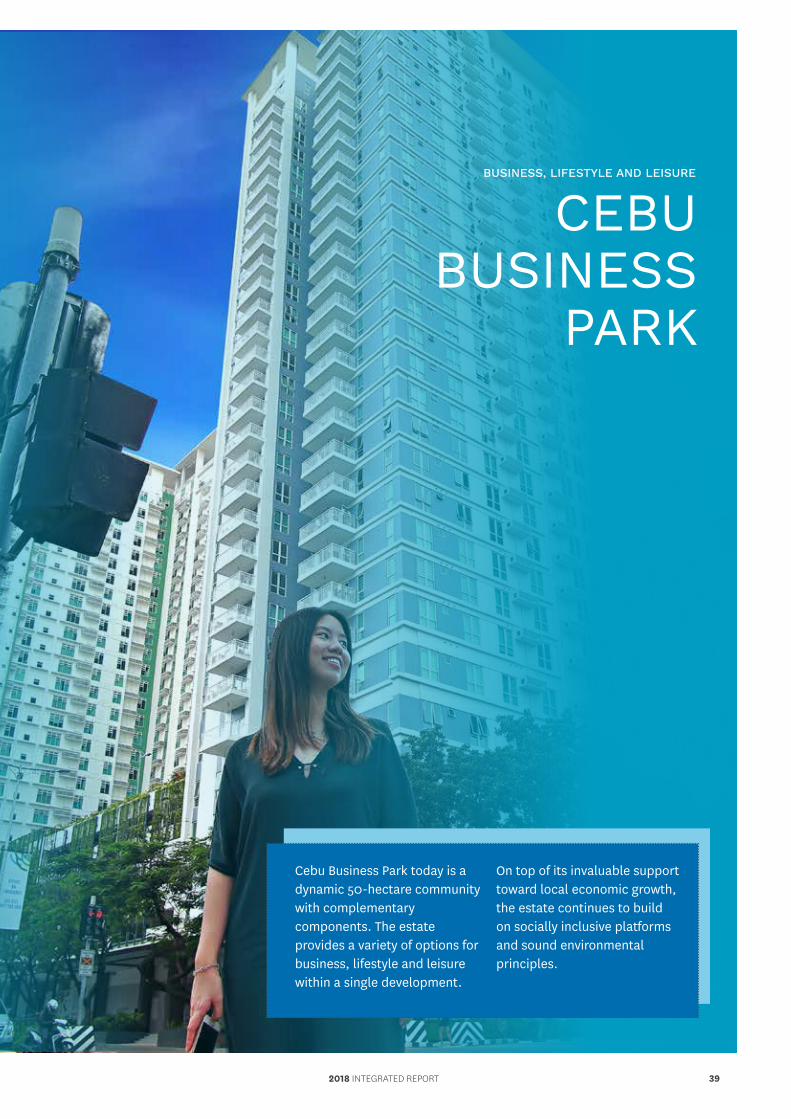

CEBUBUSINESS

PARK

BUSINESS, LIFESTYLE AND LEISURE

Cebu Business Park today is a dynamic 50-hectare community with complementary components. The estate provides a variety of options for business, lifestyle and leisure within a single development.

On top of its invaluable support toward local economic growth, the estate continues to build on socially inclusive platforms and sound environmental principles.

2018 INTEGRATED REPORT 39

45% OFFICE/BPO

18% MALL/RETAIL

4% HOTEL/RECREATIONAL

33% RESIDENTIAL

OPERATIONAL ANDUNDER CONSTRUCTION

CEBU BUSINESS PARK OPERATIONAL PERFORMANCECebu Business Park remains the premier business and lifestyle hub south of Metro Manila. A pioneer in introducing the concept of large, integrated, masterplanned, mixed-use estates, Cebu Business Park is the address of choice of top local and multinational companies for their regional offices.

In 2018, there were 42 existing buildings, with 7 more under construction. Workforce continued to increase to a total of 40,247 employed by the end of the year. In August 2018, Seda Ayala Center Cebu opened. This 301-room hotel provides signature Filipino hospitality to business travellers and tourists at the heart of Cebu Business Park.

CEBU HOLDINGS, INC.40

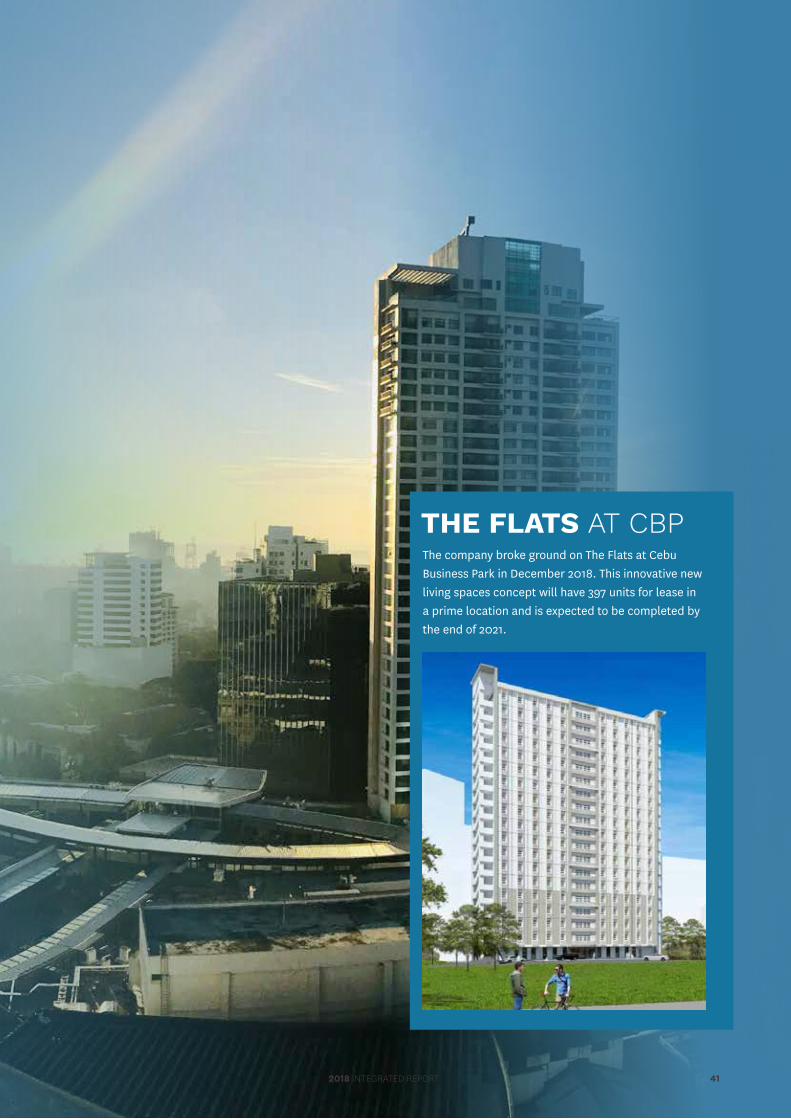

The company broke ground on The Flats at Cebu Business Park in December 2018. This innovative new living spaces concept will have 397 units for lease in a prime location and is expected to be completed by the end of 2021.

THE FLATS AT CBP

2018 INTEGRATED REPORT 41

Ayala Center Cebu remains as the region’s premier lifestyle destination after garnering recognition for its strong lineup of leisure activities in 2018 tailored to meet a variety of special interests and community needs. The mall expanded its roster of shops and restaurants with new additions such as Tavolata and Sole Academy.

It now houses the biggest The Athlete’s Foot store in Southeast Asia after the specialty store’s expansion last year. It also welcomed popular Japanese clothing brand Uniqlo with the opening of its biggest store in the Visayas.

Among the merchants at Ayala Center Cebu, 305 out of 475 are local brands.

134,686 sqmGross Leasable Area

487tourists assisted per month

97,215Daily foot traffic

6,472Daily vehicle count

Water intensity (m3/sqm)2016 2017 2018

4.8557

2.4821

4.3226

Indirect Energy Intesity (GJ/sqm)2016 2017 2018

0.6235

0.51800.5884

Total waste generated (tonnes)

2017

818.38

3,449.02

849.044

2,783.60

2018

RECYCLABLE NON-RECYCLABLE

52% PHILIPPINE BRANDS

31% FOREIGN BRANDS

18% CEBU BRANDS LOCAL HOMEGROWN

XIM TNAHCREM

CEBU HOLDINGS, INC.42

The "Happy Colorful Summer", 2018 mall campaign of Ayala Center

Cebu, was awarded the Anvil Silver Award for Specialized Public Relations Program at the 54th Anvil Awards held on January 30, 2019 at the Marriott Grand Ballroom in Pasay City. Entitled "Happy Colorful Summer", the campaign, was all about color, music and life, channeled through musical performances, fitness workshops and educational sessions such as painting, arts and crafts, voice lessons and ballet classes. The campaign proved to be very effective and it garnered positive reviews from mall-goers.

Dubbed as the “Oscars” of the Philippine PR industry, the annual Anvil Awards recognizes outstanding public relations programs and tools. It is presented by the Public Relations Society of the Philippines.

The campaign was also one of the finalists for Public Relations and Events in The International Council of Shopping Centers (ICSC) Asia-Pacific Shopping Center Awards, a premier recognition of excellence and innovation within the region's shopping center industry. Awards are

given for outstanding achievement in marketing and design/development of retail properties and retail store design.

Throughout the entire campaign, Ayala Center Cebu sought to safeguard the community's ties with the mall and reinforce its commitment to preserving Cebu's well-being and cherished traditions.

COLORFUL SUMMER

appyH

Thirty representatives from various private firms in Yokohama Japan were hosted on a tour of the Ayala Center Cebu facilities on October 29, 2018.

The cities of Yokohama and Cebu had an agreement on City-to-City collaboration, and are working together to contribute to the development of Cebu.

Their site visit focused on knowing more about energy saving and energy management practices, including wastewater treatment in commercial facilities and hotel resorts.

WORKING TOGETHER

2018 INTEGRATED REPORT 43

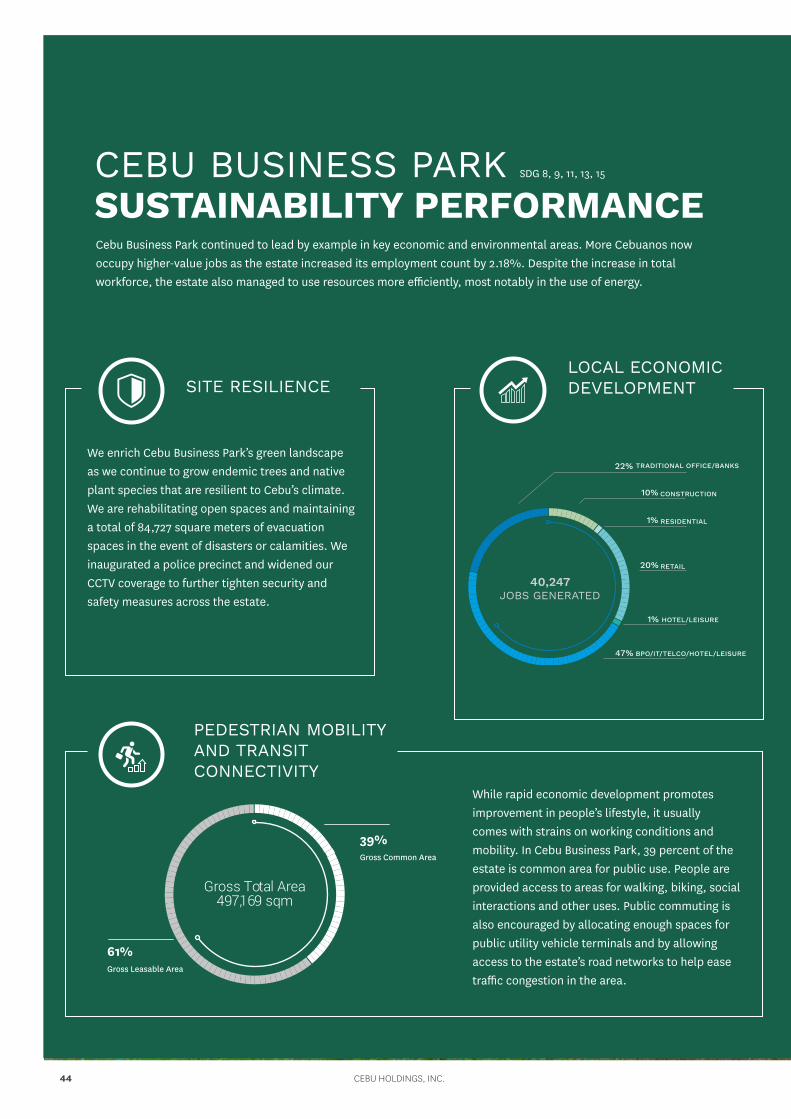

CEBU BUSINESS PARK SDG 8, 9, 11, 13, 15 SUSTAINABILITY PERFORMANCE

SITE RESILIENCE

PEDESTRIAN MOBILITY AND TRANSIT CONNECTIVITY

LOCAL ECONOMIC DEVELOPMENT

Gross Total Area497,169 sqm

Cebu Business Park continued to lead by example in key economic and environmental areas. More Cebuanos now occupy higher-value jobs as the estate increased its employment count by 2.18%. Despite the increase in total workforce, the estate also managed to use resources more efficiently, most notably in the use of energy.

We enrich Cebu Business Park’s green landscape as we continue to grow endemic trees and native plant species that are resilient to Cebu’s climate. We are rehabilitating open spaces and maintaining a total of 84,727 square meters of evacuation spaces in the event of disasters or calamities. We inaugurated a police precinct and widened our CCTV coverage to further tighten security and safety measures across the estate.

While rapid economic development promotes improvement in people’s lifestyle, it usually comes with strains on working conditions and mobility. In Cebu Business Park, 39 percent of the estate is common area for public use. People are provided access to areas for walking, biking, social interactions and other uses. Public commuting is also encouraged by allocating enough spaces for public utility vehicle terminals and by allowing access to the estate’s road networks to help ease traffic congestion in the area.

39% Gross Common Area

61% Gross Leasable Area

47% BPO/IT/TELCO/HOTEL/LEISURE

1% HOTEL/LEISURE

20% RETAIL

1% RESIDENTIAL

10% CONSTRUCTION

22%

TRADITIONAL OFFICE/BANKS

40,247JOBS GENERATED

CEBU HOLDINGS, INC.44

EFFICIENT RESOURCE USEAND WASTE MANAGEMENT

ELECTRICITY CONSUMPTIONINTENSITY, GJ/SQM

2016 2017 2018

0.0053

0.0062

0.0057

WATER CONSUMPTIONINTENSITY, CUM/SQM

2016 2017 2018

0.0102

0.0100

0.0111

NATIVE TREE NURSERY AND COMPOST PRODUCTION FACILITY

CHI continues to improve the bamboo and native tree nursery at Cebu Business Park. To date, the nursery houses 4,122 seedlings and saplings.

In 2018, enhancement of the composting facility at Cebu Business Park was completed to accommodate the estate’s biodegradable waste. Innovation in composting using starter and booster technologies was introduced to hasten the decomposition process while improving waste management process.

GHG EMISSION INTENSITY(SCOPE 2), GJ/SQM

2016 2017 2018

0.0009 0.0010

WASTE GENERATED, TONNES2017 2018

RECYCLABLENON-RECYCLABLE

0.0011

2018 INTEGRATED REPORT 45

HUB OF THE FUTURE The vision was to grow Cebu’s pioneer mixed-use zone for

high-growth industries focused on digital disruptions. First

named as Cebu Civic and Trade Center and then Asiatown I.T.

Park, the 28-hectare development was a direct response to

Cebu’s sustained economic growth in the 1990s coupled with

the demand for prime properties to house the electronics and

technological industry.

Formerly an old airport, Cebu I.T. Park earned a distinction as

the first PEZA-accredited I.T. park outside of Manila and a Special

Economic Zone. By the early 2000s, various engineering, digital,

and telecommunication locators began to relocate to Cebu given

the estate’s robust infrastructure, strategic location, and solid

position as Cebu’s home for innovative minds.

53,308 JOBSgenerated resulting in

INCREASEin property value

3% INCREASE in workforce

INTENSIFIEDlocal economy through

563Ancillary Services

28

9 MORE

DYNAMIC

operating buildings

on the rise

Masterplanned integrated estate

invested on

P 38.0 B

of land

28 HECTARES

in a

CEBU HOLDINGS, INC.46

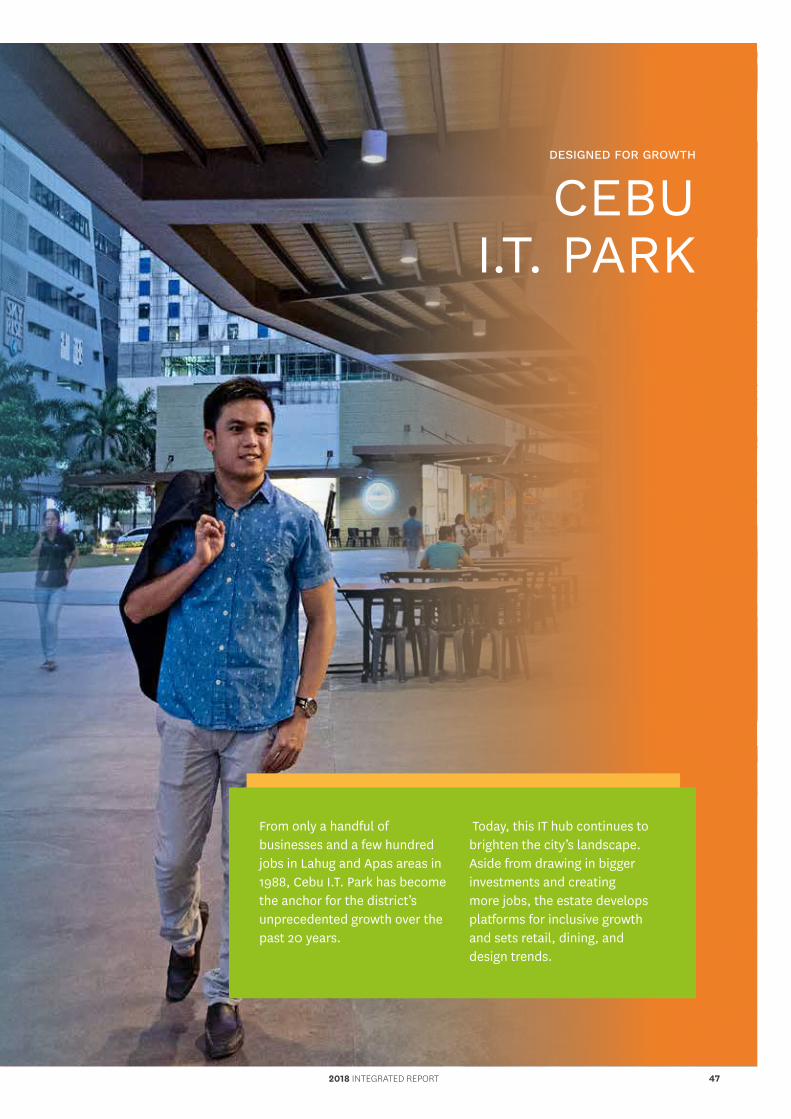

CEBUI.T. PARK

DESIGNED FOR GROWTH

From only a handful of businesses and a few hundred jobs in Lahug and Apas areas in 1988, Cebu I.T. Park has become the anchor for the district’s unprecedented growth over the past 20 years.

Today, this IT hub continues to brighten the city’s landscape. Aside from drawing in bigger investments and creating more jobs, the estate develops platforms for inclusive growth and sets retail, dining, and design trends.

2018 INTEGRATED REPORT 47

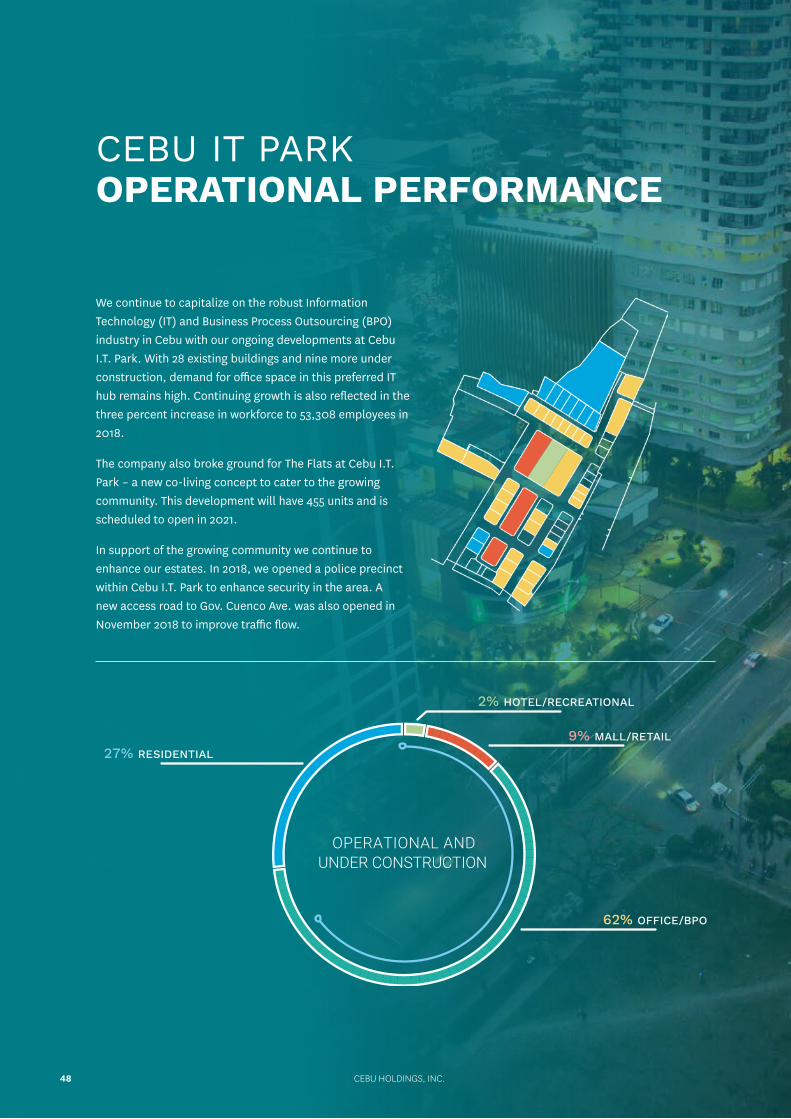

62% OFFICE/BPO

9% MALL/RETAIL

2% HOTEL/RECREATIONAL

27% RESIDENTIAL

OPERATIONAL ANDUNDER CONSTRUCTION

CEBU IT PARK OPERATIONAL PERFORMANCE

We continue to capitalize on the robust Information Technology (IT) and Business Process Outsourcing (BPO) industry in Cebu with our ongoing developments at Cebu I.T. Park. With 28 existing buildings and nine more under construction, demand for office space in this preferred IT hub remains high. Continuing growth is also reflected in the three percent increase in workforce to 53,308 employees in 2018.

The company also broke ground for The Flats at Cebu I.T. Park – a new co-living concept to cater to the growing community. This development will have 455 units and is scheduled to open in 2021.

In support of the growing community we continue to enhance our estates. In 2018, we opened a police precinct within Cebu I.T. Park to enhance security in the area. A new access road to Gov. Cuenco Ave. was also opened in November 2018 to improve traffic flow.

CEBU HOLDINGS, INC.48

CENTRAL BLOC AND GARDEN ROW

GARDEN BLOC

eBLOC TOWERS

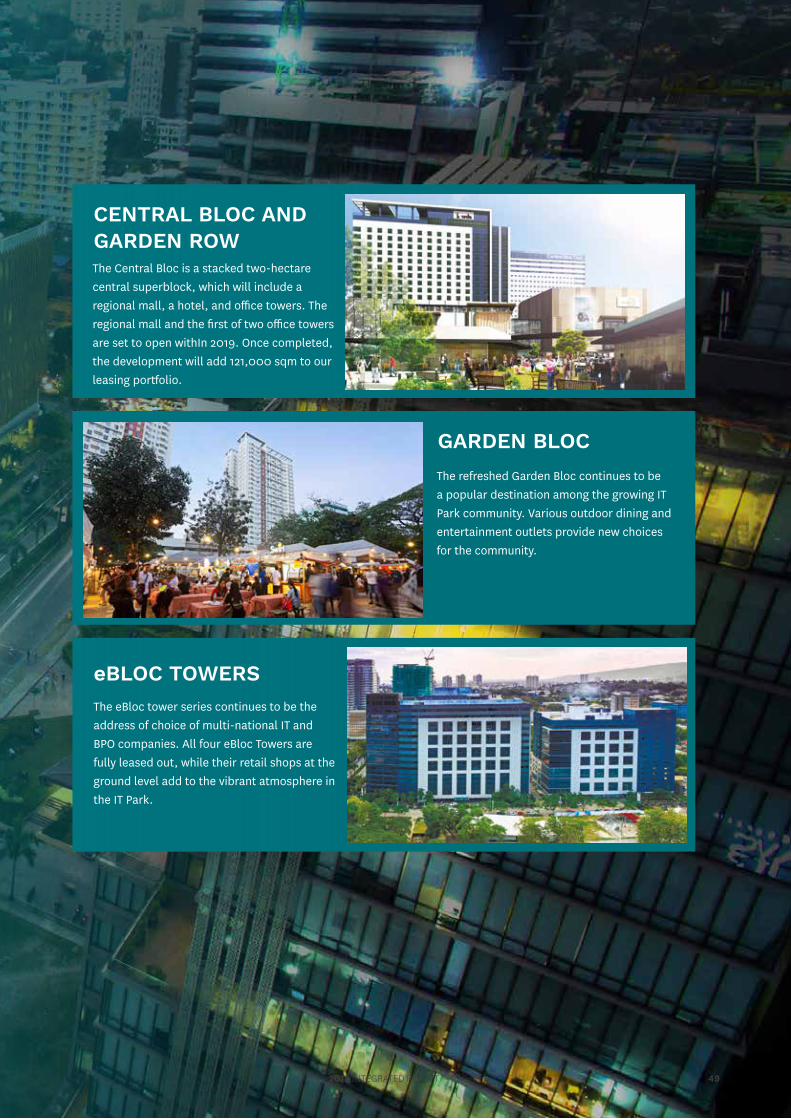

The Central Bloc is a stacked two-hectare central superblock, which will include a regional mall, a hotel, and office towers. The regional mall and the first of two office towers are set to open withIn 2019. Once completed, the development will add 121,000 sqm to our leasing portfolio.

The refreshed Garden Bloc continues to be a popular destination among the growing IT Park community. Various outdoor dining and entertainment outlets provide new choices for the community.

The eBloc tower series continues to be the address of choice of multi-national IT and BPO companies. All four eBloc Towers are fully leased out, while their retail shops at the ground level add to the vibrant atmosphere in the IT Park.

2018 INTEGRATED REPORT 49

CEBU IT PARKSUSTAINABILITY PERFORMANCE SDG 8 , 9, 11, 12

PEDESTRIAN MOBILITYAND TRANSIT CONNECTIVITY

The design of Cebu I.T. Park’s roads and walking pathways continues to evolve to ensure a vibrant and safe environment for pedestrians and the commuting public.

In 2018, the estate pursued further studies on implementing a more efficient traffic management plan, particularly for entry and exit points with high pedestrian counts.

These studies have also led to the creation of an Estate Administration

Office in November 2018 to ease traffic flow, seek proactive measures on road safety, and address pedestrian concerns. In addition, various streetscape enhancements were implemented, including the updating of PWD ramps, concrete and steel humps, and fire hydrants.

To enhance accessibility and mobility, CHI unlocked two more key access points at Cebu I.T, Park, thus opening private roads to the public and easing traffic buildup in surrounding areas.