1 Innovative Solutions. Immaculate Service. This information is for professional investors only and should not be presented to, or relied upon by, private investors. We produce a Quarterly Investment Bank Credit Report as part of our continual counterparty due diligence process. The Report includes summaries of the quarterly movements, for most of the main counterparties in the structured product issuance space, of their: ▪ Share Prices ▪ Credit Default Swap Rates ▪ Credit Ratings Investment Bank Credit Report | Q2 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Innovative Solutions. Immaculate Service.

This information is for professional investors only and should not be presented to, or relied upon by, private investors.

We produce a Quarterly Investment Bank Credit Report as part of our continual counterparty due diligence process.

The Report includes summaries of the quarterly movements, for most of the main counterparties in the structured product issuance space, of their:

▪ Share Prices▪ Credit Default Swap Rates▪ Credit Ratings

Investment Bank Credit Report | Q2 2017

2

Innovative Solutions. Immaculate Service.

Contents

Rating Agency Scales 3

Credit Default Swaps 4

Credit Ratings Overview 5

Summary of Changes 6

Summary of Share Price, CDS and Credit Ratings

Banco Bilbao Vizcaya Argentaria 8 JPMorgan Chase & Co 23

Banco Santander S.A. 9 Lloyds Banking Group plc 24

Bank of America Corporation 10 Macquarie Bank Ltd 25

Barclays Bank plc 11 Morgan Stanley 26

BNP Paribas 12 Natixis 27

Citigroup Inc. 13 Nomura Bank International plc 28

Commerzbank AG 14 NORTHERN TRUST CORP 29

Credit Agricole S.A. 15 Rabobank 30

Credit Suisse AG 16 Royal Bank of Canada 31

Danske Bank A/S 17 Santander UK plc 32

Deutsche Bank AG 18 Société Générale 33

Goldman Sachs International 19 Standard Chartered plc 34

HSBC Holdings plc 20 The Royal Bank of Scotland plc 35

ING Groep N.V. 21 UBS AG 36

Investec Bank plc 22 UniCredit Group 37

Important Information 38

3

Innovative Solutions. Immaculate Service.

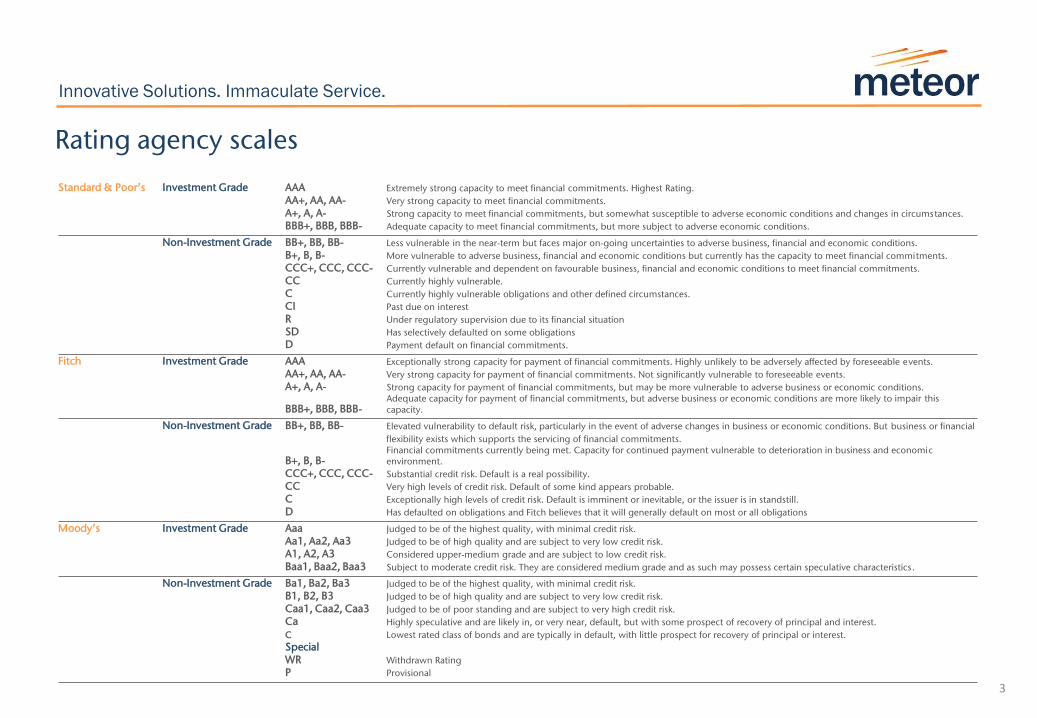

Rating agency scales

Standard & Poor’s Investment Grade AAA Extremely strong capacity to meet financial commitments. Highest Rating.

AA+, AA, AA- Very strong capacity to meet financial commitments.

A+, A, A- Strong capacity to meet financial commitments, but somewhat susceptible to adverse economic conditions and changes in circumstances.

BBB+, BBB, BBB- Adequate capacity to meet financial commitments, but more subject to adverse economic conditions.

Non-Investment Grade BB+, BB, BB- Less vulnerable in the near-term but faces major on-going uncertainties to adverse business, financial and economic conditions.

B+, B, B- More vulnerable to adverse business, financial and economic conditions but currently has the capacity to meet financial commitments.

CCC+, CCC, CCC- Currently vulnerable and dependent on favourable business, financial and economic conditions to meet financial commitments.

CC Currently highly vulnerable.

C Currently highly vulnerable obligations and other defined circumstances.

CI Past due on interest

R Under regulatory supervision due to its financial situation

SD Has selectively defaulted on some obligations

D Payment default on financial commitments.

Fitch Investment Grade AAA Exceptionally strong capacity for payment of financial commitments. Highly unlikely to be adversely affected by foreseeable events.

AA+, AA, AA- Very strong capacity for payment of financial commitments. Not significantly vulnerable to foreseeable events.

A+, A, A- Strong capacity for payment of financial commitments, but may be more vulnerable to adverse business or economic conditions.

BBB+, BBB, BBB-Adequate capacity for payment of financial commitments, but adverse business or economic conditions are more likely to impair this capacity.

Non-Investment Grade BB+, BB, BB- Elevated vulnerability to default risk, particularly in the event of adverse changes in business or economic conditions. But business or financial

flexibility exists which supports the servicing of financial commitments.

B+, B, B-Financial commitments currently being met. Capacity for continued payment vulnerable to deterioration in business and economic environment.

CCC+, CCC, CCC- Substantial credit risk. Default is a real possibility.

CC Very high levels of credit risk. Default of some kind appears probable.

C Exceptionally high levels of credit risk. Default is imminent or inevitable, or the issuer is in standstill.

D Has defaulted on obligations and Fitch believes that it will generally default on most or all obligations

Moody’s Investment Grade Aaa Judged to be of the highest quality, with minimal credit risk.

Aa1, Aa2, Aa3 Judged to be of high quality and are subject to very low credit risk.

A1, A2, A3 Considered upper-medium grade and are subject to low credit risk.

Baa1, Baa2, Baa3 Subject to moderate credit risk. They are considered medium grade and as such may possess certain speculative characteristics.

Non-Investment Grade Ba1, Ba2, Ba3 Judged to be of the highest quality, with minimal credit risk.

B1, B2, B3 Judged to be of high quality and are subject to very low credit risk.

Caa1, Caa2, Caa3 Judged to be of poor standing and are subject to very high credit risk.

Ca Highly speculative and are likely in, or very near, default, but with some prospect of recovery of principal and interest.

C Lowest rated class of bonds and are typically in default, with little prospect for recovery of principal or interest.

SpecialWR Withdrawn Rating

P Provisional

4

Innovative Solutions. Immaculate Service.

■ Historically credit ratings have been used as the principal measure of the financial strength of an underlying issuer. However, over recent years Credit Default Swap (‘CDS’) rates have become an additional measure of the financial security of a company and are now often utilised alongside ratings produced by credit rating agencies.

■ CDS rate levels are determined by the supply and demand of market participants and therefore do not rely on one single agency todetermine a company’s credit worthiness.

■ A CDS is basically an insurance contract - the buyer makes periodic payments to the seller and would receive a pay off in the event of failure in the underlying financial instrument/institution, effectively insuring against a debt default.

■ CDS spreads allow investors to analyse how risky an institution’s debt is perceived to be by the market, a relevant factor when considering the credit strength of a counterparty.

■ The CDS rates on the next page detail the % above London Interbank Offered Rate (‘LIBOR’) that buyers are willing to pay a seller in order to insure themselves against the likelihood of a credit default event of the underlying issuer.

■ Companies with higher CDS spreads are considered riskier by the market, as they are considered more likely to default than those with a lower CDS spread, all other things being equal.

■ Capital ratios are another measure of a bank's strength. These are used by regulatory authorities, with the most widely known being tier one capital ratio, which consists largely of shareholders' equity. It is the amount paid originally to purchase permanent capital (such as ordinary shares) of the bank and retained earnings (minus losses). It is the core measure of a bank's financial strength from a regulator's point of view. This ratio has been the subject of much review over recent years resulting in the Basel III Accord, requiring banks to maintain a minimum tier one capital ratio of 6%.

Credit default swaps

5

Innovative Solutions. Immaculate Service.

The banks referred to in this report include those that we currently have, or have previously had counterparty arrangements with, as well as, other banks that have or have had a presence in the structured products market. A rating outlook assesses the potential direction of a long-term credit rating over the intermediate term.

▪ Please note that not every bank listed has a rating from each of the three ratings agencies.

▪ * indicates that the credit rating agency has that company on watch. *+ indicates a possible upgrade, and *- a possible downgrade.

▪As of 10 June 2017, Moody’s ceased to display their “Long Term Rating” for banks. Not all banks listed above have been given an “Issuer Rating”.

Bloomberg/Meteor Research Department 27 July 2017

Credit rating overview

End of Q2

BANKLong Term Local Currency

Issuer Credit RatingOutlook Issuer Rating Outlook

Long Term Issuer Default

RatingOutlook

BANCO BILBAO VIZCAYA ARGENTA BBB+ POS Baa1 STABLE A- STABLE

BANCO SANTANDER SA A- STABLE A3 STABLE A- STABLE

BANK OF AMERICA CORP BBB+ STABLE Baa1 POS A STABLE

BARCLAYS BANK PLC A- NEG A1 NEG A STABLE

BNP PARIBAS A STABLE A1 STABLE A+ STABLE

CITIGROUP INC BBB+ STABLE - - A STABLE

COMMERZBANK AG A- NEG Baa1 STABLE BBB+ STABLE

CREDIT AGRICOLE SA A STABLE A1 STABLE A+ STABLE

CREDIT SUISSE AG A STABLE A1 STABLE A STABLE

DANSKE BANK A/S A STABLE A2 POS A STABLE

DEUTSCHE BANK AG-REGISTERED A- NEG Baa2 STABLE A- NEG

GOLDMAN SACHS INTERNATIONAL A+ STABLE A1 STABLE A STABLE

HSBC BANK PLC AA- NEG Aa2 NEG AA- STABLE

ING GROEP NV A- STABLE - - A+ STABLE

INVESTEC BANK PLC - - - - BBB STABLE

JPMORGAN CHASE & CO A- STABLE A3 STABLE A+ STABLE

LLOYDS BANKING GROUP PLC BBB+ NEG - - A+ STABLE

MACQUARIE BANK A NEG - - A STABLE

MORGAN STANLEY BBB+ STABLE A3 STABLE A STABLE

NATIXIS A STABLE A2 POS A STABLE

NOMURA BANK INTERNATIONAL PL A NEG - - - -

NORTHERN TRUST CORP A+ STABLE A2 STABLE AA- STABLE

COOPERATIEVE RABOBANK UA A+ STABLE Aa2 NEG AA- STABLE

ROYAL BANK OF CANADA AA- NEG A1 NEG AA NEG

SANTANDER UK PLC A NEG Aa3 NEG A STABLE

SOCIETE GENERALE SA A STABLE - - A STABLE

STANDARD CHARTERED PLC BBB+ STABLE - - A+ STABLE

ROYAL BANK OF SCOTLAND PLC/T BBB+ STABLE - - BBB+ STABLE

UBS AG-REG A+ STABLE A1 STABLE A+ STABLE

UNICREDIT SPA BBB- STABLE - - BBB STABLE

Standard & Poor's Moody's Fitch

6

Innovative Solutions. Immaculate Service.

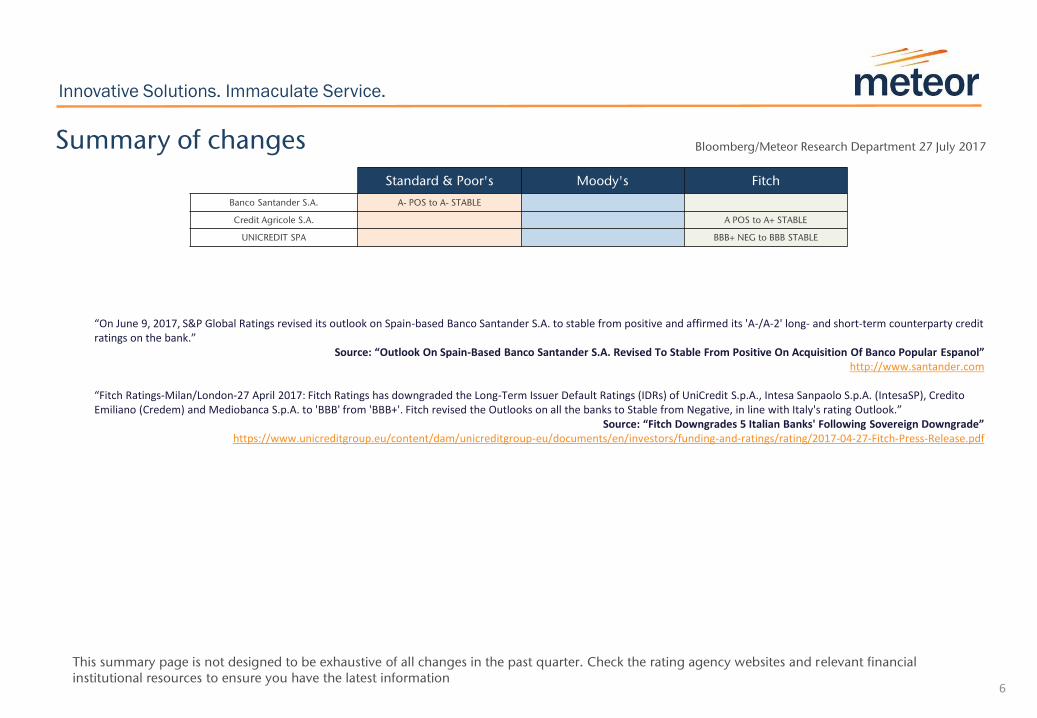

This summary page is not designed to be exhaustive of all changes in the past quarter. Check the rating agency websites and relevant financial institutional resources to ensure you have the latest information

Summary of changes Bloomberg/Meteor Research Department 27 July 2017

“On June 9, 2017, S&P Global Ratings revised its outlook on Spain-based Banco Santander S.A. to stable from positive and affirmed its 'A-/A-2' long- and short-term counterparty credit ratings on the bank.”

Source: “Outlook On Spain-Based Banco Santander S.A. Revised To Stable From Positive On Acquisition Of Banco Popular Espanol”http://www.santander.com

“Fitch Ratings-Milan/London-27 April 2017: Fitch Ratings has downgraded the Long-Term Issuer Default Ratings (IDRs) of UniCredit S.p.A., Intesa Sanpaolo S.p.A. (IntesaSP), CreditoEmiliano (Credem) and Mediobanca S.p.A. to 'BBB' from 'BBB+'. Fitch revised the Outlooks on all the banks to Stable from Negative, in line with Italy's rating Outlook.”

Source: “Fitch Downgrades 5 Italian Banks' Following Sovereign Downgrade”https://www.unicreditgroup.eu/content/dam/unicreditgroup-eu/documents/en/investors/funding-and-ratings/rating/2017-04-27-Fitch-Press-Release.pdf

Standard & Poor's Moody's Fitch

Banco Santander S.A. A- POS to A- STABLE

Credit Agricole S.A. A POS to A+ STABLE

UNICREDIT SPA BBB+ NEG to BBB STABLE

7

Innovative Solutions. Immaculate Service.

The following pages summarise the main credit indicators for the individual banks that we cover. This includes share price changes in the last quarter, CDS level changes in the last quarter and any credit rating revisions in the last quarter.

We plot a bank’s share price against their 5 year CDS on senior debt in the relevant local currency where possible. For reference, we also include the Markit iTraxx Europe Senior Generic Financial 5Y CDS Index as a benchmark for European CDS rates. This is based on 25 equally weighted CDS rates on investment grade European entities. The list below shows the constituents as at 27 July 2017.

We also plot bar charts, where possible, of the CDS rates from the last 2 quarters for comparison and include the 1, 3, 5 and 10 year tenor curves.

Bloomberg/Meteor Research Department 27 July 2017

Individual bank summaries

Aegon NV Banco Bilbao Vizcaya Argentari Cooperatieve Rabobank UA Hannover Rueck SE Mediobanca SpA Swiss Reinsurance Co Ltd

Allianz SE Banco Santander SA Credit Agricole SA HSBC Bank PLC Muenchener Rueckversicherungs- Royal Bank of Scotland PLC/The

Assicurazioni Generali SpA Barclays Bank PLC Credit Suisse Group AG ING Bank NV Prudential PLC UBS AG

Aviva PLC BNP Paribas SA Danske Bank A/S Intesa Sanpaolo SpA Societe Generale SA UniCredit SpA

AXA SA Commerzbank AG Deutsche Bank AG Lloyds Bank PLC Standard Chartered Bank Zurich Insurance Co Ltd

8

Innovative Solutions. Immaculate Service.

BBVA

0

50

100

150

200

250

300

350

400

450

500

0

2

4

6

8

10

12

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Banco Bilbao Vizcaya Argentaria 5Y CDS CDS Benchmark

1Y

CD

S, 3

3.3

6

1Y

CD

S, 1

4.8

05

3Y

CD

S, 7

4.5

2

3Y

CD

S, 4

0.4

85

5Y

CD

S, 1

14

.99

5

5Y

CD

S, 6

3.3

05

10

Y C

DS

, 1

59

.35

10

Y C

DS

, 9

6.6

95

0

20

40

60

80

100

120

140

160

180

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 7.27

End of Q2 7.265

Change on Quarter (%) -0.07%

Bloomberg Ticker: bbva sm equity

Credit Default Swap (5Y)

End of Q1 114.995

End of Q2 63.305

Change on Quarter (%) -44.95%

Bloomberg Ticker: BBVA CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating BBB+

Date Rating Effective 06/10/15

Ratings Outlook POS

Date Outlook Effective 03/04/17

Credit Rating (Moody's)

Issuer Rating Baa1

Date Rating Effective 17/06/15

Ratings Outlook STABLE

Date Outlook Effective 17/06/15

Credit Rating (Fitch)

Long Term Issuer Default Rating A-

Date Rating Effective 29/05/14

Ratings Outlook STABLE

Date Outlook Effective 29/05/14

Bloomberg Ticker: bbva sm equity

Capita l

Tier One Capital Ratio 12.1%

Market Cap (GBP millions)* 45,602

Bloomberg Ticker: bbva sm equity

*Converted from quoted currency based on prevailing exchange rate as of source date

9

Innovative Solutions. Immaculate Service.

Banco Santander S.A.

0

50

100

150

200

250

300

350

400

450

0

1

2

3

4

5

6

7

8

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Banco Santander S.A. 5Y CDS CDS Benchmark

1Y

CD

S, 2

3.8

85

1Y

CD

S, 1

1.1

4

3Y

CD

S, 6

0.9

9

3Y

CD

S, 3

1.5

8

5Y

CD

S, 9

8.7

7

5Y

CD

S, 5

3.0

1

10

Y C

DS

, 1

39

.75

10

Y C

DS

, 8

3.8

95

0

20

40

60

80

100

120

140

160

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 5.6505

End of Q2 5.6968

Change on Quarter (%) 0.82%

Bloomberg Ticker: bbva sm equity Bloomberg Ticker: san sm equity

Credit Default Swap (5Y)

End of Q1 98.77

End of Q2 53.01

Change on Quarter (%) -46.33%

Bloomberg Ticker: BBVA CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: SANTAN CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A-

Date Rating Effective 06/10/15

Ratings Outlook STABLE

Date Outlook Effective 09/06/17

Credit Rating (Moody's)

Issuer Rating A3

Date Rating Effective 17/06/15

Ratings Outlook STABLE

Date Outlook Effective 22/02/16

Credit Rating (Fitch)

Long Term Issuer Default Rating A-

Date Rating Effective 29/05/14

Ratings Outlook STABLE

Date Outlook Effective 29/05/14

Bloomberg Ticker: bbva sm equity Bloomberg Ticker: san sm equity

Capita l

Tier One Capital Ratio 12.53%

Market Cap (GBP millions)* 76,217

Bloomberg Ticker: bbva sm equity Bloomberg Ticker: san sm equity

*Converted from quoted currency based on prevailing exchange rate as of source date

10

Innovative Solutions. Immaculate Service.

Bank of America Corporation

0

50

100

150

200

250

300

0

5

10

15

20

25

30

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Bank of America Corporation 5Y CDS CDS Benchmark

1Y

CD

S, 2

5.4

5

1Y

CD

S, 1

7.1

6

3Y

CD

S, 4

1.8

4

3Y

CD

S, 2

9.9

2

5Y

CD

S, 6

3.0

6

5Y

CD

S, 4

9

10

Y C

DS

, 1

03

.36

5

10

Y C

DS

, 8

8.7

5

0

20

40

60

80

100

120

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 23.59

End of Q2 24.26

Change on Quarter (%) 2.84%

Bloomberg Ticker: san sm equity Bloomberg Ticker: bac us equity

Credit Default Swap (5Y)

End of Q1 63.06

End of Q2 49

Change on Quarter (%) -22.30%

Bloomberg Ticker: SANTAN CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: BOFA CDS USD SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating BBB+

Date Rating Effective 02/12/15

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating Baa1

Date Rating Effective 28/05/15

Ratings Outlook POS

Date Outlook Effective 24/01/17

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 15/12/11

Ratings Outlook STABLE

Date Outlook Effective 19/05/15

Bloomberg Ticker: san sm equity Bloomberg Ticker: bac us equity

Capita l

Tier One Capital Ratio 13.6%

Market Cap (GBP millions)* 181,890

Bloomberg Ticker: san sm equity Bloomberg Ticker: bac us equity

*Converted from quoted currency based on prevailing exchange rate as of source date

11

Innovative Solutions. Immaculate Service.

Barclays Bank plc

0

50

100

150

200

250

300

0

50

100

150

200

250

300

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Barclays Bank plc 5Y CDS CDS Benchmark

1Y

CD

S, 3

2.2

6

1Y

CD

S, 1

0.1

25

3Y

CD

S, 5

5.4

85

3Y

CD

S, 2

7.1

65

5Y

CD

S, 7

7.8

5Y

CD

S, 4

0.9

2

10

Y C

DS

, 1

07

.79

5

10

Y C

DS

, 6

3.6

8

0

20

40

60

80

100

120

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 225.1

End of Q2 202.75

Change on Quarter (%) -9.93%

Bloomberg Ticker: bac us equity Bloomberg Ticker: barc ln equity

Credit Default Swap (5Y)

End of Q1 77.8

End of Q2 40.92

Change on Quarter (%) -47.40%

Bloomberg Ticker: BOFA CDS USD SR 5Y D14 Curncy Bloomberg Ticker: BACR CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A-

Date Rating Effective 09/06/15

Ratings Outlook NEG

Date Outlook Effective 07/07/16

Credit Rating (Moody's)

Issuer Rating A1

Date Rating Effective 12/12/16

Ratings Outlook NEG

Date Outlook Effective 12/12/16

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 15/12/11

Ratings Outlook STABLE

Date Outlook Effective 15/12/11

Bloomberg Ticker: bac us equity Bloomberg Ticker: 8376923Z LN equity

Capita l

Tier One Capital Ratio 15.6%

Market Cap (GBP millions)* 35,592

Bloomberg Ticker: bac us equity Bloomberg Ticker: barc ln equity

12

Innovative Solutions. Immaculate Service.

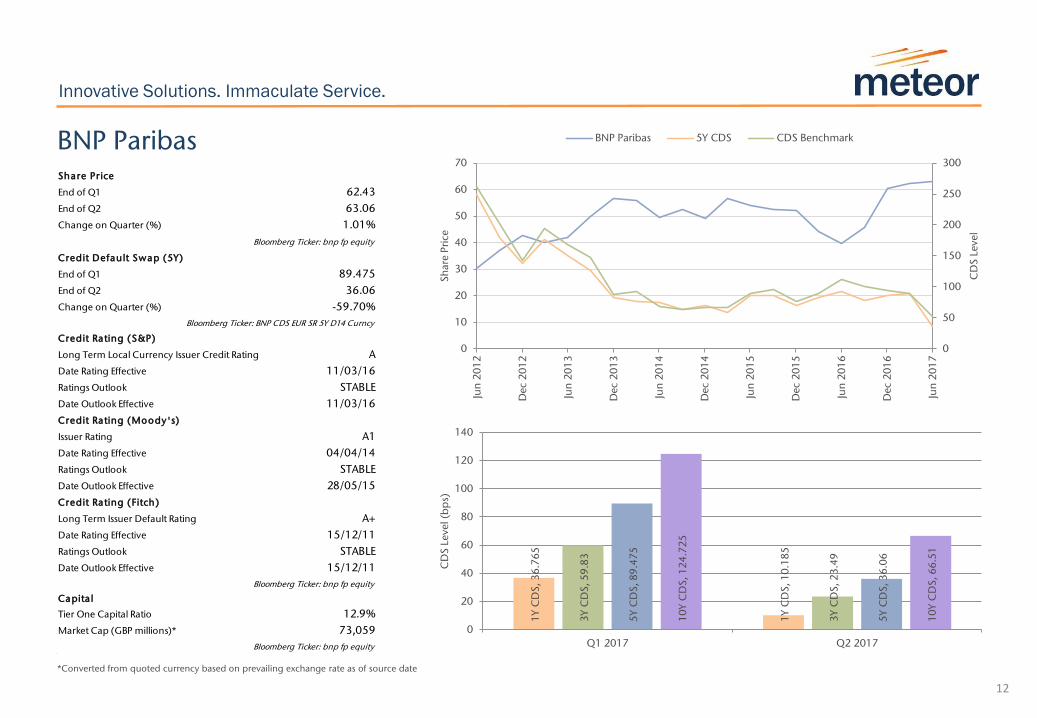

BNP Paribas

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

BNP Paribas 5Y CDS CDS Benchmark

1Y

CD

S, 3

6.7

65

1Y

CD

S, 1

0.1

85

3Y

CD

S, 5

9.8

3

3Y

CD

S, 2

3.4

9

5Y

CD

S, 8

9.4

75

5Y

CD

S, 3

6.0

6

10

Y C

DS

, 1

24

.72

5

10

Y C

DS

, 6

6.5

1

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 62.43

End of Q2 63.06

Change on Quarter (%) 1.01%

Bloomberg Ticker: barc ln equity Bloomberg Ticker: bnp fp equity

Credit Default Swap (5Y)

End of Q1 89.475

End of Q2 36.06

Change on Quarter (%) -59.70%

Bloomberg Ticker: BACR CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: BNP CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 11/03/16

Ratings Outlook STABLE

Date Outlook Effective 11/03/16

Credit Rating (Moody's)

Issuer Rating A1

Date Rating Effective 04/04/14

Ratings Outlook STABLE

Date Outlook Effective 28/05/15

Credit Rating (Fitch)

Long Term Issuer Default Rating A+

Date Rating Effective 15/12/11

Ratings Outlook STABLE

Date Outlook Effective 15/12/11

Bloomberg Ticker: 8376923Z LN equity Bloomberg Ticker: bnp fp equity

Capita l

Tier One Capital Ratio 12.9%

Market Cap (GBP millions)* 73,059

Bloomberg Ticker: barc ln equity Bloomberg Ticker: bnp fp equity

*Converted from quoted currency based on prevailing exchange rate as of source date

13

Innovative Solutions. Immaculate Service.

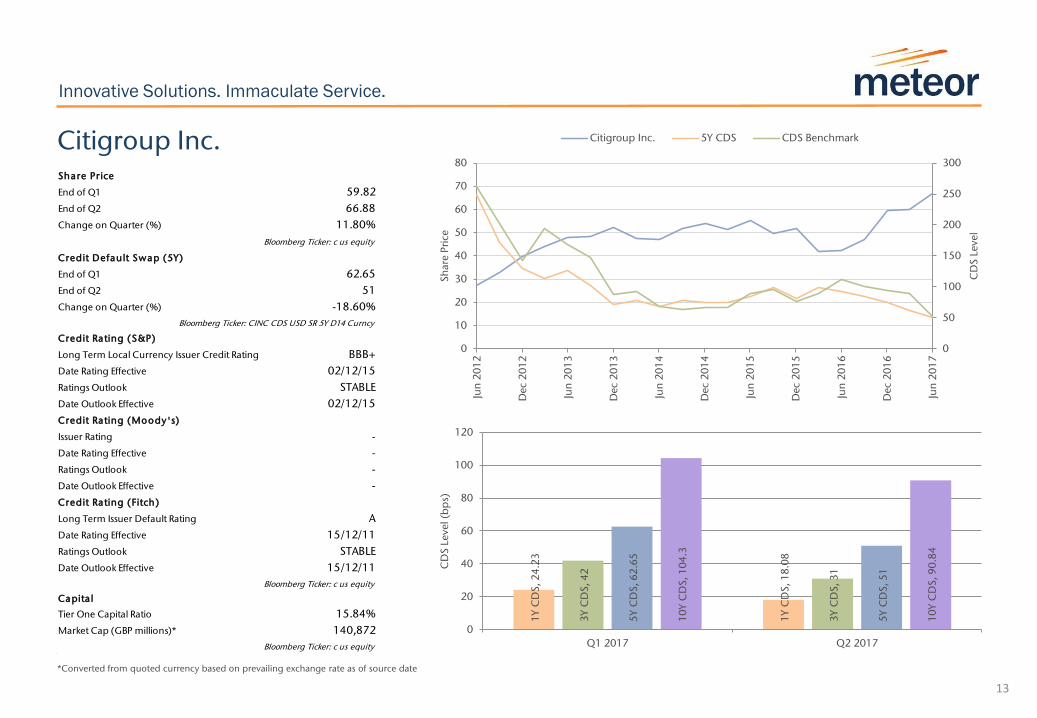

Citigroup Inc.

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Citigroup Inc. 5Y CDS CDS Benchmark

1Y

CD

S, 2

4.2

3

1Y

CD

S, 1

8.0

8

3Y

CD

S, 4

2

3Y

CD

S, 3

1

5Y

CD

S, 6

2.6

5

5Y

CD

S, 5

1

10

Y C

DS

, 1

04

.3

10

Y C

DS

, 9

0.8

4

0

20

40

60

80

100

120

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 59.82

End of Q2 66.88

Change on Quarter (%) 11.80%

Bloomberg Ticker: bnp fp equity Bloomberg Ticker: c us equity

Credit Default Swap (5Y)

End of Q1 62.65

End of Q2 51

Change on Quarter (%) -18.60%

Bloomberg Ticker: BNP CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: CINC CDS USD SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating BBB+

Date Rating Effective 02/12/15

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 15/12/11

Ratings Outlook STABLE

Date Outlook Effective 15/12/11

Bloomberg Ticker: bnp fp equity Bloomberg Ticker: c us equity

Capita l

Tier One Capital Ratio 15.84%

Market Cap (GBP millions)* 140,872

Bloomberg Ticker: bnp fp equity Bloomberg Ticker: c us equity

*Converted from quoted currency based on prevailing exchange rate as of source date

14

Innovative Solutions. Immaculate Service.

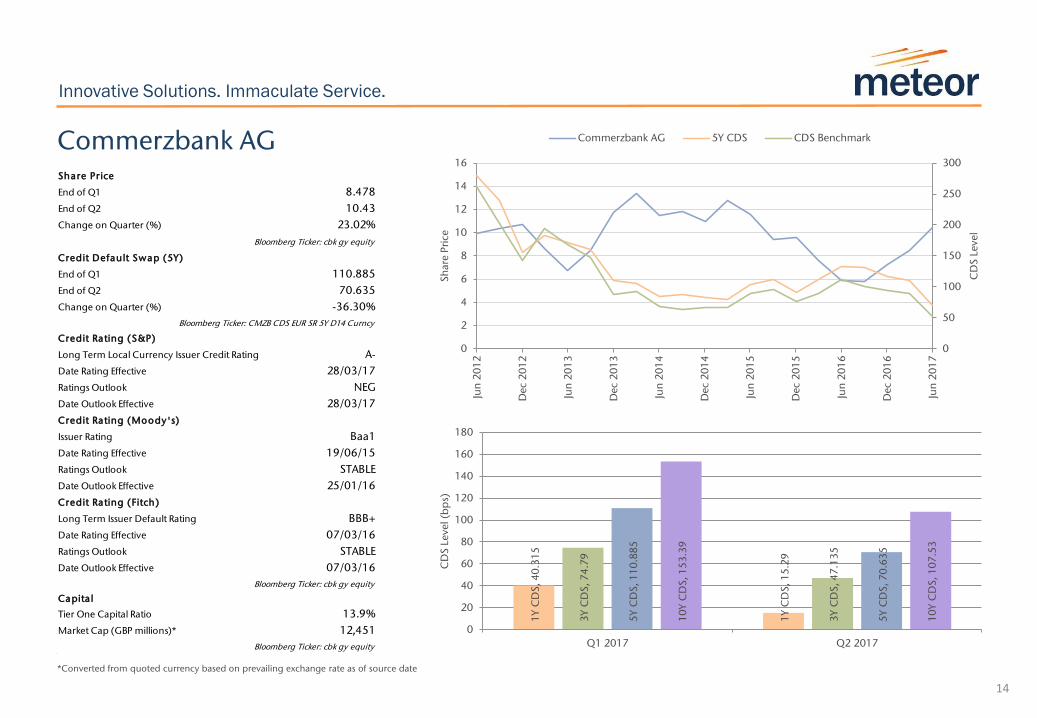

Commerzbank AG

0

50

100

150

200

250

300

0

2

4

6

8

10

12

14

16

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Commerzbank AG 5Y CDS CDS Benchmark

1Y

CD

S, 4

0.3

15

1Y

CD

S, 1

5.2

9

3Y

CD

S, 7

4.7

9

3Y

CD

S, 4

7.1

35

5Y

CD

S, 1

10

.88

5

5Y

CD

S, 7

0.6

35

10

Y C

DS

, 1

53

.39

10

Y C

DS

, 1

07

.53

0

20

40

60

80

100

120

140

160

180

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 8.478

End of Q2 10.43

Change on Quarter (%) 23.02%

Bloomberg Ticker: c us equity Bloomberg Ticker: cbk gy equity

Credit Default Swap (5Y)

End of Q1 110.885

End of Q2 70.635

Change on Quarter (%) -36.30%

Bloomberg Ticker: CINC CDS USD SR 5Y D14 Curncy Bloomberg Ticker: CMZB CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A-

Date Rating Effective 28/03/17

Ratings Outlook NEG

Date Outlook Effective 28/03/17

Credit Rating (Moody's)

Issuer Rating Baa1

Date Rating Effective 19/06/15

Ratings Outlook STABLE

Date Outlook Effective 25/01/16

Credit Rating (Fitch)

Long Term Issuer Default Rating BBB+

Date Rating Effective 07/03/16

Ratings Outlook STABLE

Date Outlook Effective 07/03/16

Bloomberg Ticker: c us equity Bloomberg Ticker: cbk gy equity

Capita l

Tier One Capital Ratio 13.9%

Market Cap (GBP millions)* 12,451

Bloomberg Ticker: c us equity Bloomberg Ticker: cbk gy equity

*Converted from quoted currency based on prevailing exchange rate as of source date

15

Innovative Solutions. Immaculate Service.

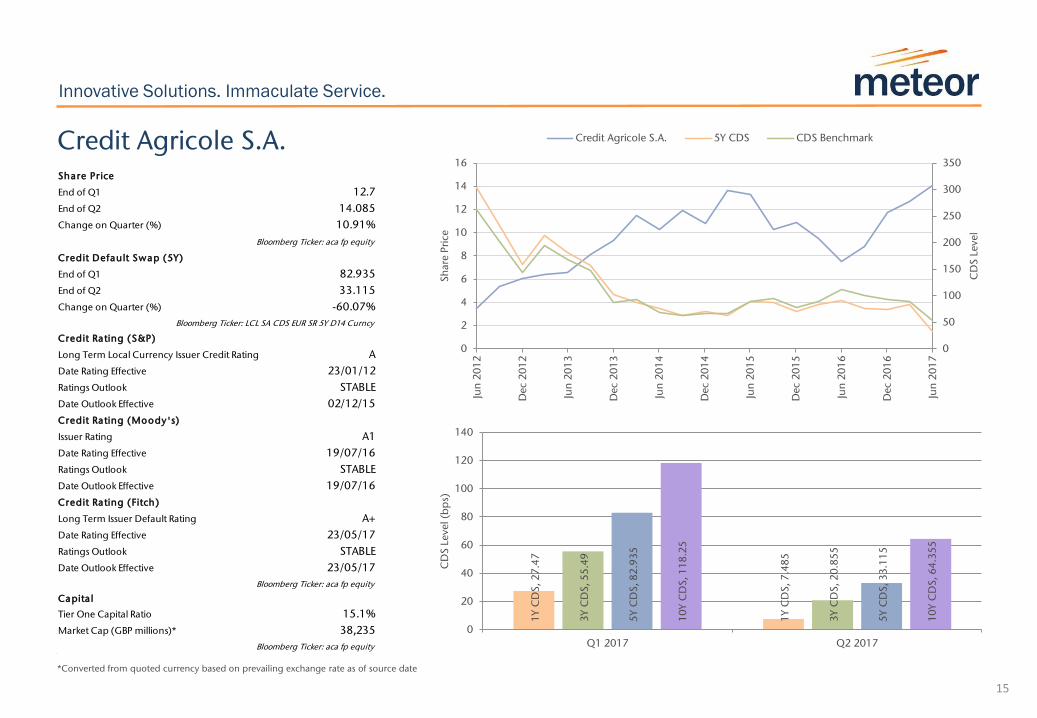

Credit Agricole S.A.

0

50

100

150

200

250

300

350

0

2

4

6

8

10

12

14

16

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Credit Agricole S.A. 5Y CDS CDS Benchmark

1Y

CD

S, 2

7.4

7

1Y

CD

S, 7

.48

5

3Y

CD

S, 5

5.4

9

3Y

CD

S, 2

0.8

55

5Y

CD

S, 8

2.9

35

5Y

CD

S, 3

3.1

15

10

Y C

DS

, 1

18

.25

10

Y C

DS

, 6

4.3

55

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 12.7

End of Q2 14.085

Change on Quarter (%) 10.91%

Bloomberg Ticker: cbk gy equity Bloomberg Ticker: aca fp equity

Credit Default Swap (5Y)

End of Q1 82.935

End of Q2 33.115

Change on Quarter (%) -60.07%

Bloomberg Ticker: CMZB CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: LCL SA CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 23/01/12

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating A1

Date Rating Effective 19/07/16

Ratings Outlook STABLE

Date Outlook Effective 19/07/16

Credit Rating (Fitch)

Long Term Issuer Default Rating A+

Date Rating Effective 23/05/17

Ratings Outlook STABLE

Date Outlook Effective 23/05/17

Bloomberg Ticker: cbk gy equity Bloomberg Ticker: aca fp equity

Capita l

Tier One Capital Ratio 15.1%

Market Cap (GBP millions)* 38,235

Bloomberg Ticker: cbk gy equity Bloomberg Ticker: aca fp equity

*Converted from quoted currency based on prevailing exchange rate as of source date

16

Innovative Solutions. Immaculate Service.

Credit Suisse AG

0

50

100

150

200

250

300

0

5

10

15

20

25

30

35

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Credit Suisse AG 5Y CDS CDS Benchmark

1Y

CD

S, 3

4.7

8

1Y

CD

S, 1

4.2

45

3Y

CD

S, 6

5.6

9

3Y

CD

S, 4

2.7

65

5Y

CD

S, 1

03

.03

5Y

CD

S, 6

7.3

7

10

Y C

DS

, 1

36

.18

5

10

Y C

DS

, 9

8.9

9

0

20

40

60

80

100

120

140

160

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 14.84

End of Q2 14.6

Change on Quarter (%) -1.62%

Bloomberg Ticker: aca fp equity Bloomberg Ticker: cs us equity

Credit Default Swap (5Y)

End of Q1 103.03

End of Q2 67.37

Change on Quarter (%) -34.61%

Bloomberg Ticker: LCL SA CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: CRDSUI CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 02/07/13

Ratings Outlook STABLE

Date Outlook Effective 09/06/15

Credit Rating (Moody's)

Issuer Rating A1

Date Rating Effective 13/12/16

Ratings Outlook STABLE

Date Outlook Effective 13/12/16

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 15/12/11

Ratings Outlook STABLE

Date Outlook Effective 24/05/16

Bloomberg Ticker: aca fp equity Bloomberg Ticker: svbzk sw equity

Capita l

Tier One Capital Ratio 18%

Market Cap (GBP millions)* 29,841

Bloomberg Ticker: aca fp equity Bloomberg Ticker: cs us equity

*Converted from quoted currency based on prevailing exchange rate as of source date

17

Innovative Solutions. Immaculate Service.

Danske Bank A/S

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Danske Bank A/S 5Y CDS CDS Benchmark

1Y

CD

S, 1

3.1

1

1Y

CD

S, 5

.42

5

3Y

CD

S, 2

6.2

8

3Y

CD

S, 1

5.6

25

5Y

CD

S, 4

7.5

4

5Y

CD

S, 2

9.6

3

10

Y C

DS

, 7

6.5

9

10

Y C

DS

, 5

3.3

45

0

10

20

30

40

50

60

70

80

90

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 237.5

End of Q2 250.4

Change on Quarter (%) 5.43%

Bloomberg Ticker: cs us equity Bloomberg Ticker: danske dc equity

Credit Default Swap (5Y)

End of Q1 47.54

End of Q2 29.63

Change on Quarter (%) -37.67%

Bloomberg Ticker: CRDSUI CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: DANBNK CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 29/04/14

Ratings Outlook STABLE

Date Outlook Effective 13/07/15

Credit Rating (Moody's)

Issuer Rating A2

Date Rating Effective 17/06/15

Ratings Outlook POS

Date Outlook Effective 12/10/16

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 14/12/11

Ratings Outlook STABLE

Date Outlook Effective 05/06/13

Bloomberg Ticker: svbzk sw equity Bloomberg Ticker: danske dc equity

Capita l

Tier One Capital Ratio 19.1%

Market Cap (GBP millions)* 28,688

Bloomberg Ticker: cs us equity Bloomberg Ticker: danske dc equity

*Converted from quoted currency based on prevailing exchange rate as of source date

18

Innovative Solutions. Immaculate Service.

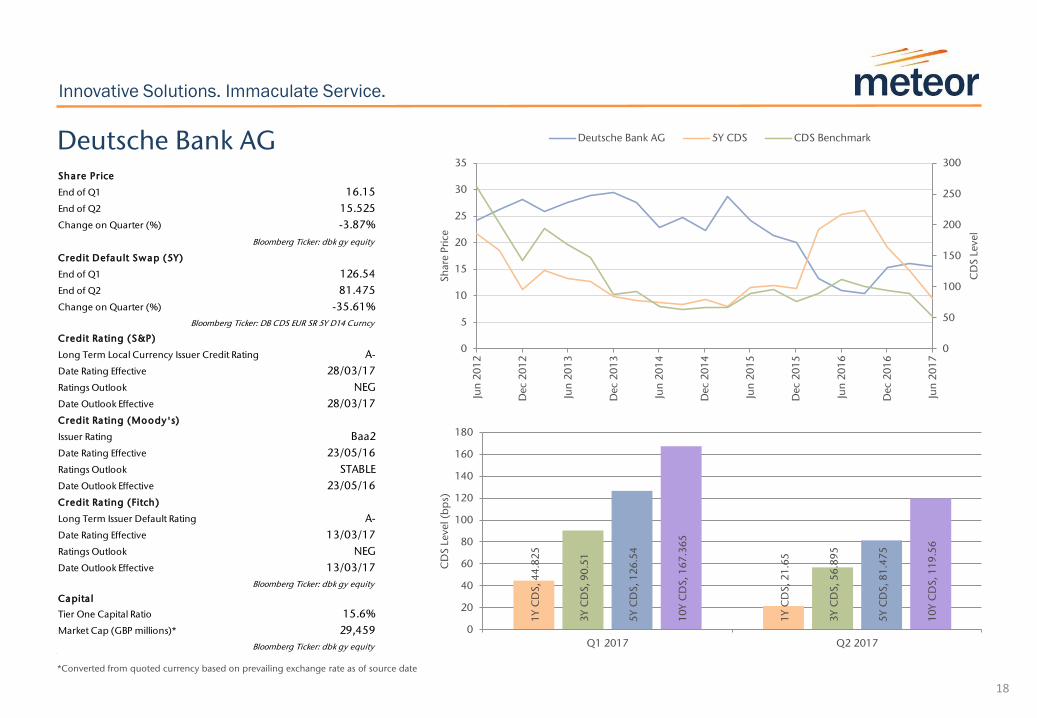

Deutsche Bank AG

0

50

100

150

200

250

300

0

5

10

15

20

25

30

35

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Deutsche Bank AG 5Y CDS CDS Benchmark

1Y

CD

S, 4

4.8

25

1Y

CD

S, 2

1.6

5

3Y

CD

S, 9

0.5

1

3Y

CD

S, 5

6.8

95

5Y

CD

S, 1

26

.54

5Y

CD

S, 8

1.4

75

10

Y C

DS

, 1

67

.36

5

10

Y C

DS

, 1

19

.56

0

20

40

60

80

100

120

140

160

180

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 16.15

End of Q2 15.525

Change on Quarter (%) -3.87%

Bloomberg Ticker: danske dc equity Bloomberg Ticker: dbk gy equity

Credit Default Swap (5Y)

End of Q1 126.54

End of Q2 81.475

Change on Quarter (%) -35.61%

Bloomberg Ticker: DANBNK CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: DB CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A-

Date Rating Effective 28/03/17

Ratings Outlook NEG

Date Outlook Effective 28/03/17

Credit Rating (Moody's)

Issuer Rating Baa2

Date Rating Effective 23/05/16

Ratings Outlook STABLE

Date Outlook Effective 23/05/16

Credit Rating (Fitch)

Long Term Issuer Default Rating A-

Date Rating Effective 13/03/17

Ratings Outlook NEG

Date Outlook Effective 13/03/17

Bloomberg Ticker: danske dc equity Bloomberg Ticker: dbk gy equity

Capita l

Tier One Capital Ratio 15.6%

Market Cap (GBP millions)* 29,459

Bloomberg Ticker: danske dc equity Bloomberg Ticker: dbk gy equity

*Converted from quoted currency based on prevailing exchange rate as of source date

19

Innovative Solutions. Immaculate Service.

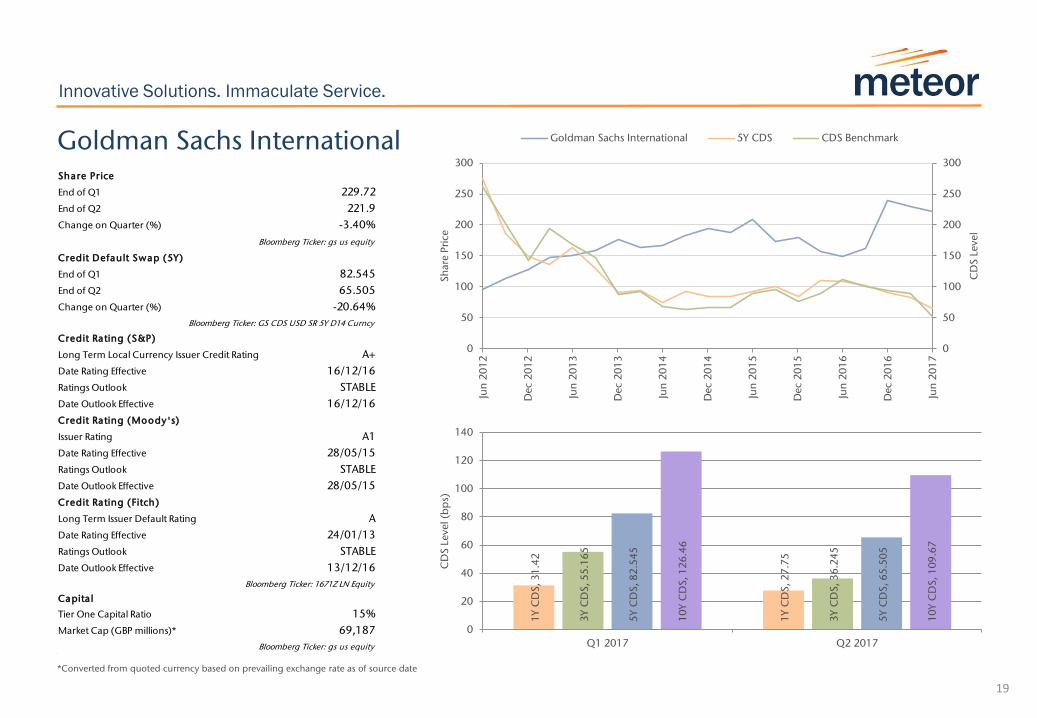

Goldman Sachs International

0

50

100

150

200

250

300

0

50

100

150

200

250

300

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Goldman Sachs International 5Y CDS CDS Benchmark

1Y

CD

S, 3

1.4

2

1Y

CD

S, 2

7.7

5

3Y

CD

S, 5

5.1

65

3Y

CD

S, 3

6.2

45

5Y

CD

S, 8

2.5

45

5Y

CD

S, 6

5.5

05

10

Y C

DS

, 1

26

.46

10

Y C

DS

, 1

09

.67

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 229.72

End of Q2 221.9

Change on Quarter (%) -3.40%

Bloomberg Ticker: dbk gy equity Bloomberg Ticker: gs us equity

Credit Default Swap (5Y)

End of Q1 82.545

End of Q2 65.505

Change on Quarter (%) -20.64%

Bloomberg Ticker: DB CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: GS CDS USD SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A+

Date Rating Effective 16/12/16

Ratings Outlook STABLE

Date Outlook Effective 16/12/16

Credit Rating (Moody's)

Issuer Rating A1

Date Rating Effective 28/05/15

Ratings Outlook STABLE

Date Outlook Effective 28/05/15

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 24/01/13

Ratings Outlook STABLE

Date Outlook Effective 13/12/16

Bloomberg Ticker: dbk gy equity Bloomberg Ticker: 1671Z LN Equity

Capita l

Tier One Capital Ratio 15%

Market Cap (GBP millions)* 69,187

Bloomberg Ticker: dbk gy equity Bloomberg Ticker: gs us equity

*Converted from quoted currency based on prevailing exchange rate as of source date

20

Innovative Solutions. Immaculate Service.

HSBC Holdings plc

0

50

100

150

200

250

300

0

100

200

300

400

500

600

700

800

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

HSBC Bank PLC 5Y CDS CDS Benchmark

1Y

CD

S, 1

6.2

8

1Y

CD

S, 6

.99

3Y

CD

S, 4

1.0

7

3Y

CD

S, 1

6.7

8

5Y

CD

S, 6

3.9

65

5Y

CD

S, 2

8.0

35

10

Y C

DS

, 9

4.4

5

10

Y C

DS

, 5

0.3

95

0

10

20

30

40

50

60

70

80

90

100

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 650.9

End of Q2 711.7

Change on Quarter (%) 9.34%

Bloomberg Ticker: gs us equity Bloomberg Ticker: hsba ln equity

Credit Default Swap (5Y)

End of Q1 63.965

End of Q2 28.035

Change on Quarter (%) -56.17%

Bloomberg Ticker: GS CDS USD SR 5Y D14 Curncy Bloomberg Ticker: HSBC BK CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating AA-

Date Rating Effective 09/06/15

Ratings Outlook NEG

Date Outlook Effective 07/07/16

Credit Rating (Moody's)

Issuer Rating Aa2

Date Rating Effective 28/05/15

Ratings Outlook NEG

Date Outlook Effective 28/06/16

Credit Rating (Fitch)

Long Term Issuer Default Rating AA-

Date Rating Effective 07/12/12

Ratings Outlook STABLE

Date Outlook Effective 07/12/12

Bloomberg Ticker: 1671Z LN Equity Bloomberg Ticker: mid ln equity

Capita l

Tier One Capital Ratio 16.1%

Market Cap (GBP millions)* 151,599

Bloomberg Ticker: gs us equity Bloomberg Ticker: hsba ln equity

*Converted from quoted currency based on prevailing exchange rate as of source date

21

Innovative Solutions. Immaculate Service.

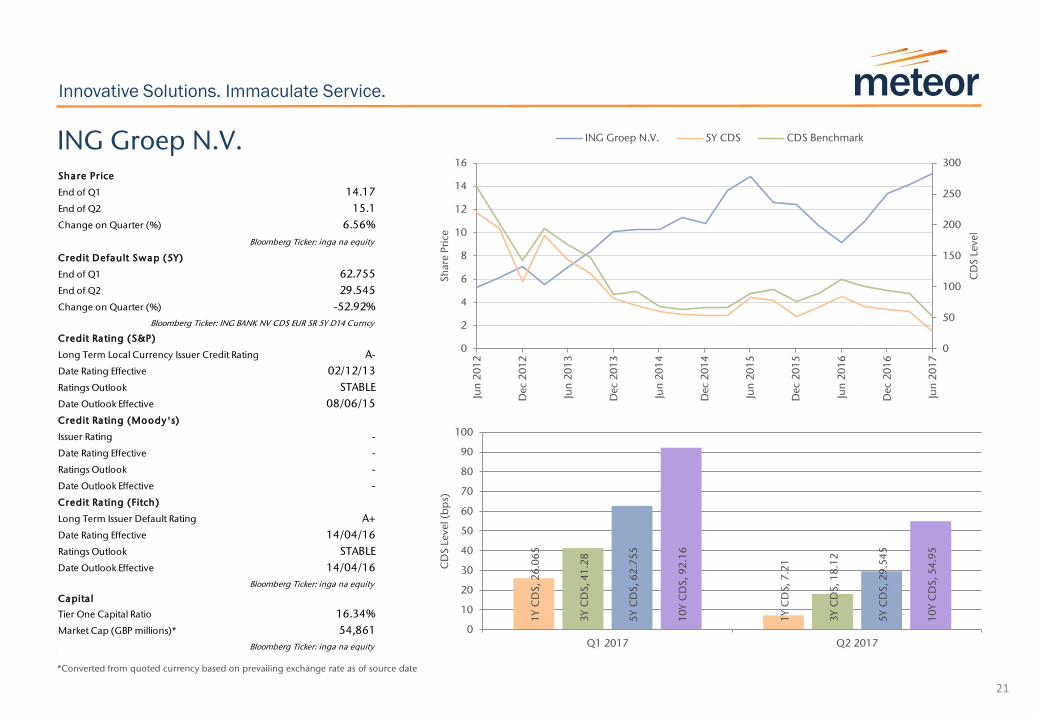

ING Groep N.V.

0

50

100

150

200

250

300

0

2

4

6

8

10

12

14

16

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

ING Groep N.V. 5Y CDS CDS Benchmark

1Y

CD

S, 2

6.0

65

1Y

CD

S, 7

.21

3Y

CD

S, 4

1.2

8

3Y

CD

S, 1

8.1

2

5Y

CD

S, 6

2.7

55

5Y

CD

S, 2

9.5

45

10

Y C

DS

, 9

2.1

6

10

Y C

DS

, 5

4.9

5

0

10

20

30

40

50

60

70

80

90

100

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 14.17

End of Q2 15.1

Change on Quarter (%) 6.56%

Bloomberg Ticker: hsba ln equity Bloomberg Ticker: inga na equity

Credit Default Swap (5Y)

End of Q1 62.755

End of Q2 29.545

Change on Quarter (%) -52.92%

Bloomberg Ticker: HSBC BK CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: ING BANK NV CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A-

Date Rating Effective 02/12/13

Ratings Outlook STABLE

Date Outlook Effective 08/06/15

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating A+

Date Rating Effective 14/04/16

Ratings Outlook STABLE

Date Outlook Effective 14/04/16

Bloomberg Ticker: mid ln equity Bloomberg Ticker: inga na equity

Capita l

Tier One Capital Ratio 16.34%

Market Cap (GBP millions)* 54,861

Bloomberg Ticker: hsba ln equity Bloomberg Ticker: inga na equity

*Converted from quoted currency based on prevailing exchange rate as of source date

22

Innovative Solutions. Immaculate Service.

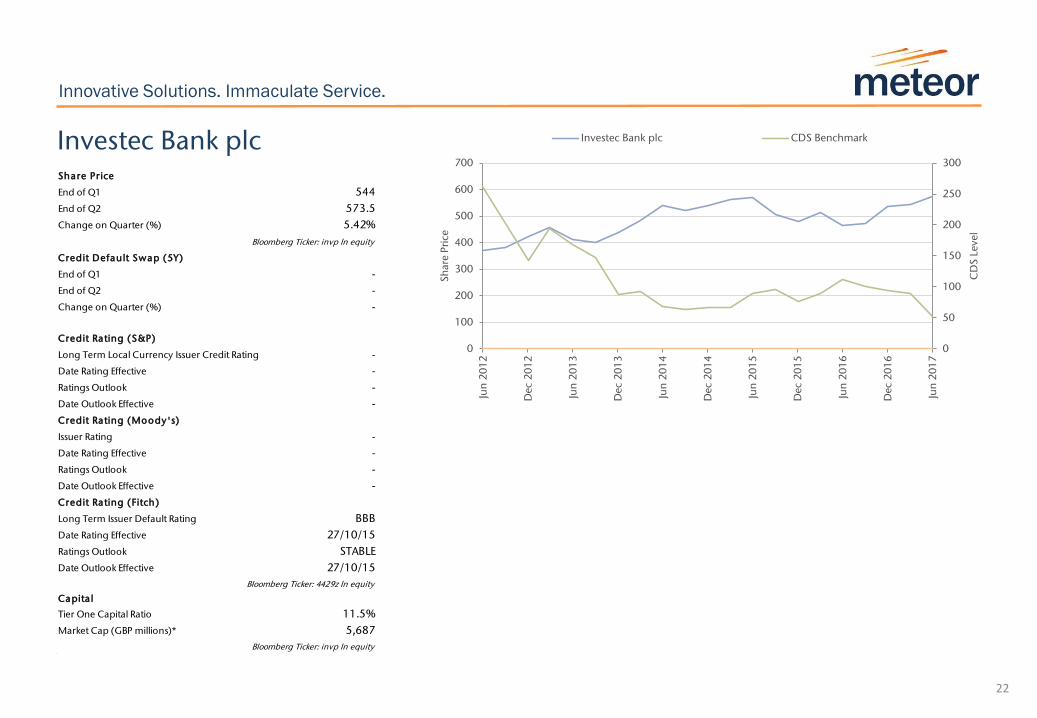

Investec Bank plc

0

50

100

150

200

250

300

0

100

200

300

400

500

600

700

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Investec Bank plc 5Y CDS CDS Benchmark

Share Pr ice

End of Q1 544

End of Q2 573.5

Change on Quarter (%) 5.42%

Bloomberg Ticker: inga na equity Bloomberg Ticker: invp ln equity

Credit Default Swap (5Y)

End of Q1 -

End of Q2 -

Change on Quarter (%) -

Bloomberg Ticker: ING BANK NV CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating BBB

Date Rating Effective 27/10/15

Ratings Outlook STABLE

Date Outlook Effective 27/10/15

Bloomberg Ticker: inga na equity Bloomberg Ticker: 4429z ln equity

Capita l

Tier One Capital Ratio 11.5%

Market Cap (GBP millions)* 5,687

Bloomberg Ticker: inga na equity Bloomberg Ticker: invp ln equity

23

Innovative Solutions. Immaculate Service.

JPMorgan Chase & Co

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

90

100

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

JPMorgan Chase & Co 5Y CDS CDS Benchmark

1Y

CD

S, 2

5.3

2

1Y

CD

S, 1

7.1

6

3Y

CD

S, 3

7.8

95

3Y

CD

S, 2

7

5Y

CD

S, 5

5.0

15

5Y

CD

S, 4

5.1

3

10

Y C

DS

, 9

4.7

55

10

Y C

DS

, 8

4.8

4

0

10

20

30

40

50

60

70

80

90

100

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 87.84

End of Q2 91.4

Change on Quarter (%) 4.05%

Bloomberg Ticker: invp ln equity Bloomberg Ticker: jpm us equity

Credit Default Swap (5Y)

End of Q1 55.015

End of Q2 45.13

Change on Quarter (%) -17.97%

Bloomberg Ticker: JPMCC CDS USD SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A-

Date Rating Effective 02/12/15

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating A3

Date Rating Effective 14/11/13

Ratings Outlook STABLE

Date Outlook Effective 14/11/13

Credit Rating (Fitch)

Long Term Issuer Default Rating A+

Date Rating Effective 10/10/12

Ratings Outlook STABLE

Date Outlook Effective 10/10/12

Bloomberg Ticker: 4429z ln equity Bloomberg Ticker: jpm us equity

Capita l

Tier One Capital Ratio 14.2%

Market Cap (GBP millions)* 248,410

Bloomberg Ticker: invp ln equity Bloomberg Ticker: jpm us equity

*Converted from quoted currency based on prevailing exchange rate as of source date

24

Innovative Solutions. Immaculate Service.

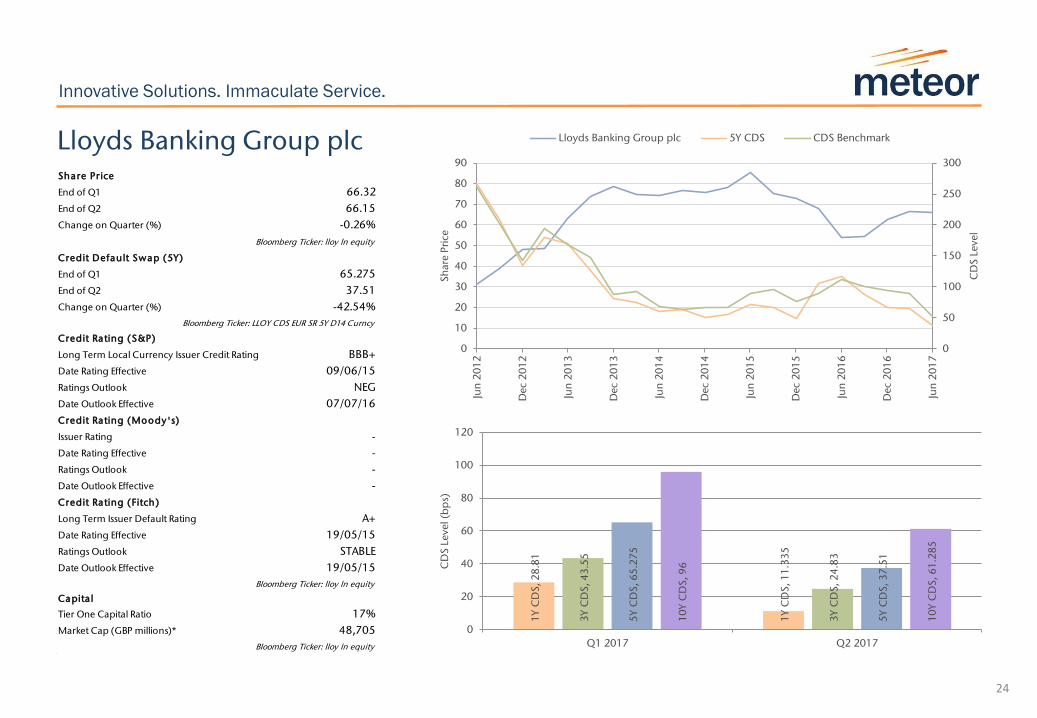

Lloyds Banking Group plc

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

90

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Lloyds Banking Group plc 5Y CDS CDS Benchmark

1Y

CD

S, 2

8.8

1

1Y

CD

S, 1

1.3

35

3Y

CD

S, 4

3.5

5

3Y

CD

S, 2

4.8

3

5Y

CD

S, 6

5.2

75

5Y

CD

S, 3

7.5

1

10

Y C

DS

, 9

6

10

Y C

DS

, 6

1.2

85

0

20

40

60

80

100

120

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 66.32

End of Q2 66.15

Change on Quarter (%) -0.26%

Bloomberg Ticker: jpm us equity Bloomberg Ticker: lloy ln equity

Credit Default Swap (5Y)

End of Q1 65.275

End of Q2 37.51

Change on Quarter (%) -42.54%

Bloomberg Ticker: JPMCC CDS USD SR 5Y D14 Curncy Bloomberg Ticker: LLOY CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating BBB+

Date Rating Effective 09/06/15

Ratings Outlook NEG

Date Outlook Effective 07/07/16

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating A+

Date Rating Effective 19/05/15

Ratings Outlook STABLE

Date Outlook Effective 19/05/15

Bloomberg Ticker: jpm us equity Bloomberg Ticker: lloy ln equity

Capita l

Tier One Capital Ratio 17%

Market Cap (GBP millions)* 48,705

Bloomberg Ticker: jpm us equity Bloomberg Ticker: lloy ln equity

25

Innovative Solutions. Immaculate Service.

Macquarie Bank Ltd

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

90

100

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Macquarie Bank Ltd 5Y CDS CDS Benchmark

1Y

CD

S, 6

.73

1Y

CD

S, 6

.78

5

3Y

CD

S, 3

5.1

15

3Y

CD

S, 3

4.5

8

5Y

CD

S, 7

6.2

4

5Y

CD

S, 7

4.6

10

Y C

DS

, 1

14

.85

10

Y C

DS

, 1

12

.37

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 90.2

End of Q2 88.5

Change on Quarter (%) -1.88%

Bloomberg Ticker: lloy ln equity Bloomberg Ticker: mqg au equity

Credit Default Swap (5Y)

End of Q1 76.24

End of Q2 74.6

Change on Quarter (%) -2.15%

Bloomberg Ticker: LLOY CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: MBL CDS USD SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 15/11/94

Ratings Outlook NEG

Date Outlook Effective 30/10/16

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 12/03/12

Ratings Outlook STABLE

Date Outlook Effective 12/03/12

Bloomberg Ticker: lloy ln equity Bloomberg Ticker: 2292186Z AU equity

Capita l

Tier One Capital Ratio 13.3%

Market Cap (GBP millions)* 18,130

Bloomberg Ticker: lloy ln equity Bloomberg Ticker: mqg au equity

*Converted from quoted currency based on prevailing exchange rate as of source date

26

Innovative Solutions. Immaculate Service.

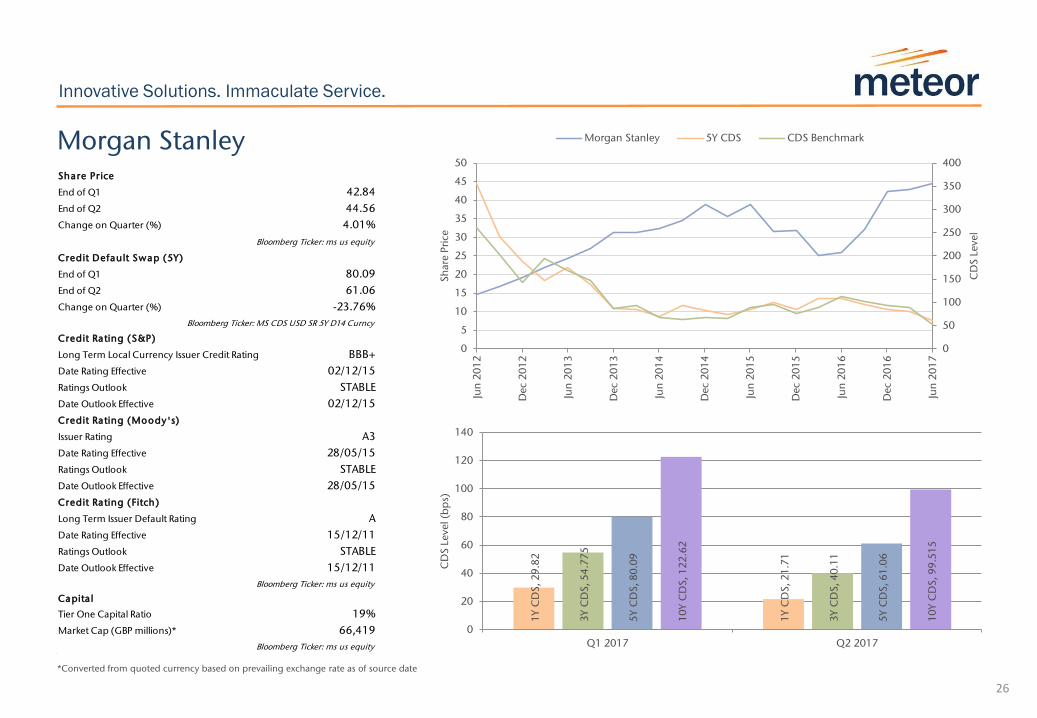

Morgan Stanley

0

50

100

150

200

250

300

350

400

0

5

10

15

20

25

30

35

40

45

50

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Morgan Stanley 5Y CDS CDS Benchmark

1Y

CD

S, 2

9.8

2

1Y

CD

S, 2

1.7

1

3Y

CD

S, 5

4.7

75

3Y

CD

S, 4

0.1

1

5Y

CD

S, 8

0.0

9

5Y

CD

S, 6

1.0

6

10

Y C

DS

, 1

22

.62

10

Y C

DS

, 9

9.5

15

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 42.84

End of Q2 44.56

Change on Quarter (%) 4.01%

Bloomberg Ticker: mqg au equity Bloomberg Ticker: ms us equity

Credit Default Swap (5Y)

End of Q1 80.09

End of Q2 61.06

Change on Quarter (%) -23.76%

Bloomberg Ticker: MBL CDS USD SR 5Y D14 Curncy Bloomberg Ticker: MS CDS USD SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating BBB+

Date Rating Effective 02/12/15

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating A3

Date Rating Effective 28/05/15

Ratings Outlook STABLE

Date Outlook Effective 28/05/15

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 15/12/11

Ratings Outlook STABLE

Date Outlook Effective 15/12/11

Bloomberg Ticker: 2292186Z AU equity Bloomberg Ticker: ms us equity

Capita l

Tier One Capital Ratio 19%

Market Cap (GBP millions)* 66,419

Bloomberg Ticker: mqg au equity Bloomberg Ticker: ms us equity

*Converted from quoted currency based on prevailing exchange rate as of source date

27

Innovative Solutions. Immaculate Service.

Natixis

0

50

100

150

200

250

300

0

1

2

3

4

5

6

7

8

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Natixis 5Y CDS CDS Benchmark

1Y

CD

S, 2

1.2

4

1Y

CD

S, 1

5.3

45

3Y

CD

S, 5

4.2

45

3Y

CD

S, 2

8.5

3

5Y

CD

S, 8

5.6

5

5Y

CD

S, 4

1.1

9

10

Y C

DS

, 1

25

.94

5

10

Y C

DS

, 6

5.6

05

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 5.776

End of Q2 5.877

Change on Quarter (%) 1.75%

Bloomberg Ticker: ms us equity Bloomberg Ticker: kn fp equity

Credit Default Swap (5Y)

End of Q1 85.65

End of Q2 41.19

Change on Quarter (%) -51.91%

Bloomberg Ticker: MS CDS USD SR 5Y D14 Curncy Bloomberg Ticker: KNFP CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 23/01/12

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating A2

Date Rating Effective 15/06/12

Ratings Outlook POS

Date Outlook Effective 26/07/17

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 17/07/13

Ratings Outlook STABLE

Date Outlook Effective 17/07/13

Bloomberg Ticker: ms us equity Bloomberg Ticker: kn fp equity

Capita l

Tier One Capital Ratio 12.3%

Market Cap (GBP millions)* 17,303

Bloomberg Ticker: ms us equity Bloomberg Ticker: kn fp equity

*Converted from quoted currency based on prevailing exchange rate as of source date

28

Innovative Solutions. Immaculate Service.

Nomura Bank International

0

50

100

150

200

250

300

350

400

0

100

200

300

400

500

600

700

800

900

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Nomura Bank International plc 5Y CDS CDS Benchmark

1Y

CD

S, 9

.17

5

1Y

CD

S, 1

2.2

05

3Y

CD

S, 2

4.4

7

3Y

CD

S, 2

4.5

75

5Y

CD

S, 4

3.2

85

5Y

CD

S, 4

1.0

6

10

Y C

DS

, 6

6.5

5

10

Y C

DS

, 6

1.9

5

0

10

20

30

40

50

60

70

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 691.9

End of Q2 673.4

Change on Quarter (%) -2.67%

Bloomberg Ticker: kn fp equity Bloomberg Ticker: 8604 jt equity

Credit Default Swap (5Y)

End of Q1 43.285

End of Q2 41.06

Change on Quarter (%) -5.14%

Bloomberg Ticker: KNFP CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: NOMURAH CDS JPY SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 17/11/16

Ratings Outlook NEG

Date Outlook Effective 17/11/16

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Bloomberg Ticker: kn fp equity Bloomberg Ticker: 146481Z LN Equity

Capita l

Tier One Capital Ratio 19.2%

Market Cap (GBP millions)* 17,225

Bloomberg Ticker: kn fp equity Bloomberg Ticker: 8604 jt equity

*Converted from quoted currency based on prevailing exchange rate as of source date

29

Innovative Solutions. Immaculate Service.

NORTHERN TRUST CORP

0

50

100

150

200

250

300

0

20

40

60

80

100

120

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

NORTHERN TRUST CORP 5Y CDS CDS Benchmark

Share Pr ice

End of Q1 86.58

End of Q2 97.21

Change on Quarter (%) 12.28%

Bloomberg Ticker: 8604 jt equity Bloomberg Ticker: ntrs us equity

Credit Default Swap (5Y)

End of Q1 -

End of Q2 -

Change on Quarter (%) -

Bloomberg Ticker: NOMURAH CDS JPY SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A+

Date Rating Effective 06/12/11

Ratings Outlook STABLE

Date Outlook Effective 06/12/11

Credit Rating (Moody's)

Issuer Rating A2

Date Rating Effective 14/11/13

Ratings Outlook STABLE

Date Outlook Effective 14/05/15

Credit Rating (Fitch)

Long Term Issuer Default Rating AA-

Date Rating Effective 28/04/09

Ratings Outlook STABLE

Date Outlook Effective 29/09/10

Bloomberg Ticker: 146481Z LN Equity Bloomberg Ticker: ntrs us equity

Capita l

Tier One Capital Ratio 13.7%

Market Cap (GBP millions)* 15,275

Bloomberg Ticker: 8604 jt equity Bloomberg Ticker: ntrs us equity

*Converted from quoted currency based on prevailing exchange rate as of source date

30

Innovative Solutions. Immaculate Service.

Rabobank

0

50

100

150

200

250

300

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Rabobank 5Y CDS CDS Benchmark

1Y

CD

S, 2

4.3

65

1Y

CD

S, 7

.88

3Y

CD

S, 3

9.1

55

3Y

CD

S, 1

9.2

5

5Y

CD

S, 6

0.2

75

5Y

CD

S, 2

9.6

9

10

Y C

DS

, 8

8.8

15

10

Y C

DS

, 5

3.0

35

0

10

20

30

40

50

60

70

80

90

100

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 -

End of Q2 -

Change on Quarter (%) -

Bloomberg Ticker: ntrs us equity

Credit Default Swap (5Y)

End of Q1 60.275

End of Q2 29.69

Change on Quarter (%) -50.74%

Bloomberg Ticker: RABOBK CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A+

Date Rating Effective 04/11/14

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating Aa2

Date Rating Effective 28/05/15

Ratings Outlook NEG

Date Outlook Effective 24/11/16

Credit Rating (Fitch)

Long Term Issuer Default Rating AA-

Date Rating Effective 21/11/13

Ratings Outlook STABLE

Date Outlook Effective 09/06/15

Bloomberg Ticker: ntrs us equity Bloomberg Ticker: rabo na equity

Capita l

Tier One Capital Ratio 17.6%

Market Cap (GBP millions)* -

Bloomberg Ticker: ntrs us equity Bloomberg Ticker: rabo na equity

31

Innovative Solutions. Immaculate Service.

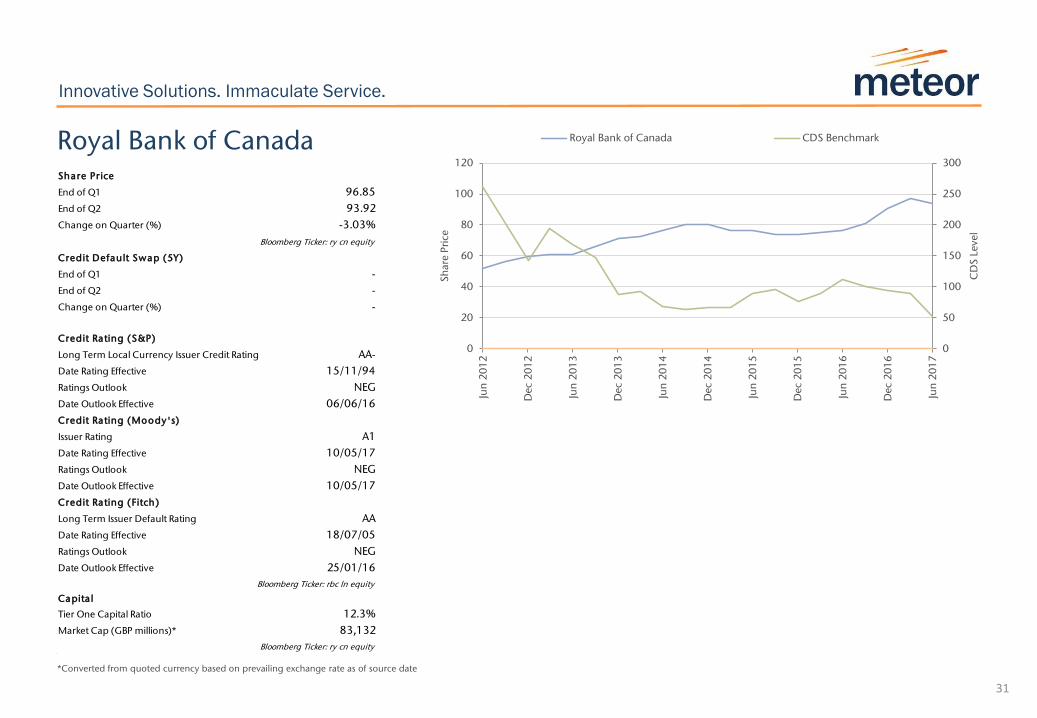

Royal Bank of Canada

0

50

100

150

200

250

300

0

20

40

60

80

100

120

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Royal Bank of Canada 5Y CDS CDS Benchmark

Share Pr ice

End of Q1 96.85

End of Q2 93.92

Change on Quarter (%) -3.03%

Bloomberg Ticker: ry cn equity

Credit Default Swap (5Y)

End of Q1 -

End of Q2 -

Change on Quarter (%) -

Bloomberg Ticker: RABOBK CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating AA-

Date Rating Effective 15/11/94

Ratings Outlook NEG

Date Outlook Effective 06/06/16

Credit Rating (Moody's)

Issuer Rating A1

Date Rating Effective 10/05/17

Ratings Outlook NEG

Date Outlook Effective 10/05/17

Credit Rating (Fitch)

Long Term Issuer Default Rating AA

Date Rating Effective 18/07/05

Ratings Outlook NEG

Date Outlook Effective 25/01/16

Bloomberg Ticker: rabo na equity Bloomberg Ticker: rbc ln equity

Capita l

Tier One Capital Ratio 12.3%

Market Cap (GBP millions)* 83,132

Bloomberg Ticker: rabo na equity Bloomberg Ticker: ry cn equity

*Converted from quoted currency based on prevailing exchange rate as of source date

32

Innovative Solutions. Immaculate Service.

Santander UK plc

0

50

100

150

200

250

300

350

0

1

2

3

4

5

6

7

8

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Santander UK plc 5Y CDS CDS Benchmark

1Y

CD

S, 3

7.0

35

1Y

CD

S, 2

0.0

5

3Y

CD

S, 5

8.7

85

3Y

CD

S, 3

5.5

2

5Y

CD

S, 7

8.5

6

5Y

CD

S, 4

9.1

10

Y C

DS

, 1

03

.48

5

10

Y C

DS

, 6

9.5

6

0

20

40

60

80

100

120

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 5.6505

End of Q2 5.6968

Change on Quarter (%) 0.82%

Bloomberg Ticker: ry cn equity Bloomberg Ticker: san sm equity

Credit Default Swap (5Y)

End of Q1 78.56

End of Q2 49.1

Change on Quarter (%) -37.50%

Bloomberg Ticker: SANTUK CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 09/06/15

Ratings Outlook NEG

Date Outlook Effective 07/07/16

Credit Rating (Moody's)

Issuer Rating Aa3

Date Rating Effective 21/12/16

Ratings Outlook NEG

Date Outlook Effective 21/12/16

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 11/06/12

Ratings Outlook STABLE

Date Outlook Effective 07/02/17

Bloomberg Ticker: rbc ln equity Bloomberg Ticker: anl ln equity

Capita l

Tier One Capital Ratio 12.53%

Market Cap (GBP millions)* 76,217

Bloomberg Ticker: ry cn equity Bloomberg Ticker: san sm equity

*Converted from quoted currency based on prevailing exchange rate as of source date

33

Innovative Solutions. Immaculate Service.

Société Générale

0

50

100

150

200

250

300

350

0

5

10

15

20

25

30

35

40

45

50

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Societe Generale 5Y CDS CDS Benchmark

1Y

CD

S, 3

5.2

3

1Y

CD

S, 1

1.2

6

3Y

CD

S, 6

2.1

8

3Y

CD

S, 2

2.8

4

5Y

CD

S, 8

9.9

3

5Y

CD

S, 3

7.2

4

10

Y C

DS

, 1

25

.68

10

Y C

DS

, 6

8.6

85

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 47.55

End of Q2 47.11

Change on Quarter (%) -0.93%

Bloomberg Ticker: san sm equity Bloomberg Ticker: gle fp equity

Credit Default Swap (5Y)

End of Q1 89.93

End of Q2 37.24

Change on Quarter (%) -58.59%

Bloomberg Ticker: SANTUK CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: SOCGEN CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating A

Date Rating Effective 23/01/12

Ratings Outlook STABLE

Date Outlook Effective 02/12/15

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating A

Date Rating Effective 17/07/13

Ratings Outlook STABLE

Date Outlook Effective 19/05/15

Bloomberg Ticker: anl ln equity Bloomberg Ticker: gle fp equity

Capita l

Tier One Capital Ratio 14.5%

Market Cap (GBP millions)* 36,001

Bloomberg Ticker: san sm equity Bloomberg Ticker: gle fp equity

*Converted from quoted currency based on prevailing exchange rate as of source date

34

Innovative Solutions. Immaculate Service.

Standard Chartered plc

0

50

100

150

200

250

300

0

200

400

600

800

1000

1200

1400

1600

1800

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

Standard Chartered plc 5Y CDS CDS Benchmark

1Y

CD

S, 2

2.5

25

1Y

CD

S, 1

1.0

35

3Y

CD

S, 5

0.2

1

3Y

CD

S, 2

5.3

05

5Y

CD

S, 7

9.5

8

5Y

CD

S, 4

0.4

95

10

Y C

DS

, 1

09

.96

5

10

Y C

DS

, 6

2.6

65

0

20

40

60

80

100

120

Q1 2017 Q2 2017

CD

S L

evel (b

ps)

Share Pr ice

End of Q1 763

End of Q2 777.2

Change on Quarter (%) 1.86%

Bloomberg Ticker: gle fp equity Bloomberg Ticker: stan ln equity

Credit Default Swap (5Y)

End of Q1 79.58

End of Q2 40.495

Change on Quarter (%) -49.11%

Bloomberg Ticker: SOCGEN CDS EUR SR 5Y D14 Curncy Bloomberg Ticker: STANLN BK CDS EUR SR 5Y D14 Curncy

Credit Rating (S&P)

Long Term Local Currency Issuer Credit Rating BBB+

Date Rating Effective 31/03/16

Ratings Outlook STABLE

Date Outlook Effective 31/03/16

Credit Rating (Moody's)

Issuer Rating -

Date Rating Effective -

Ratings Outlook -

Date Outlook Effective -

Credit Rating (Fitch)

Long Term Issuer Default Rating A+

Date Rating Effective 05/11/15

Ratings Outlook STABLE

Date Outlook Effective 14/10/16

Bloomberg Ticker: gle fp equity Bloomberg Ticker: stan ln equity

Capita l

Tier One Capital Ratio 15.7%

Market Cap (GBP millions)* 27,490

Bloomberg Ticker: gle fp equity Bloomberg Ticker: stan ln equity

*Converted from quoted currency based on prevailing exchange rate as of source date

35

Innovative Solutions. Immaculate Service.

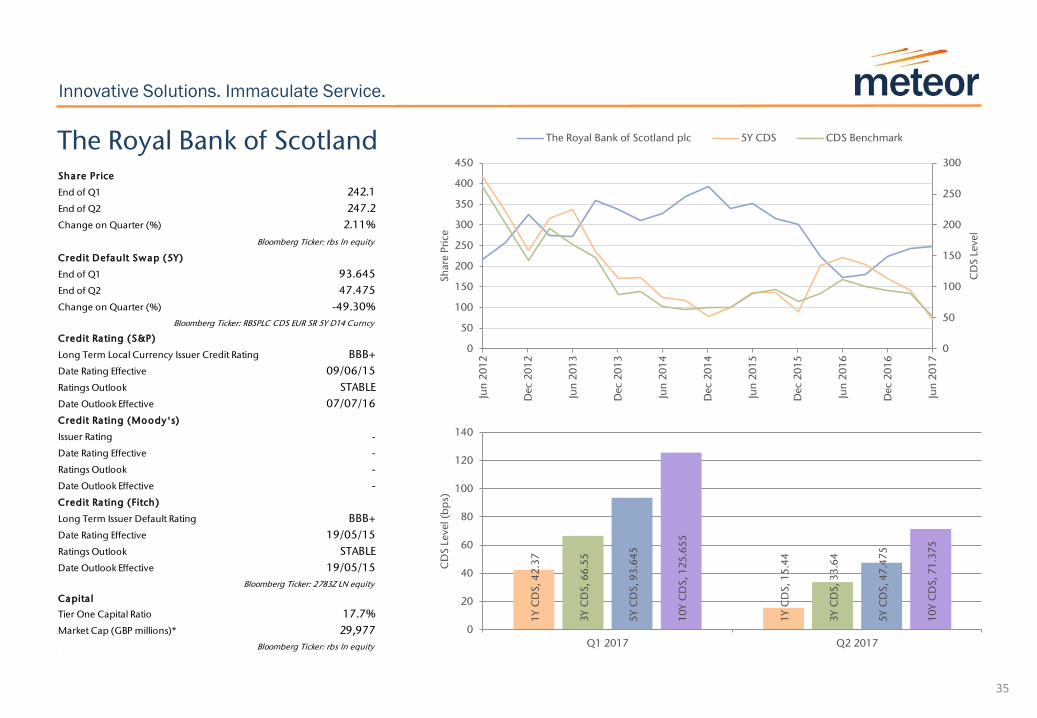

The Royal Bank of Scotland

0

50

100

150

200

250

300

0

50

100

150

200

250

300

350

400

450

Jun

20

12

Dec

20

12

Jun

20

13

Dec

20

13

Jun

20

14

Dec

20

14

Jun

20

15

Dec

20

15

Jun

20

16

Dec

20

16

Jun

20

17

CD

S L

evel

Sh

are

Pri

ce

The Royal Bank of Scotland plc 5Y CDS CDS Benchmark

1Y

CD

S, 4

2.3

7

1Y

CD

S, 1

5.4

4

3Y

CD

S, 6

6.5

5

3Y

CD

S, 3

3.6

4

5Y