See important disclosures, including any required research certifications, beginning on page 21 ■ Investment case Keppel Land is Singapore’s third- largest listed residential and commercial property developer by total assets. We see deep value in the company, a positive fundamental outlook, and initiate coverage with a Buy (1) rating. We believe Keppel Land has a positive near-term and longer-term business outlook. Near-term, the recovery under way in Singapore’s office market should boost the capital values of its portfolio here (29.1% of our estimated gross asset value [GAV]). In the mid-to-long term, positive demographics and economic developments should support its residential property business in China (28.7% of our GAV) and other emerging Asia markets. Keppel Land’s share price has lagged the rallies of local developers and office REITs over the past 3 months, likely due to its significant China residential exposure, where news flow year-to-date has been poor. Our valuation assumptions factor in these concerns and we see it as trading at an attractive level. ■ Catalysts Key share-price catalysts include a stronger-than-expected Singapore office recovery, which should enhance further the value of Keppel Land’s office portfolio. Divestments of assets at favourable valuations, which could prompt it to distribute special dividends, along with encouraging residential news flow and sales in its key markets such as China and Singapore would also be positives. Our 2015-16E EPS are 11-18% below the Bloomberg consensus forecasts, reflecting mainly our cautious assumptions for Keppel Land’s China business. If China’s residential market were to see positive sentiment return, with steady prices and sales volumes, we believe there could be upside to our (and consensus) numbers. ■ Valuation Our 6-month target price is SGD4.08, based on a 20% discount (ie, 1SD below the Singapore developers’ past- 10-year mean discount to Daiwa’s SOTP values) applied to our SOTP value of SGD5.10/share. ■ Risks The main risks to our call are poor China economic and residential property news flow or sales, and a less robust-than-expected recovery in the Singapore office market. Financials / Singapore Keppel Land SP 14 May 2014 Keppel Land Initiation: unduly undervalued • Leveraged to positive near- and long-term property themes, a key beneficiary of current Singapore office market recovery • Looks substantially undervalued; trades at a 32% discount to our SOTP valuation and an end-1Q14 PBR of just 0.75x • Initiating with a Buy rating; our top pick among the large-cap Singapore property developers Source: FactSet, Daiwa forecasts Financials / Singapore Keppel Land KPLD SP Target (SGD): 4.080 Upside: 18.3% 14 May price (SGD): 3.450 Buy (initiation) Outperform Hold Underperform Sell 1 2 3 4 5 82 87 91 96 100 3.0 3.3 3.6 3.9 4.2 May-13 Aug-13 Nov-13 Feb-14 May-14 Share price performance KPLD (LHS) Relative to FSSTI (RHS) (SGD) (%) 12-month range 3.100-4.150 Market cap (USDbn) 4.26 3m avg daily turnover (USDm) 5.94 Shares outstanding (m) 1,546 Major shareholder Keppel Corp (54.6%) Financial summary (SGD) Year to 31 Dec 14E 15E 16E Revenue (m) 1,590 1,929 1,826 Operating profit (m) 420 350 353 Net profit (m) 417 409 427 Core EPS (fully-diluted) 0.270 0.265 0.276 EPS change (%) 7.3 (1.9) 4.3 Daiwa vs Cons. EPS (%) (0.0) (10.9) (18.3) PER (x) 12.8 13.0 12.5 Dividend yield (%) 2.6 2.6 2.6 DPS 0.090 0.090 0.090 PBR (x) 0.7 0.7 0.7 EV/EBITDA (x) 11.8 11.0 9.7 ROE (%) 5.8 5.4 5.4 Evon Tan, CFA (65) 6499 6546 [email protected] David Lum, CFA (65) 6329 2102 [email protected] How do we justify our view? How do we justify our view?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

See important disclosures, including any required research certifications, beginning on page 21

■ Investment case Keppel Land is Singapore’s third-largest listed residential and commercial property developer by total assets. We see deep value in the company, a positive fundamental outlook, and initiate coverage with a Buy (1) rating. We believe Keppel Land has a positive near-term and longer-term business outlook. Near-term, the recovery under way in Singapore’s office market should boost the capital values of its portfolio here (29.1% of our estimated gross asset value [GAV]). In the mid-to-long term, positive demographics and economic developments should support its residential property business in China (28.7% of our GAV) and other emerging Asia markets. Keppel Land’s share price has lagged the rallies of local developers and

office REITs over the past 3 months, likely due to its significant China residential exposure, where news flow year-to-date has been poor. Our valuation assumptions factor in these concerns and we see it as trading at an attractive level. ■ Catalysts Key share-price catalysts include a stronger-than-expected Singapore office recovery, which should enhance further the value of Keppel Land’s office portfolio. Divestments of assets at favourable valuations, which could prompt it to distribute special dividends, along with encouraging residential news flow and sales in its key markets such as China and Singapore would also be positives. Our 2015-16E EPS are 11-18% below the Bloomberg consensus forecasts, reflecting mainly our cautious assumptions for Keppel Land’s China business. If China’s residential market were to see positive sentiment return, with steady prices and sales volumes, we believe there could be upside to our (and consensus) numbers. ■ Valuation Our 6-month target price is SGD4.08, based on a 20% discount (ie, 1SD below the Singapore developers’ past-10-year mean discount to Daiwa’s SOTP values) applied to our SOTP value of SGD5.10/share.

■ Risks The main risks to our call are poor China economic and residential property news flow or sales, and a less robust-than-expected recovery in the Singapore office market.

Financials / SingaporeKeppel Land SP

14 May 2014

Keppel Land

Initiation: unduly undervalued

• Leveraged to positive near- and long-term property themes, a key beneficiary of current Singapore office market recovery

• Looks substantially undervalued; trades at a 32% discount to our SOTP valuation and an end-1Q14 PBR of just 0.75x

• Initiating with a Buy rating; our top pick among the large-cap Singapore property developers

Source: FactSet, Daiwa forecasts

Financials / Singapore

Keppel LandKPLD SP

Target (SGD): 4.080Upside: 18.3%14 May price (SGD): 3.450

Buy (initiation)

OutperformHoldUnderperformSell

1

2

3

4

5

82

87

91

96

100

3.0

3.3

3.6

3.9

4.2

May-13 Aug-13 Nov-13 Feb-14 May-14

Share price performance

KPLD (LHS) Relative to FSSTI (RHS)

(SGD) (%)

12-month range 3.100-4.150Market cap (USDbn) 4.263m avg daily turnover (USDm) 5.94Shares outstanding (m) 1,546Major shareholder Keppel Corp (54.6%)

Financial summary (SGD)Year to 31 Dec 14E 15E 16ERevenue (m) 1,590 1,929 1,826Operating profit (m) 420 350 353Net profit (m) 417 409 427Core EPS (fully-diluted) 0.270 0.265 0.276EPS change (%) 7.3 (1.9) 4.3Daiwa vs Cons. EPS (%) (0.0) (10.9) (18.3)PER (x) 12.8 13.0 12.5Dividend yield (%) 2.6 2.6 2.6DPS 0.090 0.090 0.090PBR (x) 0.7 0.7 0.7EV/EBITDA (x) 11.8 11.0 9.7ROE (%) 5.8 5.4 5.4

Evon Tan, CFA(65) 6499 [email protected]

David Lum, CFA(65) 6329 [email protected]

How do we justify our view?How do we justify our view?

Financials / Singapore KPLD SP 14 May 2014

- 2 -

Unduly undervalued ....................................................................................................................... 6

Initiating with a Buy rating and target price of SGD4.08 .......................................................... 6

Singapore office: top grade exposure .......................................................................................... 7

China residential: driving profits in coming years ..................................................................... 9

Singapore residential: valuable plots ......................................................................................... 11

Other overseas markets ............................................................................................................. 13

Fund management: growing steadily ........................................................................................ 14

Hotels and resorts: non-core ..................................................................................................... 15

Valuation .................................................................................................................................... 15

Catalysts ..................................................................................................................................... 16

Risks ........................................................................................................................................... 16

Appendix ........................................................................................................................................ 18

Company background ................................................................................................................ 18

Contents

Financials / Singapore KPLD SP 14 May 2014

- 3 -

Growth outlook Singapore office: prime grade-A capital values (SGD/sq ft)

We believe Keppel Land offers a positive business outlook both in the short term and long term. In the short term, the recovery under way in Singapore’s office market (see chart at right) should boost the capital values of Keppel Land’s portfolio here (29.1% of our estimated GAV). In the medium-to-longer term, positive demographics and economic development should support its residential development business in China (28.7% of our estimated GAV) as well as other emerging Asia markets where it has a presence (eg, Vietnam and Indonesia). Source: Jones Lang LaSalle, Daiwa forecasts

Valuation Keppel Land: rolling PBR bands (x)

We derive our 6-month target price of SGD4.08 by applying a 20% discount to our SOTP valuation of SGD5.10/share. Our 20% discount is at 1SD below the Singapore property developers’ past-10-year mean discount to Daiwa’s SOTP values. We see this as fair given that the physical residential markets in both Singapore and China are weak currently. We see deep value in Keppel Land, both on an SOTP and PBR basis. Based on the company’s BVPS as at the end of 1Q14, the stock is trading currently at a PBR of just 0.75x, above 0.6x, which represents 1SD below its past-10-year average trading range.

Source: Bloomberg, Daiwa

Earnings revisions Keppel Land: EPS forecasts – Daiwa vs. consensus

Since the start of 2014, the Bloomberg-consensus EPS forecasts have been cut by 8.5% for 2014 and 7.2% for 2015, and raised by 4.6% for 2016. Our core EPS forecasts are in line with those of the consensus for 2014and 11-18% below those for 2015-16. We believe this is because we factor in 20% ASP declines over the 2014-16 period, in view of market concerns about China’s residential market. If the company’s China ASPs were to remain steady or decline less than we expect, there could be upside to our (and consensus) forecasts. Source: Bloomberg, Daiwa forecasts

How do we justify our view?

Growth outlook

Valuation

Earnings revisions

2,900

1,700

2,620

500

1,000

1,500

2,000

2,500

3,000

3,500

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

0

2

4

6

8

10

12

Jan-

04M

ay-0

4O

ct-0

4M

ar-0

5Au

g-05

Jan-

06Ju

n-06

Nov-

06Ap

r-07

Sep-

07Fe

b-08

Jul-0

8De

c-08

May

-09

Oct

-09

Feb-

10Ju

l-10

Dec-

10M

ay-1

1O

ct-1

1M

ar-1

2Au

g-12

Jan-

13Ju

n-13

Nov-

13Ap

r-14

KPLD SP 0.02x 0.60x1.19x 1.78x 2.36x

0.27 0.26 0.280.270.30

0.340.30

0.34 0.35

0.00

0.10

0.20

0.30

0.40

2014E 2015E 2016E

Daiwa - core EPSBloomberg consensus (as of 08-May-14)Daiwa - ex cluding assumption of 20% ASP cut

(SGD)

Buy (initiation)

OutperformHoldUnderperformSell

1

2

3

4

5

Financials / Singapore KPLD SP 14 May 2014

- 4 -

Key assumptions

Profit and loss (SGDm)

Cash flow (SGDm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2009 2010 2011 2012 2013 2014E 2015E 2016EEBITDA margin (%) - Property trading 19.6 22.5 17.3 17.2 15.7 24.1 14.9 15.8

EBITDA margin (%) - Property investment

66.7 69.2 60.9 71.2 52.6 61.8 61.7 61.7

EBITDA margin (%) - Fund management

56.1 73.7 58.8 61.1 55.5 58.3 58.3 58.3

EBITDA margin (%) - Hotels and resorts

(4.9) (1.0) 19.6 18.6 30.7 20.0 20.0 20.0

EBITDA margin (%) - Overall 22.9 29.9 20.6 23.6 19.0 27.3 18.9 20.1

Year to 31 Dec 2009 2010 2011 2012 2013 2014E 2015E 2016EProperty Trading 721 473 708 724 1,231 1,359 1,685 1,568Property Investment 75 70 80 56 49 51 53 56Other Revenue 128 142 161 158 182 180 191 202Total Revenue 924 685 949 939 1,461 1,590 1,929 1,826Other income 0 6 22 31 19 19 19 19COGS (602) (392) (636) (625) (1,047) (1,006) (1,376) (1,282)SG&A (110) (94) (140) (123) (154) (168) (207) (195)Other op.expenses (9) (9) (9) (11) (15) (15) (15) (15)Operating profit 202 196 187 211 263 420 350 353Net-interest inc./(exp.) (10) (14) (5) (1) 3 3 3 3Assoc/forex/extraord./others 166 995 1,295 777 735 307 326 280Pre-tax profit 359 1,177 1,477 987 1,001 729 679 635Tax (59) (119) (71) (122) (97) (144) (137) (133)Min. int./pref. div./others (19) (5) (31) (27) (18) (40) (29) (33)Net profit (reported) 280 1,053 1,375 838 886 545 513 470Net profit (adjusted) 281 624 755 439 389 417 409 427EPS (reported)(SGD) 0.242 0.733 0.938 0.555 0.573 0.353 0.332 0.304EPS (adjusted)(SGD) 0.243 0.434 0.515 0.291 0.252 0.270 0.265 0.276EPS (adjusted fully-diluted)(SGD) 0.243 0.434 0.514 0.291 0.252 0.270 0.265 0.276DPS (SGD) 0.080 0.180 0.200 0.120 0.130 0.090 0.090 0.090EBIT 202 196 187 211 263 420 350 353EBITDA 211 205 196 222 278 435 365 368

Year to 31 Dec 2009 2010 2011 2012 2013 2014E 2015E 2016EProfit before tax 359 1,177 1,477 987 1,001 729 679 635Depreciation and amortisation 9 9 9 11 15 15 15 15Tax paid 7 (57) (52) (46) (69) (140) (136) (132)Change in working capital 318 (1,286) (1,101) (831) (1,592) (294) 803 210Other operational CF items (180) (995) (1,271) (769) (722) (298) (318) (271)Cash flow from operations 513 (1,152) (938) (647) (1,367) 12 1,044 457Capex (80) (272) (133) (37) (88) (100) (100) (100)Net (acquisitions)/disposals (337) 727 1,035 (329) (13) 0 n.a. 0Other investing CF items 72 231 113 316 217 0 0 0Cash flow from investing (344) 686 1,014 (50) 116 (100) n.a. (100)Change in debt (382) 809 482 545 940 0 0 0Net share issues/(repurchases) 701 3 3 2 1 0 0 0Dividends paid (11) (44) (106) (129) (185) (139) (139) (139)Other financing CF items (177) 411 (109) (40) 164 0 0 0Cash flow from financing 130 1,179 270 377 920 (139) (139) (139)Forex effect/others 0 0 0 0 0 0 0 0Change in cash 299 714 347 (320) (332) (227) n.a. 218Free cash flow 433 (1,423) (1,071) (684) (1,455) (88) 944 357

Financial summary

Financials / Singapore KPLD SP 14 May 2014

- 5 -

Balance sheet (SGDm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

Company profile

Keppel Land is the property arm of the Singapore conglomerate, Keppel Group. Its major activities are property development, property investment, property-fund management, and the management of hotels and leisure/holiday resorts. Core countries of focus are Singapore and China; while the company also operates in Vietnam, Indonesia, and other parts of Asia.

As at 31 Dec 2009 2010 2011 2012 2013 2014E 2015E 2016ECash & short-term investment 893 1,589 1,942 1,597 1,285 1,058 1,863 2,082Inventory 4 3 4 4 5 5 5 5Accounts receivable 430 722 781 721 444 444 444 444Other current assets 1,152 2,538 3,535 4,159 6,392 6,686 5,882 5,672Total current assets 2,478 4,853 6,262 6,481 8,126 8,193 8,195 8,203Fixed assets 1,633 1,906 838 1,591 1,894 1,992 2,084 2,177Goodwill & intangibles 0 0 0 0 0 0 0 0Other non-current assets 2,441 1,973 2,910 3,390 3,802 4,088 4,398 4,661Total assets 6,552 8,732 10,009 11,461 13,823 14,273 14,677 15,041Short-term debt 823 317 201 715 283 283 283 283Accounts payable 715 1,455 1,438 1,459 1,786 1,786 1,786 1,786Other current liabilities 223 140 130 142 157 157 157 157Total current liabilities 1,761 1,912 1,770 2,315 2,226 2,226 2,226 2,226Long-term debt 904 2,200 2,336 2,349 3,870 3,870 3,870 3,870Other non-current liabilities 99 35 33 151 241 246 247 248Total liabilities 2,763 4,147 4,138 4,814 6,337 6,341 6,343 6,344Share capital 1,988 2,061 2,220 2,393 2,398 2,398 2,398 2,398Reserves/R.E./others 1,388 2,215 3,355 3,776 4,591 4,997 5,371 5,702Shareholders' equity 3,376 4,276 5,575 6,169 6,989 7,395 7,769 8,100Minority interests 413 309 296 477 496 536 565 598Total equity & liabilities 6,552 8,732 10,009 11,461 13,823 14,273 14,677 15,041EV 4,207 4,709 3,544 4,136 5,128 5,109 4,023 3,574Net debt/(cash) 834 927 595 1,467 2,868 3,095 2,290 2,071BVPS (SGD) 2.361 2.948 3.742 3.995 4.521 4.784 5.026 5.240

Year to 31 Dec 2009 2010 2011 2012 2013 2014E 2015E 2016ESales (YoY) n.a. (25.8) 38.5 (1.1) 55.6 8.8 21.4 (5.4)EBITDA (YoY) n.a. (3.0) (4.6) 13.4 25.4 56.2 (16.0) 0.7Operating profit (YoY) n.a. (2.9) (4.7) 12.9 24.7 59.4 (16.6) 0.7Net profit (YoY) n.a. 122.0 20.8 (41.8) (11.4) 7.1 (1.9) 4.3Core EPS (fully-diluted) (YoY) n.a. 78.6 18.5 (43.5) (13.4) 7.3 (1.9) 4.3Gross-profit margin 34.8 42.8 33.0 33.5 28.3 36.7 28.7 29.8EBITDA margin 22.9 29.9 20.6 23.6 19.0 27.3 18.9 20.1Operating-profit margin 21.9 28.6 19.7 22.5 18.0 26.4 18.2 19.3Net profit margin 30.4 91.1 79.5 46.8 26.7 26.2 21.2 23.4ROAE 16.7 16.3 15.3 7.5 5.9 5.8 5.4 5.4ROAA 8.6 8.2 8.1 4.1 3.1 3.0 2.8 2.9ROCE 7.3 3.1 2.4 2.3 2.5 3.5 2.9 2.8ROIC 7.3 3.5 3.0 2.5 2.6 3.1 2.6 2.6Net debt to equity 24.7 21.7 10.7 23.8 41.0 41.8 29.5 25.6Effective tax rate 16.5 10.1 4.8 12.4 9.7 19.8 20.2 20.9Accounts receivable (days) 84.8 306.6 289.0 291.9 145.5 102.0 84.0 88.8Current ratio (x) 1.4 2.5 3.5 2.8 3.7 3.7 3.7 3.7Net interest cover (x) 20.6 14.1 40.2 287.1 n.a. n.a. n.a. n.a.Net dividend payout 33.0 24.6 21.3 21.6 22.7 25.5 27.1 29.6Free cash flow yield 8.1 n.a. n.a. n.a. n.a. n.a. 17.7 6.7

Financial summary continued …

Financials / Singapore KPLD SP 14 May 2014

- 6 -

Unduly undervalued

We see deep value in Keppel Land and believe it is a key beneficiary of the current upturn in the Singapore office market. Longer-term, we see positive fundamental outlooks for the residential property markets in which it operates.

Initiating with a Buy rating and target price of SGD4.08

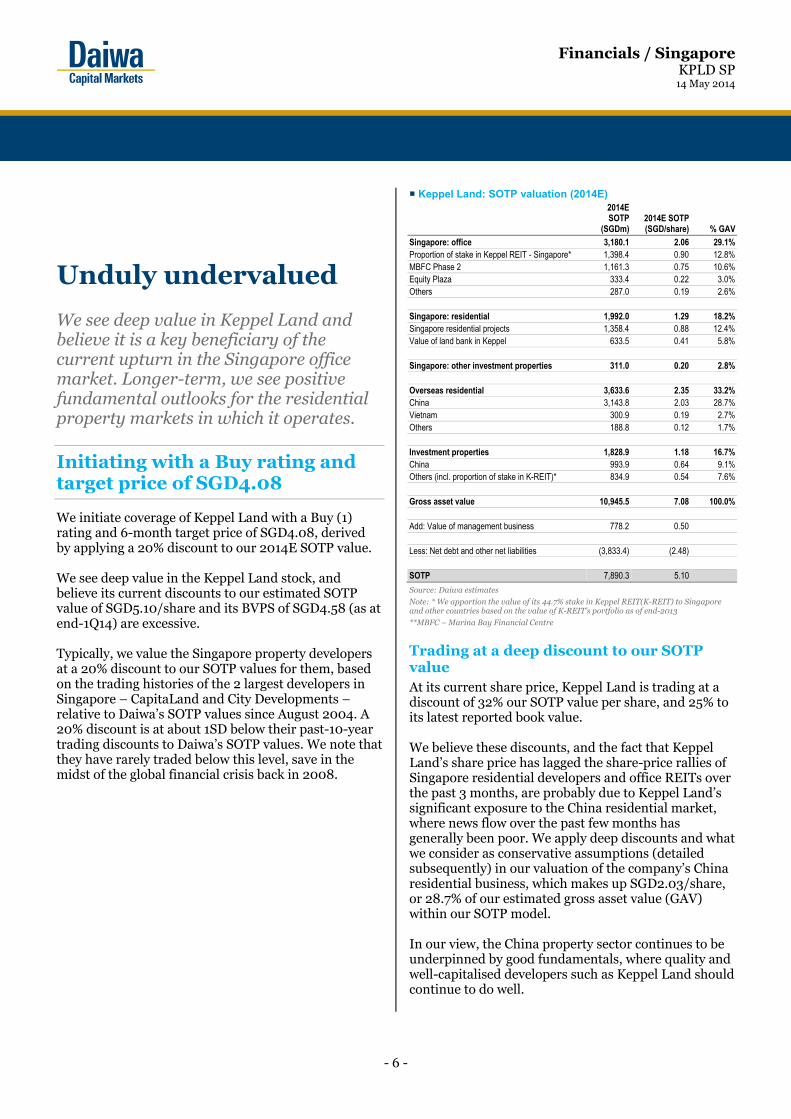

We initiate coverage of Keppel Land with a Buy (1) rating and 6-month target price of SGD4.08, derived by applying a 20% discount to our 2014E SOTP value. We see deep value in the Keppel Land stock, and believe its current discounts to our estimated SOTP value of SGD5.10/share and its BVPS of SGD4.58 (as at end-1Q14) are excessive. Typically, we value the Singapore property developers at a 20% discount to our SOTP values for them, based on the trading histories of the 2 largest developers in Singapore – CapitaLand and City Developments – relative to Daiwa’s SOTP values since August 2004. A 20% discount is at about 1SD below their past-10-year trading discounts to Daiwa’s SOTP values. We note that they have rarely traded below this level, save in the midst of the global financial crisis back in 2008.

Keppel Land: SOTP valuation (2014E) 2014E SOTP

(SGDm) 2014E SOTP (SGD/share) % GAV

Singapore: office 3,180.1 2.06 29.1%Proportion of stake in Keppel REIT - Singapore* 1,398.4 0.90 12.8%MBFC Phase 2 1,161.3 0.75 10.6%Equity Plaza 333.4 0.22 3.0%Others 287.0 0.19 2.6% Singapore: residential 1,992.0 1.29 18.2%Singapore residential projects 1,358.4 0.88 12.4%Value of land bank in Keppel 633.5 0.41 5.8% Singapore: other investment properties 311.0 0.20 2.8% Overseas residential 3,633.6 2.35 33.2%China 3,143.8 2.03 28.7%Vietnam 300.9 0.19 2.7%Others 188.8 0.12 1.7% Investment properties 1,828.9 1.18 16.7%China 993.9 0.64 9.1%Others (incl. proportion of stake in K-REIT)* 834.9 0.54 7.6% Gross asset value 10,945.5 7.08 100.0% Add: Value of management business 778.2 0.50 Less: Net debt and other net liabilities (3,833.4) (2.48) SOTP 7,890.3 5.10

Source: Daiwa estimates

Note: * We apportion the value of its 44.7% stake in Keppel REIT(K-REIT) to Singapore and other countries based on the value of K-REIT’s portfolio as of end-2013

**MBFC – Marina Bay Financial Centre

Trading at a deep discount to our SOTP value At its current share price, Keppel Land is trading at a discount of 32% our SOTP value per share, and 25% to its latest reported book value. We believe these discounts, and the fact that Keppel Land’s share price has lagged the share-price rallies of Singapore residential developers and office REITs over the past 3 months, are probably due to Keppel Land’s significant exposure to the China residential market, where news flow over the past few months has generally been poor. We apply deep discounts and what we consider as conservative assumptions (detailed subsequently) in our valuation of the company’s China residential business, which makes up SGD2.03/share, or 28.7% of our estimated gross asset value (GAV) within our SOTP model. In our view, the China property sector continues to be underpinned by good fundamentals, where quality and well-capitalised developers such as Keppel Land should continue to do well.

Financials / Singapore KPLD SP 14 May 2014

- 7 -

A key beneficiary of current Singapore office market upturn Keppel Land’s Singapore office business makes up 29.3% of our estimated GAV for the company, representing the highest proportion of our SOTP value for the Singapore property developers under our coverage. We are positive on the Singapore office sector for 2014, and see Keppel Land as a key beneficiary in the developer space of the current office market upturn. Potential for special dividends when divestments take place Keppel Land’s dividend policy is to distribute up to one-third of net realised profits to shareholders. The company has paid out higher dividends in the past when it divested or restructured its stakes in various assets, and we see the potential for a special dividend payout if it has gains from the sale of any major assets going forward, such as MBFC Phase 2.

Keppel Land: dividend history Ordinary

dividends (SGD/share)

Special dividend

(SGD/share)

Total dividend

(SGD/share) Major asset sales in the year 2007 0.08 0.12 0.20 Divested its one-third stake in One Raffles

Quay for a net gain of SGD221.6m 2008 0.08 0.08 2009 0.08 0.08 2010 0.09 0.09 0.18 Sold its 1/3 stake in MBFC Phase 1 for

SGD1,426.8m for a net gain of SGD321m (Note: purchased Keppel Towers and GE Towers from KREIT at same time)

2011 0.20 0.20 Divested an 82.5% stake in Ocean Financial Centre at a valuation of SGD2,013m (SGD2,600/sq ft) for a net gain of SGD492.7m (with an option to acquire stake back at end of 99 years)

2012 0.12 0.12 2013 0.13 0.13

Source: Company, Bloomberg, Daiwa

* Note: Dividends are not adjusted for capital changes

Valuation: major Singapore residential developers

Company BBG code Market cap

(USDbn)

Share price (local curr.)

as of 14-May-14 Rating Daiwa NAVTrading prem/

(disc) to NAV (%)PBR (x) PER (x) ROE (%) Yield (%)

FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15ECapitaland Ltd CAPL SP 10.6 3.13 Hold 3.87 -19.1% 0.78 0.75 11.7 11.1 6.9 7.0 2.9 3.0City Developments Ltd CIT SP 7.8 10.80 Outperform 14.4 -25.0% 1.23 1.15 16.2 14.5 7.8 8.2 1.5 1.9Frasers Centrepoint Ltd FCL SP 4.2 1.82 Buy 2.62 -30.5% 0.80 0.76 9.7 11.3 9.0 6.9 2.9 2.9Keppel Land Ltd Keppel Land SP 4.3 3.45 Buy 5.1 -32.4% 0.72 0.69 12.8 13.0 5.8 5.4 2.6 2.6Source: Bloomberg, Daiwa forecasts

Singapore office: top grade exposure

In our view, Keppel Land has, among the highest-quality and largest office exposure of the Singapore listed property developers. This is held through its 44.7% interest in Keppel REIT (KREIT SP, SGD1.23, Outperform [2]) and its direct stakes in several buildings in downtown Singapore. The office sector – a bright spot in 2014 We are positive on the Singapore office sector, and believe that unlike the trend for other segments of the property sector, Singapore office rents look set to appreciate in 2014. We forecast annual average (CBD prime grade-A) rents to increase by 5.4% YoY for 2014 and 6% YoY for 2015, after a reported decline of 0.7% YoY for 2013. While our base scenario is for fairly muted growth compared with previous recoveries, we see upside potential for office rents if there is office-space demand from large occupiers new to Singapore.

For further details on the outlook for the Singapore office real-estate market, please see our report on Singapore Office REITs, A bright spot in 2014, published on 18 February 2014. KREIT – loaded with grade-A assets With 87.5% of its SGD7.2bn total portfolio as of end-2013 in grade-A Singapore office properties including Marina Bay Financial Centre (MBFC) Phase 1, Ocean Financial Centre, and One Raffles Quay, KREIT (and by proxy, Keppel Land) is a prime beneficiary of the current upturn in the Singapore office sector. The REIT also holds a few grade-A office properties in Australia.

Financials / Singapore KPLD SP 14 May 2014

- 8 -

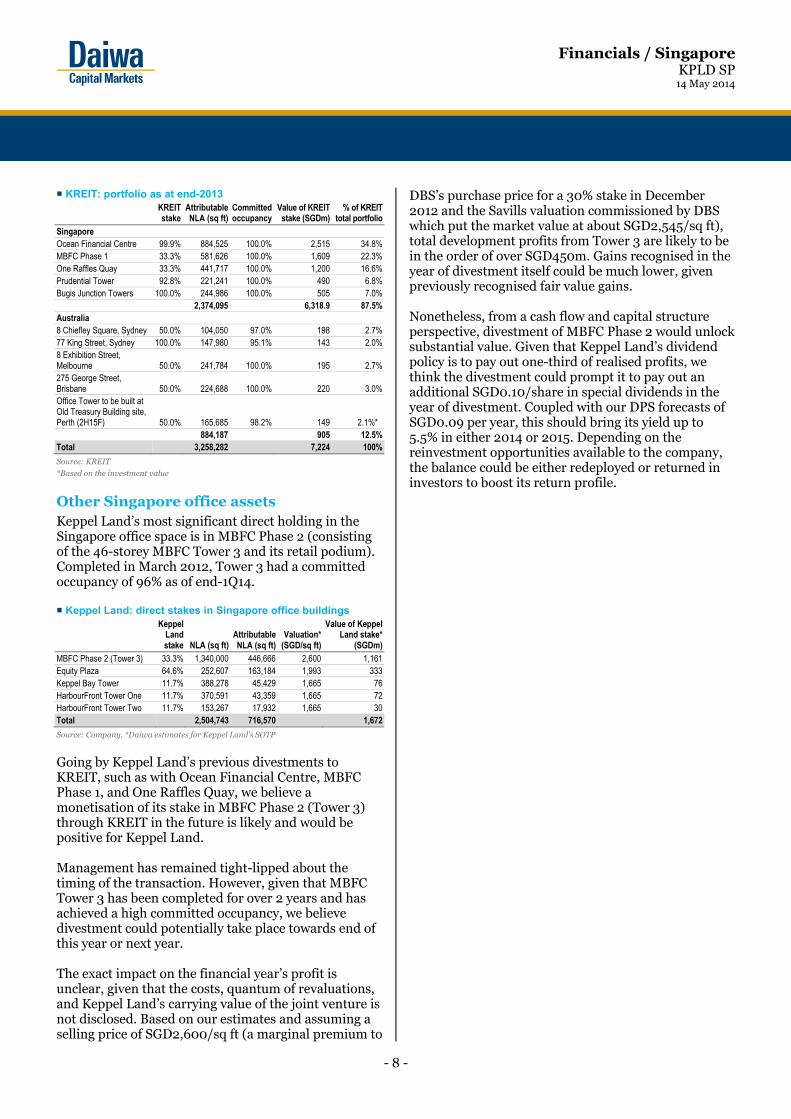

KREIT: portfolio as at end-2013 KREIT stake

Attributable NLA (sq ft)

Committed occupancy

Value of KREIT stake (SGDm)

% of KREIT total portfolio

Singapore Ocean Financial Centre 99.9% 884,525 100.0% 2,515 34.8%MBFC Phase 1 33.3% 581,626 100.0% 1,609 22.3%One Raffles Quay 33.3% 441,717 100.0% 1,200 16.6%Prudential Tower 92.8% 221,241 100.0% 490 6.8%Bugis Junction Towers 100.0% 244,986 100.0% 505 7.0%

2,374,095 6,318.9 87.5%Australia 8 Chiefley Square, Sydney 50.0% 104,050 97.0% 198 2.7%77 King Street, Sydney 100.0% 147,980 95.1% 143 2.0%8 Exhibition Street, Melbourne 50.0% 241,784 100.0% 195 2.7%275 George Street, Brisbane 50.0% 224,688 100.0% 220 3.0%Office Tower to be built at Old Treasury Building site, Perth (2H15F) 50.0% 165,685 98.2% 149 2.1%*

884,187 905 12.5%Total 3,258,282 7,224 100%

Source: KREIT

*Based on the investment value

Other Singapore office assets Keppel Land’s most significant direct holding in the Singapore office space is in MBFC Phase 2 (consisting of the 46-storey MBFC Tower 3 and its retail podium). Completed in March 2012, Tower 3 had a committed occupancy of 96% as of end-1Q14. Keppel Land: direct stakes in Singapore office buildings

Keppel Land stake NLA (sq ft)

Attributable NLA (sq ft)

Valuation* (SGD/sq ft)

Value of Keppel Land stake*

(SGDm)MBFC Phase 2 (Tower 3) 33.3% 1,340,000 446,666 2,600 1,161Equity Plaza 64.6% 252,607 163,184 1,993 333Keppel Bay Tower 11.7% 388,278 45,429 1,665 76HarbourFront Tower One 11.7% 370,591 43,359 1,665 72HarbourFront Tower Two 11.7% 153,267 17,932 1,665 30Total 2,504,743 716,570 1,672

Source: Company, *Daiwa estimates for Keppel Land's SOTP

Going by Keppel Land’s previous divestments to KREIT, such as with Ocean Financial Centre, MBFC Phase 1, and One Raffles Quay, we believe a monetisation of its stake in MBFC Phase 2 (Tower 3) through KREIT in the future is likely and would be positive for Keppel Land. Management has remained tight-lipped about the timing of the transaction. However, given that MBFC Tower 3 has been completed for over 2 years and has achieved a high committed occupancy, we believe divestment could potentially take place towards end of this year or next year. The exact impact on the financial year’s profit is unclear, given that the costs, quantum of revaluations, and Keppel Land’s carrying value of the joint venture is not disclosed. Based on our estimates and assuming a selling price of SGD2,600/sq ft (a marginal premium to

DBS’s purchase price for a 30% stake in December 2012 and the Savills valuation commissioned by DBS which put the market value at about SGD2,545/sq ft), total development profits from Tower 3 are likely to be in the order of over SGD450m. Gains recognised in the year of divestment itself could be much lower, given previously recognised fair value gains. Nonetheless, from a cash flow and capital structure perspective, divestment of MBFC Phase 2 would unlock substantial value. Given that Keppel Land’s dividend policy is to pay out one-third of realised profits, we think the divestment could prompt it to pay out an additional SGD0.10/share in special dividends in the year of divestment. Coupled with our DPS forecasts of SGD0.09 per year, this should bring its yield up to 5.5% in either 2014 or 2015. Depending on the reinvestment opportunities available to the company, the balance could be either redeployed or returned in investors to boost its return profile.

Financials / Singapore KPLD SP 14 May 2014

- 9 -

China residential: driving profits in coming years

Keppel Land entered China in the 1990s, and ventured into residential development there with Shanghai in 2000. Its foray into township developments (large-scale self-contained neighbourhoods, offering reasonably priced homes amidst a comprehensive range of amenities, with convenient mass-transport connectivity to the city and surrounding areas) from 2003 has been a major driver for its presence in China. At the end of 2013, Keppel Land had sold over 22,000 homes and completed more than 20,000 homes in China. Constructive house view on China property Our China property analysts have a positive view on the China property sector, seeing continued revenue and

profit-making opportunities for strong players given that demand remains well-supported by deepening urbanisation and rising income levels. In their view, demand will support prices in tier 1-2 cities, and over-supply is occurring mainly in some tier-2 and tier-3 cities (with differentiation by districts within those cities as well). Within China, Keppel focuses on the following tier 1-2 cities – Shanghai, Beijing, Chengdu, Wuxi, and Tianjin. While bank credit has continued to tighten, our China property and banking analysts believe the banks will remain supportive of quality developers and home buyers. A massive landbank in China As of the end of 1Q14, Keppel Land had a landbank in China of almost 7.7m sq m in GFA, with 37,980 units totalling 5.6m sq m in area in its residential landbank.

Keppel Land: China residential landbank (including townships) as of end-1Q14

Project Location Keppel Land

stake Total land area (sq m) Total GFA (sq m) Remaining area for sale (sq m) Remaining units for sale*

8 Park Avenue Shanghai 99% 33,432 133,393 44,761 240The Springdale Shanghai 99.40% 264,090 264,090 * 62,089 ^ 354Seasons Residence Shanghai 99.90% 71,621 122,351 104,102 920Landed Devt, Sheshan Shanghai 100% 175,000 85,000 85,000 200Waterfront Residence Nantong 100% 172,215 189,437 * 189,437 * 1,199Central Park City Wuxi 49.70% 352,534 670,931 261,075 ^ 1,762Waterfront Residence Wuxi 100% 215,230 322,844 322,844 2,500Mixed-Use Devt Wuxi 100% 66,010 165,025 * 165,025 1,135Stamford City Jiangyin 99.40% 82,987 299,802 ^ 128,061 ^ 673The Botanica Chengdu 44.05% 419,775 1,049,438 ^ 20,077 ^ 143Park Avenue Heights Chengdu 100% 50,782 203,129 170,030 1,235Hill Crest Villa Chengdu 100% 249,330 163,147 163,147 274Serenity Villa Chengdu 100% 286,667 238,112 238,112 573The Seasons Shenyang 100% 348,312 365,186 * 344,385 ^ 2,551Hunnan Township Development Shenyang 99.80% 302,681 756,580 756,580 7,026Serenity Villa Tianjin 100% 128,685 80,000 78,777 333Mixed-use Devt Tianjin 100% 1,666,665 1,358,202 1,358,202 11,299Tianjin Eco-City Tianjin 55% 365,722 633,798 * 540,308 * 3,427Landed Development Tianjin 100% 103,683 60,472 60,472 346Integrated Marina Lifestyle Devt Zhongshan 80% 891,752 460,000 460,000 1,647Hill Crest Residence (Ph 1) Kunming 68.80% 71,920 20,193 3,346 18Hill Crest Residence (Ph 2) Kunming 68.80% 99,759 24,428 24,637 112La Quinta II Kunming 68.80% 23,034 10,928 2,223 13Total 6,441,886 7,676,486 5,582,690 37,980

Source: Company

Note: * Includes commercial area; ^ excludes commercial area

Financials / Singapore KPLD SP 14 May 2014

- 10 -

Of these 37,980 units, 14,909 are part of township developments. While Keppel Land has not added any new township sites since 2009, with long gestation periods and multiple development phases for these projects, township developments still represent a significant part of Keppel Land's China residential exposure. Keppel Land: China township developments

Year announced Name City

Size of site (ha)

Number of units

(Total)

Remaining units of as end 1Q14

2003 The Botanica Chengdu 42.0 9,664 1432005 Central Park City Wuxi 35.3 5,182 1,7622007 The Seasons Shenyang 24.0 2,794 2,5512008 Tianjin Eco-City Tianjin 36.0 4,354 3,4272009 Hunnan Township Development Shenyang 30.3 7,026 7,026Total 167.6 29,020 14,909

Source: Company, Daiwa

Value of China sales almost quadrupled in 2013; ASP of overall sales rising Keppel Land’s China residential business had a stellar 2013, selling 3,870 units, more than double the units it did in 2012, with the value of sales almost quadrupling to reach CNY5.4bn, helped by a significant jump in the average ASP of units sold due to the mix of units sold as well as ASP increases. Keppel Land: China residential sales

2011 2012 2013 1Q14Units sold 1,400 1,650 3,870 570 Area sold (sq m) 144,200 162,000 411,500 62,000 Sales value (CNYm) 1,240 1,417 5,390 890 Average ASP (CNY/sq m) 8,599 8,747 13,098 14,355 Source: Company, Daiwa

1Q14 sales came in at 570 units, down 33% YoY vs. 1Q13, although sales value actually rose by 6% as the average ASP of its sales mix continued to rise. Exceptional margins on a number of projects According to our estimates, Keppel Land generates very high margins on some of its projects, which we believe will help to sustain the company’s overall profitability when revenue from these projects is recognised upon their sale and completion. 8 Park Avenue. One of the first sites acquired by Keppel Land in China, the 33,432sqm site (which yields an estimated total GFA of 133,393sqm) cost SGD80m in 2000. Six towers totalling 552 units have already been fully sold and handed over to buyers. At its current ASP of CNY72,000/sq m, we estimate a margin on cost in excess of 500% for units currently being sold at the remaining four towers (which total 366 units).

Eight units were sold at the project in 1Q14, and at the end of the quarter, 240 units remained for sale. Two of these 4 towers were completed in 2013, with another 2 due to be completed in 2016. The Botanica (Phase 7). The land cost for the 42-ha Botanica township site was CNY441m in 2003. The final phase of the 9,664-unit development is due to be completed in 2Q14, with just 184 units remaining unsold as of end-1Q14. Applying the ASP of CNY8,500/sq m achieved for Phase 3 in 2013, we estimate a margin on cost of over 150% for units in the last phase. Stamford City. Keppel Land announced the acquisition of the Jiangyin site for Stamford City in 2006. The 82,987sq m site, with a total GFA of 299,802sq m (excluding commercial area) was purchased for CNY460.3m. Applying the ASP of CNY9,500/sq m achieved for Phase 3 in 2013, we estimate a margin on cost of over 90% for units now being sold at the project. At Stamford City, a phase totalling 155 units was completed in 1Q14, with a further 616 units expected to be completed within the next 2 years. Discounting Keppel Land’s China residential business: our basis To address investors’ continued concerns about the China residential market, we apply a number of deep discounts and conservative estimates (in our view) to derive our numbers for Keppel Land’s residential business in China. Namely, we assume:

• A 20% discount to project ASPs, where disclosed by the company or consultant estimates of ASPs for the area/housing type are available (although the company has not generally noted declines in ASPs and has typically been able to launch new phases of projects at higher ASPs than previous phases).

• On other projects where we do not have reliable ASP estimates (mainly for sites under planning/review), we account for them at cost.

• A 50% haircut on the development profits that we expect to be recognised beyond 2018.

After discounting the above, we derive a valuation of SGD2.03/share for Keppel Land’s China residential business, representing 28.7% of our GAV.

Financials / Singapore KPLD SP 14 May 2014

- 11 -

Singapore residential: valuable plots

In Singapore, Keppel Land is known for having developed a portfolio of mid to high-end projects, especially in the Keppel Bay precinct where it obtained land through the moving out of the old Keppel Shipyard in 1999. The company has also participated very selectively in government land sales (GLS) tenders in recent years. Keppel Land: Singapore residential projects under development and launched as of end-2013

Name

Keppel Land's

effective interest

No of units

(total)

% sold as at end 2013**

Unsold units at

end 2013

% completed

as of end 2013

Estimated completion

The Lakefront Residences 100.0% 629 100.0% 0 85.0% 2015The Luxurie 100.0% 622 100.0% 0 45.3% 2015The Glades 70.0% 726 16.5% 606 0.0% 2017Corals at Keppel Bay 30.0% 366 46.2% 197 12.3% 2018Reflections at Keppel Bay* 30.0% 975 93.3% 65 100.0% CompletedMarina Bay Suites 33.3% 221 91.9% 18 100.0% 2013Total 3,539 75.0% 886

Source: Company, Daiwa

* Excludes 154 units set aside for corporate residences

** Based on number of units sold and not area sold, and thus may differ from Keppel Land disclosure.

The company’s landbank consists of minority stakes in the remaining residential sites that have not been launched around Keppel Bay and a 100% interest in Keppel Towers & GE Towers (KTGE), a freehold office building in the Tanjong Pagar area acquired from KREIT in 2010, slated for residential redevelopment. Keppel Land also acquired a site in Kim Tian Rd in April 2013 through a GLS tender. Keppel Land: Singapore residential landbank

Site Location

Keppel Land's

effective interest

Estimated no of units

Attributable GFA (sq ft)

Highline Residences Kim Tian Rd 100.0% 500 473,218 Keppel Bay Plot 4 Harbour Front Avenue 11.7% 234 40,300 Keppel Bay Plot 6 Keppel Bay 30.0% 86 67,813 Keppel Towers & GE Tower

Tanjong Pagar Rd / Hoe Chiang Rd 100.0% 250 227,960 *

Total 1,070 809,291

Source: Company, Daiwa

Note: * Excludes estimated 249,746 sq ft of attributable GFA for commercial space

Preserving values in Keppel Bay precinct Given the amount of land that it has an interest in the Keppel Bay precinct, Keppel Land has had a strong incentive to do its part to preserve the value of land and homes in the area, which we feel it has done fairly well. The first of the Keppel Bay projects – the 969-unit Caribbean at Keppel Bay – was launched in 2000 at about SGD800/sq ft. Sales were slow, but rather than

dropping prices aggressively to move sales, the company furnished and leased out unsold units instead. Sales resumed when sentiment improved. According to URA REALIS data, the cumulative ASP achieved for primary developer sales was SGD847/sq ft. Caribbean at Keppel Bay: primary sales statistics

Source: URA (REALIS), Daiwa

Following this, the 1,129-unit Reflections at Keppel Bay was launched in April 2007. Its first release of 350 units was 90% sold at around SGD1,900/sq ft, although the massive size of the development and a relatively soft high-end market meant the project has yet to fully sell out after 7 years. Again, rather than cutting prices, Keppel Land has set aside 154 units as corporate residences. According to URA REALIS data, cumulative ASP achieved for new sales recorded up to 28 April 2014 was SGD1,994/sq ft. At the end of 2013, 65 units of the project remained for sale by Keppel Land. Reflections at Keppel Bay: primary sales statistics

Source: URA (REALIS), Daiwa

The 366-unit Corals at Keppel Bay, located along the historic King’s Dock, was launched in May 2013. According to URA REALIS data, the cumulative ASP achieved for new sales recorded up to 28 April this year was SGD2,201/sq ft, illustrating that the general trend of rising prices for the area remained intact. At the end of 2013, 197 units of the project remained for sale by Keppel Land.

0

200

400

600

800

1,000

0

50

100

150

200

250

Sep-

00

Oct

-00

Nov-

00

Dec-

00

Jan-

01

Jul-0

4

Aug-

04

Sep-

04

Oct

-04

Nov-

04

Dec-

04

Jan-

05

Feb-

05

Units Sold (LHS) Median PSF (RHS)

(SGD)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

50

100

150

200

250

Apr-0

7

Jul-0

7

Oct

-07

Jan-

08

May

-08

Oct

-08

Sep-

09

Dec-

09

Apr-1

0

Jul-1

0

Oct

-10

Feb-

11

May

-11

Aug-

11

Nov-

11

Mar

-12

Jun-

12

Sep-

12

Dec-

12

Units Sold Median PSF (RHS)

(SGD)

Financials / Singapore KPLD SP 14 May 2014

- 12 -

Corals at Keppel Bay: primary sales statistics

Source: URA (REALIS), Daiwa

A beneficiary of the Greater Southern Waterfront It was first announced in 2012 that Singapore’s container port activities would be consolidated at Tuas (in the west end of the island), for more efficient port operations and to free up prime land occupied by the city terminals for redevelopment. Preliminary conceptual plans for this endeavour were unveiled by the Urban Redevelopment Authority (URA) in its Draft Master Plan 2013, and envisioned a Greater Southern Waterfront, “to be a seamless extension of the city that will open up new live-work-play opportunities”. Map of City Terminals and Pasir Panjang Terminals

Source: URA

Relocation of the City Terminals (Tanjong Pagar, Keppel and Pulau Brani) is likely to take place first, with their port leases expiring in 2027, and Pasir Panjang thereafter. While details have yet to be fleshed out on the redevelopment plans, the transformation of the area and a potential extension of the city centre should be positive for land and home values in the area.

In our SOTP valuation, we have valued Keppel Land’s landbank in the area (Keppel Bay plots and KTGE) assuming ASPs of SGD1,800/sq ft, a construction cost of SGD450/sq ft, and a 15% margin on cost, implying a residual land value of SGD1,115/sq ft or SGD653m (based on Keppel Land’s effective stakes). For each +/- 10% change in assumed ASPs for the area, we estimate a sensitivity of +/- SGD0.05/share to our SOTP value. Overall, we believe the carrying cost for these sites is low and Keppel Land has great flexibility in releasing these projects for sale given that they do not fall under the ambit of the 2005 revision to the Residential Property Act, which requires developers with foreign ownership to complete projects within 5 years of the issuance of a Qualifying Certificate and sell all units within 2 years of obtaining the Temporary Occupation Permit (failing which a substantial extension charge is levied). In our opinion, they thus pose minimal operational risk, and represent valuable “call options” on the Singapore residential market. Less sanguine on GLS sites ... Keppel Land participates in GLS tenders fairly selectively, and has won just a few sites in recent years. The Lakefront Residences, beside Lakeside Mass Rapid Transit (MRT) station, and The Luxurie, beside Sengkang MRT station, were built on GLS sites won in 2010 and 2011 respectively. Both have been fully sold, with completion expected in 2015. The Glades – the difference 6 months made. Keppel Land’s only currently launched GLS project that remains substantially unsold is the 726-unit The Glades, near Tanah Merah MRT. The company won the site in August 2012, with a bid of SGD435m, or SGD791/sq ft per plot ratio (ppr). As part of a strategic alliance, a 30% stake in the project was taken up by China developer Vanke (Not rated). We estimate the project’s breakeven ASP to be about SGD1,200-1,250/sq ft. Launched in September 2013, 120 units had been sold as of the end of 2013. Recorded transactions in URA REALIS up to 28 April 2014 indicate an ASP of SGD1,462/sq ft. The impact of the total debt servicing ratio (TDSR) implemented at the end of June 2013 is seen clearly here, with 585-unit Urban Vista (diametrically opposite The Glades, with reference to the Tanah Merah train station) earlier selling 220 units over its 3-day launch weekend in March 2013 at an average of SGD1,500/sq ft.

0

500

1,000

1,500

2,000

2,500

3,000

0

20

40

60

80

100

120

May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Feb-14 Mar-14

Units Sold Median PSF (RHS)

(SGD)

Financials / Singapore KPLD SP 14 May 2014

- 13 -

“Rival project” Urban Vista: primary sales statistics

Source: URA (REALIS), Daiwa

Urban Vista is now essentially fully sold, with 6 units left as of end-1Q14 after discounting by the developer. URA REALIS data recorded up to 28 April indicate a new sale ASP for the project of SGD1,440/sq ft, an average pulled up by strong initial sales. With competition out of the way, we expect sales for The Glades to step up, albeit at slightly moderated prices. Highline Residences – rising competition. The company is also set to launch Highline Residences in Tiong Bahru, purchased in April 2013 through a GLS tender at a land cost of SGD1,163/sq ft ppr, during or after 2Q14. We think the site has excellent merits, but with a rash of projects being launched along the Queenstown to Tiong Bahru stretch, we believe buyers of the area are also quite spoilt for choice. Launches in District 3 (Alexandra Road, Tiong Bahru, Queenstown) expected in 2014

Project Location Developer

Date of tender award

Tender price

(SGDm) GFA

(sq ft)

Land cost

(SGD/sq ft ppr)

Est,. no of units

The Crest Prince Charles Crescent

Wing Tai JV

Sep-12 516.3 537,657 960 496

Commonwealth Towers

Queensway CDL JV Feb-13 562.8 637,495 883 845

Highline Residences

Tiong Bahru Keppel Land

Apr-13 550.3 473,213 1,163 500

Unnamed Prince Charles Crescent

UOL JV Apr-14 463.1 564,308 821 655

Total 2,212,674 2,496

Source: URA, HDB, Daiwa

The take-up rate and achieved ASPs at City Development’s Commonwealth Towers, adjacent to Queenstown MRT, could be an indicator of how Highline Residences will fare. According to press reports, 210 out of 400 units released on Commonwealth Towers’ launch day (1 May) were sold, although the achieved ASP for these 210 units was not disclosed. Given Highline Residences’ location closer to the Central Business District and popularity of the Tiong

Bahru area amongst yuppies and expatriates, we think a small premium could be achieved by Keppel Land’s project. We estimate a breakeven ASP of about SGD1,600-1,700/sq ft, and expect pricing to be in the range of SGD1,700-1,900/sq ft. ... but we see a fairly low likelihood of a write-down In late February this year, Wheelock Properties (Not rated) announced that it was writing down SGD110m for The Panorama condominium project, located at Ang Mo Kio Avenue 2 and a few minutes’ walk from upcoming Mayflower MRT station (which should be completed in 2021, 2-3 years after the development). Wheelock had purchased the site in January 2013 for SGD550m, or SGD790/sq ft ppr. According to an article published on 27 February this year by The Straits Times, just 58 sales at a median price of SGD1,343/sq ft had been recorded at the 658-unit project post its launch the prior month. We think that while Keppel Land’s sites were similarly bought pre-TDSR and launched afterwards, the take-up rate should be much better as long as pricing is reasonable, given that the sites are well located. We estimate overall project ASPs of SGD1,350/sq ft for The Glades and SGD1,750/sq ft for Highline Residences, at which Keppel Land should still be able to extract slim single-digit development margins. A +/-10% change in ASPs, ceteris paribus, would result in a +/- SGD0.02 and SGD0.03 change to our SOTP values per share, respectively.

Other overseas markets

Besides Singapore and China, Vietnam and Indonesia are core growth markets for Keppel Land. Amongst the major property developers in Singapore, Keppel Land is also distinctive in having undertaken an opportunistic investment approach in promising frontier markets like Myanmar and Sri Lanka. Compared with other property companies in Singapore, Keppel Land has a comparatively salient emerging Asia focus, as it sees these countries having more favourable demographics and economic growth profiles for sustainable longer-term growth. Vietnam – first-mover advantage; in for the very long haul Keppel Land started investing in Vietnam in the early 1990s, around the same time as it did China, entering Hanoi in 1991 to develop International Centre and Ho Chi Minh City in 1992 to develop Saigon Centre. The company also has an interest in the PetroVietnam

02004006008001,0001,2001,4001,6001,800

0

50

100

150

200

250

300

350

Mar

-13

Apr-1

3

May

-13

Jun-

13

Jul-1

3

Aug-

13

Sep-

13

Oct

-13

Nov-

13

Dec-

13

Jan-

14

Feb-

14

Mar

-14

Apr-1

4

Units Sold Median PSF (RHS)

(SGD)

Financials / Singapore KPLD SP 14 May 2014

- 14 -

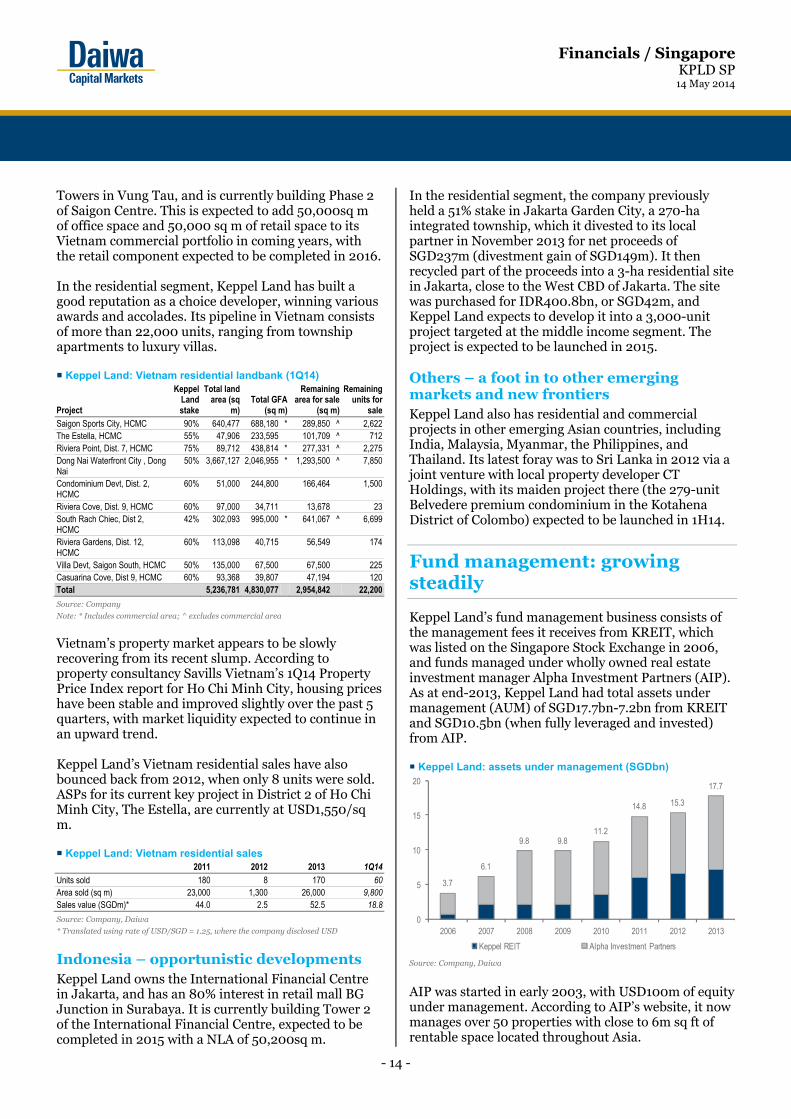

Towers in Vung Tau, and is currently building Phase 2 of Saigon Centre. This is expected to add 50,000sq m of office space and 50,000 sq m of retail space to its Vietnam commercial portfolio in coming years, with the retail component expected to be completed in 2016. In the residential segment, Keppel Land has built a good reputation as a choice developer, winning various awards and accolades. Its pipeline in Vietnam consists of more than 22,000 units, ranging from township apartments to luxury villas. Keppel Land: Vietnam residential landbank (1Q14)

Project

Keppel Land stake

Total land area (sq

m)Total GFA

(sq m)

Remaining area for sale

(sq m)

Remaining units for

saleSaigon Sports City, HCMC 90% 640,477 688,180 * 289,850 ^ 2,622The Estella, HCMC 55% 47,906 233,595 101,709 ^ 712Riviera Point, Dist. 7, HCMC 75% 89,712 438,814 * 277,331 ^ 2,275Dong Nai Waterfront City , Dong Nai

50% 3,667,127 2,046,955 * 1,293,500 ^ 7,850

Condominium Devt, Dist. 2, HCMC

60% 51,000 244,800 166,464 1,500

Riviera Cove, Dist. 9, HCMC 60% 97,000 34,711 13,678 23South Rach Chiec, Dist 2, HCMC

42% 302,093 995,000 * 641,067 ^ 6,699

Riviera Gardens, Dist. 12, HCMC

60% 113,098 40,715 56,549 174

Villa Devt, Saigon South, HCMC 50% 135,000 67,500 67,500 225Casuarina Cove, Dist 9, HCMC 60% 93,368 39,807 47,194 120Total 5,236,781 4,830,077 2,954,842 22,200

Source: Company

Note: * Includes commercial area; ^ excludes commercial area

Vietnam’s property market appears to be slowly recovering from its recent slump. According to property consultancy Savills Vietnam’s 1Q14 Property Price Index report for Ho Chi Minh City, housing prices have been stable and improved slightly over the past 5 quarters, with market liquidity expected to continue in an upward trend. Keppel Land’s Vietnam residential sales have also bounced back from 2012, when only 8 units were sold. ASPs for its current key project in District 2 of Ho Chi Minh City, The Estella, are currently at USD1,550/sq m. Keppel Land: Vietnam residential sales

2011 2012 2013 1Q14Units sold 180 8 170 60 Area sold (sq m) 23,000 1,300 26,000 9,800 Sales value (SGDm)* 44.0 2.5 52.5 18.8 Source: Company, Daiwa

* Translated using rate of USD/SGD = 1.25, where the company disclosed USD

Indonesia – opportunistic developments Keppel Land owns the International Financial Centre in Jakarta, and has an 80% interest in retail mall BG Junction in Surabaya. It is currently building Tower 2 of the International Financial Centre, expected to be completed in 2015 with a NLA of 50,200sq m.

In the residential segment, the company previously held a 51% stake in Jakarta Garden City, a 270-ha integrated township, which it divested to its local partner in November 2013 for net proceeds of SGD237m (divestment gain of SGD149m). It then recycled part of the proceeds into a 3-ha residential site in Jakarta, close to the West CBD of Jakarta. The site was purchased for IDR400.8bn, or SGD42m, and Keppel Land expects to develop it into a 3,000-unit project targeted at the middle income segment. The project is expected to be launched in 2015. Others – a foot in to other emerging markets and new frontiers Keppel Land also has residential and commercial projects in other emerging Asian countries, including India, Malaysia, Myanmar, the Philippines, and Thailand. Its latest foray was to Sri Lanka in 2012 via a joint venture with local property developer CT Holdings, with its maiden project there (the 279-unit Belvedere premium condominium in the Kotahena District of Colombo) expected to be launched in 1H14.

Fund management: growing steadily

Keppel Land’s fund management business consists of the management fees it receives from KREIT, which was listed on the Singapore Stock Exchange in 2006, and funds managed under wholly owned real estate investment manager Alpha Investment Partners (AIP). As at end-2013, Keppel Land had total assets under management (AUM) of SGD17.7bn-7.2bn from KREIT and SGD10.5bn (when fully leveraged and invested) from AIP. Keppel Land: assets under management (SGDbn)

Source: Company, Daiwa

AIP was started in early 2003, with USD100m of equity under management. According to AIP’s website, it now manages over 50 properties with close to 6m sq ft of rentable space located throughout Asia.

3.7

6.1

9.8 9.811.2

14.8 15.3

17.7

0

5

10

15

20

2006 2007 2008 2009 2010 2011 2012 2013

Keppel REIT Alpha Investment Partners

Financials / Singapore KPLD SP 14 May 2014

- 15 -

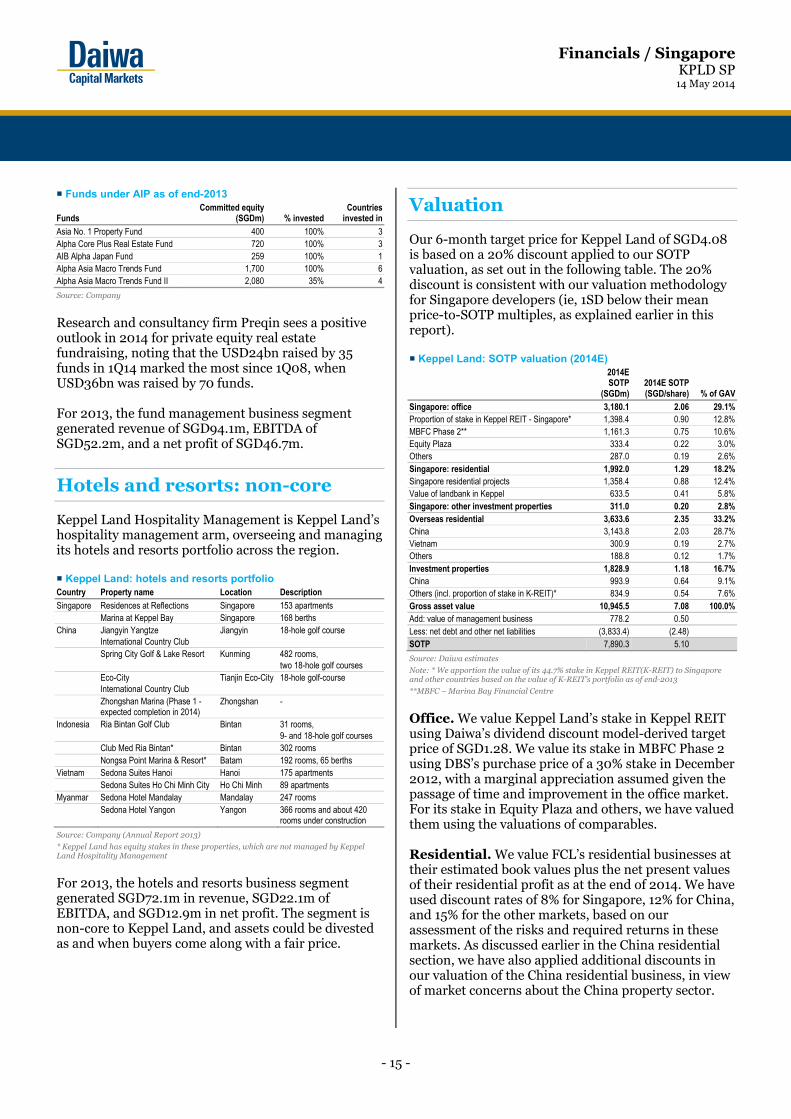

Funds under AIP as of end-2013

Funds Committed equity

(SGDm) % invested Countries

invested inAsia No. 1 Property Fund 400 100% 3Alpha Core Plus Real Estate Fund 720 100% 3AIB Alpha Japan Fund 259 100% 1Alpha Asia Macro Trends Fund 1,700 100% 6Alpha Asia Macro Trends Fund II 2,080 35% 4

Source: Company

Research and consultancy firm Preqin sees a positive outlook in 2014 for private equity real estate fundraising, noting that the USD24bn raised by 35 funds in 1Q14 marked the most since 1Q08, when USD36bn was raised by 70 funds. For 2013, the fund management business segment generated revenue of SGD94.1m, EBITDA of SGD52.2m, and a net profit of SGD46.7m.

Hotels and resorts: non-core

Keppel Land Hospitality Management is Keppel Land’s hospitality management arm, overseeing and managing its hotels and resorts portfolio across the region. Keppel Land: hotels and resorts portfolio Country Property name Location Description

Singapore Residences at Reflections Singapore 153 apartments Marina at Keppel Bay Singapore 168 berths China Jiangyin Yangtze

International Country Club Jiangyin 18-hole golf course

Spring City Golf & Lake Resort Kunming 482 rooms, two 18-hole golf courses

Eco-City International Country Club

Tianjin Eco-City 18-hole golf-course

Zhongshan Marina (Phase 1 - expected completion in 2014)

Zhongshan -

Indonesia Ria Bintan Golf Club Bintan 31 rooms, 9- and 18-hole golf courses

Club Med Ria Bintan* Bintan 302 rooms Nongsa Point Marina & Resort* Batam 192 rooms, 65 berths Vietnam Sedona Suites Hanoi Hanoi 175 apartments Sedona Suites Ho Chi Minh City Ho Chi Minh 89 apartments Myanmar Sedona Hotel Mandalay Mandalay 247 rooms Sedona Hotel Yangon Yangon 366 rooms and about 420

rooms under construction

Source: Company (Annual Report 2013)

* Keppel Land has equity stakes in these properties, which are not managed by Keppel Land Hospitality Management

For 2013, the hotels and resorts business segment generated SGD72.1m in revenue, SGD22.1m of EBITDA, and SGD12.9m in net profit. The segment is non-core to Keppel Land, and assets could be divested as and when buyers come along with a fair price.

Valuation

Our 6-month target price for Keppel Land of SGD4.08 is based on a 20% discount applied to our SOTP valuation, as set out in the following table. The 20% discount is consistent with our valuation methodology for Singapore developers (ie, 1SD below their mean price-to-SOTP multiples, as explained earlier in this report). Keppel Land: SOTP valuation (2014E)

2014E SOTP

(SGDm) 2014E SOTP (SGD/share) % of GAV

Singapore: office 3,180.1 2.06 29.1%Proportion of stake in Keppel REIT - Singapore* 1,398.4 0.90 12.8%MBFC Phase 2** 1,161.3 0.75 10.6%Equity Plaza 333.4 0.22 3.0%Others 287.0 0.19 2.6%Singapore: residential 1,992.0 1.29 18.2%Singapore residential projects 1,358.4 0.88 12.4%Value of landbank in Keppel 633.5 0.41 5.8%Singapore: other investment properties 311.0 0.20 2.8%Overseas residential 3,633.6 2.35 33.2%China 3,143.8 2.03 28.7%Vietnam 300.9 0.19 2.7%Others 188.8 0.12 1.7%Investment properties 1,828.9 1.18 16.7%China 993.9 0.64 9.1%Others (incl. proportion of stake in K-REIT)* 834.9 0.54 7.6%Gross asset value 10,945.5 7.08 100.0%Add: value of management business 778.2 0.50 Less: net debt and other net liabilities (3,833.4) (2.48)SOTP 7,890.3 5.10

Source: Daiwa estimates

Note: * We apportion the value of its 44.7% stake in Keppel REIT(K-REIT) to Singapore and other countries based on the value of K-REIT’s portfolio as of end-2013

**MBFC – Marina Bay Financial Centre

Office. We value Keppel Land’s stake in Keppel REIT using Daiwa’s dividend discount model-derived target price of SGD1.28. We value its stake in MBFC Phase 2 using DBS’s purchase price of a 30% stake in December 2012, with a marginal appreciation assumed given the passage of time and improvement in the office market. For its stake in Equity Plaza and others, we have valued them using the valuations of comparables. Residential. We value FCL’s residential businesses at their estimated book values plus the net present values of their residential profit as at the end of 2014. We have used discount rates of 8% for Singapore, 12% for China, and 15% for the other markets, based on our assessment of the risks and required returns in these markets. As discussed earlier in the China residential section, we have also applied additional discounts in our valuation of the China residential business, in view of market concerns about the China property sector.

Financials / Singapore KPLD SP 14 May 2014

- 16 -

Other investment properties. We value the company’s other investment properties using a mix of the comparison method, income approach, and book value. Keppel Land: Daiwa’s 2014E GAV breakdown (excl. value of fund management business)

Source: Company

Fund management business. We value Keppel Land’s fund management business at a multiple of 13x our 2014E EBIT of SGD59.9m for the segment. This multiple, consistent with the multiple we apply to value the fund management businesses of other Singapore-listed developers in our coverage, is based on the average 1-year forward EV/EBIT multiple for ARA Asset Management (ARA) (Not rated) since it was listed in 2007 (14.5x up to the end of April 2014). ARA is an Asia real-estate fund-management company focused on the management of publicly listed REITs in Singapore, Hong Kong and Malaysia, and private real-estate funds that invest in Singapore, Hong Kong, Malaysia and China. We subtract our forecasts for net debt and other net liabilities of SGD3.8bn (see our SOTP table above) as at the end-2014 to derive our SOTP value of SGD5.10/share for Keppel Land.

Catalysts

Stronger-than-expected office recovery News flow from the office sector has been fairly positive, with new spaces such as CapitaGreen (a soon-to-be completed grade-A office tower at Market Street in the CBD) seeing satisfactory take-up and rates. If more office-space demand from large occupiers new to Singapore comes in, we believe this would be a positive catalyst, strengthening the rate of rental growth in this recovery. A much stronger-than-expected recovery could also boost the case for cap rate compression in the sector, further enhancing the value of Keppel Land’s office assets.

Divestments of office assets Keppel Land’s key office assets are MBFC Phase 2 (Tower 3) and Equity Plaza, respectively 10.6% and 3.0% of its GAV. Completed in March 2012, MBFC Tower 3 had a committed occupancy of 96% as of end 1Q14, and we believe is quite ready for sale, although the office market only recently troughed. Going by its previous divestments to KREIT, we believe a monetisation of its stake in MBFC Phase 2 through KREIT, once it happens, would be positive for Keppel Land. With the unlocking of capital, we believe Keppel Land could pay at least an additional SGD0.10/share in special dividends in the year of divestment, which would bring that year’s yield up to 5.5%, or an even larger special dividend, which could give its ROE profile a healthy boost. It was also recently announced that a sale of Equity Plaza may be in the works. According to a Business Times report, the price may be around SGD550m to SGD560m, or SGD2,177-2,217/sq ft. This is about 10% above our current valuation for the building. Stronger-than-expected China residential sector news flow or sales Given Keppel Land’s significant exposure to the Chinese residential market, positive sector news flow should provide a boost to Keppel Land. Reporting good sales figures, especially at key projects, will also be positive for the company. Resilient Singapore residential sales The Singapore residential property market has continued to soften, with various price indices registering declines across the board. With a number of launches, such as City Development’s Commonwealth Towers (launched on 1 May) and Keppel Land’s Highline Residences (upcoming), a good take-up could be read positively for the strength of demand and the underlying market.

Risks

Poor China residential sector news flow or sales We consider this as the main risk to our positive investment view on Keppel Land. Poor sector news flow could continue to be a drag on China residential developers and developers with significant exposure to the sector, such as Keppel Land. We note, however, that this could provide opportunities for stronger developers like Keppel Land, who might be able to pick up some distressed assets when the wheat is being sorted from the chaff.

Singapore: Office29.1%

Singapore: Residential18.2%

Singapore: Otherinvestment properties

2.8%

China: Residential28.7%

China:Investment properties

9.1%

Other overseasresidential

4.5%

Other overseasinvestment properties

7.6%

Financials / Singapore KPLD SP 14 May 2014

- 17 -

Specific to Keppel Land, it would be negative if sales did not rebound from 1Q14’s seasonal weakness. While we have what we consider as fairly conservative numbers, weakness in overall sales and at key projects such as 8 Park Avenue may pose downside risks to the consensus forecasts. Disappointing office recovery An upturn in the Singapore office sector is by now a consensus call. It currently appears to be progressing as per market expectations; but any pause or slowdown may cause concerns about the sustainability of the recovery.

Financials / Singapore KPLD SP 14 May 2014

- 18 -

Appendix

Company background

Keppel Land is the property arm of the Keppel Group. As at end-April 2014, it was 54.6% owned by Keppel Corporation. By virtue of its deemed interest through its shareholding in the latter, Singapore’s Temasek Holdings is the company’s only other substantial shareholder. Business segments In terms of business segments, Keppel Land’s major activities are property development, property investment, property-fund management, and hotels and resorts. It has a target profit mix of 70% from property trading and 30% from rest of business. Keppel Land: total asset breakdown by business segment (end-1Q14)

Source: Company

Geographical focus In terms of geography, Keppel Land’s core countries of focus are Singapore, China, Indonesia and Vietnam. Its stated target capital allocation is 35% to 40% each in Singapore and China (where its focus cities are Shanghai, Beijing, Chengdu, Wuxi, and Tianjin), with the remainder going mainly to Indonesia and Vietnam.

Keppel Land: total asset breakdown by geography (end-1Q14)

Source: Company, Daiwa

Property tradingSGD8,673.0m

63.0%

Property investment

SGD4,226.4m30.7%

Fund managementSGD68.8m

0.5%

OthersSGD633.3m

4.6%

Hotels and resorts

SGD165.2m1.2%

SingaporeSGD6,374.0m

46.3%

ChinaSGD5,919.7m

43.0%

VietnamSGD757.2m

5.5%

OthersSGD399.2m

2.9%

IndonesiaSGD316.6m

2.3%

Financials / Singapore KPLD SP 14 May 2014

- 19 -

Daiwa’s Asia Pacific Research Directory

HONG KONG

Hiroaki KATO (852) 2532 4121 [email protected] Regional Research Head

John HETHERINGTON (852) 2773 8787 [email protected] Regional Deputy Head of Asia Pacific Research

Rohan DALZIELL (852) 2848 4938 [email protected] Regional Head of Product Management

Kevin LAI (852) 2848 4926 [email protected] Deputy Head of Regional Economics; Macro Economics (Regional)

Christie CHIEN (852) 2848 4482 [email protected] Macro Economics (Taiwan)

Jonas KAN (852) 2848 4439 [email protected] Head of Hong Kong Research; Head of Hong Kong and China Property

Grace WU (852) 2532 4383 [email protected] Head of Greater China FIG; Banking (Hong Kong, China)

Jerry YANG (852) 2773 8842 [email protected] Banking (Taiwan); Insurance (Taiwan and China)

Leon QI (852) 2532 4381 [email protected] Banking (Hong Kong, China); Broker (China)

Winston CAO (852) 2848 4469 [email protected] Capital Goods – Machinery (China)

Alison LAW (852) 2532 4308 [email protected] Head of Regional Consumer; Consumer (Hong Kong/China); Gaming and Leisure (Hong Kong, China)

Jamie SOO (852) 2773 8529 [email protected]

Consumer (Hong Kong/China)

Anson CHAN (852) 2532 4350 [email protected]

Consumer (Hong Kong/China)

Eric CHEN (852) 2773 8702 [email protected] Pan-Asia/Regional Head of IT/Electronics; Semiconductor/IC Design (Regional)

Lynn CHENG (852) 2773 8822 [email protected]

IT/Electronics (Semiconductor)

Felix LAM (852) 2532 4341 [email protected] Head of Materials (Hong Kong, China); Cement and Building Materials (China, Taiwan); Property (China)

Dennis IP (852) 2848 4068 [email protected] Power; Utilities; Renewables and Environment (Hong Kong/China)

John CHOI (852) 2773 8730 [email protected] Regional Head of Small/Mid Cap; Small/Mid Cap (Regional); Internet (China)

Jackson YU (852) 2848 4976 [email protected]

Small/Mid Cap (Regional)

Joey CHEN (852) 2848 4483 [email protected] Steel (China)

Kelvin LAU (852) 2848 4467 [email protected] Head of Transportation (Hong Kong, China); Transportation (Regional)

Jibo MA (852) 2848 4489 [email protected] Head of Custom Products Group; Custom Products Group

Thomas HO (852) 2773 8716 [email protected] Custom Products Group

SOUTH KOREA

Chang H LEE (82) 2 787 9177 [email protected] Head of Korea Research; Strategy; Banking

Sung Yop CHUNG (82) 2 787 9157 [email protected] Pan-Asia Co-head/Regional Head of Automobiles and Components; Automobiles; Shipbuilding; Steel

Jun Yong BANG (82) 2 787 9168 [email protected] Tyres; Chemicals

Mike OH (82) 2 787 9179 [email protected] Capital Goods (Construction and Machinery)

Sang Hee PARK (82) 2 787 9165 [email protected] Consumer/Retail

Thomas Y KWON (82) 2 787 9181 [email protected] Pan-Asia Head of Internet & Telecommunications; Software (Korea) – Internet/On-line Game

TAIWAN

Mark CHANG (886) 2 8758 6245 [email protected] Head of Taiwan Research

Steven TSENG (886) 2 8758 6252 [email protected]

IT/Technology Hardware (PC Hardware)

Christine WANG (886) 2 8758 6249 [email protected] IT/Technology Hardware (Automation); Cement; Consumer

Kylie HUANG (886) 2 8758 6248 [email protected] IT/Technology Hardware (Handsets and Components)

INDIA

Punit SRIVASTAVA (91) 22 6622 1013 [email protected] Head of India Research; Strategy; Banking/Finance

Saurabh MEHTA (91) 22 6622 1009 [email protected] Capital Goods; Utilities

SINGAPORE

Adrian LOH (65) 6499 6548 [email protected] Head of Singapore Research, Regional Head of Oil and Gas; Oil and Gas (ASEAN and China); Capital Goods (Singapore)

Benjamin LIM (65) 6321 3086 [email protected]

Oil and Gas (ASEAN and China); Capital Goods (Singapore)

Angeline LOH (65) 6499 6570 [email protected] Banking/Finance, Consumer/Retail

David LUM (65) 6329 2102 [email protected] Property and REITs

Evon TAN (65) 6499 6546 [email protected] Property and REITs

Ramakrishna MARUVADA (65) 6499 6543 [email protected] Head of ASEAN & India Telecommunications; Telecommunications (China, ASEAN & India)

Jame OSMAN (65) 6321 3092 [email protected] Telecom (ASEAN & India); Pharmaceuticals and Healthcare (Singapore)

Financials / Singapore KPLD SP 14 May 2014

- 20 -

Daiwa’s Offices

Office / Branch / Affiliate Address Tel Fax

DAIWA SECURITIES GROUP INC

HEAD OFFICE Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6753 (81) 3 5555 3111 (81) 3 5555 0661

Daiwa Securities Trust Company One Evertrust Plaza, Jersey City, NJ 07302, U.S.A. (1) 201 333 7300 (1) 201 333 7726

Daiwa Securities Trust and Banking (Europe) PLC (Head Office) 5 King William Street, London EC4N 7JB, United Kingdom (44) 207 320 8000 (44) 207 410 0129

Daiwa Europe Trustees (Ireland) Ltd Level 3, Block 5, Harcourt Centre, Harcourt Road, Dublin 2, Ireland (353) 1 603 9900 (353) 1 478 3469

Daiwa Capital Markets America Inc Financial Square, 32 Old Slip, New York, NY10005, U.S.A. (1) 212 612 7000 (1) 212 612 7100

Daiwa Capital Markets America Inc. San Francisco Branch 555 California Street, Suite 3360, San Francisco, CA 94104, U.S.A. (1) 415 955 8100 (1) 415 956 1935

Daiwa Capital Markets Europe Limited 5 King William Street, London EC4N 7AX, United Kingdom (44) 20 7597 8000 (44) 20 7597 8600

Daiwa Capital Markets Europe Limited, Frankfurt Branch Trianon Building, Mainzer Landstrasse 16, 60325 Frankfurt am Main, Federal Republic of Germany

(49) 69 717 080 (49) 69 723 340

Daiwa Capital Markets Europe Limited, Paris Representative Office 36, rue de Naples, 75008 Paris, France (33) 1 56 262 200 (33) 1 47 550 808

Daiwa Capital Markets Europe Limited, London, Geneva Branch 50 rue du Rhône, P.O.Box 3198, 1211 Geneva 3, Switzerland (41) 22 818 7400 (41) 22 818 7441

Daiwa Capital Markets Europe Limited, Moscow Representative Office

Midland Plaza 7th Floor, 10 Arbat Street, Moscow 119002, Russian Federation

(7) 495 641 3416 (7) 495 775 6238

Daiwa Capital Markets Europe Limited, Bahrain Branch 7th Floor, The Tower, Bahrain Commercial Complex, P.O. Box 30069, Manama, Bahrain

(973) 17 534 452 (973) 17 535 113

Daiwa Capital Markets Hong Kong Limited Level 28, One Pacific Place, 88 Queensway, Hong Kong (852) 2525 0121 (852) 2845 1621

Daiwa Capital Markets Singapore Limited 6 Shenton Way #26-08, DBS Building Tower Two, Singapore 068809, Republic of Singapore

(65) 6220 3666 (65) 6223 6198

Daiwa Capital Markets Australia Limited Level 34, Rialto North Tower, 525 Collins Street, Melbourne, Victoria 3000, Australia

(61) 3 9916 1300 (61) 3 9916 1330

DBP-Daiwa Capital Markets Philippines, Inc 18th Floor, Citibank Tower, 8741 Paseo de Roxas, Salcedo Village, Makati City, Republic of the Philippines

(632) 813 7344 (632) 848 0105

Daiwa-Cathay Capital Markets Co Ltd 14/F, 200, Keelung Road, Sec 1, Taipei, Taiwan, R.O.C. (886) 2 2723 9698 (886) 2 2345 3638

Daiwa Securities Capital Markets Korea Co., Ltd. One IFC, 10 Gukjegeumyung-Ro, Yeouido-dong, Yeongdeungpo-gu, Seoul, 150-876, Korea

(82) 2 787 9100 (82) 2 787 9191

Daiwa Securities Capital Markets Co Ltd, Beijing Representative Office

Room 301/302,Kerry Center, 1 Guanghua Road,Chaoyang District, Beijing 100020, People’s Republic of China

(86) 10 6500 6688 (86) 10 6500 3594

Daiwa SSC Securities Co Ltd 45/F, Hang Seng Tower, 1000 Lujiazui Ring Road, Pudong, Shanghai 200120, People’s Republic of China

(86) 21 3858 2000 (86) 21 3858 2111

Daiwa Securities Capital Markets Co. Ltd, Bangkok Representative Office

18th Floor, M Thai Tower, All Seasons Place, 87 Wireless Road, Lumpini, Pathumwan, Bangkok 10330, Thailand

(66) 2 252 5650 (66) 2 252 5665

Daiwa Capital Markets India Private Ltd 10th Floor, 3 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra East, Mumbai – 400051, India

(91) 22 6622 1000 (91) 22 6622 1019

Daiwa Securities Capital Markets Co. Ltd, Hanoi Representative Office

Suite 405, Pacific Palace Building, 83B, Ly Thuong Kiet Street, Hoan Kiem Dist. Hanoi, Vietnam

(84) 4 3946 0460 (84) 4 3946 0461

DAIWA INSTITUTE OF RESEARCH LTD

HEAD OFFICE 15-6, Fuyuki, Koto-ku, Tokyo, 135-8460, Japan (81) 3 5620 5100 (81) 3 5620 5603

MARUNOUCHI OFFICE Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6756 (81) 3 5555 7011 (81) 3 5202 2021

New York Research Center 11th Floor, Financial Square, 32 Old Slip, NY, NY 10005-3504, U.S.A. (1) 212 612 6100 (1) 212 612 8417

London Research Centre 3/F, 5 King William Street, London, EC4N 7AX, United Kingdom (44) 207 597 8000 (44) 207 597 8550

Financials / Singapore KPLD SP 14 May 2014

- 21 -

Disclaimer

This publication is produced by Daiwa Securities Group Inc. and/or its non-U.S. affiliates, and distributed by Daiwa Securities Group Inc. and/or its non-U.S. affiliates, except to the extent expressly provided herein. This publication and the contents hereof are intended for information purposes only, and may be subject to change without further notice. Any use, disclosure, distribution, dissemination, copying, printing or reliance on this publication for any other purpose without our prior consent or approval is strictly prohibited. Neither Daiwa Securities Group Inc. nor any of its respective parent, holding, subsidiaries or affiliates, nor any of its respective directors, officers, servants and employees, represent nor warrant the accuracy or completeness of the information contained herein or as to the existence of other facts which might be significant, and will not accept any responsibility or liability whatsoever for any use of or reliance upon this publication or any of the contents hereof. Neither this publication, nor any content hereof, constitute, or are to be construed as, an offer or solicitation of an offer to buy or sell any of the securities or investments mentioned herein in any country or jurisdiction nor, unless expressly provided, any recommendation or investment opinion or advice. Any view, recommendation, opinion or advice expressed in this publication may not necessarily reflect those of Daiwa Securities Capital Markets Co. Ltd., and/or its affiliates nor any of its respective directors, officers, servants and employees except where the publication states otherwise. This research report is not to be relied upon by any person in making any investment decision or otherwise advising with respect to, or dealing in, the securities mentioned, as it does not take into account the specific investment objectives, financial situation and particular needs of any person. Daiwa Securities Group Inc., its subsidiaries or affiliates, or its or their respective directors, officers and employees from time to time have trades as principals, or have positions in, or have other interests in the securities of the company under research including derivatives in respect of such securities or may have also performed investment banking and other services for the issuer of such securities. The following are additional disclosures. Japan Daiwa Securities Co. Ltd. and Daiwa Securities Group Inc. Daiwa Securities Co. Ltd. is a subsidiary of Daiwa Securities Group Inc. Investment Banking Relationship

Within the preceding 12 months, The subsidiaries and/or affiliates of Daiwa Securities Group Inc. * has lead-managed public offerings and/or secondary offerings (excluding straight bonds) of the securities of the following companies: Blackgold International Holdings Ltd (BGG AU); Tosei Corporation (8923 JP); Modern Land (China) Co. Ltd (1107 HK); China Everbright Bank Company Limited (6818 HK); econtext Asia Ltd (1390 HK); Lotte Shopping Co (023530 KS).