Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

i

NORTH-WEST UNIVERSITY POTCHEFSTROOM CAMPUS PRIVATE BAG X6001 POTCHEFSTROOM 2520

Tel +27 18 299 1810 Fax +27 18 299 4140

E-mail: [email protected]

Dr Martinette Kruger, Mr Marco Scholtz, Prof Melville Saayman & Prof Andrea Saayman

Copyright © 2012 Tourism Research in Economic Environs & Society

ii

Acknowledgements

The authors would like to thank the following individuals and institutions:

Ms Sandra Jacobs of Innibos management for her help in providing us with

quality information and support.

All the festinos for their participation and cooperation in completing the

questionnaires.

The NRF for co-funding.

Philna Scholtz for organising accommodation for the fieldworkers.

Ms S Oberholzer for managing the collation of the data.

The following students from the North-West University for the distribution of the

questionnaires:

Ms D Venter

Ms N Jacobs

Ms M Benade

Ms B Niemand

Ms B Swanepoel

Ms Cecile van Zyl for the language editing.

iii

Table of contents 1. INTRODUCTION 1 2. RESEARCH AIM 1 3. METHOD OF RESEARCH 3 4. PROFILE OF VISITORS TO INNIBOS ARTS FESTIVAL 4 4.1 Gender 4

4.2 Age groups 5

4.3 Language 6 4.4

4.5

Occupation

Annual gross income

6

6

4.6 Province of residence 7

4.7 Number of people in travelling group 8 4.8 Number of people paid for 9

4.9 Days spent at the Festival 9

4.10 Nights in Nelspruit 10 4.11 Type of accommodation 10

4.12 Expenditure per group 12

4.13 Number of tickets purchased for shows 13

4.14 Preferred type of shows 14 4.15 Festival as main reason for visit to Nelspruit 14

4.16 Other festivals attended 15

4.17

4.17.1 4.17.2

Decisions to attend Festival

Type of decision Initiator of trip

16

16 16

4.18 Sponsors associated with Innibos 17

4.19 Number of visits to the Festival 18

4.20 Motivation to attend the Festival 18 4.21 Types of media 19

4.22 Repeat visits to Festival 20

4.23 Factors that classify national arts festivals 21

4.24 Degree of exposure to the arts during childhood 23 4.25 Perception of Innibos’ contribution to the arts 24

4.25.1 Innibos’ contribution to the arts 24

4.25.2 Perceptions of Innibos’ contribution to the arts 28

4.25.3 Personal involvement in the arts 29

iv

List of figures

5. ECONOMIC CONTRIBUTION 30

5.1 The number of visitors and length of stay 30

5.2 The magnitude of spending 31

5.3 Economic contribution 31

6. CONCLUSIONS AND RECOMMENDATIONS 34

6.1 Profile of visitors 34

6 6.1 6.2 6.3

CONCLUSIONS AND RECOMMENDATIONS Profile of the visitors Conclusions Recommendations

25 25 26 27

Figure 1: Gender 4 Figure 2: Figure 3:

Occupation Annual gross income

6 7

Figure 4: Festival as main reason for visit to Nelspruit 15 Figure 5: Other festivals attended 15 Figure 6: Figure 7:

Decision to attend Festival Initiator of attendance

16 17

Figure 8: Repeat visits to Festival 21 Figure 9: Exposure 23

v

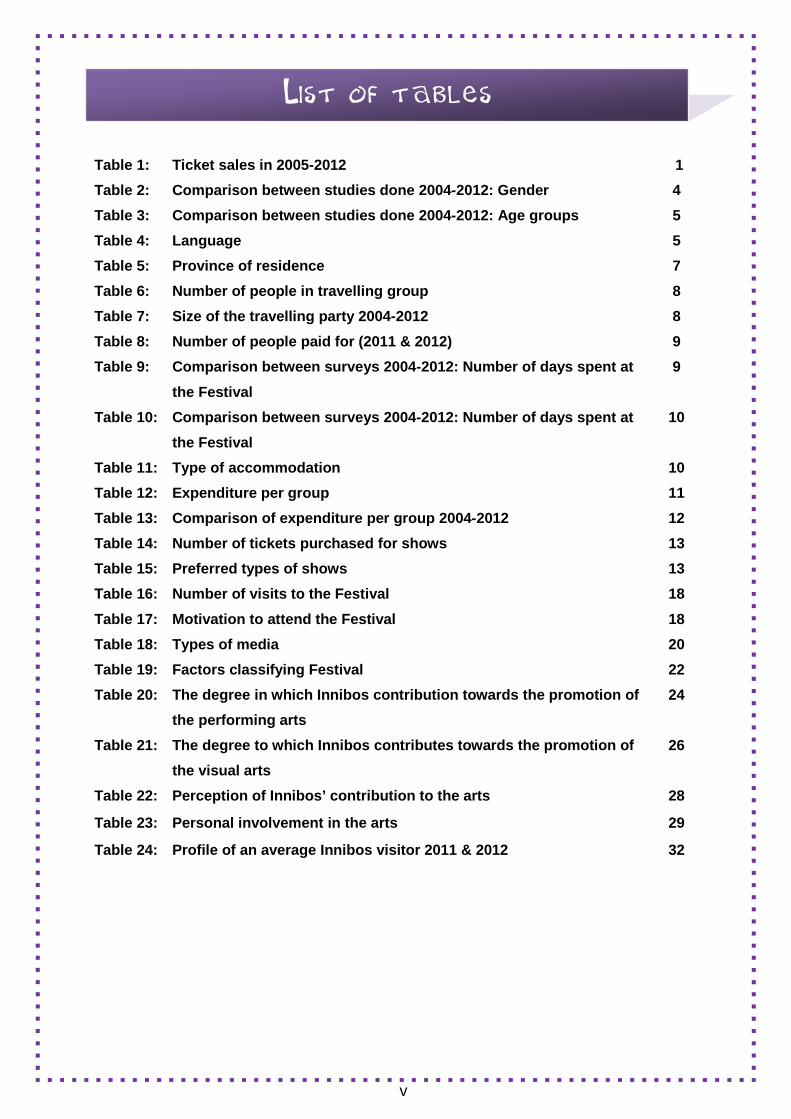

List of tables

Table 1: Ticket sales in 2005-2012 1 Table 2: Comparison between studies done 2004-2012: Gender 4 Table 3: Comparison between studies done 2004-2012: Age groups 5 Table 4: Language 5 Table 5: Province of residence 7 Table 6: Number of people in travelling group 8 Table 7: Size of the travelling party 2004-2012 8 Table 8: Number of people paid for (2011 & 2012) 9 Table 9: Comparison between surveys 2004-2012: Number of days spent at

the Festival 9

Table 10: Comparison between surveys 2004-2012: Number of days spent at the Festival

10

Table 11: Type of accommodation 10 Table 12: Expenditure per group 11 Table 13: Comparison of expenditure per group 2004-2012 12 Table 14: Number of tickets purchased for shows 13 Table 15: Preferred types of shows 13 Table 16: Number of visits to the Festival 18 Table 17: Motivation to attend the Festival 18 Table 18: Types of media 20 Table 19: Factors classifying Festival 22 Table 20: The degree in which Innibos contribution towards the promotion of

the performing arts 24

Table 21:

The degree to which Innibos contributes towards the promotion of the visual arts

26

Table 22: Perception of Innibos’ contribution to the arts 28

Table 23: Personal involvement in the arts 29

Table 24: Profile of an average Innibos visitor 2011 & 2012 32

1

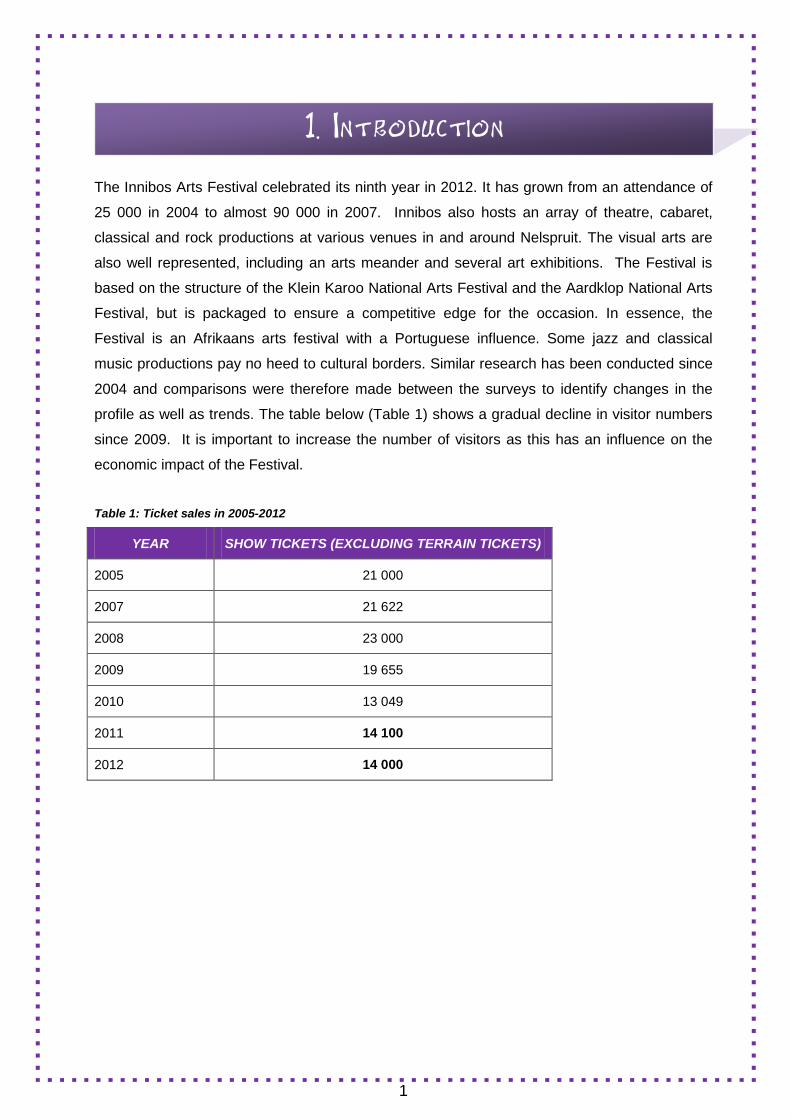

1. Introduction

The Innibos Arts Festival celebrated its ninth year in 2012. It has grown from an attendance of

25 000 in 2004 to almost 90 000 in 2007. Innibos also hosts an array of theatre, cabaret,

classical and rock productions at various venues in and around Nelspruit. The visual arts are

also well represented, including an arts meander and several art exhibitions. The Festival is

based on the structure of the Klein Karoo National Arts Festival and the Aardklop National Arts

Festival, but is packaged to ensure a competitive edge for the occasion. In essence, the

Festival is an Afrikaans arts festival with a Portuguese influence. Some jazz and classical

music productions pay no heed to cultural borders. Similar research has been conducted since

2004 and comparisons were therefore made between the surveys to identify changes in the

profile as well as trends. The table below (Table 1) shows a gradual decline in visitor numbers

since 2009. It is important to increase the number of visitors as this has an influence on the

economic impact of the Festival.

Table 1: Ticket sales in 2005-2012

YEAR SHOW TICKETS (EXCLUDING TERRAIN TICKETS)

2005 21 000

2007 21 622

2008 23 000

2009 19 655

2010 13 049

2011 14 100

2012 14 000

2

2. Research aim

Arts festivals have become important in the South African society because of a growing need

among the broader public for various forms of art. These festivals in general are important for

many reasons, some of which are:

to sustain different forms of art;

to contribute to the livelihood of artists;

to grow regional and local economies;

to promote specific destinations; and

to create specific images of these destinations.

Continuous growth of festivals in South Africa is ensured as government supports and

promotes them as part of its strategy for economic development. However, the sustainability of

the festivals has become questionable as many of these festivals compete for similar tourism

markets. Does the same group of people attend one festival after another, or is it a different

group of people attending different festivals? These are the questions that contributed to this

survey and needed answering. This survey is one in a series that was undertaken by Tourism

Research in Economic Environs and Society (TREES) at the North-West University. As

mentioned above, it has become important to unlock information pertaining to the profile of

festinos, as well as the impact of the Festival on the economy of Nelspruit and the Mbombela

Area. This information can contribute to the sustainability of the Festival, especially in terms of

its marketing value. The profile can help organisers focus on a specific market instead of using

a shotgun approach.

This research focused on the following objectives:

To determine the profile of visitors/tourists to Innibos Arts Festival:

o Who visits the Festival?

o Where do the visitors come from?

o How much money is spent at the Festival?

o What is the size of the travel group?

o In which activities do visitors participate and what is the frequency of

participation?

To determine the economic value of the Festival for Nelspruit:

o What are the spending patterns of the visitors?

3

3. Method of research

In order to determine the profile of festinos as well as the economic impact of Innibos Arts

Festival, a questionnaire was used. In total, 471 questionnaires were completed by means of

availability sampling over three days of the Festival (27 to 30 June 2012). Questionnaires were

distributed among the different venues and main festival grounds to ensure that all festinos had

an equal opportunity to participate. Questionnaires were also completed at the main festival

grounds and venues where fieldworkers moved around in order to minimise bias. During the

survey, fieldworkers approached the respondents and explained the goal of the survey as well

as the questionnaire. Hereafter the profile of the visitors to the Festival will be discussed.

4

4. Profile of visitors to the Innibos Arts Festival

This section focuses on analysing the profile of visitors to Innibos Arts Festival. The profile can

be useful in determining marketing strategies and programme planning.

DEMOGRAPHIC PROFILE

4.1 Gender

Figure 1: Gender

According to Figure 1, 64% of respondents were female, while 36% were male. This

corresponds well with previous surveys where females were also the majority (Table 2).

Table 2: Comparison between studies done 2004-2012: Gender

GENDER 2004 2005 2006 2007 2008 2009 2010 2011 2012

Male 48% 41% 41% 45% 35% 40% 37% 42% 36%

Female 52% 59% 59% 55% 65% 60% 63% 58% 64%

36%

64%

Male Female

5

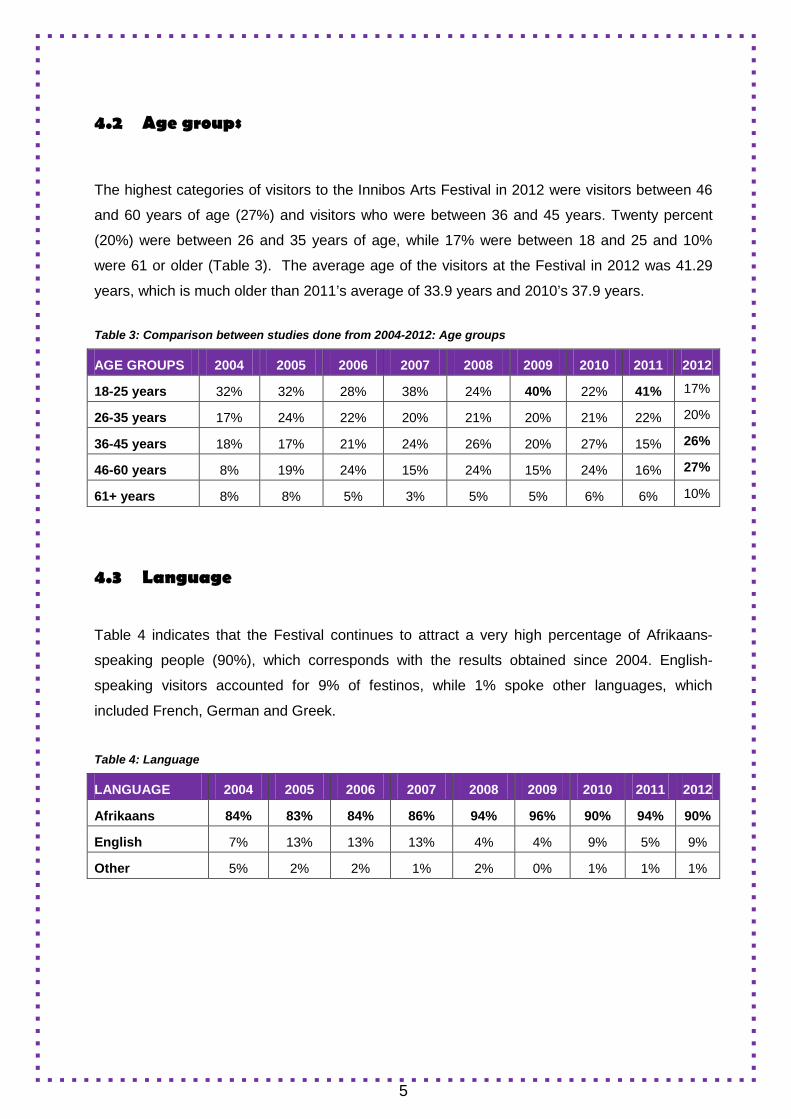

4.2 Age groups

The highest categories of visitors to the Innibos Arts Festival in 2012 were visitors between 46

and 60 years of age (27%) and visitors who were between 36 and 45 years. Twenty percent

(20%) were between 26 and 35 years of age, while 17% were between 18 and 25 and 10%

were 61 or older (Table 3). The average age of the visitors at the Festival in 2012 was 41.29

years, which is much older than 2011’s average of 33.9 years and 2010’s 37.9 years. Table 3: Comparison between studies done from 2004-2012: Age groups

AGE GROUPS 2004 2005 2006 2007 2008 2009 2010 2011 2012

18-25 years 32% 32% 28% 38% 24% 40% 22% 41% 17%

26-35 years 17% 24% 22% 20% 21% 20% 21% 22% 20%

36-45 years 18% 17% 21% 24% 26% 20% 27% 15% 26%

46-60 years 8% 19% 24% 15% 24% 15% 24% 16% 27%

61+ years 8% 8% 5% 3% 5% 5% 6% 6% 10%

4.3 Language

Table 4 indicates that the Festival continues to attract a very high percentage of Afrikaans-

speaking people (90%), which corresponds with the results obtained since 2004. English-

speaking visitors accounted for 9% of festinos, while 1% spoke other languages, which

included French, German and Greek.

Table 4: Language

LANGUAGE 2004 2005 2006 2007 2008 2009 2010 2011 2012

Afrikaans 84% 83% 84% 86% 94% 96% 90% 94% 90%

English 7% 13% 13% 13% 4% 4% 9% 5% 9%

Other 5% 2% 2% 1% 2% 0% 1% 1% 1%

6

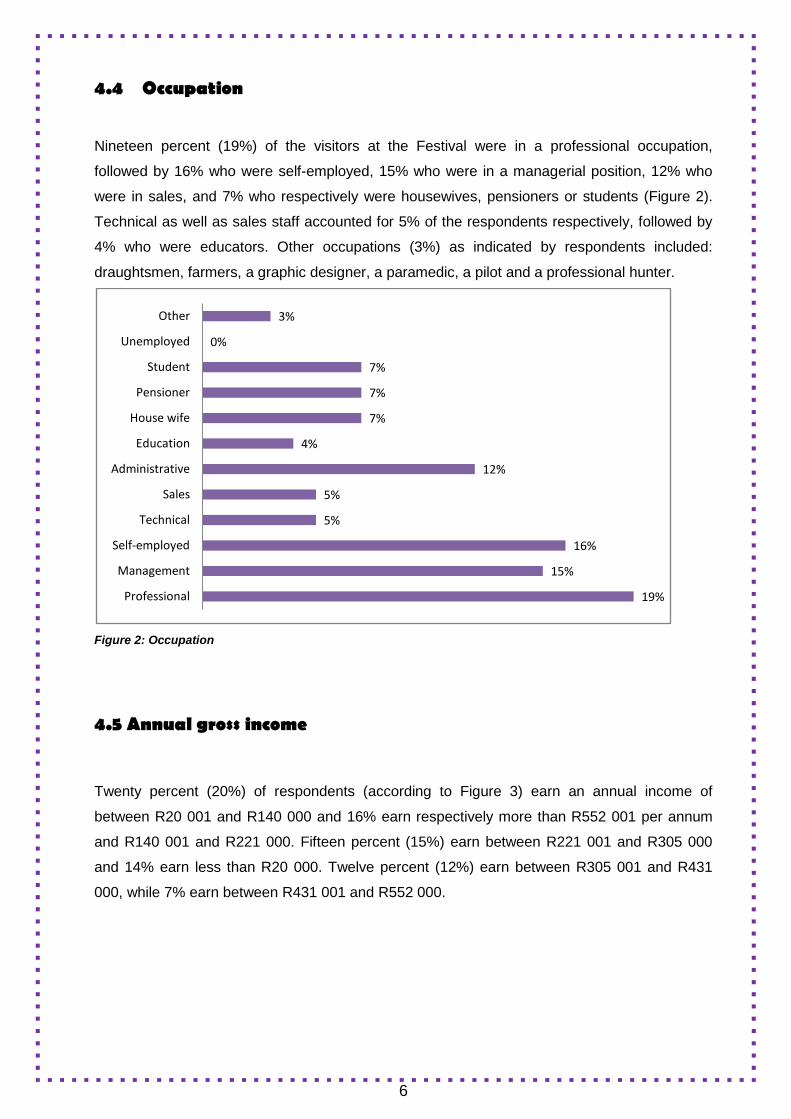

4.4 Occupation

Nineteen percent (19%) of the visitors at the Festival were in a professional occupation,

followed by 16% who were self-employed, 15% who were in a managerial position, 12% who

were in sales, and 7% who respectively were housewives, pensioners or students (Figure 2).

Technical as well as sales staff accounted for 5% of the respondents respectively, followed by

4% who were educators. Other occupations (3%) as indicated by respondents included:

draughtsmen, farmers, a graphic designer, a paramedic, a pilot and a professional hunter.

Figure 2: Occupation

4.5 Annual gross income

Twenty percent (20%) of respondents (according to Figure 3) earn an annual income of

between R20 001 and R140 000 and 16% earn respectively more than R552 001 per annum

and R140 001 and R221 000. Fifteen percent (15%) earn between R221 001 and R305 000

and 14% earn less than R20 000. Twelve percent (12%) earn between R305 001 and R431

000, while 7% earn between R431 001 and R552 000.

19%

15%

16%

5%

5%

12%

4%

7%

7%

7%

0%

3%

Professional

Management

Self-employed

Technical

Sales

Administrative

Education

House wife

Pensioner

Student

Unemployed

Other

7

Figure 3: Annual gross income

4.6 Province of residence

Forty-eight percent (48%) of the respondents were from Mpumalanga, with the second highest

number of visitors travelling from Gauteng (35%) (see Table 5). Five percent (5%) travelled

from the Limpopo Province, 4% from the North West Province and 3% from KwaZulu-Natal.

Respondents from the Free State and Western Cape accounted for 2% each, while only 1% of

respondents were from the Northern Cape. There were no respondents from the Eastern Cape.

Less than 1% was foreign visitors. When comparing the results with those from previous years,

Mpumalanga and Gauteng remain the Festival’s main target market.

Table 5: Province of residence

PROVINCE 2004 2005 2006 2007 2008 2009 2010 2011 2012

Mpumalanga 48% 56% 65% 67% 65% 53% 55% 43% 48%

Gauteng 31% 29% 24% 19% 26% 33% 30% 34% 35%

North West 6% 3% 2% 3% 2% 3% 3% 6% 4%

Free State 4% 2% 1% 3% 2% 3% 3% 3% 2%

KwaZulu-Natal 3.5% 2% 0.5% 2% 1% 2% 2% 6% 3%

Western Cape 3% 4% 2% 2% 1% 1% 1% 2% 2%

Limpopo 3% 3% 4% 2.5% 3% 3% 5% 5% 5%

Eastern Cape 0.6% 0.7% 0.8% 0.5% 0% 1% 0% 0% 0%

Northern Cape 0.3% 0.3% 0.5% 0.5% 0% 0% 0% 0% 1%

Outside RSA 0.6% 1% 0.2% 0.5% 0% 1% 1% 1% 0%

14%

20%

16%

15%

12%

7%

16%

<= R20 000

R20 001-R140 000

R140 001-R221 000

R221 001-R305 000

R305 001-R431 000

R431 001-R552 000

>= R552 001

8

ECONOMIC PROFILE

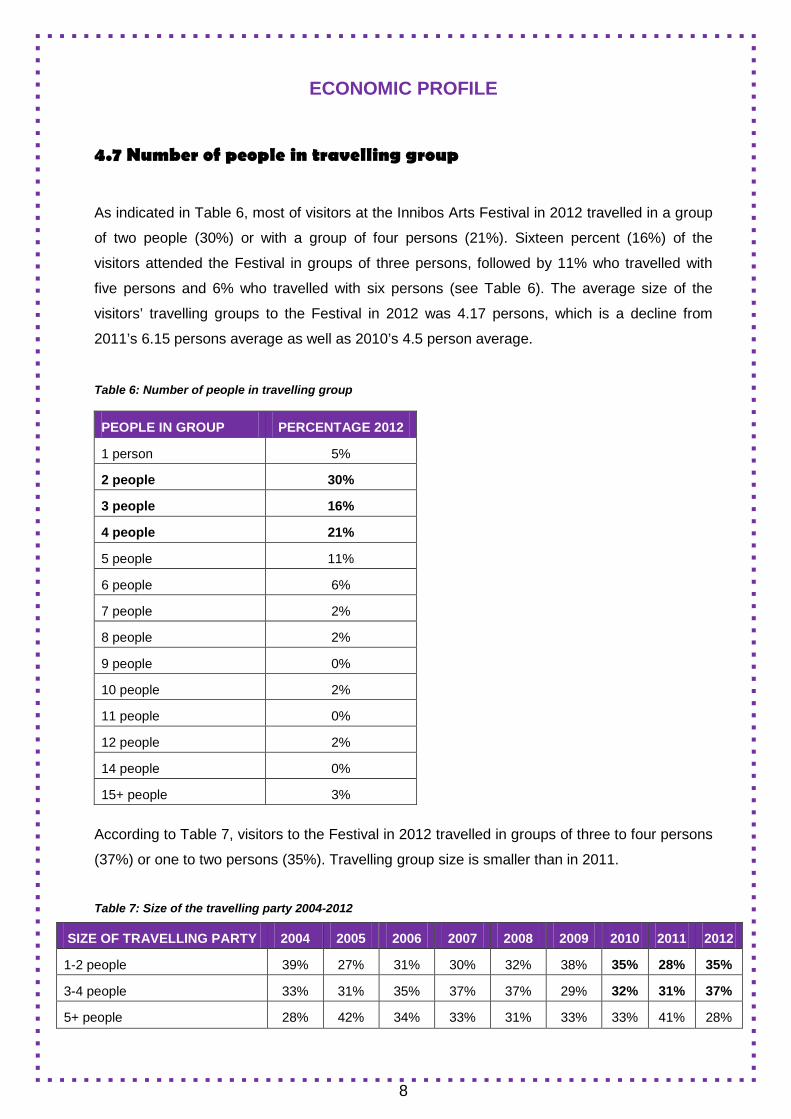

4.7 Number of people in travelling group

As indicated in Table 6, most of visitors at the Innibos Arts Festival in 2012 travelled in a group

of two people (30%) or with a group of four persons (21%). Sixteen percent (16%) of the

visitors attended the Festival in groups of three persons, followed by 11% who travelled with

five persons and 6% who travelled with six persons (see Table 6). The average size of the

visitors’ travelling groups to the Festival in 2012 was 4.17 persons, which is a decline from

2011’s 6.15 persons average as well as 2010’s 4.5 person average.

Table 6: Number of people in travelling group

According to Table 7, visitors to the Festival in 2012 travelled in groups of three to four persons

(37%) or one to two persons (35%). Travelling group size is smaller than in 2011.

Table 7: Size of the travelling party 2004-2012

SIZE OF TRAVELLING PARTY 2004 2005 2006 2007 2008 2009 2010 2011 2012

1-2 people 39% 27% 31% 30% 32% 38% 35% 28% 35%

3-4 people 33% 31% 35% 37% 37% 29% 32% 31% 37%

5+ people 28% 42% 34% 33% 31% 33% 33% 41% 28%

PEOPLE IN GROUP PERCENTAGE 2012

1 person 5%

2 people 30%

3 people 16%

4 people 21%

5 people 11%

6 people 6%

7 people 2%

8 people 2%

9 people 0%

10 people 2%

11 people 0%

12 people 2%

14 people 0%

15+ people 3%

9

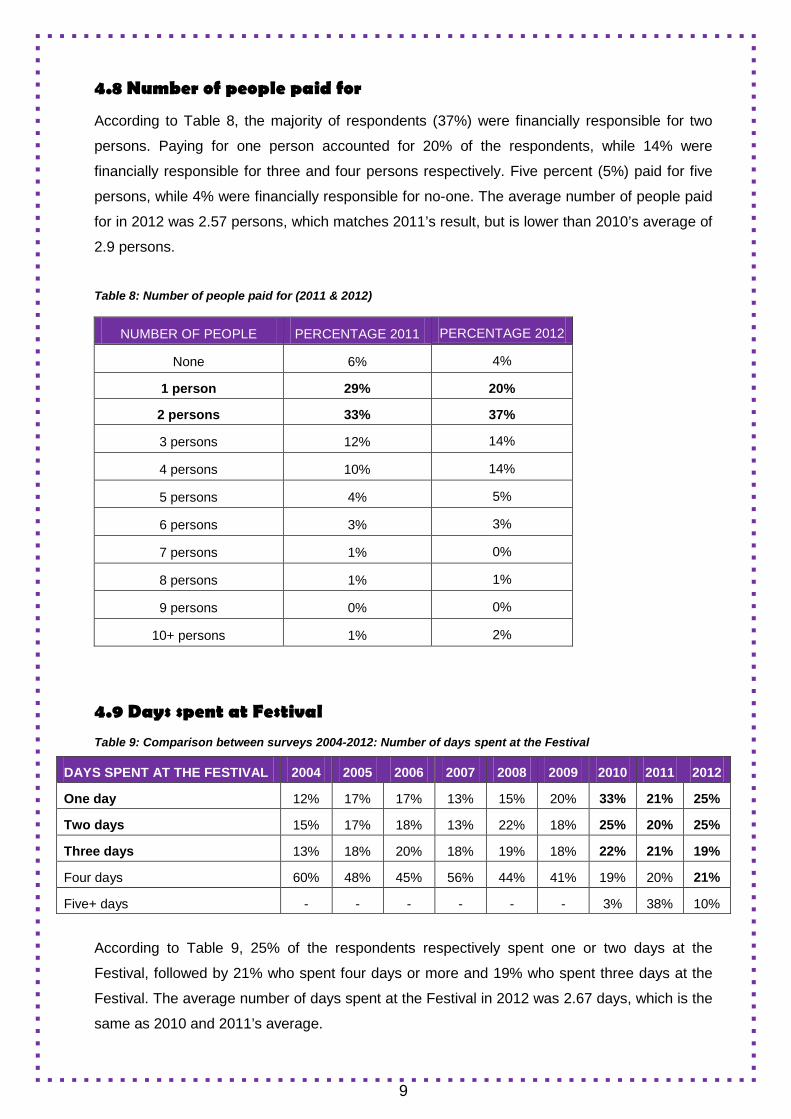

4.8 Number of people paid for

According to Table 8, the majority of respondents (37%) were financially responsible for two

persons. Paying for one person accounted for 20% of the respondents, while 14% were

financially responsible for three and four persons respectively. Five percent (5%) paid for five

persons, while 4% were financially responsible for no-one. The average number of people paid

for in 2012 was 2.57 persons, which matches 2011’s result, but is lower than 2010’s average of

2.9 persons.

Table 8: Number of people paid for (2011 & 2012)

4.9 Days spent at Festival Table 9: Comparison between surveys 2004-2012: Number of days spent at the Festival

DAYS SPENT AT THE FESTIVAL 2004 2005 2006 2007 2008 2009 2010 2011 2012

One day 12% 17% 17% 13% 15% 20% 33% 21% 25%

Two days 15% 17% 18% 13% 22% 18% 25% 20% 25%

Three days 13% 18% 20% 18% 19% 18% 22% 21% 19%

Four days 60% 48% 45% 56% 44% 41% 19% 20% 21%

Five+ days - - - - - - 3% 38% 10%

According to Table 9, 25% of the respondents respectively spent one or two days at the

Festival, followed by 21% who spent four days or more and 19% who spent three days at the

Festival. The average number of days spent at the Festival in 2012 was 2.67 days, which is the

same as 2010 and 2011’s average.

NUMBER OF PEOPLE PERCENTAGE 2011 PERCENTAGE 2012

None 6% 4%

1 person 29% 20%

2 persons 33% 37%

3 persons 12% 14%

4 persons 10% 14%

5 persons 4% 5%

6 persons 3% 3%

7 persons 1% 0%

8 persons 1% 1%

9 persons 0% 0%

10+ persons 1% 2%

10

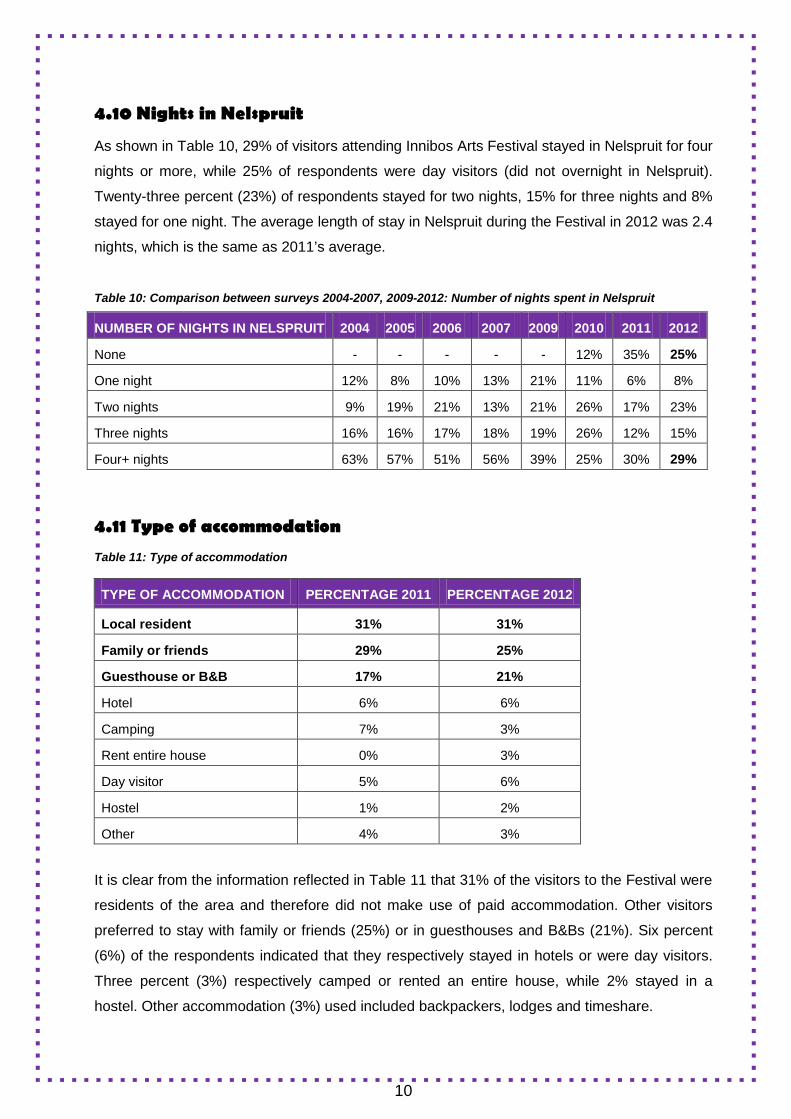

4.10 Nights in Nelspruit

As shown in Table 10, 29% of visitors attending Innibos Arts Festival stayed in Nelspruit for four

nights or more, while 25% of respondents were day visitors (did not overnight in Nelspruit).

Twenty-three percent (23%) of respondents stayed for two nights, 15% for three nights and 8%

stayed for one night. The average length of stay in Nelspruit during the Festival in 2012 was 2.4

nights, which is the same as 2011’s average.

Table 10: Comparison between surveys 2004-2007, 2009-2012: Number of nights spent in Nelspruit

NUMBER OF NIGHTS IN NELSPRUIT 2004 2005 2006 2007 2009 2010 2011 2012

None - - - - - 12% 35% 25%

One night 12% 8% 10% 13% 21% 11% 6% 8%

Two nights 9% 19% 21% 13% 21% 26% 17% 23%

Three nights 16% 16% 17% 18% 19% 26% 12% 15%

Four+ nights 63% 57% 51% 56% 39% 25% 30% 29%

4.11 Type of accommodation Table 11: Type of accommodation

It is clear from the information reflected in Table 11 that 31% of the visitors to the Festival were

residents of the area and therefore did not make use of paid accommodation. Other visitors

preferred to stay with family or friends (25%) or in guesthouses and B&Bs (21%). Six percent

(6%) of the respondents indicated that they respectively stayed in hotels or were day visitors.

Three percent (3%) respectively camped or rented an entire house, while 2% stayed in a

hostel. Other accommodation (3%) used included backpackers, lodges and timeshare.

TYPE OF ACCOMMODATION PERCENTAGE 2011 PERCENTAGE 2012

Local resident 31% 31%

Family or friends 29% 25%

Guesthouse or B&B 17% 21%

Hotel 6% 6%

Camping 7% 3%

Rent entire house 0% 3%

Day visitor 5% 6%

Hostel 1% 2%

Other 4% 3%

11

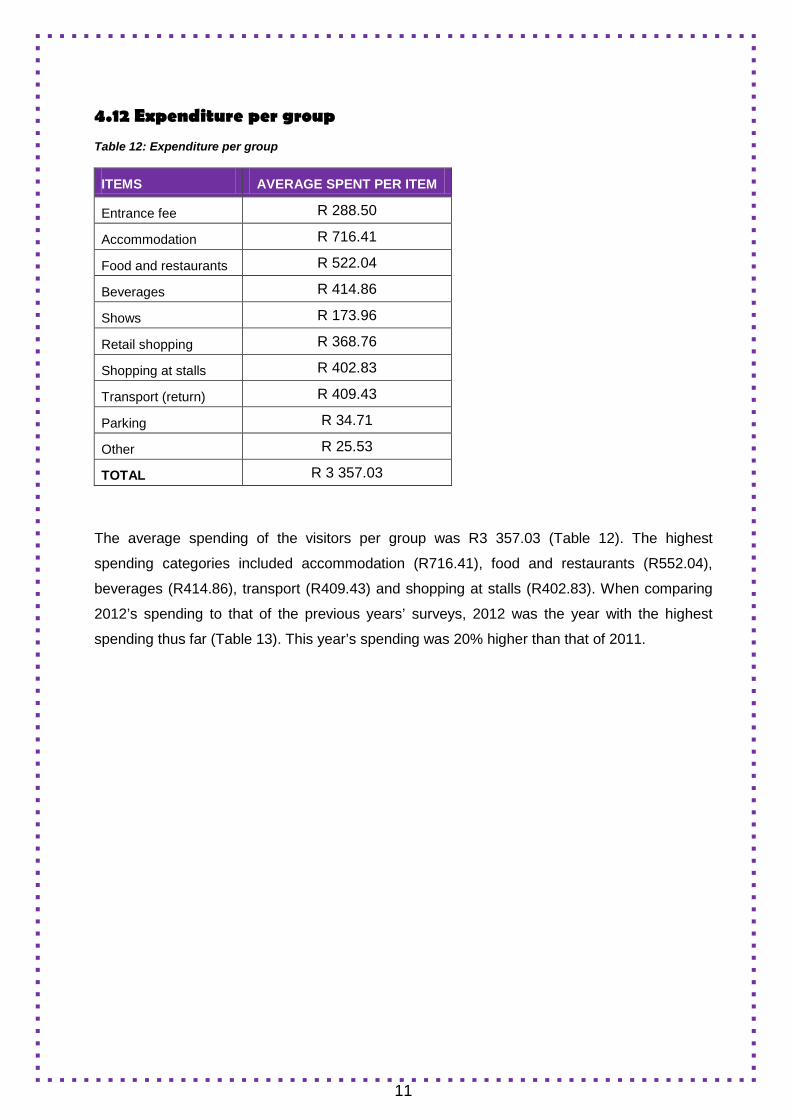

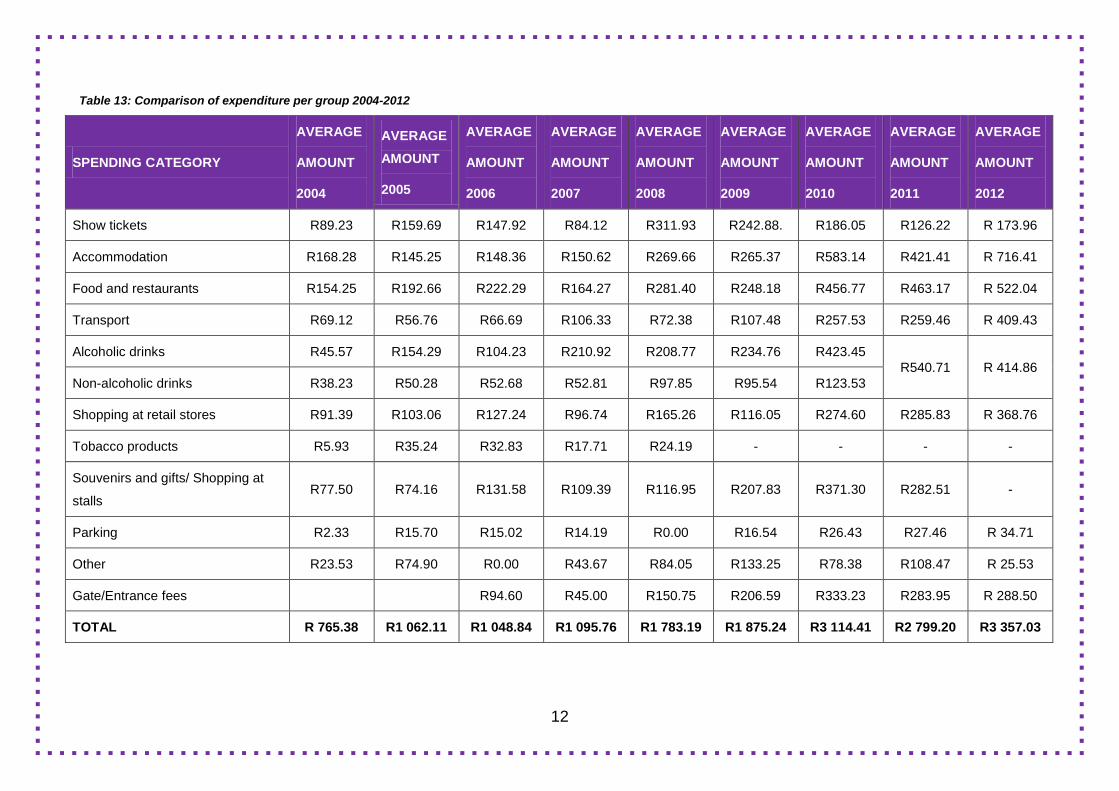

4.12 Expenditure per group Table 12: Expenditure per group

The average spending of the visitors per group was R3 357.03 (Table 12). The highest

spending categories included accommodation (R716.41), food and restaurants (R552.04),

beverages (R414.86), transport (R409.43) and shopping at stalls (R402.83). When comparing

2012’s spending to that of the previous years’ surveys, 2012 was the year with the highest

spending thus far (Table 13). This year’s spending was 20% higher than that of 2011.

ITEMS AVERAGE SPENT PER ITEM

Entrance fee R 288.50

Accommodation R 716.41

Food and restaurants R 522.04

Beverages R 414.86

Shows R 173.96

Retail shopping R 368.76

Shopping at stalls R 402.83

Transport (return) R 409.43

Parking R 34.71

Other R 25.53

TOTAL R 3 357.03

12

Table 13: Comparison of expenditure per group 2004-2012

SPENDING CATEGORY

AVERAGE

AMOUNT

2004

AVERAGE AMOUNT

2005

AVERAGE

AMOUNT

2006

AVERAGE

AMOUNT

2007

AVERAGE

AMOUNT

2008

AVERAGE

AMOUNT

2009

AVERAGE

AMOUNT

2010

AVERAGE

AMOUNT

2011

AVERAGE

AMOUNT

2012

Show tickets R89.23 R159.69 R147.92 R84.12 R311.93 R242.88. R186.05 R126.22 R 173.96

Accommodation R168.28 R145.25 R148.36 R150.62 R269.66 R265.37 R583.14 R421.41 R 716.41

Food and restaurants R154.25 R192.66 R222.29 R164.27 R281.40 R248.18 R456.77 R463.17 R 522.04

Transport R69.12 R56.76 R66.69 R106.33 R72.38 R107.48 R257.53 R259.46 R 409.43

Alcoholic drinks R45.57 R154.29 R104.23 R210.92 R208.77 R234.76 R423.45 R540.71 R 414.86

Non-alcoholic drinks R38.23 R50.28 R52.68 R52.81 R97.85 R95.54 R123.53

Shopping at retail stores R91.39 R103.06 R127.24 R96.74 R165.26 R116.05 R274.60 R285.83 R 368.76

Tobacco products R5.93 R35.24 R32.83 R17.71 R24.19 - - - -

Souvenirs and gifts/ Shopping at

stalls R77.50 R74.16 R131.58 R109.39 R116.95 R207.83 R371.30 R282.51 -

Parking R2.33 R15.70 R15.02 R14.19 R0.00 R16.54 R26.43 R27.46 R 34.71

Other R23.53 R74.90 R0.00 R43.67 R84.05 R133.25 R78.38 R108.47 R 25.53

Gate/Entrance fees R94.60 R45.00 R150.75 R206.59 R333.23 R283.95 R 288.50

TOTAL R 765.38 R1 062.11 R1 048.84 R1 095.76 R1 783.19 R1 875.24 R3 114.41 R2 799.20 R3 357.03

11

13

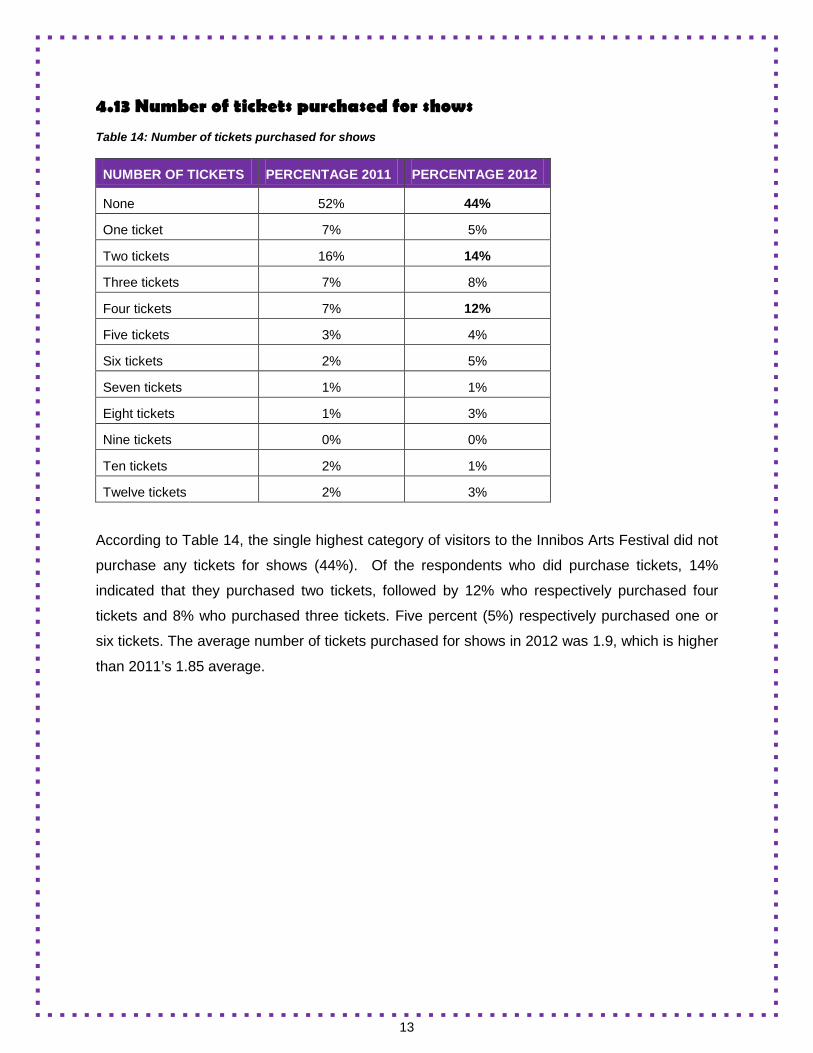

4.13 Number of tickets purchased for shows Table 14: Number of tickets purchased for shows

According to Table 14, the single highest category of visitors to the Innibos Arts Festival did not

purchase any tickets for shows (44%). Of the respondents who did purchase tickets, 14%

indicated that they purchased two tickets, followed by 12% who respectively purchased four

tickets and 8% who purchased three tickets. Five percent (5%) respectively purchased one or

six tickets. The average number of tickets purchased for shows in 2012 was 1.9, which is higher

than 2011’s 1.85 average.

NUMBER OF TICKETS PERCENTAGE 2011 PERCENTAGE 2012

None 52% 44%

One ticket 7% 5%

Two tickets 16% 14%

Three tickets 7% 8%

Four tickets 7% 12%

Five tickets 3% 4%

Six tickets 2% 5%

Seven tickets 1% 1%

Eight tickets 1% 3%

Nine tickets 0% 0%

Ten tickets 2% 1%

Twelve tickets 2% 3%

14

CONSUMER PROFILE

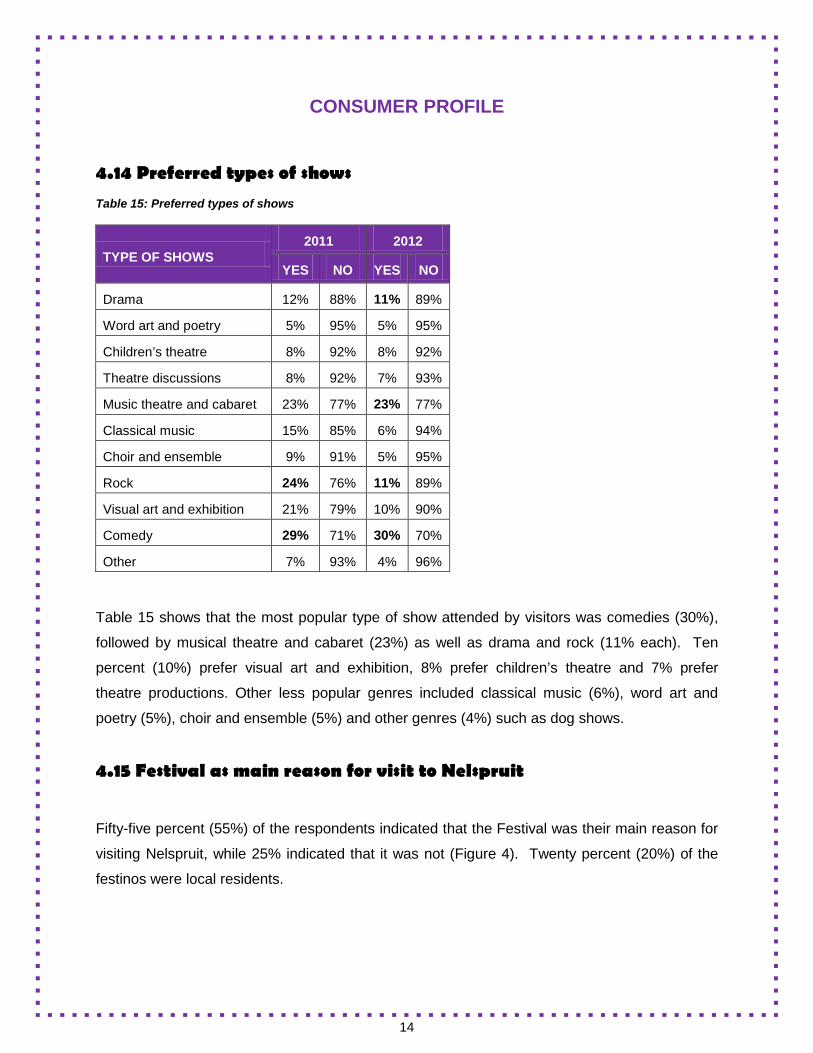

4.14 Preferred types of shows Table 15: Preferred types of shows

Table 15 shows that the most popular type of show attended by visitors was comedies (30%),

followed by musical theatre and cabaret (23%) as well as drama and rock (11% each). Ten

percent (10%) prefer visual art and exhibition, 8% prefer children’s theatre and 7% prefer

theatre productions. Other less popular genres included classical music (6%), word art and

poetry (5%), choir and ensemble (5%) and other genres (4%) such as dog shows.

4.15 Festival as main reason for visit to Nelspruit

Fifty-five percent (55%) of the respondents indicated that the Festival was their main reason for

visiting Nelspruit, while 25% indicated that it was not (Figure 4). Twenty percent (20%) of the

festinos were local residents.

TYPE OF SHOWS 2011 2012

YES NO YES NO

Drama 12% 88% 11% 89%

Word art and poetry 5% 95% 5% 95%

Children’s theatre 8% 92% 8% 92%

Theatre discussions 8% 92% 7% 93%

Music theatre and cabaret 23% 77% 23% 77%

Classical music 15% 85% 6% 94%

Choir and ensemble 9% 91% 5% 95%

Rock 24% 76% 11% 89%

Visual art and exhibition 21% 79% 10% 90%

Comedy 29% 71% 30% 70%

Other 7% 93% 4% 96%

15

Figure 4: Festival as main reason for visit to Nelspruit

4.16 Other festivals attended

Visitors indicated that they also attend the Aardklop National Arts Festival (33%), followed by

the KKNK (18%) (see Figure 5). Eight percent (8%) of the visitors indicated that they attended

other festivals such as Oppikoppi and the Crayfish festival. Four percent (4%) of respondents

also attended Vryfees and 3% attended the Grahamstown Arts Festival.

Figure 5: Other festivals attended

Yes55%

No25%

Local20%

18%

3% 4%

33%

8%

KKNK Grahamstown Vryfees Aardklop Other

16

4.17 Decision to attend Festival

In this section, respondents were asked when the decision was taken to visit the Festival, as

well as who initiated the trip to Nelspruit.

4.17.1 Type of decision

Figure 6: Decision to attend Festival

According to Figure 6, the majority of visitors (43%) to the Innibos Arts Festival made their

decision to attend the Festival more than a month ago. Thirty-one percent (31%) indicated that

it was a spontaneous decision, while 15% made their decision to attend less than a month ago.

Eleven percent (11%) (Other) indicated that they made their decision right after last years’

festival and that it was an annual commitment.

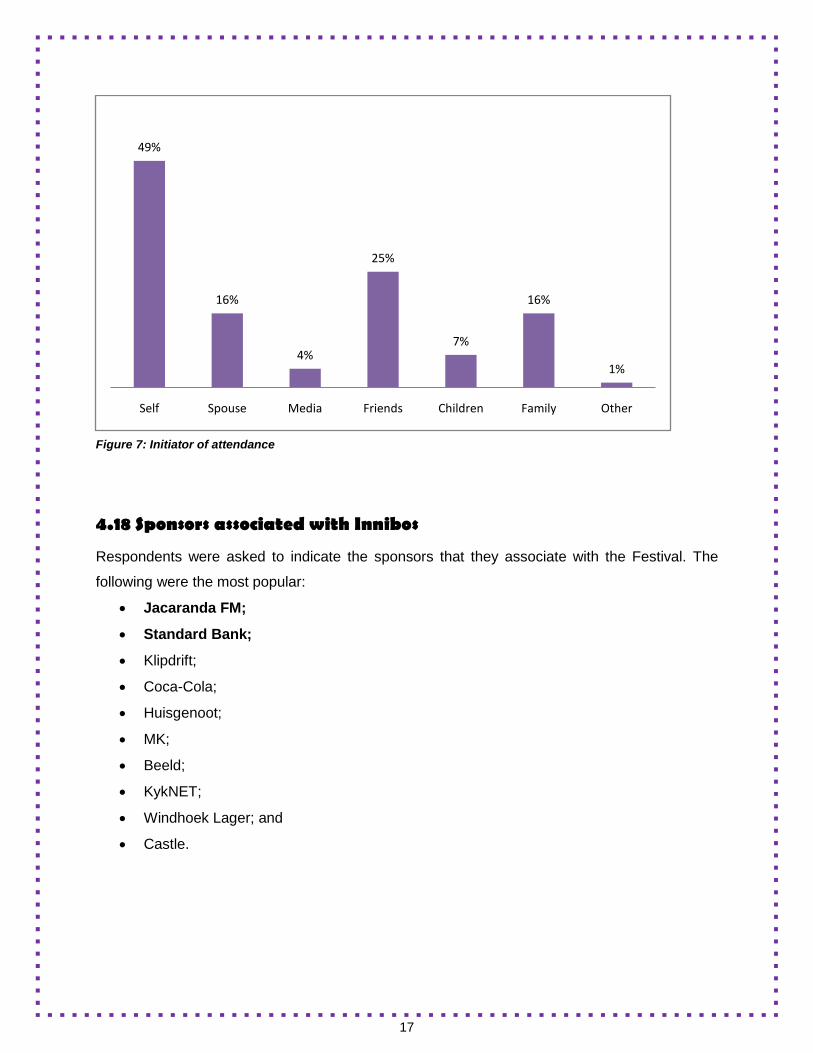

4.17.2 Initiator of trip

It is clear from Figure 7 that the majority of respondents (49%) at the Innibos National Arts

Festival in Nelspruit in 2012 initiated the trip to the Festival themselves, followed by friends

(25%), spouses or family (25% each) and media (4%) who initiated the trip. One percent (1%) of

trips was initiated by respondents’ boyfriends or girlfriends.

31%

15%

43%

11%

Spontaneous decision

Less than a month ago

More than a month ago

Other

17

Figure 7: Initiator of attendance

4.18 Sponsors associated with Innibos

Respondents were asked to indicate the sponsors that they associate with the Festival. The

following were the most popular:

• Jacaranda FM;

• Standard Bank;

• Klipdrift;

• Coca-Cola;

• Huisgenoot;

• MK;

• Beeld;

• KykNET;

• Windhoek Lager; and

• Castle.

49%

16%

4%

25%

7%

16%

1%

Self Spouse Media Friends Children Family Other

18

4.19 Number of visits to Festival

Even though this Festival was nine years old in 2012, it is interesting to note that it still attracts a

high number of first-time visitors (33%). Sixteen percent (16%) of the visitors have attended this

Festival twice and 13% have been attending the Festival since it started nine years ago. Twelve

percent (12%) attended the Festival for the third time, 8% for the fourth time and 6% for the fifth

time (Table 16). The average number of times that the visitors have attended this Festival was

3.63 times, which is more than 2011’s average of 2.52 times and 2010’s 2.6 times.

Table 16: Number of visits to the Festival

NUMBER OF VISITS 2011 2012

First time 31% 33%

Twice 17% 16%

3 Times 17% 12%

4 Times 11% 8%

5 Times 12% 6%

6 Times 6% 3%

7 Times 3% 3%

8 Times 3% 5%

9 Times - 13%

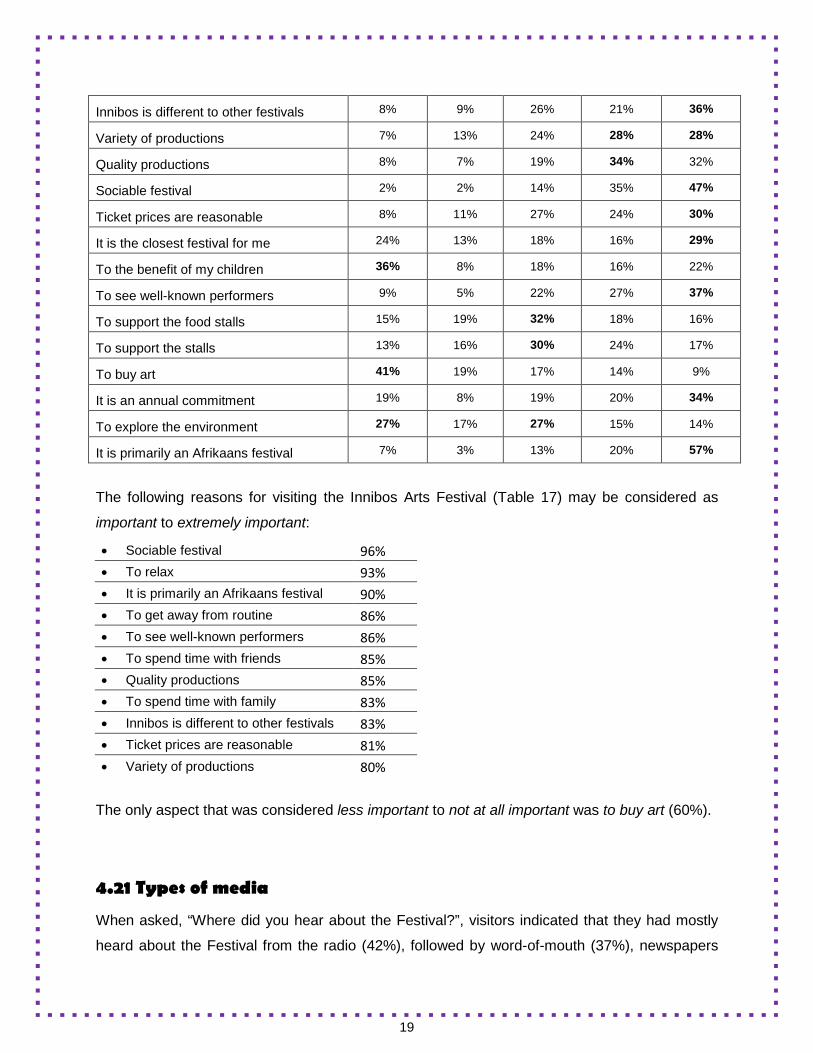

4.20 Motivation to attend the Festival

This question focused on the motivating factors for attending the Innibos Arts Festival. This

information can be used when developing marketing strategies for specific markets.

Table 17: Motivation to attend the Festival

MOTIVATIONAL FACTORS Not at all

important

Less

important Important Very

important Extremely important

To get away from routine 7% 7% 23% 20% 43%

To relax 4% 3% 15% 28% 50%

To spend time with family 9% 8% 16% 24% 43%

To spend time with friends 7% 8% 18% 28% 39%

To meet new people 26% 21% 23% 14% 16%

19

Innibos is different to other festivals 8% 9% 26% 21% 36%

Variety of productions 7% 13% 24% 28% 28%

Quality productions 8% 7% 19% 34% 32%

Sociable festival 2% 2% 14% 35% 47%

Ticket prices are reasonable 8% 11% 27% 24% 30%

It is the closest festival for me 24% 13% 18% 16% 29%

To the benefit of my children 36% 8% 18% 16% 22%

To see well-known performers 9% 5% 22% 27% 37%

To support the food stalls 15% 19% 32% 18% 16%

To support the stalls 13% 16% 30% 24% 17%

To buy art 41% 19% 17% 14% 9%

It is an annual commitment 19% 8% 19% 20% 34%

To explore the environment 27% 17% 27% 15% 14%

It is primarily an Afrikaans festival 7% 3% 13% 20% 57%

The following reasons for visiting the Innibos Arts Festival (Table 17) may be considered as

important to extremely important:

• Sociable festival 96% • To relax 93% • It is primarily an Afrikaans festival 90% • To get away from routine 86% • To see well-known performers 86% • To spend time with friends 85% • Quality productions 85% • To spend time with family 83% • Innibos is different to other festivals 83% • Ticket prices are reasonable 81% • Variety of productions 80%

The only aspect that was considered less important to not at all important was to buy art (60%).

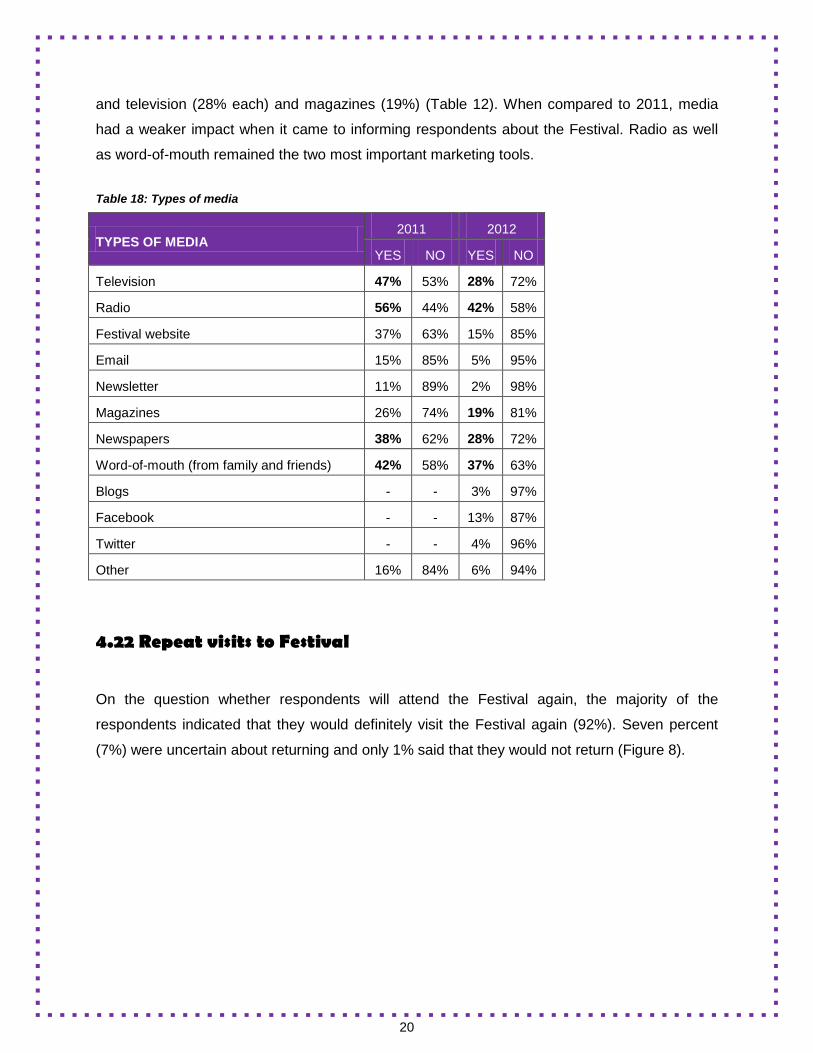

4.21 Types of media

When asked, “Where did you hear about the Festival?”, visitors indicated that they had mostly

heard about the Festival from the radio (42%), followed by word-of-mouth (37%), newspapers

20

and television (28% each) and magazines (19%) (Table 12). When compared to 2011, media

had a weaker impact when it came to informing respondents about the Festival. Radio as well

as word-of-mouth remained the two most important marketing tools.

Table 18: Types of media

TYPES OF MEDIA 2011 2012

YES NO YES NO

Television 47% 53% 28% 72%

Radio 56% 44% 42% 58%

Festival website 37% 63% 15% 85%

Email 15% 85% 5% 95%

Newsletter 11% 89% 2% 98%

Magazines 26% 74% 19% 81%

Newspapers 38% 62% 28% 72%

Word-of-mouth (from family and friends) 42% 58% 37% 63%

Blogs - - 3% 97%

Facebook - - 13% 87%

Twitter - - 4% 96%

Other 16% 84% 6% 94%

4.22 Repeat visits to Festival

On the question whether respondents will attend the Festival again, the majority of the

respondents indicated that they would definitely visit the Festival again (92%). Seven percent

(7%) were uncertain about returning and only 1% said that they would not return (Figure 8).

21

Figure 8: Repeat visits to Festival

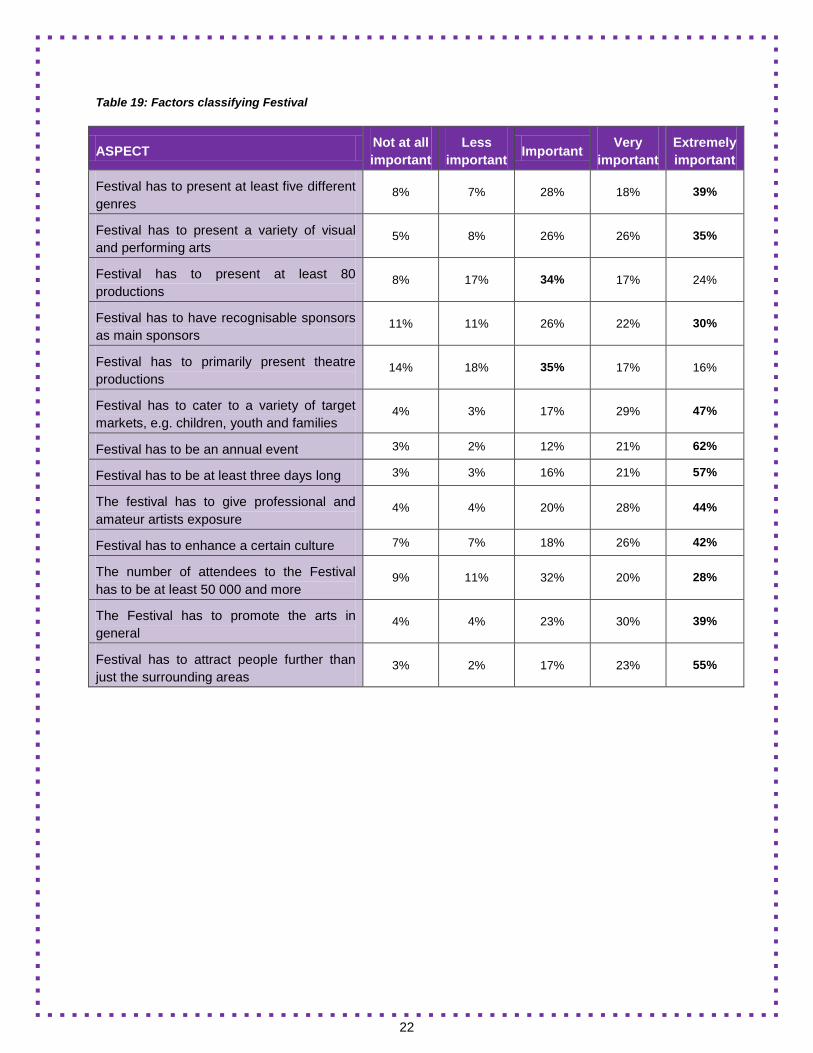

4.23 Factors that classify national arts festivals

Respondents were asked to indicate how important certain aspects are when classifying a

national arts festival. The respondents rated the following aspects as important to extremely

important:

• Festival has to attract people further than just the surrounding areas 95%

• Festival has to be an annual event 95%

• Festival has to be at least three days long 94%

• Festival has to cater to a variety of target markets, e.g. children, youth and families 93%

• The festival has to give professional and amateur artists exposure 92%

• The Festival has to promote the arts in general 92%

Respondents felt that all aspects were important for the classification of an arts festival.

Yes, definitely92%

No, definitely not1%

Perhaps7%

22

Table 19: Factors classifying Festival

ASPECT Not at all important

Less important Important Very

important Extremely important

Festival has to present at least five different genres

8% 7% 28% 18% 39%

Festival has to present a variety of visual and performing arts

5% 8% 26% 26% 35%

Festival has to present at least 80 productions

8% 17% 34% 17% 24%

Festival has to have recognisable sponsors as main sponsors

11% 11% 26% 22% 30%

Festival has to primarily present theatre productions

14% 18% 35% 17% 16%

Festival has to cater to a variety of target markets, e.g. children, youth and families

4% 3% 17% 29% 47%

Festival has to be an annual event 3% 2% 12% 21% 62%

Festival has to be at least three days long 3% 3% 16% 21% 57%

The festival has to give professional and amateur artists exposure

4% 4% 20% 28% 44%

Festival has to enhance a certain culture 7% 7% 18% 26% 42%

The number of attendees to the Festival has to be at least 50 000 and more

9% 11% 32% 20% 28%

The Festival has to promote the arts in general

4% 4% 23% 30% 39%

Festival has to attract people further than just the surrounding areas

3% 2% 17% 23% 55%

23

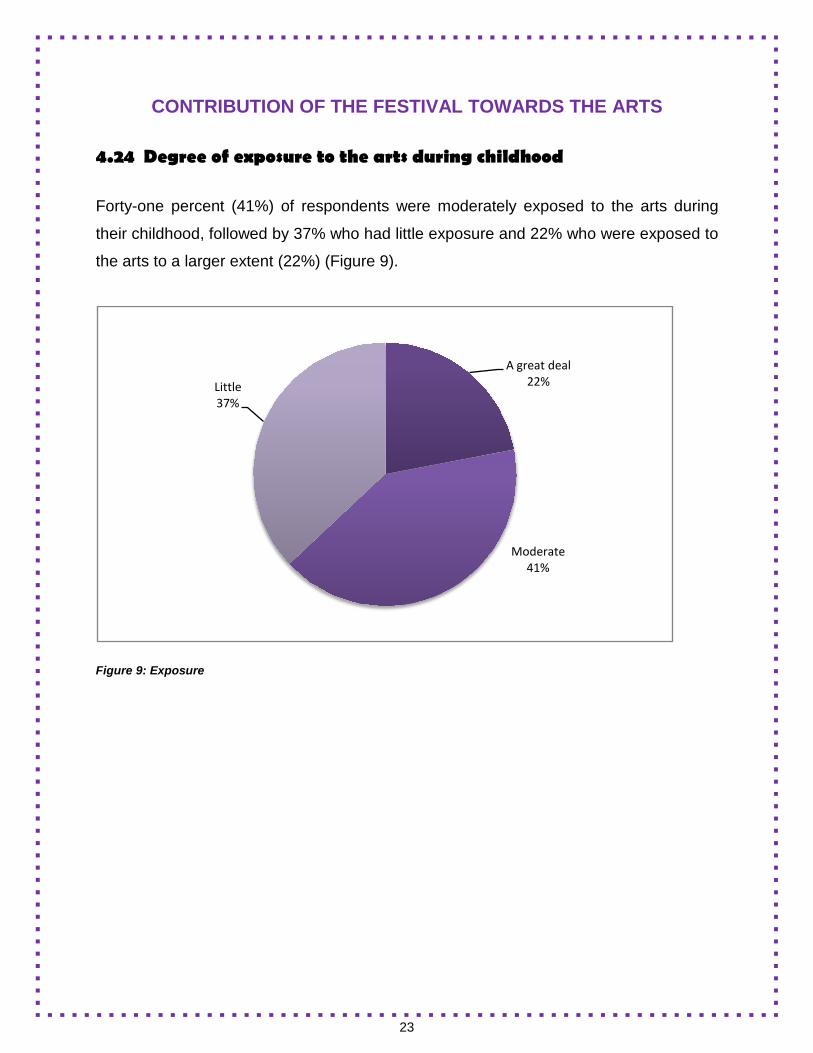

CONTRIBUTION OF THE FESTIVAL TOWARDS THE ARTS 4.24 Degree of exposure to the arts during childhood

Forty-one percent (41%) of respondents were moderately exposed to the arts during

their childhood, followed by 37% who had little exposure and 22% who were exposed to

the arts to a larger extent (22%) (Figure 9).

Figure 9: Exposure

A great deal22%

Moderate41%

Little37%

24

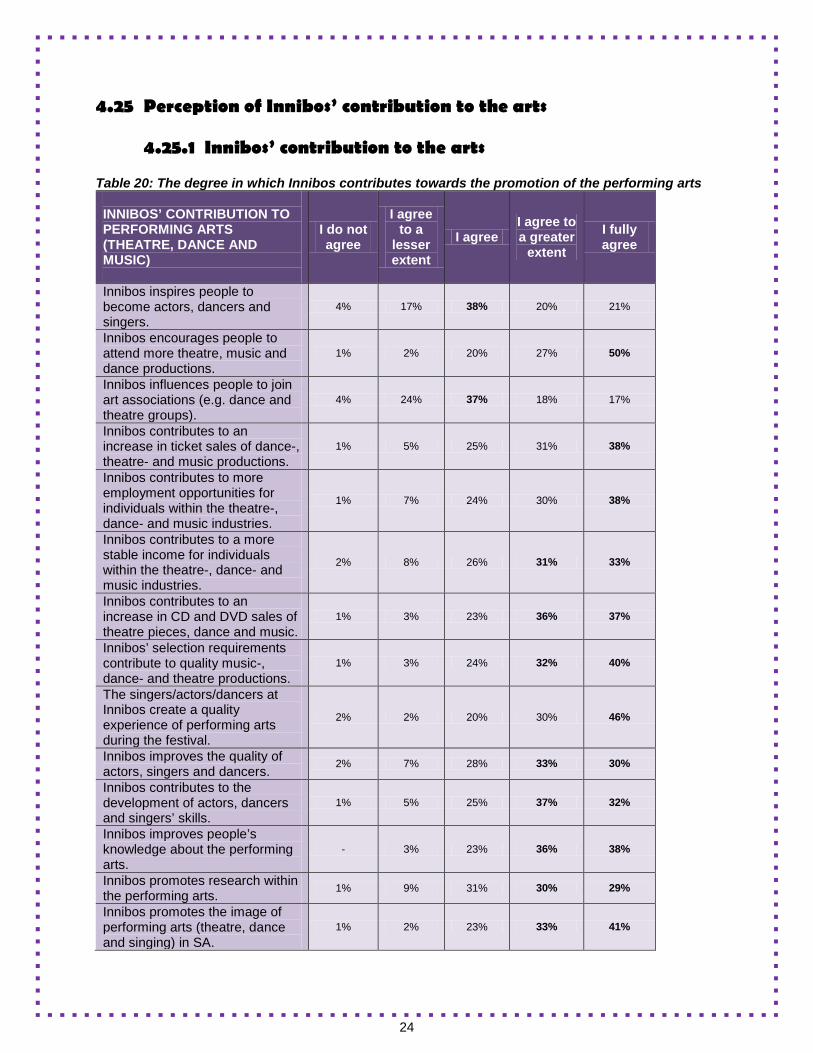

4.25 Perception of Innibos’ contribution to the arts

4.25.1 Innibos’ contribution to the arts Table 20: The degree in which Innibos contributes towards the promotion of the performing arts INNIBOS’ CONTRIBUTION TO PERFORMING ARTS (THEATRE, DANCE AND MUSIC)

I do not agree

I agree to a

lesser extent

I agree I agree to a greater

extent

I fully agree

Innibos inspires people to become actors, dancers and singers.

4% 17% 38% 20% 21%

Innibos encourages people to attend more theatre, music and dance productions.

1% 2% 20% 27% 50%

Innibos influences people to join art associations (e.g. dance and theatre groups).

4% 24% 37% 18% 17%

Innibos contributes to an increase in ticket sales of dance-, theatre- and music productions.

1% 5% 25% 31% 38%

Innibos contributes to more employment opportunities for individuals within the theatre-, dance- and music industries.

1% 7% 24% 30% 38%

Innibos contributes to a more stable income for individuals within the theatre-, dance- and music industries.

2% 8% 26% 31% 33%

Innibos contributes to an increase in CD and DVD sales of theatre pieces, dance and music.

1% 3% 23% 36% 37%

Innibos’ selection requirements contribute to quality music-, dance- and theatre productions.

1% 3% 24% 32% 40%

The singers/actors/dancers at Innibos create a quality experience of performing arts during the festival.

2% 2% 20% 30% 46%

Innibos improves the quality of actors, singers and dancers. 2% 7% 28% 33% 30%

Innibos contributes to the development of actors, dancers and singers’ skills.

1% 5% 25% 37% 32%

Innibos improves people’s knowledge about the performing arts.

- 3% 23% 36% 38%

Innibos promotes research within the performing arts. 1% 9% 31% 30% 29%

Innibos promotes the image of performing arts (theatre, dance and singing) in SA.

1% 2% 23% 33% 41%

25

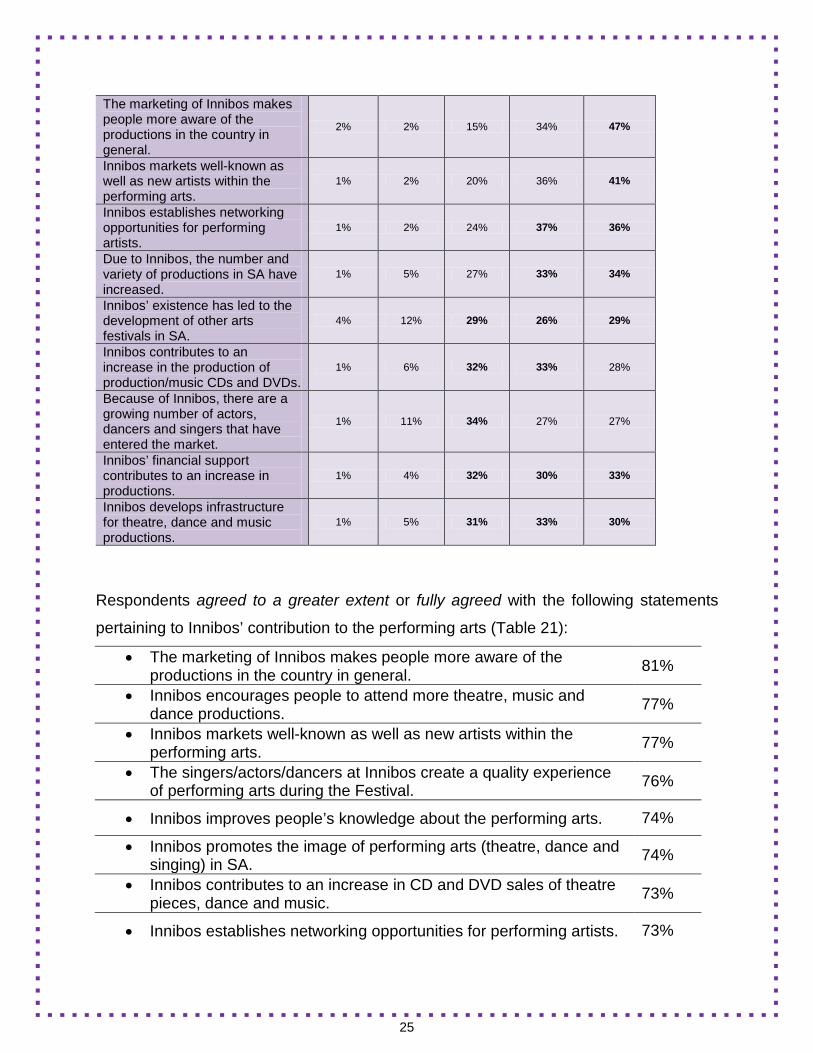

The marketing of Innibos makes people more aware of the productions in the country in general.

2% 2% 15% 34% 47%

Innibos markets well-known as well as new artists within the performing arts.

1% 2% 20% 36% 41%

Innibos establishes networking opportunities for performing artists.

1% 2% 24% 37% 36%

Due to Innibos, the number and variety of productions in SA have increased.

1% 5% 27% 33% 34%

Innibos’ existence has led to the development of other arts festivals in SA.

4% 12% 29% 26% 29%

Innibos contributes to an increase in the production of production/music CDs and DVDs.

1% 6% 32% 33% 28%

Because of Innibos, there are a growing number of actors, dancers and singers that have entered the market.

1% 11% 34% 27% 27%

Innibos’ financial support contributes to an increase in productions.

1% 4% 32% 30% 33%

Innibos develops infrastructure for theatre, dance and music productions.

1% 5% 31% 33% 30%

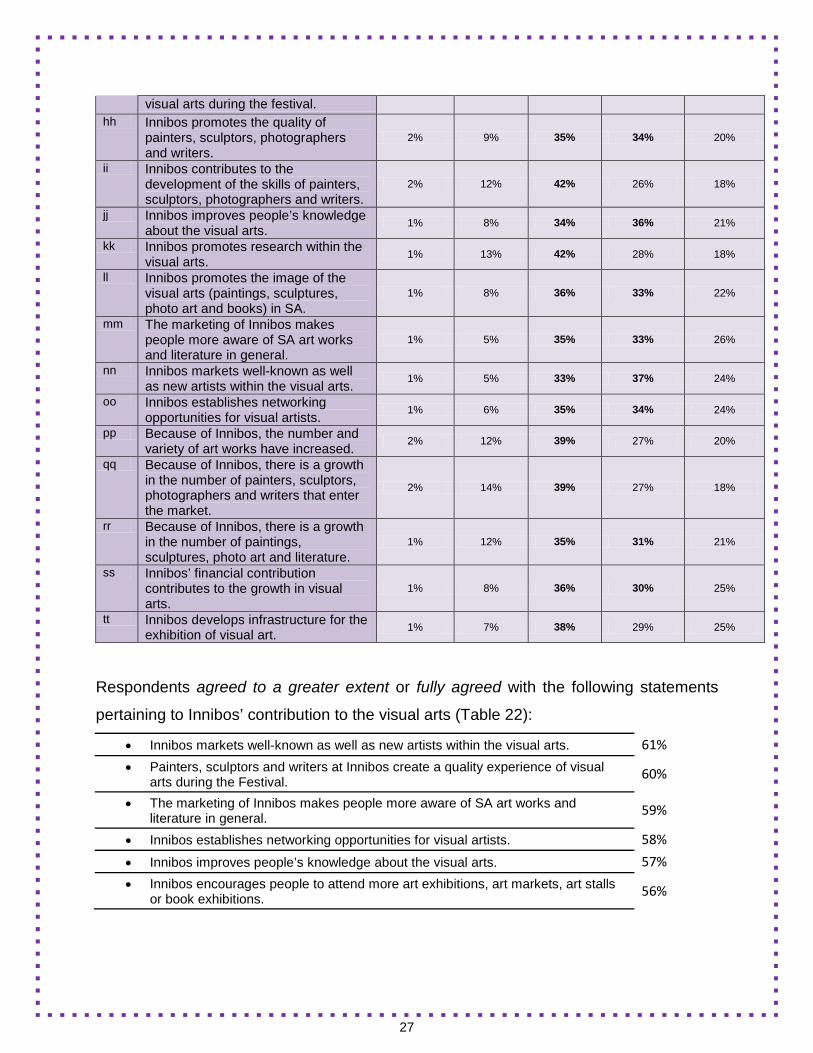

Respondents agreed to a greater extent or fully agreed with the following statements

pertaining to Innibos’ contribution to the performing arts (Table 21):

• The marketing of Innibos makes people more aware of the productions in the country in general. 81%

• Innibos encourages people to attend more theatre, music and dance productions. 77%

• Innibos markets well-known as well as new artists within the performing arts. 77%

• The singers/actors/dancers at Innibos create a quality experience of performing arts during the Festival. 76%

• Innibos improves people’s knowledge about the performing arts. 74%

• Innibos promotes the image of performing arts (theatre, dance and singing) in SA. 74%

• Innibos contributes to an increase in CD and DVD sales of theatre pieces, dance and music. 73%

• Innibos establishes networking opportunities for performing artists. 73%

26

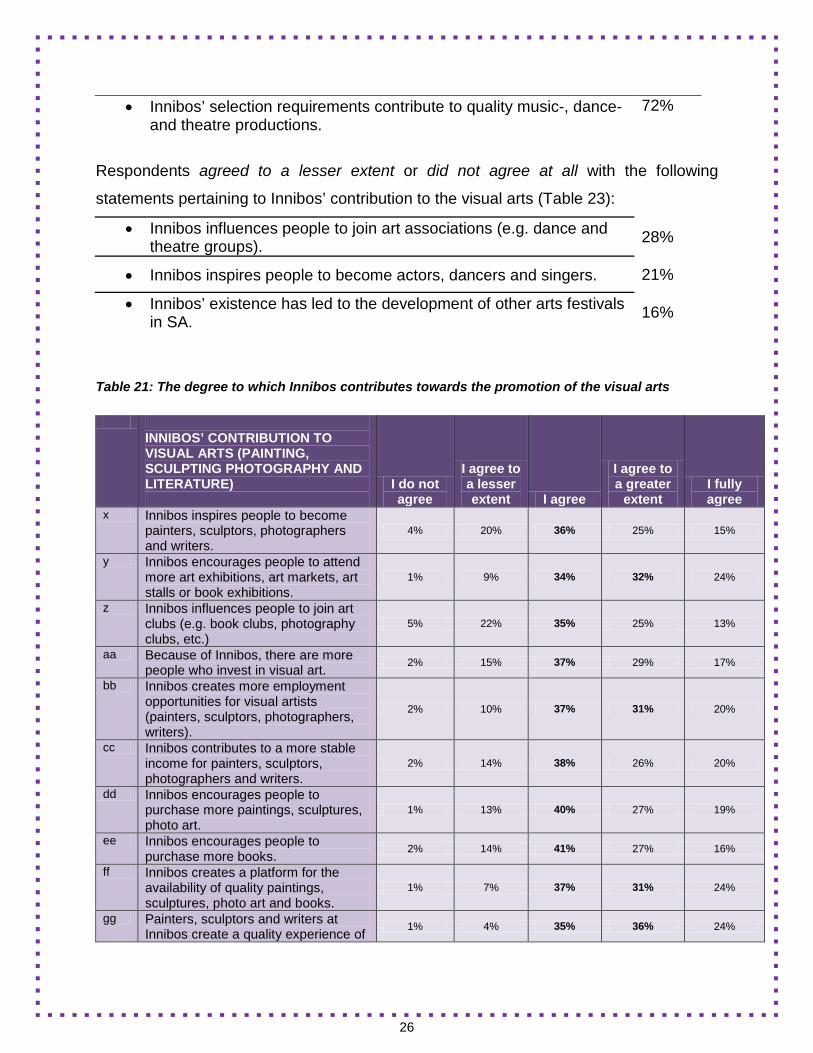

• Innibos’ selection requirements contribute to quality music-, dance- and theatre productions.

72%

Respondents agreed to a lesser extent or did not agree at all with the following

statements pertaining to Innibos’ contribution to the visual arts (Table 23):

• Innibos influences people to join art associations (e.g. dance and theatre groups). 28%

• Innibos inspires people to become actors, dancers and singers. 21%

• Innibos’ existence has led to the development of other arts festivals in SA. 16%

Table 21: The degree to which Innibos contributes towards the promotion of the visual arts

INNIBOS’ CONTRIBUTION TO VISUAL ARTS (PAINTING, SCULPTING PHOTOGRAPHY AND LITERATURE)

I do not agree

I agree to a lesser extent I agree

I agree to a greater

extent I fully agree

x Innibos inspires people to become painters, sculptors, photographers and writers.

4% 20% 36% 25% 15%

y Innibos encourages people to attend more art exhibitions, art markets, art stalls or book exhibitions.

1% 9% 34% 32% 24%

z Innibos influences people to join art clubs (e.g. book clubs, photography clubs, etc.)

5% 22% 35% 25% 13%

aa Because of Innibos, there are more people who invest in visual art. 2% 15% 37% 29% 17%

bb Innibos creates more employment opportunities for visual artists (painters, sculptors, photographers, writers).

2% 10% 37% 31% 20%

cc Innibos contributes to a more stable income for painters, sculptors, photographers and writers.

2% 14% 38% 26% 20%

dd Innibos encourages people to purchase more paintings, sculptures, photo art.

1% 13% 40% 27% 19%

ee Innibos encourages people to purchase more books. 2% 14% 41% 27% 16%

ff Innibos creates a platform for the availability of quality paintings, sculptures, photo art and books.

1% 7% 37% 31% 24%

gg Painters, sculptors and writers at Innibos create a quality experience of 1% 4% 35% 36% 24%

27

visual arts during the festival. hh Innibos promotes the quality of

painters, sculptors, photographers and writers.

2% 9% 35% 34% 20%

ii Innibos contributes to the development of the skills of painters, sculptors, photographers and writers.

2% 12% 42% 26% 18%

jj Innibos improves people’s knowledge about the visual arts. 1% 8% 34% 36% 21%

kk Innibos promotes research within the visual arts. 1% 13% 42% 28% 18%

ll Innibos promotes the image of the visual arts (paintings, sculptures, photo art and books) in SA.

1% 8% 36% 33% 22%

mm The marketing of Innibos makes people more aware of SA art works and literature in general.

1% 5% 35% 33% 26%

nn Innibos markets well-known as well as new artists within the visual arts. 1% 5% 33% 37% 24%

oo Innibos establishes networking opportunities for visual artists. 1% 6% 35% 34% 24%

pp Because of Innibos, the number and variety of art works have increased. 2% 12% 39% 27% 20%

qq Because of Innibos, there is a growth in the number of painters, sculptors, photographers and writers that enter the market.

2% 14% 39% 27% 18%

rr Because of Innibos, there is a growth in the number of paintings, sculptures, photo art and literature.

1% 12% 35% 31% 21%

ss Innibos’ financial contribution contributes to the growth in visual arts.

1% 8% 36% 30% 25%

tt Innibos develops infrastructure for the exhibition of visual art. 1% 7% 38% 29% 25%

Respondents agreed to a greater extent or fully agreed with the following statements

pertaining to Innibos’ contribution to the visual arts (Table 22):

• Innibos markets well-known as well as new artists within the visual arts. 61%

• Painters, sculptors and writers at Innibos create a quality experience of visual arts during the Festival. 60%

• The marketing of Innibos makes people more aware of SA art works and literature in general. 59%

• Innibos establishes networking opportunities for visual artists. 58%

• Innibos improves people’s knowledge about the visual arts. 57%

• Innibos encourages people to attend more art exhibitions, art markets, art stalls or book exhibitions. 56%

28

Respondents agreed to a lesser extent or did not agree at all with no aspects named

(Table 22).

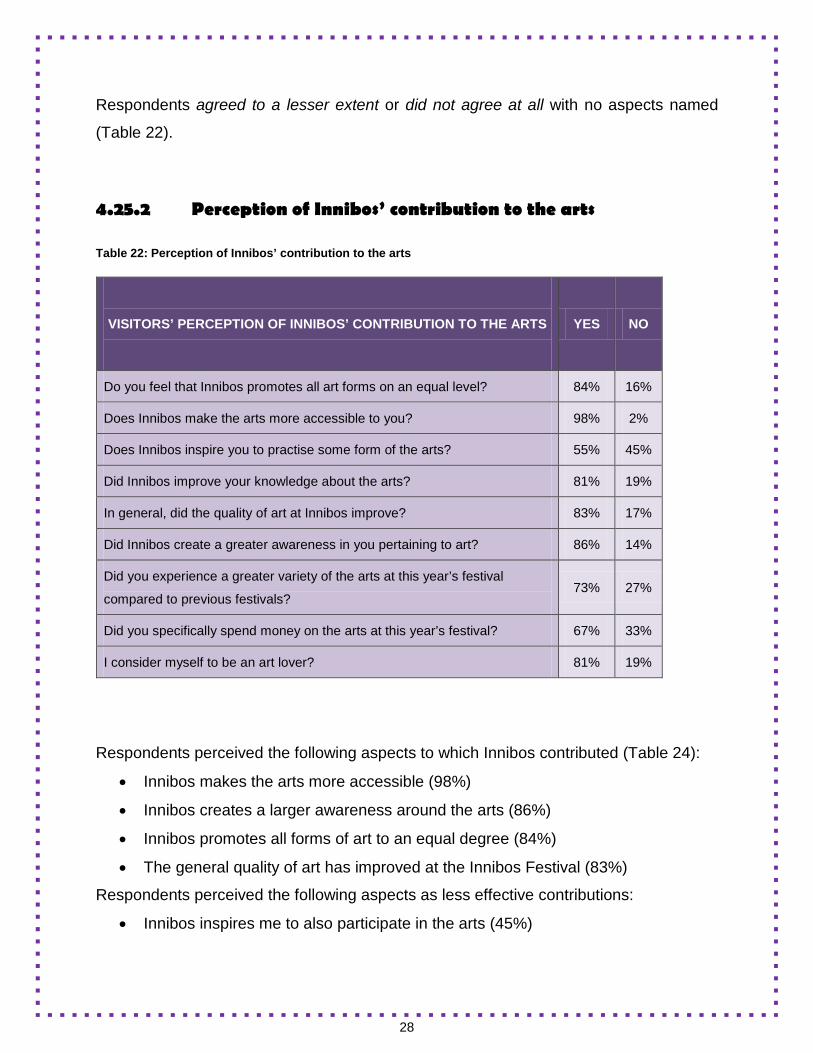

4.25.2 Perception of Innibos’ contribution to the arts

Table 22: Perception of Innibos’ contribution to the arts

Respondents perceived the following aspects to which Innibos contributed (Table 24):

• Innibos makes the arts more accessible (98%)

• Innibos creates a larger awareness around the arts (86%)

• Innibos promotes all forms of art to an equal degree (84%)

• The general quality of art has improved at the Innibos Festival (83%)

Respondents perceived the following aspects as less effective contributions:

• Innibos inspires me to also participate in the arts (45%)

VISITORS’ PERCEPTION OF INNIBOS’ CONTRIBUTION TO THE ARTS

YES NO

Do you feel that Innibos promotes all art forms on an equal level? 84% 16%

Does Innibos make the arts more accessible to you? 98% 2%

Does Innibos inspire you to practise some form of the arts? 55% 45%

Did Innibos improve your knowledge about the arts? 81% 19%

In general, did the quality of art at Innibos improve? 83% 17%

Did Innibos create a greater awareness in you pertaining to art? 86% 14%

Did you experience a greater variety of the arts at this year’s festival

compared to previous festivals? 73% 27%

Did you specifically spend money on the arts at this year’s festival? 67% 33%

I consider myself to be an art lover? 81% 19%

29

• Did you specifically spend money on art during your visit to the Festival? (33%)

• Have you experienced a larger amount of art at this year’s Festival, compared to

previous years (27%)

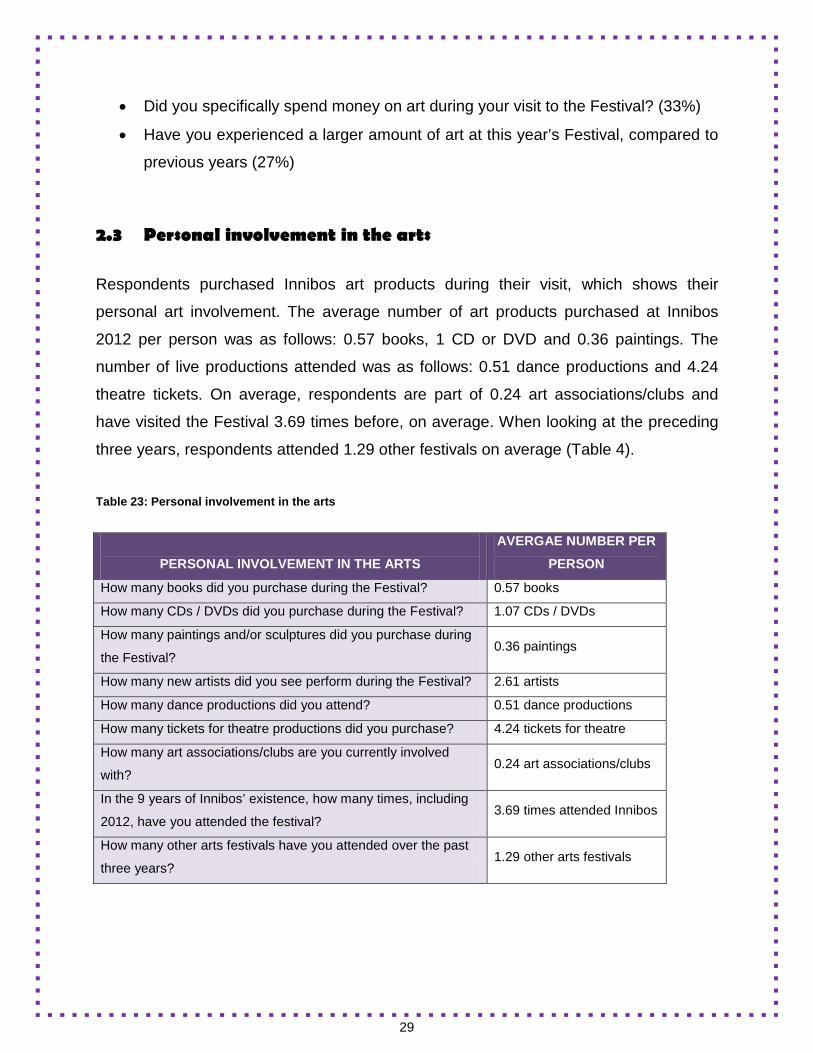

2.3 Personal involvement in the arts

Respondents purchased Innibos art products during their visit, which shows their

personal art involvement. The average number of art products purchased at Innibos

2012 per person was as follows: 0.57 books, 1 CD or DVD and 0.36 paintings. The

number of live productions attended was as follows: 0.51 dance productions and 4.24

theatre tickets. On average, respondents are part of 0.24 art associations/clubs and

have visited the Festival 3.69 times before, on average. When looking at the preceding

three years, respondents attended 1.29 other festivals on average (Table 4).

Table 23: Personal involvement in the arts

PERSONAL INVOLVEMENT IN THE ARTS

AVERGAE NUMBER PER

PERSON

How many books did you purchase during the Festival? 0.57 books

How many CDs / DVDs did you purchase during the Festival? 1.07 CDs / DVDs

How many paintings and/or sculptures did you purchase during

the Festival? 0.36 paintings

How many new artists did you see perform during the Festival? 2.61 artists

How many dance productions did you attend? 0.51 dance productions

How many tickets for theatre productions did you purchase? 4.24 tickets for theatre

How many art associations/clubs are you currently involved

with? 0.24 art associations/clubs

In the 9 years of Innibos’ existence, how many times, including

2012, have you attended the festival? 3.69 times attended Innibos

How many other arts festivals have you attended over the past

three years? 1.29 other arts festivals

30

5. Economic contribution

When events are hosted in an economy, it leads to additional spending within that economy,

which influences production and income. However, only additional spending in an economy can

cause an economic impact in that economy. This additional spending represents the cash

injection into the local economy and this is often referred to as the direct impact of an event. In

tourism, the main contributors to this additional spending are tourists. Factors that influence the

magnitude of the direct impact caused by tourists include:

The number of tourists;

The magnitude of their spending; and

The length of stay.

To determine the direct impact of visitor spending at Innibos Festival, these aspects have to be

considered. The numbers calculated are derived from the information obtained from the survey

as well as data provided by the festival organisers.

Events also generate another form of spending, namely spending by organisers. To get a true

reflection of the value of the festival for the economy of the area, the spending by organisers

should also be considered.

5.1 The number of visitors and length of stay

The total number of tickets sold for shows at Innibos 2012 was 14 000, which is very similar to

the 14 100 show tickets sold in 2011. In addition to the show tickets sold, 53 000 tickets were

sold for the festival grounds where productions were also showcased, which shows a decline

from last years’ 83 526 entrance tickets sold, but is quite similar to the 59 049 tickets sold during

2010.

Since the tickets for the festival grounds could be bought for more than one day, the total

number of visitors are estimated to be the same as the tickets sold for the festival grounds –

53 000 (compared to 83 526 last year). This is then taken as the absolute number of visitors.

Since the results from the visitor questionnaire showed that people stayed for an average of

2.67 days at the Festival, the number of visitor days is estimated at 141 510, which shows a

significant decrease compared to the 250 578 visitor days estimated for 2011, but which is

31

again very comparable to the 141 718 visitor days estimated for 2010. A visitor day counts the

visitor every day that he/she spends at the Festival, which implies that a visitor, who attends the

Festival for three days, is counted three times. Therefore, visitor days are calculated by taking

the absolute number of visitors multiplied by the average number of days spent at the Festival.

The decline in visitor days is fuelled by both the decline in time spent at the Festival as well as

the decline in the number of entrance tickets sold.

Since the expenditure is shown in per visitor group terms, the number of visitor groups should

be determined. Based on the income received from entrance tickets sold and the average

spending per visitor group on entrance tickets, the number of visitor groups at Innibos 2012 is estimated at 20 901, which is comparable to the 20 250 visitor groups that attended Innibos

2011 and the 20 362 visitor groups at Innibos 2010.

5.2 The magnitude of spending

The questionnaire distributed to visitors included a question on spending due to the Festival.

Different components were included in the spending breakdown, including accommodation,

transport, food and restaurants (see Table 12). It is estimated that a visitor group spent an

average of R3 357.03 (including entrance fees) while at the Festival. Spending due to the

Festival shows an increase from spending at the 2011 (R2 799.20) and even the 2010 festival

(R3 114.41).

A simple calculation to determine the extent of total spending by visitors due to the Festival

reveals that approximately R67.5 million was spent, which is more than the R56.7 million

estimated for 2011 and also more than the R63.4 million estimated for the 2010 Innibos

Festival. This can mainly be attributed to the increase in spending per visitor group. However,

some of this spending does not take place in the area of the Festival and in order to get a true

reflection of the extent of total spending, this should be accounted for.

5.3 Economic contribution

Since the festival organisers use the income received from show ticket sales as well as from

entrance fees to pay for services and other cost in hosting the festival, it should not be counted

twice as a spending item. Therefore, this is excluded from total visitor spending this year and

rather added to organiser spending. In addition, visitor spending is adjusted to account for

32

transport costs, which do not accrue to the local area (an adjustment of 50% is made).

Furthermore, not all of the exhibitors and food vendors at the Festival stem from the local area

and spending on souvenirs and food should therefore also be adjusted to reflect this. The

adjustments made are based on the distribution of stalls between locals and non-locals (same

distribution as 2011 was used). After these adjustments, the spending by the festinos

(excluding spending on entrance and shows) amounts to R45.1 million, which is similar to the

spending by festinos (including entrance and show tickets) during 2011’s Innibos Festival.

While visitor spending is by far the greatest contributor to the additional spending in the area,

the spending by festival organisers and exhibitors also takes place in the local economy. This

should also be accounted for to derive a realistic economic impact. The cost to host the Festival

(in terms of venues, contractors etc.) that accrued to local institutions and people is estimated

as a percentage of the ticket sales, entrance fees, sponsorships, stall rental and other income

received. Based on the cost items spent on, this percentage that remains in the local area is

estimated on 67% of total festival organiser spending and this amounts to R7.9 million.

Table 24: Economic impact

2010:

Scenario 1

2010:

Scenario 2

2011:

Scenario 1

2011:

Scenario 2

2012

Scenario 1

2012

Scenario 2

Visitor spending

(including tickets)

R51 069 804 R51 069 804 R45 123 222 R45 123 222

Visitor spending

(excluding tickets)

R45 128 292 R45 128 292

Organiser spending

(excluding tickets)

R 3 484 469 R 3 484 469 R 3 267 353 R 3 267 353

Organiser spending

(including tickets)

R7 908 000 R7 908 000

Total direct spending

R54 554 273 R54 554 273 R48 390 575 R48 390 575 R53 036 292 R53 036 292

Multiplier 1.5 1.3 1.5 1.3 1.5 1.3

Indirect impact R27 277 137 R16 366 282 R24 195 287 R14 517 172 R26 518 146 R15 910 888

Total impact R81 831 410 R70 920 555 R72 585 862 R62 907 747 R79 554 438 R68 947 180

Table 22 summarises the total spending by each of the categories. By adding the different

components, a direct impact estimate can be derived, which is estimated at R53 million

(compared to R48.4 million in 2010 and R54.6 million in 2009). When money is spent in an

area, it provides additional income to those individuals and institutions that use the additional

33

money to spend on other items. For example, businesses will pay suppliers for additional stock

and pay employees, while individuals will use the income to buy additional products. This

causes some businesses and individuals to receive additional income, which leads to an

increase in their spending and so the process continues. This process is captured by the

multiplier and represents the indirect impact of the event.

In order to draw a comparison, two scenarios are again presented. Scenario 1 uses a multiplier

of 1.5 (as in previous years), while Scenario 2 is based on the average multiplier of the business

surveys of 2008 and 2009, which is 1.3. This is reflected in Table 22, and the total impact of the

Festival is estimated at R79.6 million under Scenario 1 (multiplier of 1.5) and R68.95 million

under Scenario 2 (multiplier of 1.3). Scenario 1 can therefore be viewed as the “most optimistic”

scenario, while Scenario 2 may present a more realistic picture of the value of the Innibos

Festival.

34

6. Conclusions and recommendations The following conclusions can be made with regard to the survey:

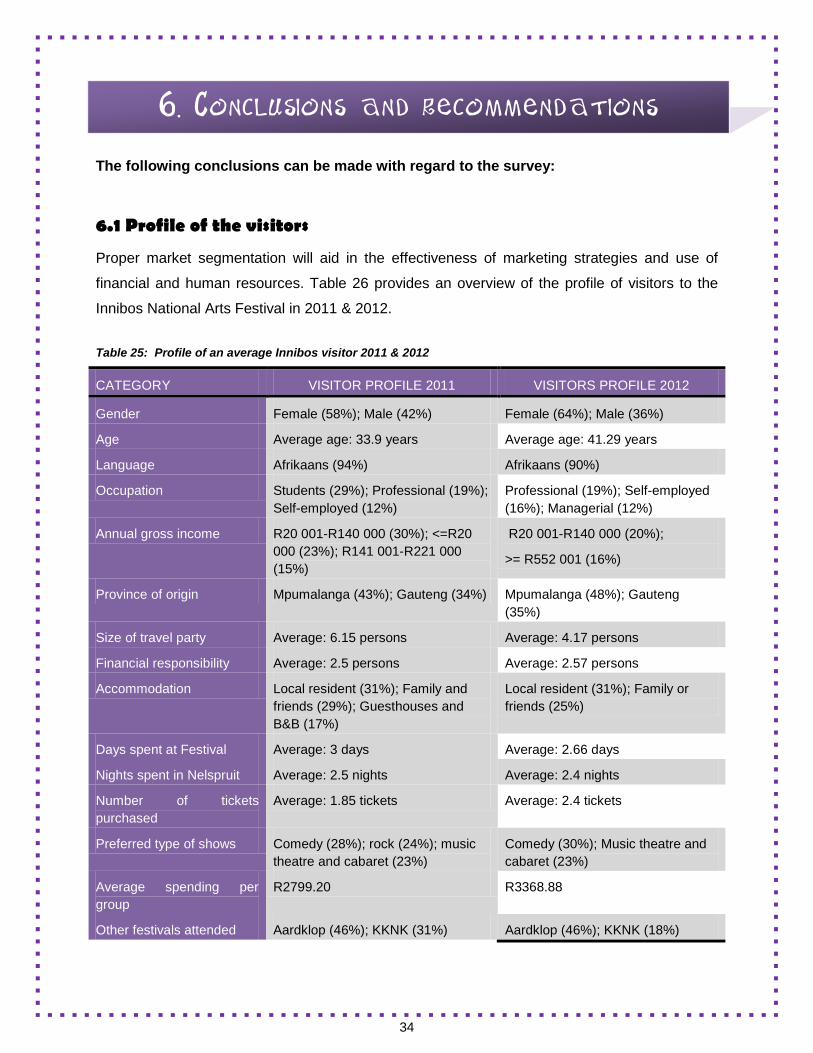

6.1 Profile of the visitors

Proper market segmentation will aid in the effectiveness of marketing strategies and use of

financial and human resources. Table 26 provides an overview of the profile of visitors to the

Innibos National Arts Festival in 2011 & 2012.

Table 25: Profile of an average Innibos visitor 2011 & 2012

CATEGORY VISITOR PROFILE 2011 VISITORS PROFILE 2012

Gender Female (58%); Male (42%) Female (64%); Male (36%)

Age Average age: 33.9 years Average age: 41.29 years

Language Afrikaans (94%) Afrikaans (90%)

Occupation Students (29%); Professional (19%); Self-employed (12%)

Professional (19%); Self-employed (16%); Managerial (12%)

Annual gross income R20 001-R140 000 (30%); <=R20 000 (23%); R141 001-R221 000 (15%)

R20 001-R140 000 (20%);

>= R552 001 (16%)

Province of origin Mpumalanga (43%); Gauteng (34%) Mpumalanga (48%); Gauteng (35%)

Size of travel party Average: 6.15 persons Average: 4.17 persons

Financial responsibility Average: 2.5 persons Average: 2.57 persons

Accommodation Local resident (31%); Family and friends (29%); Guesthouses and B&B (17%)

Local resident (31%); Family or friends (25%)

Days spent at Festival Average: 3 days Average: 2.66 days

Nights spent in Nelspruit Average: 2.5 nights Average: 2.4 nights

Number of tickets purchased

Average: 1.85 tickets Average: 2.4 tickets

Preferred type of shows Comedy (28%); rock (24%); music theatre and cabaret (23%)

Comedy (30%); Music theatre and cabaret (23%)

Average spending per group

R2799.20 R3368.88

Other festivals attended Aardklop (46%); KKNK (31%) Aardklop (46%); KKNK (18%)

35

Decision to attend Festival More than a month ago (43%); spontaneous decision (32%)

More than a month ago (43%); Spontaneous decision (31%)

Initiation of trip Self (60%); Friends (34%); Family (16%)

Self (49%); Friends (25%); Family (16%); Spouse (16%)

Preferred information source

Radio (56%); Television (47%); word-of-mouth (42%)

Radio (42%); Word-of-mouth (37%)

Number of visits to Festival Average: 2.52 times Average: 3.63 times

Main reason for attending the Festival

To relax (70%); Sociable event (70%); To spend time with friends (68%)

Sociable event (96%); To relax (93%); It is primarily an Afrikaans festival (90%)

Next year’s attendance 83% would definitely attend again Yes, definitely (92%)

Associated sponsors 94.2 Jakaranda; Standard Bank, Beeld

Jacaranda FM, Standard Bank, Beeld

Evaluation of the Festival Arts festivals such as Innibos make a contribution towards the arts in general (81%); It provides exposure to art forms/genres that generally do not get exposure (80); Arts festivals led to the number of artists increasing dramatically

Festival has to attract people further than just the surrounding areas (95%); Festival has to be an annual event (95%); Festival has to be at least three days long (94%); Festival has to cater to a variety of target markets, e.g. children, youth and families (93%)

THE FOLLOWING CONCLUSIONS CAN BE DRAWN FROM THE RESEARCH

COMPLETED AT THE INNIBOS NATIONAL ARTS FESTIVAL WITH REGARD TO THE

VISITOR PROFILE AND ECONOMIC IMPACT

• The majority of respondents to Innibos Arts Festival 2012 were Afrikaans-speaking females

in their early forties.

• Respondents were in a professional position at work, self-employed or in a managerial

position, where they earn either between R20 001 and R140 000 per annum, R140 001 and

R221 000 or more than R552 001.

• Respondents travelled from Mpumalanga or Gauteng in groups of four people, two to three

for whom they were financially responsible.

• The respondents travelling from far preferred to stay with family or friends in Nelspruit.

• An average of two tickets was purchased during the three days and respondents spent two

nights in the area.

• Comedy as well as musical theatre and cabaret were their preferred types of shows.

36

• Respondents are also of the view that the Festival makes a clear contribution to the growth

of arts in South Africa.

• Respondents mainly heard about the Festival on the radio or through word-of-mouth and

made the decision to visit the Festival for themselves more than a month before the Festival

started.

• Respondents visited this Festival four times on average, but they also indicated that they

attend other festivals, such as Aardklop National Arts Festival and KKNK.

• They will visit this Festival again.

• Innibos Arts Festival was attended because it is seen as a sociable event where visitors

can relax and enjoy everything that is Afrikaans.

• The main sponsors that were respondents recognised as part of the Festival was

Jacaranda FM, Standard Bank and Beeld.

• The festival generates approximately R70 million for the region.

• From the respondents’ point of view, a national arts festival should offer a variety of genres

(minimum five), based on at least 80 productions on an annual basis and the festival should

be at least three days long and attract 50 000 or more visitors.

• Most respondents had some degree of exposure to the arts during childhood, which

highlights the importance of children productions on the one hand, but also the importance

of parents taking children to such shows on the other hand.

THE FOLLOWING RECOMMENDATIONS WERE MADE BY THE FESTINOS

• Improve organisation at ticket sales

• Improve parking system

• Cheaper entrance fees

• Get a larger venue for the Festival

• Cheaper access and shows for children and pensioners

• Special smoking areas

• Improve signage at venues

• Improve management of dust

• More toilets

Related Documents